Yesterday’s High Breakout - Trend Following StrategyYesterday’s High Breakout it is a trading system based on the analysis of yesterday's highs, it works in trend-following mode therefore it opens a long position at the breakout of yesterday's highs even if they occur several times in one day.

There are several methods for exiting a trade, each with its own unique strategy. The first method involves setting Take-Profit and Stop-Loss percentages, while the second utilizes a trailing-stop with a specified offset value. The third method calls for a conditional exit when the candle closes below a reference EMA.

Additionally, operational filters can be applied based on the volatility of the currency pair, such as calculating the percentage change from the opening or incorporating a gap to the previous day's high levels. These filters help to anticipate or delay entry into the market, mitigating the risk of false breakouts.

In the specific case of NULS, a 9% Take-Profit and a 3% Stop-Loss were set, with an activated trailing-stop percentage. To postpone entry and avoid false breakouts, a 1% gap was added to the price of yesterday's highs.

Name : Yesterday's High Breakout - Trend Follower Strategy

Author : @tumiza999

Category : Trend Follower, Breakout of Yesterday's High.

Operating mode : Spot or Futures (only long).

Trade duration : Intraday.

Timeframe : 30M, 1H, 2H, 4H

Market : Crypto

Suggested usage : Short-term trading, when the market is in trend and it is showing high volatility.

Entry : When there is a breakout of Yesterday's High.

Exit : Profit target or Trailing stop, Stop loss or Crossunder EMA.

Configuration :

- Gap to anticipate or postpone the entry before or after the identified level

- Rate of Change for Entry Condition

- Take Profit, Stop Loss and Trailing Stop

- EMA length

Backtesting :

⁃ Exchange: BINANCE

⁃ Pair: NULSUSDT

⁃ Timeframe: 2H

⁃ Fee: 0.075%

⁃ Slippage: 1

- Initial Capital: 10000 USDT

- Position sizing: 10% of Equity

- Start : 2018-07-26 (Out Of Sample from 2022-12-23)

- Bar magnifier: on

Credits : LucF for Pine Coders (f_security function to avoid repainting using security)

Disclaimer : Risk Management is crucial, so adjust stop loss to your comfort level. A tight stop loss can help minimise potential losses. Use at your own risk.

How you or we can improve? Source code is open so share your ideas!

Leave a comment and smash the boost button!

Thanks for your attention, happy to support the TradingView community.

Algotrading

Risk Reward Calculator [lovealgotrading]

OVERVIEW:

This Risk Reward Calculator strategy can help you maximize your RR value with help of algorithmic trading.

INDICATOR:

I wanted to setup my trades more easier with this indicator, I didn't want to calculate everytime before orders, with help this indicator we can calculate R:R value, avarage price, stoploss price, take-profit price, order prices, all position cost and more ...

Our strategy is a risk revard calculation indicator that is made easy to use by using visualized lines and panels, and also has algorithmic trading support.

With the help of this indicator, we can quickly and easily calculate our risk reward values and enter the positions.

If we want to ensure that our balance grows regularly while trading in the stock market, we need to manage the risks and rewards otherwise we may fall below our initial balance at the end of the day, even if we seem to be winning.

What is the Risk-Reward value ?

This value is a value that shows how many times the amount of risk we take when entering the position is successful, we will earn.

- For example, you risked $100 while entering the trade, so if your trade stops, you will lose 100 $.

Your Risk-Reward(RR) value is 2 means that if your position is successful, you will have 200 $ in your pocket.

A trader's success is determined by the amount of R he earns monthly or yearly, not how much money he makes.

What is different in this indicator ?

I want to say thank you to © EvoCrypto. His Calculator (weighted) – evo indicator helped me when I was developed my indicator.

I want to explain what I have improved:

1-In this strategy, we can determine the time period in which we want to open our positions.

2-We can open a maximum of 4 positions in the same direction and close our positions at a single level. StopLoss or TakeProfit

3-This indicator, which works in the form of a strategy, shows where our positions have been opened or closed. With the help of this, it helps us to determine our strategy in our future positions more accurately.

4-The most important improvement is that we do not miss our positions with the help of alarms (WEB HOOK). if we want, we receive by quickly connecting all these positions to our robot, the software can enter and exit the position while we are busy.

IMPLEMENTATION DETAILS – SETTINGS:

1 - We can set the start and end dates of the positions we will take.

2- We can set our take profit, stoploss levels.

3- If your trade is stopped, we can determine the amount of the trade that we will lose.

4- We can adjust our entry levels to positions and our position sizes at entry levels.

(Sum of positions weight must be 100%)

5- We can receive our positions even if we are busy with the help of algorithmic trading. For this, we must paste our Jshon codes into the fields specified in the settings panel.

6- Finally, we can change the settings we want and don't want to have in our visual elements.

Let's make a LONG side example together

We have determined our positions to enter stoploss, take profit and long positions. We did not forget to set the start time of our strategy

Our strategy appear on the graph as follows.

Our strategy has calculated the total position size, our R-R value, the distance of the current price to the stop and take profit levels, in short, a lot of things we could look visually.

Notes:

If you're going to connect this bot to an automatic Long or Short direction,

Don’t forget! you need to Webhook URL,

Don’t miss paste this code to your message window {{strategy.order.alert_message}}

ALSO:

If you have any ideas what to add to my work to add more sources or make calculations cooler, feel free to write me.

AUTOMATIC GRID BOT STRATEGY [ilovealgotrading]

OVERVIEW:

This Grid trading strategy can help you maximize your profit in a ranging sideways market with no clear direction.

INDICATOR:

We can get some money by taking advantage of the movement of the price between the range we have determined.

Short positions are opened while the price is rising, long positions are opened while the price is falling.

Therefore, there is no need to predict the trend direction.

What is different in this indicator:

I want to say thank you to © thequantscience. His GRID SPOT TRADING ALGORITHM - GRID BOT TRADING strategy helped me when I was writing my indicator.

I want to explain what I have improved:

1- Grid strategy is a type of strategy that can be traded in very short time frames and users can trade this strategy algorithmically by connecting this strategy to their own accounts with the help of API systems. For this reason, I have developed a software that can give us signals by dynamically changing the long and short messages when users are trading.

2- We can change the start and end dates of our grid bot as we want. It is necessary to use this setting when setting up automatic bots, so that previously opened transactions are not taken into account.

3 - Lot or quantity size should not be excessively small when users are taking automatic trades because exchanges have limitations, to avoid this problem, I have prevented this error by automatically rounding up to the nearest quantity size inside the software.

4 - Users can avoid excessive losses by using stop loss on this grid bot if they wish.

5 - When our price is over the range high or below the range low, our open positions are closed, if the stop button is active. We can also change which close price time frame we take as a basis from the settings.

6 -Users can set how many dollars they can enter per transaction while performing their transactions automatically.

IMPLEMENTATION DETAILS – SETTINGS:

This script allows the user to choose the highs and lows leves of our range. Our bot trades in the specified range.

1. This strategy allows us to set start and end backtest dates.

2. We can change range high and range low leves of our bot

3. IF people want to trade algorithmically with the help of this bot, there are 6 different input systems that will receive the Json codes as an alarm

4. IF the price closes above the upper line or below the lower line, all transactions will be closed. We can determine in which time frame our transactions will be stopped if the price closes outside these levels.We can adjust how our bot works by activating or turning off the Stop Loss button.

5. In this strategy, you can determine your dollar cost for per position.

6. The user can also divide the interval we have determined into 10 parts or 20 equal parts.

7. The grid is divided and colored at the interval we set. At the same time, if we don't want we can turn off colored channels.

Notes:

If you're going to connect this bot to an automatic Long and Short direction,

Don’t forget! you need to Webhook URL,

Don’t miss paste this code to your message window {{strategy.order.alert_message}}

ALSO:

Set your range below the support zones and above the resistance zones.

Don't be afraid to take a wide range, it doesn't matter if you make a little money, the important thing is that you don't lose money.

If you have any ideas what to add to my work to add more sources or make calculations cooler, suggest in DM .

BE - Golden Cross Crude KeyTraders, i have been observing crude oil for about 3 months now and somehow I can see that crude is respecting 42 days Moving average and crosses have created massive spikes most of the time.

However you need to be mindful of the time to trade and timeframe since not all crosses creates spikes.

Note: I have been testing on a 15min timeframe.

Keeping this in mind, this indicator is a automated solution which takes trade entries on crosses plus buffer and exits based on the specified Sl type.

Enjoy!

DISCLAIMER: No sharing, copying, reselling, modifying, or any other forms of use are authorized for our documents, script / strategy, and the information published with them. This informational planning script / strategy is strictly for individual use and educational purposes only. This is not financial or investment advice. Investments are always made at your own risk and are based on your personal judgement. I am not responsible for any losses you may incur. Please invest wisely.

Happy to receive suggestions and feedback in order to improve the performance of the indicator better.

Investments/swing trading strategy for different assetsStop worrying about catching the lowest price, it's almost impossible!: with this trend-following strategy and protection from bearish phases, you will know how to enter the market properly to obtain benefits in the long term.

Backtesting context: 1899-11-01 to 2023-02-16 of SPX by Tvc. Commissions: 0.05% for each entry, 0.05% for each exit. Risk per trade: 2.5% of the total account

For this strategy, 5 indicators are used:

One Ema of 200 periods

Atr Stop loss indicator from Gatherio

Squeeze momentum indicator from LazyBear

Moving average convergence/divergence or Macd

Relative strength index or Rsi

Trade conditions:

There are three type of entries, one of them depends if we want to trade against a bearish trend or not.

---If we keep Against trend option deactivated, the rules for two type of entries are:---

First type of entry:

With the next rules, we will be able to entry in a pull back situation:

Squeeze momentum is under 0 line (red)

Close is above 200 Ema and close is higher than the past close

Histogram from macd is under 0 line and is higher than the past one

Once these rules are met, we enter into a buy position. Stop loss will be determined by atr stop loss (white point) and break even(blue point) by a risk/reward ratio of 1:1.

For closing this position: Squeeze momentum crosses over 0 and, until squeeze momentum crosses under 0, we close the position. Otherwise, we would have closed the position due to break even or stop loss.

Second type of entry:

With the next rules, we will not lose a possible bullish movement:

Close is above 200 Ema

Squeeze momentum crosses under 0 line

Once these rules are met, we enter into a buy position. Stop loss will be determined by atr stop loss (white point) and break even(blue point) by a risk/reward ratio of 1:1.

Like in the past type of entry, for closing this position: Squeeze momentum crosses over 0 and, until squeeze momentum crosses under 0, we close the position. Otherwise, we would have closed the position due to break even or stop loss.

---If we keep Against trend option activated, the rules are the same as the ones above, but with one more type of entry. This is more useful in weekly timeframes, but could also be used in daily time frame:---

Third type of entry:

Close is under 200 Ema

Squeeze momentum crosses under 0 line

Once these rules are met, we enter into a buy position. Stop loss will be determined by atr stop loss (white point) and break even(blue point) by a risk/reward ratio of 1:1.

Like in the past type of entries, for closing this position: Squeeze momentum crosses over 0 and, until squeeze momentum crosses under 0, we close the position. Otherwise, we would have closed the position due to break even or stop loss.

Risk management

For calculating the amount of the position you will use just a small percent of your initial capital for the strategy and you will use the atr stop loss for this.

Example: You have 1000 usd and you just want to risk 2,5% of your account, there is a buy signal at price of 4,000 usd. The stop loss price from atr stop loss is 3,900. You calculate the distance in percent between 4,000 and 3,900. In this case, that distance would be of 2.50%. Then, you calculate your position by this way: (initial or current capital * risk per trade of your account) / (stop loss distance).

Using these values on the formula: (1000*2,5%)/(2,5%) = 1000usd. It means, you have to use 1000 usd for risking 2.5% of your account.

We will use this risk management for applying compound interest.

In settings, with position amount calculator, you can enter the amount in usd of your account and the amount in percentage for risking per trade of the account. You will see this value in green color in the upper left corner that shows the amount in usd to use for risking the specific percentage of your account.

Script functions

Inside of settings, you will find some utilities for display atr stop loss, break evens, positions, signals, indicators, etc.

You will find the settings for risk management at the end of the script if you want to change something. But rebember, do not change values from indicators, the idea is to not over optimize the strategy.

If you want to change the initial capital for backtest the strategy, go to properties, and also enter the commisions of your exchange and slippage for more realistic results.

If you activate break even using rsi, when rsi crosses under overbought zone break even will be activated. This can work in some assets.

---Important: In risk managment you can find an option called "Use leverage ?", activate this if you want to backtest using leverage, which means that in case of not having enough money for risking the % determined by you of your account using your initial capital, you will use leverage for using the enough amount for risking that % of your acount in a buy position. Otherwise, the amount will be limited by your initial/current capital---

Some things to consider

USE UNDER YOUR OWN RISK. PAST RESULTS DO NOT REPRESENT THE FUTURE.

DEPENDING OF % ACCOUNT RISK PER TRADE, YOU COULD REQUIRE LEVERAGE FOR OPEN SOME POSITIONS, SO PLEASE, BE CAREFULL AND USE CORRECTLY THE RISK MANAGEMENT

Do not forget to change commissions and other parameters related with back testing results!

Some assets and timeframes where the strategy has also worked:

BTCUSD : 4H, 1D, W

SPX (US500) : 4H, 1D, W

GOLD : 1D, W

SILVER : 1D, W

ETHUSD : 4H, 1D

DXY : 1D

AAPL : 4H, 1D, W

AMZN : 4H, 1D, W

META : 4H, 1D, W

(and others stocks)

BANKNIFTY : 4H, 1D, W

DAX : 1D, W

RUT : 1D, W

HSI : 1D, W

NI225 : 1D, W

USDCOP : 1D, W

RSI Buy & Sell Trading ScriptThis is my first attempt at a trading script using the RSI indicator for Buy & Sell signals (so please be nice but would appreciate any constructive comments).

Starting with $100 initial capital and using 10% per trade

You can select which month the backtesting starts

There is also a monthly table (sorry can’t remember who I got this from) that shows the total monthly profits, but you’ll need to turn it on by going into settings, Properties and in the Recalculate section tick the “On every tick” box

It should do the following:

Open Buy order if the RSI > 68 and the current Moving Average is greater than the previous Moving average

• TP1 = 50% of Order at 0.4%

• TP2 = 50% of order at 0.8%

• SL = 2% below entry

• Close Buy order if the RSI < 30

Open Sell order if the RSI < 28 and the current Moving Average is less than the previous Moving average

• TP1 = 50% of Order at 0.4%

• TP2 = 50% of order at 0.8%

• SL = 2% above entry

• Close Buy order if the RSI < 60

I would like to build on this if you have any ideas/ code that could help like the following:

• Move the SL to break even when it hits TP1

• Move the SL to TP1 when TP2 hits

• Moving take profit code so I can let the some of the trade stay in play (activate if it hits 1% profit and close trade if price retracts 0.5%)

Refracted EMARefracted EMA is a price based indicator with bands that is built on moving average.

The price range between the bands directly depends on relationship of Average True Range to Moving Average. This gives us very valuable variable constant that changes with the market moves.

So the bands expand and contract due to changes in volatility of the market, which makes this tool very flexible exposing psychological levels.

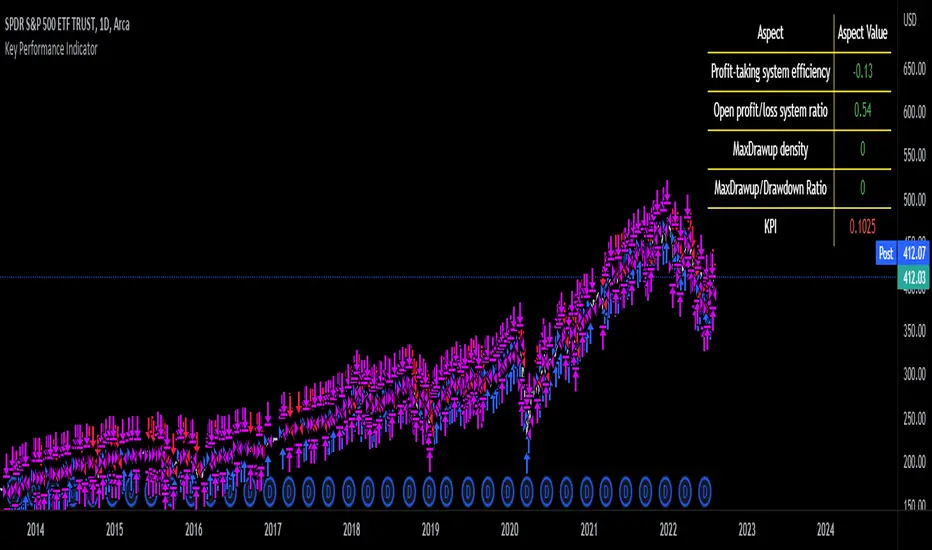

Key Performance IndicatorWe are happy to introduce the Key Performance Indicator by Detlev Matthes. This is an amazing tool to quantify the efficiency of a trading system and identify potential spots of improvement.

Abstract

A key performance indicator with high explanatory value for the quality of trading systems is introduced. Quality is expressed as an indicator and comprises the individual values of qualitative aspects. The work developing the KPI was submitted for the 2017 VTAD Award and won first prize.

Introduction

Imagine that you have a variety of stock trading systems from which to select. During backtesting, each trading system will deliver different results with regard to its indicators (depending on, inter alia, its parameters and the stock used). You will also get different forms of progression for profit development. It requires great experience to select the “best” trading system from this variety of information (provided by several indicators) and significantly varying equity progression forms. In this paper, an indicator will be introduced that expresses the quality of a trading system in just one figure. With such an indicator, you can view the results of one backtest at a glance and also more easily compare a variety of backtesting results with one another.

If you are interested in learning more about the calculations behind this indicator then I have included a link to the english version of his research paper.

Along with this, we now offer indicator development services. If you are interested in learning more then feel free to reach out to get a quote for your project.

**Please note that we have NOT inputted any real strategy into the code and therefore it is not producing any real value. Feel free to change the code as desired to test any strategy!**

drive.google.com

Level 1 - Learn to code simply - PineScriptThe goal of this script is honestly to help everyone learn about trading with bots and algos.

At least, to get started.

Level 1:

10 lines of code.

learn to plot 2 moving averages on your chart.

learn to create a signal from a crossover.

learn the very basics of Pine Script algo.

[Fedra Algotrading LR + TTP Indicator Lite]How it works?

- It calculates the linear regression of the last X candles and define a range based on a linear regression deviation (represented by the 3 parallel lines over the last candle).

-Open trades based on the breakout of the deviation of the linear regression (represented by the yellow triangle).

-Advanced trend filter to not open trades against the trend consist in 2 SMA cross and and a few other conditions, including sptionally super trend (Represented by the red and green background).

-Percentage take profit (represented by the horizontal green line. configurable)

-Percentage stop loss (represented by the horizontal red line. Configurable

-Break even when a trade has already opened and there is a change of trend. Calculated in 1.5% when the price is under the yellow SMA.

Alerts in each case to receive notifications (BUY & SELL, TP BE SL).

Added labels with entry price and PnL of each closed trade to facilitate optimization

Joint Conditions Strategy Suite + TradingConnector alerts bot"Please give us combined alerts with the possibility of having several conditions in place to trigger the alert." - was the top voted request from users under one of the recent blogposts by TradingView.

Ask and you shall receive ;)

TradingView is a great platform, with unmatched set of functionalities, yet this particular combo of features indeed seems not to be in place. Fortunately, TradingView is also very open platform, thanks to PineScript coding language, which enables developing combos like the requried one and plenty of other magic.

I have already published numerous "educational" scripts, showing how to code indicators and alerts with PineScript, but... this is not one of them. This one is for real. READY FOR USE on real markets, also by the non-coding traders. Just take my script, set parameters with dropdowns, backtest the strategy, fire the alerts and execute them.

HOW TO USE IT

In "Settings" popup I tried to mimic the CreateAlert popup dropdowns for selecting logic. Let's say you want to enter Long position at Stochastic KxD crossover. In first line of Long Entry conditions set "StochK" + "Crossing Up" + "StochD". Last field doesn't matter because in 3rd dropdown something else than "value" was selected. In second line you could set "maB" + "Greater Than" + "maC" to filter out those entries which are in direction of the uptrend. And yeah, add ADX>25 to make sure the market is actually moving: "ADX" + "Greater Than" + "value" + "25". All condition lines must be TRUE (or skipped) for the entry to be triggered. Toghether with an alert.

The same for Short entries. Combinations are limitless.

INDICATORS AND MTF (MULTI-TIMEFRAME)

In those dropdowns you can select candle values like open/close/high/low/ohlc4, but also some most popular indicators, which I have pre-built into this script: RSI, various Moving Averages, ADX-DMI, Stochastic and Bollinger Bands for start. You can configure parameters of those indicators also in "Settings" popup, in "Indicator Definitions" section. What's important, you can use any of these indicators from higher timeframe, setting MTF multiplier. So if you applied this indicator to 1h chart, but want to use rsi(close,14) from 4h chart, set MTF to 4. If you want to use current timeframe indicators, keep MTF at 1, which is a default setting here.

Note for coders: to keep focus of this script on joining conditions, entire logic for those indicators has been moved to external library, also open source. I encourage you to dig into the code and see how it's done. I love the addition of libraries concept in PineScript.

CUSTOM INDICATOR

Following the "openness" spirit of my master - which is TradingView itself - my work is also open, in 2 ways:

1. This script is open source. So you can grab it, modify or add any functionalities you want. I cannot and don't want to stop you from doing that. I'm asking for only one favor - please mention this source script in your credits.

2. You can import the plot (series) from any other indicator on TradingView. In Settings popup of my script, scroll down to "Indicator Definitions" section, and select the series of your choice in the first dropdown. Now it is ready to use in conditions dropdowns on top of the Settings popup.

Let me give you an example of that last scenario. Take another script of mine, "Pivot Points on SR lines DEMO". You can find it in "Indicators & Strategies" library or here: (). Attach it to your chart. Now come back to THIS script, open Settings popup and in "Custom Indicator aka Imported Source" select "Pivot Points on SR lines: ...". The way it works - it detects if a pivot point happened on Support/Resistance line from the past and returns 1 for PivotLow and -1 for Pivot High. Now in first Long Entry condition set: "custom indicator" + "Greater Than" + "value" + "0" and long entries will be marked on every pivot low noticed on Support/Resistance line.

ALERTS

Last but not least - the alerts. This script produces alerts on the entries calculated by strategy logic, as marked on the chart by the backtester. Moreover, syntax of those alerts is already prepared and fully compatible with TradingConnector - alerts executing tool (bot), if you want to auto-execute those trades. Apart from installing the tool, you need to set

up the alerts in TradingView, here is how:

open CreateAlert popup

in first dropdown select "Joint Conditions Strategy Template"

in second dropdown select "alert() function calls only"

And that's all. You only need to set one alert for the whole script, not one for Longs and one for Shorts as it was in the past. Also, you don't need to setup closing alerts, because stop-loss/take-profit/trailing-stop information is embedded in the entry alert so your broker receives it as early as possible. Alerts sent will look like this: "long sl=40 tp=80", which is exactly what TradingConnector expects.

Phew, that's all folks. If you think I should add something to this template (maybe other indicators?) please let me know in comments or via DM. Happy trading!

P.S. Pyramiding is not supported in this script.

Disclaimer : I'm not saying above combination of conditions will make you money. Actually none of this can be considered financial advice. It is only a software tool. Use it wisely, be aware of the risk and do your own research!

Bollinger band & Volume based strategy V2this script is upgraded version of previous one the major change is deleted script which find a highest price after entry the last of strategy is same.

If current volume is above daily average volume, and three bollinger band`s Standard Deviation, 1 and 1.5 and 2 if the current lowest price is bigger then 1 stdev and current closed is bigger then 1.5 stdev and the last,highest price is above 2.0 stdev, it defined current market is bullish and had momentum.

and the Short will entered when ma60 and ma120 is undercrossed it work as prevent current price is way lower then entry price.

**this script is working in 15min Only in BTC market or USDT**

** basic equity setting is 500$, set your own**

**if you will use this in real-trade,plz comment the result to me**

Ps: i wanna know why my script is only working well in 15 min tick, anyone who has similar phenomenon or if you had a answer about it, please comment me.

Linear SSL ShortThis script consist of two parts: linear SSL and DEMA. The difference between original SSL and current is that it calculated by linear regression. The logic is simple: when SSL "crossunder" and DEMA is above the price - we get short signal. When price became above DEMA and SSL "crossover" - close short.

Pivot Reversal Strategy + alerts via TradingConnector to indicesSoftware part of algotrading is simpler than you think. TradingView is a great place to do this actually. To present it, I'm publishing each of the default strategies you can find in Pinescript editor's "built-in" list with slight modification - I'm only adding 2 lines of code, which will trigger alerts, ready to be forwarded to your broker via TradingConnector and instantly executed there. Alerts added in this script: 14 and 22.

How it works:

1. TradingView alert fires.

2. TradingConnector catches it and forwards to MetaTrader4/5 you got from your broker.

3. Trade gets executed inside MetaTrader within 1 second of fired alert.

When configuring alert, make sure to select "alert() function calls only" in CreateAlert popup. One alert per ticker is required.

Adding stop-loss, take-profit, trailing-stop, break-even or executing pending orders is also possible. These topics have been covered in other example posts.

This routing works for Forex, indices, stocks, crypto - anything your broker offers via their MetaTrader4 or 5.

Disclaimer: This concept is presented for educational purposes only. Profitable results of trading this strategy are not guaranteed even if the backtest suggests so. By no means this post can be considered a trading advice. You trade at your own risk.

If you are thinking to execute this particular strategy, make sure to find the instrument, settings and timeframe which you like most. You can do this by your own research only.

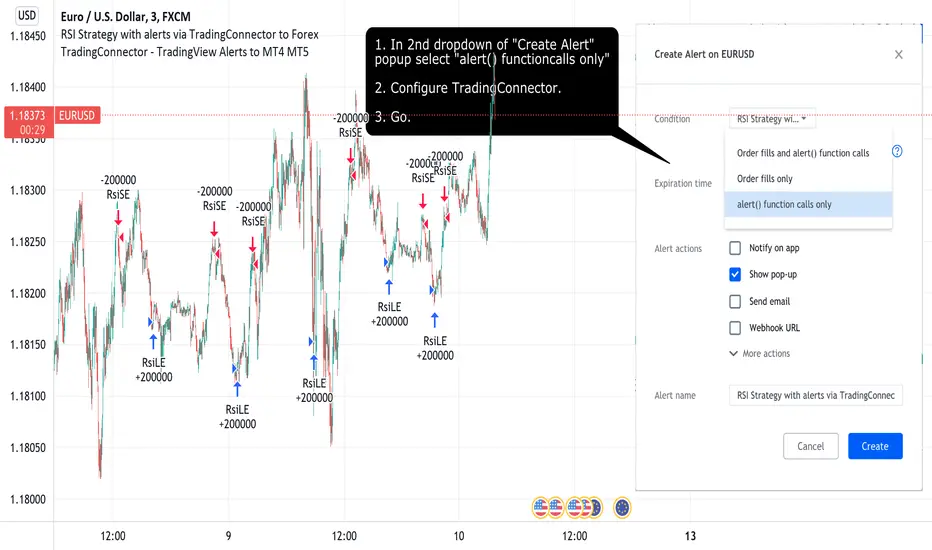

RSI Strategy with alerts via TradingConnector to ForexSoftware part of algotrading is simpler than you think. TradingView is a great place to do this actually. To present it, I'm publishing each of the default strategies you can find in Pinescript editor's "built-in" list with slight modification - I'm only adding 2 lines of code, which will trigger alerts, ready to be forwarded to your broker via TradingConnector and instantly executed there. Alerts added in this script: 12 and 17.

How it works:

1. TradingView alert fires.

2. TradingConnector catches it and forwards to MetaTrader4/5 you got from your broker.

3. Trade gets executed inside MetaTrader within 1 second of fired alert.

When configuring alert, make sure to select "alert() function calls only" in CreateAlert popup. One alert per ticker is required.

Adding stop-loss, take-profit, trailing-stop, break-even or executing pending orders is also possible. These topics have been covered in other example posts.

This routing works for Forex, indices, stocks, crypto - anything your broker offers via their MetaTrader4 or 5.

Disclaimer: This concept is presented for educational purposes only. Profitable results of trading this strategy are not guaranteed even if the backtest suggests so. By no means this post can be considered a trading advice. You trade at your own risk.

If you are thinking to execute this particular strategy, make sure to find the instrument, settings and timeframe which you like most. You can do this by your own research only.

DMI + HMA - No Risk ManagementDMI (Directional Movement Index) and HMA (Hull Moving Average)

The DMI and HMA make a great combination, The DMI will gauge the market direction, while the HMA will add confirmation to the trend strength.

What is the DMI?

The DMI is an indicator that was developed by J. Welles Wilder in 1978. The Indicator was designed to identify in which direction the price is moving. This is done by comparing previous highs and lows and drawing 2 lines.

1. A Positive movement line

2. A Negative movement line

A third line can be added, which would be known as the ADX line or Average Directional Index. This can also be used to gauge the strength in which direction the market is moving.

When the Positive movement line (DI+) is above the Negative movement line (DI-) there is more upward pressure. Ofcourse visa versa, when the DI- is above the DI+ that would indicate more downwards pressure.

Want to know more about HMA? Check out one of our other published scripts

What is this strategy doing?

We are first waiting for the DMI to cross in our favoured direction, after that, we wait for the HMA to signal the entry. Without both conditions being true, no trade will be made.

Long Entries

1. DI+ crosses above DI-

2. HMA line 1 is above HMA line 2

Short Entries

1. DI- Crosses above DI+

2. HMA line 1 is below HMA lilne 2

Its as simple as that.

Conclusion

While this strategy does have its downsides, that can be reduced by adding some risk manegment into the script. In general the trade profitability is above average, And the max drawdown is at a minimum.

The settings have been optimised to suite BTCUSDT PERP markets. Though with small adjustments it can be used on many assets!

Engulfing Candle Rejection IndicatorThis indicator allows you to filter noisy chart, with engulfing candles which have been rejected from current trend lines. Trend lines by default are 21 MA (fast) and 10 MA (slow one). If fast moving average is greater than slower one, automatically indicator would represent that like uptrend, and if opposite then like a downtrend.

Consider to work only on higher time frames like 1H and higher, so you really can find only best entries.

Have fun, best wishes!

Pinbar-Rejection-IndicatorThis indicator allows you to filter noisy pin bar chart, with pin bars which have been rejected from dynamic support/resistance level also named as 21 Moving Average.

I would consider to work only on higher time frames like 1H and higher, so you really can find only best entries.

Have fun, write your feedback in the comments section:)

P.S This is the first version of the indicator, so be free to contribute, and soon I'm going to improve this indicator.

Ichimoku Cloud Strategy Long Only [Bitduke]Slightly modificated and optimized for Pine Script 4.0, Ichimoku Cloud Strategy which, suddenly, good suitable for the several crypto assets.

Details:

Enter position when conversion line crosses base line up, and close it when the opposite happens.

Additional condition for open / close the trade is lagging span, it should be higher than cloud to open position and below - to close it.

Backtesting:

Backtested on SOLUSDT ( FTX, Binance )

+150% for 2021 year, 8% dd

+191% for all time, 32% dd

Disadvantages:

- Small number of trades

- Need to vary parameters for different coins (not very robust)

Should be tested carefully for other coins / stock market. Different parameters could be needed or even algo modifications.

Strategy doesn't repaint.

Grid Bot AutoThis script is an auto-adjusting grid bot simulator. This is an improved version of the original Grid Bot Simulator. The grid bot is best used for ranging/choppy markets. Prices are divided into grids, or trade zones, that will trigger signals each time a new zone is entered. During ranging markets, each transaction is followed by a “take profit.” As the market starts to trend, transactions are stacked (compare to DCA ), until the market consolidates. No signals are triggered above the Upper Limit or Below the Lower Limit. Unlike the previous version, the upper and lower limits are calculated automatically. Grid levels are determined by four factors: Smoothing, Laziness, Elasticity, and Grid Intervals.

Smoothing:

A moving average (or linear regression) is applied to each close price as a basis. Options for smoothing are Linear Regression, Simple Moving Average, Exponential Moving Average, Volume-Weighted Moving Average, Triple-Exponential Moving Average.

Laziness:

Laziness is the percentage change required to reach the next level. If laziness is 1.5, the price must move up or down by 1.5% before the grid will change. This concept is based on Alex Grover’s Efficient Trend Step. This allows the grids to be based on even price levels, as opposed to jagged moving averages.

Elasticity:

Elasticity is the degree of “stickiness” to the current price trend. If the smoothing line remains above (or below) the current grid center without reverting but still not enough to reach the next grid level, the grid line will start to curve toward the next grid level. Elasticity is added to (or subtracted from) the gridline by a factor of minimum system ticks for the current pair. Elasticity of zero will keep the gridlines horizontal. If elasticity is too high, the grid will distort.

Grid Intervals:

Grid intervals are the percentage of space between each grid.

Laziness = 4%, Elasticity = 0. Price must move at least 4% before reaching the next level. With zero elasticity, gridlines are straight.

Laziness = 5%, Elasticity = 100. For each bar at a new grid level, the grid will start “curve” toward the next price level (up if price is greater than the middle grid, down if less than middle grid). Elasticity is calculated by the user-inputted “Elasticity” multiplied by the minimum tick for the current pair (ELSTX = syminfo.mintick * iELSTX)

Try experimenting with different combinations of the Smoothing Length, Smoothing Type, Laziness, Elasticity, and Grid Intervals to find the optimum settings for each chart. Lower-priced pairs (e.g. XRP/ADA/DODGE) will require lower Elasticity. Also note that different exchanges may have different minimum tick values. For example, minimum tick for BITMEX:XBTUSD and BYBIT:BTCUSD is .5, but BINANCE:BTCUSDT and COINBASE:BTCUSD is .01.

s3.tradingview.com

DODGEUSDT, 5min. Laziness: 4%, Elasticity 2.5

Number of Grids: 2. Laziness: 3.75%. Elasticity: 150. Grid Interval 2%.

Settings Overview

Smoothing Length : Smoothing period

Smoothing Type : Linear Regression, Simple Moving Average, Exponential Moving Average, Volume-Weighted Moving Average, Triple-Exponential Moving Average

Laziness : Percentage required for price to move until it reaches the next level. If price does not reach the next level (up or down), the grid will remain the same as previous grid (because it’s lazy).

Elasticity : Amount of curvature toward the next grid, based on the current price trend. As elasticity increases, gridlines will curve up or down by a factor of the number of ticks since the last grid change.

Grid Interval : Percent between grid levels.

Number of Grids : Number of grids to show.

Cooldown : Number of bars to wait to prevent consecutive signals.

Grid Line Transparency : Lower transparencies brighten the gridlines; higher transparencies dim the gridlines. To hide the gridlines completely, enter 100.

Fill Transparency: Lower transparencies brighten the fill box; higher transparencies dim the fill box. To hide the fill box completely, enter 100.

Signal Size : Make signal triangles large or small.

Reset Buy/Sell Index When Grids Change : When a new grid is formed, resetting the index may prevent false signals (experimental)

Use Highs/Lows for Signals : If enabled, signals are triggered as soon as the price touches the next zone. If disabled, signals are triggered after bar closes. Enable this for “Once Per Bar alerts. Disable for “Once Per Bar Close” alerts.

Show Min Tick : If checked, syminfo.mintick is displayed in upper-righthand corner. Useful for estimating Laziness.

Reverse Fill Colors : Default fill for fill boxes is green after buy and red after sell. Check this box to reverse.

Note: The Grid Bot Simulator scripts are experimental and works in progress. Please feel free to comment or contact me if you have suggestions/complaints.

Stochastic TrendDear community,

I've made another simple trading bot for you to use. This bot is based on the Stochastic Oscillator. It only produces long trades currently.

I changed the oscillation period to a much longer one, which in turn creates opportunities to trade long term trends.

The bot goes long when the Entry lines is crossed from below and it will close its long position once the Exit line has been crossed from above.

Strategy NNFX Tester Strategy NNFX, Baseline, QQEs Fast C1, Slow C2, ATR, Volume and Exit

This is a Strategy Tester designed to work with Study (Alerts) of the same.

At time of creation based on Revision 8 of the Study.

DO NOT USE the Currency/Money Management section under settings. use the position sizing under "Inputs" - "Money Management" - "Risk per trade" which is defaulted to 2%

This has adjustable Baselines, Exits, ATR calculations, C1 and C2 are currently QQE & QQE Histo with adjustable settings but I'll include more choice of C1 & C2 as time goes on.

Find settings that work for you, then move them over to the Study version for best results.

Forward plans are to add much more options to both Alert/Strategy.

If anyone wants to collaborate or anything hit me up.

NNFX, Baseline, QQEs Fast C1, Slow C2, ATR, Volume and ExitDesigned Around the NNFX rules

Selectible Baseine

Selectible Exit Indicators

ATR bands, ATR labels for TP and TSL (1x and 1.5x ATR).

Indication (White Diamond) where candle is over 1x ATR in size.

Combined QQE Fast & Slow (C1 & C2) confirmations, Candles Grey before Trend Confirmed, change to Normal Colour when Trend established (QQE MOD used for calcualtions).

Continuations signaled by white dot above/below candle (0.9x ATR from Close Signal).

Exit Long and Exit Short signaled by Red and Blue Arrow under/above candle.