Opening Candle Zone with ATR Bands by nkChartsThis indicator highlights the opening range of each trading session and projects dynamic ATR-based zones around it.

Key Features

Plots high and low levels of the opening candle for each new daily session.

Extends these levels across the session, providing clear intraday support and resistance zones.

Adds ATR-based offset bands above and below the opening range for volatility-adjusted levels.

Customizable colors, ATR length, and multiplier for flexible use across markets and timeframes.

Adjustable session history limit to control how many past levels remain on the chart.

How to Use:

The opening range high/low often acts as strong intraday support or resistance.

The ATR bands give an adaptive volatility buffer, useful for breakout or mean-reversion strategies.

Works on any market with clear session opens.

This tool is designed for traders who want to combine session-based price action with volatility insights, helping identify potential breakouts, reversals, or consolidation areas throughout the day.

⚠️ Disclaimer: This indicator is for educational purposes only. It does not provide financial advice or guarantee profits. Always perform your own analysis before making trading decisions.

アベレージ・トゥルー・レンジ (ATR)

Swing High/Low MarkerThis indicator allows you to find the swing highs and lows of the chart and offsets it by the ATR and a custom factor to give you concrete breakout and stop loss prices.

ATR Regime Study [CHE] ATR Regime Study — ATR percentile regimes with clear bands, table and live label

Summary

This study classifies volatility into five regimes by converting ATR into a percentile rank over a rolling window, plotted on a standardized scale between zero and one hundred. Colored bands mark regime thresholds, while a compact table and an optional label report the current percentile and regime. The standardized scale makes symbols and timeframes easier to compare than raw ATR values. Implemented in Pine v6 as a separate pane (overlay set to false), it is a context tool to adapt tactics and risk handling to the prevailing volatility environment.

Motivation: Why this design?

Raw ATR varies with price scale and asset characteristics, which makes regime comparison inconsistent and leads to poor transfer of settings across symbols and timeframes. The core idea is to transform ATR into a percentile rank within a user-defined lookback, then map it into discrete regimes. This yields a stable, interpretable context signal that shifts slower than raw ATR while still responding to genuine volatility changes.

What’s different vs. standard approaches?

Reference baseline: Traditional ATR plots or ATR bands using fixed multipliers.

Architecture differences:

Percentile ranking of ATR within a rolling window.

Five discrete regimes with fixed thresholds at ninety, seventy, thirty, and ten.

Visual fills between thresholds plus a live table and a last-bar label.

Practical effect: You read a single normalized line between zero and one hundred with consistent thresholds. This improves cross-asset comparison and makes regime shifts obvious at a glance.

How it works (technical)

The script computes ATR over a configurable length, then converts that series to a percentile rank over a configurable number of bars. The percentile is naturally scaled and limited between zero and one hundred. That value is mapped to one of five regimes: above ninety (Extreme), between seventy and ninety (Elevated), between thirty and seventy (Normal), between ten and thirty (Calm), and below ten (Squeeze). Horizontal guide lines mark the thresholds, and fills shade the regions. A table is created once and updated on each bar to show regime definitions and highlight the current row. An optional label on the last bar displays the current percentile and regime. No higher-timeframe requests are used, so repaint risk is limited to normal live-bar fluctuation until the bar closes.

Parameter Guide

ATR length — Effect: Controls how fast ATR reacts to new ranges. Default: fourteen. Trade-offs/Tips: Increase to reduce noise in choppy markets; decrease to react faster during regime changes.

Percentile window (bars) — Effect: Number of bars used for the percentile ranking. Default: two hundred fifty-two. Trade-offs/Tips: Larger windows stabilize the percentile but slow adaptation after structural regime shifts; smaller windows adapt faster but may flip more often.

Table › Show — Effect: Toggles the regime overview table. Default: enabled. Trade-offs/Tips: Disable on constrained layouts to reduce visual clutter.

Table › Position — Effect: Anchors the table in a chart corner. Default: Top Right. Trade-offs/Tips: Choose a corner that avoids overlapping other panels or drawings.

Label › Show — Effect: Toggles a last-bar label with current percentile and regime. Default: enabled. Trade-offs/Tips: Useful for quick reads; disable if it obscures other annotations.

Reading & Interpretation

The white line shows ATR percentile between zero and one hundred. Crossing above seventy signals an elevated volatility environment; above ninety indicates event-driven extremes. Between thirty and seventy represents typical conditions. Between ten and thirty indicates calm conditions that often suit mean reversion. Below ten reflects compression, where breakout probability often increases. The colored bands visually reinforce these ranges. The table summarizes regime definitions and highlights the current state. The last-bar label mirrors the current percentile and regime for quick inspection.

Practical Workflows & Combinations

Trend following: Prefer continuation tactics when the percentile holds in the Normal or Elevated bands and structure confirms higher highs and higher lows. Consider wider stops and partial position sizing as percentile rises.

Mean reversion: Favor fades in Calm regimes within defined ranges; use structure filters and time-of-day constraints to avoid low-liquidity whipsaws.

Breakout preparation: Track compressions below ten; plan entries only with structure confirmation and risk caps, since compressions can persist.

Multi-asset/Multi-TF: Defaults travel well on daily charts. For intraday, reduce the percentile window to align with session dynamics. Combine with trend or market structure tools for confirmation.

Behavior, Constraints & Performance

Repaint/confirmation: The percentile updates during live bars and stabilizes on close; closed bars do not repaint.

security/HTF: Not used. If you add higher-timeframe aggregation externally, account for standard repaint caveats.

Resources: Declared maximum bars back is two thousand; limits for lines and labels are five hundred each. A short loop updates the table rows; arrays are used for table content only.

Known limits: Regime boundaries are fixed; assets with persistent volatility shifts may require window retuning. Low-liquidity periods and gaps can produce abrupt percentile changes. ATR is direction-agnostic and should be paired with trend or structure context.

Sensible Defaults & Quick Tuning

Start with ATR length fourteen and percentile window two hundred fifty-two on daily charts.

Too many flips: Increase ATR length or increase the percentile window.

Too sluggish: Decrease the percentile window or reduce ATR length.

Intraday noise: Keep ATR length moderate and reduce the window to a session-appropriate size; optionally hide the label to declutter.

Compressed markets: Maintain defaults but rely more on structure and volume filters before acting.

What this indicator is—and isn’t

This is a volatility regime context layer that standardizes ATR into interpretable regimes. It is not a complete trading system, not predictive, and not a stand-alone entry signal. Use it alongside structure analysis, confirmation tools, and disciplined risk management.

Disclaimer

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Best regards and happy trading

Chervolino

NY Open OR/ATR Diff Planner – v2.8 NY Open OR/ATR Diff Planner – v2.8 (Hi-Contrast)

Trade the Opening Range Breakout with a plan, not vibes.

This tool builds the NY Opening Range (OR) from the cash open and overlays a complete, risk-based execution plan: precise entry, structural stop, position size, targets, and R:R — all tied to the Daily ATR(14) and the remaining ATR “fuel” left in the day.

What it does

Opening Range: First N minutes after 09:30 ET (choose 5/15/30/60).

Today-only lines: Automatically resets at 09:30; no carry-over from prior days.

Session aware: Works on RTH or ETH charts. OR always anchors at 09:30 ET.

Fuel model: Computes Session Range (since 09:30) and ATR Diff Left = Daily ATR − Session Range.

Entries & Stops:

Long plan: Entry = ORH, Stop = ORL

Short plan: Entry = ORL, Stop = ORH

Targets:

TP1 = 1R (distance of entry→stop)

TP (ATR-diff cap): Entry ± ATR Diff Left (caps greed when the day’s ATR is nearly spent)

Sizing & R:R: Position size = Account × Risk% / Risk per share, with live R:R to ATR-diff target.

Hi-contrast table: Clear readout of Daily ATR, OR size, OR/ATR%, Session Range, ATR left, entries/stops/TPs, size, and max $ risk.

Inputs

Opening Range (minutes): 5 / 15 / 30 / 60

Account Size ($) and Risk % per trade

Session mode: RTH (09:30–16:00) or ETH (chart’s session; still anchored at 09:30)

Also show Short plan (toggle)

Show info table (toggle)

How to use

Add on a 1–5m chart.

Choose your OR window (e.g., 15m = 09:30–09:45).

Set Account Size and Risk % (e.g., 4–5% for small accounts; adjust to taste).

Wait for the OR to complete.

Trade the break/retest with the levels shown:

Long: Break of ORH, SL at ORL, TP1 = 1R, TP2 = ATR-diff cap.

Short: Mirror logic.

If OR/ATR% > ~50% (red), the “fuel” is thin — be selective.

Why it helps build an edge

Objective structure: Clear levels and sizing remove guesswork.

Context-aware targets: ATR-diff keeps targets realistic to the day’s potential.

Discipline by design: One framework that’s easy to review, journal, and iterate.

Notes

This is an indicator (visual planner), not an order-placing strategy.

If you want a back testable version (one trade/day, optional retest rule, TP/SL logic), say the word — I can publish a strategy variant.

Keywords: ORB, Opening Range, ATR, Risk Management, Position Sizing, Day Trading, NYSE Open, Mean Reversion Fuel, Execution Planner

MYM Edge Booster MYM Long Trading Assistant - ATR-Based Edge Booster

Clean, simple indicator that tells you when MYM long setups meet high-probability criteria. No complicated charts - just clear numbers and signals.

• ATR Targets & Stops (whole numbers)

• Quality Score (0-3 stars)

• Green Circle when conditions perfect

• Warnings for choppy/high volatility

• ES/NQ sector confirmation

Eliminates guesswork. Trade when the green circle appears.

Average True Range TrackerThis indicator calculates the daily ATR of the past 14 days. The ATR% indicates the range completed for the day. The ATR indicates the average daily range. The 20% ATR indicates the value of 20% of the daily ATR for retracement purposes.

Daily ATR TrackerThis indicator calculates the daily ATR of the past 14 days. The ATR% indicates the range completed for the day. The ATR indicates the average daily range. The 20% ATR indicates the value of 20% of the daily ATR for retracement purposes.

ATR Enhanced [DCAUT]█ ATR Enhanced

📊 OVERVIEW

Standard ATR uses only RMA smoothing, while ATR Enhanced provides 20+ professional smoothing algorithms , offering precise volatility measurement solutions for different trading scenarios and market environments.

💡 CORE VALUE

- 20+ algorithm choices : SMA, EMA, RMA, WMA, HMA, T3, KAMA, FRAMA, Kalman Filter, etc.

📋 PARAMETER SETUP

ATR Length : Calculation period (default: 14)

Moving Average Type : Choose the most suitable smoothing method from 20+ algorithms

🎨 COLOR CODING

Green : Rising volatility

Red : Falling volatility

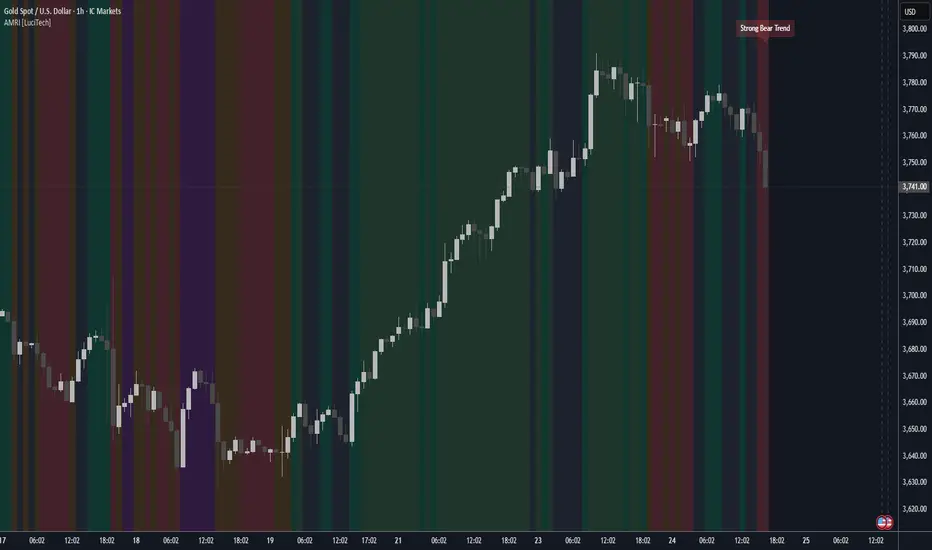

Adaptive Market Regime Identifier [LuciTech]What it Does:

AMRI visually identifies and categorizes the market into six primary regimes directly on your chart using a color-coded background. These regimes are:

-Strong Bull Trend: Characterized by robust upward momentum and low volatility.

-Weak Bull Trend: Indicates upward momentum with less conviction or higher volatility.

-Strong Bear Trend: Defined by powerful downward momentum and low volatility.

-Weak Bear Trend: Suggests downward momentum with less force or increased volatility.

-Consolidation: Periods of low volatility and sideways price action.

-Volatile Chop: High volatility without clear directional bias, often seen during transitions or indecision.

By clearly delineating these states, AMRI helps traders quickly grasp the overarching market context, enabling them to apply strategies best suited for the current conditions (e.g., trend-following in strong trends, range-bound strategies in consolidation, or caution in volatile chop).

How it Works (The Adaptive Edge)

AMRI achieves its adaptive classification by continuously analyzing three core market dimensions, with each component dynamically adjusting to current market conditions:

1.Adaptive Moving Average (KAMA): The indicator utilizes the Kaufman Adaptive Moving Average (KAMA) to gauge trend direction and strength. KAMA is unique because it adjusts its smoothing period based on market efficiency (noise vs. direction). In trending markets, it becomes more responsive, while in choppy markets, it smooths out noise, providing a more reliable trend signal than static moving averages.

2.Adaptive Average True Range (ATR): Volatility is measured using an adaptive version of the Average True Range. Similar to KAMA, this ATR dynamically adjusts its sensitivity to reflect real-time changes in market volatility. This helps AMRI differentiate between calm, ranging markets and highly volatile, directional moves or chaotic periods.

3.Normalized Slope Analysis: The slope of the KAMA is normalized against the Adaptive ATR. This normalization provides a robust measure of trend strength that is relative to the current market volatility, making the thresholds for strong and weak trends more meaningful across different instruments and timeframes.

These adaptive components work in concert to provide a nuanced and responsive classification of the market regime, minimizing lag and reducing false signals often associated with fixed-parameter indicators.

Key Features & Originality:

-Dynamic Regime Classification: AMRI stands out by not just indicating trend or range, but by classifying the type of market regime, offering a higher-level analytical framework. This is a meta-indicator that provides context for all other trading tools.

-Adaptive Core Metrics: The use of KAMA and an Adaptive ATR ensures that the indicator remains relevant and responsive across diverse market conditions, automatically adjusting to changes in volatility and trend efficiency. This self-adjusting nature is a significant advantage over indicators with static lookback periods.

-Visual Clarity: The color-coded background provides an immediate, at-a-glance understanding of the current market regime, reducing cognitive load and allowing for quicker decision-making.

-Contextual Trading: By identifying the prevailing regime, AMRI empowers traders to select and apply strategies that are most effective for that specific environment, helping to avoid costly mistakes of using a trend-following strategy in a ranging market, or vice-versa.

-Originality: While components like KAMA and ATR are known, their adaptive integration into a comprehensive, multi-regime classification system, combined with normalized slope analysis for trend strength, offers a novel approach to market analysis not commonly found in publicly available indicators.

Multi-Symbol Volatility Tracker with Range DetectionMulti-Symbol Volatility Tracker with Range Detection

🎯 Main Purpose:

This indicator is specifically designed for scalpers to quickly identify symbols with high volatility that are currently in ranging conditions . It helps you spot the perfect opportunities for buying at lows and selling at highs repeatedly within the same trading session.

📊 Table Data Explanation:

The indicator displays a comprehensive table with 5 columns for 4 major symbols (GOLD, SILVER, NASDAQ, SP500):

SYMBOL: The trading instrument being analyzed

VOLATILITY: Color-coded volatility levels (NORMAL/HIGH/EXTREME) based on ATR values

Last Candle %: The percentage range of the most recent 5-minute candle

Last 5 Candle Avg %: Average percentage range over the last 5 candles

RANGE: Shows "YES" (blue) or "NO" (gray) indicating if the symbol is currently ranging

🔍 How to Identify Trading Opportunities:

Look for symbols that combine these characteristics:

RANGE column shows "YES" (highlighted in blue) - This means the symbol is moving sideways, perfect for range trading

VOLATILITY shows "HIGH" or "EXTREME" - Ensures there's enough movement for profitable scalping

Higher candlestick percentages - Indicates larger candle ranges, meaning more profit potential per trade

⚡ Optimal Usage:

Best Timeframe: Works optimally on 5-minute charts where the ranging patterns are most reliable for scalping

Trading Strategy: When you find a symbol with "YES" in the RANGE column, switch to that symbol and look for opportunities to buy near the lows and sell near the highs of the ranging pattern

Risk Management: Higher volatility symbols offer more profit potential but require tighter risk management

⚙️ Settings:

ATR Length: Adjusts the Average True Range calculation period (default: 14)

Range Sensitivity: Fine-tune range detection sensitivity (0.1-2.0, lower = more sensitive)

💡 Pro Tips:

The indicator updates in real-time, so monitor for symbols switching from "NO" to "YES" in the RANGE column

Combine HIGH/EXTREME volatility with RANGE: YES for the most profitable scalping setups

Use the candlestick percentages to gauge potential profit per trade - higher percentages mean more movement

The algorithm uses advanced statistical analysis including standard deviation, linear regression slopes, and range efficiency to accurately detect ranging conditions

Perfect for day traders and scalpers who want to quickly identify which symbols offer the best ranging opportunities for consistent buy-low, sell-high strategies.

SMC BOS - Structure Breaks & Median Continuation ProjectionsThis tool shows what usually happens after a Break of Structure (BOS).

It scans past BOS events on your chart, finds the ones most similar to the latest break (using ATR to filter by volatility), and then plots the median continuation path.

Optional percentile bands (P10–P90) display the possible range of outcomes around the median.

Key features:

• Automatic detection of bullish and bearish BOS events

• Library of past BOS with adjustable size and spacing

• ATR-based similarity and recency weighting

• Median continuation projections with optional percentile bands

• Customizable colors, signals, and stats table

• Works on any market and timeframe

Use cases:

• See how price typically behaves after a BOS

• Support SMC analysis with data-driven projections

• Improve trade planning by visualizing likely continuations

• Apply across crypto, forex, stocks, and futures

Originality:

Instead of only marking BOS, this script learns from history and projects forward the median path of the most similar past cases, adjusted for volatility. It turns BOS signals into practical continuation scenarios.

Instructions:

Add the indicator to your chart. When a BOS is detected, the projection is drawn automatically.

Use the settings to adjust the library, ATR weighting, projection style, percentile bands, and the display of signals or stats.

For questions or customization, contact Julien Eche (Julien_Eche) on TradingView.

DashBoard 2.3.1📌 Indicator Name:

DashBoard 2.3 – Smart Visual Market Overlay

📋 Description:

DashBoard 2.3 is a clean, efficient, and highly informative market overlay, designed to give you real-time context directly on your chart — without distractions. Whether you're swing trading or investing long-term, this tool keeps critical market data at your fingertips.

🔍 Key Features:

Symbol + Timeframe + Market Cap

Shows the current ticker and timeframe, optionally with real-time market cap.

ATR 14 with Volatility Signal

Displays ATR with color-coded risk levels:

🟢 Low

🟡 Moderate

🔴 High

⚫️ Extreme

You can choose between Daily ATR or timeframe-based ATR (auto-adjusted to chart resolution).

Adaptive Labeling

The ATR label updates to reflect the resolution:

ATR 14d (daily)

ATR 14W (weekly)

ATR 14H (hourly), etc.

Moving Average Tracker

Instantly shows whether price is above or below your selected moving average (e.g., 150 MA), with green/red indication.

Earnings Countdown

Clearly shows how many days remain until the next earnings report.

Industry & Sector Info (optional)

Useful for thematic or sector-based trading strategies.

Fully Customizable UI

Choose positioning, padding, font size, and which data to show. Designed for minimalism and clarity.

✅ Smart Logic:

Color dots appear only in relevant conditions (e.g., ATR color signals shown only on daily when enabled).

ATR display automatically reflects your time frame, if selected.

Clean chart integration – the overlay sits quietly in a corner, enhancing your analysis without intruding.

🧠 Ideal for:

Swing traders, position traders, and investors who want fast, high-impact insights directly from the chart.

Anyone looking for a compact, beautiful, and informative dashboard while they trade.

Avg Candle Size (Ticks) – Last 9 Closed BarsWhat it does:

Shows the average candle size in ticks for the last N closed bars (defaults to 9). I built this so I can glance at a 5-min chart and instantly know the typical bar size in ticks, updating only after each bar closes (no intrabar wiggle).

How it works:

Measures each bar’s full range (High–Low), not ATR and not candle body.

Averages the last N closed bars, converts to ticks using syminfo.mintick.

Displays a simple line plus a small readout (e.g., “32 ticks”).

Why I built it:

Gives me a realistic sense of current volatility in ticks so I can size stops/targets quickly without doing mental math.

Extras:

Lookback is configurable (default 9).

Optional rounding (floor/nearest/ceil).

Works on any timeframe/instrument that has a defined tick size.

If you want it to match ATR exactly (in ticks), swap the range calc for ta.atr(len) / syminfo.mintick

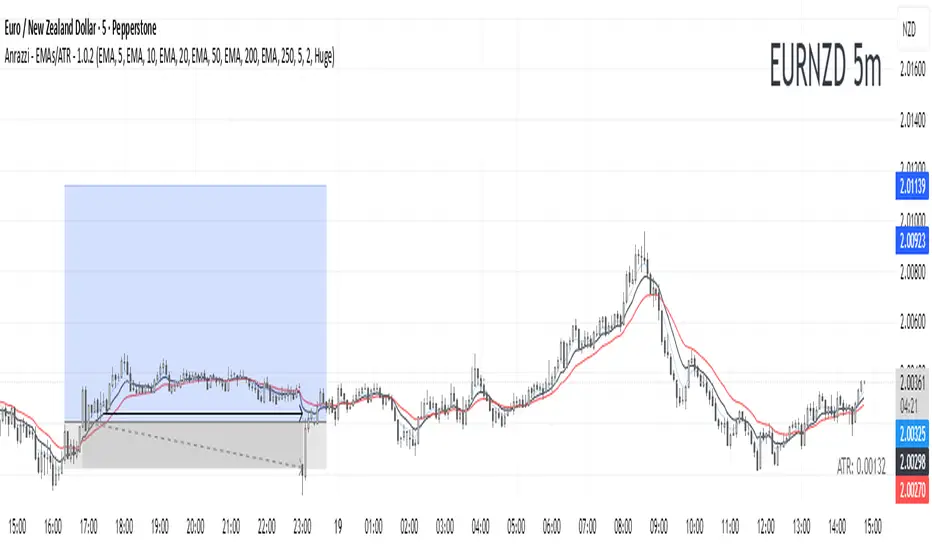

Anrazzi - EMAs/ATR - 1.0.2The Anrazzi – EMAs/ATR indicator is a multi-purpose overlay designed to help traders track trend direction and market volatility in a single clean tool.

It plots up to six customizable moving averages (MAs) and an Average True Range (ATR) value directly on your chart, allowing you to quickly identify market bias, dynamic support/resistance, and volatility levels without switching indicators.

This script is ideal for traders who want a simple, configurable, and efficient way to combine trend-following signals with volatility-based position sizing.

📌 Key Features

Six Moving Averages (MA1 → MA6)

Toggle each MA on/off individually

Choose between EMA or SMA for each

Customize length and color

Perfect for spotting trend direction and pullback zones

ATR Display

Uses Wilder’s ATR formula (ta.rma(ta.tr(true), 14))

Can be calculated on current or higher timeframe

Adjustable multiplier for position sizing (e.g., 1.5× ATR stops)

Displays cleanly in the bottom-right corner

Custom Watermark

Displays symbol + timeframe in top-right

Adjustable color and size for streamers, screenshots, or clear charting

Compact UI

Organized with group and inline inputs for quick configuration

Lightweight and optimized for real-time performance

⚙️ How It Works

MAs: The script uses either ta.ema() or ta.sma() to compute each moving average based on the user-selected type and length.

ATR: The ATR is calculated using ta.rma(ta.tr(true), 14) (Wilder’s smoothing), and optionally scaled by a multiplier for easier use in risk management.

Tables: ATR value and watermark are displayed using table.new() so they stay anchored to the screen regardless of zoom level.

📈 How to Use

Enable the MAs you want to track and adjust their lengths, type, and colors.

Enable ATR if you want to see volatility — optionally select a higher timeframe for broader context.

Use MAs to:

Identify overall trend direction (e.g. price above MA20 = bullish)

Spot pullback zones for entries

See when multiple MAs cluster together as support/resistance zones

Use ATR value to:

Size your stop-loss dynamically (e.g. stop = entry − 1.5×ATR)

Detect volatility breakouts (ATR spikes = market expansion)

🎯 Recommended For

Day traders & swing traders

Trend-following & momentum strategies

Volatility-based risk management

Traders who want a clean, all-in-one dashboard

Anrazzi - EMAs/ATR - 1.0.2Description:

The Anrazzi - EMAs/ATR indicator is a versatile tool for technical traders looking to monitor multiple moving averages alongside the Average True Range (ATR) on any chart. Designed for simplicity and customization, it allows traders to visualize up to six moving averages with configurable type, color, and length, while keeping real-time volatility information via ATR directly on the chart.

This indicator is perfect for spotting trends, identifying support/resistance zones, and gauging market volatility for intraday or swing trading strategies.

Key Features:

Supports up to six independent moving averages (MA1 → MA6)

Each MA is fully customizable:

Enable/disable individually

Type: EMA or SMA

Length

Color

ATR Display:

Custom timeframe

Color and position configurable

Adjustable multiplier

Compact and organized settings for easy configuration

Lightweight and efficient code for smooth chart performance

Watermark

Inputs / Settings:

MA Options: MA1 → MA6 (Enable/Disable, Type, Length, Color)

Additional Settings: ATR (Enable, Timeframe, Color, Multiplier)

How to Use:

Enable the moving averages you want to track

Configure type, length, and color for each MA

Enable ATR if needed and adjust settings

Watch MAs plotted dynamically and ATR in bottom-right corner

Recommended For:

Day traders and swing traders

Trend-following strategies

Volatility analysis and breakout detection

Traders needing a compact multi-MA dashboard

Omega ATR Indicator📖 Introduction

The Ω ATR Indicator was created to provide a more complete and professional framework for volatility analysis than the classic Average True Range (ATR).

While the traditional ATR is a useful tool, it has limitations: it delivers a simple rolling average of volatility, but it does not adapt to market regimes, it does not highlight extreme events, and it often leaves the trader with incomplete information about risk.

The Ω ATR takes the same foundation and elevates it into a multi-dimensional volatility dashboard, adding statistical layers, adaptive calculations, and clear visual references that allow traders to interpret volatility in a way that is immediately actionable.

🔎 What makes it different from a standard ATR?

This indicator introduces several features beyond the classic formula:

True Range Core – plots the raw True Range (TR) for each bar, providing a direct, bar-by-bar view of volatility impulses.

Standard & Adjusted ATR – includes both the conventional ATR (smoothed average) and an Adjusted ATR that automatically corrects for extreme conditions by incorporating percentile rescaling.

Percentile Volatility Levels – dynamically calculated extreme thresholds (99.8%, 75%, 50%, 25%), plotted as dotted levels across the chart. These act as reference lines for “normal” vs. “abnormal” volatility, useful for spotting unusual price expansions or contractions.

Linear Regression Volatility Trend – overlays a regression line of volatility, showing whether the market is moving toward expansion (rising vol), contraction (falling vol), or stability.

Monetary Value Translation – the indicator converts volatility into points, ticks, and dollar values (based on the instrument’s point value). This allows futures traders and high-value instruments users to immediately see how much volatility is “worth” in cash terms.

Interactive Table Display – a real-time statistics table is displayed directly on the chart, showing:

SMA of ATR in $ and points

Percentile-based volatility range (VAR) in $ and points

Tick equivalences, for quick position sizing

⚡ How traders can use it

The Ω ATR Indicator is designed to be versatile, fitting both discretionary traders and systematic strategy developers.

Risk Management: ATR-based stop losses and position sizing are significantly improved by using the adjusted ATR and percentile thresholds. Traders can size their positions according to volatility regimes, not just raw averages.

Breakout & Exhaustion Detection: When TR or ATR values spike above the 99.8% or 95% percentile levels, this often corresponds to breakout conditions or volatility exhaustion — useful for breakout strategies, mean-reversion setups, and volatility fades.

Market Regime Identification: The regression line helps distinguish if volatility is rising (trending environment, larger swings expected) or compressing (range-bound environment, lower risk opportunities).

Multi-Asset Flexibility: Works equally well on equities, futures, crypto, and FX. Its point/tick/dollar conversion makes it especially powerful for futures traders who need to quantify risk precisely.

Scalping to Swing Trading: On lower timeframes, it acts as a micro-volatility detector; on higher timeframes, it functions as a strategic risk gauge for position management.

⚙️ Settings and Customization

Length: The ATR lookback period (default = 34).

Shorter lengths (14–21) for intraday traders who want fast response.

Longer lengths (34–55) for swing/position traders who want smoother readings.

AVG / ADJ AVG: Toggle to display the standard ATR or the adjusted ATR.

Volatility Levels: Enable/disable up to 4 percentile-based levels (1st = 25%, 2nd = 50%, 3rd = 75%, 4th = 99.8%). Recommended: keep 3 levels active for clarity.

Color Controls: All plots and levels are fully customizable to match your chart style.

Table Display: Positioned on the chart (default: middle-right) with key values updated in real time.

🧭 Best Practices for Use

Combine with Trend Tools: Volatility readings are most powerful when combined with trend filters or volume analysis. For example, a breakout with both high volatility and trend confirmation is stronger than either alone.

ATR Stops: Use the Adjusted ATR rather than the standard one when trailing stops in highly volatile instruments like crypto or Nasdaq futures, as it adapts to outlier spikes.

Dollar Risk Translation: Use the dollar-value outputs to predefine maximum acceptable risk per trade (e.g., “I only risk $250 per position”). This bridges volatility to portfolio risk management.

Event Monitoring: Around economic events or earnings, expect volatility spikes above higher percentile levels. The indicator makes these moves instantly visible.

📌 Summary

The Ω ATR Indicator is not just “another ATR.” It is a comprehensive volatility framework that transforms volatility from a simple statistic into an actionable trading signal.

By combining:

the classic ATR,

an adjusted ATR,

percentile extremes,

regression-based volatility trends,

and real-time dollar conversions,

…this tool allows traders to precisely understand, visualize, and act on volatility in ways that a standard ATR simply cannot provide.

Whether you are scalping intraday moves, swing trading equities, or managing futures positions, the Ω ATR equips you with a professional-grade volatility dashboard that clarifies risk, highlights opportunity, and adapts across all markets and timeframes.

👉 Designed and developed by OmegaTools for traders who demand precision, clarity, and adaptability in their volatility analysis.

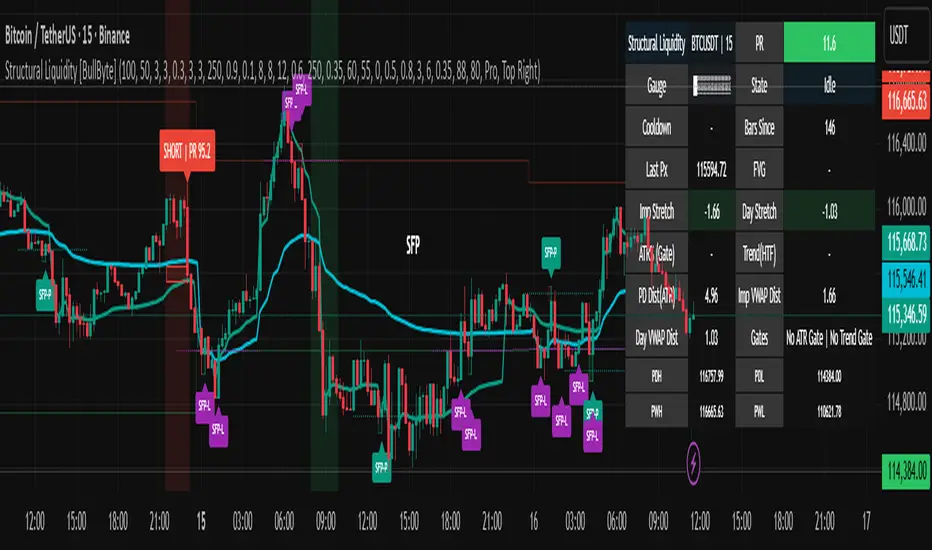

Structural Liquidity Signals [BullByte]Structural Liquidity Signals (SFP, FVG, BOS, AVWAP)

Short description

Detects liquidity sweeps (SFPs) at pivots and PD/W levels, highlights the latest FVG, tracks AVWAP stretch, arms percentile extremes, and triggers after confirmed micro BOS.

Full description

What this tool does

Structural Liquidity Signals shows where price likely tapped liquidity (stop clusters), then waits for structure to actually change before it prints a trigger. It spots:

Liquidity sweeps (SFPs) at recent pivots and at prior day/week highs/lows.

The latest Fair Value Gap (FVG) that often “pulls” price or serves as a reaction zone.

How far price is stretched from two VWAP anchors (one from the latest impulse, one from today’s session), scaled by ATR so it adapts to volatility.

A “percentile” extreme of an internal score. At extremes the script “arms” a setup; it only triggers after a small break of structure (BOS) on a closed bar.

Originality and design rationale, why it’s not “just a mashup”

This is not a mashup for its own sake. It’s a purpose-built flow that links where liquidity is likely to rest with how structure actually changes:

- Liquidity location: We focus on areas where stops commonly cluster—recent pivots and prior day/week highs/lows—then detect sweeps (SFPs) when price wicks beyond and closes back inside.

- Displacement context: We track the last Fair Value Gap (FVG) to account for recent inefficiency that often acts as a magnet or reaction zone.

- Stretch measurement: We anchor VWAP to the latest N-bar impulse and to the Daily session, then normalize stretch by ATR to assess dislocation consistently across assets/timeframes.

- Composite exhaustion: We combine stretch, wick skew, and volume surprise, then bend the result with a tanh transform so extremes are bounded and comparable.

- Dynamic extremes and discipline: Rather than triggering on every sweep, we “arm” at statistical extremes via percent-rank and only fire after a confirmed micro Break of Structure (BOS). This separates “interesting” from “actionable.”

Key concepts

SFP (liquidity sweep): A candle briefly trades beyond a level (where stops sit) and closes back inside. We detect these at:

Pivots (recent swing highs/lows confirmed by “left/right” bars).

Prior Day/Week High/Low (PDH/PDL/PWH/PWL).

FVG (Fair Value Gap): A small 3‑bar gap (bar2 high vs bar1 low, or vice versa). The latest gap often acts like a magnet or reaction zone. We track the most recent Up/Down gap and whether price is inside it.

AVWAP stretch: Distance from an Anchored VWAP divided by ATR (volatility). We use:

Impulse AVWAP: resets on each new N‑bar high/low.

Daily AVWAP: resets each new session.

PR (Percentile Rank): Where the current internal score sits versus its own recent history (0..100). We arm shorts at high PR, longs at low PR.

Micro BOS: A small break of the recent high (for longs) or low (for shorts). This is the “go/no‑go” confirmation.

How the parts work together

Find likely liquidity grabs (SFPs) at pivots and PD/W levels.

Add context from the latest FVG and AVWAP stretch (how far price is from “fair”).

Build a bounded score (so different markets/timeframes are comparable) and compute its percentile (PR).

Arm at extremes (high PR → short candidate; low PR → long candidate).

Only print a trigger after a micro BOS, on a closed bar, with spacing/cooldown rules.

What you see on the chart (legend)

Lines:

Teal line = Impulse AVWAP (resets on new N‑bar extreme).

Aqua line = Daily AVWAP (resets each session).

PDH/PDL/PWH/PWL = prior day/week levels (toggle on/off).

Zones:

Greenish box = latest Up FVG; Reddish box = latest Down FVG.

The shading/border changes after price trades back through it.

SFP labels:

SFP‑P = SFP at Pivot (dotted line marks that pivot’s price).

SFP‑L = SFP at Level (at PDH/PDL/PWH/PWL).

Throttle: To reduce clutter, SFPs are rate‑limited per direction.

Triggers:

Triangle up = long trigger after BOS; triangle down = short trigger after BOS.

Optional badge shows direction and PR at the moment of trigger.

Optional Trigger Zone is an ATR‑sized box around the trigger bar’s close (for visualization only).

Background:

Light green/red shading = a long/short setup is “armed” (not a trigger).

Dashboard (Mini/Pro) — what each item means

PR: Percentile of the internal score (0..100). Near 0 = bullish extreme, near 100 = bearish extreme.

Gauge: Text bar that mirrors PR.

State: Idle, Armed Long (with a countdown), or Armed Short.

Cooldown: Bars remaining before a new setup can arm after a trigger.

Bars Since / Last Px: How long since last trigger and its price.

FVG: Whether price is in the latest Up/Down FVG.

Imp/Day VWAP Dist, PD Dist(ATR): Distance from those references in ATR units.

ATR% (Gate), Trend(HTF): Status of optional regime filters (volatility/trend).

How to use it (step‑by‑step)

Keep the Safety toggles ON (default): triggers/visuals on bar‑close, optional confirmed HTF for trend slope.

Choose timeframe:

Intraday (5m–1h) or Swing (1h–4h). On very fast/thin charts, enable Performance mode and raise spacing/cooldown.

Watch the dashboard:

When PR reaches an extreme and an SFP context is present, the background shades (armed).

Wait for the trigger triangle:

It prints only after a micro BOS on a closed bar and after spacing/cooldown checks.

Use the Trigger Zone box as a visual reference only:

This script never tells you to buy/sell. Apply your own plan for entry, stop, and sizing.

Example:

Bullish: Sweep under PDL (SFP‑L) and reclaim; PR in lower tail arms long; BOS up confirms → long trigger on bar close (ATR-sized trigger zone shown).

Bearish: Sweep above PDH/pivot (SFP‑L/P) and reject; PR in upper tail arms short; BOS down confirms → short trigger on bar close (ATR-sized trigger zone shown).

Settings guide (with “when to adjust”)

Safety & Stability (defaults ON)

Confirm triggers at bar close, Draw visuals at bar close: Keep ON for clean, stable prints.

Use confirmed HTF values: Applies to HTF trend slope only; keeps it from changing until the HTF bar closes.

Performance mode: Turn ON if your chart is busy or laggy.

Core & Context

ATR Length: Bigger = smoother distances; smaller = more reactive.

Impulse AVWAP Anchor: Larger = fewer resets; smaller = resets more often.

Show Daily AVWAP: ON if you want session context.

Use last FVG in logic: ON to include FVG context in arming/score.

Show PDH/PDL/PWH/PWL: ON to see prior day/week levels that often attract sweeps.

Liquidity & Microstructure

Pivot Left/Right: Higher values = stronger/rarer pivots.

Min Wick Ratio (0..1): Higher = only more pronounced SFP wicks qualify.

BOS length: Larger = stricter BOS; smaller = quicker confirmations.

Signal persistence: Keeps SFP context alive for a few bars to avoid flicker.

Signal Gating

Percent‑Rank Lookback: Larger = more stable extremes; smaller = more reactive extremes.

Arm thresholds (qHi/qLo): Move closer to 0.5 to see more arms; move toward 0/1 to see fewer arms.

TTL, Cooldown, Min bars and Min ATR distance: Space out triggers so you’re not reacting to minor noise.

Regime Filters (optional)

ATR percentile gate: Only allow triggers when volatility is at/above a set percentile.

HTF trend gate: Only allow longs when the HTF slope is up (and shorts when it’s down), above a minimum slope.

Visuals & UX

Only show “important” SFPs: Filters pivot SFPs by Volume Z and |Impulse stretch|.

Trigger badges/history and Max badge count: Control label clutter.

Compact labels: Toggle SFP‑P/L vs full names.

Dashboard mode and position; Dark theme.

Reading PR (the built‑in “oscillator”)

PR ~ 0–10: Potential bullish extreme (long side can arm).

PR ~ 90–100: Potential bearish extreme (short side can arm).

Important: “Armed” ≠ “Enter.” A trigger still needs a micro BOS on a closed bar and spacing/cooldown to pass.

Repainting, confirmations, and HTF notes

By default, prints wait for the bar to close; this reduces repaint‑like effects.

Pivot SFPs only appear after the pivot confirms (after the chosen “right” bars).

PD/W levels come from the prior completed candles and do not change intraday.

If you enable confirmed HTF values, the HTF slope will not change until its higher‑timeframe bar completes (safer but slightly delayed).

Performance tips

If labels/zones clutter or the chart lags:

Turn ON Performance mode.

Hide FVG or the Trigger Zone.

Reduce badge history or turn badge history off.

If price scaling looks compressed:

Keep optional “score”/“PR” plots OFF (they overlay price and can affect scaling).

Alerts (neutral)

Structural Liquidity: LONG TRIGGER

Structural Liquidity: SHORT TRIGGER

These fire when a trigger condition is met on a confirmed bar (with defaults).

Limitations and risk

Not every sweep/extreme reverses; false triggers occur, especially on thin markets and low timeframes.

This indicator does not provide entries, exits, or position sizing—use your own plan and risk control.

Educational/informational only; no financial advice.

License and credits

© BullByte - MPL 2.0. Open‑source for learning and research.

Built from repeated observations of how liquidity runs, imbalance (FVG), and distance from “fair” (AVWAPs) combine, and how a small BOS often marks the moment structure actually shifts.

Trend-Strong Candle - Pro Multi Assetighlights:

Major Assets Mode (optional): EURUSD, GBPUSD, USDJPY, AUDUSD, USDCAD, NZDUSD, EURGBP, EURJPY

One‑per‑bar alerts, 24/7 toggle, no session limits

Default EMAs 20/40/60, improved stability and EMA-close filters

Lightweight performance, warning-free calculations, and clearer arrows/plots

VIX CCI Oscillator [Compression + EMA Trigger + Bounce Glow]VIX CCI OSCILLATOR

ADJ CHART FOR YOUR LIKING

NOT AS SMOOTH AS PREVIOUS VERSION (STOCH)

SHOWS TIGER SIGNAL ON EMA

SAMEOUTPUT

HUD Box: emoji-coded tactical feedback

bounce 100 "💥 Expansion" :

bounce 0.8 "🔴 Overbought" :

bounce 0.618 "📉 Distribution" :

bounce 0.5 "🧠 Midline" :

bounce 0.382 "📈 Accumulation" :

bounce 0.2 "🟢 Oversold" :

bounce0.0 "💣 Expansion" : "⚪ Neutral"

Tiger EMA/STOCH

This logic checks if the oscillator is trending above or below its 48-period EMA,

If above, it paints the line GREEN🟢 (bullish),

If below, it paints it RED🔴 (bearish),

If compression is active, it overrides both with purple🟣 to highlight tactical squeeze conditions,

⚠️WARNING⚠️

ALWAYS REMEMBER THIS CHART IS VIX/USD

IN MOST CASES SPY MOVES VICE VERSA

I AM NOT RESPOSIBLE FOR YOUR OWN ACTIONS/TRADE IDEAS

2ATR / Current Price %### **Real-Time 2ATR Volatility Ratio Indicator**

---

### **Overview**

This indicator provides a quick and visual way to understand market volatility by calculating the ratio between the **2ATR (Average True Range)** and the **current price**.

* **ATR (Average True Range)** is a widely-used measure of market volatility, showing the average price movement over a specific period.

* **2ATR** represents a price move that is twice the average volatility. Traders often use this value as a benchmark for potential support/resistance levels or for setting a dynamic stop-loss.

### **Key Features**

* **Real-Time Calculation**: Unlike many indicators that rely on the previous candle's close, this script calculates the 2ATR ratio using the **real-time current price**, providing you with up-to-the-second data.

* **Intuitive Display**: The final percentage value is shown in a clear **yellow label** at the **bottom-right** of your chart, making it easy to monitor without cluttering your view.

* **Customizable Input**: You can adjust the `ATR Period` setting to change the sensitivity of the volatility calculation, allowing you to adapt the indicator to different trading styles and timeframes.

### **How to Use It**

This tool is especially useful for **risk management and setting stop-loss orders**. The percentage displayed on the label tells you how much the price would need to move from its current level to equal a 2ATR change.

**Example**: If the indicator shows **3.5%**, it means a price drop of 3.5% from the current level would be equal to a 2ATR move. This gives you a clear and quantifiable number to help you set a **logical stop-loss** or to quickly assess the potential downside risk before entering a trade.

Turtle Trading with LayeringCrafted professional write-up for TradingView indicator publication.

Turtle Trading with Layering System

A complete implementation of the famous turtle trading strategy with proper position layering/pyramiding for manual trading.

Features

Core Turtle System:

20-day breakout entries (primary signals)

55-day breakout entries (backup after losses)

10-day reverse breakout exits

ATR-based stop losses and position sizing

Position Layering:

Build positions gradually as trends develop

Add up to 4 units per position

Each unit added every 0.5 ATR in your favor

Single stop loss protects entire position

LBM-Strategy Engine Pro: The Ultimate Confluence IndicatorOverview

Welcome to the Strategy Engine Pro , the ultimate confluence indicator designed for traders who demand precision and full control over their trading signals. This is not just an indicator; it is a complete, customizable strategy-building framework.

It seamlessly integrates three powerful concepts into a single, intuitive tool:

Advanced Moving Average Trend Analysis to define the market context.

An intelligent Support & Resistance Cycle Engine to identify key price levels.

A flexible 10-rule Strategy Builder that lets you design, test, and refine your own entry signals with surgical precision.

Core Features

1. Advanced Moving Average Trend Analysis

The indicator plots 5 fully configurable Moving Averages (MAs). You can choose the Period and Type (SMA, EMA, WMA, HMA, RMA) for each one. But its true power lies in its unique color-coding system, which analyzes the slope and momentum of each MA, not just its price.

MA Color Code:

Green: The MA is in a strong, confirmed uptrend.

Red: The MA is in a strong, confirmed downtrend.

Yellow: The MA is flat or in a transitional (sideways) phase.

This provides an instant visual snapshot of the market trend across five different timeframes.

2. Support & Resistance Cycle Engine

Forget simple pivot points. This indicator incorporates a sophisticated engine that identifies and plots significant "Master Cycle" levels on your chart.

Anchored Levels: These S/R lines are persistent and intelligent. When a key resistance level is broken, it automatically "flips" and becomes the new anchored support level, and vice-versa. This accurately maps out the market's structural progression.

The Strategy Builder: Your Personal Trading Lab

This is the heart of the indicator. You have 10 sequential rules that allow you to define the exact conditions for a Buy signal. The Sell signal is generated as the logical, symmetrical opposite.

For each rule, you can configure:

Source A & Source B: Choose from a wide range of data points:

Price values: Close, Open, High, Low.

Previous candle values: Close Before, Open Before, etc.

Moving Average values: MA 1 through MA 5.

MA Trend Colors: MA 1 Color, MA 2 Color Before, etc.

Operator: Define the comparison logic:

Standard: >, <, >=, <=

Events: Crossover, Crossunder

Color Logic: Is Color, Is NOT Color, Turned Color, Ceased to be Color

Important Note on Sell Signals: Sell conditions are designed to be the symmetrical opposite of the buy conditions you create.

If Buy is Close > MA 1, Sell will be Close < MA 1.

If Buy is MA 1 Color Is Green, Sell will be MA 1 Color Is Red.

If Buy is MA 1 Color Turned Green, Sell will be MA 1 Color Turned Red.

This ensures your sell strategy mirrors the logic of your buy strategy, preventing the "inverse problem" of getting sell signals on every candle that isn't a buy signal.

Mastering the Connectors: ( ) AND and ( ) OR

The true power of the Strategy Builder lies in its connectors, which allow you to create complex, multi-layered logic. The connector on a rule defines how it connects to the next active rule.

AND & OR: These work as you'd expect, creating a continuous chain of conditions.

Rule 1 (AND) & Rule 2 is evaluated as (R1 AND R2).

( ) OR (The Group Separator): This is your most powerful tool. It acts like closing a parenthesis in an equation. It finalizes the current group of rules and connects it to the

next group with a big "OR".

Example: (R1 AND R2) OR (R3 AND R4)

This creates two possible paths for a signal.

- Rule 1: Condition R1, Connector AND

- Rule 2: Condition R2, Connector ( ) OR <-- This closes the first group and links to the next with OR.

- Rule 3: Condition R3, Connector AND

- Rule 4: Condition R4

( ) AND (The Super-Filter): This allows you to create a "master" condition that must be true in addition to other complex conditions.

Example: (R1 OR R2) AND (R3 OR R4)

This requires a condition from the first group and a condition from the second group to be true.

- Rule 1: Condition R1, Connector OR

- Rule 2: Condition R2, Connector ( ) AND <-- This closes the first OR group and links to the next with AND.

- Rule 3: Condition R3, Connector OR

- Rule 4: Condition R4

By strategically combining these connectors, you can build any logical trading scenario you can imagine. We look forward to seeing the powerful strategies the community creates with this engine.

Composite Time ProfileComposite Time Profile Overlay (CTPO) - Market Profile Compositing Tool

Automatically composite multiple time periods to identify key areas of balance and market structure

What is the Composite Time Profile Overlay?

The Composite Time Profile Overlay (CTPO) is a Pine Script indicator that automatically composites multiple time periods to identify key areas of balance and market structure. It's designed for traders who use market profile concepts and need to quickly identify where price is likely to find support or resistance.

The indicator analyzes TPO (Time Price Opportunity) data across different timeframes and merges overlapping profiles to create composite levels that represent the most significant areas of balance. This helps you spot where institutional traders are likely to make decisions based on accumulated price action.

Why Use CTPO for Market Profile Trading?

Eliminate Manual Compositing Work

Instead of manually drawing and compositing profiles across different timeframes, CTPO does this automatically. You get instant access to composite levels without spending time analyzing each individual period.

Spot Areas of Balance Quickly

The indicator highlights the most significant areas of balance by compositing overlapping profiles. These areas often act as support and resistance levels because they represent where the most trading activity occurred across multiple time periods.

Focus on What Matters

Rather than getting lost in individual session profiles, CTPO shows you the composite levels that have been validated across multiple timeframes. This helps you focus on the levels that are most likely to hold.

How CTPO Works for Market Profile Traders

Automatic Profile Compositing

CTPO uses a proprietary algorithm that:

- Identifies period boundaries based on your selected timeframe (sessions, daily, weekly, monthly, or auto-detection)

- Calculates TPO profiles for each period using the C2M (Composite 2 Method) row sizing calculation

- Merges overlapping profiles using configurable overlap thresholds (default 50% overlap required)

- Updates composite levels as new price action develops in real-time

Key Levels for Market Profile Analysis

The indicator displays:

- Value Area High (VAH) and Value Area Low (VAL) levels calculated from composite TPO data

- Point of Control (POC) levels where most trading occurred across all composited periods

- Composite zones representing areas of balance with configurable transparency

- 1.618 Fibonacci extensions for breakout targets based on composite range

Multiple Timeframe Support

- Sessions: For intraday market profile analysis

- Daily: For swing trading with daily profiles

- Weekly: For position trading with weekly structure

- Monthly: For long-term market profile analysis

- Auto: Automatically selects timeframe based on your chart

Trading Applications for Market Profile Users

Support and Resistance Trading

Use composite levels as dynamic support and resistance zones. These levels often hold because they represent areas where significant trading decisions were made across multiple timeframes.

Breakout Trading

When composite levels break, they often lead to significant moves. The indicator calculates 1.618 Fibonacci extensions to give you clear targets for breakout trades.

Mean Reversion Strategies

Value Area levels represent the price range where most trading activity occurred. These levels often act as magnets, drawing price back when it moves too far from the mean.

Institutional Level Analysis

Composite levels represent areas where institutional traders have made significant decisions. These levels often hold more weight than traditional technical analysis levels because they're based on actual trading activity.

Key Features for Market Profile Traders

Smart Compositing Logic

- Automatic overlap detection using price range intersection algorithms

- Configurable overlap thresholds (minimum 50% overlap required for merging)

- Dead composite identification (profiles that become engulfed by newer composites)

- Real-time updates as new price action develops using barstate.islast optimization

Visual Customization

- Customizable colors for active, broken, and dead composites

- Adjustable transparency levels for each composite state

- Premium/Discount zone highlighting based on current price vs composite range

- TPO aggression coloring using TPO distribution analysis to identify buying/selling pressure

- Fibonacci level extensions with 1.618 target calculations based on composite range

Clean Chart Presentation

- Only shows the most relevant composite levels (maximum 10 active composites)

- Eliminates clutter from individual session profiles

- Focuses on areas of balance that matter most to current price action

Real-World Trading Examples

Day Trading with Session Composites

Use session-based composites to identify intraday areas of balance. The VAH and VAL levels often act as natural profit targets and stop-loss levels for scalping strategies.

Swing Trading with Daily Composites

Daily composites provide excellent swing trading levels. Look for price reactions at composite zones and use the 1.618 extensions for profit targets.

Position Trading with Weekly Composites

Weekly composites help identify major trend changes and long-term areas of balance. These levels often hold for months or even years.

Risk Management

Composite levels provide natural stop-loss levels. If a composite level breaks, it often signals a significant shift in market sentiment, making it an ideal place to exit losing positions.

Why Composite Levels Work

Composite levels work because they represent areas where significant trading decisions were made across multiple timeframes. When price returns to these levels, traders often remember the previous price action and make similar decisions, creating self-fulfilling prophecies.

The compositing process uses a proprietary algorithm that ensures only levels validated across multiple time periods are displayed. This means you're looking at levels that have proven their significance through actual market behavior, not just random technical levels.

Technical Foundation

The indicator uses TPO (Time Price Opportunity) data combined with price action analysis to identify areas of balance. The C2M row sizing method ensures accurate profile calculations, while the overlap detection algorithm (minimum 50% price range intersection) ensures only truly significant composites are displayed. The algorithm calculates row size based on ATR (Average True Range) divided by 10, then converts to tick size for precise level calculations.

How the Code Actually Works

1. Period Detection and ATR Calculation

The code first determines the appropriate timeframe based on your chart:

- 1m-5m charts: Session-based profiles

- 15m-2h charts: Daily profiles

- 4h charts: Weekly profiles

- 1D charts: Monthly profiles

For each period type, it calculates the number of bars needed for ATR calculation:

- Sessions: 540 minutes divided by chart timeframe

- Daily: 1440 minutes divided by chart timeframe

- Weekly: 7 days worth of minutes divided by chart timeframe

- Monthly: 30 days worth of minutes divided by chart timeframe

2. C2M Row Size Calculation

The code calculates True Range for each bar in the determined period:

- True Range = max(high-low, |high-prevClose|, |low-prevClose|)

- Averages all True Range values to get ATR

- Row Size = (ATR / 10) converted to tick size

- This ensures each TPO row represents a meaningful price movement

3. TPO Profile Generation

For each period, the code:

- Creates price levels from lowest to highest price in the range

- Each level is separated by the calculated row size

- Counts how many bars touch each price level (TPO count)

- Finds the level with highest count = Point of Control (POC)

- Calculates Value Area by expanding from POC until 68.27% of total TPO blocks are included

4. Overlap Detection Algorithm

When a new profile is created, the code checks if it overlaps with existing composites:

- Calculates overlap range = min(currentVAH, prevVAH) - max(currentVAL, prevVAL)

- Calculates current profile range = currentVAH - currentVAL

- Overlap percentage = (overlap range / current profile range) * 100

- If overlap >= 50%, profiles are merged into a composite

5. Composite Merging Logic

When profiles overlap, the code creates a new composite by:

- Taking the earliest start bar and latest end bar

- Using the wider VAH/VAL range (max of both profiles)

- Keeping the POC from the profile with more TPO blocks

- Marking the composite as "active" until price breaks through

6. Real-Time Updates

The code uses barstate.islast to optimize performance:

- Only recalculates on the last bar of each period

- Updates active composite with live price action if enabled

- Cleans up old composites to prevent memory issues

- Redraws all visual elements from scratch each bar

7. Visual Rendering System

The code uses arrays to manage drawing objects:

- Clears all lines/boxes arrays on every bar

- Iterates through composites array to redraw everything

- Uses different colors for active, broken, and dead composites

- Calculates 1.618 Fibonacci extensions for broken composites

Getting Started with CTPO

Step 1: Choose Your Timeframe

Select the period type that matches your trading style:

- Use "Sessions" for day trading

- Use "Daily" for swing trading

- Use "Weekly" for position trading

- Use "Auto" to let the indicator choose based on your chart timeframe

Step 2: Customize the Display

Adjust colors, transparency, and display options to match your charting preferences. The indicator offers extensive customization options to ensure it fits seamlessly into your existing analysis.

Step 3: Identify Key Levels

Look for:

- Composite zones (blue boxes) - major areas of balance

- VAH/VAL lines - value area boundaries

- POC lines - areas of highest trading activity

- 1.618 extension lines - breakout targets

Step 4: Develop Your Strategy

Use these levels to:

- Set entry points near composite zones

- Place stop losses beyond composite levels

- Take profits at 1.618 extension levels

- Identify trend changes when major composites break

Perfect for Market Profile Traders

If you're already using market profile concepts in your trading, CTPO eliminates the manual work of compositing profiles across different timeframes. Instead of spending time analyzing each individual period, you get instant access to the composite levels that matter most.

The indicator's automated compositing process ensures you're always looking at the most relevant areas of balance, while its real-time updates keep you informed of changes as they happen. Whether you're a day trader looking for intraday levels or a position trader analyzing long-term structure, CTPO provides the market profile intelligence you need to succeed.

Streamline Your Market Profile Analysis

Stop wasting time on manual compositing. Let CTPO do the heavy lifting while you focus on executing profitable trades based on areas of balance that actually matter.

Ready to Streamline Your Market Profile Trading?

Add the Composite Time Profile Overlay to your charts today and experience the difference that automated profile compositing can make in your trading performance.