Institutional Volume RSI [Adaptive]The Institutional Volume RSI is a next-generation momentum oscillator designed to solve the two biggest problems with standard RSI: Price Deception and Static Thresholds.

Standard RSI uses fixed 70/30 levels to define "Overbought" and "Oversold." This is flawed because in a strong institutional trend, the market can stay "Overbought" for weeks. Selling just because RSI hit 70 is a guaranteed way to lose money.

This tool fixes that.

It replaces static lines with Adaptive Volatility Bands . These bands breathe with the market—expanding during trends and contracting during squeezes—giving you a dynamic, statistically significant view of true momentum.

How It Works

The engine runs on three institutional concepts:

1. Volume-Weighted Source (VWMA) 📊

We calculate RSI based on Volume Weighted Moving Average , not just Close price.

Low Volume Move: RSI ignores it (Fakeout).

High Volume Move: RSI reacts aggressively (True Momentum).

2. Adaptive Volatility Bands 🌊

Instead of fixed lines, we use dynamic bands (similar to Bollinger Bands) applied directly to the RSI.

The Trend Ride: As long as the RSI line stays inside or above the Upper Band, the trend is strong. Do not sell.

The Squeeze: When the bands contract (get tight), it signals that volatility is dead and a massive explosive move is imminent.

3. Dynamic Sentiment Coloring 🎨

Green Line: RSI is above the baseline (Bullish Control).

Red Line: RSI is below the baseline (Bearish Control).

White Dots: These appear when RSI breaks outside the bands, signaling an extreme statistical anomaly (often a climax top or bottom).

The "Elastic Snap" Strategy

Recommended Companion: Hooke's Law: Market Elasticity

This indicator is the perfect "Trigger" for a Mean Reversion system. We recommend pairing it with a Reversal indicator (like Hooke's Law) to create a complete Setup + Trigger system.

The Strategy Rules:

1. The Setup (The Stretch) 📏

Wait for your Reversal Indicator (e.g., Hooke's Law) to identify an overextended market condition (Overbought/Oversold).

Context: The rubber band is stretched tight.

2. The Trigger (The Snap) 🔫

Do not enter blindly! Look at the IV-RSI :

For Shorts: Wait for the RSI line to turn RED . This confirms that momentum has actually rolled over.

For Longs: Wait for the RSI line to turn GREEN . This confirms that buyers have stepped in.

3. The Filter (The Safety) 🛡️

If price hits your Stop Loss level before the IV-RSI changes color, cancel the trade . This prevents you from shorting a strong trend that is simply "melting up" without volume exhaustion.

Settings & Configuration

RSI Length: Default is 14.

Source Type: VWMA (Volume Weighted) is recommended for institutional analysis.

Bands Multiplier: Default is 2.0 (Standard Deviation). Increasing this to 2.5 will make the "White Dot" extremes rarer and more significant.

Disclaimer

Trading involves a high level of risk and is not suitable for all investors. The content provided here is for educational purposes only and does not constitute financial advice. Past performance is not indicative of future results. The author (abgthecoder) is not responsible for any financial losses incurred from the use of this indicator. Always use proper risk management and never trade with money you cannot afford to lose. This tool is provided "as is" with open source code for the benefit of the trading community.

Reversion

CPR OI Toolkit - All in one indicatorThis is experimental indicator which is an extend my pre triple EMA indicator. I have been using this indicator to identify potential entry and exit for commodity market. I had used it for couple of week and it helps.

I would like to share with you. It is meant identify and analyze then plan your trade. I have developed this indicator using Google Antigravity , which is an awesome tool for developing trading indicator and strategies.

My CPR OI tool kit includes following.

Triple EMA

Stochastic - for trend catching

Previous Low/high base trial and visual indication

Price action concepts

Reversion logic.

Visual indication - buy / sell / setup initialization / exit

Visual dashboard.

---

## 🎨 Visual Signal Guide

| Marker | Meaning | Action |

|--------|---------|--------|

| 🔵 Tiny Blue Circle | Stochastic bullish setup START | Wait for EMA + breakout |

| 🟢 Green Triangle UP | **LONG ENTRY** - All conditions met | **ENTER LONG** |

| 🔴 Red Triangle DOWN | **SHORT ENTRY** | **ENTER SHORT** |

| 🟠 Orange Circle | **EXIT** - EMA1/2 cross | **CLOSE POSITION** |

| 💧 Aqua "R" | Mean reversion long | Scalp opportunity |

| 💜 Fuchsia "R" | Mean reversion short | Scalp opportunity |

---

## 💰 Open Interest Interpretation

| Status | Price vs Prev | OI Change | Meaning |

|--------|---------------|-----------|---------|

| **Long Accumulation**🟢 | ↑ | ↑ | Bulls building positions |

| **Short Accumulation**🔴 | ↓ | ↑ | Bears building positions |

| **Short Covering**🟡 | ↑ | ↓ | Bears exiting (bullish) |

| **Long Unwinding**🟠 | ↓ | ↓ | Bulls exiting (bearish) |

---

## 🔔 Alerts (All Enabled by Default)

1. "LONG Signal | Stochastic confirmed | EMA Bullish"

2. "SHORT Signal | Stochastic confirmed | EMA Bearish"

3. "EMA Alignment: BULLISH/BEARISH"

4. "Position CLOSED - Trailing Stop Hit"

---

VWAP Tension Bands + Osc Sigma Gap [MAXmks]Hello Traders,

This indicator started as an accident. I was building a different tool — a multi-metric dashboard — and added VWAP deviation as one of the components. I expected it to help catch falling knives. It didn't.

But I noticed something else. During cooling-off periods — when volatility fades and price just sits there, not really going anywhere — VWAP deviation on lower timeframes would start climbing quietly. And more often than not, a pullback followed. Sometimes a liquidity sweep first, then a pullback. I watched this pattern for months before deciding to build a dedicated tool around it, adding oscillator confirmation to filter the noise.

This is that tool.

The core idea

Markets act like a rubber band around VWAP — the further price stretches, the higher the tension. But raw deviation isn't enough. The real question: is momentum confirming the stretch, or lagging behind?

The σ-Gap captures when these two disagree — price pushed hard, but internals haven't caught up. That's where mean-reversion setups tend to appear.

The indicator tracks VWAP deviation across 2m / 5m / 15m simultaneously and compares it against a composite of momentum oscillators (Williams %R, CVD-based metrics). Signals require multi-timeframe consensus — no single timeframe can trigger alone.

Adaptive thresholds

What counts as "extreme" isn't fixed. Distance is measured in standard deviations (σ) , not pips or percentages — so the indicator adapts to volatility automatically. Thresholds scale with regime and historical distribution, adjusting to current market conditions in real time.

Two modes

Standard — adaptive thresholds, more signals. Good for active sessions and exploration.

High Precision — adds divergence confirmation from multiple oscillators (MFI, Delta RSI, CVD Z-Score). Fewer signals, higher selectivity.

Extreme Tension

When σ-Gap exceeds 1.6× the threshold, the indicator can fire without full confirmation. Rare, but these are the "overstretched" moments worth watching.

Filters (so you don't trade ghosts)

RVOL filter blocks signals during low activity. Session close filter avoids entries near VWAP reset. 24h volume filter skips illiquid instruments. Cooldown prevents signal clustering in the same direction.

Best use case

Built for short-term mean-reversion — quick snapback plays on 5m–15m charts where price overextends and reverts within a few candles. The engine is optimized for this rhythm, not for trend-following or swings.

On-chart

Tension Bands show dynamic threshold zones around VWAP. Signals are non-repainting and confirmed on bar close. Compact HUD displays all metrics, filter states, and signal status in real time.

Alerts

Pre-signal alerts when conditions start forming. Confirmed signal alerts with full breakdown: VWAP deviation values, σ-Gap readings, divergences detected, current mode.

Volume matters

This is a VWAP-based indicator. No volume data = no signal. If your instrument shows "No Volume" in the dashboard, switch to a data feed that provides it (crypto spot, futures, stocks with real volume).

A note on expectations

I use this logic in my own research and it has shown useful results for me in my backtesting scenarios. But this is an indicator for analysis , not a magic button. Your execution, fees, slippage, and market regime all matter. Treat signals as context, not commands. DYOR.

Feedback welcome.

For educational and analysis purposes only. Not financial advice.

Mean Reversion [SIMI]This mean reversion indicator identifies extreme price deviations from the mean, providing high-probability reversal signals. Designed for confluence-based trading, it works best when combined with complementary indicators such as VWAP, price action, and volume analysis.

📊 Core Features

Signal Types

Prime Signals (Bright Green/Red Dots): Extreme reversions usually beyond ±1.5 SD - highest probability setups (you can customise this zone!)

Regular Signals (Dark Green/Red Dots): Standard reversions - moderate probability

Leader Line (Pink Dotted): Early warning indicator for potential reversals

Histogram Weakness: Momentum divergence signals

Normalisation Methods:

Institutional Hybrid (Z-ATR) (Recommended): Volatility-adjusted Z-score - adapts to changing market conditions

Percentile Ranking: Statistical ranking - excellent for ranging markets

PPO + ATR Hybrid: Percentage-based with volatility adjustment

Efficiency Ratio: Trend-strength weighted

ATR: Pure volatility-based

None: Raw Z-score

⚙️ Quick Setup Guide

1. Institutional Presets

Pre-configured parameter sets optimised for different timeframes:

5M Day Trading (5/21/5): Intraday scalping

1H Options Trading (6/24/5): Options-focused setups

1D Monthly Cycle (5/20/5): Swing trading

2. Signal Filtering

Prime Thresholds: Adjust ±1.5 SD to control signal quality (tighter = fewer, higher quality, adjust this zone per asset traded)

Dot Filters: Fine-tune entry zones (-0.03/+0.03 default - this ignores noisy signals near Zero line)

Volume Filter: Enable to require volume confirmation (1.4x average recommended, but fine tune yourself)

3. Advanced Filters

Dynamic SD Thresholds: Auto-adjusts for volatility regimes (tighter in low vol, wider in high vol)

Time of Day Filter: Avoids first 30 minutes, last 15 minutes, and lunch hour (11:30-13:00 EST)

💡 Trading Strategy Recommendations

Optimal Usage

This indicator is not intended as a standalone system. Use it for confluence alongside:

VWAP (institutional positioning)

Price action (support/resistance)

Options flow (institutional direction)

Volume analysis (conviction confirmation)

Signal Interpretation

Prime Signals: Wait for these for highest-probability entries - mean reversion may take hours to days

Manual Entries: Don't wait for dots - trade the ±2 SD zones directly using your own confirmation

Options Strategy: Prime sell signals at +2 SD make excellent short call setups; prime buy signals at -2 SD for long calls

Timeframe Guidance

Lower Timeframes (1M-5M): Higher noise - require additional confluence

Higher Timeframes (1H-1D): More reliable signals - suitable for options and swing trades

Best Results: Multi-timeframe analysis (check 1H and 4H alignment on 5M entries)

🔔 Alert System

Master Alert

Enable customisable alerts via the Master Alert System:

Toggle individual signal types (Prime Buy/Sell, SD Crosses, Leader, Histogram)

Receives bespoke messages with ticker, timeframe, and price

One alert condition handles all selected signals

Individual Alerts

Separate alert conditions available for Prime and Regular signals if preferred.

📈 Backtesting Notes

Important: Backtest results are date-sensitive and should not be the primary focus. Instead:

Dial in settings visually on your chosen asset

Aim for signals near actual tops and bottoms

Test different normalisation methods for your specific instrument

Optimise for signal quality, not backtest ROI

Asset Testing: Primarily developed using SPY, QQQ, and IWM as main assets to trade. Other instruments may require parameter adjustment - mess around!

Backtest Engine

Entry/Exit modes (All Signals, Prime Only, Early Signals)

Position sizing (percentage-based)

Slippage and fill method (candle close recommended)

Date range selection

⚠️ Best Practices

Always use confluence - never trade on MR signals alone

Start with Institutional Hybrid normalisation - most adaptive to market conditions

Focus on Prime signals for quality over quantity

Test on your specific asset - optimal settings vary by instrument

Longer timeframes = higher reliability - 1H+ for best results

Enable Time Filter on intraday charts to avoid volatile periods

Use Dynamic SD in highly volatile markets (earnings, FOMC, etc.)

🛠️ Troubleshooting

Too many signals: Increase Prime Thresholds or enable Volume Filter

Too few signals: Decrease Prime Thresholds or reduce Dot Filters

False signals: Enable Time of Day Filter and Dynamic SD

Signals don't align with tops/bottoms: Try different normalisation method

📝 Feedback & Development

Bug Reports: Please report any issues via TradingView comments or direct message.

Strategy Sharing: I'd love to hear how you're using this indicator and what strategies you've developed.

Open Source: Feel free to fork and modify this indicator. If you create an improved version, please share it with the community!

🙏 Acknowledgements

Developed through AI-assisted collaboration.

Special thanks to Lazy Bear for his open source MACD histogram (volume based).

Open source forever - use freely, modify, and share.

Happy Trading!

Remember: Past performance does not guarantee future results. Always manage risk appropriately.

Pandas rock \m/

Mean Reversion Mirror📌 Mean Reversion Mirror — Multi‑Level Mean Reversion Strategy

Mean Reversion Mirror is an advanced modular mean‑reversion strategy built around dynamic and static deviation levels from a moving average.

The strategy automatically scales into positions across six levels (LONG and SHORT), using both dynamic MA‑based deviation levels and static levels that lock in after entry.

🔍 Core Concept

Price tends to revert toward its mean.

This strategy exploits that behavior by opening an initial base entry at the first deviation and adding positions as the imbalance grows.

Each additional level improves the average entry price and increases the probability of exiting profitably.

⚙️ Key Features

📈 Six Dynamic Deviation Levels

Levels are calculated as percentage deviations from a selected MA (WMA, SMA, EMA, RMA, HMA).

This makes the strategy adaptive to volatility and market structure.

📉 Six Static Levels

Once triggered, each level becomes fixed and no longer changes.

This creates a stable averaging grid independent of future MA movement.

🎯 Flexible Take‑Profit System

fixed take‑profit

or trailing take‑profit with dynamic offset

🖐 Manual Entry Support

You can manually set a price for LONG or SHORT, and the strategy will execute the base entry automatically.

📊 Rich Visualization

dynamic deviation levels

static levels

dotted “last chance” levels

average position price

take‑profit line

compact mini‑table with key position metrics

📦 Two Operating Modes

STK Mode — fixed unit size

Classic Mode — quantity calculated from USD value

🧠 Entry Logic

The strategy uses sequences B1–B6 (LONG) and S1–S6 (SHORT):

B1/S1 — base entry

B2–B6 / S2–S6 — averaging entries as deviation increases

L6/S6 — “last chance” level with its own size

Each level activates only after the previous one.

📌 Who This Strategy Is For

mean‑reversion traders

grid/averaging system users

pullback‑based investors

traders who want clear visual levels

users who prefer manual control over entry points

⚠️ Disclaimer

This strategy is not financial advice.

Always backtest and adjust parameters according to your risk tolerance before using it in live markets.

VixTrixVixTrix - Because markets move in both directions.

VixTrix was born from a fundamental limitation in traditional volatility indicators: they only measure downside panic, completely missing the greed-driven extremes that form market tops.

How It Works:

Dual-Component Analysis:

vixBear = Panic selling intensity (distance from recent highs)

vixBull = FOMO buying intensity (distance from recent lows)

Oscillator = vixBear - vixBull = Net fear/greed imbalance

When the oscillator is positive, fear dominates (potential bottom forming). When negative, greed dominates (potential top forming).

Professional-Grade Filtering:

The magic happens with the symmetric RMS (Root Mean Square) bands. Unlike fixed percentage bands or standard deviation, RMS:

Creates mathematically symmetric positive/negative thresholds

Naturally adapts to changing volatility regimes

Provides statistical significance to extremes

VixTrix also adds selectable MA smoothing for the RMS calculation:

WMA (default): Balanced – middle-ground approach

VWMA: Volume-weighted – filters low-volume noise

EMA: Responsive – catches quick reversals

SMA: Stable – for swing trading

HMA: Fast and smooth – ideal for day trading

Signals require triple confirmation:

Statistical Extreme: Oscillator beyond RMS band

Price Action Confirmation: Correct candle color (bullish for bottoms, bearish for tops)

Momentum Continuation: Oscillator still moving toward extreme (exhaustion)

This multi-filter approach reduces premature entries and false signals while maintaining early positioning at potential reversal points.

Why This Matters for Your Trading:

In bull markets, traditional fear indicators sit near zero, giving no warning of impending tops.

VixTrix identifies when greed becomes excessive – when FOMO buying reaches statistical extremes that often precede corrections.

In range-bound markets, VixTrix excels at identifying overreactions in both directions, providing high-probability mean reversion opportunities.

During crashes, it captures the panic selling with the same precision as VixFix, but with better timing through its momentum confirmation.

VixTrix spots continuations through:

"No Signal" = Healthy Trend – Oscillator stays between RMS bands (no exhaustion)

Failed Extremes – Touches band but no triple confirmation = trend likely continues

Hidden Divergence – Price makes higher low while oscillator makes shallower low = uptrend continues

Controlled Emotions – Oscillator negative but not extreme in uptrends (greed present but not excessive)

Key Insight: When VixTrix doesn't give a signal during a pullback, institutions aren't panicking – they're just pausing before resuming the trend.

Green columns = Bullish exhaustion (potential bottoms)

Red columns = Bearish exhaustion (potential tops)

Golden RMS bands = Dynamic thresholds adapting to current volatility

Background highlights = Active signal conditions

The Result: A professional-grade oscillator that works in all market conditions – trending up, trending down, or ranging – by measuring the complete emotional spectrum driving price action.

LuxyEnergyIndexThe Luxy Energy Index (LEI) library provides functions to measure price movement exhaustion by analyzing three dimensions: Extension (distance from fair value), Velocity (speed of movement), and Volume (confirmation level).

LEI answers a different question than traditional momentum indicators: instead of "how far has price gone?" (like RSI), LEI asks "how tired is this move?"

This library allows Pine Script developers to integrate LEI calculations into their own indicators and strategies.

How to Import

//@version=6

indicator("My Indicator")

import OrenLuxy/LuxyEnergyIndex/1 as LEI

Main Functions

`lei(src)` → float

Returns the LEI value on a 0-100 scale.

src (optional): Price source, default is `close`

Returns : LEI value (0-100) or `na` if insufficient data (first 50 bars)

leiValue = LEI.lei()

leiValue = LEI.lei(hlc3) // custom source

`leiDetailed(src)` → tuple

Returns LEI with all component values for detailed analysis.

= LEI.leiDetailed()

Returns:

`lei` - Final LEI value (0-100)

`extension` - Distance from VWAP in ATR units

`velocity` - 5-bar price change in ATR units

`volumeZ` - Volume Z-Score

`volumeModifier` - Applied modifier (1.0 = neutral)

`vwap` - VWAP value used

Component Functions

| Function | Description | Returns |

|-----------------------------------|---------------------------------|---------------|

| `calcExtension(src, vwap)` | Distance from VWAP / ATR | float |

| `calcVelocity(src)` | 5-bar price change / ATR | float |

| `calcVolumeZ()` | Volume Z-Score | float |

| `calcVolumeModifier(volZ)` | Volume modifier | float (≥1.0) |

| `getVWAP()` | Auto-detects asset type | float |

Signal Functions

| Function | Description | Returns |

|---------------------------------------------|----------------------------------|-----------|

| `isExhausted(lei, threshold)` | LEI ≥ threshold (default 70) | bool |

| `isSafe(lei, threshold)` | LEI ≤ threshold (default 30) | bool |

| `crossedExhaustion(lei, threshold)` | Crossed into exhaustion | bool |

| `crossedSafe(lei, threshold)` | Crossed into safe zone | bool |

Utility Functions

| Function | Description | Returns |

|----------------------------|-------------------------|-----------|

| `getZone(lei)` | Zone name | string |

| `getColor(lei)` | Recommended color | color |

| `hasEnoughHistory()` | Data check | bool |

| `minBarsRequired()` | Required bars | int (50) |

| `version()` | Library version | string |

Interpretation Guide

| LEI Range | Zone | Meaning |

|-------------|--------------|--------------------------------------------------|

| 0-30 | Safe | Low exhaustion, move may continue |

| 30-50 | Caution | Moderate exhaustion |

| 50-70 | Warning | Elevated exhaustion |

| 70-100 | Exhaustion | High exhaustion, increased reversal risk |

Example: Basic Usage

//@version=6

indicator("LEI Example", overlay=false)

import OrenLuxy/LuxyEnergyIndex/1 as LEI

// Get LEI value

leiValue = LEI.lei()

// Plot with dynamic color

plot(leiValue, "LEI", LEI.getColor(leiValue), 2)

// Reference lines

hline(70, "High", color.red)

hline(30, "Low", color.green)

// Alert on exhaustion

if LEI.crossedExhaustion(leiValue) and barstate.isconfirmed

alert("LEI crossed into exhaustion zone")

Technical Details

Fixed Parameters (by design):

Velocity Period: 5 bars

Volume Period: 20 bars

Z-Score Period: 50 bars

ATR Period: 14

Extension/Velocity Weights: 50/50

Asset Support:

Stocks/Forex: Uses Session VWAP (daily reset)

Crypto: Uses Rolling VWAP (50-bar window) - auto-detected

Edge Cases:

Returns `na` until 50 bars of history

Zero volume: Volume modifier defaults to 1.0 (neutral)

Credits and Acknowledgments

This library builds upon established technical analysis concepts:

VWAP - Industry standard volume-weighted price measure

ATR by J. Welles Wilder Jr. (1978) - Volatility normalization

Z-Score - Statistical normalization method

Volume analysis principles from Volume Spread Analysis (VSA) methodology

Disclaimer

This library is provided for **educational and informational purposes only**. It does not constitute financial advice. Past performance does not guarantee future results. The exhaustion readings are probabilistic indicators, not guarantees of price reversal. Always conduct your own research and use proper risk management when trading.

Luxy VWAP Magic - MTF Projection EngineThis indicator transforms the classic VWAP into a comprehensive trading system. Instead of switching between multiple indicators, you get everything in one place: multi-timeframe analysis, statistical bands, momentum detection, volume profiling, session tracking, and divergence signals.

What Makes This Different

Traditional VWAP indicators show a single line. This tool treats VWAP as a foundation for complete market analysis. The indicator automatically detects your asset type (stocks, crypto, forex, futures) and adjusts its behavior accordingly. Crypto traders get 24/7 session tracking. Stock traders get proper market hours handling. Everyone gets institutional-grade analytics.

Anchor Period Options

The anchor period determines when VWAP resets and recalculates. You have three categories of options:

Time-Based Anchors:

Session - Resets at market open. Best for intraday stock trading where you want fresh VWAP each day.

Day - Resets at midnight UTC. Standard option for most traders.

Week / Month / Quarter / Year - Longer reset periods for swing traders and position traders who want broader context.

Rolling Window Anchors:

Rolling 5D - A sliding 5-day window that never resets. Solves the Monday problem where weekly VWAP equals daily VWAP on first day of week.

Rolling 21D - Approximately one month of trading data in continuous calculation. Excellent for crypto and forex markets that trade 24/7 without clear session breaks.

Event-Based Anchors:

Dividends - Resets on ex-dividend dates. Track institutional cost basis from dividend events.

Splits - Resets on stock split dates. Useful for analyzing post-split trading behavior.

Earnings - Resets on earnings report dates. See where volume-weighted trading occurred since last quarterly report.

Standard Deviation Bands

Three sets of bands surround the main VWAP line:

Band 1 (Aqua) - Plus and minus one standard deviation. Approximately 68% of price action occurs within this range under normal distribution. Touches suggest minor extension.

Band 2 (Fuchsia) - Plus and minus two standard deviations. Only 5% of trading should occur outside this range statistically. Touches here indicate significant overextension and high probability of mean reversion.

Band 3 (Purple) - Plus and minus three standard deviations. Touches are rare (0.3% probability) and represent extreme conditions. Often marks climax moves or panic selling/buying.

Each band can be toggled independently. Most traders show Band 1 by default and add Band 2 and 3 for specific setups or volatile instruments.

Multi-Timeframe VWAP System

The MTF section plots previous period VWAPs as horizontal support and resistance levels:

Daily VWAP - Previous day's final VWAP value. Key intraday reference level.

Weekly VWAP - Previous week's final VWAP. Important for swing traders.

Monthly VWAP - Previous month's final VWAP. Institutional benchmark level.

Quarterly VWAP - Previous quarter's final VWAP. Major support/resistance for position traders.

Previous Day VWAP - Yesterday's closing VWAP specifically, separate from current daily calculation.

The Confluence Zone percentage setting determines how close multiple VWAPs must be to trigger a confluence alert. When two or more timeframe VWAPs converge within this threshold, you get a high-probability support/resistance zone.

Session VWAPs for Global Markets

For forex, crypto, and futures traders who operate in 24/7 markets, the indicator tracks three major global sessions:

Asia Session - UTC 21:00 to 08:00. Gold colored line. Typically lower volatility, range-bound action that sets overnight levels.

London Session - UTC 08:00 to 17:00. Orange colored line. Often determines daily direction with high volume European participation.

New York Session - UTC 13:00 to 22:00. Blue colored line. Highest volume session globally. Sharp directional moves common.

Previous session VWAP values display as horizontal lines when each session closes, acting as intraday support and resistance. The table shows which sessions are currently active with checkmarks.

On-Chart Labels and Signals

The indicator plots several types of labels directly on price action when significant events occur:

Volume Spike Labels

Fire when current bar volume exceeds configurable thresholds relative to both the previous bar and the 20-bar average. Default settings require 300% of previous bar AND 200% of average volume. Green labels indicate bullish candles. Red labels indicate bearish candles. These spikes often mark institutional entry points.

Momentum Shift Labels

Appear when VWAP acceleration changes direction. The Slowing label warns when an active trend loses steam, often preceding reversal. The Accelerating label confirms trend continuation or potential bottom during downtrends. Filters available to show only reversal signals in existing trends.

VWAP Squeeze Labels

Detect when standard deviation bands contract relative to ATR (Average True Range). Low volatility compression often precedes explosive breakout moves. When the squeeze fires (releases), a label appears with directional prediction based on VWAP slope.

Divergence Labels

Mark price/volume divergences using CVD (Cumulative Volume Delta) analysis:

Bullish divergence: Price makes lower low, but CVD makes higher low. Hidden accumulation despite price weakness.

Bearish divergence: Price makes higher high, but CVD makes lower high. Hidden distribution despite price strength.

Dynamic VWAP Coloring

The main VWAP line changes color based on its slope direction:

Green - VWAP is rising. Institutional buying pressure. Volume-weighted price increasing.

Red - VWAP is falling. Institutional selling pressure. Volume-weighted price decreasing.

Gray - VWAP is flat. Consolidation or balance between buyers and sellers.

This coloring can be disabled for a static blue line if you prefer cleaner visuals. The VWAP label next to the line shows the current trend direction and delta percentage.

Calculated Projection Cone

One of the most powerful features is the Calculated Projection Cone. Unlike traditional extrapolation methods that simply extend a trend line forward, this system analyzes what actually happened in similar market conditions throughout the chart's history.

How It Works:

The system classifies each bar into one of 27 unique market states:

Z-Score Level - LOW (oversold), MID (fair value), or HIGH (overbought) based on configurable thresholds

Trend Direction - DOWN, FLAT, or UP based on VWAP slope

Volume Profile - LOW (below 80%), NORMAL (80-150%), or HIGH (above 150%) relative volume

When you look at the current bar, the indicator:

1. Identifies the current market state (e.g., LOW Z-Score + UP Trend + HIGH Volume)

2. Searches through all historical bars on the chart that had the same state

3. Calculates what happened in those bars X bars later (where X is your projection horizon)

4. Shows you the probability of up/down and the average move size

Visual Elements:

Probability Cone - Colored green (bullish probability above 55%), red (bearish below 45%), or gold (neutral). The cone width represents the historical range of outcomes (roughly the 20th to 80th percentile).

Center Line - Shows the average expected price based on historical outcomes in similar conditions.

Probability Label - Displays direction probability and average move. Example: "67% UP (+0.8%)" means 67% of similar past cases moved up, averaging 0.8% gain.

Fallback System:

When the exact 27-state match has insufficient historical data:

First fallback: Uses Z-Score plus Trend only (9 broader states, ignoring volume)

Second fallback: Uses Z-Score only (3 states)

When fallback is active, confidence automatically adjusts

Settings:

Projection Horizon - How many bars forward to analyze outcomes (5, 10, 15, or 20 bars, default 10)

Lookback Period - Historical data window in days (30-252, default 60)

Minimum Samples - Cases needed before using fallback (5-30, default 10)

Z-Score Threshold - Bucket boundary for LOW/MID/HIGH classification (1.0, 1.5, or 2.0 sigma)

Cloud Transparency - Adjust visibility (50-95%)

Colors - Customize bullish, bearish, and neutral cone colors

Confidence Levels:

HIGH - 30 or more similar historical cases found

MEDIUM - 15-29 similar cases

LOW - Fewer than 15 cases (more uncertainty)

IMPORTANT DISCLAIMER:

The Calculated Projection is based on past patterns only. It is NOT a price prediction or financial advice. Similar market states in the past do not guarantee similar outcomes in the future. The probability shown is historical frequency, not a guarantee. Always combine with other analysis and never rely solely on projections for trading decisions.

Alert Conditions

The indicator includes over 20 pre-built alert conditions:

Price vs VWAP:

Price crosses above VWAP

Price crosses below VWAP

Band Touches:

Price touches plus or minus one sigma band

Price touches plus or minus two sigma band (extreme)

Price touches plus or minus three sigma band (very extreme)

Z-Score Extremes:

Z-Score crosses above plus two (overbought extreme)

Z-Score crosses below minus two (oversold extreme)

Momentum and Trend:

Momentum slowing

Momentum accelerating

Trend turns bullish/bearish/neutral

Volume:

Volume spike detected

CVD Direction:

Buyers take control

Sellers take control

High Probability Signals:

Bullish reversal signal (oversold plus accelerating momentum)

Bearish reversal signal (overbought plus slowing momentum)

MTF and Special:

MTF confluence zone entry

VWAP squeeze fired

Bullish/Bearish divergence detected

Any significant signal (catch-all)

All signals use confirmed bar data to prevent false alerts from incomplete candles.

Settings Overview

Settings are organized into logical groups:

VWAP Settings

Anchor Period selection

Show/Hide VWAP line

Dynamic coloring toggle

VWAP label visibility

Bands Visibility

Toggle each of three bands independently

Info Table

Show/Hide table

Table position (9 options)

Text size

Volume spike label settings with adjustable thresholds

Momentum label settings with filters

Signal labels limited to 5 most recent (auto-managed)

Probability engine lookback period

Multi-Timeframe VWAP

Enable/Disable MTF system

Show MTF in table

Show MTF lines on chart

Individual timeframe toggles

Confluence zone threshold

Squeeze detection toggle

Session VWAPs

Enable/Disable session tracking

Apply to all assets option

Show session labels

Divergence Detection

Enable/Disable divergence

Pivot lookback period

Show divergence labels

Calculated Projection

Enable/Disable projection cone

Projection horizon (5, 10, 15, or 20 bars)

Lookback period in days (30-252)

Minimum samples threshold

Z-Score classification threshold (1.0, 1.5, or 2.0 sigma)

Cloud transparency adjustment

Bullish, bearish, and neutral colors

The Info Table - Your Trading Dashboard

The right side of your chart displays a compact table with up to twelve metrics.

Row-by-Row Breakdown:

Asset and Period - Shows what the indicator detected (US Stock, Crypto, Forex, etc.) and your selected anchor period. The detection happens automatically based on exchange data, so VWAP resets and calculations match your actual trading instrument.

Delta Percentage - How far current price sits from VWAP, expressed as a percentage. Positive means price trades above fair value. Negative means below. Large delta values (beyond 1-2%) often precede mean reversion moves. Day traders watch this for overextension.

Z-Score - Statistical deviation from VWAP measured in standard deviations. Unlike raw delta, Z-Score accounts for volatility. A 2% move in a volatile biotech stock differs from 2% in a stable utility. Z-Score normalizes this. Values beyond plus or minus two sigma occur only 5% of the time statistically.

Trend Direction - Whether VWAP itself is rising, falling, or flat. Rising VWAP means the volume-weighted average price is increasing, which indicates institutional accumulation. Falling VWAP suggests distribution. This differs from price trend since it weights by volume.

Momentum State - Is the trend accelerating or slowing down? This measures the rate of change in VWAP slope. When an uptrend shows slowing momentum, it often precedes reversal. Accelerating momentum in a downtrend can signal capitulation and potential bottom.

Relative Volume - Current bar volume compared to the 20-bar average, shown as percentage. Values above 150% indicate above-average activity. Spikes above 200-300% often mark institutional involvement. Low volume (below 80%) warns of potential fake moves.

MTF Bias - Four checkmarks or X marks showing whether price sits above or below Daily, Weekly, Monthly, and Quarterly VWAP. Four checkmarks means strong bullish alignment across all timeframes. Four X marks indicates bearish alignment. Mixed readings suggest consolidation or transition.

Band Probabilities - Historical statistics showing how often price touched each standard deviation band over your lookback period. This helps you understand if mean reversion or trend following works better for your specific instrument.

Session Status - Which global trading sessions are currently active (Asia, London, New York). Shows checkmarks for active sessions. Important for forex and crypto traders who need to know when major liquidity windows open and close.

Divergence State - Whether the indicator detects bullish or bearish divergence between price and cumulative volume delta. Bullish divergence occurs when price makes lower lows but buying pressure (CVD) makes higher lows, suggesting hidden accumulation.

Confidence Score - A weighted composite of all factors displayed as a progress bar and percentage. Combines MTF alignment, Z-Score, trend direction, volume delta, momentum, and relative volume into a single 0-100 score. Higher scores indicate stronger conviction setups.

Calculated Projection - When the Projection Cone is enabled, shows the historical probability of price direction and expected move. For example: "▲ 67% (+0.8%)" means in similar market states historically, price moved up 67% of the time with an average gain of 0.8%. The system analyzes 27 unique market states based on Z-Score, Trend, and Volume conditions.

Recommended Use Cases

Day Trading Stocks:

Use Session anchor with Band 1 visible. Watch for price returning to VWAP after morning move. Volume spikes near VWAP often mark institutional accumulation zones.

Swing Trading:

Use Weekly or Rolling 21D anchor. Enable MTF lines for Daily and Weekly levels. Trade pullbacks to these levels in direction of MTF bias.

Crypto and Forex:

Enable Session VWAPs. Use Rolling anchors to avoid artificial resets. Monitor session transitions for breakout opportunities.

Mean Reversion:

Focus on Z-Score reaching plus or minus two. Add Band 2 visibility. Combine with slowing momentum for highest probability reversals.

Trend Following:

Watch MTF bias alignment. Four checkmarks plus accelerating momentum plus high volume confirms trend continuation setups.

Projection Planning:

Enable the Calculated Projection to see what happened historically in similar market conditions. Use 5-10 bars for intraday setups, 15-20 bars for swing trade planning. Focus on high probability readings (above 60%) with HIGH confidence (30 or more samples). The cone shows the probable range of outcomes based on actual historical data. Combine with other factors like MTF alignment and volume for higher conviction setups.

Important Notes

The indicator does not repaint. MTF values use previous period's confirmed data.

Rolling VWAP works best on 15-minute timeframes and above due to bar lookback requirements.

Session VWAPs apply to global markets by default (forex, crypto, futures). Enable the all-assets option for stocks if desired.

Volume data for forex represents tick volume, not actual traded volume.

All alert conditions fire only on confirmed (closed) bars to prevent false signals.

The Calculated Projection updates each bar as market state changes. This is expected behavior. The projection shows probabilities based on similar past conditions, not a fixed prediction.

Q AND A

Q: Does this indicator repaint?

A: No. The main VWAP calculation uses standard TradingView VWAP methodology. Multi-timeframe values use previous period's confirmed data with appropriate lookahead settings. All alert signals require bar confirmation.

Q: Why does my Rolling VWAP look different on 1-minute versus 15-minute charts?

A: Rolling VWAP calculates across a fixed number of trading days. On very short timeframes, the bar lookback may hit TradingView limits. For best Rolling VWAP accuracy, use 15-minute or higher timeframes.

Q: Can I use this on any instrument?

A: Yes. The indicator automatically detects asset type and adjusts behavior. Stocks use standard market hours. Crypto uses 24/7 calculations. Forex uses tick volume. Everything adapts automatically.

Q: What does the Confidence Score actually measure?

A: The score combines six weighted factors: MTF alignment (25%), Z-Score position (20%), Trend direction (20%), CVD pressure (15%), Momentum state (10%), and Relative volume (10%). Higher scores indicate more factors aligned in one direction.

Q: Why are Session VWAPs not showing on my stock chart?

A: Session VWAPs apply to 24-hour markets by default (forex, crypto, futures). For stocks, enable the Use for All Assets option in Session VWAP settings.

Q: The Divergence labels appear delayed. Is this a bug?

A: Divergence detection requires pivot confirmation, which needs bars on both sides of the pivot point. The label appears at the actual pivot location (several bars back) once confirmed. This is intentional and prevents false signals.

Q: Can I change the band colors?

A: Yes. Each of the three bands has its own color input setting. You can customize Band 1, Band 2, and Band 3 colors to match your preferences. The defaults are Aqua, Fuchsia, and Purple. The main VWAP line color adapts dynamically based on slope direction or can be set to static blue.

Q: How do I set up alerts?

A: Right-click on the chart, select Add Alert, choose this indicator, and select your desired condition from the dropdown. All conditions include descriptive alert messages with relevant data.

Q: What is the Probability Engine lookback period?

A: This setting determines how many trading days the indicator analyzes to calculate band touch rates and mean reversion statistics. Default is 60 days (approximately 3 months). Longer periods provide more stable statistics but may miss recent behavior changes.

Q: Why do I see fewer labels than expected?

A: Signal labels (Volume, Momentum, Squeeze, Divergence) are limited to 5 most recent labels on the chart to keep it clean. When a new label appears, the oldest one is automatically removed. Additionally, momentum labels have several filters: check the slope multiplier setting (higher values require stronger trends) and the Only Reversal Signals option (when enabled, labels only appear for potential reversals, not trend confirmations).

Q: What is the Calculated Projection and how accurate is it?

A: The Calculated Projection analyzes what happened in past market conditions similar to the current state. It classifies each bar by Z-Score level, Trend direction, and Volume profile (27 unique states), then shows the historical probability of up vs down and the average move size. It is NOT a price prediction or guarantee. The probability shown is how often similar conditions led to up/down moves historically, not a future guarantee. Always use it as one input among many.

Q: Why does the Projection probability change?

A: The projection updates on each bar as market state changes. If Z-Score moves from LOW to MID, or trend shifts from UP to FLAT, the system looks up a different historical category. This is expected behavior. The projection shows what happened in similar past conditions to the current bar's state.

Q: The Projection shows LOW confidence. What does that mean?

A: Confidence levels indicate sample size: HIGH means 30 or more historical cases found, MEDIUM means 15-29 cases, LOW means fewer than 15 cases. When sample size is low, the system uses a fallback: first aggregating by Z-Score plus Trend only (ignoring volume), then by Z-Score only. LOW confidence means less statistical reliability, so weight other factors more heavily in your decision.

Q: Why does the cone sometimes show 50/50 probability?

A: A 50/50 reading means that in similar past market states, price moved up roughly half the time and down half the time. This indicates a neutral or balanced condition where historical patterns provide no directional edge. Consider waiting for a higher probability setup or using other analysis methods.

CREDITS AND ACKNOWLEDGMENTS

Methodology Foundation:

VWAP (Volume Weighted Average Price) - Standard institutional benchmark calculation, widely used since the 1980s for algorithmic execution and fair value assessment

Standard Deviation Bands - Statistical volatility measurement applying normal distribution principles to price deviation from mean

Z-Score Analysis - Classic statistical normalization technique for comparing values across different volatility regimes

Cumulative Volume Delta (CVD) - Order flow analysis concept measuring aggressive buying versus selling pressure

Concept Integration:

Mean reversion probability engine - Custom historical statistics tracking for band touch rates

Momentum acceleration detection - Second derivative analysis of VWAP slope changes

VWAP Squeeze - Volatility compression concept adapted from TTM Squeeze methodology applied to VWAP bands versus ATR

Confidence scoring system - Weighted composite scoring combining multiple technical factors

Calculated Projection Cone - Probability-based projection using 27-state market classification (Z-Score, Trend, Volume) with historical outcome analysis and weighted fallback system

All calculations use standard public domain formulas and TradingView built-in functions. No proprietary third-party code was used.

For questions, feedback, or feature requests, please comment below or send a private message.

Happy Trading!

Bollinger Bands Mean Reversion using RSI [Krishna Peri]How it Works

Long entries trigger when:

- RSI reaches oversold levels, and

- At least one bullish candle closes inside the lower Bollinger Band

Short entries trigger when:

- RSI reaches overbought levels, and

- At least one bearish candle closes inside the upper Bollinger Band

This approach aims to capture exhaustion moves where price pushes into extreme deviation from its mean and then snaps back toward the middle band.

Important Disclaimer

This is a mean-reversion strategy, which means it performs best in sideways, ranging, or slowly oscillating market conditions. When markets shift into strong trends, Bollinger Bands expand and volatility increases, which may cause some signals to become inaccurate or fail altogether.

For best results, combine this script with:

- Price action

- Market structure

- Higher-timeframe trend context

- Previous day/week/month highs & lows

- Untested liquidity levels or imbalance zones

- Session timing (Asia, London, NY)

Using these confluences helps filter out low-probability trades and significantly improves consistency and precision.

Stochastic Hash Strat [Hash Capital Research]# Stochastic Hash Strategy by Hash Capital Research

## 🎯 What Is This Strategy?

The **Stochastic Slow Strategy** is a momentum-based trading system that identifies oversold and overbought market conditions to capture mean-reversion opportunities. Think of it as a "buy low, sell high" approach with smart mathematical filters that remove emotion from your trading decisions.

Unlike fast-moving indicators that generate excessive noise, this strategy uses **smoothed stochastic oscillators** to identify only the highest-probability setups when momentum truly shifts.

---

## 💡 Why This Strategy Works

Most traders fail because they:

- **Chase prices** after big moves (buying high, selling low)

- **Overtrade** in choppy, directionless markets

- **Exit too early** or hold losses too long

This strategy solves all three problems:

1. **Entry Discipline**: Only trades when the stochastic oscillator crosses in extreme zones (oversold for longs, overbought for shorts)

2. **Cooldown Filter**: Prevents revenge trading by forcing a waiting period after each trade

3. **Fixed Risk/Reward**: Pre-defined stop-loss and take-profit levels ensure consistent risk management

**The Math Behind It**: The stochastic oscillator measures where the current price sits relative to its recent high-low range. When it's below 25, the market is oversold (time to buy). When above 70, it's overbought (time to sell). The crossover with its moving average confirms momentum is shifting.

---

## 📊 Best Markets & Timeframes

### ⭐ OPTIMAL PERFORMANCE:

**Crude Oil (WTI) - 12H Timeframe**

- **Why it works**: Oil markets have predictable volatility patterns and respect technical levels

**AAVE/USD - 4H to 12H Timeframe**

- **Why it works**: DeFi tokens exhibit strong momentum cycles with clear extremes

### ✅ Also Works Well On:

- **BTC/USD** (12H, Daily) - Lower frequency but high win rate

- **ETH/USD** (8H, 12H) - Balanced volatility and liquidity

- **Gold (XAU/USD)** (Daily) - Classic mean-reversion asset

- **EUR/USD** (4H, 8H) - Lower volatility, requires patience

### ❌ Avoid Using On:

- Timeframes below 4H (too much noise)

- Low-liquidity altcoins (wide spreads kill performance)

- Strongly trending markets without pullbacks (Bitcoin in 2021)

- News-driven instruments during major events

---

## 🎛️ Understanding The Settings

### Core Stochastic Parameters

**Stochastic Length (Default: 16)**

- Controls the lookback period for price comparison

- Lower = faster reactions, more signals (10-14 for volatile markets)

- Higher = smoother signals, fewer trades (16-21 for stable markets)

- **Pro tip**: Use 10 for crypto 4H, 16 for commodities 12H

**Overbought Level (Default: 70)**

- Threshold for short entries

- Lower values (65-70) = more trades, earlier entries

- Higher values (75-80) = fewer but higher-conviction trades

- **Sweet spot**: 70 works for most assets

**Oversold Level (Default: 25)**

- Threshold for long entries

- Higher values (25-30) = more trades, earlier entries

- Lower values (15-20) = fewer but stronger bounce setups

- **Sweet spot**: 20-25 depending on market conditions

**Smooth K & Smooth D (Default: 7 & 3)**

- Additional smoothing to filter out whipsaws

- K=7 makes the indicator slower and more reliable

- D=3 is the signal line that confirms the trend

- **Don't change these unless you know what you're doing**

---

### Risk Management

**Stop Loss % (Default: 2.2%)**

- Automatically exits losing trades

- Should be 1.5x to 2x your average market volatility

- Too tight = death by a thousand cuts

- Too wide = uncontrolled losses

- **Calibration**: Check ATR indicator and set SL slightly above it

**Take Profit % (Default: 7%)**

- Automatically exits winning trades

- Should be 2.5x to 3x your stop loss (reward-to-risk ratio)

- This default gives 7% / 2.2% = 3.18:1 R:R

- **The golden rule**: Never have R:R below 2:1

---

### Trade Filters

**Bar Cooldown Filter (Default: ON, 3 bars)**

- **What it does**: Forces you to wait X bars after closing a trade before entering a new one

- **Why it matters**: Prevents emotional revenge trading and overtrading in choppy markets

- **Settings guide**:

- 3 bars = Standard (good for most cases)

- 5-7 bars = Conservative (oil, slow-moving assets)

- 1-2 bars = Aggressive (only for experienced traders)

**Exit on Opposite Extreme (Default: ON)**

- Closes your long when stochastic hits overbought (and vice versa)

- Acts as an early profit-taking mechanism

- **Leave this ON** unless you're testing other exit strategies

**Divergence Filter (Default: OFF)**

- Looks for price/momentum divergences for additional confirmation

- **When to enable**: Trending markets where you want fewer but higher-quality trades

- **Keep OFF for**: Mean-reverting markets (oil, forex, most of the time)

---

## 🚀 Quick Start Guide

### Step 1: Set Up in TradingView

1. Open TradingView and navigate to your chart

2. Click "Pine Editor" at the bottom

3. Copy and paste the strategy code

4. Click "Add to Chart"

5. The strategy will appear in a separate pane below your price chart

### Step 2: Choose Your Market

**If you're trading Crude Oil:**

- Timeframe: 12H

- Keep all default settings

- Watch for signals during London/NY overlap (8am-11am EST)

**If you're trading AAVE or crypto:**

- Timeframe: 4H or 12H

- Consider these adjustments:

- Stochastic Length: 10-14 (faster)

- Oversold: 20 (more aggressive)

- Take Profit: 8-10% (higher targets)

### Step 3: Wait for Your First Signal

**LONG Entry** (Green circle appears):

- Stochastic crosses up below oversold level (25)

- Price likely near recent lows

- System places limit order at take profit and stop loss

**SHORT Entry** (Red circle appears):

- Stochastic crosses down above overbought level (70)

- Price likely near recent highs

- System places limit order at take profit and stop loss

**EXIT** (Orange circle):

- Position closes either at stop, target, or opposite extreme

- Cooldown period begins

### Step 4: Let It Run

The biggest mistake? **Interfering with the system.**

- Don't close trades early because you're scared

- Don't skip signals because you "have a feeling"

- Don't increase position size after a big win

- Don't revenge trade after a loss

**Follow the system or don't use it at all.**

---

### Important Risks:

1. **Drawdown Pain**: You WILL experience losing streaks of 5-7 trades. This is mathematically normal.

2. **Whipsaw Markets**: Choppy, range-bound conditions can trigger multiple small losses.

3. **Gap Risk**: Overnight gaps can cause your actual fill to be worse than the stop loss.

4. **Slippage**: Real execution prices differ from backtested prices (factor in 0.1-0.2% slippage).

---

## 🔧 Optimization Guide

### When to Adjust Settings:

**Market Volatility Increased?**

- Widen stop loss by 0.5-1%

- Increase take profit proportionally

- Consider increasing cooldown to 5-7 bars

**Getting Too Few Signals?**

- Decrease stochastic length to 10-12

- Increase oversold to 30, decrease overbought to 65

- Reduce cooldown to 2 bars

**Getting Too Many Losses?**

- Increase stochastic length to 18-21 (slower, smoother)

- Enable divergence filter

- Increase cooldown to 5+ bars

- Verify you're on the right timeframe

### A/B Testing Method:

1. **Run default settings for 50 trades** on your chosen market

2. Document: Win rate, profit factor, max drawdown, emotional tolerance

3. **Change ONE variable** (e.g., oversold from 25 to 20)

4. Run another 50 trades

5. Compare results

6. Keep the better version

**Never change multiple settings at once** or you won't know what worked.

---

## 📚 Educational Resources

### Key Concepts to Learn:

**Stochastic Oscillator**

- Developed by George Lane in the 1950s

- Measures momentum by comparing closing price to price range

- Formula: %K = (Close - Low) / (High - Low) × 100

- Similar to RSI but more sensitive to price movements

**Mean Reversion vs. Trend Following**

- This is a **mean reversion** strategy (price returns to average)

- Works best in ranging markets with defined support/resistance

- Fails in strong trending markets (2017 Bitcoin, 2020 Tech stocks)

- Complement with trend filters for better results

**Risk:Reward Ratio**

- The cornerstone of profitable trading

- Winning 40% of trades with 3:1 R:R = profitable

- Winning 60% of trades with 1:1 R:R = breakeven (after fees)

- **This strategy aims for 45% win rate with 2.5-3:1 R:R**

### Recommended Reading:

- *"Trading Systems and Methods"* by Perry Kaufman (Chapter on Oscillators)

- *"Mean Reversion Trading Systems"* by Howard Bandy

- *"The New Trading for a Living"* by Dr. Alexander Elder

---

## 🛠️ Troubleshooting

### "I'm not seeing any signals!"

**Check:**

- Is your timeframe 4H or higher?

- Is the stochastic actually reaching extreme levels (check if your asset is stuck in middle range)?

- Is cooldown still active from a previous trade?

- Are you on a low-liquidity pair?

**Solution**: Switch to a more volatile asset or lower the overbought/oversold thresholds.

---

### "The strategy keeps losing money!"

**Check:**

- What's your win rate? (Below 35% is concerning)

- What's your profit factor? (Below 0.8 means serious issues)

- Are you trading during major news events?

- Is the market in a strong trend?

**Solution**:

1. Verify you're using recommended markets/timeframes

2. Increase cooldown period to avoid choppy markets

3. Reduce position size to 5% while you diagnose

4. Consider switching to daily timeframe for less noise

---

### "My stop losses keep getting hit!"

**Check:**

- Is your stop loss tighter than the average ATR?

- Are you trading during high-volatility sessions?

- Is slippage eating into your buffer?

**Solution**:

1. Calculate the 14-period ATR

2. Set stop loss to 1.5x the ATR value

3. Avoid trading right after market open or major news

4. Factor in 0.2% slippage for crypto, 0.1% for oil

---

## 💪 Pro Tips from the Trenches

### Psychological Discipline

**The Three Deadly Sins:**

1. **Skipping signals** - "This one doesn't feel right"

2. **Early exits** - "I'll just take profit here to be safe"

3. **Revenge trading** - "I need to make back that loss NOW"

**The Solution:** Treat your strategy like a business system. Would McDonald's skip making fries because the cashier "doesn't feel like it today"? No. Systems work because of consistency.

---

### Position Management

**Scaling In/Out** (Advanced)

- Enter 50% position at signal

- Add 50% if stochastic reaches 10 (oversold) or 90 (overbought)

- Exit 50% at 1.5x take profit, let the rest run

**This is NOT for beginners.** Master the basic system first.

---

### Market Awareness

**Oil Traders:**

- OPEC meetings = volatility spikes (avoid or widen stops)

- US inventory reports (Wed 10:30am EST) = avoid trading 2 hours before/after

- Summer driving season = different patterns than winter

**Crypto Traders:**

- Monday-Tuesday = typically lower volatility (fewer signals)

- Thursday-Sunday = higher volatility (more signals)

- Avoid trading during exchange maintenance windows

---

## ⚖️ Legal Disclaimer

This trading strategy is provided for **educational purposes only**.

- Past performance does not guarantee future results

- Trading involves substantial risk of loss

- Only trade with capital you can afford to lose

- No one associated with this strategy is a licensed financial advisor

- You are solely responsible for your trading decisions

**By using this strategy, you acknowledge that you understand and accept these risks.**

---

## 🙏 Acknowledgments

Strategy development inspired by:

- George Lane's original Stochastic Oscillator work

- Modern quantitative trading research

- Community feedback from hundreds of backtests

Built with ❤️ for retail traders who want systematic, disciplined approaches to the markets.

---

**Good luck, stay disciplined, and trade the system, not your emotions.**

Order-Flow Proxy (VWAP Deviation Zones)Order-Flow Proxy (VWAP Deviation Zones) helps traders visualize when market price moves unusually far away from its Volume-Weighted Average Price (VWAP) — a key fair-value level used by institutional participants.

When price stretches too far above or below VWAP, it often signals temporary imbalance between buying and selling pressure.

This tool highlights those moments using simple color zones and an optional statistical Z-Score filter for deeper precision.

In short: it’s a clean, minimal mean-reversion indicator showing when price is statistically “too far” from fair value.

Red zone → Price extended above VWAP → possible buyer exhaustion or short setup.

Green zone → Price extended below VWAP → possible seller exhaustion or long setup.

VWAP line → Acts as a dynamic fair-value anchor.

Concept:

VWAP combines both price and traded volume to define where most transactions occurred.

Deviations from it — measured either by a fixed distance (1%) or by Z-Score — can reveal overvaluation or undervaluation zones used by professional traders for contrarian setups.

How to use:

Apply the indicator to any intraday chart (1m–1h recommended).

Watch for background color shifts — red or green.

Optionally enable the Z-Score filter to focus only on statistically extreme deviations.

Combine with volume spikes, liquidity sweeps, or your own order-flow tools for confirmation.

Tip:

Best used as a visual overlay for detecting stretched markets and potential reversals.

VWAP Entry Assistant (v1.0)Description:

Anchored VWAP with a lightweight assistant for VWAP reversion trades.

It shows the distance to VWAP, an estimated hit probability for the current bar, the expected number of bars to reach VWAP, and a recommended entry price.

If the chance of touching VWAP is low, the script suggests an adjusted limit using a fraction of ATR.

The VWAP line is white by default, and a compact summary table appears at the bottom-left.

Educational tool. Not financial advice. Not affiliated with TradingView or any exchange. Always backtest before use.

Volume Delta [BigBeluga]🔵 OVERVIEW

The Volume Delta indicator visualizes the dominance between buying and selling volume within a given period. It calculates the percentage of bullish (buy) versus bearish (sell) volume, then color-codes the candles and provides a real-time dashboard comparing delta values across multiple currency pairs. This makes it a powerful tool for monitoring order-flow strength and intermarket relationships in real time.

🔵 CONCEPTS

Each bar’s buy volume is counted when the close is higher than the open.

Each bar’s sell volume is counted when the close is lower than the open.

volumeBuy = 0.

volumeSell = 0.

for i = 0 to period

if close > open

volumeBuy += volume

else

volumeSell += volume

The indicator sums both over a chosen period to calculate the ratio of buy-to-sell pressure.

Delta (%) = (Buy Volume ÷ (Buy Volume + Sell Volume)) × 100.

Gradient colors highlight whether buying or selling pressure dominates.

🔵 FEATURES

Calculates real-time Volume Delta for the selected chart or for multiple assets.

Colors candles dynamically based on the delta intensity (green = buy pressure, red = sell pressure).

Displays a dashboard table showing volume delta % for up to five instruments.

The dashboard features visual progress bars for quick intermarket comparison.

An optional Delta Bar Panel shows the ratio of Buy/Sell volumes near the latest bar.

A floating label shows the exact Buy/Sell percentages.

Works across all symbols and timeframes for multi-asset delta tracking.

🔵 HOW TO USE

When Buy % > Sell % , it often signals bullish momentum or strong accumulation—but can also indicate over-excitement and a possible market top.

Market Tops

When Sell % > Buy % , it typically reflects bearish pressure or distribution—but may also occur near a market bottom where selling exhaustion forms.

Market Bottom

Use the Dashboard to compare volume flow across correlated assets (e.g., major Forex pairs or sector groups).

Combine readings with trend or volatility filters to confirm whether the imbalance aligns with broader directional conviction.

Treat the Delta Bar visualization as a real-time sentiment gauge—showing which side (buyers or sellers) dominates the current session.

🔵 CONCLUSION

Volume Delta transforms volume analysis into an intuitive directional signal.

By quantifying buy/sell pressure and displaying it as a percentage or color gradient, it provides traders with a clearer picture of real-time volume imbalance — whether within one market or across multiple correlated instruments.

20 MA ReversionA mean reversion tactic with the 20 SMA:

the indicator is chcking specific parameters, such as the volume related to the last day's volume, distance from 20 SMA, CCI values and changes, trends, and recent gaps that will act as a magnet.

enjoy!

Monthly VWAPDescription

This indicator identifies potential mean reversion opportunities by tracking price deviations from monthly VWAP with dynamic volatility-adjusted thresholds.

Core Logic:

The indicator monitors when price moves significantly away from monthly VWAP and looks for potential reversal opportunities. It uses ATR-based dynamic thresholds that adapt to current market volatility, combined with volume confirmation to filter out weak signals.

Key Features:

Adaptive Thresholds: ATR-based bands that adjust to market volatility

Volume Confirmation: Requires average volume spike to validate signals

Monthly Reset: VWAP anchors reset each month for fresh reference levels

Visual Clarity: Color-coded deviation line with background highlights for active signals

Info Panel: Shows days from anchor and current price context vs fair value

Signal Generation:

Buy Signal: Price below monthly VWAP by threshold amount with elevated volume

Sell Signal: Price above monthly VWAP by threshold amount with elevated volume

Neutral: Price within threshold range or insufficient volume

Best Used For:

Mean reversion strategies in ranging markets

Identifying potential oversold/overbought conditions

Understanding price position relative to monthly fair value

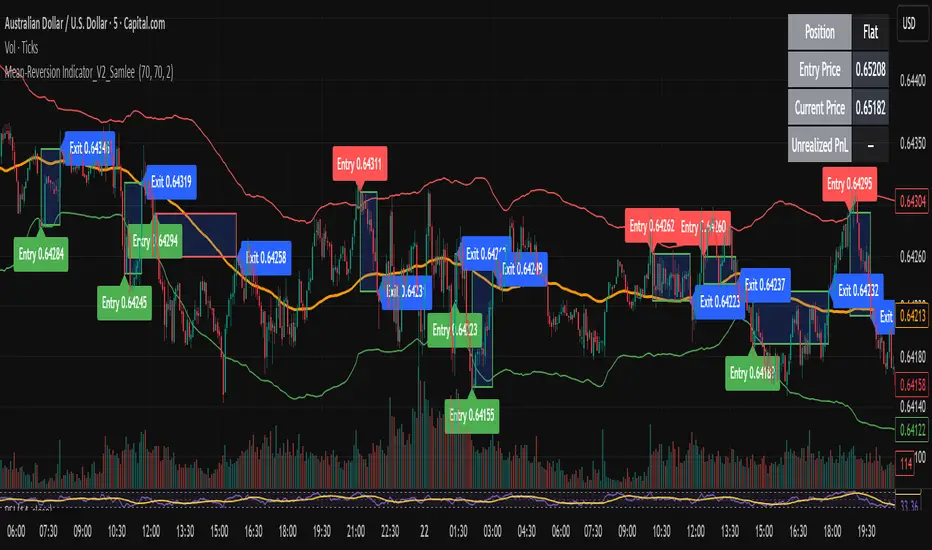

Mean-Reversion Indicator_V2_SamleeOverview

This is the second version of my mean reversion indicator. It combines a moving average with adaptive standard deviation bands to detect when the price deviates significantly from its mean. The script provides automatic entry/exit signals, real-time PnL tracking, and shaded trade zones to make mean reversion trading more intuitive.

Core Logic

Mean benchmark: Simple Moving Average (MA).

Volatility bands: Standard deviation of the spread (close − MA) defines upper and lower bands.

Trading rules:

Price breaks below the lower band → Enter Long

Price breaks above the upper band → Enter Short

Price reverts to MA → Exit position

What’s different vs. classic Bollinger/Keltner

Bandwidth is based on the standard deviation of the price–MA spread, not raw closing prices.

Entry signals use previous-bar confirmation to reduce intrabar noise.

Exit rule is a mean-touch condition, rather than fixed profit/loss targets.

Enhanced visualization:

A shaded box dynamically shows the distance between entry and current/exit price, making it easy to see profit/loss zones over the holding period.

Instant PnL labels display current position side (Long/Short/Flat) and live profit/loss in both pips and %.

Entry and exit points are clearly marked on the chart with labels and exact prices.

These visualization tools go beyond what most indicators provide, giving traders a clearer, more practical view of trade evolution.

Key Features

Automatic detection of position status (Long / Short / Flat).

Chart labels for entries (“Entry”) and exits (“Exit”).

Real-time floating PnL calculation in both pips and %.

Info panel (top-right) showing entry price, current price, position side, and PnL.

Dynamic shading between entry and current/exit price to visualize profit/loss zones.

Usage Notes & Risk

Mean reversion may underperform in strong trending markets; parameters (len_ma, len_std, mult) should be validated per instrument and timeframe.

Works best on relatively stable, mean-reverting pairs (e.g., AUDNZD).

Risk management is essential: use independent stop-loss rules (e.g., limit risk to 1–2% of equity per trade).

This script is provided for educational purposes only and is not financial advice.

Mean Reversion & Momentum Hybrid | D_QUANT 📌 Mean Reversion & Momentum Hybrid | D_QUANT

📖 Description:

This indicator combines mean reversion logic, volatility filtering, and percentile-based momentum to deliver clear, context-aware buy/sell signals designed for trend-following and contrarian setups.

At its core, it merges:

A Bollinger Band % Positioning Model (BB%)

A 75th/25th Percentile Momentum System

A Volatility-Adjusted Trend Filter using RMA + ATR

All tied together with a dynamic gradient-style oscillator that visualizes signal strength and persistence over time — making it easy to track high-conviction setups.

Signals only trigger when all three core components align, filtering out noise and emphasizing high-probability turning points or trend continuations.

⚙️ Methodology Overview:

Bollinger Bands % (BB%):

Price is measured as a percentage between upper and lower Bollinger Bands (based on OHLC4). Entries are only considered when price exceeds custom BB% thresholds — emphasizing market extremes.

Volatility-Based Trend Filter (RMA + ATR):

A smoothed RMA baseline is paired with ATR to define trend bias. This ensures signals only occur when price deviates meaningfully beyond recent volatility.

Percentile Momentum Model (75th/25th Rank):

Price is compared against its rolling 75th and 25th percentile. If price breaks these statistical boundaries (adjusted by ATR), it triggers a directional momentum condition.

Signal Consensus Engine:

All three layers must agree — BB% condition, trend filter, and percentile momentum — before a buy or sell signal is plotted.

Gradient Oscillator Visualization:

Signals appear as a fading oscillator line with a gradient-filled area beneath it. The color intensity represents how “fresh” or “strong” the signal is, fading over time if not reconfirmed, offering both clarity and signal aging at a glance.

🔧 User Inputs:

🧠 Core Settings:

Source: Select the price input (default: close)

Bollinger Bands Length: Period for BB basis and deviation

Bollinger Bands Multiplier: Width of the bands

Minimum BB Width (% of Price): Prevents signals during low-volatility chop

📊 BB% Thresholds:

BB% Long Threshold (L): Minimum %B to consider a long

BB% Short Threshold (S): Maximum %B to consider a short

🔍 Trend Filter Parameters:

RMA Length: Period for the smoothed trend baseline

ATR Length: Lookback for ATR in trend deviation filter

⚡️ Momentum Parameters:

Momentum Length: Period for percentile momentum calculation

Mult_75 / Mult_25: ATR-adjusted thresholds for breakout above/below percentile levels

🎨 Visualization:

Bar Coloring: Highlights candles during active signals

Background Coloring: Optional background shading for signals

Show Oscillator Plot: Toggle the gradient-style oscillator

🧪 Use Case:

This indicator works well across all assets for trend identification. It is particularly effective when used on higher timeframes (e.g. 12H, 1D,2D) to capture mean reversion bounces or confirm breakouts backed by percentile momentum and volatility expansion.

⚠️ Notes:

This is not financial advice. Use in combination with proper risk management and confluence from other tools.

Institutional MACD (Z-Score Edition) [VolumeVigilante]📈 Institutional MACD (Z-Score Edition) — Professional-Grade Momentum Signal

This is not your average MACD .

The Institutional MACD (Z-Score Edition) is a statistically enhanced momentum tool, purpose-built for serious traders and breakout hunters . By applying Z-Score normalization to the classic MACD structure, this indicator uncovers statistically significant momentum shifts , enabling cleaner reads on price extremes, trend continuation, and potential reversals.

💡 Why It Matters

The classic MACD is powerful — but raw momentum values can be noisy and relative , especially on volatile assets like BTC/USD . By transforming the MACD line, signal line, and histogram into Z-scores , we anchor these signals in statistical context . This makes the Institutional MACD:

✔️ Timeframe-agnostic and asset-normalized

✔️ Ideal for spotting true breakouts , not false flags

✔️ A reliable tool for detecting momentum divergence and exhaustion

🧪 Key Features

✅ Full Z-Score normalization (MACD, Signal, Histogram)

✅ Highlighted ±Z threshold bands for overbought/oversold zones

✅ Customizable histogram coloring for visual momentum shifts

✅ Built-in alerts for zero-crosses and Z-threshold breaks

✅ Clean overlay with optional display toggles

🔁 Strategy Tip: Mean Reversion Signals with Statistical Confidence

This indicator isn't just for spotting breakouts — it also shines as a mean reversion tool , thanks to its Z-Score normalization .

When the Z-Score histogram crosses beyond ±2, it marks a statistically significant deviation from the mean — often signaling that momentum is overstretched and the asset may be due for a pullback or reversal .

📌 How to use it:

Z > +2 → Price action is in overbought territory. Watch for exhaustion or short setups.

Z < -2 → Momentum is deeply oversold. Look for reversal confirmation or long opportunities.

These zones often precede snap-back moves , especially in range-bound or corrective markets .

🎯 Combine Z-Score extremes with:

Candlestick confirmation

Support/resistance zones

Volume or price divergence

Other mean reversion tools (e.g., RSI, Bollinger Bands)

Unlike the raw MACD, this version delivers statistical thresholds , not guesswork — helping traders make decisions rooted in probability, not emotion.

📢 Trade Smart. Trade Vigilantly.

Published by VolumeVigilante

Consecutive Bearish Candle Strategy█ STRATEGY DESCRIPTION

The "Consecutive Bearish Candle Strategy" is a momentum-based strategy designed to identify potential reversals after a sustained bearish move. It enters a long position when a specific number of consecutive bearish candles occur and exits when the price shows strength by exceeding the previous bar's high. This strategy is optimized for use on various timeframes and instruments.

█ SIGNAL GENERATION

1. LONG ENTRY

A Buy Signal is triggered when:

The close price has been lower than the previous close for at least `Lookback` consecutive bars. This indicates a sustained bearish move, suggesting a potential reversal.

The signal occurs within the specified time window (between `Start Time` and `End Time`).

2. EXIT CONDITION

A Sell Signal is generated when the current closing price exceeds the high of the previous bar (`close > high `). This indicates that the price has shown strength, potentially confirming the reversal and prompting the strategy to exit the position.

█ ADDITIONAL SETTINGS

Lookback: The number of consecutive bearish bars required to trigger a Buy Signal. Default is 3.

Start Time and End Time: The time window during which the strategy is allowed to execute trades.

█ PERFORMANCE OVERVIEW

This strategy is designed for markets with frequent momentum shifts.

It performs best in volatile conditions where price movements are significant.