TriautoETF(TQQQ) Short Strategy B1○ Objective.

This is a strategy for the TQQQ NASDAQ:TQQQ short strategy in the TriAuto ETF .

It is used as a hedging short rather than for profit-making purposes.

Entry and close points are indicated.

○ Strategy

The strategy is to hold a short position when the price falls below the moving average line, which is a market-conscious line that is rarely broken.

The close (settlement) is determined by using the moving average.

The moving average is based on the market-conscious QQQ NASDAQ:QQQ .

This script is used on the daily chart of the TQQQ.

It works as a hedge for long positions because open interest is held even at the major bottoms of the China and Corona shocks.

The system is set up to quickly cut its losses even if the moving average is "tricked" into falling below the moving average.

"上证综指etf"に関するスクリプトを検索

Morningstar Equity Style Box HeatmapStyle boxes are a classification scheme created by Morningstar. They visually provide a graphical representation of investing categories for equity investments. A style box is a valuable tool for investors to use when determining asset allocation.

There are 9 categories:

Large Value, Large Blend, Large Growth

Medium Value, Medium Blend, Medium Growth

Small Value, Small Blend, Small Growth

The strength of the 9 categories are found by using 9 Vanguard ETF's that follow the respective CRSP index of their category.

Donchian Screener█ OVERVIEW

This is a screener script for the Donchian Channel indicator . It's an excellent indicator for trend following, a trading strategy which tries to take advantage of long, medium or short-term moves that seem to play out in various markets.

█ DESCRIPTION

The screener works by scanning through up to 10 symbols and list down symbols that are currently breaking through the upper or lower band as definied by the Donchian Channels, at which point the market signals the start of a bullish or bearish trend.

█ HOW TO USE

After adding the indicator, open the script settings and type the symbol name and length to be used on the Donchian Channels for each stock.

█ PARAMETERS

- Use High/Low Price Breakouts: check this box if you want to use price high/low instead of price close to identify breakouts

- Panel Position: choose whether you want to position the panel on the top, middle or bottom right side of the graph (default is top)

- Default Timeframe: what timeframe to use on the screener (default is daily)

- Ticker: the ticker name you want to monitor

- Length: length parameter used on Donchian Channel indicator

█ FEATURES

The screener can scan up to 10 symbols each time.

█ LIMITATIONS

The screener will scan the symbols breaking out bands on the current bar, and as such, there maybe some delays depending on the stock/ etf /crypto you choose. Some exchanges require an additional subscription to get realtime data.

Linear Regression Relative Strength[image/x/iZvwDWEY/

Relative Strength indicator comparing the current symbol to SPY (or any other benchmark). It may help to pick the right assets to complement the portfolio build around core ETFs such as SPY.

The general idea is to show if the current symbol outperforms or underperforms the benchmark (SPY by default) when bought some certain time ago. Relative performance is displayed as percent and is calculated for three different time ranges - short (1 mo by default), mid (1 quarter), and long (half a year). To smooth the volatility, the script uses linear regression to estimate the trend and takes the start and the end points of the linear regression line to compute the relative strength.

It is important to remember that the script shows the gain relative to SPY (or other selected benchmark), not the asset's gain. Therefore, it may indicate that the asset is profitable, but it still may lose value if SPY is in downtrend.

Therefore, it is crucial to check other indicators before making a decision. In the example above, standard linear regression for one quarter is used to indicate the direction of the trend.

Market DirectionThis script uses the ETF "VTI" to track the trend of the market

It requires 2 consecutive 5 day periods up or down to verify the direction otherwise the trend is neutral

It also uses a BB%B calculation to determine over bought and over sold conditions.

It will display numbers for 10 days ago, 5 days ago, downtrend today and uptrend today and finally the %B

Feel free to use or modify and offer suggestions for improvements

Cumulative RSI StrategyI suppose nothing drives a point home like a 10+ year backtest! A couple of weeks ago I published a custom indicator called the Cumulative RSI. This indicator was straight out of chapter 9 of "Short Term Trading Strategies That Work." Today I am publishing a basic sample strategy in that uses the Cumulative RSI as its only entry and exit signals on a Nasdaq 100 leveraged index ETF (TQQQ). In this example, the indicator is being used as a longer term strategy with just 10% leverage over the account equity and a $25k start balance.

If I had it 10 years ago I would probably be retired! I'm sharing because I've found that it can provide an edge when determining exit/take profit points for trades. Many traders wait for a price reversal / trailing-stop to exit a trade when it starts losing. I've found that, using tools like the Cumulative RSI, you can achieve better exit points over the long term. Disclaimer: Even though this example significantly beats buy and hold, I wouldn't advise using it as a stand-alone strategy without significant additions/modifications to strategy and risk management functions.

No gaps candlesThis indicator repaints the candles so that every candle's open price is the previous candle's close price. This helps visualize stocks and ETFs that have big gaps, usually between trading days.

You should hide visibility of the ticker for this to be displayed properly.

Long/Short Volatility AlgoA modification of my leveraged ETF algorithm. Giving out for free because it's a sloppy algorithm, and I personally use a much more refined algorithm developed by someone much smarter than me.

McClellan Oscillator StrategyBuy and sell programs when 5 day EMA goes above and below zero, respectively.

Useful for LEVERAGED ETF trading such as SPXL, TECL, FNGU, etc. Not so much for general portfolio holdings.

RSI of MACD Strategy [Long only]This strategy uses the RSI on MACD indicator.

BUY

====

When RSI indicator crossing over 30 or 35 line and price above slow ema

Note: when the position already taken, you may reenter on the purple candle

Partial Exit

==========

Partial profit taking option is available in settings. If this is selected , 1/3 position exited when RSI indicator crossing down 80 line

Close

=====

When RSI indicator crossing below 15

Stop Loss

=========

I havent used hard stop loss in this strategy. Reason is , when price going down , indicator may go up ... so just wanted to ride along with indicator ...

Stop loss mentioned in the settings is used in calculation of how many units can be be purchased based on risk level

Tested with SPY and QQQ ETFs on hourly chart

Warning

=========

For the eductional purposes only ...

This is not a financial advise. please do your own research before taking any trading decission

Volatility Bands Reversal Strategy [Long Only]This strategy based on existng indicator available on TV

If finds the reversals for LONG entries ... I have modified the settings to back test it ...

BUY

====

When the price touches lower band , and tries to close above lower band

some signals are mixed up, you can research and look for a confirmation ...

if the middle band is above EMA50 , you can simply follow the strategy BUY signal

but if the middle band is EMA50 , wait for the price to close above middle band

Sell / Close

==========

wait for the sell signa OR close when price touches the upper band

How do you want to close , you can chose in settings. Chnage these values and see the performance

Please note , sell means just closing the existing LONG position , not short selling

Stop Loss

=========

Stop Loss is defaulted to 6%

This is tested in 1HR, 2HR and 4 HRs chart for SPY and QQQ ETFS ...

for long term investing style , 4 Hrs is the best time frme for this strategy

Warning

========

It is not a financial advise , it is for educational purposes only. Please do your own research before taking any trading decission

Gap driven intraday trade (better in 15 Min chart)// Based on yesterday's High, Low, today's open, and Bollinger Band (20) in current minute chart,

// Defined intraday Trading opportunity: Stop, Entry, T0, Target (S.E.T.T)

// Back test in 60, 30, 15, 5 Min charts with SPY, QQQ, XOP, AAPL, TSLA, NVDA, UAL

// In 60 and 30 min chart, the stop and target are too big. 5 min is too small.

// 15 min Chart is the best time frame for this strategy;

// -------------------------------------------------------------------------------

// There will be Four lines in this study:

// 1. Entry Line,

// 1.1 Green Color line to Buy, If today's open price above Yesterday's High, and current price below BB upper line.

// 1.2 Red Color line to Short, if today's open price below Yesterday's Low, and current above BB Lower line.

//

// 2. Black line to show initial stop, one ATR in current min chart;

//

// 3. Blue Line (T0) to show where trader can move stop to make even, one ATR in current min chart;

//

// 4. Orange Line to show initial target, Three ATR in current min chart;

//

// Trading opportunity:

// If Entry line is green color, Set stop buy order at today's Open;

// Whenever price is below the green line, Prepare to buy;

//

// If Entry line is Red color, Set Stop short at today's Open;

// Whenever price is above the red line, Prepare to short;

//

// Initial Stop: One ATR in min chart;

// Initial T0: One ATR in min chart;

// Initial Target: Three ATR in min chart;

// Initial RRR: Reward Risk Ratio = 3:1;

//

// Maintain: Once the position moves to T0, Move stop to "Make even + Lunch (such as, Entry + $0.10)";

// Allow to move target bigger, such as, next demand/supply zone;

// When near target or demand/supply zone or near Market close, move stop tightly;

//

// Close position: Limit order filled, or near Market Close, or trendline break;

//

// Key Step: Move stop to "Make even" after T0, Do not turn winner to loser;

// Willing to "in and out" many times in one day, and trade the same direction, same price again and again.

//

// Basic trading platform requests:

// To use this strategy, user needs to:

// 1. Scan Stocks Before market open:

// Prepare a watch list for top 10 ETF and Top 90 stocks which are most actively traded.

// Stock might be limited by price range, Beta, optionable, ...

// Before market open, Run a scan for these stocks, find which has GAP and inside BB;

// create watch list for that day.

//

// 2. Attach OSO and OCO orders:

// User needs to Send Entry, Stop (loss), and limit (target) orders at one time;

// Order Send order ( OSO ): Entry order sends Stop order and limit order;

// Order Cancel order ( OCO ): Stop order and limit order, when one is filled, it will cancel the other instantly;

Selectable Ticker DIXWith this script you can select 10 tickers and see the aggregated DIX for them. I have the highest volume equity ETFs as defaults, but one could easily select FAANGM and a few other mega caps and make a FAANGM DIX index by changing the tickers in the settings. One improvement item that I have not gotten around to doing is to create a dollar weighted version of this, similar to the actual Squeezemetrics SPX DIX. This is "equal weighted" To make a dollar weighted version, multiply each by the daily closing price essentially and THEN find the average. It is possible to do I just have not taken the time to do it. It is on the list of things to do. If anyone has a solution PM me and I will add it. Thanks.

Stochastic based on Closing Prices - Identify and Rank TrendsStochClose is a trend indicator that can be used on its own to measure trend strength, in a scan to rank a group of securities according to trend strength or as part of a trend following strategy. Moreover, it acts as a volatility-adjusted trend indicator that puts securities on an equal footing.

StochClose measures the location of the current close relative to the close-only high-low range over a given period of time. In contrast to the traditional Stochastic Oscillator, this indicator only uses closing prices. Traditional Stochastic uses intraday highs and lows to calculate the range. The focus on closing prices reduces signal noise caused by intraday highs and lows, and filters out errant or irrationally exuberant price spikes.

Here are some examples when the high or low was out of proportion and suspect. Perhaps most famously, there were errant spike lows in dozens of ETFs in August 2015 (XLK, IJR, ITB). There were other spikes in VMBS (October 2014), IJR (October 2008) and KRE (May 2011). Elsewhere, there were suspicious spikes in IEI (April 2020), CHD (March 2020), CCRN (March 2020) and FNB (March 2020)

The preferred setting to identify medium and long-term uptrends is 125 days with 5 days smoothing. 125 days covers around six months. Thus, StochClose(125,5) is a 5-day SMA of the 125-day Stochastic based on closing prices. Smoothing with the 5-day SMA introduces a little lag, but reduces whipsaws and signal noise.

StochClose fluctuates between 0 and 100 with 50 as the midpoint. Values above 80 indicate that the current price is near the high end of the 125-day range, while values below 20 indicate that price is near the low end of the range. For signals, a move above 60 puts the indicator firmly in the top half of the range and points to an uptrend. A move below 40 puts the indicator firmly in the bottom half of the range and points to a downtrend.

StochClose values can also be ranked to separate the leaders from the laggards. In contrast to Rate-of-Change and Percentage Above/Below a Moving Average, StochClose acts as a volatility-adjusted indicator that can identify trend strength or weakness. The Consumer Staples SPDR is unlikely to win in a Rate-of-Change contest with the Technology SPDR. However, it is just as easy for the Consumer Staples SPDR to get in the top of its range as it is for the Technology SPDR. StochClose puts securities on an equal footing.

StochClose measures trend direction and trend strength with one number. The indicator value tells us immediately if the security is trending higher or lower. Furthermore, we can compare this value against the values for other securities. Securities with higher StochClose values are stronger than those with lower values.

Chart Mojo Neutral Unwound CloudPlots days high/low and the Chart Mojo neutral cloud, the zone between vwap and 50% range. A secondary gravity right behind the opening 1 min range. The gray crosses are the vwap the gold dots are 50% of developing range. The shaded area between vwap and 50% range is the Chart Mojo cloud...I think of it as traders from the open tend to unwind to it many times a day. More returns on a trend day but you will see urges toward it on trend days. Price tends to urge to it ahead of 10:30 session "1" and 1:15 Session 2. If you get used to watching it and its relationship to price and the opening 1 min range you should start to see tendencies as to when price unwinds toward it.. etc. Where price is in relation to the cloud and the clouds relationship to the opening 1 min range can reveal real time bias. You will being to see, upon observation how traders target the vwap and 50% with target tier of buys and sells etc. Often unwinds to the zones gravity. It takes force or a catalyst to break the gravity. I use it in conjuction with Time Zone theory and Wave and Pattern force...and look to leading correlating hi beta movers and internals like tick and new streaming highs-new straming lows to get jump on what you see on a big etf or index etc. If you intraday tendencies the neutral is very helpful.

Sector High/LowHighlights which S&P SPDR Sector ETFs are at highs of day (green letter) or lows of day (red letter)

The first candle of the day is always all-green because by default the first candle of the day has the high of the day. So this indicator is more meaningful later in the day when sectors are making repeated highs/lows

Modulate 40 SymbolsModulates (multiplies) 40 securities

Useful for assessing breadth

Defaults with the Top 40 holdings in SPX

Change symbols to measure breadth in an ETF

EMA DifferenceI put together a simple script for visualizing how far above/below the EMA the current price is. I applied this to all the S&P -0.12% sector ETFs to get a quick look at which sectors are over/underperforming. I hope someone else finds this helpful

Pseudo VIX -Intraday -.betaFor Educational Purpose -

Intraday VIX estimation using yesterdays VIX, previous overnight roll , and intraday values for the VXX etf (scaled up to VIX)

Works in all intraday time frames.

First attempt...feedback welcome.

UCS_Squeeze_Timing-V3Another Version with More Features . I am confident enough this works fine now. I am Sure this will be a valuable tool for you guys who love squeezes.

///////////////// This can be further optimized, Let me know with a comment, if you still need this to be optimized. ////////////////////

This update includes

- Added Options to detect squeeze using Heikin Ashi Candle

- Added Options to use BBR or Momentum (ROC) for the Momentum Histogram

- Custom Momentum Smoothing time period

- Removed the Separate Look back periods for BB/KC - Since it doesn't really make sense using different lengths for KC and BB.

HA Closes can be really helpful in trading ETFs like FXE, GLD, FXY, SLV etc, which constantly gaps on daily basis. This helps in smoothing out. And most Importantly it Lines up with the Underlying's Squeeze.

[The Next Major Version is currently being Back tested with better timing triggers etc...... That will replace all other Squeeze indicators in the market - Some Major upgrades have been done to the squeezes to read the consolidation is with support or resistance. Also plan on adding best bet entries and pre-breakout signals. So far so good, this recent contradicting trends in daily / weekly in the market is making the indicator hard to work per theory]

The delay is because, I do not like to post any script (with signals) without sufficient back testing . I will not post these indicator with signals, unless I am sure it works per my theoretical derivations.

-

Thanks for Being Patient and all your support.

Until then - Good Luck Trading.

ETF Leverage VerificationDo leveraged ETFs really return what they promise?

Do they return the exact 2x or 3x? Or a slightly different multiple?

How much do they deviate from the promised leverage multiples?

Do these deviations impact investors in a positive or negative manner?

These are the questions that I want to answer with this indicator.

The ETF Leverage Verification indicator challenges the conventional understanding of leveraged ETFs by measuring how they actually perform versus their theoretical targets.

Instead of assuming leveraged ETFs perfectly track their target multiple, this indicator quantifies the real-world behavior by comparing the expected returns versus the actual results on every trading day.

Key Features

Measures actual versus expected performance of leveraged ETFs

Tracks deviation patterns across thousands of trading days

Identifies asymmetric behavior in up versus down markets

Quantifies beneficial "cushioning effect" during market declines

Provides statistical summary of performance patterns

Works with any leverage factor (2x, 3x, -1x, etc.)

Compatible with all leveraged ETFs (equity, bond, commodity, volatility)

How to Use the Indicator

Enter the Expected Leverage Factor (default: 2.0)

Select the Base Asset (underlying index, e.g., SPX)

Select the Leveraged Asset (leveraged ETF, e.g., SSO)

Understanding the Results

Green markers: Days when the ETF outperformed its expected multiple

Red markers: Days when the ETF underperformed its expected multiple

Data Table:

Positive Deviations: Count of days with better-than-expected performance

Negative Deviations: Count of days with worse-than-expected performance

Avg Deviation: Average magnitude of deviation from expected returns

Frequency Skew: Difference between beneficial deviations in down vs. up markets

Impact: Overall assessment of pattern benefit to investors

Summary Label:

Percentage of positive deviations in up and down markets

Total sample size for statistical significance

Key Patterns to Look For

Positive Deviation in Negative Days:

This occurs when a leveraged ETF falls less than expected during market declines. For example, if SPX falls 1% and a 2x ETF falls only 1.8% (instead of the expected 2%), this creates a +0.2% deviation. This pattern is beneficial as it provides downside protection.

Negative Deviation in Positive Days:

This happens when a leveraged ETF rises less than expected during market advances. For example, if SPX rises 1% and a 2x ETF rises only 1.9% (instead of the expected 2%), this creates a -0.1% deviation. This pattern reduces upside performance.

Frequency Skew:

The most critical metric that measures how much more frequently beneficial deviations occur in down markets compared to up markets. A higher positive skew indicates a stronger asymmetric pattern that helps long-term performance.

Mathematical Background

The indicator computes the deviation between expected and actual performance:

Deviation = Actual Return - Expected Return

Where:

Expected Return = Base Asset Return × Leverage Factor

The deviation is then categorized into four possible outcomes:

Positive deviation on positive market days

Negative deviation on positive market days

Positive deviation on negative market days

Negative deviation on negative market days

In short, more positive deviations are good for investors.

Please feel free to criticize. I'm happy to improve the indicator.

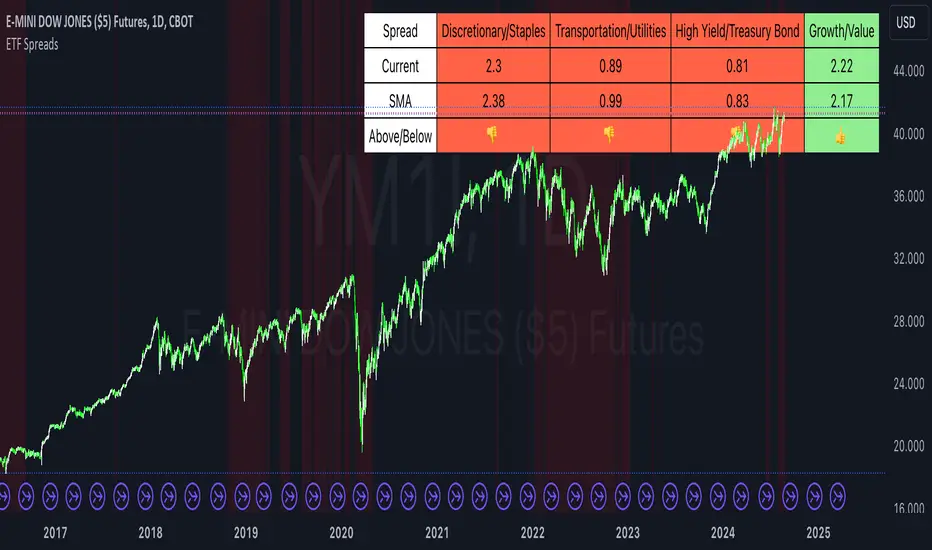

ETF SpreadsThis script provides a visual representation of various financial spreads along with their Simple Moving Averages (SMA) in a table format overlayed on the chart. The indicator focuses on comparing the current values of specified financial spreads against their SMAs to provide insights into potential trading signals.

Key Components:

SMA Length Input:

Users can input the length of the SMA, which determines the period over which the average is calculated. The default length is set to 20 days.

Symbols for Spreads:

The indicator tracks the closing prices of eight different financial instruments: XLY (Consumer Discretionary ETF), XLP (Consumer Staples ETF), IYT (Transportation ETF), XLU (Utilities ETF), HYG (High Yield Bond ETF), TLT (Long-Term Treasury Bond ETF), VUG (Growth ETF), and VTV (Value ETF).

Spread Calculations:

The script calculates spreads between different pairs of these instruments. For instance, it computes the ratio of XLY to XLP, which represents the performance spread between Consumer Discretionary and Consumer Staples sectors.

SMA Calculations:

SMAs for each spread are calculated to serve as a benchmark for comparing current spread values.

Table Display:

The indicator displays a table in the top-right corner of the chart with the following columns: Spread Name, Current Spread Value, SMA Value, and Status (indicating whether the current spread is above or below its SMA).

Status and Background Color:

The indicator uses colored backgrounds to show whether the current spread is above (light green) or below (tomato red) its SMA. Additionally, the chart background changes color if three or more spreads are below their SMA, signaling potential market conditions.

Scientific Literature on Spreads and Their Importance for Portfolio Management

"The Value of Financial Spreads in Portfolio Diversification"

Authors: G. Gregoriou, A. Z. P. G. Constantinides

Journal: Financial Markets, Institutions & Instruments, 2012

Abstract: This study explores how financial spreads between different asset classes can enhance portfolio diversification and reduce overall risk. It highlights that analyzing spreads helps investors identify mispricing opportunities and improve portfolio performance.

"The Role of Spreads in Investment Strategy and Risk Management"

Authors: R. J. Hodrick, E. S. S. Zhang

Journal: Journal of Portfolio Management, 2010

Abstract: This paper discusses the significance of spreads in investment strategies and their impact on risk management. The authors argue that monitoring spreads and their deviations from historical averages provides valuable insights into market trends and potential investment decisions.

"Spread Trading: An Overview and Its Use in Portfolio Management"

Authors: J. M. M. Perkins, L. A. B. Smith

Journal: Financial Review, 2009

Abstract: This review article provides an overview of spread trading techniques and their applications in portfolio management. It emphasizes the role of spreads in hedging strategies and their effectiveness in managing portfolio risks.

"Analyzing Financial Spreads for Better Portfolio Allocation"

Authors: A. S. Dechow, J. E. Stambaugh

Journal: Journal of Financial Economics, 2007

Abstract: The authors analyze various methods of financial spread calculations and their implications for portfolio allocation decisions. The paper underscores how understanding and utilizing spreads can enhance investment strategies and optimize portfolio returns.

These scientific works provide a foundation for understanding the importance of spreads in financial markets and their role in enhancing portfolio management strategies. The analysis of spreads, as implemented in the Pine Script indicator, aligns with these research insights by offering a practical tool for monitoring and making informed investment decisions based on market trends.