Trading IQ - ICT LibraryLibrary "ICTlibrary"

Used to calculate various ICT related price levels and strategies. An ongoing project.

Hello Coders!

This library is meant for sourcing ICT related concepts. While some functions might generate more output than you require, you can specify "Lite Mode" as "true" in applicable functions to slim down necessary inputs.

isLastBar(userTF)

Identifies the last bar on the chart before a timeframe change

Parameters:

userTF (simple int) : the timeframe you wish to calculate the last bar for, must be converted to integer using 'timeframe.in_seconds()'

Returns: bool true if bar on chart is last bar of higher TF, dalse if bar on chart is not last bar of higher TF

necessaryData(atrTF)

returns necessaryData UDT for historical data access

Parameters:

atrTF (float) : user-selected timeframe ATR value.

Returns: logZ. log return Z score, used for calculating order blocks.

method gradBoxes(gradientBoxes, idColor, timeStart, bottom, top, rightCoordinate)

creates neon like effect for box drawings

Namespace types: array

Parameters:

gradientBoxes (array) : an array.new() to store the gradient boxes

idColor (color)

timeStart (int) : left point of box

bottom (float) : bottom of box price point

top (float) : top of box price point

rightCoordinate (int) : right point of box

Returns: void

checkIfTraded(tradeName)

checks if recent trade is of specific name

Parameters:

tradeName (string)

Returns: bool true if recent trade id matches target name, false otherwise

checkIfClosed(tradeName)

checks if recent closed trade is of specific name

Parameters:

tradeName (string)

Returns: bool true if recent closed trade id matches target name, false otherwise

IQZZ(atrMult, finalTF)

custom ZZ to quickly determine market direction.

Parameters:

atrMult (float) : an atr multiplier used to determine the required price move for a ZZ direction change

finalTF (string) : the timeframe used for the atr calcuation

Returns: dir market direction. Up => 1, down => -1

method drawBos(id, startPoint, getKeyPointTime, getKeyPointPrice, col, showBOS, isUp)

calculates and draws Break Of Structure

Namespace types: array

Parameters:

id (array)

startPoint (chart.point)

getKeyPointTime (int) : the actual time of startPoint, simplystartPoint.time

getKeyPointPrice (float) : the actual time of startPoint, simplystartPoint.price

col (color) : color of the BoS line / label

showBOS (bool) : whether to show label/line. This function still calculates internally for other ICT related concepts even if not drawn.

isUp (bool) : whether BoS happened during price increase or price decrease.

Returns: void

method drawMSS(id, startPoint, getKeyPointTime, getKeyPointPrice, col, showMSS, isUp, upRejections, dnRejections, highArr, lowArr, timeArr, closeArr, openArr, atrTFarr, upRejectionsPrices, dnRejectionsPrices)

calculates and draws Market Structure Shift. This data is also used to calculate Rejection Blocks.

Namespace types: array

Parameters:

id (array)

startPoint (chart.point)

getKeyPointTime (int) : the actual time of startPoint, simplystartPoint.time

getKeyPointPrice (float) : the actual time of startPoint, simplystartPoint.price

col (color) : color of the MSS line / label

showMSS (bool) : whether to show label/line. This function still calculates internally for other ICT related concepts even if not drawn.

isUp (bool) : whether MSS happened during price increase or price decrease.

upRejections (array)

dnRejections (array)

highArr (array) : array containing historical highs, should be taken from the UDT "necessaryData" defined above

lowArr (array) : array containing historical lows, should be taken from the UDT "necessaryData" defined above

timeArr (array) : array containing historical times, should be taken from the UDT "necessaryData" defined above

closeArr (array) : array containing historical closes, should be taken from the UDT "necessaryData" defined above

openArr (array) : array containing historical opens, should be taken from the UDT "necessaryData" defined above

atrTFarr (array) : array containing historical atr values (of user-selected TF), should be taken from the UDT "necessaryData" defined above

upRejectionsPrices (array) : array containing up rejections prices. Is sorted and used to determine selective looping for invalidations.

dnRejectionsPrices (array) : array containing down rejections prices. Is sorted and used to determine selective looping for invalidations.

Returns: void

method getTime(id, compare, timeArr)

gets time of inputted price (compare) in an array of data

this is useful when the user-selected timeframe for ICT concepts is greater than the chart's timeframe

Namespace types: array

Parameters:

id (array) : the array of data to search through, to find which index has the same value as "compare"

compare (float) : the target data point to find in the array

timeArr (array) : array of historical times

Returns: the time that the data point in the array was recorded

method OB(id, highArr, signArr, lowArr, timeArr, sign)

store bullish orderblock data

Namespace types: array

Parameters:

id (array)

highArr (array) : array of historical highs

signArr (array) : array of historical price direction "math.sign(close - open)"

lowArr (array) : array of historical lows

timeArr (array) : array of historical times

sign (int) : orderblock direction, -1 => bullish, 1 => bearish

Returns: void

OTEstrat(OTEstart, future, closeArr, highArr, lowArr, timeArr, longOTEPT, longOTESL, longOTElevel, shortOTEPT, shortOTESL, shortOTElevel, structureDirection, oteLongs, atrTF, oteShorts)

executes the OTE strategy

Parameters:

OTEstart (chart.point)

future (int) : future time point for drawings

closeArr (array) : array of historical closes

highArr (array) : array of historical highs

lowArr (array) : array of historical lows

timeArr (array) : array of historical times

longOTEPT (string) : user-selected long OTE profit target, please create an input.string() for this using the example below

longOTESL (int) : user-selected long OTE stop loss, please create an input.string() for this using the example below

longOTElevel (float) : long entry price of selected retracement ratio for OTE

shortOTEPT (string) : user-selected short OTE profit target, please create an input.string() for this using the example below

shortOTESL (int) : user-selected short OTE stop loss, please create an input.string() for this using the example below

shortOTElevel (float) : short entry price of selected retracement ratio for OTE

structureDirection (string) : current market structure direction, this should be "Up" or "Down". This is used to cancel pending orders if market structure changes

oteLongs (bool) : input.bool() for whether OTE longs can be executed

atrTF (float) : atr of the user-seleceted TF

oteShorts (bool) : input.bool() for whether OTE shorts can be executed

@exampleInputs

oteLongs = input.bool(defval = false, title = "OTE Longs", group = "Optimal Trade Entry")

longOTElevel = input.float(defval = 0.79, title = "Long Entry Retracement Level", options = , group = "Optimal Trade Entry")

longOTEPT = input.string(defval = "-0.5", title = "Long TP", options = , group = "Optimal Trade Entry")

longOTESL = input.int(defval = 0, title = "How Many Ticks Below Swing Low For Stop Loss", group = "Optimal Trade Entry")

oteShorts = input.bool(defval = false, title = "OTE Shorts", group = "Optimal Trade Entry")

shortOTElevel = input.float(defval = 0.79, title = "Short Entry Retracement Level", options = , group = "Optimal Trade Entry")

shortOTEPT = input.string(defval = "-0.5", title = "Short TP", options = , group = "Optimal Trade Entry")

shortOTESL = input.int(defval = 0, title = "How Many Ticks Above Swing Low For Stop Loss", group = "Optimal Trade Entry")

Returns: void (0)

displacement(logZ, atrTFreg, highArr, timeArr, lowArr, upDispShow, dnDispShow, masterCoords, labelLevels, dispUpcol, rightCoordinate, dispDncol, noBorders)

calculates and draws dispacements

Parameters:

logZ (float) : log return of current price, used to determine a "significant price move" for a displacement

atrTFreg (float) : atr of user-seleceted timeframe

highArr (array) : array of historical highs

timeArr (array) : array of historical times

lowArr (array) : array of historical lows

upDispShow (int) : amount of historical upside displacements to show

dnDispShow (int) : amount of historical downside displacements to show

masterCoords (map) : a map to push the most recent displacement prices into, useful for having key levels in one data structure

labelLevels (string) : used to determine label placement for the displacement, can be inside box, outside box, or none, example below

dispUpcol (color) : upside displacement color

rightCoordinate (int) : future time for displacement drawing, best is "last_bar_time"

dispDncol (color) : downside displacement color

noBorders (bool) : input.bool() to remove box borders, example below

@exampleInputs

labelLevels = input.string(defval = "Inside" , title = "Box Label Placement", options = )

noBorders = input.bool(defval = false, title = "No Borders On Levels")

Returns: void

method getStrongLow(id, startIndex, timeArr, lowArr, strongLowPoints)

unshift strong low data to array id

Namespace types: array

Parameters:

id (array)

startIndex (int) : the starting index for the timeArr array of the UDT "necessaryData".

this point should start from at least 1 pivot prior to find the low before an upside BoS

timeArr (array) : array of historical times

lowArr (array) : array of historical lows

strongLowPoints (array) : array of strong low prices. Used to retrieve highest strong low price and see if need for

removal of invalidated strong lows

Returns: void

method getStrongHigh(id, startIndex, timeArr, highArr, strongHighPoints)

unshift strong high data to array id

Namespace types: array

Parameters:

id (array)

startIndex (int) : the starting index for the timeArr array of the UDT "necessaryData".

this point should start from at least 1 pivot prior to find the high before a downside BoS

timeArr (array) : array of historical times

highArr (array) : array of historical highs

strongHighPoints (array)

Returns: void

equalLevels(highArr, lowArr, timeArr, rightCoordinate, equalHighsCol, equalLowsCol, liteMode)

used to calculate recent equal highs or equal lows

Parameters:

highArr (array) : array of historical highs

lowArr (array) : array of historical lows

timeArr (array) : array of historical times

rightCoordinate (int) : a future time (right for boxes, x2 for lines)

equalHighsCol (color) : user-selected color for equal highs drawings

equalLowsCol (color) : user-selected color for equal lows drawings

liteMode (bool) : optional for a lite mode version of an ICT strategy. For more control over drawings leave as "True", "False" will apply neon effects

Returns: void

quickTime(timeString)

used to quickly determine if a user-inputted time range is currently active in NYT time

Parameters:

timeString (string) : a time range

Returns: true if session is active, false if session is inactive

macros(showMacros, noBorders)

used to calculate and draw session macros

Parameters:

showMacros (bool) : an input.bool() or simple bool to determine whether to activate the function

noBorders (bool) : an input.bool() to determine whether the box anchored to the session should have borders

Returns: void

po3(tf, left, right, show)

use to calculate HTF po3 candle

@tip only call this function on "barstate.islast"

Parameters:

tf (simple string)

left (int) : the left point of the candle, calculated as bar_index + left,

right (int) : :the right point of the candle, calculated as bar_index + right,

show (bool) : input.bool() whether to show the po3 candle or not

Returns: void

silverBullet(silverBulletStratLong, silverBulletStratShort, future, userTF, H, L, H2, L2, noBorders, silverBulletLongTP, historicalPoints, historicalData, silverBulletLongSL, silverBulletShortTP, silverBulletShortSL)

used to execute the Silver Bullet Strategy

Parameters:

silverBulletStratLong (simple bool)

silverBulletStratShort (simple bool)

future (int) : a future time, used for drawings, example "last_bar_time"

userTF (simple int)

H (float) : the high price of the user-selected TF

L (float) : the low price of the user-selected TF

H2 (float) : the high price of the user-selected TF

L2 (float) : the low price of the user-selected TF

noBorders (bool) : an input.bool() used to remove the borders from box drawings

silverBulletLongTP (series silverBulletLevels)

historicalPoints (array)

historicalData (necessaryData)

silverBulletLongSL (series silverBulletLevels)

silverBulletShortTP (series silverBulletLevels)

silverBulletShortSL (series silverBulletLevels)

Returns: void

method invalidFVGcheck(FVGarr, upFVGpricesSorted, dnFVGpricesSorted)

check if existing FVGs are still valid

Namespace types: array

Parameters:

FVGarr (array)

upFVGpricesSorted (array) : an array of bullish FVG prices, used to selective search through FVG array to remove invalidated levels

dnFVGpricesSorted (array) : an array of bearish FVG prices, used to selective search through FVG array to remove invalidated levels

Returns: void (0)

method drawFVG(counter, FVGshow, FVGname, FVGcol, data, masterCoords, labelLevels, borderTransp, liteMode, rightCoordinate)

draws FVGs on last bar

Namespace types: map

Parameters:

counter (map) : a counter, as map, keeping count of the number of FVGs drawn, makes sure that there aren't more FVGs drawn

than int FVGshow

FVGshow (int) : the number of FVGs to show. There should be a bullish FVG show and bearish FVG show. This function "drawFVG" is used separately

for bearish FVG and bullish FVG.

FVGname (string) : the name of the FVG, "FVG Up" or "FVG Down"

FVGcol (color) : desired FVG color

data (FVG)

masterCoords (map) : a map containing the names and price points of key levels. Used to define price ranges.

labelLevels (string) : an input.string with options "Inside", "Outside", "Remove". Determines whether FVG labels should be inside box, outside,

or na.

borderTransp (int)

liteMode (bool)

rightCoordinate (int) : the right coordinate of any drawings. Must be a time point.

Returns: void

invalidBlockCheck(bullishOBbox, bearishOBbox, userTF)

check if existing order blocks are still valid

Parameters:

bullishOBbox (array) : an array declared using the UDT orderBlock that contains bullish order block related data

bearishOBbox (array) : an array declared using the UDT orderBlock that contains bearish order block related data

userTF (simple int)

Returns: void (0)

method lastBarRejections(id, rejectionColor, idShow, rejectionString, labelLevels, borderTransp, liteMode, rightCoordinate, masterCoords)

draws rejectionBlocks on last bar

Namespace types: array

Parameters:

id (array) : the array, an array of rejection block data declared using the UDT rejection block

rejectionColor (color) : the desired color of the rejection box

idShow (int)

rejectionString (string) : the desired name of the rejection blocks

labelLevels (string) : an input.string() to determine if labels for the block should be inside the box, outside, or none.

borderTransp (int)

liteMode (bool) : an input.bool(). True = neon effect, false = no neon.

rightCoordinate (int) : atime for the right coordinate of the box

masterCoords (map) : a map that stores the price of key levels and assigns them a name, used to determine price ranges

Returns: void

method OBdraw(id, OBshow, BBshow, OBcol, BBcol, bullishString, bearishString, isBullish, labelLevels, borderTransp, liteMode, rightCoordinate, masterCoords)

draws orderblocks and breaker blocks for data stored in UDT array()

Namespace types: array

Parameters:

id (array) : the array, an array of order block data declared using the UDT orderblock

OBshow (int) : the number of order blocks to show

BBshow (int) : the number of breaker blocks to show

OBcol (color) : color of order blocks

BBcol (color) : color of breaker blocks

bullishString (string) : the title of bullish blocks, which is a regular bullish orderblock or a bearish orderblock that's converted to breakerblock

bearishString (string) : the title of bearish blocks, which is a regular bearish orderblock or a bullish orderblock that's converted to breakerblock

isBullish (bool) : whether the array contains bullish orderblocks or bearish orderblocks. If bullish orderblocks,

the array will naturally contain bearish BB, and if bearish OB, the array will naturally contain bullish BB

labelLevels (string) : an input.string() to determine if labels for the block should be inside the box, outside, or none.

borderTransp (int)

liteMode (bool) : an input.bool(). True = neon effect, false = no neon.

rightCoordinate (int) : atime for the right coordinate of the box

masterCoords (map) : a map that stores the price of key levels and assigns them a name, used to determine price ranges

Returns: void

FVG

UDT for FVG calcualtions

Fields:

H (series float) : high price of user-selected timeframe

L (series float) : low price of user-selected timeframe

direction (series string) : FVG direction => "Up" or "Down"

T (series int) : => time of bar on user-selected timeframe where FVG was created

fvgLabel (series label) : optional label for FVG

fvgLineTop (series line) : optional line for top of FVG

fvgLineBot (series line) : optional line for bottom of FVG

fvgBox (series box) : optional box for FVG

labelLine

quickly pair a line and label together as UDT

Fields:

lin (series line) : Line you wish to pair with label

lab (series label) : Label you wish to pair with line

orderBlock

UDT for order block calculations

Fields:

orderBlockData (array) : array containing order block x and y points

orderBlockBox (series box) : optional order block box

vioCount (series int) : = 0 violation count of the order block. 0 = Order Block, 1 = Breaker Block

traded (series bool)

status (series string) : = "OB" status == "OB" => Level is order block. status == "BB" => Level is breaker block.

orderBlockLab (series label) : options label for the order block / breaker block.

strongPoints

UDT for strong highs and strong lows

Fields:

price (series float) : price of the strong high or strong low

timeAtprice (series int) : time of the strong high or strong low

strongPointLabel (series label) : optional label for strong point

strongPointLine (series line) : optional line for strong point

overlayLine (series line) : optional lines for strong point to enhance visibility

overlayLine2 (series line) : optional lines for strong point to enhance visibility

displacement

UDT for dispacements

Fields:

highPrice (series float) : high price of displacement

lowPrice (series float) : low price of displacement

timeAtPrice (series int) : time of bar where displacement occurred

displacementBox (series box) : optional box to draw displacement

displacementLab (series label) : optional label for displacement

po3data

UDT for po3 calculations

Fields:

dHigh (series float) : higher timeframe high price

dLow (series float) : higher timeframe low price

dOpen (series float) : higher timeframe open price

dClose (series float) : higher timeframe close price

po3box (series box) : box to draw po3 candle body

po3line (array) : line array to draw po3 wicks

po3Labels (array) : label array to label price points of po3 candle

macros

UDT for session macros

Fields:

sessions (array) : Array of sessions, you can populate this array using the "quickTime" function located above "export macros".

prices (matrix) : Matrix of session data -> open, high, low, close, time

sessionTimes (array) : Array of session names. Pairs with array sessions.

sessionLines (matrix) : Optional array for sesion drawings.

OTEtimes

UDT for data storage and drawings associated with OTE strategy

Fields:

upTimes (array) : time of highest point before trade is taken

dnTimes (array) : time of lowest point before trade is taken

tpLineLong (series line) : line to mark tp level long

tpLabelLong (series label) : label to mark tp level long

slLineLong (series line) : line to mark sl level long

slLabelLong (series label) : label to mark sl level long

tpLineShort (series line) : line to mark tp level short

tpLabelShort (series label) : label to mark tp level short

slLineShort (series line) : line to mark sl level short

slLabelShort (series label) : label to mark sl level short

sweeps

UDT for data storage and drawings associated with liquidity sweeps

Fields:

upSweeps (matrix) : matrix containing liquidity sweep price points and time points for up sweeps

dnSweeps (matrix) : matrix containing liquidity sweep price points and time points for down sweeps

upSweepDrawings (array) : optional up sweep box array. Pair the size of this array with the rows or columns,

dnSweepDrawings (array) : optional up sweep box array. Pair the size of this array with the rows or columns,

raidExitDrawings

UDT for drawings associated with the Liquidity Raid Strategy

Fields:

tpLine (series line) : tp line for the liquidity raid entry

tpLabel (series label) : tp label for the liquidity raid entry

slLine (series line) : sl line for the liquidity raid entry

slLabel (series label) : sl label for the liquidity raid entry

m2022

UDT for data storage and drawings associated with the Model 2022 Strategy

Fields:

mTime (series int) : time of the FVG where entry limit order is placed

mIndex (series int) : array index of FVG where entry limit order is placed. This requires an array of FVG data, which is defined above.

mEntryDistance (series float) : the distance of the FVG to the 50% range. M2022 looks for the fvg closest to 50% mark of range.

mEntry (series float) : the entry price for the most eligible fvg

fvgHigh (series float) : the high point of the eligible fvg

fvgLow (series float) : the low point of the eligible fvg

longFVGentryBox (series box) : long FVG box, used to draw the eligible FVG

shortFVGentryBox (series box) : short FVG box, used to draw the eligible FVG

line50P (series line) : line used to mark 50% of the range

line100P (series line) : line used to mark 100% (top) of the range

line0P (series line) : line used to mark 0% (bottom) of the range

label50P (series label) : label used to mark 50% of the range

label100P (series label) : label used to mark 100% (top) of the range

label0P (series label) : label used to mark 0% (bottom) of the range

sweepData (array)

silverBullet

UDT for data storage and drawings associated with the Silver Bullet Strategy

Fields:

session (series bool)

sessionStr (series string) : name of the session for silver bullet

sessionBias (series string)

sessionHigh (series float) : = high high of session // use math.max(silverBullet.sessionHigh, high)

sessionLow (series float) : = low low of session // use math.min(silverBullet.sessionLow, low)

sessionFVG (series float) : if applicable, the FVG created during the session

sessionFVGdraw (series box) : if applicable, draw the FVG created during the session

traded (series bool)

tp (series float) : tp of trade entered at the session FVG

sl (series float) : sl of trade entered at the session FVG

sessionDraw (series box) : optional draw session with box

sessionDrawLabel (series label) : optional label session with label

silverBulletDrawings

UDT for trade exit drawings associated with the Silver Bullet Strategy

Fields:

tpLine (series line) : tp line drawing for strategy

tpLabel (series label) : tp label drawing for strategy

slLine (series line) : sl line drawing for strategy

slLabel (series label) : sl label drawing for strategy

unicornModel

UDT for data storage and drawings associated with the Unicorn Model Strategy

Fields:

hPoint (chart.point)

hPoint2 (chart.point)

hPoint3 (chart.point)

breakerBlock (series box) : used to draw the breaker block required for the Unicorn Model

FVG (series box) : used to draw the FVG required for the Unicorn model

topBlock (series float) : price of top of breaker block, can be used to detail trade entry

botBlock (series float) : price of bottom of breaker block, can be used to detail trade entry

startBlock (series int) : start time of the breaker block, used to set the "left = " param for the box

includes (array) : used to store the time of the breaker block, or FVG, or the chart point sequence that setup the Unicorn Model.

entry (series float) : // eligible entry price, for longs"math.max(topBlock, FVG.get_top())",

tpLine (series line) : optional line to mark PT

tpLabel (series label) : optional label to mark PT

slLine (series line) : optional line to mark SL

slLabel (series label) : optional label to mark SL

rejectionBlocks

UDT for data storage and drawings associated with rejection blocks

Fields:

rejectionPoint (chart.point)

bodyPrice (series float) : candle body price closest to the rejection point, for "Up" rejections => math.max(open, close),

rejectionBox (series box) : optional box drawing of the rejection block

rejectionLabel (series label) : optional label for the rejection block

equalLevelsDraw

UDT for data storage and drawings associated with equal highs / equal lows

Fields:

connector (series line) : single line placed at the first high or low, y = avgerage of distinguished equal highs/lows

connectorLab (series label) : optional label to be placed at the highs or lows

levels (array) : array containing the equal highs or lows prices

times (array) : array containing the equal highs or lows individual times

startTime (series int) : the time of the first high or low that forms a sequence of equal highs or lows

radiate (array) : options label to "radiate" the label in connector lab. Can be used for anything

necessaryData

UDT for data storage of historical price points.

Fields:

highArr (array) : array containing historical high points

lowArr (array) : array containing historical low points

timeArr (array) : array containing historical time points

logArr (array) : array containing historical log returns

signArr (array) : array containing historical price directions

closeArr (array) : array containing historical close points

binaryTimeArr (array) : array containing historical time points, uses "push" instead of "unshift" to allow for binary search

binaryCloseArr (array) : array containing historical close points, uses "push" instead of "unshift" to allow the correct

binaryOpenArr (array) : array containing historical optn points, uses "push" instead of "unshift" to allow the correct

atrTFarr (array) : array containing historical user-selected TF atr points

openArr (array) : array containing historical open points

"文华财经tick价格"に関するスクリプトを検索

Theta Shield | Flux Charts💎 GENERAL OVERVIEW

Introducing our new Theta Shield indicator! Theta is the options risk factor concerning how fast there is a decline in the value of an option over time. This indicator aims to help the trader avoid sideways market phases in the current ticker, to minimize the risk of theta decay. For more information, please check the "How Does It Work" section.

Features of the new Theta Shield Indicator :

Foresight Of Accumulation Zones

Decrease Risk Of Theta Decay

Clear "Valid" & "Non-Valid" Signals

Validness Trail

Alerts

📌 HOW DOES IT WORK ?

In options trading, theta is defined as the rate of decline in the value of an option due to the passage of time. Traders want to avoid this kind of decay in the value of an option. One of the best ways to avoid it is not holding an option contract when the market is going sideways. This indicator uses a stochastic oscillator to try to get a foresight of sideways markets, warning the trader to not hold an option contract while the price is in a range.

The indicator starts by calculating the stochastic value using close, high & low prices of the candlesticks. Then a stoch threshold & a theta length are determined depending on the option contract type defined by the user in the settings of the indicator. Each candlestick that falls above or below the stoch threshold value is counted, and a "theta valid strength" is calculated using the counted candlesticks, which has a value between -100 & 100. Here is the formula of the "theta valid strength" value :

f_lin_interpolate(float x0, float x1, float y0, float y1, float x) =>

y0 + (x - x0) * (y1 - y0) / (x1 - x0)

thetaValid = Total Candlesticks That Fall Above & Below The Threshold In Last "Theta Length" bars.

thetaValidStrength = f_lin_interpolate(0, thetaLength, -100, 100, thetaValid)

Then a trail is rendered, and "Valid" & "Non-Valid" signals are given using this freshly calculated strength value. Valid means that the indicator currently thinks that no accumulation will happen in the near future, so the option positions in the current ticker are protected from the theta decay. Non-Valid means that the indicator thinks the ticker has entered the accumulation phase, so holding any option position is not recommended, as they may be affected by the theta decay.

🚩 UNIQUENESS

This indicator offers a unique way to avoid theta decay in options trading. It uses a stochastic oscillator and thresholds to calculate a "theta strength" value, which is used for rendering validness signals and a trail. Traders can follow the valid & non-valid signals when deciding to hold their options position or not. The indicator also has an alerts feature, so you can get notified when a ticker is about to enter a range, or when it's about to get out of it.

⚙️ SETTINGS

1. General Configuration

Contract Type -> You can set the option contract type here. The indicator will adjust itself to get a better foresight depending on the contract length.

2. Style

Fill Validness -> Will render a trail based on "theta strength" value.

Basic FVGBasic Fair Value Gap (FVG) Indicator

The Basic Fair Value Gap (FVG) Indicator is a tool designed for traders using the TradingView platform to identify and visualize Fair Value Gaps (FVGs) on any given chart.

Key Features:

Bullish and Bearish FVG Detection: The indicator automatically detects and highlights both bullish and bearish Fair Value Gaps on the chart. Bullish gaps are highlighted in blue, while bearish gaps are marked in red, with customizable transparency for clear visibility.

Customizable Parameters:

Max Bars Back: Users can set the maximum number of bars to look back in order to find potential FVGs.

Box Length: The length of the FVG box can be adjusted to fit the user's preference, allowing for better visual management on different timeframes.

Tick Buffer for Close Validation: The indicator only considers an FVG filled if the price closes beyond the gap by a customizable tick buffer, ensuring precise gap closure recognition.

Automatic Removal of Filled Gaps: Once an FVG is filled (i.e., the price closes beyond the gap by the defined tick buffer), the corresponding FVG box is automatically removed from the chart. This keeps the chart clean and focused on active gaps.

Real-Time Updates: The indicator updates in real-time, ensuring that traders have the most current information about potential gaps in price, which could signify strong support or resistance levels.

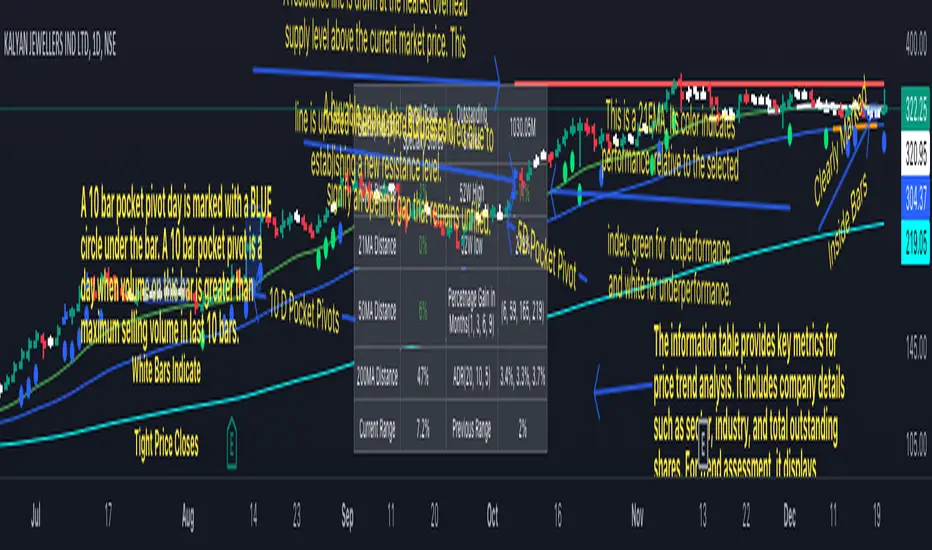

Swing Trend AnalysisIntroducing the Swing Trend Analyzer: A Powerful Tool for Swing and Positional Trading

The Swing Trend Analyzer is a cutting-edge indicator designed to enhance your swing and positional trading by providing precise entry points based on volatility contraction patterns and other key technical signals. This versatile tool is packed with features that cater to traders of all timeframes, offering flexibility, clarity, and actionable insights.

Key Features:

1. Adaptive Moving Averages:

The Swing Trend Analyzer offers multiple moving averages tailored to the timeframe you are trading on. On the daily chart, you can select up to four different moving average lengths, while all other timeframes provide three moving averages. This flexibility allows you to fine-tune your analysis according to your trading strategy. Disabling a moving average is as simple as setting its value to zero, making it easy to customize the indicator to your needs.

2. Dynamic Moving Average Colors Based on Relative Strength:

This feature allows you to compare the performance of the current ticker against a major index or any symbol of your choice. The moving average will change color based on whether the ticker is outperforming or underperforming the selected index over the chosen period. For example, on a daily chart, if the 21-day moving average turns blue, it indicates that the ticker has outperformed the selected index over the last 21 days. This visual cue helps you quickly identify relative strength, a key factor in successful swing trading.

3. Visual Identification of Price Contractions:

The Swing Trend Analyzer changes the color of price bars to white (on a dark theme) or black (on a light theme) when a contraction in price is detected. Price contractions are highlighted when either of the following conditions is met: a) the current bar is an inside bar, or b) the price range of the current bar is less than the 14-period Average Daily Range (ADR). This feature makes it easier to spot price contractions across all timeframes, which is crucial for timing entries in swing trading.

4. Overhead Supply Detection with Automated Resistance Lines:

The indicator intelligently detects the presence of overhead supply and draws a single resistance line to avoid clutter on the chart. As price breaches the resistance line, the old line is automatically deleted, and a new resistance line is drawn at the appropriate level. This helps you focus on the most relevant resistance levels, reducing noise and improving decision-making.

5. Buyable Gap Up Marker: The indicator highlights bars in blue when a candle opens with a gap that remains unfilled. These bars are potential Buyable Gap Up (BGU) candidates, signaling opportunities for long-side entries.

6. Comprehensive Swing Trading Information Table:

The indicator includes a detailed table that provides essential data for swing trading:

a. Sector and Industry Information: Understand the sector and industry of the ticker to identify stocks within strong sectors.

b. Key Moving Averages Distances (10MA, 21MA, 50MA, 200MA): Quickly assess how far the current price is from key moving averages. The color coding indicates whether the price is near or far from these averages, offering vital visual cues.

c. Price Range Analysis: Compare the current bar's price range with the previous bar's range to spot contraction patterns.

d. ADR (20, 10, 5): Displays the Average Daily Range over the last 20, 10, and 5 periods, crucial for identifying contraction patterns. On the weekly chart, the ADR continues to provide daily chart information.

e. 52-Week High/Low Data: Shows how close the stock is to its 52-week high or low, with color coding to highlight proximity, aiding in the identification of potential breakout or breakdown candidates.

f. 3-Month Price Gain: See the price gain over the last three months, which helps identify stocks with recent momentum.

7. Pocket Pivot Detection with Visual Markers:

Pocket pivots are a powerful bullish signal, especially relevant for swing trading. Pocket pivots are crucial for swing trading and are effective across all timeframes. The indicator marks pocket pivots with circular markers below the price bar:

a. 10-Day Pocket Pivot: Identified when the volume exceeds the maximum selling volume of the last 10 days. These are marked with a blue circle.

b. 5-Day Pocket Pivot: Identified when the volume exceeds the maximum selling volume of the last 5 days. These are marked with a green circle.

The Swing Trend Analyzer is designed to provide traders with the tools they need to succeed in swing and positional trading. Whether you're looking for precise entry points, analyzing relative strength, or identifying key price contractions, this indicator has you covered. Experience the power of advanced technical analysis with the Swing Trend Analyzer and take your trading to the next level.

Portfolio Index Generator [By MUQWISHI]▋ INTRODUCTION:

The “Portfolio Index Generator” simplifies the process of building a custom portfolio management index, allowing investors to input a list of preferred holdings from global securities and customize the initial investment weight of each security. Furthermore, it includes an option for rebalancing by adjusting the weights of assets to maintain a desired level of asset allocation. The tool serves as a comprehensive approach for tracking portfolio performance, conducting research, and analyzing specific aspects of portfolio investment. The output includes an index value, a table of holdings, and chart plotting, providing a deeper understanding of the portfolio's historical movement.

_______________________

▋ OVERVIEW:

The image can be taken as an example of building a custom portfolio index. I created this index and named it “My Portfolio Performance”, which comprises several global companies and crypto assets.

_______________________

▋ OUTPUTS:

The output can be divided into 4 sections:

1. Portfolio Index Title (Name & Value).

2. Portfolio Specifications.

3. Portfolio Holdings.

4. Portfolio Index Chart.

1. Portfolio Index Title, displays the index name at the top, and at the bottom, it shows the index value, along with the chart timeframe, e.g., daily change in points and percentage.

2. Portfolio Specifications, displays the essential information on portfolio performance, including the investment date range, initial capital, returns, assets, and equity.

3. Portfolio Holdings, a list of the holding securities inside a table that contains the ticker, average entry price, last price, return percentage of the portfolio's initial capital, and customized weighted percentage of the portfolio. Additionally, a tooltip appears when the user passes the cursor over a ticker's cell, showing brief information about the company, such as the company's name, exchange market, country, sector, and industry.

4. Index Chart, display a plot of the historical movement of the index in the form of a bar, candle, or line chart.

_______________________

▋ INDICATOR SETTINGS:

Section(1): Style Settings

(1) Naming the index.

(2) Table location on the chart and cell size.

(3) Sorting Holdings Table. By securities’ {Return(%) Portfolio, Weight(%) Portfolio, or Ticker Alphabetical} order.

(4) Choose the type of index: {Equity or Return (%)}, and the plot type for the index: {Candle, Bar, or Line}.

(5) Positive/Negative colors.

(6) Table Colors (Title, Cell, and Text).

(7) To show/hide any indicator’s components.

Section(2): Performance Settings

(1) Calculation window period: from DateTime to DateTime.

(2) Initial Capital and specifying currency.

(3) Option to enable portfolio rebalancing in {Monthly, Quarterly, or Yearly} intervals.

Section(3): Portfolio Holdings

(1) Enable and count security in the investment portfolio.

(2) Initial weight of security. For example, if the initial capital is $100,000 and the weight of XYZ stock is 4%, the initial value of the shares would be $4,000.

(3) Select and add up to 30 symbols that interested in.

Please let me know if you have any questions.

BB Position CalculatorPosition Size Calculator Instructions

Overview

The Position Size Calculator is designed to help traders automatically determine the appropriate lot size based on the dollar amount they are willing to risk. It includes features for automatic lot sizing, fixed lot risk calculations, take profit calculations (both automatic and fixed), max run-up, and max drawdown. Calculated values are displayed in ticks, points, and USD.

Key Features

• Automatic Lot Sizing: Automatically calculates lot size based on the amount of money you are willing to risk.

• Fixed Lot Risk Calculations: Provides risk calculations for fixed lot sizes.

• Take Profit Calculations: Offers both automatic and fixed take profit calculations.

• Max Run-Up and Max Drawdown: Monitors and displays the maximum run-up and drawdown of your trade.

• Detailed Metrics: Displays all calculated values in ticks, points, and USD.

Setup Instructions

1. Add and Remove for Each Position: The calculator is designed to be added to your chart for each new position. Once your preferences are set the first time, save them as your default to retain your settings for future use.

2. Adding the Indicator to Favorites:

• Use the TradingView keyboard shortcut “/” then type “pos.”

• Use the arrow key to select the Position Size Calculator and press enter.

• Close the indicator selection pop-up.

3. Setting the Trigger Price:

• A blue pop-up labeled “SET TRIGGER PRICE” will appear at the bottom of the chart.

• Click on the chart at the price level where you want to enter the trade.

4. Setting the Stop Loss:

• The pop-up will change to “SET STOP LOSS.”

• Click on the chart at the price level where your stop loss will be set.

5. Setting the Take Profit:

• The pop-up will change to “SET TAKE PROFIT.”

• Click on the chart at the price level where you want to take profit. If you have selected the option to overwrite with a set risk/reward ratio (R:R), the calculation will use this price level.

6. Setting the Trade Window Start:

• The pop-up will change to “SET TRADE WINDOW START.”

• Click on the bar in time where you want the indicator to start monitoring for price to trigger the position.

7. Adjusting the Position:

• Clicking on any part of the indicator will display draggable lines, allowing you to fine-tune the position that was previously plotted by the first four chart clicks.

Additional Notes

• Compatibility: This calculator has only been tested with futures trading.

• Customization: Once your preferences are set, save them as your default to make setup quicker for future trades.

• Support: If you have any questions or feature requests, please feel free to reach out.

ATR/ADR Support and Resistance LevelsATR/ADR Support and Resistance Levels Indicator

This script is designed to provide traders with precise ATR (Average True Range) and ADR (Average Daily Range) support and resistance levels. It can be effectively used to identify price breakouts or rejections near these critical lines and assist in confirming trend retests.

How It Works:

Support and Resistance Lines: The script plots ATR/ADR-based support and resistance lines, which can be toggled on or off.

Daily Data Integration: It incorporates daily open and close prices to enhance the accuracy of the support and resistance levels.

Clear Visuals: The indicator uses distinct colors for support (green) and resistance (red) levels, providing clear visual cues.

Default Settings: The default settings are optimized for most trading environments. Adjusting the ATR/ADR Length can fine-tune the indicator's responsiveness to market movements.

Key Features:

ATR & ADR Calculation: Choose between using ATR, ADR, or both. ATR is recommended for most scenarios.

Customizable Lengths: Adjust the ATR/ADR Length to refine the average calculation to your preference, with 14 being the standard value.

EMA for Market Bias: The EMA helps determine the ticker bias. It is colored green when the market is above the average price and red when it is below. This allows you to more easily determine whether or not the ADR/ATR levels are valid.

Versatile Usage: Suitable for various trading types, ensuring broad applicability across different market conditions.

How to Use:

ATR vs ADR: You should use ADR if you are day trading AND do not want to include gap data in the levels. It is recommended you use ATR.

Bounces off Levels: When price bounces off of a support/resistance level, it is very likely that price will respect this level. This indicates that price is unlikely to move beyond the ticker's average volatility. You should wait for an additional bounce to confirm.

Breakthroughs of Levels: When price breaks through a support/resistance level, it is very likely that price will continue beyond this level. This indicates that price has moved beyond that ticker's average volatility. You should wait for a bounce off the level to confirm.

This indicator is a valuable tool for traders seeking to enhance their technical analysis with support and resistance levels based on ATR and ADR calculations. It is perfect for identifying key price points and understanding market trends.

OrderFlow Absorption IndicatorWhat it Does

The OrderFlow Absorption Indicator marks areas where the price absorbs a large volume of aggressive market trades. This indicates areas where price may bounce back due to large limit (resting) orders absorbing significant aggressor volume (market orders). Absorption can also be seen as "preventing" or "stopping" the other side from breaking through a price level (e.g. bids stopping an influx of sell market orders). Absorption may signal a change in sentiment, potentially leading to a pullback or reversal.

An Example of Absorption

Of course, it is not always the case that such bullish absorption will initiate a trend as the example above. The OrderFlow Absorption Indicator merely serves as a tool for spotting possible absorption points in the market which you can incorporate into your trading arsenal.

How it Works

The indicator actively monitors price changes and records volume accumulated at a price level. If the price bounces back to at least where it was before the current price move, the indicator records this as absorption, provided it meets the Volume Requirement and optional Time Requirement.

How to Use it

1. Set Parameters

Choose your desired tick size and volume filter value. If unsure, refer to the table on the top right of the chart for recommended values. An automatic volume limit filter mode is also available.

Automatic Limit Mode : Enable this mode to have the indicator automatically select a volume filter value. It calculates the standard deviation of the last n minutes of volume and multiplies it by a volume multiplier. You can adjust these parameters.

Higher Volume Filter : Setting a higher volume filter value results in fewer, but higher quality detections, reducing noise.

2. Enabling the Time Limit

Enabling the time limit further improves detection quality by filtering out price levels that can defend against quick, sudden aggressive orders, acting as confirmation and indicating strong sentiment and resilient liquidity.

3. Enabling Historical Data Absorption

The indicator can also detect absorption in historical data, though less accurately than in real-time due to OHLCV aggregation.

You can select the granularity of historical data.

Lower granularity (e.g., 1 second) : Provides more accurate detections but may slow down the indicator.

Higher granularity : Improves speed but reduces detection accuracy.

Other Features

Hovering : When hovering over an absorption point, the interface reveals the price where the absorption occurred, along with the volume absorbed by the bids and asks, as well as the volume filter value used.

Delta Mode : In Delta mode, the system calculates the difference between the volume absorbed by bids and asks, revealing points only when the absolute value of this difference exceeds the volume filter value. Especially useful for larger tick sizes.

Troubleshooting

If the indicator doesn't mark anything, it means the traded volume hasn't exceeded the set volume filter value within the specified price intervals(tick size) and time limit. Adjust these settings as necessary.

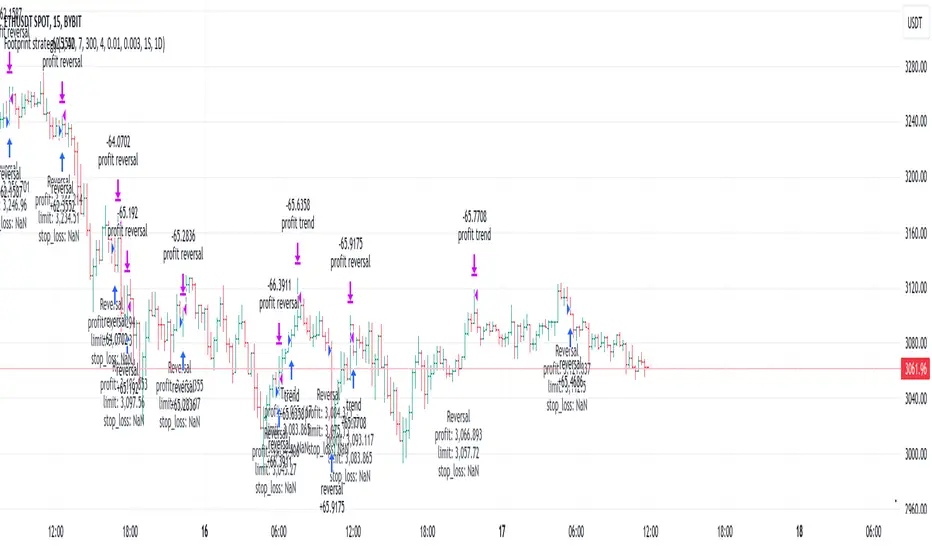

Footprint strategyThis strategy uses imbalance volume data obtained by footprint calculation technology.

There are two signals to enter a trade:

trend - the current buy volume on the bar is greater than the current sell volume and there is at least one imbalance line.

reversal - the current bar is falling, but the general market trend is positive (growing) and the imbalance buy volume exceeds the imbalance sell volume.

When any of the conditions is triggered, two orders are placed: Take Profit and Stop loss (according to the percentage value from the inputs).

A little advice on use:

The strategy performs best on a 15 minute timeframe.

It is necessary to choose acceptable values of Take Profit and Stop loss depending on the order of symbol prices.

Inputs related to the strategy:

Stop loss - percentage size of stop loss to exit the trade.

Enable stop loss - stop loss activation.

Take Profit - percentage size of Take Profit.

Calculation timeframe - this is the timeframe from which the volume will be collected for distribution to buy and sell (if you do not have access to the seconds chart, set here 1 minute, the accuracy will be less, but it will work).

Trend timeframe - this is the timeframe from which the trend will be calculated.

Enable trend - activation of trend calculation.

Inputs related to the calculation of footprints (collection of the volume of purchases and sales):

Count show bars - Number of bars from rt bar to history to calculate.

Display all available bars - Strategy calculation on all available bars (based on the available amount of data with reduced resolution (set in Calculation timeframe)).

Ticks Per Row - Sets the price step, calculated by multiplying the entered value by syminfo.mintick.

Auto - The automatic "Ticks Per Row" calculation is based on the first available bar and applied to subsequent bars.

Max row - sets the acceptable number of rows within a bar.

Imbalance Percent - A percentage coefficient to determine the Imbalance of price levels.

Stacked levels - And minimum number of consecutive Imbalance levels required to draw extended lines.

If you have suggestions for improving the strategy and adding new conditions for entering and exiting the trade, please write).

Index Generator [By MUQWISHI]▋ INTRODUCTION :

The “Index Generator” simplifies the process of building a custom market index, allowing investors to enter a list of preferred holdings from global securities. It aims to serve as an approach for tracking performance, conducting research, and analyzing specific aspects of the global market. The output will include an index value, a table of holdings, and chart plotting, providing a deeper understanding of historical movement.

_______________________

▋ OVERVIEW:

The image can be taken as an example of building a custom index. I created this index and named it “My Oil & Gas Index”. The index comprises several global energy companies. Essentially, the indicator weights each company by collecting the number of shares and then computes the market capitalization before sorting them as seen in the table.

_______________________

▋ OUTPUTS:

The output can be divided into 3 sections:

1. Index Title (Name & Value).

2. Index Holdings.

3. Index Chart.

1. Index Title , displays the index name at the top, and at the bottom, it shows the index value, along with the daily change in points and percentage.

2. Index Holdings , displays list the holding securities inside a table that contains the ticker, price, daily change %, market cap, and weight %. Additionally, a tooltip appears when the user passes the cursor over a ticker's cell, showing brief information about the company, such as the company's name, exchange market, country, sector, and industry.

3. Index Chart , display a plot of the historical movement of the index in the form of a bar, candle, or line chart.

_______________________

▋ INDICATOR SETTINGS:

(1) Naming the index.

(2) Entering a currency. To unite all securities in one currency.

(3) Table location on the chart.

(4) Table’s cells size.

(5) Table’s colors.

(6) Sorting table. By securities’ (Market Cap, Change%, Price, or Ticker Alphabetical) order.

(7) Plotting formation (Candle, Bar, or Line)

(8) To show/hide any indicator’s components.

(9) There are 34 fields where user can fill them with symbols.

Please let me know if you have any questions.

Volatility Adjusted Weighted DEMA [BackQuant]Volatility Adjusted Weighted DEMA

The Volatility Adjusted Weighted Double Exponential Moving Average (VAWDEMA) by BackQuant is a sophisticated technical analysis tool designed for traders seeking to integrate volatility into their moving average calculations. This innovative indicator adjusts the weighting of the Double Exponential Moving Average (DEMA) according to recent volatility levels, offering a more dynamic and responsive measure of market trends.

Primarily, the single Moving average is very noisy, but can be used in the context of strategy development, where as the crossover, is best used in the context of defining a trading zone/ macro uptrend on higher timeframes.

Why Volatility Adjustment is Beneficial

Volatility is a fundamental aspect of financial markets, reflecting the intensity of price changes. A volatility adjustment in moving averages is beneficial because it allows the indicator to adapt more quickly during periods of high volatility, providing signals that are more aligned with the current market conditions. This makes the VAWDEMA a versatile tool for identifying trend strength and potential reversal points in more volatile markets.

Understanding DEMA and Its Advantages

DEMA is an indicator that aims to reduce the lag associated with traditional moving averages by applying a double smoothing process. The primary benefit of DEMA is its sensitivity and quicker response to price changes, making it an excellent tool for trend following and momentum trading. Incorporating DEMA into your analysis can help capture trends earlier than with simple moving averages.

The Power of Combining Volatility Adjustment with DEMA

By adjusting the weight of the DEMA based on volatility, the VAWDEMA becomes a powerful hybrid indicator. This combination leverages the quick responsiveness of DEMA while dynamically adjusting its sensitivity based on current market volatility. This results in a moving average that is both swift and adaptive, capable of providing more relevant signals for entering and exiting trades.

Core Logic Behind VAWDEMA

The core logic of the VAWDEMA involves calculating the DEMA for a specified period and then adjusting its weighting based on a volatility measure, such as the average true range (ATR) or standard deviation of price changes. This results in a weighted DEMA that reflects both the direction and the volatility of the market, offering insights into potential trend continuations or reversals.

Utilizing the Crossover in a Trading System

The VAWDEMA crossover occurs when two VAWDEMAs of different lengths cross, signaling potential bullish or bearish market conditions. In a trading system, a crossover can be used as a trigger for entry or exit points:

Bullish Signal: When a shorter-period VAWDEMA crosses above a longer-period VAWDEMA, it may indicate an uptrend, suggesting a potential entry point for a long position.

Bearish Signal: Conversely, when a shorter-period VAWDEMA crosses below a longer-period VAWDEMA, it might signal a downtrend, indicating a possible exit point or a short entry.

Incorporating VAWDEMA crossovers into a trading strategy can enhance decision-making by providing timely and adaptive signals that account for both trend direction and market volatility. Traders should combine these signals with other forms of analysis and risk management techniques to develop a well-rounded trading strategy.

Alert Conditions For Trading

alertcondition(vwdema>vwdema , title="VWDEMA Long", message="VWDEMA Long - {{ticker}} - {{interval}}")

alertcondition(vwdema

Volume Liqidations [EagleVSniper]The Volume Liquidations Indicator is designed for traders who want to spot significant liquidation events in the cryptocurrency markets, particularly between spot and futures volumes. This powerful tool auto-detects the trading asset and compares the volume data from both spot and futures markets to highlight potential high-volume liquidation points that can significantly impact price movement. Raw source code owner - tartigradia

Features:

Auto-Detect Functionality: Automatically identifies the current trading asset, providing an option for manual selection for both spot and futures symbols.

Volume Comparison: Calculates the difference between futures and spot volumes within a user-defined timeframe, helping to identify liquidation events.

Customizable Parameters: Offers customizable options for multipliers, lookback periods, and timeframe selection to tailor the indicator to your trading strategy.

Visual Indicators: Displays liquidation volumes as color-coded columns, with green indicating potential long liquidations and red for short liquidations. It also highlights bars that exceed the high-volume threshold, providing a clear visual cue for significant liquidation events.

Spot and Futures Volume MA: Includes optional moving average plots for both spot and futures volumes, allowing for a deeper analysis of market trends.

Highlighting High-Volatility Candles: The indicator uniquely colors candles that reach a predefined volatility threshold, determined by the user-set multiplier. This functionality aims to spotlight moments of significant market volatility, providing traders with immediate visual cues.

Dynamic Ticker Selection: Seamlessly switches between auto and manual ticker selection, providing flexibility for all types of traders.

How to Use:

Setup: Configure the indicator to your preferences. You can choose between automatic or manual ticker selection, set the multiplier for the high-volume threshold, and define the lookback period for the moving average calculation.

Analysis: The indicator plots differences in volume between futures and spot markets as columns on your chart, color-coded to indicate the direction of potential liquidations.

Decision Making: Use the indicator to identify potential liquidation events. High-volume thresholds are highlighted, suggesting significant market movements. Combine this information with other analysis tools to make informed trading decisions.

Debasement Adjusted CAGREquity growth may appear less significant when juxtaposed with the expansion of the money supply. This is because markets tend to adjust prices to reflect changes in money supply almost immediately.

Our indicator offers a unique perspective by adjusting the current ticker price for the M2 money supply and normalizing this data to show the percentage appreciation since the first visible bar on the chart. Users can also select alternative money supply measures, such as the EU-M2, via the indicator's settings.

This approach essentially redefines the price as the "growth of the relative share of the total money supply," providing a novel lens through which to view equity performance.

Additionally, the indicator computes both the Compound Annual Growth Rate (CAGR) and the total growth observed from this adjusted standpoint. These metrics are calculated within the context of the selected time range, adding depth to the analysis.

Although this indicator is compatible with all timeframes, it is primarily designed as a macroeconomic tool. It yields the most meaningful insights when applied to longer-term perspectives, such as weekly or monthly timeframes.

This tool builds upon the foundational work presented in the "Inflation Adjusted Performance Ticker," accessible at Inflation Adjusted Performance Ticker , enhancing its application by normalizing the results and computing CAGR and total growth.

Custom Dual SMADescription

The Custom Dual SMA Indicator is designed for traders who wish to track and compare the moving averages of two different financial instruments simultaneously on the same chart, usually if there is correlation between to different asset such as TQQQ vs SQQQ. This indicator is particularly useful for those who engage in comparative analysis or pairs trading strategies.

Features

Dual Ticker Input: Users can input any two ticker symbols (e.g., stocks, currencies, commodities) to analyze. This flexibility allows for a broad range of comparative analyses across different markets or sectors.

Customizable SMA Length: The indicator provides the option to set the length of the SMA for each ticker symbol independently. This feature is critical for traders who wish to analyze the moving averages over different time periods, depending on their trading strategy or the specific characteristics of the instruments being analyzed.

Overlay on Price Chart: The calculated SMAs are overlaid directly on the price chart, enabling users to easily visualize how the moving averages of the two instruments move in relation to each other and to their respective price actions.

Color-Coded for Clarity: Each SMA is plotted in a different color (red and blue by default), ensuring clear differentiation and easy interpretation at a glance.

Use Case

This indicator is particularly beneficial for:

Comparative Analysis: Traders can compare the performance and trends of two different instruments, observing how their moving averages converge or diverge over time.

Pairs Trading: Those involved in pairs trading can use this tool to identify potential entry and exit points by analyzing the moving averages of two correlated or inversely correlated instruments.

Diversification Analysis: Investors looking to diversify their portfolio can use this indicator to understand the moving average trends of various instruments, helping them make informed decisions about asset allocation.

Summary

The Custom Dual SMA Indicator is a versatile tool for traders and investors who require a comparative view of the moving averages of two different instruments on the same chart. Its customizable nature and ease of use make it suitable for a wide range of trading strategies and market analyses.

Cryptocurrency Cointegration Matrix (SpiritualHealer117)This indicator plots a cointegration matrix for the pairings of 100 cryptocurrencies. The matrix is populated with ADF t-stats (from an ADF-test with 1 lag). An ADF-test (Augmented Dickey-Fuller test) tests the null hypothesis that an AR process has a unit root. If rejected, the alternative hypothesis is usually that the AR process is either stationary or trend-stationary. This model extends upon Lejmer's Cointegration Matrix for forex by enabling the indicator to use cryptocurrency pairs and allows for significantly more pairs to be analyzed using the group selection feature. This indicator arose from collaboration with TradingView user CryptoJuju.

This indicator runs an ADF-test on the residuals (spread) of each pairing (i.e. a cointegration test). It tests if there is a unit root in the spread between the two assets of a pairing. If there is a unit root in the spread, it means the spread varies randomly over time, and any mean reversion in the spread is very hard to predict. By contrast, if a unit root does not exist, the spread (distance between the assets) should remain more or less constant over time, or rise/fall in close to the same rate over time. The more negative the number from an ADF-test, the stronger the rejection of the idea that the spread has a unit root. In statistics, there are different levels which correspond with the confidence level of the test. For this indicator, -3.238 equals a confidence level of 90%, -3.589 equals a confidence level of 95% and -4.375 equals a confidence level of 99% that there is not a unit root. So the colors are based on the confidence level of the test statistic (the t-stat, i.e. the number of the pairing in the matrix). So if the number is greater than -3.238 it is green, if it's between -3.238 and -3.589 it's yellow, if it's between -3.589 and -4.375 it's orange, and if its lower than -4.375 it's red.

There are multiple ways to interpret the results. A strong rejection of the presence of a unit root (i.e. a value of -4.375 or below) is not a guarantee that there is no unit root, or that any of the two alternative hypotheses (that the spread is stationary or trend-stationary) are correct. It only means that in 99% of the cases, if the spread is an AR process, the test is right, and there is no unit root in the spread. Therefore, the results of this test is no guarantee that the result proves one of the alternative solutions. Green therefore means that a unit root cannot be ruled out (which can be interpreted as "the two cryptocurrencies probably don't move together over time"), and red means that a unit root is likely not present (which can be interpreted as "the two cryptocurrencies may move together over time").

One possible way to use this indicator is to make sure you don't trade two pairs that move together at the same time. So basically the idea is that if you already have a trade open in one of the currency pairs of the pairing, only enter a trade in the other currency pair of that pairing if the color is green, or you may be doubling your risk. Alternatively, you could implement this indicator into a pairs trading system, such as a simple strategy where you buy the spread between two cryptocurrencies with a red result when the spread's value drops one standard deviation away from its moving average, and conversely sell when it moves up one standard deviation above the moving average. However, this strategy is not guaranteed to work, since historical data does not guarantee the future.

Specific to this indicator, there are 100 different cryptocurrency tickers which are included in the matrix, and the cointegration matrices between all the tickers can be checked by switching asset group 1 and asset group 2 to different asset groups. The ADF test is computed using a specified length, and if there is insufficient data for the length, the test produces a grayed out box.

NOTE: The indicator can take a while to load since it computes the value of 400 ADF tests each time it is run.

WP_MMThis indicator is set with 3 EMA's:

- EMA9

- EMA20

- EMA50

When EMA9 is up to EMA20 and:

- the distance between them is up to 30 ticks

- both is directional ( diff between current ema and last ema is up to 15 ticks )

the range will be painted in green. And if the EMA 9 is below EMA20 and

the same rules above is true, rthe range will be painted in red

Strengh Candle:

- Candle without huge shadow

- If is bearish minium down shadow

- if is bullish minimum up shadow

OBS: More info inside code comments

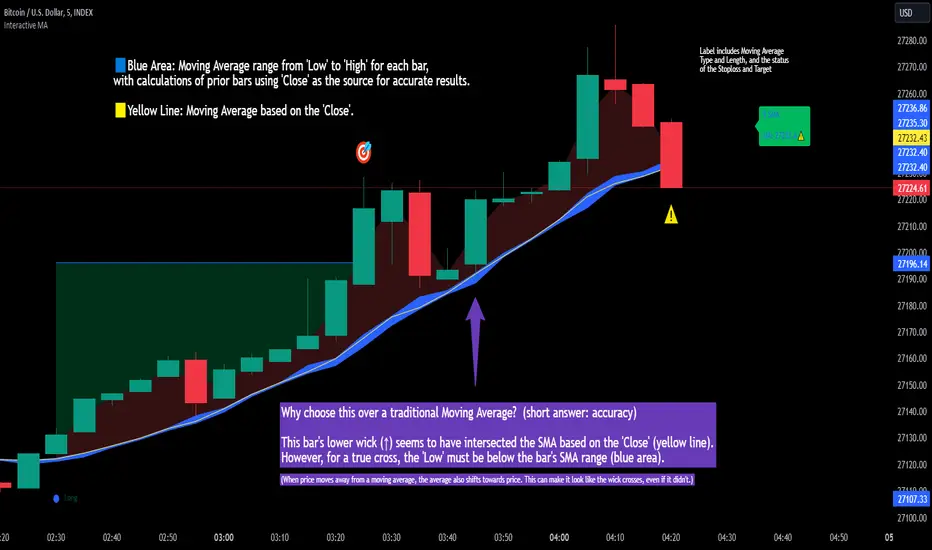

Interactive MA Stop Loss [TANHEF]This indicator is "Interactive." Once added to the chart, you need to click the start point for the moving average stoploss. Dragging it afterward will modify its position.

Why choose this indicator over a traditional Moving Average?

To accurately determine that a wick has crossed a moving average, you must examine the moving average's range on that bar (blue area on this indicator) and ensure the wick fully traverses this area.

When the price moves away from a moving average, the average also shifts towards the price. This can make it look like the wick crossed the average, even if it didn't.

How is the moving average area calculated?

For each bar, the moving average calculation is standard, but when the current bar is involved, its high or low is used instead of the close. For precise results, simply setting the source in a typical moving average calculation to 'Low' or 'High' is not sufficient in calculating the moving average area on a current bar.

Moving Average Options:

Simple Moving Average

Exponential Moving Average

Relative Moving Average

Weighted Moving Average

Indicator Explanation

After adding indicator to chart, you must click on a location to begin an entry.

The moving average type can be set and length modified to adjust the stoploss. An optional profit target may be added.

A symbol is display when the stoploss and profit target are hit. If a position is create that is not valid, "Overlapping MA and Bar" is displayed.

Alerts

'Check' alerts to use within indicator settings (stop hit and/or profit target hit).

Select 'Create Alert'

Set the condition to 'Interactive MA''

Select create.

Alert messages can have additional details using these words in between two Curly (Brace) Brackets:

{{stop}} = MA stop-loss (price)

{{upper}} = Upper MA band (price)

{{lower}} = Lower MA band (price)

{{band}} = Lower or Upper stoploss (word)

{{type}} = Long or Short stop-loss (word)

{{stopdistance}} = Stoploss Distance (%)

{{targetdistance}} = Target Distance (%)

{{starttime}} = Start time of stoploss (day:hour:minute)

{{maLength}} = MA Length (input)

{{maType}} = MA Type (input)

{{target}} = Price target (price)

{{trigger}} = Wick or Close Trigger input (input)

{{ticker}} = Ticker of chart (word)

{{exchange}} = Exchange of chart (word)

{{description}} = Description of ticker (words)

{{close}} = Bar close (price)

{{open}} = Bar open (price)

{{high}} = Bar high (price)

{{low}} = Bar low (price)

{{hl2}} = Bar HL2 (price)

{{volume}} = Bar volume (value)

{{time}} = Current time (day:hour:minute)

{{interval}} = Chart timeframe

{{newline}} = New line for text

I will add further moving averages types in the future. If you suggestions post them below.

Quadratic & Linear Time Series Regression [SS]Hey everyone,

Releasing the Quadratic/Linear Time Series regression indicator.

About the indicator:

Most of you will be familiar with the conventional linear regression trend boxes (see below):

This is an awesome feature in Tradingview and there are quite a few indicators that follow this same principle.

However, because of the exponential and cyclical nature of stocks, linear regression tends to not be the best fit for stock time series data. From my experience, stocks tend to fit better with quadratic (or curvlinear) regression, which there really isn't a lot of resources for.

To put it into perspective, let's take SPX on the 1 month timeframe and plot a linear regression trend from 1930 till now:

You can see that its not really a great fit because of the exponential growth that SPX has endured since the 1930s. However, if we take a quadratic approach to the time series data, this is what we get:

This is a quadratic time series version, extended by up to 3 standard deviations. You can see that it is a bit more fitting.

Quadratic regression can also be helpful for looking at cycle patterns. For example, if we wanted to plot out how the S&P has performed from its COVID crash till now, this is how it would look using a linear regression approach:

But this is how it would look using the quadratic approach:

So which is better?

Both linear regression and quadratic regression are pivotal and important tools for traders. Sometimes, linear regression is more appropriate and others quadratic regression is more appropriate.

In general, if you are long dating your analysis and you want to see the trajectory of a ticker further back (over the course of say, 10 or 15 years), quadratic regression is likely going to be better for most stocks.

If you are looking for short term trades and short term trend assessments, linear regression is going to be the most appropriate.

The indicator will do both and it will fit the linear regression model to the data, which is different from other linreg indicators. Most will only find the start of the strongest trend and draw from there, this will fit the model to whatever period of time you wish, it just may not be that significant.

But, to keep it easy, the indicator will actually tell you which model will work better for the data you are selecting. You can see it in the example in the main chart, and here:

Here we see that the indicator indicates a better fit on the quadratic model.

And SPY during its recent uptrend:

For that, let's take a look at the Quadratic Vs the Linear, to see how they compare:

Quadratic:

Linear:

Functions:

You will see that you have 2 optional tables. The statistics table which shows you:

The R Squared to assess for Variance.

The Correlation to assess for the strength of the trend.

The Confidence interval which is set at a default of 1.96 but can be toggled to adjust for the confidence reading in the settings menu. (The confidence interval gives us a range of values that is likely to contain the true value of the coefficient with a certain level of confidence).

The strongest relationship (quadratic or linear).

Then there is the range table, which shows you the anticipated price ranges based on the distance in standard deviations from the mean.

The range table will also display to you how often a ticker has spent in each corresponding range, whether that be within the anticipated range, within 1 SD, 2 SD or 3 SD.

You can select up to 3 additional standard deviations to plot on the chart and you can manually select the 3 standard deviations you want to plot. Whether that be 1, 2, 3, or 1.5, 2.5 or 3.5, or any combination, you just enter the standard deviations in the settings menu and the indicator will adjust the price targets and plotted bands according to your preferences. It will also count the amount of time the ticker spent in that range based on your own selected standard deviation inputs.

Tips on Use:

This works best on the larger timeframes (1 hour and up), with RTH enabled.

The max lookback is 5,000 candles.

If you want to ascertain a longer term trend (over years to months), its best to adjust your chart timeframe to the weekly and/or monthly perspective.

And that's the indicator! Hopefully you all find it helpful.

Let me know your questions and suggestions below!

Safe trades to all!

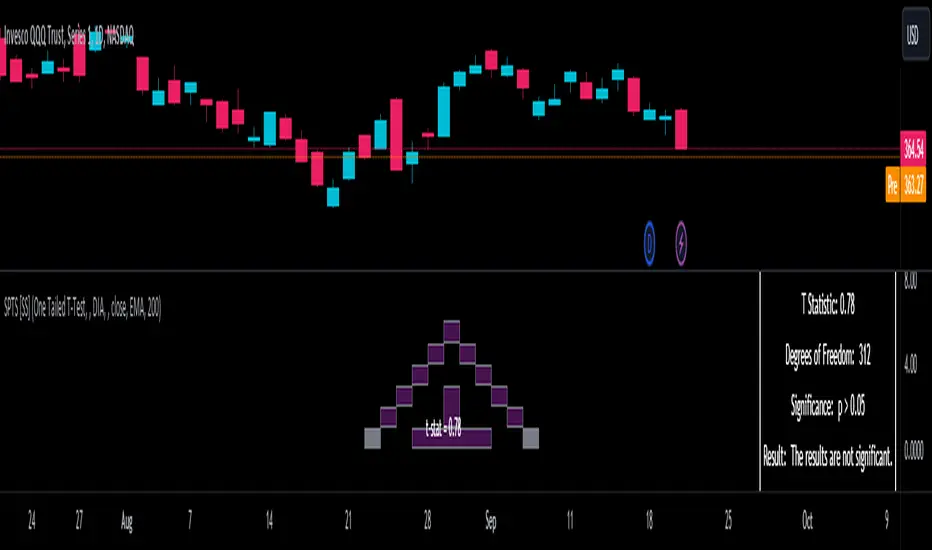

Statistical Package for the Trading Sciences [SS]

This is SPTS.

It stands for Statistical Package for the Trading Sciences.

Its a play on SPSS (Statistical Package for the Social Sciences) by IBM (software that, prior to Pinescript, I would use on a daily basis for trading).

Let's preface this indicator first:

This isn't so much an indicator as it is a project. A passion project really.

This has been in the works for months and I still feel like its incomplete. But the plan here is to continue to add functionality to it and actually have the Pinecoding and Tradingview community contribute to it.

As a math based trader, I relied on Excel, SPSS and R constantly to plan my trades. Since learning a functional amount of Pinescript and coding a lot of what I do and what I relied on SPSS, Excel and R for, I use it perhaps maybe a few times a week.

This indicator, or package, has some of the key things I used Excel and SPSS for on a daily and weekly basis. This also adds a lot of, I would say, fairly complex math functionality to Pinescript. Because this is adding functionality not necessarily native to Pinescript, I have placed most, if not all, of the functionality into actual exportable functions. I have also set it up as a kind of library, with explanations and tips on how other coders can take these functions and implement them into other scripts.

The hope here is that other coders will take it, build upon it, improve it and hopefully share additional functionality that can be added into this package. Hence why I call it a project. Okay, let's get into an overview:

Current Functions of SPTS:

SPTS currently has the following functionality (further explanations will be offered below):

Ability to Perform a One-Tailed, Two-Tailed and Paired Sample T-Test, with corresponding P value.

Standard Pearson Correlation (with functionality to be able to calculate the Pearson Correlation between 2 arrays).

Quadratic (or Curvlinear) correlation assessments.

R squared Assessments.

Standard Linear Regression.

Multiple Regression of 2 independent variables.