Opening Range Breakout (ORB)This is an Opening Range Break indicator. Best if used on a 5 minute chart. It plots the opening 30 minutes high and low of a ticker. (meaning mostly for stocks, options, etfs) and then it alerts a buy signal upon break of opening high and a sell signal upon break of opening low. This is a day trading type of indicator and there is a new opening range everyday.

"文华财经tick价格"に関するスクリプトを検索

Triad Trade MatrixOverview

Triad Trade Matrix is an advanced multi-strategy indicator built using Pine Script v5. It is designed to simultaneously track and display key trading metrics for three distinct trading styles on a single chart:

Swing Trading (Swing Supreme):

This mode captures longer-term trends and is designed for trades that typically span several days. It uses customizable depth and deviation parameters to determine swing signals.

Day Trading (Day Blaze):

This mode focuses on intraday price movements. It generates signals that are intended to be executed within a single trading session. The parameters for depth and deviation are tuned to capture more frequent, shorter-term moves.

Scalping (Scalp Surge):

This mode is designed for very short-term trades where quick entries and exits are key. It uses more sensitive parameters to detect rapid price movements suitable for scalping strategies.

Each trading style is represented by its own merged table that displays real-time metrics. The tables update automatically as new trading signals are generated.

Key Features

Multi-Style Tracking:

Swing Supreme (Large): For swing trading; uses a purple theme.

Day Blaze (Medium): For day trading; uses an orange theme.

Scalp Surge (Small): For scalping; uses a green theme.

Real-Time Metrics:

Each table displays key trade metrics including:

Entry Price: The price at which the trade was entered.

Exit Price: The price at which the previous trade was exited.

Position Size: Calculated as the account size divided by the entry price.

Direction: Indicates whether the trade is “Up” (long) or “Down” (short).

Time: The time when the trade was executed (formatted to hours and minutes).

Wins/Losses: The cumulative number of winning and losing trades.

Current Price & PnL: The current price on the chart and the profit/loss computed relative to the entry price.

Duration: The number of bars that the trade has been open.

History Column: A merged summary column that shows the most recent trade’s details (entry, exit, and result).

Customizability:

Column Visibility: Users can toggle individual columns (Ticker, Timeframe, Entry, Exit, etc.) on or off according to their preference.

Appearance Settings: You can customize the table border width, frame color, header background, and text colors.

History Toggle: The merged history column can be enabled or disabled.

Chart Markers: There is an option to show or hide chart markers (labels and lines) that indicate trade entries and exits on the chart.

Trade History Management:

The indicator maintains a rolling history (up to three recent trades per trading style) and displays the latest summary in the merged table.

This history column provides a quick reference to recent performance.

How It Works

Signal Generation & Trade Metrics

Trade Entry/Exit Calculation:

For each trading style, the indicator uses built-in functions (such as ta.lowestbars and ta.highestbars) to analyze price movements. Based on a customizable "depth" and "deviation" parameter, it determines the point of entry for a trade.

Swing Supreme: Uses larger depth/deviation values to capture swing trends.

Day Blaze: Uses intermediate values for intraday moves.

Scalp Surge: Uses tighter parameters to pick up rapid price changes.

Metrics Update:

When a new trade signal is generated (i.e., when the trade entry price is updated), the indicator calculates:

The current PnL as the difference between the current price and the entry price (or vice versa, depending on the trade direction).

The duration as the number of bars since the trade was opened.

The position size using the formula: accountSize / entryPrice.

History Recording:

Each time a new trade is triggered (i.e., when the entry price is updated), a summary string is created (showing entry, exit, and win/loss status) and appended to the corresponding trade history array. The merged table then displays the latest summary from this history.

Table Display

Merged Table Structure:

Each trading style (Swing Supreme, Day Blaze, and Scalp Surge) is represented by a table that has 15 columns. The columns are:

Trade Type (e.g., Swing Supreme)

Ticker

Timeframe

Entry Price

Exit Price

Position Size

Direction

Time of Entry

Account Size

Wins

Losses

Current Price

Current PnL

Duration (in bars)

History (the latest trade summary)

User Customization:

Through the settings panel, users can choose which columns to display.

If a column is toggled off, its cells will remain blank, allowing traders to focus on the metrics that matter most to them.

Appearance & Themes:

The table headers and cell backgrounds are customizable via color inputs. The trading style names are color-coded:

Swing Supreme (Large): Uses a purple theme.

Day Blaze (Medium): Uses an orange theme.

Scalp Surge (Small): Uses a green theme.

How to Use the Indicator

Add the Indicator to Your Chart:

Once published, add "Triad Trade Matrix" to your TradingView chart.

Configure the Settings:

Adjust the Account Size to match your trading capital.

Use the Depth and Deviation inputs for each trading style to fine-tune the signal sensitivity.

Toggle the Chart Markers on if you want visual entry/exit markers on the chart.

Customize which columns are visible via the column visibility toggles.

Enable or disable the History Column to show the merged trade history in the table.

Adjust the appearance settings (colors, border width, etc.) to suit your chart background and preferences.

Interpret the Tables:

Swing Supreme:

This table shows metrics for swing trades.

Look for changes in entry price, PnL, and trade duration to monitor longer-term moves.

Day Blaze:

This table tracks day trading activity.It will update more frequently, reflecting intraday trends.

Scalp Surge:

This table is dedicated to scalping signals.Use it to see quick entry/exit data and rapid profit/loss changes.

The History column (if enabled) gives you a snapshot of the most recent trade (e.g., "E:123.45 X:124.00 Up Win").

Use allerts:

The indicator includes alert condition for new trade entries(both long and short)for each trading style.

Summary:

Triad Trade Matrix provides an robust,multi-dimensional view of your trading performance across swing trading, day trading, and scalping.

Best to be used whith my other indicators

True low high

Vma Ext_Adv_CustomTbl

This indicator is ideal for traders who wish to monitor multiple trading styles simultaneously, with a clear, technical, and real-time display of performance metrics.

Happy Trading!

ELHAI Futures Trend Checker (ES, NQ, YM)The ELHAI Futures Trend Checker is a powerful TradingView indicator designed for futures traders who want to monitor the trend synchronization of the three major U.S. futures indices:

✅ E-mini S&P 500 (ES1!)

✅ E-mini Nasdaq 100 (NQ1!)

✅ E-mini Dow Jones (YM1!)

This indicator checks whether all three futures indices are bullish or bearish during each candle formation. If one of them is out of sync (e.g., two indices are bullish while one is bearish), the indicator triggers an alert and highlights the background in red, helping traders identify potential market indecision or divergence.

Key Features

📌 Designed for Futures Traders – Focuses on ES, NQ, and YM futures contracts.

📌 Live Market Monitoring – Works in real-time and updates dynamically with each tick.

📌 Bullish/Bearish Trend Confirmation – Detects when all three indices are in sync.

📌 Mismatch Detection – Alerts you when at least one index is out of trend.

📌 Custom Alerts – Set up TradingView alerts to be notified instantly when a trend mismatch occurs.

📌 Visual Background Highlight – A red background warns of a market divergence.

How It Works

The script retrieves open and close prices for ES, NQ, and YM.

Determines whether each futures index is bullish (close > open) or bearish (close < open).

If all three indices are bullish or all are bearish, it remains neutral.

If one index is different, an alert is triggered and the background turns red.

How to Use

Apply the indicator to your TradingView chart.

Choose any timeframe – Works well on intraday, daily, or higher timeframes.

Enable alerts: Go to Alerts → Create Alert, select "Futures Trend Mismatch", and set your preferred alert frequency.

Use alongside other indicators like moving averages, RSI, or MACD for better trade confirmation.

Best Use Cases

✔ Day traders & scalpers – Quickly spot market divergence in live trading.

✔ Swing traders – Identify when futures markets lose synchronization.

✔ Trend followers – Confirm if all major futures markets are aligned before making a move.

Final Notes

This indicator was built for Elhai to provide real-time trend analysis across major U.S. futures indices. Use it as a confirmation tool to improve market timing and decision-making.

TTM FCFF Yield %An indicator that shows the Free Cash Flow yield daily for the underlying ticker. Useful for when you need to screen for ideas, or the news just broke out and you want to make a calculated purchase - rather than buying at whatever price it is at the moment.

Green line tracks daily Free Cash Flow yield to Enterprise Value.

Where Free Cash Flow is defined as = Cashflow from Operations + Depreciation and Amortization (from the income statement) - Capital Expenditure (fixed assets) - Change in Working Capital

And where Enterprise Value is defined as = Market Capitalization + Net Debt

Red line tracks Free Cash Flow of financial year and what FCFF yield does that equate to if the stock current trades at the price right now.

Reminder: When working with international equities. Be mindful of whether they report FQ or FH. For example, France only reports FH, so it's better to use TTM FHFree Cash Flow results. If you didn't toggle FH in the indicator settings, it will automatically set as FQ and it will not show anything.

GLHF

Enhanced SPX and BTC Overlay with EMASPX-BTC Momentum Gauge and EMA Cross Indicator

Thorough Analysis:

• Combined Overlay (Green/Red Line):

o Function: Plots a wide line over the price chart, representing a composite of SPX and BTC dynamics adjusted by volume data.

o Color Coding:

Green: Indicates bullish conditions when the combined value exceeds its 10-period SMA and Bitcoin volume increases.

Red: Signals bearish conditions when the combined value drops below its 10-period SMA and Bitcoin volume decreases.

o Line Characteristics:

Width: Set at 8 for high visibility.

Transparency: 86% for both colors to overlay without obscuring candlesticks.

Scaling: Uses a factor of 0.02446 to amplify movements, making trend changes more noticeable.

• Continuous Bright Red and Green Lines:

o 20-period EMA of Current Ticker (Red):

Purpose: Acts as a medium-term trend indicator, smoothing price data to reflect the asset's general direction over time.

Color: Bright red for easy identification.

Transparency: 60% to keep it visible but not overpowering.

o 5-period EMA of BTC (Green):

Purpose: Provides insights into short-term Bitcoin momentum, capturing rapid changes in market sentiment.

Color: Bright green to distinguish from the red EMA.

Transparency: 30% for high visibility against price movements.

Detailed Analysis of the EMA Cross:

• Crossing Points:

o Bullish Crossover:

Occurs when the 5-period BTC EMA (green) moves above the 20-period EMA of the current ticker (red).

Suggests that Bitcoin's short-term momentum is gaining strength relative to the asset's medium-term trend, potentially signaling an upcoming uptrend or strengthening of an existing one.

o Bearish Crossover:

When the green line falls below the red, it indicates that Bitcoin's immediate momentum is weakening compared to the asset's medium-term trend, which might precede a downtrend or confirm one.

• Early Trade Signals:

o Entry/Exit Points:

These crossovers can guide traders in making timely decisions to enter or exit trades, especially when corroborated by the combined overlay's color.

o Confirmation:

EMA crossovers can confirm trends indicated by the combined overlay. For example, a bullish crossover with a green combined line could validate a buying opportunity.

o Volatility Insights:

The rapid shifts in Bitcoin's 5-period EMA highlight potential volatility spikes, offering an additional layer of market analysis, particularly useful in volatile markets.

• Strategic Use:

o Multi-Market Insight: The script integrates data from both traditional (SPX) and crypto (BTC) markets, allowing for a more comprehensive analysis of market conditions.

o Decision-Making: Provides traders with visual cues for market sentiment, trend direction, and potential reversals, enhancing strategic trading decisions.

o Trend Confirmation: The combination of EMA crossovers and the overlay's color changes offers a multi-faceted approach to trend confirmation or divergence.

In Summary:

• This script merges elements of traditional stock market analysis with cryptocurrency dynamics, utilizing color changes, line thickness, and EMA crossovers to visually communicate market conditions, offering traders a robust tool for analyzing and acting on market movements.

200WMA ScreenerDescription:

This custom indicator helps identify stocks trading below their 200-week moving average (200WMA), a key technical indicator often used to analyze long-term trends. The script calculates the 200WMA using weekly close prices and provides the following features:

Visual Plot: Displays the 200WMA as a smooth line on the chart for easy trend analysis.

Background Highlight: Automatically highlights the chart background when the current price is below the 200WMA, signaling a potential bearish trend or undervalued stock.

Alert System: Includes an alert condition to notify you when a stock trades below its 200WMA, so you never miss an opportunity.

Compatibility: Works across all assets (stocks, forex, crypto) and automatically adapts to the selected ticker.

This script is ideal for traders and investors looking for long-term opportunities, identifying potential trend reversals, or spotting undervalued stocks.

Cash and Carry: Annualized BTC Basis (Parametric)This indicator calculates the annualized BTC basis (premium or discount) between a specified futures contract and a given spot symbol. You can customize the spot ticker, the futures ticker, and the exact expiration date/time. As time moves toward expiration, the annualized yield (basis) will adjust accordingly. Ideal for monitoring potential arbitrage or cash-and-carry opportunities!

Hybrid Adaptive Double Exponential Smoothing🙏🏻 This is HADES (Hybrid Adaptive Double Exponential Smoothing) : fully data-driven & adaptive exponential smoothing method, that gains all the necessary info directly from data in the most natural way and needs no subjective parameters & no optimizations. It gets applied to data itself -> to fit residuals & one-point forecast errors, all at O(1) algo complexity. I designed it for streaming high-frequency univariate time series data, such as medical sensor readings, orderbook data, tick charts, requests generated by a backend, etc.

The HADES method is:

fit & forecast = a + b * (1 / alpha + T - 1)

T = 0 provides in-sample fit for the current datum, and T + n provides forecast for n datapoints.

y = input time series

a = y, if no previous data exists

b = 0, if no previous data exists

otherwise:

a = alpha * y + (1 - alpha) * a

b = alpha * (a - a ) + (1 - alpha) * b

alpha = 1 / sqrt(len * 4)

len = min(ceil(exp(1 / sig)), available data)

sig = sqrt(Absolute net change in y / Sum of absolute changes in y)

For the start datapoint when both numerator and denominator are zeros, we define 0 / 0 = 1

...

The same set of operations gets applied to the data first, then to resulting fit absolute residuals to build prediction interval, and finally to absolute forecasting errors (from one-point ahead forecast) to build forecasting interval:

prediction interval = data fit +- resoduals fit * k

forecasting interval = data opf +- errors fit * k

where k = multiplier regulating intervals width, and opf = one-point forecasts calculated at each time t

...

How-to:

0) Apply to your data where it makes sense, eg. tick data;

1) Use power transform to compensate for multiplicative behavior in case it's there;

2) If you have complete data or only the data you need, like the full history of adjusted close prices: go to the next step; otherwise, guided by your goal & analysis, adjust the 'start index' setting so the calculations will start from this point;

3) Use prediction interval to detect significant deviations from the process core & make decisions according to your strategy;

4) Use one-point forecast for nowcasting;

5) Use forecasting intervals to ~ understand where the next datapoints will emerge, given the data-generating process will stay the same & lack structural breaks.

I advise k = 1 or 1.5 or 4 depending on your goal, but 1 is the most natural one.

...

Why exponential smoothing at all? Why the double one? Why adaptive? Why not Holt's method?

1) It's O(1) algo complexity & recursive nature allows it to be applied in an online fashion to high-frequency streaming data; otherwise, it makes more sense to use other methods;

2) Double exponential smoothing ensures we are taking trends into account; also, in order to model more complex time series patterns such as seasonality, we need detrended data, and this method can be used to do it;

3) The goal of adaptivity is to eliminate the window size question, in cases where it doesn't make sense to use cumulative moving typical value;

4) Holt's method creates a certain interaction between level and trend components, so its results lack symmetry and similarity with other non-recursive methods such as quantile regression or linear regression. Instead, I decided to base my work on the original double exponential smoothing method published by Rob Brown in 1956, here's the original source , it's really hard to find it online. This cool dude is considered the one who've dropped exponential smoothing to open access for the first time🤘🏻

R&D; log & explanations

If you wanna read this, you gotta know, you're taking a great responsability for this long journey, and it gonna be one hell of a trip hehe

Machine learning, apprentissage automatique, машинное обучение, digital signal processing, statistical learning, data mining, deep learning, etc., etc., etc.: all these are just artificial categories created by the local population of this wonderful world, but what really separates entities globally in the Universe is solution complexity / algorithmic complexity.

In order to get the game a lil better, it's gonna be useful to read the HTES script description first. Secondly, let me guide you through the whole R&D; process.

To discover (not to invent) the fundamental universal principle of what exponential smoothing really IS, it required the review of the whole concept, understanding that many things don't add up and don't make much sense in currently available mainstream info, and building it all from the beginning while avoiding these very basic logical & implementation flaws.

Given a complete time t, and yet, always growing time series population that can't be logically separated into subpopulations, the very first question is, 'What amount of data do we need to utilize at time t?'. Two answers: 1 and all. You can't really gain much info from 1 datum, so go for the second answer: we need the whole dataset.

So, given the sequential & incremental nature of time series, the very first and basic thing we can do on the whole dataset is to calculate a cumulative , such as cumulative moving mean or cumulative moving median.

Now we need to extend this logic to exponential smoothing, which doesn't use dataset length info directly, but all cool it can be done via a formula that quantifies the relationship between alpha (smoothing parameter) and length. The popular formulas used in mainstream are:

alpha = 1 / length

alpha = 2 / (length + 1)

The funny part starts when you realize that Cumulative Exponential Moving Averages with these 2 alpha formulas Exactly match Cumulative Moving Average and Cumulative (Linearly) Weighted Moving Average, and the same logic goes on:

alpha = 3 / (length + 1.5) , matches Cumulative Weighted Moving Average with quadratic weights, and

alpha = 4 / (length + 2) , matches Cumulative Weighted Moving Average with cubic weghts, and so on...

It all just cries in your shoulder that we need to discover another, native length->alpha formula that leverages the recursive nature of exponential smoothing, because otherwise, it doesn't make sense to use it at all, since the usual CMA and CMWA can be computed incrementally at O(1) algo complexity just as exponential smoothing.

From now on I will not mention 'cumulative' or 'linearly weighted / weighted' anymore, it's gonna be implied all the time unless stated otherwise.

What we can do is to approach the thing logically and model the response with a little help from synthetic data, a sine wave would suffice. Then we can think of relationships: Based on algo complexity from lower to higher, we have this sequence: exponential smoothing @ O(1) -> parametric statistics (mean) @ O(n) -> non-parametric statistics (50th percentile / median) @ O(n log n). Based on Initial response from slow to fast: mean -> median Based on convergence with the real expected value from slow to fast: mean (infinitely approaches it) -> median (gets it quite fast).

Based on these inputs, we need to discover such a length->alpha formula so the resulting fit will have the slowest initial response out of all 3, and have the slowest convergence with expected value out of all 3. In order to do it, we need to have some non-linear transformer in our formula (like a square root) and a couple of factors to modify the response the way we need. I ended up with this formula to meet all our requirements:

alpha = sqrt(1 / length * 2) / 2

which simplifies to:

alpha = 1 / sqrt(len * 8)

^^ as you can see on the screenshot; where the red line is median, the blue line is the mean, and the purple line is exponential smoothing with the formulas you've just seen, we've met all the requirements.

Now we just have to do the same procedure to discover the length->alpha formula but for double exponential smoothing, which models trends as well, not just level as in single exponential smoothing. For this comparison, we need to use linear regression and quantile regression instead of the mean and median.

Quantile regression requires a non-closed form solution to be solved that you can't really implement in Pine Script, but that's ok, so I made the tests using Python & sklearn:

paste.pics

^^ on this screenshot, you can see the same relationship as on the previous screenshot, but now between the responses of quantile regression & linear regression.

I followed the same logic as before for designing alpha for double exponential smoothing (also considered the initial overshoots, but that's a little detail), and ended up with this formula:

alpha = sqrt(1 / length) / 2

which simplifies to:

alpha = 1 / sqrt(len * 4)

Btw, given the pattern you see in the resulting formulas for single and double exponential smoothing, if you ever want to do triple (not Holt & Winters) exponential smoothing, you'll need len * 2 , and just len * 1 for quadruple exponential smoothing. I hope that based on this sequence, you see the hint that Maybe 4 rounds is enough.

Now since we've dealt with the length->alpha formula, we can deal with the adaptivity part.

Logically, it doesn't make sense to use a slower-than-O(1) method to generate input for an O(1) method, so it must be something universal and minimalistic: something that will help us measure consistency in our data, yet something far away from statistics and close enough to topology.

There's one perfect entity that can help us, this is fractal efficiency. The way I define fractal efficiency can be checked at the very beginning of the post, what matters is that I add a square root to the formula that is not typically added.

As explained in the description of my metric QSFS , one of the reasons for SQRT-transformed values of fractal efficiency applied in moving window mode is because they start to closely resemble normal distribution, yet with support of (0, 1). Data with this interesting property (normally distributed yet with finite support) can be modeled with the beta distribution.

Another reason is, in infinitely expanding window mode, fractal efficiency of every time series that exhibits randomness tends to infinitely approach zero, sqrt-transform kind of partially neutralizes this effect.

Yet another reason is, the square root might better reflect the dimensional inefficiency or degree of fractal complexity, since it could balance the influence of extreme deviations from the net paths.

And finally, fractals exhibit power-law scaling -> measures like length, area, or volume scale in a non-linear way. Adding a square root acknowledges this intrinsic property, while connecting our metric with the nature of fractals.

---

I suspect that, given analogies and connections with other topics in geometry, topology, fractals and most importantly positive test results of the metric, it might be that the sqrt transform is the fundamental part of fractal efficiency that should be applied by default.

Now the last part of the ballet is to convert our fractal efficiency to length value. The part about inverse proportionality is obvious: high fractal efficiency aka high consistency -> lower window size, to utilize only the last data that contain brand new information that seems to be highly reliable since we have consistency in the first place.

The non-obvious part is now we need to neutralize the side effect created by previous sqrt transform: our length values are too low, and exponentiation is the perfect candidate to fix it since translating fractal efficiency into window sizes requires something non-linear to reflect the fractal dynamics. More importantly, using exp() was the last piece that let the metric shine, any other transformations & formulas alike I've tried always had some weird results on certain data.

That exp() in the len formula was the last piece that made it all work both on synthetic and on real data.

^^ a standalone script calculating optimal dynamic window size

Omg, THAT took time to write. Comment and/or text me if you need

...

"Versace Pip-Boy, I'm a young gun coming up with no bankroll" 👻

∞

Gold Friday Anomaly StrategyThis script implements the " Gold Friday Anomaly Strategy ," a well-known historical trading strategy that leverages the gold market's behavior from Thursday evening to Friday close. It is a backtesting-focused strategy designed to assess the historical performance of this pattern. Traders use this anomaly as it captures a recurring market tendency observed over the years.

What It Does:

Entry Condition: The strategy enters a long position at the beginning of the Friday trading session (Thursday evening close) within the defined backtesting period.

Exit Condition: Friday evening close.

Backtesting Controls: Allows users to set custom backtesting periods to evaluate strategy performance over specific date ranges.

Key Features:

Custom Backtest Periods: Easily configurable inputs to set the start and end date of the backtesting range.

Fixed Slippage and Commission Settings: Ensures realistic simulation of trading conditions.

Process Orders on Close: Backtesting is optimized by processing orders at the bar's close.

Important Notes:

Backtesting Only: This script is intended purely for backtesting purposes. Past performance is not indicative of future results.

Live Trading Recommendations: For live trading, it is highly recommended to use limit orders instead of market orders, especially during evening sessions, as market order slippage can be significant.

Default Settings:

Entry size: 10% of equity per trade.

Slippage: 1 tick.

Commission: 0.05% per trade.

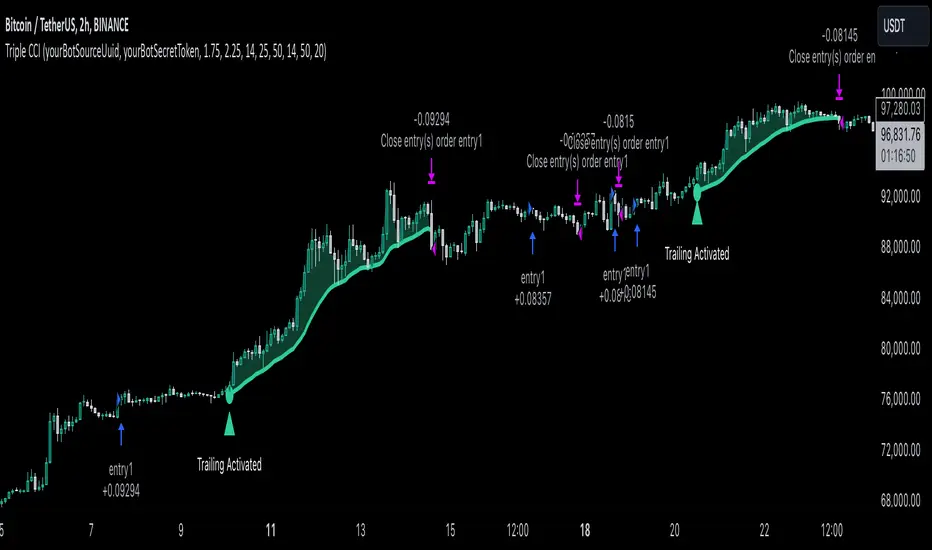

Triple CCI Strategy MFI Confirmed [Skyrexio]Overview

Triple CCI Strategy MFI Confirmed leverages 3 different periods Commodity Channel Index (CCI) indicator in conjunction Money Flow Index (MFI) and Exponential Moving Average (EMA) to obtain the high probability setups. Fast period CCI is used for having the high probability to enter in the direction of short term trend, middle and slow period CCI are used for confirmation, if market now likely in the mid and long-term uptrend. MFI is used to confirm trade with the money inflow/outflow with the high probability. EMA is used as an additional trend filter. Moreover, strategy uses exponential moving average (EMA) to trail the price when it reaches the specific level. More information in "Methodology" and "Justification of Methodology" paragraphs. The strategy opens only long trades.

Unique Features

Dynamic stop-loss system: Instead of fixed stop-loss level strategy utilizes average true range (ATR) multiplied by user given number subtracted from the position entry price as a dynamic stop loss level.

Configurable Trading Periods: Users can tailor the strategy to specific market windows, adapting to different market conditions.

Four layers trade filtering system: Strategy utilizes two different period CCI indicators, MFI and EMA indicators to confirm the signals produced by fast period CCI.

Trailing take profit level: After reaching the trailing profit activation level scrip activate the trailing of long trade using EMA. More information in methodology.

Methodology

The strategy opens long trade when the following price met the conditions:

Fast period CCI shall crossover the zero-line.

Slow and Middle period CCI shall be above zero-lines.

Price shall close above the EMA. Crossover is not obligatory

MFI shall be above 50

When long trade is executed, strategy set the stop-loss level at the price ATR multiplied by user-given value below the entry price. This level is recalculated on every next candle close, adjusting to the current market volatility.

At the same time strategy set up the trailing stop validation level. When the price crosses the level equals entry price plus ATR multiplied by user-given value script starts to trail the price with EMA. If price closes below EMA long trade is closed. When the trailing starts, script prints the label “Trailing Activated”.

Strategy settings

In the inputs window user can setup the following strategy settings:

ATR Stop Loss (by default = 1.75)

ATR Trailing Profit Activation Level (by default = 2.25)

CCI Fast Length (by default = 14, used for calculation short term period CCI)

CCI Middle Length (by default = 25, used for calculation short term period CCI)

CCI Slow Length (by default = 50, used for calculation long term period CCI)

MFI Length (by default = 14, used for calculation MFI

EMA Length (by default = 50, period of EMA, used for trend filtering EMA calculation)

Trailing EMA Length (by default = 20)

User can choose the optimal parameters during backtesting on certain price chart.

Justification of Methodology

Before understanding why this particular combination of indicator has been chosen let's briefly explain what is CCI, MFI and EMA.

The Commodity Channel Index (CCI) is a momentum-based technical indicator that measures the deviation of a security's price from its average price over a specific period. It helps traders identify overbought or oversold conditions and potential trend reversals.

The CCI formula is:

CCI = (Typical Price − SMA) / (0.015 × Mean Deviation)

Typical Price (TP): This is calculated as the average of the high, low, and closing prices for the period.

Simple Moving Average (SMA): This is the average of the Typical Prices over a specific number of periods.

Mean Deviation: This is the average of the absolute differences between the Typical Price and the SMA.

The result is a value that typically fluctuates between +100 and -100, though it is not bounded and can go higher or lower depending on the price movement.

The Money Flow Index (MFI) is a technical indicator that measures the strength of money flowing into and out of a security. It combines price and volume data to assess buying and selling pressure and is often used to identify overbought or oversold conditions. The formula for MFI involves several steps:

1. Calculate the Typical Price (TP):

TP = (high + low + close) / 3

2. Calculate the Raw Money Flow (RMF):

Raw Money Flow = TP × Volume

3. Determine Positive and Negative Money Flow:

If the current TP is greater than the previous TP, it's Positive Money Flow.

If the current TP is less than the previous TP, it's Negative Money Flow.

4. Calculate the Money Flow Ratio (MFR):

Money Flow Ratio = Sum of Positive Money Flow (over n periods) / Sum of Negative Money Flow (over n periods)

5. Calculate the Money Flow Index (MFI):

MFI = 100 − (100 / (1 + Money Flow Ratio))

MFI above 80 can be considered as overbought, below 20 - oversold.

The Exponential Moving Average (EMA) is a type of moving average that places greater weight and significance on the most recent data points. It is widely used in technical analysis to smooth price data and identify trends more quickly than the Simple Moving Average (SMA).

Formula:

1. Calculate the multiplier

Multiplier = 2 / (n + 1) , Where n is the number of periods.

2. EMA Calculation

EMA = (Current Price) × Multiplier + (Previous EMA) × (1 − Multiplier)

This strategy leverages Fast period CCI, which shall break the zero line to the upside to say that probability of short term trend change to the upside increased. This zero line crossover shall be confirmed by the Middle and Slow periods CCI Indicators. At the moment of breakout these two CCIs shall be above 0, indicating that there is a high probability that price is in middle and long term uptrend. This approach increases chances to have a long trade setup in the direction of mid-term and long-term trends when the short-term trend starts to reverse to the upside.

Additionally strategy uses MFI to have a greater probability that fast CCI breakout is confirmed by this indicator. We consider the values of MFI above 50 as a higher probability that trend change from downtrend to the uptrend is real. Script opens long trades only if MFI is above 50. As you already know from the MFI description, it incorporates volume in its calculation, therefore we have another one confirmation factor.

Finally, strategy uses EMA an additional trend filter. It allows to open long trades only if price close above EMA (by default 50 period). It increases the probability of taking long trades only in the direction of the trend.

ATR is used to adjust the strategy risk management to the current market volatility. If volatility is low, we don’t need the large stop loss to understand the there is a high probability that we made a mistake opening the trade. User can setup the settings ATR Stop Loss and ATR Trailing Profit Activation Level to realize his own risk to reward preferences, but the unique feature of a strategy is that after reaching trailing profit activation level strategy is trying to follow the trend until it is likely to be finished instead of using fixed risk management settings. It allows sometimes to be involved in the large movements. It’s also important to make a note, that script uses another one EMA (by default = 20 period) as a trailing profit level.

Backtest Results

Operating window: Date range of backtests is 2022.04.01 - 2024.11.25. It is chosen to let the strategy to close all opened positions.

Commission and Slippage: Includes a standard Binance commission of 0.1% and accounts for possible slippage over 5 ticks.

Initial capital: 10000 USDT

Percent of capital used in every trade: 50%

Maximum Single Position Loss: -4.13%

Maximum Single Profit: +19.66%

Net Profit: +5421.21 USDT (+54.21%)

Total Trades: 108 (44.44% win rate)

Profit Factor: 2.006

Maximum Accumulated Loss: 777.40 USDT (-7.77%)

Average Profit per Trade: 50.20 USDT (+0.85%)

Average Trade Duration: 44 hours

These results are obtained with realistic parameters representing trading conditions observed at major exchanges such as Binance and with realistic trading portfolio usage parameters.

How to Use

Add the script to favorites for easy access.

Apply to the desired timeframe and chart (optimal performance observed on 2h BTC/USDT).

Configure settings using the dropdown choice list in the built-in menu.

Set up alerts to automate strategy positions through web hook with the text: {{strategy.order.alert_message}}

Disclaimer:

Educational and informational tool reflecting Skyrex commitment to informed trading. Past performance does not guarantee future results. Test strategies in a simulated environment before live implementation

US/JP Factor/Sector Performance RankingThis indicator is designed to help you easily understand the strengths and weaknesses of different factors and sectors in the U.S. stock market. It looks at various ETFs, ranks their performance over a specific period (20 days by default), and shows the results visually.

= How the Ranking Works

The best-performing rank is shown as -1, with lower ranks as -2, -3, -4, and so on. This setup makes it easy to see rank order in TradingView’s default view.

If you turn on the “Inverse” setting, ranks will be shown as positive numbers in order (e.g., 1, 2, 3…). In this case, it’s recommended to reverse the TradingView scale for better understanding.

= How the Indicator Reacts to Market Conditions

- Normal Market Conditions

Certain factors or sectors often stay at the top rank. For example, during the rallies at the start of 2024 and in May, the Momentum factor performed well, showing a risk-on market environment.

On the other hand, sectors at the bottom rank also tend to stay in specific positions.

- Market Tops

Capital flows within sectors slow down, and top ranks begin to change frequently. This may suggest a market turning point.

- Bear Markets or High Volatility

Rankings become more chaotic in these conditions. These large changes can help you understand market sentiment and the level of volatility.

= Way of using the Indicator

You can use this indicator in the following ways:

- To apply sector rotation strategies.

- To build positions after volatile markets calm down.

- To take long positions on strong elements (higher ranks) and short positions on weaker ones (lower ranks).

= Things to Keep in Mind

It’s a Lagging Indicator

This indicator calculates rankings using the past 20 days of data. It doesn’t provide signals for the future but is a tool for analyzing past performance. To predict the market, you should combine this with other tools or leading indicators.

However, since trends in capital flows often continue, this indicator can help you spot those trends.

= Customization

This indicator is set up for U.S. and Japanese stock markets. However, you can customize it for other markets by changing the ticker and label description in the script.

==Japanese Description==

このインジケーターは、米国株市場におけるファクターやセクターの強弱を直感的に把握するために設計されています。

各ETFを参照し、特定期間(デフォルトでは20日間)のパフォーマンスを順位付けし、それを視覚的に表示します。

= インジケーターの特徴

- ランク付けの仕様

ランク1位は-1で表され、順位が下がるごとに-2、-3、-4…と減少します。この仕様により、TradingViewの標準状態でランクの高低を直感的に把握できるようにしました。

さらに、Inverse設定をONにすると、1位から順に正の値(例: 1, 2, 3…)で表示されるようになります。この場合、TradingViewのスケールを反転させることを推奨します。

= 市況とインジケーターの動き

- 平常時の市況

特定のファクターやセクターがランク1位を維持することが多いです。

例えば、2024年の年初や同年5月の上昇相場では、Momentumファクターが効果を発揮し、リスクオンの市場環境であったことを示しています。

一方、最下位に位置するセクターも特定の順位を維持する傾向があります。

- 天井圏の市況

セクター内の資金流入や流出が停滞し、上位ランクの変動が起こり始めます。これが市場の転換点を示唆する場合があります。

- 下落相場や荒れた市況

ランク順位が大きく乱れることが特徴です。この変動の大きさは、市況の雰囲気やボラティリティの高さを感じ取る材料として活用できます。

= 活用方法

このインジケーターは以下のような投資戦略に役立てることができます:

- セクターローテーションを活用した投資戦略

- 荒れた相場が落ち着いたタイミングでのポジション構築

- 強い要素(ランク上位)のロング、弱い要素(ランク下位)のショート

= 注意点

- 遅行指標であること

本インジケーターは、過去20日間のデータを基にランクを算出します。そのため、先行的なシグナルを提供するものではなく、過去のパフォーマンスに基づいた分析ツールです。市場を先回りするには、別途先行指標や分析を組み合わせる必要があります。

ただし、特定のファクターやセクターへの資金流入・流出が継続する傾向があるため、これを見極める手助けにはなります。

= カスタマイズについて

このインジケーターは米国・日本株市場に特化しています。ただし、他国のファクターやセクターのETFや指数が利用可能であれば、スクリプト内のtickerとlabel descriptionを変更することでカスタマイズが可能です。

Supertrend StrategyThe Supertrend Strategy was created based on the Supertrend and Relative Strength Index (RSI) indicators, widely respected tools in technical analysis. This strategy combines these two indicators to capture market trends with precision and reliability, looking for optimizing exit levels at oversold or overbought price levels.

The Supertrend indicator identifies trend direction based on price and volatility by using the Average True Range (ATR). The ATR measures market volatility by calculating the average range between an asset’s high and low prices over a set period. It provides insight into price fluctuations, with higher ATR values indicating increased volatility and lower values suggesting stability. The Supertrend Indicator plots a line above or below the price, signaling potential buy or sell opportunities: when the price closes above the Supertrend line, an uptrend is indicated, while a close below the line suggests a downtrend. This line shifts as price movements and volatility levels change, acting as both a trailing stop loss and trend confirmation.

To enhance the Supertrend strategy, the Relative Strength Index (RSI) has been added as an exit criterion. As a momentum oscillator, the RSI indicates overbought (usually above 70) or oversold (usually below 30) conditions. This integration allows trades to close when the asset is overbought or oversold, capturing gains before a possible reversal, even if the percentage take profit level has not been reached. This mechanism aims to prevent losses due to market reversals before the Supertrend signal changes.

### Key Features

1. **Entry criteria**:

- The strategy uses the Supertrend indicator calculated by adding or subtracting a multiple of the ATR from the closing price, depending on the trend direction.

- When the price crosses above the Supertrend line, the strategy signals a long (buy) entry. Conversely, when the price crosses below, it signals a short (sell) entry.

- The strategy performs a reversal if there is an open position and a change in the direction of the supertrend occurs

2. **Exit criteria**:

- Take profit of 30% (default) on the average position price.

- Oversold (≤ 5) or overbought (≥ 95) RSI

- Reversal when there is a change in direction of the Supertrend

3. **No Repainting**:

- This strategy is not subject to repainting, as long as the timeframe configured on your chart is the same as the supertrend timeframe .

4. **Position Sizing by Equity and risk management**:

- This strategy has a default configuration to operate with 35% of the equity. At the time of opening the position, the supertrend line is typically positioned at about 12 to 16% of the entry price. This way, the strategy is putting at risk about 16% of 35% of equity, that is, around 5.6% of equity for each trade. The percentage of equity can be adjusted by the user according to their risk management.

5. **Backtest results**:

- This strategy was subjected to deep backtesting and operations in replay mode, including transaction fees of 0.12%, and slippage of 5 ticks.

- The past results in deep backtest and replay mode were compatible and profitable (Variable results depending on the take profit used, supertrend and RSI parameters). However, it should be noted that few operations were evaluated, since the currency in question has been created for a short time and the frequency of operations is relatively small.

- Past results are no guarantee of future results. The strategy's backtest results may even be due to overfitting with past data.

Default Settings

Chart timeframe: 2h

Supertrend Factor: 3.42

ATR period: 14

Supertrend timeframe: 2 h

RSI timeframe: 15 min

RSI Lenght: 5 min

RSI Upper limit: 95

RSI Lower Limit: 5

Take Profit: 30%

BYBIT:1000000MOGUSDT.P

(Early Test) Weekly Seasonality with Dynamic Kelly Criterion# Enhancing Trading Strategies with the Weekly Seasonality Dynamic Kelly Criterion Indicator

Amidst this pursuit to chase price, a common pitfall emerges: an overemphasis on price movements without adequate attention to risk management, probabilistic analysis, and strategic position sizing. To address these challenges, I developed the **Weekly Seasonality with Dynamic Kelly Criterion Indicator**. It is designed to refocus traders on essential aspects of trading, such as risk management and probabilistic returns, thereby catering to both short-term swing traders and long-term investors aiming for tax-efficient positions.

## The Motivation Behind the Indicator

### Overemphasis on Price: A Common Trading Pitfall

Many traders concentrate heavily on price charts and technical indicators, often neglecting the underlying principles of risk management and probabilistic analysis. This overemphasis on price can lead to:

- **Overtrading:** Making frequent trades based solely on price movements without considering the associated risks.

- **Poor Risk Management:** Failing to set appropriate stop-loss levels or position sizes, increasing the potential for significant losses.

- **Emotional Trading:** Letting emotions drive trading decisions rather than objective analysis, which can result in impulsive and irrational trades.

### The Need for Balanced Focus

To achieve sustained trading success, it is crucial to balance price analysis with robust risk management and probabilistic strategies. Key areas of focus include:

1. **Risk Management:** Implementing strategies to protect capital, such as setting stop-loss orders and determining appropriate position sizes based on risk tolerance.

2. **Probabilistic Analysis:** Assessing the likelihood of various market outcomes to make informed trading decisions.

3. **Swing Trading Percent Returns:** Capitalizing on short- to medium-term price movements by buying assets below their average return and selling them above.

## Introducing the Weekly Seasonality with Dynamic Kelly Criterion Indicator

The **Weekly Seasonality with Dynamic Kelly Criterion Indicator** is designed to integrate these essential elements into a comprehensive tool that aids traders in making informed, risk-aware decisions. Below, we explore the key components and functionalities of this indicator.

### Key Components of the Indicator

1. **Average Return (%)**

- **Definition:** The mean percentage return for each week across multiple years.

- **Purpose:** Serves as a benchmark to identify weeks with above or below-average performance, guiding buy and sell decisions.

2. **Positive Percentage (%)**

- **Definition:** The proportion of weeks that yielded positive returns.

- **Purpose:** Indicates the consistency of positive returns, helping traders gauge the reliability of certain weeks for trading.

3. **Volatility (%)**

- **Definition:** The standard deviation of weekly returns.

- **Purpose:** Measures the variability of returns, providing insights into the risk associated with trading during specific weeks.

4. **Kelly Ratio**

- **Definition:** A mathematical formula used to determine the optimal size of a series of bets to maximize the logarithmic growth of capital.

- **Purpose:** Balances potential returns against risks, guiding traders on the appropriate position size to take.

5. **Adjusted Kelly Fraction**

- **Definition:** The Kelly Ratio adjusted based on user-defined risk tolerance and external factors like Federal Reserve (Fed) stance.

- **Purpose:** Personalizes the Kelly Criterion to align with individual risk preferences and market conditions, enhancing risk management.

6. **Position Size ($)**

- **Definition:** The calculated amount to invest based on the Adjusted Kelly Fraction.

- **Purpose:** Ensures that position sizes are aligned with risk management strategies, preventing overexposure to any single trade.

7. **Max Drawdown (%)**

- **Definition:** The maximum observed loss from a peak to a trough of a portfolio, before a new peak is attained.

- **Purpose:** Assesses the worst-case scenario for losses, crucial for understanding potential capital erosion.

### Functionality and Benefits

- **Weekly Data Aggregation:** Aggregates weekly returns across multiple years to provide a robust statistical foundation for decision-making.

- **Quarterly Filtering:** Allows users to filter weeks based on quarters, enabling seasonality analysis and tailored strategies aligned with specific timeframes.

- **Dynamic Risk Adjustment:** Incorporates the Dynamic Kelly Criterion to adjust position sizes in real-time based on changing risk profiles and market conditions.

- **User-Friendly Visualization:** Presents all essential metrics in an organized Summary Table, facilitating quick and informed decision-making.

## The Origin of the Kelly Criterion and Addressing Its Limitations

### Understanding the Kelly Criterion

The Kelly Criterion, developed by John L. Kelly Jr. in 1956, is a formula used to determine the optimal size of a series of bets to maximize the long-term growth of capital. The formula considers both the probability of winning and the payout ratio, balancing potential returns against the risk of loss.

**Kelly Formula:**

\

Where:

- \( b \) = the net odds received on the wager ("b to 1")

- \( p \) = probability of winning

- \( q \) = probability of losing ( \( q = 1 - p \) )

### The Risk of Ruin

While the Kelly Criterion is effective in optimizing growth, it carries inherent risks:

- **Overbetting:** If the input probabilities or payout ratios are misestimated, the Kelly Criterion can suggest overly aggressive position sizes, leading to significant losses.

- **Assumption of Constant Probabilities:** The criterion assumes that probabilities remain constant, which is rarely the case in dynamic markets.

- **Ignoring External Factors:** Traditional Kelly implementations do not account for external factors such as Federal Reserve rates, margin requirements, or market volatility, which can impact risk and returns.

### Addressing Traditional Limitations

Recognizing these limitations, the **Weekly Seasonality with Dynamic Kelly Criterion Indicator** introduces enhancements to the traditional Kelly approach:

- **Incorporation of Fed Stance:** Adjusts the Kelly Fraction based on the current stance of the Federal Reserve (neutral, dovish, or hawkish), reflecting broader economic conditions that influence market behavior.

- **Margin and Leverage Considerations:** Accounts for margin rates and leverage, ensuring that position sizes remain within manageable risk parameters.

- **Dynamic Adjustments:** Continuously updates position sizes based on real-time risk assessments and probabilistic analyses, mitigating the risk of ruin associated with static Kelly implementations.

## How the Indicator Aids Traders

### For Short-Term Swing Traders

Short-term swing traders thrive on capitalizing over weekly price movements. The indicator aids them by:

- **Identifying Favorable Weeks:** Highlights weeks with above-average returns and favorable volatility, guiding entry and exit points.

- **Optimal Position Sizing:** Utilizes the Adjusted Kelly Fraction to determine the optimal amount to invest, balancing potential returns with risk exposure.

- **Probabilistic Insights:** Provides metrics like Positive Percentage (%) and Kelly Ratio to assess the likelihood of favorable outcomes, enhancing decision-making.

### For Long-Term Tax-Free Investors

This is effectively a drop-in replacement for DCA which uses fixed position size that doesn't change based on market conditions, as a result, it's like catching multiple falling knifes by the blade and smiling with blood on your hand... I don't know about you, but I'd rather juggle by the hilt and look like an actual professional...

Long-term investors, especially those seeking tax-free positions (e.g., through retirement accounts), benefit from:

- **Consistent Risk Management:** Ensures that position sizes are aligned with long-term capital preservation strategies.

- **Seasonality Analysis:** Allows for strategic positioning based on historical performance trends across different weeks and quarters.

- **Dynamic Adjustments:** Adapts to changing market conditions, maintaining optimal risk profiles over extended investment horizons.

### Developers

Please double check the logic and functionality because I think there are a few issue and I need to crowd source solutions and be responsible about the code I publish. If you have corrections, please DM me or leave a respectful comment.

I want to publish this by the end of the year and include other things like highlighting triple witching weeks, adding columns for volume % stats, VaR and CVaR, alpha, beta (to see the seasonal alpha and beta based off a benchmark ticker and risk free rate ticker and other little goodies.

TASC 2024.10 Adaptive Oscillator Threshold█ OVERVIEW

This script introduces a more dynamic approach to generating trading signals using the RSI indicator and a threshold that adapts to price trends and dispersion. This methodology comes from Francesco Bufi's article "Overbought/Oversold Oscillators: Useless Or Just Misused" from the October 2024 edition of TASC's Traders' Tips .

█ CONCEPTS

According to Francesco Bufi's observations, an oscillator-based buy signal should have a threshold that varies with the trend direction: higher during uptrends and lower during downtrends. Additionally, the level should decrease as the distance from the price to its mean increases to reduce signals in volatile conditions. Accordingly, Bufi proposes a formula for an adaptive buy level whose value is proportional to the trend (linear regression slope) and inversely proportional to the typical distance between price and its mean (standard deviation). Traders can apply this method to any oscillator to add adaptivity without modifying the oscillator's calculations, as it's simply an adaptive technique for interpreting the calculated values.

This script demonstrates the application of Bufi's Adaptive Threshold (BAT) in a simple RSI-based strategy and allows users to compare its performance to the traditional fixed-threshold approach. Bufi's observations suggest that using the BAT instead of a static threshold can help improve the backtest performance of oscillator-based systems.

█ DISCLAIMER

This strategy script educates users on the trading systems outlined by the TASC article. By default, it uses 10% of equity as the order size and a slippage amount of 5 ticks. Traders should adjust these settings and the commission amount when using this script.

Futures Risk CalculatorFutures Risk Calculator Script - Description

The Futures Risk Calculator (FRC) is a comprehensive tool designed to help traders effectively manage risk when trading futures contracts. This script allows users to calculate risk/reward ratios directly on the chart by specifying their entry price and stop loss. It's an ideal tool for futures traders who want to quantify their potential losses and gains with precision, based on their trading account size and the number of contracts they trade.

What the Script Does:

1. Risk and Reward Calculation:

The script calculates your total risk in dollars and as a percentage of your account size based on the entry and stop-loss prices you input.

It also calculates two key levels where potential reward (Take Profit 1 and Take Profit 2) can be expected, helping you assess the reward-to-risk ratio for any trade.

2. Customizable Settings:

You can specify the size of your trading account (available $ for Futures trading) and the number of futures contracts you're trading. This allows for tailored risk management that reflects your exact trading conditions.

3. Live Chart Integration:

You add the script to your chart after opening a futures chart in TradingView. Simply click on the chart to set your Entry Price and Stop Loss. The script will instantly calculate and display the risk and reward levels based on the points you set.

Adjusting the entry and stop-loss points later is just as easy: drag and drop the levels directly on the chart, and the risk and reward calculations update automatically.

4. Futures Contract Support:

The script is pre-configured with a list of popular futures symbols (like ES, NQ, CL, GC, and more). If your preferred futures contract isn’t in the list, you can easily add it by modifying the script.

The script uses each symbol’s point value to ensure precise risk calculations, providing you with an accurate dollar risk and potential reward based on the specific contract you're trading.

How to Use the Script:

1. Apply the Script to a Futures Chart:

Open a futures contract chart in TradingView.

Add the Futures Risk Calculator (FRC) script as an indicator.

2. Set Entry and Stop Loss:

Upon applying the script, it will prompt you to select your entry price by clicking the chart where you plan to enter the market.

Next, click on the chart to set your stop-loss level.

The script will then calculate your total risk in dollars and as a percentage of your account size.

3. View Risk, Reward, and (Take Profit):

You can immediately see visual lines representing your entry, stop loss, and the calculated reward-to-risk ratio levels (Take Profit 1 and Take Profit 2).

If you want to adjust the entry or stop loss after plotting them, simply move the points on

the chart, and the script will recalculate everything for you.

4. Configure Account and Contracts:

In the script settings, you can enter your account size and adjust the number of contracts you are trading. These inputs allow the script to calculate risk in monetary terms and as a percentage, making it easier to manage your risk effectively.

5. Understand the Information in the Table:

Once you apply the script, a table will appear in the top-right corner of your chart, providing you with key information about your futures contract and the trade setup. Here's what each field represents:

Account Size: Displays your total account value, which you can set in the script's settings.

Future: Shows the selected futures symbol, along with key details such as its tick size and point value. This gives you a clear understanding of how much one point or tick is worth in dollar terms.

Entry Price: The exact price at which you plan to enter the trade, displayed in green.

Stop Loss Price: The price level where you plan to exit the trade if the market moves against you, shown in red.

Contracts: The number of futures contracts you are trading, which you can adjust in the settings.

Risk: Highlighted in orange, this field shows your total risk in dollars, as well as the percentage risk based on your account size. This is a crucial value to help you stay within your risk tolerance and manage your trades effectively.

RSI Trend Following StrategyOverview

The RSI Trend Following Strategy utilizes Relative Strength Index (RSI) to enter the trade for the potential trend continuation. It uses Stochastic indicator to check is the price is not in overbought territory and the MACD to measure the current price momentum. Moreover, it uses the 200-period EMA to filter the counter trend trades with the higher probability. The strategy opens only long trades.

Unique Features

Dynamic stop-loss system: Instead of fixed stop-loss level strategy utilizes average true range (ATR) multiplied by user given number subtracted from the position entry price as a dynamic stop loss level.

Configurable Trading Periods: Users can tailor the strategy to specific market windows, adapting to different market conditions.

Two layers trade filtering system: Strategy utilizes MACD and Stochastic indicators measure the current momentum and overbought condition and use 200-period EMA to filter trades against major trend.

Trailing take profit level: After reaching the trailing profit activation level script activates the trailing of long trade using EMA. More information in methodology.

Wide opportunities for strategy optimization: Flexible strategy settings allows users to optimize the strategy entries and exits for chosen trading pair and time frame.

Methodology

The strategy opens long trade when the following price met the conditions:

RSI is above 50 level.

MACD line shall be above the signal line

Both lines of Stochastic shall be not higher than 80 (overbought territory)

Candle’s low shall be above the 200 period EMA

When long trade is executed, strategy set the stop-loss level at the price ATR multiplied by user-given value below the entry price. This level is recalculated on every next candle close, adjusting to the current market volatility.

At the same time strategy set up the trailing stop validation level. When the price crosses the level equals entry price plus ATR multiplied by user-given value script starts to trail the price with trailing EMA(by default = 20 period). If price closes below EMA long trade is closed. When the trailing starts, script prints the label “Trailing Activated”.

Strategy settings

In the inputs window user can setup the following strategy settings:

ATR Stop Loss (by default = 1.75)

ATR Trailing Profit Activation Level (by default = 2.25)

MACD Fast Length (by default = 12, period of averaging fast MACD line)

MACD Fast Length (by default = 26, period of averaging slow MACD line)

MACD Signal Smoothing (by default = 9, period of smoothing MACD signal line)

Oscillator MA Type (by default = EMA, available options: SMA, EMA)

Signal Line MA Type (by default = EMA, available options: SMA, EMA)

RSI Length (by default = 14, period for RSI calculation)

Trailing EMA Length (by default = 20, period for EMA, which shall be broken close the trade after trailing profit activation)

Justification of Methodology

This trading strategy is designed to leverage a combination of technical indicators—Relative Strength Index (RSI), Moving Average Convergence Divergence (MACD), Stochastic Oscillator, and the 200-period Exponential Moving Average (EMA)—to determine optimal entry points for long trades. Additionally, the strategy uses the Average True Range (ATR) for dynamic risk management to adapt to varying market conditions. Let's look in details for which purpose each indicator is used for and why it is used in this combination.

Relative Strength Index (RSI) is a momentum indicator used in technical analysis to measure the speed and change of price movements in a financial market. It helps traders identify whether an asset is potentially overbought (overvalued) or oversold (undervalued), which can indicate a potential reversal or continuation of the current trend.

How RSI Works? RSI tracks the strength of recent price changes. It compares the average gains and losses over a specific period (usually 14 periods) to assess the momentum of an asset. Average gain is the average of all positive price changes over the chosen period. It reflects how much the price has typically increased during upward movements. Average loss is the average of all negative price changes over the same period. It reflects how much the price has typically decreased during downward movements.

RSI calculates these average gains and losses and compares them to create a value between 0 and 100. If the RSI value is above 70, the asset is generally considered overbought, meaning it might be due for a price correction or reversal downward. Conversely, if the RSI value is below 30, the asset is considered oversold, suggesting it could be poised for an upward reversal or recovery. RSI is a useful tool for traders to determine market conditions and make informed decisions about entering or exiting trades based on the perceived strength or weakness of an asset's price movements.

This strategy uses RSI as a short-term trend approximation. If RSI crosses over 50 it means that there is a high probability of short-term trend change from downtrend to uptrend. Therefore RSI above 50 is our first trend filter to look for a long position.

The MACD (Moving Average Convergence Divergence) is a popular momentum and trend-following indicator used in technical analysis. It helps traders identify changes in the strength, direction, momentum, and duration of a trend in an asset's price.

The MACD consists of three components:

MACD Line: This is the difference between a short-term Exponential Moving Average (EMA) and a long-term EMA, typically calculated as: MACD Line = 12 period EMA − 26 period EMA

Signal Line: This is a 9-period EMA of the MACD Line, which helps to identify buy or sell signals. When the MACD Line crosses above the Signal Line, it can be a bullish signal (suggesting a buy); when it crosses below, it can be a bearish signal (suggesting a sell).

Histogram: The histogram shows the difference between the MACD Line and the Signal Line, visually representing the momentum of the trend. Positive histogram values indicate increasing bullish momentum, while negative values indicate increasing bearish momentum.

This strategy uses MACD as a second short-term trend filter. When MACD line crossed over the signal line there is a high probability that uptrend has been started. Therefore MACD line above signal line is our additional short-term trend filter. In conjunction with RSI it decreases probability of following false trend change signals.

The Stochastic Indicator is a momentum oscillator that compares a security's closing price to its price range over a specific period. It's used to identify overbought and oversold conditions. The indicator ranges from 0 to 100, with readings above 80 indicating overbought conditions and readings below 20 indicating oversold conditions.

It consists of two lines:

%K: The main line, calculated using the formula (CurrentClose−LowestLow)/(HighestHigh−LowestLow)×100 . Highest and lowest price taken for 14 periods.

%D: A smoothed moving average of %K, often used as a signal line.

This strategy uses stochastic to define the overbought conditions. The logic here is the following: we want to avoid long trades in the overbought territory, because when indicator reaches it there is a high probability that the potential move is gonna be restricted.

The 200-period EMA is a widely recognized indicator for identifying the long-term trend direction. The strategy only trades in the direction of this primary trend to increase the probability of successful trades. For instance, when the price is above the 200 EMA, only long trades are considered, aligning with the overarching trend direction.

Therefore, strategy uses combination of RSI and MACD to increase the probability that price now is in short-term uptrend, Stochastic helps to avoid the trades in the overbought (>80) territory. To increase the probability of opening long trades in the direction of a main trend and avoid local bounces we use 200 period EMA.

ATR is used to adjust the strategy risk management to the current market volatility. If volatility is low, we don’t need the large stop loss to understand the there is a high probability that we made a mistake opening the trade. User can setup the settings ATR Stop Loss and ATR Trailing Profit Activation Level to realize his own risk to reward preferences, but the unique feature of a strategy is that after reaching trailing profit activation level strategy is trying to follow the trend until it is likely to be finished instead of using fixed risk management settings. It allows sometimes to be involved in the large movements.

Backtest Results

Operating window: Date range of backtests is 2023.01.01 - 2024.08.01. It is chosen to let the strategy to close all opened positions.

Commission and Slippage: Includes a standard Binance commission of 0.1% and accounts for possible slippage over 5 ticks.

Initial capital: 10000 USDT

Percent of capital used in every trade: 30%

Maximum Single Position Loss: -3.94%

Maximum Single Profit: +15.78%

Net Profit: +1359.21 USDT (+13.59%)

Total Trades: 111 (36.04% win rate)

Profit Factor: 1.413

Maximum Accumulated Loss: 625.02 USDT (-5.85%)

Average Profit per Trade: 12.25 USDT (+0.40%)

Average Trade Duration: 40 hours

These results are obtained with realistic parameters representing trading conditions observed at major exchanges such as Binance and with realistic trading portfolio usage parameters.

How to Use

Add the script to favorites for easy access.

Apply to the desired timeframe and chart (optimal performance observed on 2h BTC/USDT).

Configure settings using the dropdown choice list in the built-in menu.

Set up alerts to automate strategy positions through web hook with the text: {{strategy.order.alert_message}}

Disclaimer:

Educational and informational tool reflecting Skyrex commitment to informed trading. Past performance does not guarantee future results. Test strategies in a simulated environment before live implementation

VRS (Vegas Reversal Strategy)It is based on the reversal of the price after an accentuated volatility of the previous day. It is tested only on BTC, TF Day, and has an activation value equal to a spike of minimum 2.4% amplitude, a value that I have left in the settings free to be modified if it is found valid for other assets.

In the settings you can change how many of the latest longs or shorts I want to view in the past, colors and various aesthetics.

When the system detects a spike at the end of the day from 2.4% onwards it will signal the direction of Reversal, generating the 3 TP, dotted lines.

Entry into the market must be done at the close of the candle day, unfortunately at night time if you want to enter on the tick.

Stop above/below the spike that generated the condition.

If the Day2 candle closes FULL inside the spike, immediate and early closing of the operation.

There cannot be two consecutive Day events: if you are Long or Short and have taken a stop on the next candle, even if the latter generates another entry, this must not be activated.

TP 1 and 2 are both mandatory at 33% of the position, TP3, based on the current movement, can be considered to be left to run to the bitter end or in any case to structuring confirmations of a slowdown in the price.

Upon reaching TP1 it is mandatory to move the STOP to even.

In the event of the presence of extremely strong directional movements, for example Long direction, an opposite activation, Short, must be done but with reduced capital, on the contrary an activation in the same direction as the trend movement can be done with a surcharge. Always pay attention to Money Management and Risk Management.

Always manage Risk and Money Management in an adequate, technical and sustainable manner in relation to your capital. A fair exposure per transaction is between 1% and 2% of the capital.

4C Data Table SuiteOverview

The 4C Data Table Suite is a versatile TradingView indicator, designed for traders who focus on the critical role of prior bar levels in their strategy. By highlighting the high and low points of previous bars, this tool aids in pinpointing crucial support and resistance zones, which often act as psychological triggers for market participants. The unique feature of this indicator is its dual-color coding: it colors bars green for bullish closes and red for bearish closes in the Prior Bar Table, and for the current timeframe, it highlights whether the current price is above (green) or below (red) these levels.

Concepts

1 — This sophisticated indicator is not just about visual cues; it provides a rich tableau of data including:

• Current timeframe countdown to bar close

• GMT-adjusted clock for precise trade timing

• Real-time updates on market internals and volatility measures such as the NYSE TICK and ATR

2 — The configuration is highly customizable, allowing users to:

• Adjust the table's positioning and text size

• Choose color settings for text, background, and borders to suit their visual preference

• Toggle the display of various data components based on their trading needs

3 — The Prior Bar Table is particularly valuable for:

• Traders using prior bar levels as triggers for trade entries and exits

• Quick visual assessment of market sentiment

• Real-time decision-making supported by dynamic color coding based on current price movements relative to prior highs and lows

Features

• Prior Bar Levels Table: Visualizes high and low levels of prior bars with intuitive color coding, aiding traders in assessing market trends.

• Dynamic Color Coding: Updates colors based on the closure of the previous bar and current price positions relative to the past bar's highs and lows.

• Comprehensive Market Data: Includes a suite of essential data such as market internals, the prior bar’s range, and the latest price information.

• Customizable Visuals: Offers extensive options for customizing the appearance and data presented, ensuring the tool fits seamlessly into any trader's strategy.

How to Use

1. To add the indicator, search for "4C Data Table Suite" under indicators on TradingView and apply it to your chart.

2. Navigate to the indicator settings to customize the display properties, including table position, color schemes, and which data points to display.

3. Utilize the toggles within the "Prior Bar Levels Table" settings to adjust the visibility and behavior of the table, depending on your trading approach.

Limitations

• This indicator is optimized for use on time-based charts and may not perform as intended on tick charts or non-standard timeframes.

• The color coding is based on the closure of bars, which may not always reflect intrabar movements, potentially affecting real-time decision-making in highly volatile markets.

Notes

• Ensure your TradingView interface is set to the correct timezone settings to align the GMT clock accurately.

• The dynamic color updates are designed to provide at-a-glance insights but should be used in conjunction with other analysis tools for best results.

*If you find that the indicator is blocking some of the candles at the bottom of the screen, go to (Chart) Settings, Canvas, and then adjust the Bottom/Top margin by increasing the % Amount.

Thanks

Special thanks to the TradingView community and developers whose feedback and insights have helped refine the functionalities of the 4C Data Table Suite. Your collaborative spirit is what makes continuous improvement possible.

MACD with 1D Stochastic Confirmation Reversal StrategyOverview

The MACD with 1D Stochastic Confirmation Reversal Strategy utilizes MACD indicator in conjunction with 1 day timeframe Stochastic indicators to obtain the high probability short-term trend reversal signals. The main idea is to wait until MACD line crosses up it’s signal line, at the same time Stochastic indicator on 1D time frame shall show the uptrend (will be discussed in methodology) and not to be in the oversold territory. Strategy works on time frames from 30 min to 4 hours and opens only long trades.

Unique Features

Dynamic stop-loss system: Instead of fixed stop-loss level strategy utilizes average true range (ATR) multiplied by user given number subtracted from the position entry price as a dynamic stop loss level.

Configurable Trading Periods: Users can tailor the strategy to specific market windows, adapting to different market conditions.

Higher time frame confirmation: Strategy utilizes 1D Stochastic to establish the major trend and confirm the local reversals with the higher probability.

Trailing take profit level: After reaching the trailing profit activation level scrip activate the trailing of long trade using EMA. More information in methodology.

Methodology

The strategy opens long trade when the following price met the conditions:

MACD line of MACD indicator shall cross over the signal line of MACD indicator.

1D time frame Stochastic’s K line shall be above the D line.

1D time frame Stochastic’s K line value shall be below 80 (not overbought)