Sentiment Heatmap with EMA Sentiment Heatmap with EMA Let’s build a script mini-LuxAlgo-style sentiment heatmap Enhanced Simple Sentiment Heatmap + Right-Side Legend Automatic legend on the right side

Just like professional indicators:

MAX GREED

GREED

NEUTRAL

FEAR

MAX FEAR

✔ Legend stays updated on the last bar

It moves automatically as price moves.

✔ Trend EMA included (optional) 9 EMA → White

20 EMA → Red

50 EMA → Yellow

100 EMA → Blue

200 EMA → Purple Alerts (e.g., “Max Fear – Buy Zone”)

✔ Liquidity line / support-resistance auto zones Full sentiment heatmap (Greed → Fear)

✔ Right-side legend like LuxAlgo

✔ All 5 EMAs added (my colors): EMA trend cloud (9/20, 20/50, 50/200)

Buy/Sell circles based on sentiment reversals Right-side legend: MAX GREED / GREED / NEUTRAL / FEAR / MAX FEAR

5 EMAs:

9 → White

20 → Red

50 → Yellow

100 → Blue

200 → Purple

"科创50成分股"に関するスクリプトを検索

MTF MACD – 1m / 15m / 1D / 1W//@version=6

indicator("MTF MACD – 1m / 15m / 1D / 1W", overlay=false)

// MACD inputs

fastLen = input.int(12, "Fast length")

slowLen = input.int(26, "Slow length")

signalLen = input.int(9, "Signal length")

// Multi-timeframe MACD using built-in ta.macd()

= request.security(syminfo.tickerid, "1", ta.macd(close, fastLen, slowLen, signalLen))

= request.security(syminfo.tickerid, "15", ta.macd(close, fastLen, slowLen, signalLen))

= request.security(syminfo.tickerid, "D", ta.macd(close, fastLen, slowLen, signalLen))

= request.security(syminfo.tickerid, "W", ta.macd(close, fastLen, slowLen, signalLen))

// Plot MACD lines for each timeframe

plot(macd_1m, title="MACD 1m", color=color.red, linewidth=2)

plot(macd_15m, title="MACD 15m", color=color.blue, linewidth=2)

plot(macd_1d, title="MACD 1D", color=color.green, linewidth=2)

plot(macd_1w, title="MACD 1W", color=color.orange, linewidth=2)

// (Optional) you can uncomment these if you also want signals/histograms:

// plot(signal_1m, title="Signal 1m", color=color.new(color.red, 50), style=plot.style_dotted)

// plot(signal_15m, title="Signal 15m", color=color.new(color.blue, 50), style=plot.style_dotted)

// plot(signal_1d, title="Signal 1D", color=color.new(color.green, 50), style=plot.style_dotted)

// plot(signal_1w, title="Signal 1W", color=color.new(color.orange, 50), style=plot.style_dotted)

// plot(hist_1m, title="Hist 1m", color=color.red, style=plot.style_histogram)

// plot(hist_15m, title="Hist 15m", color=color.blue, style=plot.style_histogram)

// plot(hist_1d, title="Hist 1D", color=color.green, style=plot.style_histogram)

// plot(hist_1w, title="Hist 1W", color=color.orange, style=plot.style_histogram)

ENTRY CONFIRMATION V2// This source code is subject to the terms of the Mozilla Public License 2.0 at mozilla.org

// © Zerocapitalmx

//@version=5

indicator(title="ENTRY CONFIRMATION V2", format=format.price, timeframe="", timeframe_gaps=true)

len = input.int(title="RSI Period", minval=1, defval=50)

src = input(title="RSI Source", defval=close)

lbR = input(title="Pivot Lookback Right", defval=5)

lbL = input(title="Pivot Lookback Left", defval=5)

rangeUpper = input(title="Max of Lookback Range", defval=60)

rangeLower = input(title="Min of Lookback Range", defval=5)

plotBull = input(title="Plot Bullish", defval=true)

plotHiddenBull = input(title="Plot Hidden Bullish", defval=false)

plotBear = input(title="Plot Bearish", defval=true)

plotHiddenBear = input(title="Plot Hidden Bearish", defval=false)

bearColor = color.red

bullColor = color.green

hiddenBullColor = color.new(color.green, 80)

hiddenBearColor = color.new(color.red, 80)

textColor = color.white

noneColor = color.new(color.white, 100)

osc = ta.rsi(src, len)

rsiPeriod = input.int(50, minval = 1, title = "RSI Period")

bandLength = input.int(1, minval = 1, title = "Band Length")

lengthrsipl = input.int(1, minval = 0, title = "Fast MA on RSI")

lengthtradesl = input.int(50, minval = 1, title = "Slow MA on RSI")

r = ta.rsi(src, rsiPeriod) // RSI of Close

ma = ta.sma(r, bandLength ) // Moving Average of RSI

offs = (1.6185 * ta.stdev(r, bandLength)) // Offset

fastMA = ta.sma(r, lengthrsipl) // Moving Average of RSI 2 bars back

slowMA = ta.sma(r, lengthtradesl) // Moving Average of RSI 7 bars back

plot(slowMA, "Slow MA", color=color.black, linewidth=1) // Plot Slow MA

plot(osc, title="RSI", linewidth=2, color=color.purple)

hline(50, title="Middle Line", color=#787B86, linestyle=hline.style_dotted)

obLevel = hline(70, title="Overbought", color=#787B86, linestyle=hline.style_dotted)

osLevel = hline(30, title="Oversold", color=#787B86, linestyle=hline.style_dotted)

plFound = na(ta.pivotlow(osc, lbL, lbR)) ? false : true

phFound = na(ta.pivothigh(osc, lbL, lbR)) ? false : true

_inRange(cond) =>

bars = ta.barssince(cond == true)

rangeLower <= bars and bars <= rangeUpper

//------------------------------------------------------------------------------

// Regular Bullish

// Osc: Higher Low

oscHL = osc > ta.valuewhen(plFound, osc , 1) and _inRange(plFound )

// Price: Lower Low

priceLL = low < ta.valuewhen(plFound, low , 1)

bullCond = plotBull and priceLL and oscHL and plFound

plot(

plFound ? osc : na,

offset=-lbR,

title="Regular Bullish",

linewidth=1,

color=(bullCond ? bullColor : noneColor)

)

plotshape(

bullCond ? osc : na,

offset=-lbR,

title="Regular Bullish Label",

text=" EDM ",

style=shape.labelup,

location=location.absolute,

color=bullColor,

textcolor=textColor

)

//------------------------------------------------------------------------------

// Hidden Bullish

// Osc: Lower Low

oscLL = osc < ta.valuewhen(plFound, osc , 1) and _inRange(plFound )

// Price: Higher Low

priceHL = low > ta.valuewhen(plFound, low , 1)

hiddenBullCond = plotHiddenBull and priceHL and oscLL and plFound

plot(

plFound ? osc : na,

offset=-lbR,

title="Hidden Bullish",

linewidth=1,

color=(hiddenBullCond ? hiddenBullColor : noneColor)

)

plotshape(

hiddenBullCond ? osc : na,

offset=-lbR,

title="Hidden Bullish Label",

text=" EDM ",

style=shape.labelup,

location=location.absolute,

color=bullColor,

textcolor=textColor

)

//------------------------------------------------------------------------------

// Regular Bearish

// Osc: Lower High

oscLH = osc < ta.valuewhen(phFound, osc , 1) and _inRange(phFound )

// Price: Higher High

priceHH = high > ta.valuewhen(phFound, high , 1)

bearCond = plotBear and priceHH and oscLH and phFound

plot(

phFound ? osc : na,

offset=-lbR,

title="Regular Bearish",

linewidth=1,

color=(bearCond ? bearColor : noneColor)

)

plotshape(

bearCond ? osc : na,

offset=-lbR,

title="Regular Bearish Label",

text=" EDM ",

style=shape.labeldown,

location=location.absolute,

color=bearColor,

textcolor=textColor

)

//------------------------------------------------------------------------------

// Hidden Bearish

// Osc: Higher High

oscHH = osc > ta.valuewhen(phFound, osc , 1) and _inRange(phFound )

// Price: Lower High

priceLH = high < ta.valuewhen(phFound, high , 1)

hiddenBearCond = plotHiddenBear and priceLH and oscHH and phFound

plot(

phFound ? osc : na,

offset=-lbR,

title="Hidden Bearish",

linewidth=1,

color=(hiddenBearCond ? hiddenBearColor : noneColor)

)

plotshape(

hiddenBearCond ? osc : na,

offset=-lbR,

title="Hidden Bearish Label",

text=" EDM ",

style=shape.labeldown,

location=location.absolute,

color=bearColor,

textcolor=textColor

)

RSI (Custom Background) KDMThis code is a custom version of the RSI (Relative Strength Index) indicator.

Its main purpose is to compare recent price gains and losses to determine whether the market is in an overbought or oversold condition.

30–50 zone (purple tone): represents a weak or pullback area.

50–70 zone (green tone): represents a strengthening or dominant buying area.

Additionally, when the RSI line moves above 70, a green gradient background highlights the overbought region; when it moves below 30, a red gradient background emphasizes the oversold region.

Like the classic RSI, this version is a momentum indicator showing whether the price is losing or gaining strength.

The key difference is the colored background, which allows you to visually identify the RSI zones (e.g., 30–50 weak, 50–70 strong) much faster and more clearly.

TraderDemircan Auto Fibonacci RetracementDescription:

What This Indicator Does:This indicator automatically identifies significant swing high and swing low points within a customizable lookback period and draws comprehensive Fibonacci retracement and extension levels between them. Unlike the manual Fibonacci tool that requires you to constantly redraw levels as price action evolves, this automated version continuously updates the Fibonacci grid based on the most recent major swing points, ensuring you always have current and relevant support/resistance zones displayed on your chart.Key Features:

Automatic Swing Detection: Continuously scans the specified lookback period to find the most significant high and low points, eliminating manual drawing errors

Comprehensive Level Coverage: Plots 16 Fibonacci levels including 7 retracement levels (0.0 to 1.0) and 9 extension levels (1.115 to 3.618)

Top-Down Methodology: Draws from swing high to swing low (right-to-left), following the traditional Fibonacci retracement convention where 100% is at the top

Dual Labeling System: Shows both exact price values and Fibonacci percentages for easy reference

Complete Customization: Individual toggle controls and color selection for each of the 16 levels

Flexible Display Options: Adjust line thickness (1-5), style (solid/dashed/dotted), and extension direction (left/right/both)

Visual Swing Markers: Red diamond at the swing high (starting point) and green diamond at the swing low (ending point)

Optional Trend Line: Connects the two swing points to visualize the overall price movement direction

How It Works:The indicator employs a sophisticated swing point detection algorithm that operates in two stages:Stage 1 - Find the Swing Low (Support Base):

Scans the entire lookback period to identify the lowest low, which becomes the anchor point (0.0 level in traditional retracement terms, though displayed at the bottom of the grid).Stage 2 - Find the Swing High (Resistance Peak):

After identifying the swing low, searches for the highest high that occurred after that low point, establishing the swing range. This creates a valid price movement range for Fibonacci analysis.Fibonacci Calculation Method:

The indicator uses the top-down approach where:

1.0 Level = Swing High (100% retracement, the top)

0.0 Level = Swing Low (0% retracement, the bottom)

Retracement Levels (0.236 to 0.786) = Potential support zones during pullbacks from the high

Extension Levels (1.115 to 3.618) = Potential target zones below the swing low

Formula: Price = SwingHigh - (SwingHigh - SwingLow) × FibonacciLevelThis ensures that 0.0 is at the bottom and extensions (>1.0) plot below the swing low, following standard Fibonacci retracement convention.Fibonacci Levels Explained:Retracement Levels (0.0 - 1.0):

0.0 (Gray): Swing low - the base support level

0.236 (Red): Shallow retracement, first minor support

0.382 (Orange): Moderate retracement, commonly watched support

0.5 (Purple): Psychological midpoint, significant support/resistance

0.618 (Blue - Golden Ratio): The most important retracement level, high-probability reversal zone

0.786 (Cyan): Deep retracement, last defense before full reversal

1.0 (Gray): Swing high - the initial resistance level

Extension Levels (1.115 - 3.618):

1.115 (Green): First extension, minimal downside target

1.272 (Light Green): Minor extension, common profit target

1.414 (Yellow-Green): Square root of 2, mathematical significance

1.618 (Gold - Golden Extension): Primary downside target, most watched extension level

2.0 (Orange-Red): 200% extension, psychological round number

2.382 (Pink): Secondary extension target

2.618 (Purple): Deep extension, major target zone

3.272 (Deep Purple): Extreme extension level

3.618 (Blue): Maximum extension, rare but powerful target

How to Use:For Retracement Trading (Buying Pullbacks in Uptrends):

Wait for price to make a significant move up from swing low to swing high

When price starts pulling back, watch for reactions at key Fibonacci levels

Most common entry zones: 0.382, 0.5, and especially 0.618 (golden ratio)

Enter long positions when price shows reversal signals (candlestick patterns, volume increase) at these levels

Place stop loss below the next Fibonacci level

Target: Return to swing high or higher extension levels

For Extension Trading (Profit Targets):

After price breaks below the swing low (0.0 level), use extensions as profit targets

First target: 1.272 (conservative)

Primary target: 1.618 (golden extension - most commonly reached)

Extended target: 2.618 (for strong trends)

Extreme target: 3.618 (only in powerful trending moves)

For Counter-Trend Trading (Fading Extremes):

When price reaches deep retracements (0.786 or below), look for exhaustion signals

Watch for divergences between price and momentum indicators at these levels

Enter reversal trades with tight stops below the swing low

Target: 0.5 or 0.382 levels on the bounce

For Trend Continuation:

In strong uptrends, shallow retracements (0.236 to 0.382) often hold

Use these as low-risk entry points to join the existing trend

Failure to hold 0.5 suggests weakening momentum

Breaking below 0.618 often indicates trend reversal, not just retracement

Multi-Timeframe Strategy:

Use daily timeframe Fibonacci for major support/resistance zones

Use 4H or 1H Fibonacci for precise entry timing within those zones

Confluence between multiple timeframe Fibonacci levels creates high-probability zones

Example: Daily 0.618 level aligning with 4H 0.5 level = strong support

Settings Guide:Lookback Period (10-500):

Short (20-50): Captures recent swings, more frequent updates, suited for day trading

Medium (50-150): Balanced approach, good for swing trading (default: 100)

Long (150-500): Identifies major market structure, suited for position trading

Higher values = more stable levels but slower to adapt to new trends

Pivot Sensitivity (1-20):

Controls how many candles are required to confirm a swing point

Low (1-5): More sensitive, identifies minor swings (default: 5)

High (10-20): Less sensitive, only major swings qualify

Use higher sensitivity on lower timeframes to filter noise

Individual Level Toggles:

Enable only the levels you actively trade to reduce chart clutter

Common minimalist setup: Show only 0.382, 0.5, 0.618, 1.0, 1.618, 2.618

Comprehensive setup: Enable all levels for maximum information

Visual Customization:

Line Thickness: Thicker lines (3-5) for presentation, thinner (1-2) for trading

Line Style: Solid for primary levels (0.5, 0.618, 1.618), dashed/dotted for secondary

Price Labels: Essential for knowing exact entry/exit prices

Percent Labels: Helpful for quickly identifying which Fibonacci level you're looking at

Extension Direction: Extend right for forward-looking analysis, left for historical context

What Makes This Original:While Fibonacci indicators are common on TradingView, this script's originality comes from:

Intelligent Two-Stage Detection: Unlike simple high/low finders, this uses a sequential approach (find low first, then find the high that occurred after it), ensuring logical price flow representation

Comprehensive Level Set: Includes 16 levels spanning from retracement to extreme extensions, more than most Fibonacci tools

Top-Down Methodology: Properly implements the traditional Fibonacci retracement convention (high to low) rather than the reverse

Automatic Range Validation: Only draws Fibonacci when both swing points are valid and in the correct temporal order

Dual Extension Options: Separate controls for extending lines left (historical context) and right (forward projection)

Smart Label Positioning: Places percentage labels on the left and price labels on the right for clarity

Visual Swing Confirmation: Diamond markers at swing points help users understand why levels are positioned where they are

Important Considerations:

Historical Nature: Fibonacci retracements are based on past price swings; they don't predict future moves, only suggest potential support/resistance

Self-Fulfilling Prophecy: Fibonacci levels work partly because many traders watch them, creating actual support/resistance at those levels

Not All Levels Hold: In strong trends, price may slice through multiple Fibonacci levels without pausing

Context Matters: Fibonacci works best when aligned with other support/resistance (previous highs/lows, moving averages, trendlines)

Volume Confirmation: The most reliable Fibonacci reversals occur with volume spikes at key levels

Dynamic Updates: The levels will redraw as new swing highs/lows form, so don't rely solely on static screenshots

Best Practices:

Don't Trade Blindly: Fibonacci levels are zones, not exact prices. Look for confirmation (candlestick patterns, indicators, volume)

Combine with Price Action: Watch for pin bars, engulfing candles, or doji at key Fibonacci levels

Use Stop Losses: Place stops beyond the next Fibonacci level to give trades room but limit risk

Scale In/Out: Consider entering partial positions at 0.5 and adding more at 0.618 rather than all-in at one level

Check Multiple Timeframes: Daily Fibonacci + 4H Fibonacci convergence = high-probability zone

Respect the 0.618: This golden ratio level is historically the most reliable for reversals

Extensions Need Strong Trends: Don't expect extensions to be hit unless there's clear momentum beyond the swing low

Optimal Timeframes:

Scalping (1-5 minutes): Lookback 20-30, watch 0.382, 0.5, 0.618 only

Day Trading (15m-1H): Lookback 50-100, all retracement levels important

Swing Trading (4H-Daily): Lookback 100-200, focus on 0.5, 0.618, 0.786, and extensions

Position Trading (Daily-Weekly): Lookback 200-500, all levels relevant for long-term planning

Common Fibonacci Trading Mistakes to Avoid:

Wrong Swing Selection: Choosing insignificant swings produces meaningless levels

Premature Entry: Entering as soon as price touches a Fibonacci level without confirmation

Ignoring Trend: Fighting the main trend by buying deep retracements in downtrends

Over-Reliance: Using Fibonacci in isolation without confirming with other technical factors

Static Analysis: Not updating your Fibonacci as market structure evolves

Arbitrary Lookback: Using the same lookback period for all assets and timeframes

Integration with Other Tools:Fibonacci + Moving Averages:

When 0.618 level aligns with 50 or 200 EMA, confluence creates stronger support

Price bouncing from both Fibonacci and MA simultaneously = high-probability trade

Fibonacci + RSI/Stochastic:

Oversold indicators at 0.618 or deeper retracements = strong buy signal

Overbought indicators at swing high (1.0) = potential reversal warning

Fibonacci + Volume Profile:

High-volume nodes aligning with Fibonacci levels create robust support/resistance

Low-volume areas near Fibonacci levels may see rapid price movement through them

Fibonacci + Trendlines:

Fibonacci retracement level + ascending trendline = double support

Breaking both simultaneously confirms trend change

Technical Notes:

Uses ta.lowest() and ta.highest() for efficient swing detection across the lookback period

Implements dynamic line and label arrays for clean redraws without memory leaks

All calculations update in real-time as new bars form

Extension options allow customization without modifying core code

Format.mintick ensures price labels match the symbol's minimum price increment

Tooltip on swing markers shows exact price values for precision

Major exchages total Open interest & Long/Short OI trends📊 Indicator: Major Exchanges Total OI & Long/Short Trends

This Pine Script™ indicator is designed to provide a comprehensive analysis of Open Interest (OI) and Long/Short position trends across major cryptocurrency exchanges (Binance, Bybit, OKX, Bitget, HTX, Deribit). It serves as a powerful tool for traders seeking to understand market liquidity, participant positioning, and overall market sentiment.

🔑 Key Features and Functionalities

Aggregated Multi-Exchange Open Interest (OI):

Consolidates real-time Open Interest data from user-selected major cryptocurrency exchanges.

Provides a unified view of the total OI, offering insights into the collective market liquidity and the aggregate size of participants' open positions.

Visualized Combined OI Candles:

Presents the aggregated total OI data in a candlestick chart format.

Displays the Open, High, Low, and Close of the combined OI, with color variations indicating increases or decreases from the previous period. This enables intuitive visualization of OI trend shifts.

Estimated Long/Short OI and Visualization:

Calculates and visualizes estimated Long and Short position Open Interest based on the total aggregated OI data.

Estimation Logic:

Employs a sophisticated logic that considers both price changes and OI fluctuations to infer the balance between Long and Short positions. For instance, an increase in both price and OI may suggest an accumulation of Long positions, while a price decrease coupled with an OI increase might indicate growing Short positions.

Initial 50:50 Ratio:

The estimation for Long/Short OI begins with an assumption of a 50:50 ratio at the initial data point available for the selected timeframe. This establishes a neutral baseline, from which subsequent price and OI changes drive the divergence and evolution of the estimated Long/Short balance.

Flexible Visualization Options:

Allows users to display Long/Short OI data in either line or candlestick styles, with customizable color schemes. This flexibility aids in clearly discerning bullish or bearish positioning trends.

💡 Development Background

The development of this indicator stems from the critical importance of Open Interest data in the cryptocurrency derivatives market. Recognizing the limitations of analyzing individual exchange OI in isolation, the primary objective was to integrate data from leading exchanges to offer a holistic perspective on market sentiment and overall positioning dynamics.

The inclusion of the Long/Short position estimation feature is crucial for deciphering the specific directional biases of market participants, which is often not evident from raw OI data alone. This enables a deeper understanding of how positions are being accumulated or liquidated, moving beyond simple OI change analysis.

Furthermore, a key design consideration was to leverage the characteristic where the indicator's data start point dynamically adjusts with the chart's timeframe selection. This allows for the analysis of short-term Long/Short trends on shorter timeframes and long-term trends on longer timeframes. This inherent flexibility empowers traders to conduct analyses across various time scales, aligning with their diverse trading strategies.

🚀 Trading Applications

Leveraging Combined Open Interest (OI):

Trend Confirmation: A sustained increase in total OI signifies growing market interest and capital inflow, potentially confirming the strength of an existing trend. Conversely, decreasing OI may suggest diminishing participant interest or widespread position liquidation.

Validation of Price Extremes: If price forms a new high but OI fails to increase or declines, it could signal a potential trend reversal (divergence). Conversely, a sharp increase in OI during a price decline might indicate a surge in short positions or renewed selling pressure.

Identifying Volatility Triggers: Monitoring rapid shifts in OI during significant news events or market catalysts can help assess immediate market reactions and liquidity changes.

📈Utilizing Long/Short OI Trends

Assessing Market Bias: A sustained dominance or rapid increase in Long OI suggests a prevalent bullish sentiment, which could inform decisions to enter or maintain long positions. The inverse scenario indicates bearish sentiment and potential short entry opportunities.

Anticipating Squeezes: The indicator can help identify scenarios conducive to short or long squeezes. Excessive short positioning followed by a price uptick can trigger a short squeeze, leading to rapid price appreciation. Conversely, an oversupply of long positions preceding a price drop can result in a long squeeze and sharp declines.

Divergence Analysis: Divergences between price action and Long/Short OI estimates can signal potential trend reversals. For example, if price is rising but the increase in Long OI slows down or Short OI begins to grow, it may suggest weakening buying pressure.

🕔Timeframe-Specific Trend Analysis:

Shorter Timeframes (e.g., 1m, 5m, 15m): Ideal for identifying short-term shifts in participant positioning, beneficial for day trading and scalping strategies. Provides insights into immediate market reactions to price movements.

Longer Timeframes (e.g., 1h, 4h, Daily): Valuable for evaluating broader positioning trends and the sustainability or potential reversal of medium-to-long-term trends. Offers a macro perspective on Long/Short dynamics, suitable for swing trading or long-term investment strategies.

This indicator integrates complex market data, provides nuanced Long/Short position estimations, and offers multi-timeframe analytical capabilities, empowering traders to make more informed and strategic decisions.

QQQ TimingThis is a trend-following position trading strategy designed for the QQQ and the leveraged ETF QLD (ProShares Ultra QQQ). The primary goal is to capture multi-month holds for maximal profit.

Key Instruments & Performance

The strategy performs best with QLD, which yields far superior results compared to QQQ.

TQQQ (triple-leveraged) results in higher drawdowns and is not the optimal choice.

Important: The system is not intended for use with other indexes, individual stocks, or investments (like crypto or gold), as performance can vary widely.

Buy Signals

The strategy's signals are rooted in the S&P 500 Index (SPX), as testing showed it provides more reliable triggers than using QQQ itself.

Primary Buy Signal (Credit to IBD/Mike Webster): The SPX triggers a buy when its low closes above the 21-day Exponential Moving Average (EMA) for three consecutive days.

Refinement with Downtrend Lines: During corrective or bear periods, results and drawdowns can be significantly improved by incorporating downtrend lines. These lines connect lower highs. The strategy waits for the price to close above a drawn downtrend line before executing a buy. This refinement can modify the primary signal, either by allowing for an earlier entry or, in some cases, completely nullifying a false signal until the trend change proves itself.

Risk Management & Exit Strategy

Initial Buy Risk: A 3.7% stop loss is applied immediately upon the initial entry.

Initial Exit Rule: An exit is required if the QQQ's low drops below the 50-day Simple Moving Average (SMA).

Note: The 3.7% stop often provides protection when the initial buy occurs below the 50-day SMA. However, if QQQ is already trading above its 50-day SMA at the time of the SPX signal (indicating relative strength), historically, it has been better to use the 50-day SMA rule to give the position more room to run.

Trend Exit (Profit-Taking): To stay in a strong trend for the optimal amount of time, the long position is exited when a moving average crossover to the downside is triggered, based around the 107-day Simple Moving Average (SMA).

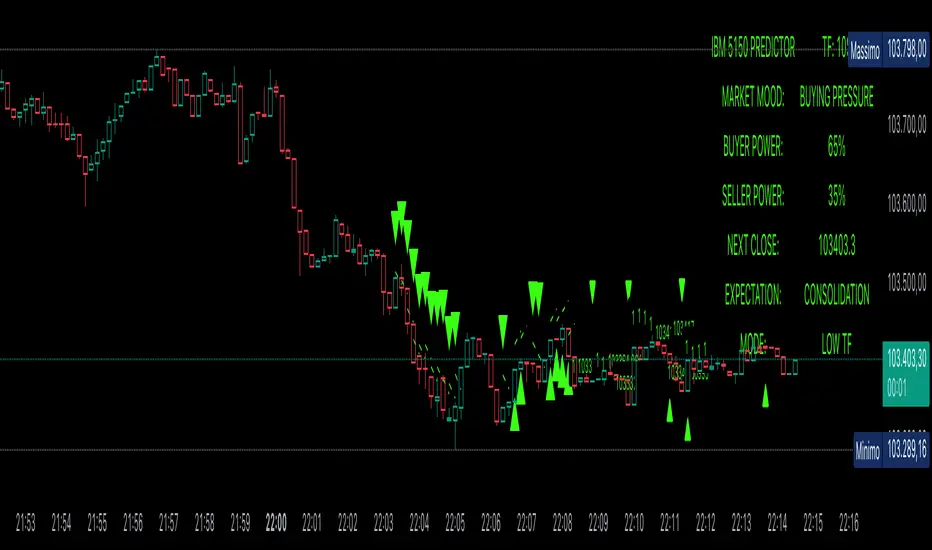

Power Balance ForecasterHey trader buddy! Remember the old IBM 5150 on Wall Street back in the 80s? :) Well, I wanted to pay tribute to it with this retro-style code when MS DOS and CRT screens were the cutting edge of technology...

Analysis of the balance of power between buyers and sellers with price predictions

What This Indicator Does

The Power Balance Forecaster indicator analyzes the relationship between buyer and seller strength to predict future price movements. Here's what it does in detail:

Main Features:

Power Balance Analysis: Calculates real-time percentage of buyer power vs seller power

Price Predictions: Estimates next closing level based on current momentum

Market State Detection: Identifies 5 different market conditions

Visual Signals: Shows directional arrows and price targets

How the Trading Logic Works

Power Balance Calculation:

Analyzes Consecutive Bars - Counts consecutive bullish and bearish bars

Calculates Momentum - Uses ATR-normalized momentum to measure trend strength

Determines Market State - Assigns one of 5 market states based on conditions

Market States:

Bull Control: Strong uptrend (75% buyer power)

Bear Control: Strong downtrend (75% seller power)

Buying Pressure: Bullish pressure (65% buyer power)

Selling Pressure: Bearish pressure (65% seller power)

Balance Area: Market in equilibrium (50/50)

Prediction System:

Bullish Condition: Buyer power > 55% + Positive momentum = Bullish prediction

Bearish Condition: Seller power > 55% + Negative momentum = Bearish prediction

Price Target: Based on ATR multiplied by timeframe factor

Configurable Parameters:

Analysis Sensitivity (5-50): Controls how responsive the indicator is

Low values (5-15): More sensitive, ideal for scalping

High values (30-50): More stable, ideal for swing trading

Table Position: Choose from 9 positions to display the data table

Trading Signals:

Green Triangle ▲: Bullish signal, price expected to increase

Green Triangle ▼: Bearish signal, price expected to decrease

Dashed Line: Shows the price target projection

Label: Displays the exact target value

Recommended Timeframes:

Lower Timeframes (1-15 minutes):

Sensitivity: 10-20

Automatic Low TF mode

Higher Timeframes (1 hour - 1 day):

Sensitivity: 25-40

Automatic High TF mode

Important Notes:

Always use this indicator in combination with:

Market context analysis

Proper risk management

Confirmation from other indicators

Mandatory stop losses

The indicator works best in trending markets and may be less effective during extreme consolidation periods.

Victoria RSI Hybrid Pro – Momentum + Volume + DivergenceConditions and Actions:

RSI > 50 → Bullish regime → Consider Calls

RSI < 50 → Bearish regime → Consider Puts

RSI crosses up → Momentum shift up → Buy confirmation

RSI crosses down → Momentum shift down → Sell confirmation

RSI > 70 → Overbought → Take profits

RSI < 30 → Oversold → Watch for reversal

Bullish divergence → Hidden upward momentum → Reversal watch

Bearish divergence → Hidden downward momentum → Reversal watch

4. Multi-Indicator Confirmation Rules

Combine signals from EMA, SMA, RSI, and Volume to identify high-confidence trades.

Rules:

Triple Green → EMA1>SMA3, RSI>50, Volume Up → Buy Calls / Shares

Triple Red → EMA1 70 + Weak Volume → Exit Calls early

EMA1 flips direction + Strong Volume → Confirm bias immediately

RSI on 1H agrees with main chart → Trend continuation likely

6. Timeframes

Scalps: 1m–5m

Next-Day Options: 15m–1H

Swings: 4H–1D

7. Key Mindset Rules

Patience beats prediction. Wait for confirmations.

Volume confirms conviction, not direction.

If RSI and Overlay disagree → No trade.

Only act when 2 of 3 systems (EMA, RSI, Volume) align.

chart Pattern & Candle sticks Strategy# **XAUUSD Pattern & Candle Strategy - Complete Description**

## **Overview**

This Pine Script indicator is a comprehensive multi-factor trading system specifically designed for **XAUUSD (Gold) scalping and swing trading**. It combines classical technical analysis methods including candlestick patterns, chart patterns, moving averages, and volume analysis to generate high-probability buy/sell signals with automatic stop-loss and take-profit levels.

***

## **Core Components**

### **1. Moving Average System (Triple MA)**

**Purpose:** Identifies trend direction and momentum

- **Fast MA (20-period)** - Short-term price action

- **Medium MA (50-period)** - Intermediate trend

- **Slow MA (200-period)** - Long-term trend direction

**How it works:**

- **Bullish alignment**: MA20 > MA50 > MA200 (all pointing up)

- **Bearish alignment**: MA20 < MA50 < MA200 (all pointing down)

- **Crossover signals**: When Fast MA crosses Medium MA, it triggers buy/sell signals

- **Choice of SMA or EMA**: Adjustable based on preference

**Visual indicators:**

- Blue line = Fast MA

- Orange line = Medium MA

- Light red line = Slow MA

- Green background tint = Bullish trend

- Red background tint = Bearish trend

---

### **2. Candlestick Pattern Recognition (13 Patterns)**

**Purpose:** Identifies reversal and continuation signals based on price action

#### **Bullish Patterns (Signal potential upward moves):**

1. **Hammer** 🔨

- Long lower wick (2x body size)

- Small body at top

- Indicates rejection of lower prices (buyers stepping in)

- Best at support levels

2. **Inverted Hammer**

- Long upper wick

- Small body at bottom

- Shows buying pressure despite initial selling

3. **Bullish Engulfing** 📈

- Green candle completely engulfs previous red candle

- Strong reversal signal

- Body must be 1.2x larger than previous

4. **Morning Star** ⭐

- 3-candle pattern

- Red candle → Small indecision candle → Large green candle

- Powerful reversal at bottoms

5. **Piercing Line** ⚡

- Green candle closes above 50% of previous red candle

- Indicates strong buying interest

6. **Bullish Marubozu**

- Almost no wicks (95% body)

- Very strong bullish momentum

- Body must be 1.3x average size

#### **Bearish Patterns (Signal potential downward moves):**

7. **Shooting Star** 💫

- Long upper wick

- Small body at bottom

- Indicates rejection of higher prices (sellers in control)

- Best at resistance levels

8. **Hanging Man**

- Similar to hammer but appears at top

- Warning of potential reversal down

9. **Bearish Engulfing** 📉

- Red candle completely engulfs previous green candle

- Strong reversal signal

10. **Evening Star** 🌙

- 3-candle pattern (opposite of Morning Star)

- Green → Small → Large red candle

- Powerful top reversal

11. **Dark Cloud Cover** ☁️

- Red candle closes below 50% of previous green candle

- Indicates strong selling pressure

12. **Bearish Marubozu**

- Almost no wicks, pure red body

- Very strong bearish momentum

#### **Neutral Pattern:**

13. **Doji**

- Open and close nearly equal (tiny body)

- Indicates indecision

- Often precedes major moves

**Detection Logic:**

- Compares body size, wick ratios, and position relative to previous candles

- Uses 14-period average body size as reference

- All patterns validated against volume confirmation

***

### **3. Chart Pattern Recognition**

**Purpose:** Identifies major support/resistance and reversal patterns

#### **Patterns Detected:**

**Double Bottom** 📊 (Bullish)

- Two lows at approximately same level

- Indicates strong support

- Breakout above neckline triggers buy signal

- Most reliable at major support zones

**Double Top** 📊 (Bearish)

- Two highs at approximately same level

- Indicates strong resistance

- Breakdown below neckline triggers sell signal

- Most reliable at major resistance zones

**Support & Resistance Levels**

- Automatically plots recent pivot highs (resistance)

- Automatically plots recent pivot lows (support)

- Uses 3-bar strength for validation

- Levels shown as dashed horizontal lines

**Price Action Patterns**

- **Uptrend detection**: Higher highs + higher lows

- **Downtrend detection**: Lower highs + lower lows

- Confirms overall market structure

***

### **4. Volume Analysis**

**Purpose:** Confirms signal strength and filters false signals

**Metrics tracked:**

- **Volume MA (20-period)**: Baseline average volume

- **High volume threshold**: 1.5x the volume average

- **Volume increase**: Current volume > previous 2 bars

**How it's used:**

- All buy/sell signals **require volume confirmation**

- High volume = institutional participation

- Low volume signals are filtered out

- Prevents whipsaw trades during quiet periods

**Visual indicator:**

- Dashboard shows "High" volume in orange when active

- "Normal" shown in gray during low volume

***

### **5. Signal Generation Logic**

**BUY SIGNALS triggered when ANY of these occur:**

1. **Candlestick + Volume**

- Bullish candle pattern detected

- High volume confirmation

- Price above Fast MA

2. **MA Crossover + Volume**

- Fast MA crosses above Medium MA

- High volume confirmation

3. **Double Bottom Breakout**

- Price breaks above support level

- Volume confirmation present

4. **Trend Continuation**

- Uptrend structure intact (higher highs/lows)

- All MAs in bullish alignment

- Price above Fast MA

- Volume confirmation

**SELL SIGNALS triggered when ANY of these occur:**

1. **Candlestick + Volume**

- Bearish candle pattern detected

- High volume confirmation

- Price below Fast MA

2. **MA Crossunder + Volume**

- Fast MA crosses below Medium MA

- High volume confirmation

3. **Double Top Breakdown**

- Price breaks below resistance level

- Volume confirmation present

4. **Trend Continuation**

- Downtrend structure intact (lower highs/lows)

- All MAs in bearish alignment

- Price below Fast MA

- Volume confirmation

***

### **6. Risk Management System**

**Automatic Stop Loss Calculation:**

- Based on ATR (Average True Range) - 14 periods

- **Formula**: Entry price ± (ATR × SL Multiplier)

- **Default multiplier**: 1.5 (adjustable)

- Adapts to market volatility automatically

**Automatic Take Profit Calculation:**

- **Formula**: Entry price ± (ATR × TP Multiplier)

- **Default multiplier**: 2.5 (adjustable)

- **Default Risk:Reward ratio**: 1:1.67

- Higher TP multiplier = more aggressive targets

**Position Management:**

- Tracks ONE position at a time (no pyramiding)

- Automatically closes position when:

- Stop loss is hit

- Take profit is reached

- Opposite MA crossover occurs

- Prevents revenge trading and over-leveraging

**Visual Representation:**

- **Red horizontal line** = Stop Loss level

- **Green horizontal line** = Take Profit level

- Lines remain on chart while position is active

- Automatically disappear when position closes

***

### **7. Visual Elements**

**On-Chart Displays:**

1. **Moving Average Lines**

- Fast MA (Blue, thick)

- Medium MA (Orange, thick)

- Slow MA (Red, thin)

2. **Support/Resistance**

- Green crosses = Support levels

- Red crosses = Resistance levels

3. **Buy/Sell Arrows**

- Large GREEN "BUY" label below bars

- Large RED "SELL" label above bars

4. **Pattern Labels** (Small markers)

- "Hammer", "Bull Engulf", "Morning Star" (green, below bars)

- "Shooting Star", "Bear Engulf", "Evening Star" (red, above bars)

- "Double Bottom" / "Double Top" (blue/orange)

5. **Signal Detail Labels** (Medium size)

- Shows signal reason (e.g., "Bullish Candle", "MA Cross Up")

- Displays Entry, SL, and TP prices

- Color-coded (green for long, red for short)

6. **Background Coloring**

- Light green tint = Bullish MA alignment

- Light red tint = Bearish MA alignment

***

### **8. Information Dashboard**

**Top-right corner table showing:**

| Metric | Description |

|--------|-------------|

| **Position** | Current trade status (LONG/SHORT/None) |

| **MA Trend** | Overall trend direction (Bullish/Bearish/Neutral) |

| **Volume** | Current volume status (High/Normal) |

| **Pattern** | Last detected candlestick pattern |

| **ATR** | Current volatility measurement |

**Purpose:**

- Quick at-a-glance market assessment

- Real-time position tracking

- No need to check multiple indicators

***

### **9. Alert System**

**Complete alert coverage for:**

✅ **Entry Alerts**

- "Buy Signal" - Triggers when buy conditions met

- "Sell Signal" - Triggers when sell conditions met

✅ **Exit Alerts**

- "Long TP Hit" - Take profit reached on long position

- "Long SL Hit" - Stop loss triggered on long position

- "Short TP Hit" - Take profit reached on short position

- "Short SL Hit" - Stop loss triggered on short position

**How to use:**

1. Click "Create Alert" button

2. Select desired alert from dropdown

3. Set notification method (popup, email, SMS, webhook)

4. Never miss a trade opportunity

***

## **Recommended Settings**

### **For Scalping (Quick trades):**

- **Timeframe**: 5-minute

- **Fast MA**: 9

- **Medium MA**: 21

- **Slow MA**: 50

- **SL Multiplier**: 1.0

- **TP Multiplier**: 2.0

- **Volume Threshold**: 1.5x

### **For Swing Trading (Longer holds):**

- **Timeframe**: 1-hour or 4-hour

- **Fast MA**: 20

- **Medium MA**: 50

- **Slow MA**: 200

- **SL Multiplier**: 2.0

- **TP Multiplier**: 3.0

- **Volume Threshold**: 1.3x

### **Best Trading Hours for XAUUSD:**

- **Asian Session**: 00:00 - 08:00 GMT (lower volatility)

- **London Session**: 08:00 - 16:00 GMT (high volatility) ⭐

- **New York Session**: 13:00 - 21:00 GMT (highest volume) ⭐

- **London-NY Overlap**: 13:00 - 16:00 GMT (BEST for scalping) 🔥

***

## **How to Use This Strategy**

### **Step 1: Setup**

1. Open TradingView

2. Load XAUUSD chart

3. Select timeframe (5m, 15m, 1H, or 4H)

4. Add indicator from Pine Editor

5. Adjust settings based on your trading style

### **Step 2: Wait for Signals**

- Watch for GREEN "BUY" or RED "SELL" labels

- Check the signal reason in the detail label

- Verify dashboard shows favorable conditions

- Confirm volume is "High" (not required but preferred)

### **Step 3: Enter Trade**

- Enter at market or limit order near signal price

- Note the displayed Entry, SL, and TP prices

- Set your broker's SL/TP to match indicator levels

### **Step 4: Manage Position**

- Watch for SL/TP lines on chart

- Monitor dashboard for trend changes

- Exit manually if opposite MA crossover occurs

- Let SL/TP do their job (don't move them!)

### **Step 5: Review & Learn**

- Track win rate over 20+ trades

- Adjust multipliers if needed

- Note which patterns work best for you

- Refine entry timing

***

## **Key Advantages**

✅ **Multi-confirmation approach** - Reduces false signals significantly

✅ **Automatic risk management** - No manual calculation needed

✅ **Adapts to volatility** - ATR-based SL/TP adjusts to market conditions

✅ **Volume filtered** - Ensures institutional participation

✅ **Visual clarity** - Easy to understand at a glance

✅ **Complete alert system** - Never miss opportunities

✅ **Pattern education** - Learn patterns as they appear

✅ **Works on all timeframes** - Scalping to swing trading

***

## **Limitations & Considerations**

⚠️ **Not a holy grail** - No strategy wins 100% of trades

⚠️ **Requires practice** - Demo trade first to understand signals

⚠️ **Market conditions matter** - Works best in trending or volatile markets

⚠️ **News events** - Avoid trading during major economic releases

⚠️ **Slippage on 5m** - Fast markets may have execution delays

⚠️ **Pattern subjectivity** - Some patterns may trigger differently than expected

***

## **Risk Management Rules**

1. **Never risk more than 1-2% per trade**

2. **Maximum 3 positions per day** (avoid overtrading)

3. **Don't trade during major news** (NFP, FOMC, etc.)

4. **Use proper position sizing** (0.01 lot per $100 for micro accounts)

5. **Keep trade journal** (track patterns, win rate, mistakes)

6. **Stop trading after 3 consecutive losses** (psychological reset)

7. **Don't move stop loss further away** (accept losses)

8. **Take partial profits** at 1:1 R:R if desired

***

## **Expected Performance**

**Realistic expectations:**

- **Win rate**: 50-65% (depending on market conditions and timeframe)

- **Risk:Reward**: 1:1.67 default (adjustable to 1:2 or 1:3)

- **Signals per day**: 3-8 on 5m, 1-3 on 1H

- **Best months**: High volatility periods (news events, economic uncertainty)

- **Drawdowns**: Expect 3-5 losing trades in a row occasionally

***

## **Customization Options**

All inputs are adjustable in settings panel:

**Moving Averages:**

- Type (SMA or EMA)

- All three period lengths

**Volume:**

- Volume MA length

- High volume multiplier threshold

**Chart Patterns:**

- Pattern strength (bars for pivot detection)

- Show/hide pattern labels

**Risk Management:**

- ATR period

- Stop loss multiplier

- Take profit multiplier

**Display:**

- Toggle pattern labels

- Customize colors (in code)

***

## **Conclusion**

This is a **professional-grade, multi-factor trading system** that combines the best of classical technical analysis with modern risk management. It's designed to give clear, actionable signals while automatically handling the complex calculations of stop loss and take profit levels.

**Best suited for traders who:**

- Understand basic technical analysis

- Can follow rules consistently

- Prefer systematic approach over gut feeling

- Want visual confirmation before entering trades

- Value proper risk management

**Start with demo trading** for at least 20-30 trades to understand how the signals work in different market conditions. Once comfortable and profitable on demo, transition to live trading with minimal risk per trade.

Happy trading! 📈🎯

MCL RSI Conflux v2.5 — Multi-Timeframe Momentum & Z-Score Full Description

Overview

The MCL RSI Conflux v2.5 is a multi-timeframe momentum model that integrates daily, weekly, and monthly RSI values into a unified composite. It extends the classical RSI framework with adaptive overbought/oversold thresholds and statistical normalization (Z-score confluence).

This combination allows traders to visualize cross-timeframe alignment, identify synchronized momentum shifts, and detect exhaustion zones with higher statistical confidence.

Methodology

The script extracts RSI data from three major time horizons:

Daily RSI (short-term momentum)

Weekly RSI (intermediate trend)

Monthly RSI (macro bias)

Each RSI is optionally smoothed, weighted, and aggregated into a Composite RSI.

A Z-score transformation then measures how far each RSI deviates from its historical mean, revealing when momentum strength is statistically extreme or aligned across timeframes.

Key Features

Multi-Timeframe RSI Engine – Computes RSI across D/W/M intervals with individual weighting controls.

Adaptive Overbought/Oversold Bands – Automatically adjusts OB/OS thresholds based on rolling volatility (standard deviation of daily RSI).

Composite RSI Score – Weighted consensus RSI that represents total market momentum.

Z-Score Confluence Analysis – Identifies when all three timeframes are statistically synchronized.

Z-Composite Histogram – Displays aggregated Z-score strength around the midline (50).

Divergence Detection – Flags confirmed pivot-based bull and bear divergences on the daily RSI.

Dynamic Gradient Background – Shifts from red to green based on composite momentum regime.

Customizable Control Panel – Displays RSI values, Z-scores, state, and adaptive bands for each timeframe.

Integrated Alerts – For crossovers, risk-on/off thresholds, alignment, and Z-confluence events.

Interpretation

All RSI values above 50: multi-timeframe bullish alignment.

All RSI values below 50: multi-timeframe bearish alignment.

Composite RSI > 60: risk-on environment; momentum expansion.

Composite RSI < 45: risk-off environment; momentum contraction.

Adaptive OB/OS hits: potential exhaustion or mean reversion setup.

Green Z-ribbon: all Z-scores positive and aligned (statistical confirmation).

Red Z-ribbon: all Z-scores negative and aligned (broad market weakness).

Divergences: short-term warning signals against the prevailing momentum bias.

Practical Application

Use the Composite RSI as a global momentum gauge for position bias.

Trade only in the direction of higher-timeframe alignment (avoid countertrend RSI).

Combine Z-ribbon confirmation with Composite RSI crosses to filter noise.

Use divergence labels and adaptive thresholds for risk reduction or exit timing.

Ideal for swing traders and macro momentum models seeking trend synchronization filters.

Recommended Settings

Market Mode k-Band Lookback Use Case

Stocks / ETFs Adaptive 0.85 200 Medium-term rotation filter

Crypto Adaptive 1.00 150 Volatility-responsive swing filter

Commodities Fixed 70/30 100 Mean reversion model

Alerts Included

Daily RSI crossed above/below Weekly RSI

Composite RSI > Risk-On threshold

Composite RSI < Risk-Off threshold

All RSI aligned above/below 50

Z-Score Conformity (All positive or all negative)

Overbought/Oversold triggers

Author’s Note

This indicator was designed for research and systematic confluence analysis within Mongoose Capital Labs.

It is not financial advice and should be used in combination with independent risk assessment, volume confirmation, and higher-timeframe context.

3D Institutional Battlefield [SurgeGuru]Professional Presentation: 3D Institutional Flow Terrain Indicator

Overview

The 3D Institutional Flow Terrain is an advanced trading visualization tool that transforms complex market structure into an intuitive 3D landscape. This indicator synthesizes multiple institutional data points—volume profiles, order blocks, liquidity zones, and voids—into a single comprehensive view, helping you identify high-probability trading opportunities.

Key Features

🎥 Camera & Projection Controls

Yaw & Pitch: Adjust viewing angles (0-90°) for optimal perspective

Scale Controls: Fine-tune X (width), Y (depth), and Z (height) dimensions

Pro Tip: Increase Z-scale to amplify terrain features for better visibility

🌐 Grid & Surface Configuration

Resolution: Adjust X (16-64) and Y (12-48) grid density

Visual Elements: Toggle surface fill, wireframe, and node markers

Optimization: Higher resolution provides more detail but requires more processing power

📊 Data Integration

Lookback Period: 50-500 bars of historical analysis

Multi-Source Data: Combine volume profile, order blocks, liquidity zones, and voids

Weighted Analysis: Each data source contributes proportionally to the terrain height

How to Use the Frontend

💛 Price Line Tracking (Your Primary Focus)

The yellow price line is your most important guide:

Monitor Price Movement: Track how the yellow line interacts with the 3D terrain

Identify Key Levels: Watch for these critical interactions:

Order Blocks (Green/Red Zones):

When yellow price line enters green zones = Bullish order block

When yellow price line enters red zones = Bearish order block

These represent institutional accumulation/distribution areas

Liquidity Voids (Yellow Zones):

When yellow price line enters yellow void areas = Potential acceleration zones

Voids indicate price gaps where minimal trading occurred

Price often moves rapidly through voids toward next liquidity pool

Terrain Reading:

High Terrain Peaks: High volume/interest areas (support/resistance)

Low Terrain Valleys: Low volume areas (potential breakout zones)

Color Coding:

Green terrain = Bullish volume dominance

Red terrain = Bearish volume dominance

Purple = Neutral/transition areas

📈 Volume Profile Integration

POC (Point of Control): Automatically marks highest volume level

Volume Bins: Adjust granularity (10-50 bins)

Height Weight: Control how much volume affects terrain elevation

🏛️ Order Block Detection

Detection Length: 5-50 bar lookback for block identification

Strength Weighting: Recent blocks have greater impact on terrain

Candle Body Option: Use full candles or body-only for block definition

💧 Liquidity Zone Tracking

Multiple Levels: Track 3-10 key liquidity zones

Buy/Sell Side: Different colors for bid/ask liquidity

Strength Decay: Older zones have diminishing terrain impact

🌊 Liquidity Void Identification

Threshold Multiplier: Adjust sensitivity (0.5-2.0)

Height Amplification: Voids create significant terrain depressions

Acceleration Zones: Price typically moves quickly through void areas

Practical Trading Application

Bullish Scenario:

Yellow price line approaches green order block terrain

Price finds support in elevated bullish volume areas

Terrain shows consistent elevation through key levels

Bearish Scenario:

Yellow price line struggles at red order block resistance

Price falls through liquidity voids toward lower terrain

Bearish volume peaks dominate the landscape

Breakout Setup:

Yellow price line consolidates in flat terrain

Minimal resistance (low terrain) in projected direction

Clear path toward distant liquidity zones

Pro Tips

Start Simple: Begin with default settings, then gradually customize

Focus on Yellow Line: Your primary indicator of current price position

Combine Timeframes: Use the same terrain across multiple timeframes for confluence

Volume Confirmation: Ensure terrain peaks align with actual volume spikes

Void Anticipation: When price enters voids, prepare for potential rapid movement

Order Blocks & Voids Architecture

Order Blocks Calculation

Trigger: Price breaks fractal swing points

Bullish OB: When close > swing high → find lowest low in lookback period

Bearish OB: When close < swing low → find highest high in lookback period

Strength: Based on price distance from block extremes

Storage: Global array maintains last 50 blocks with FIFO management

Liquidity Voids Detection

Trigger: Price gaps exceeding ATR threshold

Bull Void: Low - high > (ATR200 × multiplier)

Bear Void: Low - high > (ATR200 × multiplier)

Validation: Close confirms gap direction

Storage: Global array maintains last 30 voids

Key Design Features

Real-time Updates: Calculated every bar, not just on last bar

Global Persistence: Arrays maintain state across executions

FIFO Management: Automatic cleanup of oldest entries

Configurable Sensitivity: Adjustable lookback periods and thresholds

Scientific Testing Framework

Hypothesis Testing

Primary Hypothesis: 3D terrain visualization improves detection of institutional order flow vs traditional 2D charts

Testable Metrics:

Prediction Accuracy: Does terrain structure predict future support/resistance?

Reaction Time: Faster identification of key levels vs conventional methods

False Positive Reduction: Lower rate of failed breakouts/breakdowns

Control Variables

Market Regime: Trending vs ranging conditions

Asset Classes: Forex, equities, cryptocurrencies

Timeframes: M5 to H4 for intraday, D1 for swing

Volume Conditions: High vs low volume environments

Data Collection Protocol

Terrain Features to Quantify:

Slope gradient changes at price inflection points

Volume peak clustering density

Order block terrain elevation vs subsequent price action

Void depth correlation with momentum acceleration

Control Group: Traditional support/resistance + volume profile

Experimental Group: 3D Institutional Flow Terrain

Statistical Measures

Signal-to-Noise Ratio: Terrain features vs random price movements

Lead Time: Terrain formation ahead of price confirmation

Effect Size: Performance difference between groups (Cohen's d)

Statistical Power: Sample size requirements for significance

Validation Methodology

Blind Testing:

Remove price labels from terrain screenshots

Have traders identify key levels from terrain alone

Measure accuracy vs actual price action

Backtesting Framework:

Automated terrain feature extraction

Correlation with future price reversals/breakouts

Monte Carlo simulation for significance testing

Expected Outcomes

If hypothesis valid:

Significant improvement in level prediction accuracy (p < 0.05)

Reduced latency in institutional level identification

Higher risk-reward ratios on terrain-confirmed trades

Research Questions:

Does terrain elevation reliably indicate institutional interest zones?

Are liquidity voids statistically significant momentum predictors?

Does multi-timeframe terrain analysis improve signal quality?

How does terrain persistence correlate with level strength?

LuxAlgo BigBeluga hapharmonic

🔥 QUANT MOMENTUM SKORQUANT MOMENTUM SCORE – Description (EN)

Summary: This indicator fuses Price ROC, RSI, MACD, Trend Strength (ADX+EMA) and Volume into a single 0-100 “Momentum Score.” Guide bands (50/60/70/80) and ready-to-use alert conditions are included.

How it works

Price Momentum (ROC): Rate of change normalized to 0-100.

RSI Momentum: RSI treated as a momentum proxy and mapped to 0-100.

MACD Momentum: MACD histogram normalized to capture acceleration.

Trend Strength: ADX is direction-aware (DI+ vs DI–) and blended with EMA state (above/below) to form a combined trend score.

Volume Momentum: Volume relative to its moving average (ratio-based).

Weighting: All five components are weighted, auto-normalized, and summed into the final 0-100 score.

Visuals & Alerts: Score line with 50/60/70/80 guides; threshold-cross alerts for High/Strong/Ultra-Strong regimes.

Inputs, weights and thresholds are configurable; total weights are normalized automatically.

How to use

Timeframes: Works on any timeframe—lower TFs react faster; higher TFs reduce noise.

Reading the score:

<50: Weak momentum

50-60: Transition

60-70: Moderate-Strong (potential acceleration)

≥70: Strong, ≥80: Ultra Strong

Practical tip: Use it as a filter, not a stand-alone signal. Combine score breakouts with market structure/trend context (e.g., pullback-then-re-acceleration) to improve selectivity.

Disclaimer: This is not financial advice; past performance does not guarantee future results.

TrendFlowTrendFlow is a visual trend analysis tool that helps identify changes in market direction and momentum.

It uses three exponential moving averages (EMA 21, EMA 50, and EMA 200) to define short-, medium-, and long-term trend structure.

A dynamic color fill highlights the relationship between the 21 and 50 EMAs:

When EMA 21 is above EMA 50, a green fill indicates upward momentum.

When EMA 21 is below EMA 50, a red fill shows downward momentum.

The EMA 200 line adapts its color based on its position relative to the shorter EMAs:

Red when above both EMAs (strong upward structure)

Green when below both EMAs (strong downward structure)

Gray when between them (neutral or consolidation phase)

This setup provides a clear visual framework for observing trend flow and directional bias over multiple timeframes.

Developed by The Volume Hub Fintech and Strategy Development

S&P Trading System with PivotsThe S&P Trading System with Pivots is a TradingView indicator designed for the 30-minute SPX chart to guide SPY options trading. It uses a trend-following strategy with:

10 SMA and 50 SMA: Plots a 10-period (blue) and 50-period (red) Simple Moving Average. A bullish crossover (10 SMA > 50 SMA) signals a potential buy (green triangle below bar), while a bearish crossunder (10 SMA < 50 SMA) signals a sell or exit (red triangle above bar).

Trend Bias: Colors the background green (bullish) or red (bearish) based on SMA positions.

Pivot Points: Marks recent highs (orange circles) and lows (purple circles) as potential resistance and support levels, using a 5-bar lookback period.

ICT Macro Time WindowsICT Macro Time Windows - Master institutional market timing with automated 'Macro' trading session tracking.

What are 'Macros'?

In ICT terminology, 'Macros' refer to the key institutional trading windows throughout the day where major banks and liquidity providers are most active. These specific time frames see heightened volatility, liquidity, and strategic positioning.

Perfect Timing Automation:

• 8 Critical Macro Sessions:

London 1: 02:33-03:00 EST

London 2: 04:03-04:30 EST

NY AM1: 08:50-09:10 EST

NY AM2: 09:50-10:10 EST

NY AM3: 10:50-11:10 EST

Lunch: 11:50-12:10 EST

PM: 13:10-13:40 EST

Close: 15:15-15:45 EST

• Fully customizable time zones and session times

• Real-time session detection with visual zones & labels

• Automatic High/Low range tracking within each window

• Boxes, lines, and labels for clear visual reference

• Never miss optimal entry/exit timing again

Trade when institutions trade - stop guessing and start timing your setups with precision during these key liquidity windows! All session times are easily adjustable in settings to match your preferred trading hours.

Perfect for Forex, Futures, and Index traders following ICT concepts and institutional flow analysis.

Historical Matrix Analyzer [PhenLabs]📊Historical Matrix Analyzer

Version: PineScriptv6

📌Description

The Historical Matrix Analyzer is an advanced probabilistic trading tool that transforms technical analysis into a data-driven decision support system. By creating a comprehensive 56-cell matrix that tracks every combination of RSI states and multi-indicator conditions, this indicator reveals which market patterns have historically led to profitable outcomes and which have not.

At its core, the indicator continuously monitors seven distinct RSI states (ranging from Extreme Oversold to Extreme Overbought) and eight unique indicator combinations (MACD direction, volume levels, and price momentum). For each of these 56 possible market states, the system calculates average forward returns, win rates, and occurrence counts based on your configurable lookback period. The result is a color-coded probability matrix that shows you exactly where you stand in the historical performance landscape.

The standout feature is the Current State Panel, which provides instant clarity on your active market conditions. This panel displays signal strength classifications (from Strong Bullish to Strong Bearish), the average return percentage for similar past occurrences, an estimated win rate using Bayesian smoothing to prevent small-sample distortions, and a confidence level indicator that warns you when insufficient data exists for reliable conclusions.

🚀Points of Innovation

Multi-dimensional state classification combining 7 RSI levels with 8 indicator combinations for 56 unique trackable market conditions

Bayesian win rate estimation with adjustable smoothing strength to provide stable probability estimates even with limited historical samples

Real-time active cell highlighting with “NOW” marker that visually connects current market conditions to their historical performance data

Configurable color intensity sensitivity allowing traders to adjust heat-map responsiveness from conservative to aggressive visual feedback

Dual-panel display system separating the comprehensive statistics matrix from an easy-to-read current state summary panel

Intelligent confidence scoring that automatically warns traders when occurrence counts fall below reliable thresholds

🔧Core Components

RSI State Classification: Segments RSI readings into 7 distinct zones (Extreme Oversold <20, Oversold 20-30, Weak 30-40, Neutral 40-60, Strong 60-70, Overbought 70-80, Extreme Overbought >80) to capture momentum extremes and transitions

Multi-Indicator Condition Tracking: Simultaneously monitors MACD crossover status (bullish/bearish), volume relative to moving average (high/low), and price direction (rising/falling) creating 8 binary-encoded combinations

Historical Data Storage Arrays: Maintains rolling lookback windows storing RSI states, indicator states, prices, and bar indices for precise forward-return calculations

Forward Performance Calculator: Measures price changes over configurable forward bar periods (1-20 bars) from each historical state, accumulating total returns and win counts per matrix cell

Bayesian Smoothing Engine: Applies statistical prior assumptions (default 50% win rate) weighted by user-defined strength parameter to stabilize estimated win rates when sample sizes are small

Dynamic Color Mapping System: Converts average returns into color-coded heat map with intensity adjusted by sensitivity parameter and transparency modified by confidence levels

🔥Key Features

56-Cell Probability Matrix: Comprehensive grid displaying every possible combination of RSI state and indicator condition, with each cell showing average return percentage, estimated win rate, and occurrence count for complete statistical visibility

Current State Info Panel: Dedicated display showing your exact position in the matrix with signal strength emoji indicators, numerical statistics, and color-coded confidence warnings for immediate situational awareness

Customizable Lookback Period: Adjustable historical window from 50 to 500 bars allowing traders to focus on recent market behavior or capture longer-term pattern stability across different market cycles

Configurable Forward Performance Window: Select target holding periods from 1 to 20 bars ahead to align probability calculations with your trading timeframe, whether day trading or swing trading

Visual Heat Mapping: Color-coded cells transition from red (bearish historical performance) through gray (neutral) to green (bullish performance) with intensity reflecting statistical significance and occurrence frequency

Intelligent Data Filtering: Minimum occurrence threshold (1-10) removes unreliable patterns with insufficient historical samples, displaying gray warning colors for low-confidence cells

Flexible Layout Options: Independent positioning of statistics matrix and info panel to any screen corner, accommodating different chart layouts and personal preferences

Tooltip Details: Hover over any matrix cell to see full RSI label, complete indicator status description, precise average return, estimated win rate, and total occurrence count

🎨Visualization

Statistics Matrix Table: A 9-column by 8-row grid with RSI states labeling vertical axis and indicator combinations on horizontal axis, using compact abbreviations (XOverS, OverB, MACD↑, Vol↓, P↑) for space efficiency

Active Cell Indicator: The current market state cell displays “⦿ NOW ⦿” in yellow text with enhanced color saturation to immediately draw attention to relevant historical performance

Signal Strength Visualization: Info panel uses emoji indicators (🔥 Strong Bullish, ✅ Bullish, ↗️ Weak Bullish, ➖ Neutral, ↘️ Weak Bearish, ⛔ Bearish, ❄️ Strong Bearish, ⚠️ Insufficient Data) for rapid interpretation

Histogram Plot: Below the price chart, a green/red histogram displays the current cell’s average return percentage, providing a time-series view of how historical performance changes as market conditions evolve

Color Intensity Scaling: Cell background transparency and saturation dynamically adjust based on both the magnitude of average returns and the occurrence count, ensuring visual emphasis on reliable patterns

Confidence Level Display: Info panel bottom row shows “High Confidence” (green), “Medium Confidence” (orange), or “Low Confidence” (red) based on occurrence counts relative to minimum threshold multipliers

📖Usage Guidelines

RSI Period

Default: 14

Range: 1 to unlimited

Description: Controls the lookback period for RSI momentum calculation. Standard 14-period provides widely-recognized overbought/oversold levels. Decrease for faster, more sensitive RSI reactions suitable for scalping. Increase (21, 28) for smoother, longer-term momentum assessment in swing trading. Changes affect how quickly the indicator moves between the 7 RSI state classifications.

MACD Fast Length

Default: 12

Range: 1 to unlimited

Description: Sets the faster exponential moving average for MACD calculation. Standard 12-period setting works well for daily charts and captures short-term momentum shifts. Decreasing creates more responsive MACD crossovers but increases false signals. Increasing smooths out noise but delays signal generation, affecting the bullish/bearish indicator state classification.

MACD Slow Length

Default: 26

Range: 1 to unlimited

Description: Defines the slower exponential moving average for MACD calculation. Traditional 26-period setting balances trend identification with responsiveness. Must be greater than Fast Length. Wider spread between fast and slow increases MACD sensitivity to trend changes, impacting the frequency of indicator state transitions in the matrix.

MACD Signal Length

Default: 9

Range: 1 to unlimited

Description: Smoothing period for the MACD signal line that triggers bullish/bearish state changes. Standard 9-period provides reliable crossover signals. Shorter values create more frequent state changes and earlier signals but with more whipsaws. Longer values produce more confirmed, stable signals but with increased lag in detecting momentum shifts.

Volume MA Period

Default: 20

Range: 1 to unlimited

Description: Lookback period for volume moving average used to classify volume as “high” or “low” in indicator state combinations. 20-period default captures typical monthly trading patterns. Shorter periods (10-15) make volume classification more reactive to recent spikes. Longer periods (30-50) require more sustained volume changes to trigger state classification shifts.

Statistics Lookback Period

Default: 200

Range: 50 to 500

Description: Number of historical bars used to calculate matrix statistics. 200 bars provides substantial data for reliable patterns while remaining responsive to regime changes. Lower values (50-100) emphasize recent market behavior and adapt quickly but may produce volatile statistics. Higher values (300-500) capture long-term patterns with stable statistics but slower adaptation to changing market dynamics.

Forward Performance Bars

Default: 5

Range: 1 to 20

Description: Number of bars ahead used to calculate forward returns from each historical state occurrence. 5-bar default suits intraday to short-term swing trading (5 hours on hourly charts, 1 week on daily charts). Lower values (1-3) target short-term momentum trades. Higher values (10-20) align with position trading and longer-term pattern exploitation.

Color Intensity Sensitivity

Default: 2.0

Range: 0.5 to 5.0, step 0.5

Description: Amplifies or dampens the color intensity response to average return magnitudes in the matrix heat map. 2.0 default provides balanced visual emphasis. Lower values (0.5-1.0) create subtle coloring requiring larger returns for full saturation, useful for volatile instruments. Higher values (3.0-5.0) produce vivid colors from smaller returns, highlighting subtle edges in range-bound markets.

Minimum Occurrences for Coloring

Default: 3

Range: 1 to 10

Description: Required minimum sample size before applying color-coded performance to matrix cells. Cells with fewer occurrences display gray “insufficient data” warning. 3-occurrence default filters out rare patterns. Lower threshold (1-2) shows more data but includes unreliable single-event statistics. Higher thresholds (5-10) ensure only well-established patterns receive visual emphasis.

Table Position

Default: top_right

Options: top_left, top_right, bottom_left, bottom_right

Description: Screen location for the 56-cell statistics matrix table. Position to avoid overlapping critical price action or other indicators on your chart. Consider chart orientation and candlestick density when selecting optimal placement.

Show Current State Panel

Default: true

Options: true, false

Description: Toggle visibility of the dedicated current state information panel. When enabled, displays signal strength, RSI value, indicator status, average return, estimated win rate, and confidence level for active market conditions. Disable to declutter charts when only the matrix table is needed.

Info Panel Position

Default: bottom_left

Options: top_left, top_right, bottom_left, bottom_right

Description: Screen location for the current state information panel (when enabled). Position independently from statistics matrix to optimize chart real estate. Typically placed opposite the matrix table for balanced visual layout.

Win Rate Smoothing Strength

Default: 5

Range: 1 to 20

Description: Controls Bayesian prior weighting for estimated win rate calculations. Acts as virtual sample size assuming 50% win rate baseline. Default 5 provides moderate smoothing preventing extreme win rate estimates from small samples. Lower values (1-3) reduce smoothing effect, allowing win rates to reflect raw data more directly. Higher values (10-20) increase conservatism, pulling win rate estimates toward 50% until substantial evidence accumulates.

✅Best Use Cases

Pattern-based discretionary trading where you want historical confirmation before entering setups that “look good” based on current technical alignment

Swing trading with holding periods matching your forward performance bar setting, using high-confidence bullish cells as entry filters

Risk assessment and position sizing, allocating larger size to trades originating from cells with strong positive average returns and high estimated win rates

Market regime identification by observing which RSI states and indicator combinations are currently producing the most reliable historical patterns

Backtesting validation by comparing your manual strategy signals against the historical performance of the corresponding matrix cells

Educational tool for developing intuition about which technical condition combinations have actually worked versus those that feel right but lack historical evidence

⚠️Limitations

Historical patterns do not guarantee future performance, especially during unprecedented market events or regime changes not represented in the lookback period

Small sample sizes (low occurrence counts) produce unreliable statistics despite Bayesian smoothing, requiring caution when acting on low-confidence cells

Matrix statistics lag behind rapidly changing market conditions, as the lookback period must accumulate new state occurrences before updating performance data

Forward return calculations use fixed bar periods that may not align with actual trade exit timing, support/resistance levels, or volatility-adjusted profit targets

💡What Makes This Unique

Multi-Dimensional State Space: Unlike single-indicator tools, simultaneously tracks 56 distinct market condition combinations providing granular pattern resolution unavailable in traditional technical analysis

Bayesian Statistical Rigor: Implements proper probabilistic smoothing to prevent overconfidence from limited data, a critical feature missing from most pattern recognition tools