Heikin-Ashi Rolling Time Decay Volume OscillatorThe indicator calculates a time-decayed moving sum of volume data for both bullish (green) and bearish (red) candles. It then generates a volume share oscillator as a smoothed and weighted (time-decayed) moving sum of bullish volume (positive share) or bearish volume (negative share) relative to the total volume.

The volume share is displayed as an area chart with gradient fills representing overbought and oversold regions. Additionally, an Arnaud Legoux Moving Average (ALMA) of the volume oscillator is plotted on the chart.

Trend Momentum and Price Control :

This indicator serves as a powerful tool for traders to gauge trend momentum and identify which side, bulls or bears, is controlling price movements. When the volume oscillator trends strongly in the green territory, it suggests that bulls are in control of price movements, indicating a potential uptrend. Conversely, when the oscillator tilts into the red, it indicates bearish dominance and a potential downtrend. With the incorporation of ALMA for smoothing, this indicator becomes an essential tool for traders and analysts navigating the dynamics of traded assets.

Source Candles :

This indicator is designed to work with Heiken Ashi or Japanese candlesticks to discern candle bias, whether it's red or green. Heiken Ashi tends to produce red candles during downtrends and green candles during uptrends, providing a clearer trend indication. In contrast, traditional candlesticks alternate colors regardless of the dominant price direction. Users can select between "Heikin-Ashi Candles" and regular "Japanese Candles" as the source for price direction."

A time decay cumulative sum, also known as a weighted moving sum or exponentially weighted moving sum, offers several advantages when it comes to determining market dynamics compared to other methods:

Responsive to Recent Data: Time decay cumulative sum gives more weight to recent data points and gradually reduces the impact of older data. This responsiveness is crucial in rapidly changing market conditions where recent price and volume information is more relevant for analysis.

Adaptive to Market Volatility : It adapts to changes in market volatility. When markets are highly volatile, it places more emphasis on recent data to reflect the current market environment accurately. Conversely, during calmer periods, it considers older data less important.

Effective for Identifying Turning Points : Time decay cumulative sums are particularly effective at identifying turning points in market dynamics. They can indicate shifts from bullish to bearish sentiment and vice versa, providing early signals of potential trend reversals.

Reduces Lag : Traditional cumulative sums or simple moving averages can lag behind actual market changes, making them less effective for real-time decision-making. Time decay cumulative sums reduce this lag by giving more weight to recent events.

Dynamic Weighting: The weighting scheme can be adjusted to fit specific market dynamics or trading strategies. Traders can customize the decay rate or smoothing factor to align with their analysis goals and timeframes.

Improved Signal Clarity : The time decay cumulative sum can provide clearer and more precise signals for overbought and oversold conditions, as well as trend strength, due to its ability to emphasize recent relevant data.

In summary, a time decay cumulative sum is a valuable tool in determining market dynamics because it adapts to changing market conditions, reduces noise, and provides timely and accurate insights into trends, turning points, and the relative strength of bullish and bearish forces. Its responsiveness and adaptability make it an essential component of many technical analysis and trading strategies.

"Exponential"に関するスクリプトを検索

[SMT] Binary Option 1 MinuteThis indicator called " Binary Option 1 Minute" is designed to trade binary options on 1-minute time frames. It is based on two moving averages and a crossover signal. The moving averages used are calculated from the average prices of the last time periods. The first moving average is calculated with a shorter period, while the second is calculated with a longer period.

The signal is generated when the first moving average crosses above or below the second moving average, and then an additional filter is applied. The signal filter is calculated using an exponentially weighted moving average of the difference between the two moving averages. When the signal crosses above the zero line, a buy signal is generated, and when the signal crosses below the zero line, a sell signal is generated.

The indicator plots buy and sell arrows on the chart when a signal is generated. Additionally, it can also display gains and losses in the form of background colors. The green color indicates a gain, and the red color indicates a loss. Finally, the indicator includes sound and text alerts to inform the trader about the generation of a signal.

Attention: This indicator does not repaint! Wait for the candle to close to confirm the entry signal. Remember that signals do not imply guarantees of accuracy or gains. It is highly recommended that you test the indicator on a demo account before using it on a real account.

Quick Shot[ChartPrime]This indicator plots green and red dots when the trend changes based on a moving average slope. The curved line aims to exponentially increase the slope of the moving average based on the slope at the time of the dots origination as the bars progress. Once the curved line makes contact with the price action, an x shape will be plotted to signify an exit signal.

This indicator is best used in confluence with other indicators in order to develop a reliable strategy.

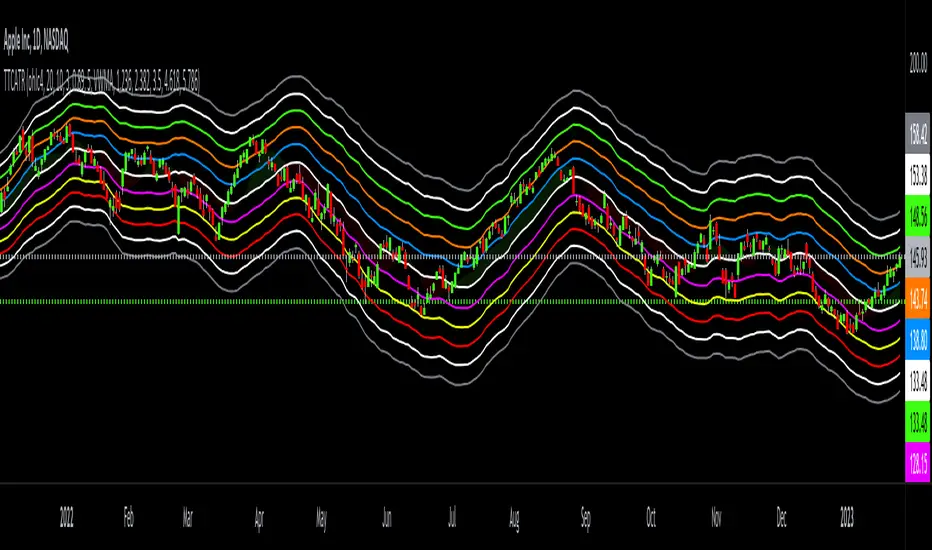

Triangular Trend Channel ATRTTCATR: Triangular Trend Channel ATR is a script to dynamically create a trend channel. It uses Moving Average & the Average True Range function to calculate support and resistance levels automatically.

The MA choices available are:

SMA = simple moving average

EMA = exponentially weighted moving average

RMA = moving average used in RSI

WMA = weighted moving average

VWMA = volume weighted moving average

VWAP = volume weighted average price

HMA = Hull moving average

SWMA = symmetrically weighted moving average

ALMA = Arnaud Legoux moving average

The default setting inputs are:

source = OHLC4

MA length = 20

MA signal = 10

ATR Multiply = 3

ALMA offset = 0.89

ALMA sigma = 5

Moving average type = VWMA

Level 1 ATR = 1.236

Level 2 ATR = 2.382

Level 3 ATR = 3.5

Level 4 ATR = 4.618

Level 5 ATR = 5.786

The default setting colors are:

Top = gray

R4 = white

R3 = green

R2 = orange

R1 = blue

pivot = white

(track pivot line = bullish is green, bearish is red)

S1 = purple

S2 = yellow

S3 = red

S4 = white

Bottom = gray

* This script uses altered pieces of code from my @Options360 TTC: Triangular Trend Channel and @TradingView "Intrabar Efficiency Ratio indicator". *

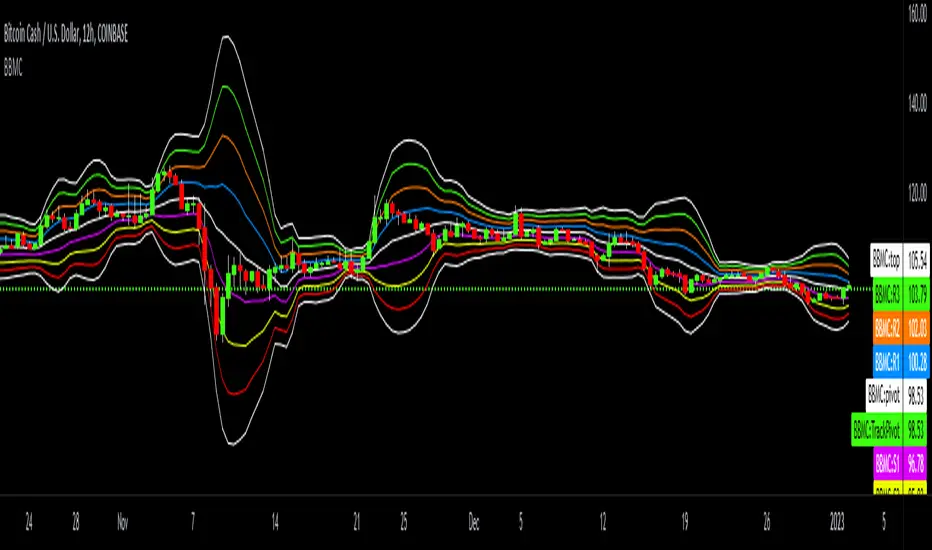

Bollinger-Bands.Multi_Choice(BBMC) "Bollinger-Bands.Multi_Choice" indicator gives the end user a choice of which Moving Average they want to use.

The MA choices available are:

SMA = simple moving average

EMA = exponentially weighted moving average

RMA = moving average used in RSI

WMA = weighted moving average

VWMA = volume weighted moving average

VWAP = volume weighted average price

HMA = Hull moving average

SWMA = symmetrically weighted moving average

ALMA = Arnaud Legoux moving average

The default setting inputs are:

source = OHLC4

length = 13

ALMA offset = 0.89

ALMA sigma = 5

Moving average type = VWMA

Level 1 standard deviation = 1.0

Level 2 standard deviation = 2.0

Level 3 standard deviation = 3.0

Level 3 standard deviation = 4.0

The default setting colors are:

Top = white

R3 = green

R2 = orange

R1 = blue

pivot = white

(track pivot line = bullish is green, bearish is red)

S1 = purple

S2 = yellow

S3 = red

Bottom = white

I made this indicator from an idea I had for a few months with the help of pine coder scripts before me. Kudos to @TradingView & @Madrid.

* This script uses altered pieces of code from @TradingView "Intrabar Efficiency Ratio indicator" & @Madrid "Bollinger Bands indicator" *

Multiple EMAAn exponentially weighted moving average reacts more significantly to recent price changes than a simple moving average (SMA), which applies an equal weight to all observations in the period.

Here, i have merged multiple EMA into one indicator. traders would find it very convenient as multiple widely used EMA`s are merged into 1 indicator. one can also change the time and color from its settings as per their convenience.

About the practicality of this EMA`s:

Every EMA suggests the sentiments in a period of time.

The longer-day EMAs (i.e. 50 and 200-day) tend to be used more by long-term investors, while short-term investors tend to use 8 and 20 day EMAs.

One may prefer to short or to hedge their position when 200 day moving average is broken downside. vise-versa for long. Normally in one may expect around 2-3% move on either side when broken with volumes supporting it.

Stop Loss With Average True Range (ATR)Stop Loss With Average True Range (ATR)

It simplifies the calculation of stop loss price for stop loss method using the average true range (ATR).

For example;

You want to stop loss below 3 ATR. Let's assume the price is 100, the average true range is 5. You will multiply the average true range by 3 and subtract from the price and enter a stop loss order at the 85 price you have reached. Instead of doing this calculation every time, you just need to use this script and set the multiplier to 3. A stop loss line will be drawn below the price candles.

You can set the method to be used when averaging the true range. Methods you can use to average: EMA (exponentially moving average), HMA (hull moving average), RMA (moving average used in RSI), SMA (simple moving average), SWMA (symmetrically weighted moving average), VWMA (volume-weighted moving average), WMA (weighted moving average).

You can set the length to be used when averaging the true range.

You can set the multiplier to be used when determining the stop loss price.

Turkish

Ortalama Gerçek Aralıkla (ATR) Zarar Durdurma

Gerçek aralığın ortalamasını kullanarak zarar durdurma yöntemi için zarar durdurma fiyatının hesaplanmasını kolaylaştırır.

Örneğin;

3 ATR kadar aşağıda zarar durdurmak istiyorsunuz. Fiyatın 100, ortalama gerçek aralığın 5 olduğunu varsayalım. Ortalama gerçek aralığı 3 ile çarparak fiyattan çıkaracaksınız ve ulaştığınız 85 fiyatına zarar durdurma emri gireceksiniz. Bu hesabı her seferinde yapmak yerine bu betiği kullanmanız ve çarpanı 3 olarak ayarlamanız yeterli. Bu sayede fiyat mumlarının altına zarar durdurma çizgisi çizilecektir.

Gerçek aralığın ortalaması alınırken kullanılacak yöntemi ayarlayabilirsiniz. Ortalama almak için seçebileceğiniz yöntemler: EMA (üstel hareketli ortalama), HMA (gövde hareketli ortalama), RMA (göreceli hareketli ortalama), SMA (basit hareketli ortalama), SWMA (simetrik ağırlıklı hareketli ortalama), VWMA (hacim ağırıklı hareketli ortalama), WMA (ağırlıklı hareketli ortalama).

Gerçek aralığın ortalaması alınırken kullanılacak periyot uzunluğunu ayarlayabilirsiniz.

Zarar durdurma fiyatını belirlerken kullanılacak çarpanı ayarlayabilirsiniz.

cowen risk indexThis is my attempt at remaking the cowen risk index. It's definitely not correct, but should give a rough estimate of where his indicator is at. I am taking the price divided by the 400sma to get an oscillator, then we need to account for diminishing returns so I just made an exponentially increasing variable and mutliplying that by the oscillator value. Then I normalized the data as best as I could. Not sure exactly how to do that so if anyone has any suggestions, please let me know.

This only works on the daily and weekly timeframe. You will need to edit the code if you want to have it work for other timeframes.

Rolling EMAVWAP with Standard Deviation BandsThis is experimental code trying to implement exponentially decreasing weights over time in a simple VWAP.

Also i applied EMA rules when calculating the Standard Deviation Bands.

The script produces results from 1 candle.

There is an "log space" option to neutralize bands shifts when charting in log space - this gives the correct geometrically equal distances on both sides of the emaVWAP.

Bitcoin Logarithmic Fractal Growth Model By ARUDDThis model, which I'm calling the Logarithmic Fractal Growth Mode (L.F.G) , uses Bitcoin's mathematical monetary policy to evaluate the future possible price valuation.

It takes into account fractal (and logarithmic) growth as well as how those who hold bitcoins might react to certain events such as changes in supply and demand. It also shows that it is mathematically logical that someday it must become stable.

The information gained from knowing this helps people make more informed decisions when buying bitcoin and thinking of its future possibilities.

The model can serve as some type of general guideline for determining how much bitcoins should be worth in the future if it follows a certain path from its current price.

Modeling Bitcoin's money supply mathematically, and knowing that there is a finite number of them, makes this whole process much more rational than just thinking about the possibilities in pure subjective terms.

Before going any further I want to say that no one can know with absolute certainty what will happen to bitcoins price in the future, but using mathematics gives us an idea of where things are headed.

The results presented here are based on very reasonable assumptions for how bitcoin might continue to grow (and then level out) once there are over 21 million bitcoins in existence.

The model shows that bitcoin's price can never go down to zero (thus creating the "death spiral" phenomenon), and as such, bitcoin has an extremely high probability of becoming stable as it approaches infinity.

Conversely, this model also shows that at some point there is a high probability that bitcoin will not continue to grow exponentially forever.

Credit goes to Quantadelic for the awesome original script.

ARUDD

"DSS" Bessert Double Smooth Stochastic Alma Variant Hi colleagues I share this time DSS bressert.

As usual they have all the adjustable colors and signals. I hope you enjoy them and leave here below the length of signals that best suit your needs so that we can continue sharing content

Description

One after the other, William Blau and Walter Bressert each presented a version of the Double Smoothed Stochastics. Two exponentially smoothed MAs are used to even out the input values (H, L and C), in a similar way to the well-known stochastic formula.

Parameters

The adjustable period length can be chosen from 2 to 500. The most common settings will have a period length ranging from 5 to 30. In addition, the indicator can be smoothed in the interval from 1 to 50. Meaningful smoothing values lie in the short-term range.

Interpretation

The application of the DSS is comparable with that of the stochastic method. Accordingly, values above 70 or 80 must be regarded as overbought and values below 20 or 30 as oversold. A rise of the DSS above its center line should be viewed as bullish, and a fall of the DSS below its center line as bearish.

/// Quick Explained ALMA ///

//Window size: The window size is the look-back period and it is a basic setting of ALMA.

//Experienced traders can change this setting according to their preference.

//But if you are using this indicator for the first time, it is recommended to go with the default setting.

//Offset: The offset value is used to tweak the ALMA so that it will be more inclined

//towards responsiveness or smoothness. You can set the offset in decimals between the 0 to1.

//The value of 0.01 makes it smoother, while a setting of 0.99 makes the indicator more responsive.

//Sigma: The sigma is used for the filter. Any value less than 6 makes the indicator

//more focused, whereas the setting of 6 makes the filter large. According to Mr Arnaud,

//a sigma value of 6 is offer good performance.

/// Explain DSS ///

//Parameters

//The adjustable period length can be chosen from 2 to 500.

//The most common settings will have a period length ranging from 5 to 30.

//In addition, the indicator can be smoothed in the interval from 1 to 50.

//Meaningful smoothing values lie in the short-term range.

//Interpretation

//The application of the DSS is comparable with that of the stochastic method.

//Accordingly, values above 70 or 80 must be regarded as overbought and values below 20 or 30 as oversold.

//A rise of the DSS above its center line should be viewed as bullish,

//and a fall of the DSS below its center line as bearish

/// End Of The Code///

4 MA Strategy + Position Management// This is a simple crossover Moving Average strategy, good for long term crypto trades.

// It buys when the MA "X" crosses up the MA "Y", viceversa for shorts.

// Both MAs are selectable from the Inputs section in the front panel.

// There is also a Position Management option thats

// sizes positions to have the same USD risk (using leverage) on each trade,

// based on the percentage distance to the stop loss level.

// If you turn this option on you will see how the profit

// grows exponentially while the drawdown percentage almost remains the same.

Volume, Momentum and Volatility weighted moving averageMoving averages are filters on price data. This moving average creates a filter which factors in:

- the price RSI or it's Momentum

- the volume RSI

- the RVI or Volatility

Each factor is put through a least squares filter to smooth them first.

Then the factors are used to build a coefficient for an exponentially weighted average.

The chart above shows a comparison of standard average types with this script.

This is useful if you are looking for a moving average based trigger and do not wish to react to candle noise price action.

Linear Regression + Moving Average1. Linear Regression including 2 x Standard Deviation + High / Low. Middle line colour depends on colour change of Symmetrically Weighted Moving Average . Green zones indicate good long positions. Red zones indicate good short positions. (Custom)

2. Symmetrically Weighted Moving Average. Colour change depending on cross of offset -1. (Fixed)

3. Exponentially Weighted Moving Average. Colour change depending on cross with Symmetrically Weighted Moving Average. (Custom)

Log MACDThis is just a MACD indicator using the log of the closing price rather than the normal closing price. Useful for exponentially growing stocks and cryptocurrency.

Volume Weighted Directional BiasThis indicator uses a series of five volume weighted moving averages cast out in successive powers of three to calculate a value which expresses the direction and momentum of a trend. It can be used as a contrary indicator to identify waning momentum at the top or bottom of a rally or selloff. It can be used to identify trendline divergence. It can also be used for trend confirmation.

The length of the moving averages can be changed in the indicator inputs, but each should be longer than the previous.

The problem with most trend indicators is that they are either too lagging or too noisy. This indicator seeks to combine smoothed data and a long lookback period with an exponentially forward weighted calculation, making it still very responsive to market changes without too much signal noise.

Grid ToolThe core idea of this grid tool is that you have to concentrate less on the trade entries (this happens automatically time-independent but price-dependant) but rather on the validity of the macro trend. Exiting a trend when it is no longer valid is more important than entering a trade. But as long as the trend is valid, the trader participates exponentially in the overall trend.

It is advisable to start with a basic position and then "set up" the grid on this in a ratio of 1/10.

A major advantage of grid trading is that the average entry price in a trend moves further and further away from the current market price while the position continues to grow.

A small timeframe should be used so that the distance between the trades corresponds as closely as possible to the selected grid gap and since TV backtests are carried out with closed bars.

Before starting a grid, pre-analysis the market to make sure it is trending. Select the grid gap and grid position size that you are comfortable with. Monitor the trend and from time to time take some profit :).

PS: The ADX filter looks interesting.

[SCL] Bitcoin Hashrate Dips (Miner Capitulation)Gives long-term buy signals for Bitcoin from dips and recoveries in the hashrate (the "miner capitulation" theory). It has an overlay and a standalone mode and is fully configurable. It uses Williams Lows and ATR instead of moving averages.

Features that might be interesting for Pinescripters:

+ Automatic (as far as is possible currently) adjustment of plots for overlay and standalone display modes.

+ A neat label function for debugging floats

+ Fully commented

+ The debug that I used to overcome problems in developing it is left in

+ Ideas for how to deal with a wildly oscillating and exponentially increasing data source

You need to run this indicator on the Bitcoin daily chart for it to make any sense. The best is a BTC/USD chart with a long history, such as BNC:BLX.

KINSKI Flexible Multi MA (EMA, SMA, RMA, WMA, VWMA, KAMA, HMA)This Multi Moving Average (MA) indicator is more flexible than any other indicator of this type offered so far. You can define up to 10 different Moving Average (MA) lines based on different calculation variants.

The following MA types can be configured.

- EMA: Exponentially Moving Average

- SMA: Small Moving Average

- RMA: Rolling Moving Average

- WMA: Weighted Moving Average

- VWMA: Volume Weighted Moving Average

- KAMA: Kaufman's Adaptive Moving Average

- HMA: Hull Moving Average

Which settings can be made?

- Selection for calculation formula ("Calculation Source"). The default value is "close".

- for each MA line the "Length" and the "Type" can be defined

- furthermore you can make layout adjustments via the "Style" menu

Dynamic Money FlowDynamic Money Flow is a volume indicator based on Marc Chaikin's Money Flow with a few improvements.

It can be used to confirm break-outs and trends.

Zero line crosses and divergences can provide useful signals while considering chart analysis as well.

Two weaknesses of CMF have been already fixed by Colin Twiggs (IncredibleCharts)...

1.CMF uses Chaikin's accumulation/distribution line to calculate the flow of money.

Accumulation/distribution line does not take the gaps into account. This can be solved using true range.

I call it true accumulation/distribution.

2.Oscillators have a tendency to center because of averaging calculations.

DMF is average of flowing volume divided by average of total volume. This means indicator plots the change of first factor compared to the other one. In Simple Averaging method every data is given an equal weight thus when the last data drops it will have heavy impact on the averages and the change of them.

It is much easier to identity these impacts after the drop of very high or very low data... So reducing the weight exponentially is a better option.

3.There is something else with CMF... changes of close price is ignored, because the formula only compares close price to its range.

To include the movements of close beside the close to range comparison, the distance between two last close prices should be compared to true range as well.

So volume can be distributed between close to range comparison (True Accumulation/Distribution) and close to close comparison automatically. And then results are summed to have a single multiplier.

An example for how close to close comparison affects DMF...

Or here you can see how lower wicks keep TMF (same as CMF in this case) from crossing zero line while price is trending down.

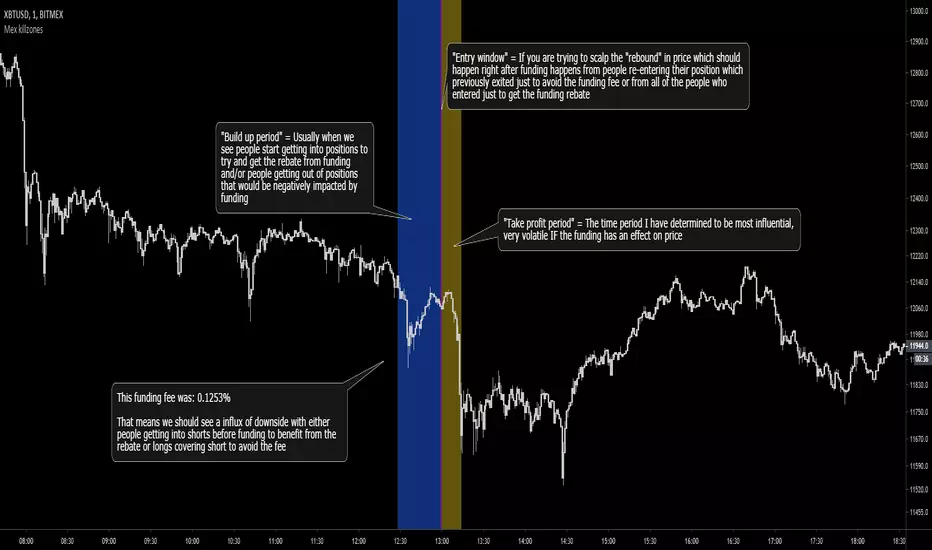

Bitmex Funding Killzones v3 [MaliciousUpload]Originally built off of "Oscarvs: BITCOIN KILL ZONES v2" indicator, updated to now highlight a different time period based event.

1. The indicator should not be affected by what time zone you are in, it will show true Funding periods by default.

2. This needs to be used on the 1min time frame to be used to its full extent

3. The more the funding fee is the more likely you are to have price get manipulated by people looking to act on its benefit

4. This indicator will work only for XBTUSD and ETHUSD perpetual contract symbols as they are the only two ones with funding...

My opinion: Funding is literally the exchanges insurance policy, they are "the house", they will always win.

With that in mind you can trade "with the house" in this regard, getting onto the side that will benefit from exponentially large funding rebates.

Do you ever ask how those "whales" got to be rich? It was by saving every penny they could while trading.

Funding gives people the option to jump out right before, avoiding the fee and then immediately enter in after at no loss (assuming limit orders ofc).

If that doesn't make sense to you i cant help, sorry. :pray: :pray: :pray:

"Build up period" = Usually when we see people start getting into positions to try and get the rebate from funding and/or people getting out of positions that would be negatively impacted by funding

"Entry window" = If you are trying to scalp the "rebound" in price which should happen right after funding happens from people re-entering their position which previously exited just to avoid the funding fee or from all of the people who entered just to get the funding rebate

"Take profit period" = The time period I have determined to be most influential, very volatile IF the funding has an effect on price

Hit me up on Discord if you are an **experienced** trader that takes trading seriously.

MaliciousUpload#1637

VWMA RibbonVolume Weighted Moving Average of HLC3's, spread over a wide range of periods to get an overall feel of any market.

The 15 periods used are exponentially increasing to provide somewhat even spacings in moving markets, which can be useful for progressive stop-buys (dollar cost averaging in) or progressive stop-losses (dollar cost averaging out):

4

7

12

20

33

54

87

140

226

365

590

955

1545

2500

5000