MA CloudThis indicator plots a Moving Average (MA) cloud with ultra-smooth visuals, designed to help traders identify trend direction, momentum, and volatility in a clear and intuitive way.

Features:

Multiple MA types: choose between EMA, SMA, WMA, or RMA

Adaptive cloud width: based on standard deviation of price to visualize volatility

Smoothing controls: post-processed smoothing gives a silky, curved appearance

Multi-Timeframe (MTF) support: default to chart timeframe, or override to any custom timeframe (e.g. 1H, 1D, etc.)

Custom styling: adjustable colours, line thickness, and cloud opacity

Use cases:

Quickly assess trend strength and direction

Use cloud thickness as a volatility proxy

Spot pullback entries during trending conditions

Combine with price action or support/resistance for confluence

Settings:

MA Type – select your preferred moving average method

MA Length – period for the average

Cloud Width Factor – adjusts the distance of the cloud edges

Smoothing Length – softens the output for a polished look

Timeframe – optional override to analyse data from a higher or lower timeframe

"curve"に関するスクリプトを検索

Bradley SiderographThis indicator functions as a Planetary Barometer, bringing the Bradley-Siderograph directly onto your TradingView chart. Designed for tracking the algebraic sum of planetary aspects and declination values in relation to market movements, it analyzes sidereal potential, long-term and mid-term planetary aspects, and the declination factor to provide insight into potential shifts in mass psychology. The built-in gauges act like a barometer, visually measuring the intensity and range of the components.

As Donald Bradley states in Stock Market Prediction:

" The siderograph is nothing more than a time chart showing a wavy line, which represents the algebraic total of the declination factor, the long terms, and the middle terms. It can be computed for any period—past or future—for which an ephemeris is available. Every aspect, whether long or middle term, is assigned a theoretical value of 10 at its peak. The value of the declination factor is half the algebraic sum of the given declinations of Venus and Mars, with northern declination considered positive and southern declination negative. "

How the Bradley-Siderograph Works:

The Siderograph assigns positive and negative valencies based on the transits of inner and outer planets, categorized into long-term and mid-term aspects.

Each aspect (15° orb) is given a theoretical value, with the peak set at ±10. The approach and separation phases influence the weighting of each aspect leading up to its peak.

The sign of the valency depends on the type of aspect:

Squares and oppositions are assigned negative values

Trines and sextiles are assigned positive values

Conjunctions can be either positive or negative, depending on the planetary combination

Formula Used:

The Siderograph is computed as follows:

𝑃 = 𝑋 (𝐿 + 𝐷) + 𝑀

Where:

P = Sidereal Potential (final computed value)

X = Multiplier (to weight long-term aspects)

L = Long-term aspects (10 aspect combinations)

D = Declination factor (half the sum of Venus and Mars declinations)

M = Mid-term aspects

The long-term component (L + D) can be multiplied by a chosen factor (X) to emphasize its influence relative to the mid-term aspects.

How to Use the Indicator:

Once applied, the Siderograph line overlays on the chart, using the left-side scale for reference.

The indicator provides separate plots for:

Sidereal potential

Long-term aspects

Mid-term aspects

Declination factor

Each component can be toggled on or off for deeper analysis.

Gauges "provided by @faiyaz7283 library" display the high and low range for each curve, allowing quick identification of extreme values.

The indicator also marks the yearly high and low of the current year’s sidereal potential, providing a reference for when the market is trading above or below key levels. This feature was inspired by an observation made by Bradley in his book, which I wanted to incorporate here.

Users can fully customize the indicator by:

Switching between geocentric and heliocentric views.

Adjusting the orb of planetary transits to refine aspect sensitivity.

Multiplier (to weight long-term aspects)

Explore the Bradley-Siderograph and experiment with its settings.

Main Use Case

The Siderograph can be thought of as a psychological wind sock, gauging shifts in mass sentiment in response to planetary influences. Rather than forecasting market direction outright, it serves as an early warning system, signaling when conditions may be primed for changes in collective psychology.

As Donald Bradley notes in Stock Market Prediction:

" A limitation of the siderograph is that it cannot be construed as a forecast of secular trend. In statistical terminology, 'lines of regression' fitted to the market course and to the potential should not be expected to completely agree, for reasons obvious to everybody with keen business sense or commercial training. However, the siderograph may be depended upon to reward its analyst with foreknowledge of coming conditions in general, so that the non-psychological factors may be evaluated accordingly. By this, we mean that the potential will afford one with clues as to how the mass mind will 'take' the other mechanical or governmental vicissitudes affecting high finance. The siderograph may be thought of as a principle 'symptom' in diagnosing current market circumstances and as a sounding-board for prognoses concerning further developments. "

Planned Improvement:

While Bradley did not construct the Siderograph for direct forecasting, an enhancement to this indicator would be the ability to project each curve forward in time, providing a clearer view of how upcoming planetary aspects.

This indicator is being released as open source with the hope of further refining and expanding its capabilities—particularly in developing future plots that improve visualization and analysis. Contributions and feedback are encouraged to enhance its usability and advance the study of planetary influences in market behavior.

Credits & Acknowledgments:

Inspired by Donald Bradley and his work in Stock Market Prediction: The Planetary Barometer and How to Use It.

Built using Astrolib, developed by @BarefootJoey

Built using Gauges, developed by @faiyaz7283

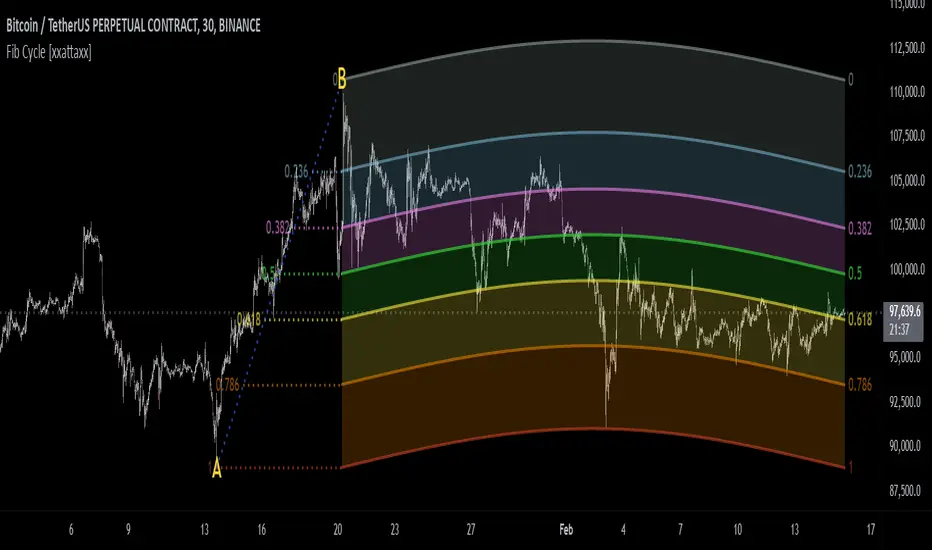

Fibonacci Cycle Finder🟩 Fibonacci Cycle Finder is an indicator designed to explore Fibonacci-based waves and cycles through visualization and experimentation, introducing a trigonometric approach to market structure analysis. Unlike traditional Fibonacci tools that rely on static horizontal levels, this indicator incorporates the dynamic nature of market cycles, using adjustable wavelength, phase, and amplitude settings to visualize the rhythm of price movements. By applying a sine function, it provides a structured way to examine Fibonacci relationships in a non-linear context.

Fibonacci Cycle Finder unifies Fibonacci principles with a wave-based method by employing adjustable parameters to align each wave with real-time price action. By default, the wave begins with minimal curvature, preserving the structural familiarity of horizontal Fibonacci retracements. By adjusting the input parameters, the wave can subtly transition from a horizontal line to a more pronounced cycle,visualizing cyclical structures within price movement. This projective structure extends potential cyclical outlines on the chart, opening deeper exploration of how Fibonacci relationships may emerge over time.

Fibonacci Cycle Finder further underscores a non-linear representation of price by illustrating how wave-based logic can uncover shifts that are missed by static retracement tools. Rather than imposing immediate oscillatory behavior, the indicator encourages a progressive approach, where the parameters may be incrementally modified to align wave structures with observed price action. This refinement process deepens the exploration of Fibonacci relationships, offering a systematic way to experiment with non-linear price dynamics. In doing so, it revisits fundamental Fibonacci concepts, demonstrating their broader adaptability beyond fixed horizontal retracements.

🌀 THEORY & CONCEPT 🌀

What if Fibonacci relationships could be visualized as dynamic waves rather than confined to fixed horizontal levels? Fibonacci Cycle Finder introduces a trigonometric approach to market structure analysis, offering a different perspective on Fibonacci-based cycles. This tool provides a way to visualize market fluctuations through cyclical wave motion, opening the door to further exploration of Fibonacci’s role in non-linear price behavior.

Traditional Fibonacci tools, such as retracements and extensions, have long been used to identify potential support and resistance levels. While valuable for analyzing price trends, these tools assume linear price movement and rely on static horizontal levels. However, market fluctuations often exhibit cyclical tendencies , where price follows natural wave-like structures rather than strictly adhering to fixed retracement points. Although Fibonacci-based tools such as arcs, fans, and time zones attempt to address these patterns, they primarily apply geometric projections. The Fibonacci Cycle Finder takes a different approach by mapping Fibonacci ratios along structured wave cycles, aligning these relationships with the natural curvature of market movement rather than forcing them onto rigid price levels.

Rather than replacing traditional Fibonacci methods, the Fibonacci Cycle Finder supplements existing Fibonacci theory by introducing an exploratory approach to price structure analysis. It encourages traders to experiment with how Fibonacci ratios interact with cyclical price structures, offering an additional layer of insight beyond static retracements and extensions. This approach allows Fibonacci levels to be examined beyond their traditional static form, providing deeper insights into market fluctuations.

📊 FIBONACCI WAVE IMPLEMENTATION 📊

The Fibonacci Cycle Finder uses two user-defined swing points, A and B, as the foundation for projecting these Fibonacci waves. It first establishes standard horizontal levels that correspond to traditional Fibonacci retracements, ensuring a baseline reference before wave adjustments are applied. By default, the wave is intentionally subtle— Wavelength is set to 1 , Amplitude is set to 1 , and Phase is set to 0 . In other words, the wave starts as “stretched out.” This allows a slow, measured start, encouraging users to refine parameters incrementally rather than producing abrupt oscillations. As these parameters are increased, the wave takes on more distinct sine and cosine characteristics, offering a flexible approach to exploring Fibonacci-based cyclicity within price action.

Three parameters control the shape of the Fibonacci wave:

1️⃣ Wavelength Controls the horizontal spacing of the wave along the time axis, determining the length of one full cycle from peak to peak (or trough to trough). In this indicator, Wavelength acts as a scaling input that adjusts how far the wave extends across time, rather than a strict mathematical “wavelength.” Lower values further stretch the wave, increasing the spacing between oscillations, while higher values compress it into a more frequent cycle. Each full cycle is divided into four quarter-cycle segments, a deliberate design choice to minimize curvature by default. This allows for subtle oscillations and smoother transitions, preventing excessive distortion while maintaining flexibility in wave projections. The wavelength is calculated relative to the A-B swing, ensuring that its scale adapts dynamically to the selected price range.

2️⃣ Amplitude Defines the vertical displacement of the wave relative to the baseline Fibonacci level. Higher values increase the height of oscillations, while lower values reduce the height, Negative values will invert the wave’s initial direction. The amplitude is dynamically applied in relation to the A-B swing direction, ensuring that an upward swing results in upward oscillations and a downward swing results in downward oscillations.

3️⃣ Phase Shifts the wave’s starting position along its cycle, adjusting alignment relative to the swing points. A phase of 0 aligns with a sine wave, where the cycle starts at zero and rises. A phase of 25 aligns with a cosine wave, starting at a peak and descending. A phase of 50 inverts the sine wave, beginning at zero but falling first, while a phase of 75 aligns with an inverted cosine , starting at a trough and rising. Intermediate values between these phases create gradual shifts in wave positioning, allowing for finer alignment with observed market structures.

By fine-tuning these parameters, users can adapt Fibonacci waves to better reflect observed market behaviors. The wave structure integrates with price movements rather than simply overlaying static levels, allowing for a more dynamic representation of cyclical price tendencies. This indicator serves as an exploratory tool for understanding potential market rhythms, encouraging traders to test and visualize how Fibonacci principles extend beyond their traditional applications.

🖼️ CHART EXAMPLES 🖼️

Following this downtrend, price interacts with curved Fibonacci levels, highlighting resistance at the 0.236 and 0.382 levels, where price stalls before pulling back. Support emerges at the 0.5, 0.618, and 0.786 levels, where price finds stability and rebounds

In this Fibonacci retracement, price initially finds support at the 1.0 level, following the natural curvature of the cycle. Resistance forms at 0.786, leading to a pullback before price breaks through and tests 0.618 as resistance. Once 0.618 is breached, price moves upward to test 0.5, illustrating how Fibonacci-based cycles may align with evolving market structure beyond static, horizontal retracements.

Following this uptrend, price retraces downward and interacts with the Fibonacci levels, demonstrating both support and resistance at key levels such as 0.236, 0.382, 0.5, and 0.618.

With only the 0.5 and 1.0 levels enabled, this chart remains uncluttered while still highlighting key price interactions. The short cycle length results in a mild curvature, aligning smoothly with market movement. Price finds resistance at the 0.5 level while showing strong support at 1.0, which follows the natural flow of the market. Keeping the focus on fewer levels helps maintain clarity while still capturing how price reacts within the cycle.

🛠️ CONFIGURATION AND SETTINGS 🛠️

Wave Parameters

Wavelength : Stretches or compresses the wave along the time axis, determining the length of one full cycle. Higher values extend the wave across more bars, while lower values compress it into a shorter time frame.

Amplitude : Expands or contracts the wave along the price axis, determining the height of oscillations relative to Fibonacci levels. Higher values increase the vertical range, while negative values invert the wave’s initial direction.

Phase : Offsets the wave along the time axis, adjusting where the cycle begins. Higher values shift the starting position forward within the wave pattern.

Fibonacci Levels

Levels : Enable or disable specific Fibonacci levels (0.0, 0.236, 0.382, 0.5, 0.618, 0.786, 1.0) to focus on relevant price zones.

Color : Modify level colors for enhanced visual clarity.

Visibility

Trend Line/Color : Toggle and customize the trend line connecting swing points A and B.

Setup Lines : Show or hide lines linking Fibonacci levels to projected waves.

A/B Labels Visibility : Control the visibility of swing point labels.

Left/Right Labels : Manage the display of Fibonacci level labels on both sides of the chart.

Fill % : Adjust shading intensity between Fibonacci levels (0% = no fill, 100% = maximum fill).

A and B Points (Time/Price):

These user-defined anchor points serve as the basis for Fibonacci wave calculations and can be manually set. A and B points can also be adjusted directly on the chart, with automatic synchronization to the settings panel, allowing for seamless modifications without needing to manually input values.

⚠️ DISCLAIMER ⚠️

The Fibonacci Cycle Finder is a visual analysis tool designed to illustrate Fibonacci relationships and serve as a supplement to traditional Fibonacci tools. While the indicator employs mathematical and geometric principles, no guarantee is made that its calculations will align with other Fibonacci tools or proprietary methods. Like all technical and visual indicators, the Fibonacci levels generated by this tool may appear to visually align with key price zones in hindsight. However, these levels are not intended as standalone signals for trading decisions. This indicator is intended for educational and analytical purposes, complementing other tools and methods of market analysis.

🧠 BEYOND THE CODE 🧠

Fibonacci Cycle Finder is the latest indicator in the Fibonacci Geometry Series. Building on the concepts of the Fibonacci Time-Price Zones and the Fibonacci 3-D indicators, this tool introduces a trigonometric approach to market structure analysis.

The Fibonacci Cycle Finder indicator, like other xxattaxx indicators , is designed to encourage both education and community engagement. Your feedback and insights are invaluable to refining and enhancing the Fibonacci Cycle Finder indicator. We look forward to the creative applications, observations, and discussions this tool inspires within the trading community.

Accurate Bollinger Bands mcbw_ [True Volatility Distribution]The Bollinger Bands have become a very important technical tool for discretionary and algorithmic traders alike over the last decades. It was designed to give traders an edge on the markets by setting probabilistic values to different levels of volatility. However, some of the assumptions that go into its calculations make it unusable for traders who want to get a correct understanding of the volatility that the bands are trying to be used for. Let's go through what the Bollinger Bands are said to show, how their calculations work, the problems in the calculations, and how the current indicator I am presenting today fixes these.

--> If you just want to know how the settings work then skip straight to the end or click on the little (i) symbol next to the values in the indicator settings window when its on your chart <--

--------------------------- What Are Bollinger Bands ---------------------------

The Bollinger Bands were formed in the 1980's, a time when many retail traders interacted with their symbols via physically printed charts and computer memory for personal computer memory was measured in Kb (about a factor of 1 million smaller than today). Bollinger Bands are designed to help a trader or algorithm see the likelihood of price expanding outside of its typical range, the further the lines are from the current price implies the less often they will get hit. With a hands on understanding many strategies use these levels for designated levels of breakout trades or to assist in defining price ranges.

--------------------------- How Bollinger Bands Work ---------------------------

The calculations that go into Bollinger Bands are rather simple. There is a moving average that centers the indicator and an equidistant top band and bottom band are drawn at a fixed width away. The moving average is just a typical moving average (or common variant) that tracks the price action, while the distance to the top and bottom bands is a direct function of recent price volatility. The way that the distance to the bands is calculated is inspired by formulas from statistics. The standard deviation is taken from the candles that go into the moving average and then this is multiplied by a user defined value to set the bands position, I will call this value 'the multiple'. When discussing Bollinger Bands, that trading community at large normally discusses 'the multiple' as a multiplier of the standard deviation as it applies to a normal distribution (gaußian probability). On a normal distribution the number of standard deviations away (which trades directly use as 'the multiple') you are directly corresponds to how likely/unlikely something is to happen:

1 standard deviation equals 68.3%, meaning that the price should stay inside the 1 standard deviation 68.3% of the time and be outside of it 31.7% of the time;

2 standard deviation equals 95.5%, meaning that the price should stay inside the 2 standard deviation 95.5% of the time and be outside of it 4.5% of the time;

3 standard deviation equals 99.7%, meaning that the price should stay inside the 3 standard deviation 99.7% of the time and be outside of it 0.3% of the time.

Therefore when traders set 'the multiple' to 2, they interpret this as meaning that price will not reach there 95.5% of the time.

---------------- The Problem With The Math of Bollinger Bands ----------------

In and of themselves the Bollinger Bands are a great tool, but they have become misconstrued with some incorrect sense of statistical meaning, when they should really just be taken at face value without any further interpretation or implication.

In order to explain this it is going to get a bit technical so I will give a little math background and try to simplify things. First let's review some statistics topics (distributions, percentiles, standard deviations) and then with that understanding explore the incorrect logic of how Bollinger Bands have been interpreted/employed.

---------------- Quick Stats Review ----------------

.

(If you are comfortable with statistics feel free to skip ahead to the next section)

.

-------- I: Probability distributions --------

When you have a lot of data it is helpful to see how many times different results appear in your dataset. To visualize this people use "histograms", which just shows how many times each element appears in the dataset by stacking each of the same elements on top of each other to form a graph. You may be familiar with the bell curve (also called the "normal distribution", which we will be calling it by). The normal distribution histogram looks like a big hump around zero and then drops off super quickly the further you get from it. This shape (the bell curve) is very nice because it has a lot of very nifty mathematical properties and seems to show up in nature all the time. Since it pops up in so many places, society has developed many different shortcuts related to it that speed up all kinds of calculations, including the shortcut that 1 standard deviation = 68.3%, 2 standard deviations = 95.5%, and 3 standard deviations = 99.7% (these only apply to the normal distribution). Despite how handy the normal distribution is and all the shortcuts we have for it are, and how much it shows up in the natural world, there is nothing that forces your specific dataset to look like it. In fact, your data can actually have any possible shape. As we will explore later, economic and financial datasets *rarely* follow the normal distribution.

-------- II: Percentiles --------

After you have made the histogram of your dataset you have built the "probability distribution" of your own dataset that is specific to all the data you have collected. There is a whole complicated framework for how to accurately calculate percentiles but we will dramatically simplify it for our use. The 'percentile' in our case is just the number of data points we are away from the "middle" of the data set (normally just 0). Lets say I took the difference of the daily close of a symbol for the last two weeks, green candles would be positive and red would be negative. In this example my dataset of day by day closing price difference is:

week 1:

week 2:

sorting all of these value into a single dataset I have:

I can separate the positive and negative returns and explore their distributions separately:

negative return distribution =

positive return distribution =

Taking the 25th% percentile of these would just be taking the value that is 25% towards the end of the end of these returns. Or akin the 100%th percentile would just be taking the vale that is 100% at the end of those:

negative return distribution (50%) = -5

positive return distribution (50%) = +4

negative return distribution (100%) = -10

positive return distribution (100%) = +20

Or instead of separating the positive and negative returns we can also look at all of the differences in the daily close as just pure price movement and not account for the direction, in this case we would pool all of the data together by ignoring the negative signs of the negative reruns

combined return distribution =

In this case the 50%th and 100%th percentile of the combined return distribution would be:

combined return distribution (50%) = 4

combined return distribution (100%) = 10

Sometimes taking the positive and negative distributions separately is better than pooling them into a combined distribution for some purposes. Other times the combined distribution is better.

Most financial data has very different distributions for negative returns and positive returns. This is encapsulated in sayings like "Price takes the stairs up and the elevator down".

-------- III: Standard Deviation --------

The formula for the standard deviation (refereed to here by its shorthand 'STDEV') can be intimidating, but going through each of its elements will illuminate what it does. The formula for STDEV is equal to:

square root ( (sum ) / N )

Going back the the dataset that you might have, the variables in the formula above are:

'mean' is the average of your entire dataset

'x' is just representative of a single point in your dataset (one point at a time)

'N' is the total number of things in your dataset.

Going back to the STDEV formula above we can see how each part of it works. Starting with the '(x - mean)' part. What this does is it takes every single point of the dataset and measure how far away it is from the mean of the entire dataset. Taking this value to the power of two: '(x - mean) ^ 2', means that points that are very far away from the dataset mean get 'penalized' twice as much. Points that are very close to the dataset mean are not impacted as much. In practice, this would mean that if your dataset had a bunch of values that were in a wide range but always stayed in that range, this value ('(x - mean) ^ 2') would end up being small. On the other hand, if your dataset was full of the exact same number, but had a couple outliers very far away, this would have a much larger value since the square par of '(x - mean) ^ 2' make them grow massive. Now including the sum part of 'sum ', this just adds up all the of the squared distanced from the dataset mean. Then this is divided by the number of values in the dataset ('N'), and then the square root of that value is taken.

There is nothing inherently special or definitive about the STDEV formula, it is just a tool with extremely widespread use and adoption. As we saw here, all the STDEV formula is really doing is measuring the intensity of the outliers.

--------------------------- Flaws of Bollinger Bands ---------------------------

The largest problem with Bollinger Bands is the assumption that price has a normal distribution. This is assumption is massively incorrect for many reasons that I will try to encapsulate into two points:

Price return do not follow a normal distribution, every single symbol on every single timeframe has is own unique distribution that is specific to only itself. Therefore all the tools, shortcuts, and ideas that we use for normal distributions do not apply to price returns, and since they do not apply here they should not be used. A more general approach is needed that allows each specific symbol on every specific timeframe to be treated uniquely.

The distributions of price returns on the positive and negative side are almost never the same. A more general approach is needed that allows positive and negative returns to be calculated separately.

In addition to the issues of the normal distribution assumption, the standard deviation formula (as shown above in the quick stats review) is essentially just a tame measurement of outliers (a more aggressive form of outlier measurement might be taking the differences to the power of 3 rather than 2). Despite this being a bit of a philosophical question, does the measurement of outlier intensity as defined by the STDEV formula really measure what we want to know as traders when we're experiencing volatility? Or would adjustments to that formula better reflect what we *experience* as volatility when we are actively trading? This is an open ended question that I will leave here, but I wanted to pose this question because it is a key part of what how the Bollinger Bands work that we all assume as a given.

Circling back on the normal distribution assumption, the standard deviation formula used in the calculation of the bands only encompasses the deviation of the candles that go into the moving average and have no knowledge of the historical price action. Therefore the level of the bands may not really reflect how the price action behaves over a longer period of time.

------------ Delivering Factually Accurate Data That Traders Need------------

In light of the problems identified above, this indicator fixes all of these issue and delivers statistically correct information that discretionary and algorithmic traders can use, with truly accurate probabilities. It takes the price action of the last 2,000 candles and builds a huge dataset of distributions that you can directly select your percentiles from. It also allows you to have the positive and negative distributions calculated separately, or if you would like, you can pool all of them together in a combined distribution. In addition to this, there is a wide selection of moving averages directly available in the indicator to choose from.

Hedge funds, quant shops, algo prop firms, and advanced mechanical groups all employ the true return distributions in their work. Now you have access to the same type of data with this indicator, wherein it's doing all the lifting for you.

------------------------------ Indicator Settings ------------------------------

.

---- Moving average ----

Select the type of moving average you would like and its length

---- Bands ----

The percentiles that you enter here will be pulled directly from the return distribution of the last 2,000 candles. With the typical Bollinger Bands, traders would select 2 standard deviations and incorrectly think that the levels it highlights are the 95.5% levels. Now, if you want the true 95.5% level, you can just enter 95.5 into the percentile value here. Each of the three available bands takes the true percentile you enter here.

---- Separate Positive & Negative Distributions----

If this box is checked the positive and negative distributions are treated indecently, completely separate from each other. You will see that the width of the top and bottom bands will be different for each of the percentiles you enter.

If this box is unchecked then all the negative and positive distributions are pooled together. You will notice that the width of the top and bottom bands will be the exact same.

---- Distribution Size ----

This is the number of candles that the price return is calculated over. EG: to collect the price return over the last 33 candles, the difference of price from now to 33 candles ago is calculated for the last 2,000 candles, to build a return distribution of 2000 points of price differences over 33 candles.

NEGATIVE NUMBERS(<0) == exact number of candles to include;

EG: setting this value to -20 will always collect volatility distributions of 20 candles

POSITIVE NUMBERS(>0) == number of candles to include as a multiple of the Moving Average Length value set above;

EG: if the Moving Average Length value is set to 22, setting this value to 2 will use the last 22*2 = 44 candles for the collection of volatility distributions

MORE candles being include will generally make the bands WIDER and their size will change SLOWER over time.

I wish you focus, dedication, and earnest success on your journey.

Happy trading :)

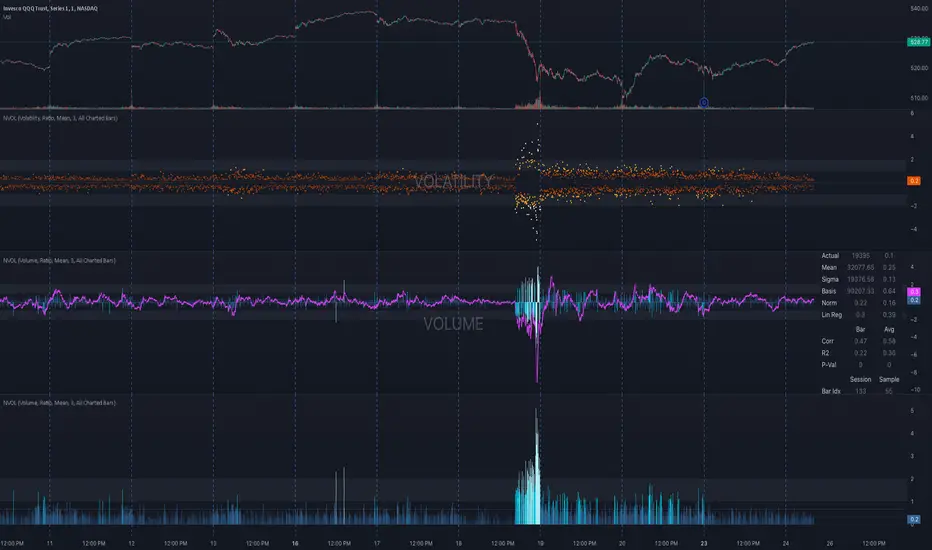

NVOL Normalized Volume & VolatilityOVERVIEW

Plots a normalized volume (or volatility) relative to a given bar's typical value across all charted sessions. The concept is similar to Relative Volume (RVOL) and Average True Range (ATR), but rather than using a moving average, this script uses bar data from previous sessions to more accurately separate what's normal from what's anomalous. Compatible on all timeframes and symbols.

Having volume and volatility processed within a single indicator not only allows you to toggle between the two for a consistent data display, it also allows you to measure how correlated they are. These measurements are available in the data table.

DATA & MATH

The core formula used to normalize each bar is:

( Value / Basis ) × Scale

Value

The current bar's volume or volatility (see INPUTS section). When set to volume, it's exactly what you would expect (the volume of the bar). When set to volatility, it's the bar's range (high - low).

Basis

A statistical threshold (Mean, Median, or Q3) plus a Sigma multiple (standard deviations). The default is set to the Mean + Sigma × 3 , which represents 99.7% of data in a normal distribution. The values are derived from the current bar's equivalent in other sessions. For example, if the current bar time is 9:30 AM, all previous 9:30 AM bars would be used to get the Mean and Sigma. Thus Mean + Sigma × 3 would represent the Normal Bar Vol at 9:30 AM.

Scale

Depends on the Normalize setting, where it is 1 when set to Ratio, and 100 when set to Percent. This simply determines the plot's scale (ie. 0 to 1 vs. 0 to 100).

INPUTS

While the default configuration is recommended for a majority of use cases (see BEST PRACTICES), settings should be adjusted so most of the Normalized Plot and Linear Regression are below the Signal Zone. Only the most extreme values should exceed this area.

Normalize

Allows you to specify what should be normalized (Volume or Volatility) and how it should be measured (as a Ratio or Percentage). This sets the value and scale in the core formula.

Basis

Specifies the statistical threshold (Mean, Median, or Q3) and how many standard deviations should be added to it (Sigma). This is the basis in the core formula.

Mean is the sum of values divided by the quantity of values. It's what most people think of when they say "average."

Median is the middle value, where 50% of the data will be lower and 50% will be higher.

Q3 is short for Third Quartile, where 75% of the data will be lower and 25% will be higher (think three quarters).

Sample

Determines the maximum sample size.

All Charted Bars is the default and recommended option, and ignores the adjacent lookback number.

Lookback is not recommended, but it is available for comparisons. It uses the adjacent lookback number and is likely to produce unreliable results outside a very specific context that is not suitable for most traders. Normalization is not a moving average. Unless you have a good reason to limit the sample size, do not use this option and instead use All Charted Bars .

Show Vol. name on plot

Overlays "VOLUME" or "VOLATILITY" on the plot (whichever you've selected).

Lin. Reg.

Polynomial regressions are great for capturing non-linear patterns in data. TradingView offers a "linear regression curve", which this script uses as a substitute. If you're unfamiliar with either term, think of this like a better moving average.

You're able to specify the color, length, and multiple (how much to amplify the value). The linear regression derives its value from the normalized values.

Norm. Val.

This is the color of the normalized value of the current bar (see DATA & MATH section). You're able to specify the default, within signal, and beyond signal colors. As well as the plot style.

Fade in colors between zero and the signal

Programmatically adjust the opacity of the primary plot color based on it's normalized value. When enabled, values equal to 0 will be fully transparent, become more opaque as they move away from 0, and be fully opaque at the signal. Adjusting opacity in this way helps make difference more obvious.

Plot relative to bar direction

If enabled, the normalized value will be multiplied by -1 when a bar's open is greater than the bar's close, mirroring price direction.

Technically volume and volatility are directionless. Meaning there's really no such thing as buy volume, sell volume, positive volatility, or negative volatility. There is just volume (1 buy = 1 sell = 1 volume) and volatility (high - low). Even so, visually reflecting the net effect of pricing pressure can still be useful. That's all this setting does.

Sig. Zone

Signal zones make identifying extremes easier. They do not signal if you should buy or sell, only that the current measurement is beyond what's normal. You are able to adjust the color and bounds of the zone.

Int. Levels

Interim levels can be useful when you want to visually bracket values into high / medium / low. These levels can have a value anywhere between 0 and 1. They will automatically be multiplied by 100 when the scale is set to Percent.

Zero Line

This setting allows you to specify the visibility of the zero line to best suit your trading style.

Volume & Volatility Stats

Displays a table of core values for both volume and volatility. Specifically the actual value, threshold (mean, median, or Q3), sigma (standard deviation), basis, normalized value, and linear regression.

Correlation Stats

Displays a table of correlation statistics for the current bar, as well as the data set average. Specifically the coefficient, R2, and P-Value.

Indices & Sample Size

Displays a table of mixed data. Specifically the current bar's index within the session, the current bar's index within the sample, and the sample size used to normalize the current bar's value.

BEST PRACTICES

NVOL can tell you what's normal for 9:30 AM. RVOL and ATR can only tell you if the current value is higher or lower than a moving average.

In a normal distribution (bell curve) 99.7% of data occurs within 3 standard deviations of the mean. This is why the default basis is set to "Mean, 3"; it includes the typical day-to-day fluctuations, better contextualizing what's actually normal, minimizing false positives.

This means a ratio value greater than 1 only occurs 0.3% of the time. A series of these values warrants your attention. Which is why the default signal zone is between 1 and 2. Ratios beyond 2 would be considered extreme with the default settings.

Inversely, ratio values less than 1 (the normal daily fluctuations) also tell a story. We should expect most values to occur around the middle 3rd, which is why interim levels default to 0.33 and 0.66, visually simplifying a given move's participation. These can be set to whatever you like and only serve as visual aids for your specific trading style.

It's worth noting that the linear regression oscillates when plotted directionally, which can help clarify short term move exhaustion and continuation. Akin to a relative strength index (RSI), it may be used to inform a trading decision, but it should not be the only factor.

Fibonacci Time-Price Zones🟩 Fibonacci Time-Price Zones is a chart visualization tool that combines Fibonacci ratios with time-based and price-based geometry to analyze market behavior. Unlike typical Fibonacci indicators that focus solely on horizontal price levels, this indicator incorporates time into the analysis, providing a more dynamic perspective on price action.

The indicator offers multiple ways to visualize Fibonacci relationships. Drawing segmented circles creates a unique perspective on price action by incorporating time into the analysis. These segmented circles, similar to TradingView's built-in Fibonacci Circles, are derived from Fibonacci time and price levels, allowing traders to identify potential turning points based on the dynamic interaction between price and time.

As another distinct visualization method, the indicator incorporates orthogonal patterns, created by the intersection of horizontal and vertical Fibonacci levels. These intersections form L-shaped connections on the chart, derived from key Fibonacci price and time intervals, highlighting potential areas of support or resistance at specific points in time.

In addition to these geometric approaches, another option is sloped lines, which project Fibonacci levels that account for both time and price along the trendline. These projections derive their angles from the interplay between Fibonacci price levels and Fibonacci time intervals, creating dynamic zones on the chart. The slope of these lines reflects the direction and angle of the trend, providing a visual representation of price alignment with market direction, while maintaining the time-price relationship unique to this indicator

The indicator also includes horizontal Fibonacci levels similar to traditional retracement and extension tools. However, unlike standard tools, traders can display retracement levels, extension levels, or both simultaneously from a single instance of the indicator. These horizontal levels maintain consistency with the chosen visualization method, automatically scaling and adapting whether used with circles, orthogonal patterns, or slope-based analysis.

By combining these distinct methods—circles, orthogonal patterns, sloped projections, and horizontal levels—the indicator provides a comprehensive approach to Fibonacci analysis based on both time and price relationships. Each visualization method offers a unique perspective on market structure while maintaining the core principle of time-price interaction.

⭕ THEORY AND CONCEPT ⭕

While traditional Fibonacci tools excel at identifying potential support and resistance levels through price-based ratios (0.236, 0.382, 0.618), they do not incorporate the dimension of time in market analysis. Extensions and retracements effectively measure price relationships within trends, yet markets move through both price and time dimensions simultaneously.

Fibonacci circles represent an evolution in technical analysis by incorporating time intervals alongside price levels. Based on the mathematical principle that markets often move in circular patterns proportional to Fibonacci ratios, these circles project potential support and resistance zones as partial circles radiating from significant price points. However, traditional circle-based tools can create visual complexity that obscures key market relationships. The integration of time into Fibonacci analysis reveals how price movements often respect both temporal and price-based ratios, suggesting a deeper geometric structure to market behavior.

The Fibonacci Time-Price Zones indicator advances these concepts by providing multiple geometric approaches to visualize time-price relationships. Each shape option—circles, orthogonal patterns, slopes, and horizontal levels—represents a different mathematical perspective on how Fibonacci ratios manifest across both dimensions. This multi-faceted approach allows traders to observe how price responds to Fibonacci-based zones that account for both time and price movements, potentially revealing market structure that purely price-based tools might miss.

Shape Options

The indicator employs four distinct geometric approaches to analyze Fibonacci relationships across time and price dimensions:

Circular : Represents the cyclical nature of market movements through partial circles, where each radius is scaled by Fibonacci ratios incorporating both time and price components. This geometry suggests market movements may follow proportional circular paths from significant pivot points, reflecting the harmonic relationship between time and price.

Orthogonal : Constructs L-shaped patterns that separate the time and price components of Fibonacci relationships. The horizontal component represents price levels, while the vertical component measures time intervals, allowing analysis of how these dimensions interact independently at key market points.

Sloped : Projects Fibonacci levels along the prevailing trend, incorporating both time and price in the angle of projection. This approach suggests that support and resistance levels may maintain their relationship to price while adjusting to the temporal flow of the market.

Horizontal : Provides traditional static Fibonacci levels that serve as a reference point for comparing price-only analysis with the dynamic time-price relationships shown in the other three shapes. This baseline approach allows traders to evaluate how the incorporation of time dimension enhances or modifies traditional Fibonacci analysis.

By combining these geometric approaches, the Fibonacci Time-Price Zones indicator creates a comprehensive analytical framework that bridges traditional and advanced Fibonacci analysis. The horizontal levels serve as familiar reference points, while the dynamic elements—circular, orthogonal, and sloped projections—reveal how price action responds to temporal relationships. This multi-dimensional approach enables traders to study market structure through various geometric lenses, providing deeper insights into time-price symmetry within technical analysis. Whether applied to retracements, extensions, or trend analysis, the indicator offers a structured methodology for understanding how markets move through both price and time dimensions.

🛠️ CONFIGURATION AND SETTINGS 🛠️

The Fibonacci Time-Price Zones indicator offers a range of configurable settings to tailor its functionality and visual representation to your specific analysis needs. These options allow you to customize zone visibility, structures, horizontal lines, and other features.

Important Note: The indicator's calculations are anchored to user-defined start and end points on the chart. When switching between charts with significantly different price scales (e.g., from Bitcoin at $100,000 to Silver at $30), adjustment of these anchor points is required to ensure correct positioning of the Fibonacci elements.

Fibonacci Levels

The indicator allows users to customize Fibonacci levels for both retracement and extension analysis. Each level can be individually configured with the following options:

Visibility : Toggle the visibility of each level to focus on specific areas of interest.

Level Value : Set the Fibonacci ratio for the level, such as 0.618 or 1.000, to align with your analysis needs.

Color : Customize the color of each level for better visual clarity.

Line Thickness : Adjust the line thickness to emphasize critical levels or maintain a cleaner chart.

Setup

Zone Type : Select which Fibonacci zones to display:

- Retracement : Shows potential pull back levels within the trend

- Extension : Projects levels beyond the trend for potential continuation targets

- Both : Displays both retracement and extension zones simultaneously

Shape : Choose from four visualization methods:

- Circular : Time-price based semicircles centered on point B

- Orthogonal : L-shaped patterns combining time and price levels

- Sloped : Trend-aligned projections of Fibonacci levels

- Horizontal : Traditional horizontal Fibonacci levels

Visual Settings

Fill % : Adjusts the fill intensity of zones:

0% : No fill between levels

100% : Maximum fill between levels

Lines :

Trendline : The base A-B trend with customizable color

Extension : B-C projection line

Retracement : B-D pullback line

Labels :

Points : Show/hide A, B, C, D markers

Levels : Show/hide Fibonacci percentages

Time-Price Points

Set the time and price for the points that define the Fibonacci zones and horizontal levels. These points are defined upon loading the chart. These points can be configured directly in the settings or adjusted interactively on the live chart.

A and B Points : These user-defined time and price points determine the basis for calculating the semicircles and Fibonacci levels. While the settings panel displays their exact values for fine-tuning, the easiest way to modify these points is by dragging them directly on the chart for quick adjustments.

Interactive Adjustments : Any changes made to the points on the chart will automatically synchronize with the settings panel, ensuring consistency and precision.

🖼️ CHART EXAMPLES 🖼️

Fibonacci Time-Price Zones using the 'Circular' Shape option. Note the price interaction at the 0.786 level, which acts as a support zone. Additional points of interest include resistance near the 0.618 level and consolidation around the 0.5 level, highlighting the utility of both horizontal and semicircular Fibonacci projections in identifying key price areas.

Fibonacci Time-Price Zones using the 'Sloped' Shape option. The chart displays price retracing along the sloped Fibonacci levels, with blue arrows highlighting potential support zones at 0.618 and 0.786, and a red arrow indicating potential resistance at the 1.0 level. This visual representation aligns with the prevailing downtrend, suggesting potential selling pressure at the 1.0 Fibonacci level.

Fibonacci Time-Price Zones using the 'Orthogonal' Shape option. The chart demonstrates price action interacting with vertical zones created by the orthogonal lines at the 0.618, 0.786, and 1.0 Fibonacci levels. Blue arrows highlight potential support areas, while red arrows indicate potential resistance areas, revealing how the orthogonal lines can identify distinct points of price interaction.

Fibonacci Time-Price Zones using the 'Circular' Shape option. The chart displays price action in relation to segmented circles emanating from the starting point (point A). The circles represent different Fibonacci ratios (0.382, 0.5, 0.618, 0.786) and their intersections with the price axis create potential zones of support and resistance. This approach offers a visually distinct way to analyze potential turning points based on both price and time.

Fibonacci Time-Price Zones using the 'Sloped' Shape option. The sloped Fibonacci levels (0.786, 0.618, 0.5) create zones of potential support and resistance, with price finding clear interaction within these areas. The ellipses highlight this price action, particularly the support between 0.786 and 0.618, which aligns closely with the trend.

Fibonacci Time-Price Zones using the 'Circular' Shape option. The price action appears to be ‘hugging’ the 0.5 Fibonacci level, suggesting potential resistance. This demonstrates how the circular zones can identify potential turning points and areas of consolidation which might not be seen with linear analysis.

Fibonacci Time-Price Zones using the 'Sloped' Shape option with Point D marker enabled. The chart demonstrates clear price action closely following along the sloped Retracement line until the orthogonal intersection at the 0.618 levels where the trend is broken and price dips throughout the 0.618 to 0.786 horizontal zone. Price jumps back to the retracement slope at the start of the 0.786 horizontal zone and continues to the 1.0 horizontal zone. The aqua-colored retracement line is enabled to further emphasize this retracement slope .

Geometric validation using TradingView's built-in Fibonacci Circle tool (overlaid). The alignment at the 0.5 and 1.0 levels demonstrates the indicator's consistent approximation of Fibonacci Circles.

Comparison of Fibonacci Time-Price Zones (Shape: Horizontal) with TradingView's Built-in Retracement and Extension Tools (overlaid): This example demonstrates how the Horizontal structure aligns with TradingView’s retracement and extension levels, allowing users to integrate multiple tools seamlessly. The Fibonacci circle connects retracement and extension zones, highlighting the potential relationship between past retracements and future extensions.

📐 GEOMETRIC FOUNDATIONS 📐

This indicator integrates circular and straight representations of Fibonacci levels, specifically the Circular , Orthogonal , Sloped , and Horizontal shape options. The geometric principles behind these shapes differ significantly, requiring distinct scaling methods for accurate representation. The Circular shape employs logarithmic scaling with radial expansion, where the distance from a central point determines the level's position, creating partial circles that align with TradingView's built-in Fibonacci Circle tool. The other three shapes utilize geometric progression scaling for linear extension from a starting point, resulting in straight lines that align with TradingView's built-in Fibonacci retracement and extension tools. Due to these distinct geometric foundations and scaling methods, perfectly aligning both the partial circles and straight lines simultaneously is mathematically constrained, though any differences are typically visually imperceptible.

The Circular shape's partial circles are calculated and scaled to align with TradingView's built-in Fibonacci Circles. These circles are plotted from the second swing point onward. This approach ensures consistent and accurate visualization across all market types, including those with gaps or closed sessions, which unlike 24/7 markets, do not have a direct one-to-one correspondence between bar indices and time. To maintain accurate geometric proportions across varying chart scales, the indicator calculates an aspect ratio by normalizing the proportional difference between vertical (price) and horizontal (time) distances of the swing points. This normalization factor ensures geometric shapes maintain their mathematical properties regardless of price scale magnitude or time period span, while maintaining the correct proportions of the geometric constructions at any chart zoom level.

The indicator automatically applies the appropriate scaling factor based on the selected shape option, optimizing either circular proportions and proper radius calculations for each Fibonacci level, or straight-line relationships between Fibonacci levels. These distinct scaling approaches maintain mathematical integrity while preserving the essential characteristics of each geometric representation, ensuring optimal visualization accuracy whether using circular or linear shapes.

⚠️ DISCLAIMER ⚠️

The Fibonacci Time-Price Zones indicator is a visual analysis tool designed to illustrate Fibonacci relationships through geometric constructions incorporating both curved and straight lines, providing a structured framework for identifying potential areas of price interaction. It is not intended as a predictive or standalone trading signal indicator.

The indicator calculates levels and projections using user-defined anchor points and Fibonacci ratios. While it aims to align with TradingView’s Fibonacci extension, retracement, and circle tools by employing mathematical and geometric formulas, no guarantee is made that its calculations are identical to TradingView's proprietary methods.

Like all technical and visual indicators, these visual representations may visually align with key price zones in hindsight, reflecting observed price dynamics. However, these visualizations are not standalone signals for trading decisions and should be interpreted as part of a broader analytical approach.

This indicator is intended for educational and analytical purposes, complementing other tools and methods of market analysis. Users are encouraged to integrate it into a comprehensive trading strategy, customizing its settings to suit their specific needs and market conditions.

🧠 BEYOND THE CODE 🧠

The Fibonacci Time-Price Zones indicator is designed to encourage both education and community engagement. By integrating time-sensitive geometry with Fibonacci-based frameworks, it bridges traditional grid-based analysis with dynamic time-price relationships. The inclusion of semicircles, horizontal levels, orthogonal structures, and sloped trends provides users with versatile tools to explore the interaction between price movements and temporal intervals while maintaining clarity and adaptability.

As an open-source tool, the indicator invites exploration, experimentation, and customization. Whether used as a standalone resource or alongside other technical strategies, it serves as a practical and educational framework for understanding market structure and Fibonacci relationships in greater depth.

Your feedback and contributions are essential to refining and enhancing the Fibonacci Time-Price Zones indicator. We look forward to the creative applications, adaptations, and insights this tool inspires within the trading community.

Financial Crisis Predictor - Doomsday ClockThe **Financial Crisis Predictor - Doomsday Clock** is a composite indicator that evaluates multiple market conditions to determine financial risk levels. It combines four key metrics: market volatility (via VIX), yield curve spread, stock market momentum, and credit risk (via high-yield spread). Each metric contributes to a weighted "risk score," scaled between 0 and 100, which helps gauge the probability of a financial crisis. Here's a breakdown of how it works:

### 1. **Market Volatility (VIX)**

- **How it's measured:**

- Uses the VIX index, which represents expected market volatility.

- Applies two exponential moving averages (EMAs) to smooth out the data—one fast and one slow.

- Triggers a signal if the fast EMA crosses above the slow EMA and VIX exceeds a defined threshold (default is 30).

- **Weighting:**

- Contributes up to 35% of the total risk score when active.

### 2. **Yield Curve Spread**

- **How it's measured:**

- Takes the difference between the yields of 10-year and 2-year U.S. Treasury bonds (inversion indicates recession risk).

- If the spread drops below a certain threshold (default is 0.2), it signals a potential recession.

- **Weighting:**

- Contributes up to 25% of the risk score.

### 3. **Stock Market Momentum**

- **How it's measured:**

- Analyzes the S&P 500 (SPY) using a 20-day EMA for price momentum.

- Checks for a cross under the 20-day EMA and if the 5-day rate of change (ROC) is less than -2.

- This combination signals bearish market momentum.

- **Weighting:**

- Contributes up to 20% of the risk score.

### 4. **Credit Risk (High Yield Spread)**

- **How it's measured:**

- Assesses high-yield corporate bond spreads using EMAs, similar to the VIX logic.

- A crossover of the fast EMA above the slow EMA combined with spreads exceeding a defined threshold (default is 5.0) indicates increased credit risk.

- **Weighting:**

- Contributes up to 20% of the total risk score.

### 5. **Risk Score Calculation**

- The final **risk score** ranges from 0 to 100 and is calculated using the weighted sum of the four indicators.

- The score is smoothed to minimize false signals and maintain stability.

### 6. **Risk Zones**

- **Extreme Risk:** If the risk score is ≥ 75, indicating a severe crisis warning.

- **High Risk:** If the risk score is between 15 and 75, signaling heightened risk.

- **Moderate Risk:** If the risk score is between 10 and 15, representing potential concerns.

- **Low Risk:** If the risk score is < 10, suggesting stable conditions.

### 7. **Visual & Alerts**

- The indicator plots the risk score on a chart with color-coded backgrounds to indicate risk levels: green (low), yellow (moderate), orange (high), and red (extreme).

- Alert conditions are set for each risk zone, notifying users when the risk level transitions into a higher zone.

This indicator aims to quickly detect potential financial crises by aggregating signals from key market factors, making it a versatile tool for traders, analysts, and risk managers.

Cosine-Weighted MA ATR [InvestorUnknown]The Cosine-Weighted Moving Average (CWMA) ATR (Average True Range) indicator is designed to enhance the analysis of price movements in financial markets. By incorporating a cosine-based weighting mechanism , this indicator provides a unique approach to smoothing price data and measuring volatility, making it a valuable tool for traders and investors.

Cosine-Weighted Moving Average (CWMA)

The CWMA is calculated using weights derived from the cosine function, which emphasizes different data points in a distinctive manner. Unlike traditional moving averages that assign equal weight to all data points, the cosine weighting allocates more significance to values at the edges of the data window. This can help capture significant price movements while mitigating the impact of outlier values.

The weights are shifted to ensure they remain non-negative, which helps in maintaining a stable calculation throughout the data series. The normalization of these weights ensures they sum to one, providing a proportional contribution to the average.

// Function to calculate the Cosine-Weighted Moving Average with shifted weights

f_Cosine_Weighted_MA(series float src, simple int length) =>

var float cosine_weights = array.new_float(0)

array.clear(cosine_weights) // Clear the array before recalculating weights

for i = 0 to length - 1

weight = math.cos((math.pi * (i + 1)) / length) + 1 // Shift by adding 1

array.push(cosine_weights, weight)

// Normalize the weights

sum_weights = array.sum(cosine_weights)

for i = 0 to length - 1

norm_weight = array.get(cosine_weights, i) / sum_weights

array.set(cosine_weights, i, norm_weight)

// Calculate Cosine-Weighted Moving Average

cwma = 0.0

if bar_index >= length

for i = 0 to length - 1

cwma := cwma + array.get(cosine_weights, i) * close

cwma

Cosine-Weighted ATR Calculation

The ATR is an essential measure of volatility, reflecting the average range of price movement over a specified period. The Cosine-Weighted ATR uses a similar weighting scheme to that of the CWMA, allowing for a more nuanced understanding of volatility. By emphasizing more recent price movements while retaining sensitivity to broader trends, this ATR variant offers traders enhanced insight into potential price fluctuations.

// Function to calculate the Cosine-Weighted ATR with shifted weights

f_Cosine_Weighted_ATR(simple int length) =>

var float cosine_weights_atr = array.new_float(0)

array.clear(cosine_weights_atr)

for i = 0 to length - 1

weight = math.cos((math.pi * (i + 1)) / length) + 1 // Shift by adding 1

array.push(cosine_weights_atr, weight)

// Normalize the weights

sum_weights_atr = array.sum(cosine_weights_atr)

for i = 0 to length - 1

norm_weight_atr = array.get(cosine_weights_atr, i) / sum_weights_atr

array.set(cosine_weights_atr, i, norm_weight_atr)

// Calculate Cosine-Weighted ATR using true ranges

cwatr = 0.0

tr = ta.tr(true) // True Range

if bar_index >= length

for i = 0 to length - 1

cwatr := cwatr + array.get(cosine_weights_atr, i) * tr

cwatr

Signal Generation

The indicator generates long and short signals based on the relationship between the price (user input) and the calculated upper and lower bands, derived from the CWMA and the Cosine-Weighted ATR. Crossover conditions are used to identify potential entry points, providing a systematic approach to trading decisions.

// - - - - - CALCULATIONS - - - - - //{

bar b = bar.new()

float src = b.calc_src(cwma_src)

float cwma = f_Cosine_Weighted_MA(src, ma_length)

// Use normal ATR or Cosine-Weighted ATR based on input

float atr = atr_type == "Normal ATR" ? ta.atr(atr_len) : f_Cosine_Weighted_ATR(atr_len)

// Calculate upper and lower bands using ATR

float cwma_up = cwma + (atr * atr_mult)

float cwma_dn = cwma - (atr * atr_mult)

float src_l = b.calc_src(src_long)

float src_s = b.calc_src(src_short)

// Signal logic for crossovers and crossunders

var int signal = 0

if ta.crossover(src_l, cwma_up)

signal := 1

if ta.crossunder(src_s, cwma_dn)

signal := -1

//}

Backtest Mode and Equity Calculation

To evaluate its effectiveness, the indicator includes a backtest mode, allowing users to test its performance on historical data:

Backtest Equity: A detailed equity curve is calculated based on the generated signals over a user-defined period (startDate to endDate).

Buy and Hold Comparison: Alongside the strategy’s equity, a Buy-and-Hold equity curve is plotted for performance comparison.

Visualization and Alerts

The indicator features customizable plots, allowing users to visualize the CWMA, ATR bands, and signals effectively. The colors change dynamically based on market conditions, with clear distinctions between long and short signals.

Alerts can be configured to notify users of crossover events, providing timely information for potential trading opportunities.

Sine-Weighted MA ATR [InvestorUnknown]The Sine-Weighted MA ATR is a technical analysis tool designed to emphasize recent price data using sine-weighted calculations , making it particularly well-suited for analyzing cyclical markets with repetitive patterns . The indicator combines the Sine-Weighted Moving Average (SWMA) and a Sine-Weighted Average True Range (SWATR) to enhance price trend detection and volatility analysis.

Sine-Weighted Moving Average (SWMA):

Unlike traditional moving averages that apply uniform or exponentially decaying weights, the SWMA applies Sine weights to the price data.

Emphasis on central data points: The Sine function assigns more weight to the middle of the lookback period, giving less importance to the beginning and end points. This helps capture the main trend more effectively while reducing noise from recent volatility or older data.

// Function to calculate the Sine-Weighted Moving Average

f_Sine_Weighted_MA(series float src, simple int length) =>

var float sine_weights = array.new_float(0)

array.clear(sine_weights) // Clear the array before recalculating weights

for i = 0 to length - 1

weight = math.sin((math.pi * (i + 1)) / length)

array.push(sine_weights, weight)

// Normalize the weights

sum_weights = array.sum(sine_weights)

for i = 0 to length - 1

norm_weight = array.get(sine_weights, i) / sum_weights

array.set(sine_weights, i, norm_weight)

// Calculate Sine-Weighted Moving Average

swma = 0.0

if bar_index >= length

for i = 0 to length - 1

swma := swma + array.get(sine_weights, i) * close

swma

Sine-Weighted ATR:

This is a variation of the Average True Range (ATR), which measures market volatility. Like the SWMA, the ATR is smoothed using Sine-based weighting, where central values are more heavily considered compared to the extremities. This improves sensitivity to changes in volatility while maintaining stability in highly volatile markets.

// Function to calculate the Sine-Weighted ATR

f_Sine_Weighted_ATR(simple int length) =>

var float sine_weights_atr = array.new_float(0)

array.clear(sine_weights_atr)

for i = 0 to length - 1

weight = math.sin((math.pi * (i + 1)) / length)

array.push(sine_weights_atr, weight)

// Normalize the weights

sum_weights_atr = array.sum(sine_weights_atr)

for i = 0 to length - 1

norm_weight_atr = array.get(sine_weights_atr, i) / sum_weights_atr

array.set(sine_weights_atr, i, norm_weight_atr)

// Calculate Sine-Weighted ATR using true ranges

swatr = 0.0

tr = ta.tr(true) // True Range

if bar_index >= length

for i = 0 to length - 1

swatr := swatr + array.get(sine_weights_atr, i) * tr

swatr

ATR Bands:

Upper and lower bands are created by adding/subtracting the Sine-Weighted ATR from the SWMA. These bands help identify overbought or oversold conditions, and when the price crosses these levels, it may generate long or short trade signals.

// - - - - - CALCULATIONS - - - - - //{

bar b = bar.new()

float src = b.calc_src(swma_src)

float swma = f_Sine_Weighted_MA(src, ma_length)

// Use normal ATR or Sine-Weighted ATR based on input

float atr = atr_type == "Normal ATR" ? ta.atr(atr_len) : f_Sine_Weighted_ATR(atr_len)

// Calculate upper and lower bands using ATR

float swma_up = swma + (atr * atr_mult)

float swma_dn = swma - (atr * atr_mult)

float src_l = b.calc_src(src_long)

float src_s = b.calc_src(src_short)

// Signal logic for crossovers and crossunders

var int signal = 0

if ta.crossover(src_l, swma_up)

signal := 1

if ta.crossunder(src_s, swma_dn)

signal := -1

//}

Signal Logic:

Long/Short Signals are triggered when the price crosses above or below the Sine-Weighted ATR bands

Backtest Mode and Equity Calculation

To evaluate its effectiveness, the indicator includes a backtest mode, allowing users to test its performance on historical data:

Backtest Equity: A detailed equity curve is calculated based on the generated signals over a user-defined period (startDate to endDate).

Buy and Hold Comparison: Alongside the strategy’s equity, a Buy-and-Hold equity curve is plotted for performance comparison.

Alerts

The indicator includes built-in alerts for both long and short signals, ensuring users are promptly notified when market conditions meet the criteria for an entry or exit.

Global Liquidity Index and DEMA1001. Global Liquidity Index:

The code calculates global liquidity from economic data from multiple countries and regions. Specifically, it aggregates money supply data from major economies such as the United States, Europe, China, and Japan, and sums and adjusts them to get a global liquidity index.

This index is calculated by summing data from different sources and subtracting the impact of some financial instruments (such as reverse repurchase agreements, etc.), and then converting the result into a number in trillions. This can help analyze the liquidity conditions in global money markets.

2. ROC SMA (Simple Moving Average of Rate of Change):

The code calculates the rate of change (ROC) of the global liquidity index, which is a way to measure the speed of change of the index.

Then, a simple moving average (SMA) is applied to the rate of change, which helps smooth the data and identify trends.

The ROC SMA curve is displayed in yellow to help users observe the trend of liquidity changes.

3. DEMA (Double Exponential Moving Average):

DEMA is a more complex moving average that attempts to reduce the lag of the moving average and provide a more sensitive trend response.

The calculation method is to first calculate a standard exponential moving average (EMA), then calculate the EMA of this EMA, and use these two results to calculate DEMA.

The code allows users to set the period length of DEMA (default is 100), which can adjust the speed of DEMA's response to price changes.

The DEMA curve is displayed in blue, helping users to more accurately capture the trends and changes of global liquidity indicators.

DrawingLibrary "Drawing"

User Defined types and methods for basic drawing structure. Consolidated from the earlier libraries - DrawingTypes and DrawingMethods

method get_price(this, bar)

get line price based on bar

Namespace types: Line

Parameters:

this (Line) : (series Line) Line object.

bar (int) : (series/int) bar at which line price need to be calculated

Returns: line price at given bar.

method init(this)

Namespace types: PolyLine

Parameters:

this (PolyLine)

method tostring(this, sortKeys, sortOrder, includeKeys)

Converts DrawingTypes/Point object to string representation

Namespace types: chart.point

Parameters:

this (chart.point) : DrawingTypes/Point object

sortKeys (bool) : If set to true, string output is sorted by keys.

sortOrder (int) : Applicable only if sortKeys is set to true. Positive number will sort them in ascending order whreas negative numer will sort them in descending order. Passing 0 will not sort the keys

includeKeys (array) : Array of string containing selective keys. Optional parmaeter. If not provided, all the keys are considered

Returns: string representation of DrawingTypes/Point

method tostring(this, sortKeys, sortOrder, includeKeys)

Converts DrawingTypes/LineProperties object to string representation

Namespace types: LineProperties

Parameters:

this (LineProperties) : DrawingTypes/LineProperties object

sortKeys (bool) : If set to true, string output is sorted by keys.

sortOrder (int) : Applicable only if sortKeys is set to true. Positive number will sort them in ascending order whreas negative numer will sort them in descending order. Passing 0 will not sort the keys

includeKeys (array) : Array of string containing selective keys. Optional parmaeter. If not provided, all the keys are considered

Returns: string representation of DrawingTypes/LineProperties

method tostring(this, sortKeys, sortOrder, includeKeys)

Converts DrawingTypes/Line object to string representation

Namespace types: Line

Parameters:

this (Line) : DrawingTypes/Line object

sortKeys (bool) : If set to true, string output is sorted by keys.

sortOrder (int) : Applicable only if sortKeys is set to true. Positive number will sort them in ascending order whreas negative numer will sort them in descending order. Passing 0 will not sort the keys

includeKeys (array) : Array of string containing selective keys. Optional parmaeter. If not provided, all the keys are considered

Returns: string representation of DrawingTypes/Line

method tostring(this, sortKeys, sortOrder, includeKeys)

Converts DrawingTypes/LabelProperties object to string representation

Namespace types: LabelProperties

Parameters:

this (LabelProperties) : DrawingTypes/LabelProperties object

sortKeys (bool) : If set to true, string output is sorted by keys.

sortOrder (int) : Applicable only if sortKeys is set to true. Positive number will sort them in ascending order whreas negative numer will sort them in descending order. Passing 0 will not sort the keys

includeKeys (array) : Array of string containing selective keys. Optional parmaeter. If not provided, all the keys are considered

Returns: string representation of DrawingTypes/LabelProperties

method tostring(this, sortKeys, sortOrder, includeKeys)

Converts DrawingTypes/Label object to string representation

Namespace types: Label

Parameters:

this (Label) : DrawingTypes/Label object

sortKeys (bool) : If set to true, string output is sorted by keys.

sortOrder (int) : Applicable only if sortKeys is set to true. Positive number will sort them in ascending order whreas negative numer will sort them in descending order. Passing 0 will not sort the keys

includeKeys (array) : Array of string containing selective keys. Optional parmaeter. If not provided, all the keys are considered

Returns: string representation of DrawingTypes/Label

method tostring(this, sortKeys, sortOrder, includeKeys)

Converts DrawingTypes/Linefill object to string representation

Namespace types: Linefill

Parameters:

this (Linefill) : DrawingTypes/Linefill object

sortKeys (bool) : If set to true, string output is sorted by keys.

sortOrder (int) : Applicable only if sortKeys is set to true. Positive number will sort them in ascending order whreas negative numer will sort them in descending order. Passing 0 will not sort the keys

includeKeys (array) : Array of string containing selective keys. Optional parmaeter. If not provided, all the keys are considered

Returns: string representation of DrawingTypes/Linefill

method tostring(this, sortKeys, sortOrder, includeKeys)

Converts DrawingTypes/BoxProperties object to string representation

Namespace types: BoxProperties

Parameters:

this (BoxProperties) : DrawingTypes/BoxProperties object

sortKeys (bool) : If set to true, string output is sorted by keys.

sortOrder (int) : Applicable only if sortKeys is set to true. Positive number will sort them in ascending order whreas negative numer will sort them in descending order. Passing 0 will not sort the keys

includeKeys (array) : Array of string containing selective keys. Optional parmaeter. If not provided, all the keys are considered

Returns: string representation of DrawingTypes/BoxProperties

method tostring(this, sortKeys, sortOrder, includeKeys)

Converts DrawingTypes/BoxText object to string representation

Namespace types: BoxText

Parameters:

this (BoxText) : DrawingTypes/BoxText object

sortKeys (bool) : If set to true, string output is sorted by keys.

sortOrder (int) : Applicable only if sortKeys is set to true. Positive number will sort them in ascending order whreas negative numer will sort them in descending order. Passing 0 will not sort the keys

includeKeys (array) : Array of string containing selective keys. Optional parmaeter. If not provided, all the keys are considered

Returns: string representation of DrawingTypes/BoxText

method tostring(this, sortKeys, sortOrder, includeKeys)

Converts DrawingTypes/Box object to string representation

Namespace types: Box

Parameters:

this (Box) : DrawingTypes/Box object

sortKeys (bool) : If set to true, string output is sorted by keys.