ETF Leverage VerificationDo leveraged ETFs really return what they promise?

Do they return the exact 2x or 3x? Or a slightly different multiple?

How much do they deviate from the promised leverage multiples?

Do these deviations impact investors in a positive or negative manner?

These are the questions that I want to answer with this indicator.

The ETF Leverage Verification indicator challenges the conventional understanding of leveraged ETFs by measuring how they actually perform versus their theoretical targets.

Instead of assuming leveraged ETFs perfectly track their target multiple, this indicator quantifies the real-world behavior by comparing the expected returns versus the actual results on every trading day.

Key Features

Measures actual versus expected performance of leveraged ETFs

Tracks deviation patterns across thousands of trading days

Identifies asymmetric behavior in up versus down markets

Quantifies beneficial "cushioning effect" during market declines

Provides statistical summary of performance patterns

Works with any leverage factor (2x, 3x, -1x, etc.)

Compatible with all leveraged ETFs (equity, bond, commodity, volatility)

How to Use the Indicator

Enter the Expected Leverage Factor (default: 2.0)

Select the Base Asset (underlying index, e.g., SPX)

Select the Leveraged Asset (leveraged ETF, e.g., SSO)

Understanding the Results

Green markers: Days when the ETF outperformed its expected multiple

Red markers: Days when the ETF underperformed its expected multiple

Data Table:

Positive Deviations: Count of days with better-than-expected performance

Negative Deviations: Count of days with worse-than-expected performance

Avg Deviation: Average magnitude of deviation from expected returns

Frequency Skew: Difference between beneficial deviations in down vs. up markets

Impact: Overall assessment of pattern benefit to investors

Summary Label:

Percentage of positive deviations in up and down markets

Total sample size for statistical significance

Key Patterns to Look For

Positive Deviation in Negative Days:

This occurs when a leveraged ETF falls less than expected during market declines. For example, if SPX falls 1% and a 2x ETF falls only 1.8% (instead of the expected 2%), this creates a +0.2% deviation. This pattern is beneficial as it provides downside protection.

Negative Deviation in Positive Days:

This happens when a leveraged ETF rises less than expected during market advances. For example, if SPX rises 1% and a 2x ETF rises only 1.9% (instead of the expected 2%), this creates a -0.1% deviation. This pattern reduces upside performance.

Frequency Skew:

The most critical metric that measures how much more frequently beneficial deviations occur in down markets compared to up markets. A higher positive skew indicates a stronger asymmetric pattern that helps long-term performance.

Mathematical Background

The indicator computes the deviation between expected and actual performance:

Deviation = Actual Return - Expected Return

Where:

Expected Return = Base Asset Return × Leverage Factor

The deviation is then categorized into four possible outcomes:

Positive deviation on positive market days

Negative deviation on positive market days

Positive deviation on negative market days

Negative deviation on negative market days

In short, more positive deviations are good for investors.

Please feel free to criticize. I'm happy to improve the indicator.

"etf当天可以买卖吗"に関するスクリプトを検索

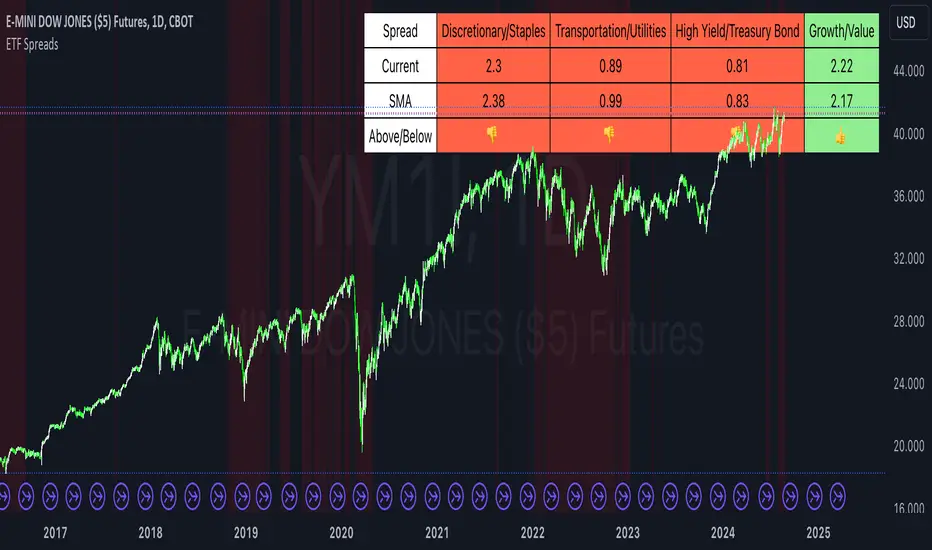

ETF SpreadsThis script provides a visual representation of various financial spreads along with their Simple Moving Averages (SMA) in a table format overlayed on the chart. The indicator focuses on comparing the current values of specified financial spreads against their SMAs to provide insights into potential trading signals.

Key Components:

SMA Length Input:

Users can input the length of the SMA, which determines the period over which the average is calculated. The default length is set to 20 days.

Symbols for Spreads:

The indicator tracks the closing prices of eight different financial instruments: XLY (Consumer Discretionary ETF), XLP (Consumer Staples ETF), IYT (Transportation ETF), XLU (Utilities ETF), HYG (High Yield Bond ETF), TLT (Long-Term Treasury Bond ETF), VUG (Growth ETF), and VTV (Value ETF).

Spread Calculations:

The script calculates spreads between different pairs of these instruments. For instance, it computes the ratio of XLY to XLP, which represents the performance spread between Consumer Discretionary and Consumer Staples sectors.

SMA Calculations:

SMAs for each spread are calculated to serve as a benchmark for comparing current spread values.

Table Display:

The indicator displays a table in the top-right corner of the chart with the following columns: Spread Name, Current Spread Value, SMA Value, and Status (indicating whether the current spread is above or below its SMA).

Status and Background Color:

The indicator uses colored backgrounds to show whether the current spread is above (light green) or below (tomato red) its SMA. Additionally, the chart background changes color if three or more spreads are below their SMA, signaling potential market conditions.

Scientific Literature on Spreads and Their Importance for Portfolio Management

"The Value of Financial Spreads in Portfolio Diversification"

Authors: G. Gregoriou, A. Z. P. G. Constantinides

Journal: Financial Markets, Institutions & Instruments, 2012

Abstract: This study explores how financial spreads between different asset classes can enhance portfolio diversification and reduce overall risk. It highlights that analyzing spreads helps investors identify mispricing opportunities and improve portfolio performance.

"The Role of Spreads in Investment Strategy and Risk Management"

Authors: R. J. Hodrick, E. S. S. Zhang

Journal: Journal of Portfolio Management, 2010

Abstract: This paper discusses the significance of spreads in investment strategies and their impact on risk management. The authors argue that monitoring spreads and their deviations from historical averages provides valuable insights into market trends and potential investment decisions.

"Spread Trading: An Overview and Its Use in Portfolio Management"

Authors: J. M. M. Perkins, L. A. B. Smith

Journal: Financial Review, 2009

Abstract: This review article provides an overview of spread trading techniques and their applications in portfolio management. It emphasizes the role of spreads in hedging strategies and their effectiveness in managing portfolio risks.

"Analyzing Financial Spreads for Better Portfolio Allocation"

Authors: A. S. Dechow, J. E. Stambaugh

Journal: Journal of Financial Economics, 2007

Abstract: The authors analyze various methods of financial spread calculations and their implications for portfolio allocation decisions. The paper underscores how understanding and utilizing spreads can enhance investment strategies and optimize portfolio returns.

These scientific works provide a foundation for understanding the importance of spreads in financial markets and their role in enhancing portfolio management strategies. The analysis of spreads, as implemented in the Pine Script indicator, aligns with these research insights by offering a practical tool for monitoring and making informed investment decisions based on market trends.

Sector ETF macro trendThe Sector ETF Macro Trend indicator is designed for technical analysis of broad economic trends through sector-specific exchange-traded funds (ETFs). It uses logarithmic price transformation, linear regression, and volatility analysis to examine sector trends and stability, providing a technical basis for analytical assessment.

Core Analysis Techniques

Logarithmic Transformation and Regression: Converts ETF closing prices logarithmically to reveal sector growth patterns and dynamics. Linear regression on these prices defines the main trend direction, essential for trend analysis.

Volatility Bands for Market State Assessment: Applies standard deviation on logarithmic prices to create dynamic bands around the trendline, identifying overbought or oversold sector conditions by marking deviations from the central trend.

Sector-Specific Analysis: Selection among different sector ETFs allows for precise examination of sectors like technology, healthcare, and financials, enabling focused insights into specific market segments.

Adaptability and Insight

Customizable Parameters: Offers flexibility in modifying regression length and smoothing factors to accommodate various analysis strategies and risk preferences.

Trend Direction and Momentum: Evaluates the ETF's trajectory against historical data and volatility bands to determine sector trend strength and direction, aiding in the prediction of market shifts.

Strategic Application

Without providing explicit trading signals, the indicator focuses on trend and volatility analysis for a strategic view on sector investments. It supports:

Identifying macroeconomic trends through ETF performance analysis.

Informing portfolio decisions with insights into sector momentum and stability.

Forecasting market movements by analyzing overbought or oversold conditions against the ETF price movement and volatility bands.

The Sector ETF Macro Trend indicator serves as a technical tool for analyzing sector-level market trends, offering detailed insights into the dynamics of economic sectors for thorough market analysis.

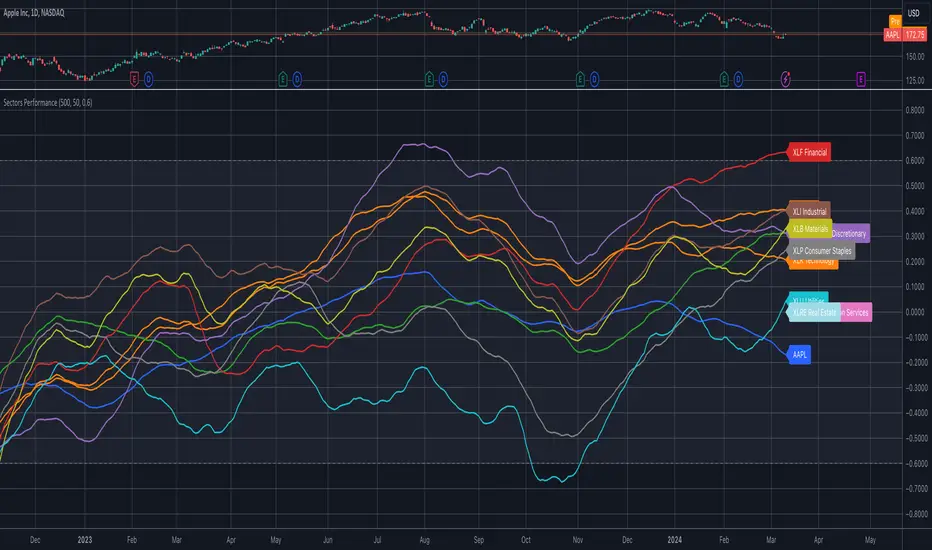

Sector ETFs performance overviewThe indicator provides a nuanced view of sector performance through ETF analysis, focusing on long-term price trends and deviations from these trends to gauge relative strength or weakness. It utilizes a methodical approach to smooth out ETF price data and then applies a regression analysis to pinpoint the primary trend direction. By examining how far the current price deviates from this regression line, the indicator identifies potential overbought or oversold conditions within various sectors.

Core Analysis Techniques:

Logarithmic Transformation and Regression: This process transforms ETF closing prices on a logarithmic scale to better understand sector growth patterns and dynamics. A linear regression of these prices helps define the overarching trend, crucial for understanding market movements.

Volatility Bands for Market State Assessment: The indicator calculates standard deviation based on logarithmic prices to establish dynamic bands around the regression line. These bands are instrumental in identifying market states, highlighting when sectors may be overextended from their central trend.

Sector-Specific Analysis: By focusing on distinct sector ETFs, the tool enables targeted analysis across various market segments. This specificity allows for a granular look at sectors like technology, healthcare, and financials, providing insights tailored to each area.

Adaptability and Insight:

Customizable Parameters: The indicator offers users the ability to adjust key parameters such as regression length and smoothing factors. This customization ensures that the analysis can be tailored to individual preferences and market outlooks.

Trend Direction and Momentum: It assesses the ETF's price movement relative to historical data and the established volatility bands, helping to clarify the sector's trend strength and potential directional shifts.

Strategic Application:

Focusing on trend and volatility analysis rather than direct trading signals, the indicator aids in forming a strategic view of sector investments. It's particularly useful for:

Spotting macroeconomic trends through the lens of sector ETF performance.

Informing portfolio decisions with nuanced insights into sector momentum and market conditions.

Anticipating potential market shifts by evaluating how current prices align with historical volatility and trend patterns.

This tool stands out as a vital resource for analyzing sector-level market trends, offering detailed insights into the dynamics of economic sectors for comprehensive market analysis.

Mongoose Capital: BTC ETF DriftScope ProMongoose Capital: BTC ETF DriftScope Pro

A proprietary indicator for monitoring drift between Bitcoin Spot (BTCUSD) and Bitcoin Spot ETFs (such as IBIT). Designed to detect ETF premium/discount zones and generate actionable Fade or Long bias signals.

What it Does

Tracks IBIT and BTCUSD spread to highlight ETF price deviations.

Calculates correlation Z-Score for ETF/Spot alignment.

Outputs numeric bias signals: Fade (1), Long (1), Neutral (1).

How to Use

Apply to a BTCUSD chart (4H, 1D, or higher recommended).

Open the Data Window to view:

IBIT Spread %

Correlation Z-Score

Correlation %

Bias Flags (Fade, Long, Neutral)

Configure alerts for Fade and Long Bias conditions.

Confirm all signals with your trade plan and risk management.

Methodology

This tool calculates the percentage spread between IBIT and BTC Spot. A rolling Z-Score of the correlation is used to detect periods of significant divergence.

Fade Bias suggests potential short setups in premium zones with high Z-Scores.

Long Bias suggests potential long setups in discount zones with low Z-Scores.

Disclaimer

This indicator is for educational purposes only. It is not financial advice. Use at your own risk and verify signals independently.

CE - Market Performance TableThe 𝓜𝓪𝓻𝓴𝓮𝓽 𝓟𝓮𝓻𝓯𝓸𝓻𝓶𝓪𝓷𝓬𝓮 𝓣𝓪𝓫𝓵𝓮 is a sophisticated market tool designed to provide valuable insights into the current market trends and the approximate current position in the Macroeconomic Regime.

Furthermore the 𝓜𝓪𝓻𝓴𝓮𝓽 𝓟𝓮𝓻𝓯𝓸𝓻𝓶𝓪𝓷𝓬𝓮 𝓣𝓪𝓫𝓵𝓮 provides the Correlation Implied Trend for the Asset on the Chart. Lastly it provides information about current "RISK ON" or "RISK OFF" periods.

Methodology:

𝓜𝓪𝓻𝓴𝓮𝓽 𝓟𝓮𝓻𝓯𝓸𝓻𝓶𝓪𝓷𝓬𝓮 𝓣𝓪𝓫𝓵𝓮 tracks the 15 underlying Stock ETF's to identify their performance and puts the combined performances together to visualize 42MACRO's GRID Equity Model.

For this it uses the below ETF's:

Dividends (SPHD)

Low Beta (SPLV)

Quality (QUAL)

Defensives (DEF)

Growth (IWF)

High Beta (SPHB)

Cyclicals (IYT, IWN)

Value (IWD)

Small Caps (IWM)

Mid Caps (IWR)

Mega Cap Growth (MGK)

Size (OEF)

Momentum (MTUM)

Large Caps (IWB)

Overall Settings:

The main time values you want to change are:

Correlation Length

- Defines the time horizon for the Correlation Table

ROC Period

- Defines the time horizon for the Performance Table

Normalization lookback

- Defines the time horizon for the Trend calculation of the ETF's

- For longer term Trends over weeks or months a length of 50 is usually pretty accurate

Visuals:

There is a variety of options to change the visual settings of what is being plotted and the two table positions and additional considerations.

Everything that is relevant in the underlying logic that can help comprehension can be visualized with these options.

Market Correlation:

The Market Correlation Table takes the Correlation of the above ETF's to the Asset on the Chart, it furthermore uses the Normalized KAMA Oscillator by IkkeOmar to analyse the current trend of every single ETF.

It then Implies a Correlation based on the Trend and the Correlation to give a probabilistically adjusted expectation for the future Chart Asset Movement. This is strengthened by taking the average of all Implied Trends.

With this the Correlation Table provides valuable insights about probabilistically likely Movement of the Asset, for Traders and Investors alike, over the defined time duration.

Market Performance:

𝓜𝓪𝓻𝓴𝓮𝓽 𝓟𝓮𝓻𝓯𝓸𝓻𝓶𝓪𝓷𝓬𝓮 𝓣𝓪𝓫𝓵𝓮 is the actual valuable part of this Indicator.

It provides valuable information about the current market environment (whether it's risk on or risk off), the rough GRID models from 42MACRO and the actual market performance.

This allows you to obtain a deeper understanding of how the market works and makes it simple to identify the actual market direction.

Utility:

The 𝓜𝓪𝓻𝓴𝓮𝓽 𝓟𝓮𝓻𝓯𝓸𝓻𝓶𝓪𝓷𝓬𝓮 𝓣𝓪𝓫𝓵𝓮 is divided in 4 Sections which are the GRID regimes:

Economic Growth:

Goldilocks

Reflation

Economic Contraction:

Inflation

Deflation

Top 5 Equity Style Factors:

Are the values green for a specific Column? If so then the market reflects the corresponding GRID behavior.

Bottom 5 Equity Style Factors:

Are the values red for a specific Column? If so then the market reflects the corresponding GRID behavior.

So if we have Goldilocks as current regime we would see green values in the Top 5 Goldilocks Cells and red values in the Bottom 5 Goldilocks Cells.

You will find that Reflation will look similar, as it is also a sign of Economic Growth.

Same is the case for the two Contraction regimes.

(SPY to ES) ETF→Futures Multi-Level (10 Levels + Select All)Converts selected ETF levels (SPY or QQQ) into equivalent futures levels (ES or NQ).

Uses live price ratio between ETF and futures for real-time level translation.

Supports 10 independent levels (A–J) with user-defined ETF price inputs.

Provides checkboxes to toggle each level’s visibility or show all at once.

Applies smoothing (ta.sma) to reduce noise from short-term price movement.

Lets user customize each line’s color, width, and style (solid, dashed, dotted).

Automatically updates lines as new bars form without user interaction.

Uses persistent line objects to keep levels stable when scrolling or zooming.

Adapts to either SPY→ES or QQQ→NQ depending on the “Convert SPY?” toggle.

Draws clean horizontal lines without legend clutter for visual precision.

SOME ONE PUBLISHED THIS FUNCTIONALITY FOR A CHARGE SO I MADE IT FREE.

-rA

Sector SPDR ETFsThis script automatically identifies the SPDR sector ETF that corresponds to the currently viewed US stock ticker. It maps over 500 US-listed stocks to their respective SPDR sector ETFs — such as XLK (Technology), XLF (Financials), XLY (Consumer Discretionary), and others — based on pre-defined symbol lists.

When applied to a chart, the script displays a label below the last candle showing the SPDR sector symbol (e.g., "XLE" for Energy stocks like XOM). This allows traders and investors to quickly understand the sector classification of any stock they analyze.

Key Features:

Maps tickers to SPDR sector ETFs: XLC, XLY, XLP, XLE, XLF, XLV, XLI, XLB, XLRE, XLK, and XLU.

Displays the corresponding sector label on the chart.

Helpful for sector rotation strategies, macro analysis, or thematic investing.

BTC ETF Inflows and Outflows with Combined BTC CorrelationThis script tracks Bitcoin Spot ETF inflows and outflows, calculating their correlation with Bitcoin's price to identify market trends and sentiment. It provides visual insights into ETF flows and the relationship with BTC price movements.

NOTE: The script relies on volume and opens / closes for calculating inflows and outflows. An ETF might issue more shares, which would skew the numbers.

Trailing Stops Only - For Leveraged ETFs (UGAZ/DGAZ)Looking for Statistical trades that work. This one seems to work on some Leveraged ETFs with a lot of noise like UGAZ/DGAZ. It can also be used on Futures Contracts, but be sure to change up the type of investment from % of equity to contracts. Also one point I'm trying to make with this strategy is the trades are best made in the morning around market open. When used with Contracts, be sure to make use of the time settings. It will limit buying between the hours set. Selling will occur at any time the trailing stop is triggered.

This Strategy is best used on 5min or 15min charts.

!!!! very important !!!!

Due to decay, leveraged ETFs will give false results if the price gets far out of range. For example, your ETF is trading around $20 and you choose a 1 hour chart, it may back test back to a time before a reverse split. If the price gets to be too large, like $200, or $1200, the movement on the chart creates false indication of profit/loss.

Most important. Do not trade off this strategy, you may lose lots of money. This is for educational use only.

Hyper SAR Reactor Trend StrategyHyperSAR Reactor Adaptive PSAR Strategy

Summary

Adaptive Parabolic SAR strategy for liquid stocks, ETFs, futures, and crypto across intraday to daily timeframes. It acts only when an adaptive trail flips and confirmation gates agree. Originality comes from a logistic boost of the SAR acceleration using drift versus ATR, plus ATR hysteresis, inertia on the trail, and a bear-only gate for shorts. Add to a clean chart and run on bar close for conservative alerts.

Scope and intent

• Markets: large cap equities and ETFs, index futures, major FX, liquid crypto

• Timeframes: one minute to daily

• Default demo: BTC on 60 minute

• Purpose: faster yet calmer PSAR that resists chop and improves short discipline

• Limits: this is a strategy that places simulated orders on standard candles

Originality and usefulness

• Novel fusion: PSAR AF is boosted by a logistic function of normalized drift, trail is monotone with inertia, entries use ATR buffers and optional cooldown, shorts are allowed only in a bear bias

• Addresses false flips in low volatility and weak downtrends

• All controls are exposed in Inputs for testability

• Yardstick: ATR normalizes drift so settings port across symbols

• Open source. No links. No solicitation

Method overview

Components

• Adaptive AF: base step plus boost factor times logistic strength

• Trail inertia: one sided blend that keeps the SAR monotone

• Flip hysteresis: price must clear SAR by a buffer times ATR

• Volatility gate: ATR over its mean must exceed a ratio

• Bear bias for shorts: price below EMA of length 91 with negative slope window 54

• Cooldown bars optional after any entry

• Visual SAR smoothing is cosmetic and does not drive orders

Fusion rule

Entry requires the internal flip plus all enabled gates. No weighted scores.

Signal rule

• Long when trend flips up and close is above SAR plus buffer times ATR and gates pass

• Short when trend flips down and close is below SAR minus buffer times ATR and gates pass

• Exit uses SAR as stop and optional ATR take profit per side

Inputs with guidance

Reactor Engine

• Start AF 0.02. Lower slows new trends. Higher reacts quicker

• Max AF 1. Typical 0.2 to 1. Caps acceleration

• Base step 0.04. Typical 0.01 to 0.08. Raises speed in trends

• Strength window 18. Typical 10 to 40. Drift estimation window

• ATR length 16. Typical 10 to 30. Volatility unit

• Strength gain 4.5. Typical 2 to 6. Steepness of logistic

• Strength center 0.45. Typical 0.3 to 0.8. Midpoint of logistic

• Boost factor 0.03. Typical 0.01 to 0.08. Adds to step when strength rises

• AF smoothing 0.50. Typical 0.2 to 0.7. Adds inertia to AF growth

• Trail smoothing 0.35. Typical 0.15 to 0.45. Adds inertia to the trail

• Allow Long, Allow Short toggles

Trade Filters

• Flip confirm buffer ATR 0.50. Typical 0.2 to 0.8. Raise to cut flips

• Cooldown bars after entry 0. Typical 0 to 8. Blocks re entry for N bars

• Vol gate length 30 and Vol gate ratio 1. Raise ratio to trade only in active regimes

• Gate shorts by bear regime ON. Bear bias window 54 and Bias MA length 91 tune strictness

Risk

• TP long ATR 1.0. Set to zero to disable

• TP short ATR 0.0. Set to 0.8 to 1.2 for quicker shorts

Usage recipes

Intraday trend focus

Confirm buffer 0.35 to 0.5. Cooldown 2 to 4. Vol gate ratio 1.1. Shorts gated by bear regime.

Intraday mean reversion focus

Confirm buffer 0.6 to 0.8. Cooldown 4 to 6. Lower boost factor. Leave shorts gated.

Swing continuation

Strength window 24 to 34. ATR length 20 to 30. Confirm buffer 0.4 to 0.6. Use daily or four hour charts.

Properties visible in this publication

Initial capital 10000. Base currency USD. Order size Percent of equity 3. Pyramiding 0. Commission 0.05 percent. Slippage 5 ticks. Process orders on close OFF. Bar magnifier OFF. Recalculate after order filled OFF. Calc on every tick OFF. No security calls.

Realism and responsible publication

No performance claims. Past results never guarantee future outcomes. Shapes can move while a bar forms and settle on close. Strategies execute only on standard candles.

Honest limitations and failure modes

High impact events and thin books can void assumptions. Gap heavy symbols may prefer longer ATR. Very quiet regimes can reduce contrast and invite false flips.

Open source reuse and credits

Public domain building blocks used: PSAR concept and ATR. Implementation and fusion are original. No borrowed code from other authors.

Strategy notice

Orders are simulated on standard candles. No lookahead.

Entries and exits

Long: flip up plus ATR buffer and all gates true

Short: flip down plus ATR buffer and gates true with bear bias when enabled

Exit: SAR stop per side, optional ATR take profit, optional cooldown after entry

Tie handling: stop first if both stop and target could fill in one bar

Yelober - Intraday ETF Dashboard# How to Read the Yelober Intraday ETF Dashboard

The Intraday ETF Dashboard provides a powerful at-a-glance view of sector performance and trading opportunities. Here's how to interpret and use the information:

## Basic Dashboard Reading

### Color-Coding System

- **Green values**: Positive performance or bullish signals

- **Red values**: Negative performance or bearish signals

- **Symbol colors**: Green = buy signal, Red = sell signal, Gray = neutral

### Example 1: Identifying Strong Sectors

If you see XLF (Financials) with:

- Day % showing +2.65% (green background)

- Symbol in green color

- RSI of 58 (not overbought)

**Interpretation**: Financial sector is showing strength and momentum without being overextended. Consider long positions in top financial stocks like JPM or BAC.

### Example 2: Spotting Weakness

If you see XLK (Technology) with:

- Day % showing -1.20% (red background)

- Week % showing -3.50% (red background)

- Symbol in red color

- RSI of 35 (approaching oversold)

**Interpretation**: Technology sector is showing weakness across multiple timeframes. Consider avoiding tech stocks or taking short positions in names like MSFT or AAPL, but be cautious as the low RSI suggests a bounce may be coming.

## Advanced Interpretations

### Example 3: Sector Rotation Detection

If you observe:

- XLE (Energy) showing +2.10% while XLK (Technology) showing -1.50%

- Both sectors' Week % values showing the opposite trend

**Interpretation**: This suggests money is rotating out of technology into energy stocks. This rotation pattern is actionable - consider reducing tech exposure and increasing energy positions (look at XOM, CVX in the Top Stocks column).

### Example 4: RSI Divergences

If you see XLU (Utilities) with:

- Day % showing +0.50% (small positive)

- RSI showing 72 (overbought, red background)

**Interpretation**: Despite positive performance, the high RSI suggests the sector is overextended. This divergence between price and indicator suggests caution - the rally in utilities may be running out of steam.

### Example 5: Relative Strength in Weak Markets

If SPY shows -1.20% but XLP (Consumer Staples) shows +0.30%:

**Interpretation**: Consumer staples are showing defensive strength during market weakness. This is typical risk-off behavior. Consider defensive positions in stocks like PG, KO, or PEP for protection.

## Practical Application Scenarios

### Day Trading Setup

1. **Morning Market Assessment**:

- Check which sectors are green pre-market

- Focus on sectors with Day % > 1% and RSI between 40-70

- Identify 2-3 stocks from the Top Stocks column of the strongest sector

2. **Midday Reversal Hunting**:

- Look for sectors with symbol color changing from red to green

- Confirm with RSI moving away from extremes

- Trade stocks from that sector showing similar pattern changes

### Swing Trading Application

1. **Trend Following**:

- Identify sectors with positive Day % and Week %

- Look for RSI values in uptrend but not overbought (45-65)

- Enter positions in top stocks from these sectors, using daily charts for confirmation

2. **Contrarian Setups**:

- Find sectors with deeply negative Day % but RSI < 30

- Look for divergence (price making new lows but RSI rising)

- Consider counter-trend positions in the stronger stocks within these oversold sectors

## Reading Special Conditions

### Example 6: Risk-Off Environment

If you observe:

- XLP (Consumer Staples) and XLU (Utilities) both green

- XLK (Technology) and XLY (Consumer Disc) both red

- SPY slightly negative

**Interpretation**: Classic risk-off rotation. Investors are moving to safety. Consider defensive positioning and reducing exposure to growth sectors.

### Example 7: Market Breadth Analysis

Count the number of sectors in green vs. red:

- If 7+ sectors are green: Strong bullish breadth, consider aggressive long positioning

- If 7+ sectors are red: Weak market breadth, consider defensive positioning or shorts

- If evenly split: Market is indecisive, focus on specific sector strength instead of broad market exposure

Remember that this dashboard is most effective when combined with broader market analysis and appropriate risk management strategies.

BTC ETF Flow Trading SignalsTracks large money flows (500M+) across major Bitcoin ETFs (IBIT, BTCO, FBTC, ARKB, BITB)

Generates long/short signals based on institutional money movement

Shows flow trends and strength of movements

This script provides a foundation for comparing ETF inflows and Bitcoin price. The effectiveness of the analysis depends on the quality of the data and your interpretation of the results. Key levels of 500M and 350M Inflow/Outflow Enjoy

Collaboration with Vivid Vibrations

Enjoy & improve!

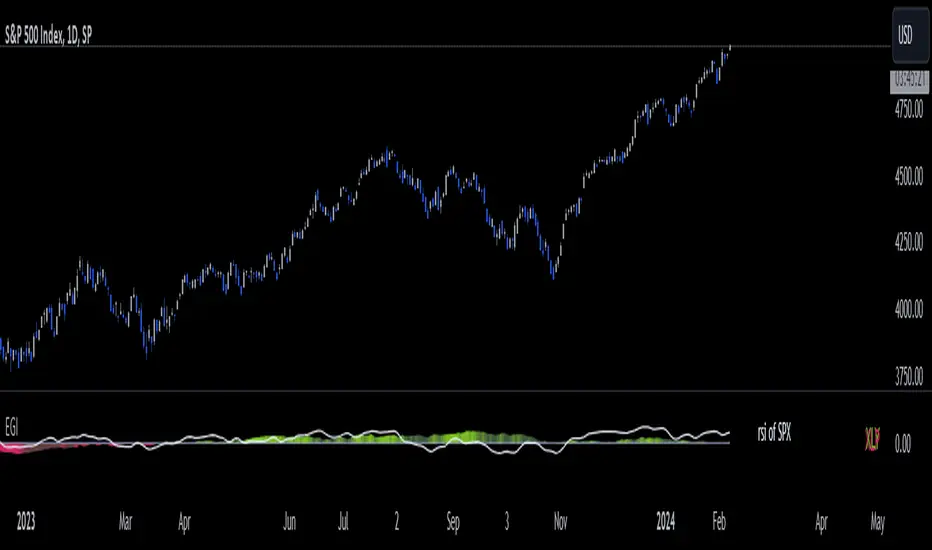

Economic Growth Index (XLY/XLP)Keeping an eye on the macroeconomic environment is an essential part of a successful investing and trading strategy. Piecing together and analysing its complex patterns are important to detect probable changing trends. This may seem complicated, or even better left to experts and gurus, but it’s made a whole lot easier by this indicator, the Economic Growth Index (EGI).

Common sense shows that in an expanding economy, consumers have access to cash and credit in the form of disposable income, and spend it on all sorts of goods, but mainly crap they don’t need (consumer discretionary items). Companies making these goods do well in this phase of the economy, and can charge well for their products.

Conversely, in a contracting economy, disposable income and credit dry up, so demand for consumer discretionary products slows, because people have no choice but to spend what they have on essential goods. Now, companies making staple goods do well, and keep their pricing power.

These dynamics are represented in EGI, which plots the Rate of Change of the Consumer Discretionary ETF (XLY) in relation to the Consumer Staples ETF (XLP). Put simply, green is an expanding phase of the economy, and red shrinking. The signal line is the market, a smoothed RSI of the S&P500. Run this on a Daily timeframe or higher. Check it occasionally to see where the smart money is heading.

Blackrock Spot ETF Premium BTCUSD (COINBASE) V1I created an indicator that takes the spot BTC/USD pair from major exchanges and compares it to the Spot BTC/USD pair on Coinbase that institutions will use for their Spot ETFs.

Blackrock Spot ETF Premium BTCUSD (COINBASE)

I suspect we will see a new "Kimchi Premium" where the Spot ETF pressures from institutions will raise the Coinbase Bitcoin price by a factor of 10-50% premium to the other exchanges.

Naturally excess coins from other exchanges will flow into Coinbase to capture this.

This indicator should be good for some time until one of the other exchanges delist or stop using BTCUSD "spot" If it breaks it I will update it if I remember.

FederalXBT,

Convert ETF to Futures/IndexThis indicator is used to automatically map an ETF's VWAP and 10 levels above and below the strike of your choice, to the futures or index instrument currently being viewed/traded. This works very well when using both SPY to ES/MES/SPX or QQQ to NQ/MNQ/NDX to plot the ETF strikes and can lead to some incredible trades, especially when trading level to level. Since SPY, QQQ, IWM, and DIA have the same price action as their futures iteration, there seems to be a direct correlation between their levels and VWAP . This indicator is made to easily map these key levels to the appropriate futures instrument. If you have a way to measure GEX centered around a certain level, I recommend color coding the lines to help indicate whether the level will have strong positive or negative gamma hedging associated with it.

NIFTY / BANKNIFTY ETF SIP NOTIFIERNIFTY / BANKNIFTY - ETF SIP NOTIFIER

STUDY concept -

- As a market investor, one cannot time the market.

- Specailly, working professionals and job holders don't have time for market tracking.

- The idea of the script is - When Nifty closes below 2% previous day high, market has corrected and it's available at a discount w.r.t. previous day

- One can then invest in NIFTY / BANKNIFTY via ETF option on same or next day.

- If you like this idea, Save this script and add alert condition of this script in NIFTY / BANKNIFTY chart.

- One can get notification on TradingView mobile app or via email when the criteria is met.

- Logic can be applied to investing in INDEXES , NIFTY, BANKNIFTY.

Logic may be improved later.

NOTE - Investing is a serious and risky business. Profit / Loss from this investing idea is sole responsibility of the investor. This script is for education and learning purpose.

Oil ETF VolumeDirexxion Daily has both 'bear' and 'bull' oil ETFs. This tracks the volume in both combined. It also tracks them individually: the bear ETF is the red line, and bull the green.

NOTE: the color of the volume bars is determined by whatever ticker you're currently looking at, and whether current close is gt/lt previous close. It is intended to be used while looking at the USOIL chart. The colors will be inverted if you're looking at the 'bear' ETF! as the higher closes will actually mean price is going down :D

Leveraged ETF Volume Ratio3x/2x Long/short etf pairs for popular tickers, including TSLA, QQQ, META, PLTR... Extreme values indicate bullish/bearish sentiment.

Standardized Leveraged ETF Fund of FlowsThis indicator tracks and standardizes the 3-month fund flows of major leveraged ETFs across different asset classes, including equities, gold, and bonds.

The fund flows are summed over a 3-month period (63 trading days) and then standardized using a 500-day rolling mean and standard deviation.

The resulting normalized fund flow values are plotted in three distinct colors:

Blue for Equities Fund Flows

Yellow for Gold Fund Flows

Green for Bond Fund Flows

CE - 42MACRO Fixed Income and Macro This is Part 2 of 2 from the 42MACRO Recreation Series

However, there will be a bonus Indicator coming soon!

The CE - 42MACRO Fixed Income and Macro Table is a next level Macroeconomic and market analysis indicator.

It aims to provide a probabilistic insight into the market realized GRID Macro regimes,

track a multiplex of important Assets, Indices, Bonds and ETF's to derive extra market insights by showing the most important aggregates and their performance over multiple timeframes... and what that might mean for the whole market direction.

For traders and especially investors, the unique functionalities will be of high value.

Quick guide on how to use it:

docs.google.com

WARNING

By the nature of the macro regimes, the outcomes are more accurate over longer Chart Timeframes (Week to Months).

However, it is also a valuable tool to form an advanced,

market realized, short to medium term bias.

NOTE

This Indicator is intended to be used alongside the 1nd part "CE - 42MACRO Equity Factor"

for a more wholistic approach and higher accuracy.

Methodology:

The Equity Factor Table tracks specifically chosen Assets to identify their performance and add the combined performances together to visualize 42MACRO's GRID Equity Model.

For this it uses the below Assets:

Convertibles ( AMEX:CWB )

Leveraged Loans ( AMEX:BKLN )

High Yield Credit ( AMEX:HYG )

Preferreds ( NASDAQ:PFF )

Emerging Market US$ Bonds ( NASDAQ:EMB )

Long Bond ( NASDAQ:TLT )

5-10yr Treasurys ( NASDAQ:IEF )

5-10yr TIPS ( AMEX:TIP )

0-5yr TIPS ( AMEX:STIP )

EM Local Currency Bonds ( AMEX:EMLC )

BDCs ( AMEX:BIZD )

Barclays Agg ( AMEX:AGG )

Investment Grade Credit ( AMEX:LQD )

MBS ( NASDAQ:MBB )

1-3yr Treasurys ( NASDAQ:SHY )

Bitcoin ( AMEX:BITO )

Industrial Metals ( AMEX:DBB )

Commodities ( AMEX:DBC )

Gold ( AMEX:GLD )

Equity Volatility ( AMEX:VIXM )

Interest Rate Volatility ( AMEX:PFIX )

Energy ( AMEX:USO )

Precious Metals ( AMEX:DBP )

Agriculture ( AMEX:DBA )

US Dollar ( AMEX:UUP )

Inverse US Dollar ( AMEX:UDN )

Functionalities:

Fixed Income and Macro Table

Shows relative market Asset performance

Comes with different Calculation options like RoC,

Sharpe ratio, Sortino ratio, Omega ratio and Normalization

Allows for advanced market (health) performance

Provides the calculated, realized GRID market regimes

Informs about "Risk ON" and "Risk OFF" market states

Visuals - for your best experience only use one (+ BarColoring) at a time:

You can visualize all important metrics:

- GRID regimes of the currently chosen calculation type

- Risk On/Risk Off with background colouring and additional +1/-1 values

- a smoother GRID model

- a smoother Risk On/ Risk Off metric

- Barcoloring for enabled metric of the above

If you have more suggestions, please write me

Fixed Income and Macro:

The visualisation of the relative performance of the different assets provides valuable information about the current market environment and the actual market performance.

It furthermore makes it possible to obtain a deeper understanding of how the interconnected market works and makes it simple to identify the actual market direction,

thus also providing all the information to derive overall market health, market strength or weakness.

Utility:

The Fixed Income and Macro Table is divided in 4 Columns which are the GRID regimes:

Economic Growth:

Goldilocks

Reflation

Economic Contraction:

Inflation

Deflation

Top 5 Fixed Income/ Macro Factors:

Are the values green for a specific Column?

If so then the market reflects the corresponding GRID behavior.

Bottom 5 Fixed Income/ Macro Factors:

Are the values red for a specific Column?

If so then the market reflects the corresponding GRID behavior.

So if we have Goldilocks as current regime we would see green values in the Top 5 Goldilocks Cells and red values in the Bottom 5 Goldilocks Cells.

You will find that Reflation will look similar, as it is also a sign of Economic Growth.

Same is the case for the two Contraction regimes.

******

This Indicator again is based to a majority on 42MACRO's models.

I only brought them into TV and added things on top of it.

If you have questions or need a more in-depth guide DM me.

GM

RSI - S&P Sector ETFsThe script displays RSI of each S&P SPDR Sector ETF

XLB - Materials

XLC - Communications

XLE - Energy

XLF - Financials

XLI - Industrials

XLK - Technology

XLP - Consumer Staples

XLRE - Real Estate

XLU - Utilities

XLV - Healthcare

XLY - Consumer Discretionary

It is meant to identify changes in sector rotation, compare oversold/overbought signals of each sector, and/or any price momentum trading strategy applicable to a trader.

InfoPanel - SeasonalityThis panel will show which is the best month to buy a stock, index or ETF or even a cryptocurrency in the past 5 years.

Script to use only with MONTHLY timeframe.

Thanks to: RicardoSantos for his hard work.

Please use comment section for any feedback.