TCP | Market Session | Session Analyzer📌 TCP | Market Session Indicator | Crypto Version

A powerful, real-time market session visualization tool tailored for crypto traders. Track the heartbeat of Asia, Europe, and US trading hours directly on your chart with live session boxes, behavioral analysis, liquidity grab detection, and countdown timers. Know when the action starts, how the market behaves, and where the traps lie.

🔰 Introduction:

Trade the Right Hours with the Right Tools

Time matters in trading. Most significant moves happen during key sessions—and knowing when and how each session unfolds can give you a sharp edge. The TCP Market Session Indicator, developed by Trade City Pro (TCP), puts professional session tracking and behavioral insights at your fingertips.

Whether you're a scalper or swing trader, this indicator gives you the timing context to enter and exit trades with greater confidence and clarity.

🕒 Core Features

• Live Session Boxes :

Highlight active ranges during Asia, Europe, and US sessions with dynamic high/low updates.

• Session Start/End Labels :

Know exactly when each session begins and ends plotted clearly on your chart with context.

• Session Behavior Analysis :

At the end of each session, the indicator classifies the price action as:

- Trend Up

- Trend Down

- Consolidation

- Manipulation

• Liquidity Grab Detection: Automatically detects possible stop hunts (fake breakouts) and marks them on the chart with precision filters (volume, ATR, reversal).

• Session Countdown Table: A live dashboard showing:

- Current active session

- Time left in session

- Upcoming session and how many minutes until it starts

- Utility time converter (e.g. 90 min = 01:30)

• Vertical Session Lines: Visualize past and upcoming session boundaries with customizable history and future range.

• Multi-Day Support: Draw session ranges for previous, current, and future days for better backtesting and forecasting.

⚙️ Settings Panel

Customize everything to fit your trading style and schedule:

• Session Time Settings:

Set the opening and closing time for each session manually using UTC-based minute inputs.

→ For example, enter Asia Start: 0, Asia End: 480 for 00:00–08:00 UTC.

This gives full flexibility to adjust session hours to match your preferred market behavior.

• Enable or Disable Elements:

Toggle the visibility of each session (Asia, Europe, US), as well as:

- Session Boxes

- Countdown Table

- Session Lines

- Liquidity Grab Labels

• Timezone Selection:

Choose between using UTC or your chart’s local timezone for session calculations.

• Customization Options:

Select number of past and future days to draw session data

Adjust vertical line transparency

Fine-tune label offset and spacing for clean layout

📊 Smart Session Boxes

Each session box tracks high, low, open, and close in real time, providing visual clarity on market structure. Once a session ends, the box closes, and the behavior type is saved and labeled ideal for spotting patterns across sessions.

• Asia: Green Box

• Europe: Orange Box

• US: Blue Box

💡 Why Use This Tool?

• Perfect Timing: Don’t get chopped in low-liquidity hours. Focus on sessions where volume and volatility align.

• Pattern Recognition: Study how price behaves session-to-session to build better strategies.

• Trap Detection: Spot manipulation moves (liquidity grabs) early and avoid common retail pitfalls.

• Macro Session Mapping: Use as a foundational layer to align trades with market structure and news cycles.

🔍 Example Use Case

You're watching BTC at 12:45 UTC. The indicator tells you:

The Asia session just ended (label shows “Asia Session End: Trend Up”)

Europe session starts in 15 minutes

A liquidity grab just triggered at the previous high—label confirmed

Now you know who’s active, what the market just did, and what’s about to start—all in one glance.

✅ Why Traders Trust It

• Visual & Intuitive: Fully chart-based, no clutter, no guessing

• Crypto-Focused: Designed specifically for 24/7 crypto markets (not outdated forex models)

• Non-Repainting: All labels and boxes stay as printed—no tricks

• Reliable: Tested across multiple exchanges, pairs, and timeframes

🧩 Built by Trade City Pro (TCP)

The TCP Market Session Indicator is part of a suite of professional tools used by over 150,000 traders. It’s coded in Pine Script v6 for full compatibility with TradingView’s latest capabilities.

🔗 Resources

• Tutorial: Learn how to analyze sessions like a pro in our TradingView guide:

"TradeCityPro Academy: Session Mapping & Liquidity Traps"

• More Tools: Explore our full library of indicators on

"liquidity"に関するスクリプトを検索

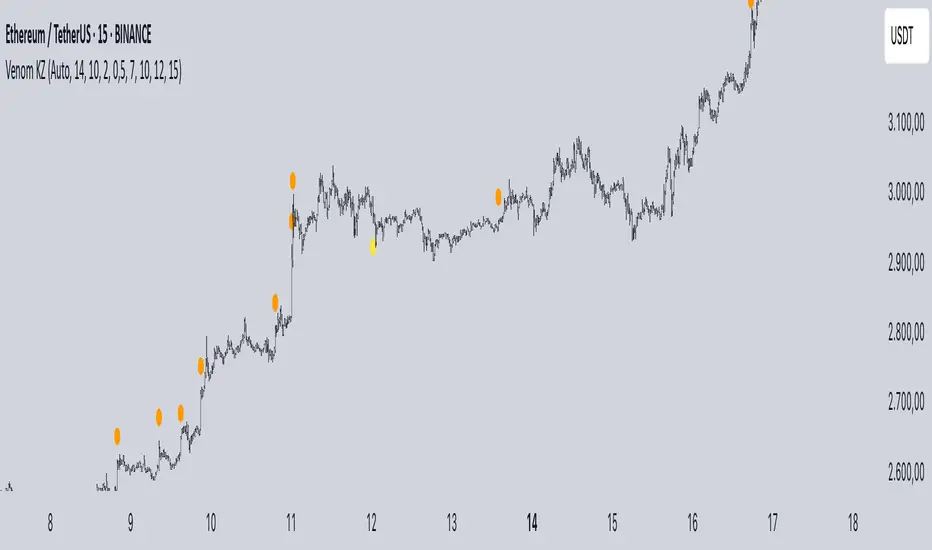

Mig Trade Model - Kill Zones

Key features:

Liquidity Hunt Detection: Spots aggressive moves that "hunt" stops beyond recent swing highs/lows.

Consolidation Filter: Requires 1-3 small-range candles after a hunt before confirming with a strong candle.

Bias Application: Uses daily open/close to auto-detect bias or allows manual override.

Kill Zone Restriction: Limits signals to London (default: 7-10 AM UTC) and NY (default: 12-3 PM UTC) sessions for better relevance in active markets.

This strategy is inspired by smart money concepts (SMC) and ICT (Inner Circle Trader) methodologies, aiming to capture venom-like "stings" in price action where liquidity is grabbed before reversals.

How It Works

ATR Calculation: Uses a user-defined ATR length (default: 14) to measure volatility, which scales candle body and range thresholds.

Bias Determination:

Auto: Compares daily close to open (bullish if close > open).

Manual: User selects "Bullish" or "Bearish."

Strong Candles:

Bullish: Green candle with body > 2x ATR (configurable).

Bearish: Red candle with body > 2x ATR.

Small Range Candles:

Candles where high-low < 0.5x ATR (configurable).

Liquidity Hunt:

Bullish Hunt: Strong bearish candle making a new low below the past swing low (default: 10 bars).

Bearish Hunt: Strong bullish candle making a new high above the past swing high.

Signal Generation:

After a hunt, counts 1-3 small-range candles.

Confirms with a strong candle in the opposite direction (e.g., strong bullish after bearish hunt).

Resets if >3 small candles or an opposing strong candle appears.

Kill Zone Filter:

Checks if the current bar's time (in UTC) falls within London or NY Kill Zones.

Only allows final "Buy" (bullish entry) or "Sell" (bearish entry) if bias matches and in Kill Zone.

Plots:

Yellow circle (below): Bullish liquidity hunt.

Orange circle (above): Bearish liquidity hunt.

Blue diamond (below): Raw bullish signal.

Purple diamond (above): Raw bearish signal.

Green triangle up ("Buy"): Filtered bullish entry.

Red triangle down ("Sell"): Filtered bearish entry.

Inputs

Bias: "Auto" (default), "Bullish", or "Bearish" – Controls signal direction based on daily trend.

ATR Length: 14 (default) – Period for ATR calculation.

Swing Length for Liquidity Hunt: 10 (default) – Bars to look back for swing highs/lows.

Strong Candle Body Multiplier (x ATR): 2.0 (default) – Threshold for strong candle bodies.

Small Range Multiplier (x ATR): 0.5 (default) – Threshold for small-range candles.

London Kill Zone Start/End Hour (UTC): 7/10 (default) – Customize London session hours.

NY Kill Zone Start/End Hour (UTC): 12/15 (default) – Customize New York session hours.

Usage Tips

Timeframe: Best on lower timeframes (e.g., 5-15 min) for intraday trading, especially forex pairs like EURUSD or GBPUSD.

Timezone Adjustment: Inputs are in UTC. If your chart is in a different timezone (e.g., EST = UTC-5), adjust hours accordingly (e.g., London: 2-5 AM EST → 7-10 UTC).

Risk Management: Use with stop-loss (e.g., beyond the hunt low/high) and take-profit based on ATR multiples. Not financial advice—backtest thoroughly.

Customization: Tweak multipliers for different assets; higher for volatile cryptos, lower for stocks.

Limitations: Relies on historical data; may generate false signals in ranging markets. Combine with other indicators like volume or support/resistance.

This indicator is for educational purposes. Always use discretion and proper risk management in live trading. If you find it useful, feel free to share feedback or suggestions!

FEDFUNDS Rate Divergence Oscillator [BackQuant]FEDFUNDS Rate Divergence Oscillator

1. Concept and Rationale

The United States Federal Funds Rate is the anchor around which global dollar liquidity and risk-free yield expectations revolve. When the Fed hikes, borrowing costs rise, liquidity tightens and most risk assets encounter head-winds. When it cuts, liquidity expands, speculative appetite often recovers. Bitcoin, a 24-hour permissionless asset sometimes described as “digital gold with venture-capital-like convexity,” is particularly sensitive to macro-liquidity swings.

The FED Divergence Oscillator quantifies the behavioural gap between short-term monetary policy (proxied by the effective Fed Funds Rate) and Bitcoin’s own percentage price change. By converting each series into identical rate-of-change units, subtracting them, then optionally smoothing the result, the script produces a single bounded-yet-dynamic line that tells you, at a glance, whether Bitcoin is outperforming or underperforming the policy backdrop—and by how much.

2. Data Pipeline

• Fed Funds Rate – Pulled directly from the FRED database via the ticker “FRED:FEDFUNDS,” sampled at daily frequency to synchronise with crypto closes.

• Bitcoin Price – By default the script forces a daily timeframe so that both series share time alignment, although you can disable that and plot the oscillator on intraday charts if you prefer.

• User Source Flexibility – The BTC series is not hard-wired; you can select any exchange-specific symbol or even swap BTC for another crypto or risk asset whose interaction with the Fed rate you wish to study.

3. Math under the Hood

(1) Rate of Change (ROC) – Both the Fed rate and BTC close are converted to percent return over a user-chosen lookback (default 30 bars). This means a cut from 5.25 percent to 5.00 percent feeds in as –4.76 percent, while a climb from 25 000 to 30 000 USD in BTC over the same window converts to +20 percent.

(2) Divergence Construction – The script subtracts the Fed ROC from the BTC ROC. Positive values show BTC appreciating faster than policy is tightening (or falling slower than the rate is cutting); negative values show the opposite.

(3) Optional Smoothing – Macro series are noisy. Toggle “Apply Smoothing” to calm the line with your preferred moving-average flavour: SMA, EMA, DEMA, TEMA, RMA, WMA or Hull. The default EMA-25 removes day-to-day whips while keeping turning points alive.

(4) Dynamic Colour Mapping – Rather than using a single hue, the oscillator line employs a gradient where deep greens represent strong bullish divergence and dark reds flag sharp bearish divergence. This heat-map approach lets you gauge intensity without squinting at numbers.

(5) Threshold Grid – Five horizontal guides create a structured regime map:

• Lower Extreme (–50 pct) and Upper Extreme (+50 pct) identify panic capitulations and euphoria blow-offs.

• Oversold (–20 pct) and Overbought (+20 pct) act as early warning alarms.

• Zero Line demarcates neutral alignment.

4. Chart Furniture and User Interface

• Oscillator fill with a secondary DEMA-30 “shader” offers depth perception: fat ribbons often precede high-volatility macro shifts.

• Optional bar-colouring paints candles green when the oscillator is above zero and red below, handy for visual correlation.

• Background tints when the line breaches extreme zones, making macro inflection weeks pop out in the replay bar.

• Everything—line width, thresholds, colours—can be customised so the indicator blends into any template.

5. Interpretation Guide

Macro Liquidity Pulse

• When the oscillator spends weeks above +20 while the Fed is still raising rates, Bitcoin is signalling liquidity tolerance or an anticipatory pivot view. That condition often marks the embryonic phase of major bull cycles (e.g., March 2020 rebound).

• Sustained prints below –20 while the Fed is already dovish indicate risk aversion or idiosyncratic crypto stress—think exchange scandals or broad flight to safety.

Regime Transition Signals

• Bullish cross through zero after a long sub-zero stint shows Bitcoin regaining upward escape velocity versus policy.

• Bearish cross under zero during a hiking cycle tells you monetary tightening has finally started to bite.

Momentum Exhaustion and Mean-Reversion

• Touches of +50 (or –50) come rarely; they are statistically stretched events. Fade strategies either taking profits or hedging have historically enjoyed positive expectancy.

• Inside-bar candlestick patterns or lower-timeframe bearish engulfings simultaneously with an extreme overbought print make high-probability short scalp setups, especially near weekly resistance. The same logic mirrors for oversold.

Pair Trading / Relative Value

• Combine the oscillator with spreads like BTC versus Nasdaq 100. When both the FED Divergence oscillator and the BTC–NDQ relative-strength line roll south together, the cross-asset confirmation amplifies conviction in a mean-reversion short.

• Swap BTC for miners, altcoins or high-beta equities to test who is the divergence leader.

Event-Driven Tactics

• FOMC days: plot the oscillator on an hourly chart (disable ‘Force Daily TF’). Watch for micro-structural spikes that resolve in the first hour after the statement; rapid flips across zero can front-run post-FOMC swings.

• CPI and NFP prints: extremes reached into the release often mean positioning is one-sided. A reversion toward neutral in the first 24 hours is common.

6. Alerts Suite

Pre-bundled conditions let you automate workflows:

• Bullish / Bearish zero crosses – queue spot or futures entries.

• Standard OB / OS – notify for first contact with actionable zones.

• Extreme OB / OS – prime time to review hedges, take profits or build contrarian swing positions.

7. Parameter Playground

• Shorten ROC Lookback to 14 for tactical traders; lengthen to 90 for macro investors.

• Raise extreme thresholds (for example ±80) when plotting on altcoins that exhibit higher volatility than BTC.

• Try HMA smoothing for responsive yet smooth curves on intraday charts.

• Colour-blind users can easily swap bull and bear palette selections for preferred contrasts.

8. Limitations and Best Practices

• The Fed Funds series is step-wise; it only changes on meeting days. Rapid BTC oscillations in between may dominate the calculation. Keep that perspective when interpreting very high-frequency signals.

• Divergence does not equal causation. Crypto-native catalysts (ETF approvals, hack headlines) can overwhelm macro links temporarily.

• Use in conjunction with classical confirmation tools—order-flow footprints, market-profile ledges, or simple price action to avoid “pure-indicator” traps.

9. Final Thoughts

The FEDFUNDS Rate Divergence Oscillator distills an entire macro narrative monetary policy versus risk sentiment into a single colourful heartbeat. It will not magically predict every pivot, yet it excels at framing market context, spotting stretches and timing regime changes. Treat it as a strategic compass rather than a tactical sniper scope, combine it with sound risk management and multi-factor confirmation, and you will possess a robust edge anchored in the world’s most influential interest-rate benchmark.

Trade consciously, stay adaptive, and let the policy-price tension guide your roadmap.

Midnight 30min High/LowMidnight 30min High/Low — Overnight Liquidity Range Tracker

Capture the Overnight Session: A Strategic Level Identification Tool from Professional Trading Methodology

This indicator captures the high and low prices during the critical 30-minute midnight session (12:00-12:30 AM EST) and projects these levels forward as key support and resistance zones. These overnight ranges often contain significant liquidity and serve as crucial reference points for intraday price action, representing areas where institutional activity may have established important levels.

🔍 What This Script Does:

Identifies Critical Overnight Session Levels

- Automatically detects the 12:00-12:30 AM EST session window

- Captures the highest and lowest prices during this 30-minute period

- Projects these levels forward for multiple trading days

Creates Dynamic Support/Resistance Zones

- Extends midnight high/low levels as horizontal lines with customizable projection periods

- Fills the area between high and low to create a visual trading range

- Updates automatically each trading day with new overnight levels

Provides Clear Visual Reference Points

- Optional session start markers (●) highlight when the midnight session begins

- Color-coded lines distinguish between high and low levels

- Transparent fill area creates an easy-to-identify trading zone

Real-Time Level Tracking

- Updates levels in real-time during the active midnight session

- Maintains historical levels for reference and backtesting

- Compatible with data window for precise level values

⚙️ Customization Options:

Extend Days (1-30):** Control how many days forward the levels are projected (default: 5 days)

High Line Color:** Customize the midnight high line color (default: blue)

Low Line Color:** Customize the midnight low line color (default: orange)

Fill Color:** Adjust the transparency and color of the range area (default: light aqua, 80% transparency)

Show Session Markers:** Toggle yellow session start indicators on/off (default: enabled)

💡 How to Use:

Deploy on lower timeframes (1m-15m) for precise level identification and reaction monitoring**

Watch for key price interactions:

- Rejection at midnight high levels (potential resistance)

- Bounce from midnight low levels (potential support)

- Range-bound trading between the high and low levels

Combine with liquidity concepts:

- Monitor for stop hunts above/below these levels

- Look for false breakouts that snap back into the range

- Use as confluence with other ICT concepts like FVGs and Order Blocks

Strategic Applications:

- Range trading between midnight levels

- Breakout confirmation when price closes decisively outside the range

- Support/resistance validation for entry and exit planning

🔗 Combine With These Tools for Complete Market Structure Analysis:

✅ First FVG — Opening Range Fair Value Gap Detector.

✅ ICT Turtle Soup (Liquidity Reversal)— Spot stop hunts and false breakout scenarios

✅ ICT Macro Zones (Grey Box Version)- It tracks real-time highs and lows for each Silver Bullet session

✅ ICT SMC Liquidity Grabs and OBs- Liquidity Grabs, Order Block Zones, and Fibonacci OTE Levels, allowing traders to identify institutional entry models with clean, rule-based visual signals.

Together, these tools create a comprehensive Smart Money Concepts (SMC) framework — helping traders identify, anticipate, and capitalize on institutional-level price movements with precision and confidence during critical overnight sessions.

PRO SMC DASHBOARDPRO SMC DASHBOARD - PRO LEVEL

Advanced Supply & Demand / SMC dashboard for scalping and intraday:

Multi-Timeframe Trend: Visualizes trend direction for M1, M5, M15, H1, H4.

HTF Supply/Demand: Shows closest high time frame (HTF) supply/demand zone and distance (in pips).

Smart “Flip” & Liquidity Signals: Flip and Liquidity Sweep arrows/signals are shown only when truly significant:

Near HTF Supply/Demand zone

And confirmed by volume spike or high confluence score

Momentum & Bias: Real-time momentum (RSI M1), H1 bias and fakeout detection.

Confluence Score: Objective score (out of 7) for trade confidence.

Volume Spike, Divergence, BOS: Includes volume spikes, RSI divergence (M1), and Break of Structure (BOS) for both M15 & H1.

Ultra-clean chart: Only valid signals/alerts shown; no spam or visual clutter.

Full dashboard with all signals and context, always visible bottom-right.

Best used for:

Forex, Gold/Silver, US indices, and crypto

Scalping/intraday with fast, clear decisions based on multi-factor SMC logic

Usage:

Add to your chart, monitor the dashboard for valid setups, and trade only when multiple factors align for high-probability entries.

How to Use the PRO SMC DASHBOARD

1. Add the Script to Your Chart:

Apply the indicator to your favorite Forex, Gold, crypto, or indices chart (best on M1, M5, or M15 for entries).

2. Read the Dashboard (Bottom Right):

The dashboard shows real-time information from multiple timeframes and key SMC filters, including:

Trend (M1, M5, M15, H1, H4):

Arrows show up (↑) or down (↓) trend for each timeframe, based on EMA.

Momentum (RSI M1):

Shows “Strong Up,” “Strong Down,” or “Neutral” plus the current RSI value.

RSI (H1):

Higher timeframe momentum confirmation.

ATR State:

Indicates current volatility (High, Normal, Low).

Session:

Detects if the market is in London, NY, or Asia session (based on UTC).

HTF S/D Zone:

Shows the nearest high timeframe Supply or Demand zone, its timeframe (M15, H1, H4), and exact pip distance.

Fakeout (last 3):

Detects recent false breakouts—if there are multiple fakeouts, potential for reversal is higher.

FVG (Fair Value Gap):

Indicates direction and distance to the nearest FVG (Above/Below).

Bias:

“Strong Buy,” “Strong Sell,” or “Neutral”—multi-timeframe, momentum, and volatility filtered.

Inducement:

Alerts for possible “stop hunt” or liquidity grab before reversal.

BOS (Break of Structure):

Recent or live breaks of market structure (for both M15 & H1).

Liquidity Sweep:

Shows if price just swept a key high/low and then reversed (often key reversal point).

Confluence Score (0-7):

Higher score means more factors align—look for 5+ for strong setups.

Volume Spike:

“YES” appears if the current volume is significantly above average—big players are active!

RSI Divergence:

Bullish or bearish divergence on M1—signals early reversal risk.

Momentum Flip:

“UP” or “DN” appears if RSI M1 crosses the 50 line, confirmed by location and other filters.

Chart Signals (Arrows & Markers):

Flip arrows (up/down) and Liquidity markers only appear when price is at/near a key Supply/Demand zone and confirmed by either a volume spike or strong confluence.

No signal spam:

If you see an arrow or LIQ tag, it’s a truly significant moment!

Suggested Trading Workflow:

Scan the Dashboard:

Is the multi-timeframe trend aligned?

Are you near a major Supply or Demand zone?

Is the Confluence Score high (5 or more)?

Check for Signals:

Is there a Flip or LIQ marker near a Supply/Demand zone?

Is volume spiking or a fakeout just occurred?

Look for Reversal or Continuation:

If there’s a Flip at Demand (with high confluence), consider a long setup.

If there’s a LIQ sweep + flip + volume at Supply, consider a short.

Manage Risk:

Don’t chase every signal.

Confirm with your entry criteria and preferred session timing.

Pro Tips:

Highest confidence trades:

When dashboard signals and chart arrows/markers agree, especially with high confluence and volume spike.

Adapt pip distance filter:

Dashboard is tuned for FX and gold; for other assets, adjust pip-size filter if needed.

Use alerts (if enabled):

Set up custom TradingView alerts for “Flip” or “Liquidity” signals for auto-notifications.

Designed to help you make professional, objective decisions—without chart clutter or second-guessing!

CandelaCharts - HTF Sweeps📝 Overview

This indicator lets you overlay a higher timeframe (HTF) onto your current chart, giving you a clearer view of broader market movements without switching timeframes.

This indicator also detects liquidity sweeps and plots them on both the higher timeframe (HTF) and the current lower timeframe (LTF), helping traders clearly spot potential reversal points. It adds LTF dividers for better structure clarity, making it easier to align with HTF shifts and refine entry timing with greater precision.

📦 Features

This indicator identifies price sweeps and their invalidations, helping traders spot potential liquidity grabs and failed breakout attempts.

Overlay a configurable higher timeframe (HTF) on the current chart

Detects and plots liquidity sweeps on both HTF and LTF

Adds lower timeframe (LTF) dividers for improved structure clarity

Ideal for ICT-style top-down analysis and precision entries without switching charts

⚙️ Settings

Customize the indicator to suit your strategy. Alert options are also available, so you can stay informed when key market events are triggered.

Timeframes: Select the higher timeframe (HTF) to overlay on your current chart.

HTF Coloring: Customize the color scheme for HTF candles.

HTF Offset: Space of HTF Candles and current chart.

HTF Size: Adjust the size of HTF candles.

HTF Labels: Toggle labels for HTF.

LTF H/L Line: Show or hide high/low lines from the lower timeframe.

LTF O/C Line: Display open/close lines from the lower timeframe.

Sweep: Enable detection and plotting of liquidity sweeps.

I-sweep: Toggle invalidated sweep detection.

Alerts: Enable Sweep Formation or Invalidation alerts

⚡️ Showcase

See the indicator applied in live market scenarios, illustrating how sweep detections and invalidations unfold on various charts.

HTF Candles

HTF Sweeps

LTF Sweeps

Invalidated Sweeps

🚨 Alerts

This indicator includes built-in alert functionality to keep you informed of key market events in real time. It supports the following customizable alerts on TradingView:

Sweep Detection: Notifies you when a price sweep is detected—either a liquidity sweep above recent highs or below recent lows. This can be a strong signal of potential reversals or liquidity grabs by larger market participants.

Sweep Invalidation: Alerts you when a previously detected sweep becomes invalidated due to price action moving beyond a defined threshold. This helps traders stay adaptive and avoid acting on outdated signals.

These alerts are fully integrated with TradingView’s native alert system, so you can receive notifications via app, email, or pop-up—ensuring you're always up to date, even when you're away from the chart.

⚠️ Disclaimer

Trading involves significant risk, and many participants may incur losses. The content on this site is not intended as financial advice and should not be interpreted as such. Decisions to buy, sell, hold, or trade securities, commodities, or other financial instruments carry inherent risks and are best made with guidance from qualified financial professionals. Past performance is not indicative of future results.

Sniper SweepsPurpose

Detect when price sweeps above recent highs (buy-side liquidity) or below recent lows (sell-side liquidity), but closes back inside the range. This is often interpreted as a stop-hunt or liquidity grab by institutional traders.

Core Concepts

Liquidity Sweep: When price briefly breaks a recent swing high/low (potentially triggering stop losses), but then closes back within the previous range.

Buy-side Sweep: Price breaks a previous high, but closes below it.

Sell-side Sweep: Price breaks a previous low, but closes above it.

Summary

This indicator is useful for:

Identifying potential stop-hunts or liquidity grabs.

Recognizing SMC trade setups around swept highs/lows.

Getting alerted when significant liquidity levels are manipulated.

PRO SMC Full Suite BY Mashrur“PRO SMC Full Suite BY Mashrur”

A Pine Script (v5) indicator for TradingView, focused on Smart Money Concepts (SMC). It overlays on price charts and provides visual tools for identifying key institutional trading behaviors.

🎯 Purpose

This script is designed to help traders analyze and trade using SMC principles by automatically detecting:

Order Blocks (OBs)

Fair Value Gaps (FVGs)

Breaks of Structure (BoS)

Liquidity Sweeps (Buy/Sell Side Liquidity Grabs)

Mitigation Entries

⚙️ Inputs / Settings

Show Fair Value Gaps: Toggle FVGs on/off

Higher Timeframe (HTF): Choose HTF for OB analysis

Use HTF OBs: Switch between current TF OBs and HTF OBs

Show Order Blocks: Toggle OBs on/off

Show OB Mitigation Entries: Toggle mitigation entry signals on/off

🧠 Core Logic Overview

🔹 1. Swing Points Detection

Identifies swing highs/lows using a 3-bar pattern (pivot-based structure).

🔹 2. Break of Structure (BoS)

A bullish BoS happens when price closes above the last swing high.

A bearish BoS occurs when price closes below the last swing low.

🔹 3. Order Block Detection

Upon BoS, the script marks the previous candle as the Order Block.

Uses either:

Current TF OBs (based on price action)

HTF OBs (based on candle body direction)

🔹 4. Mitigation Entry Logic

A mitigation occurs when price returns to the OB and reacts with confirmation:

Bullish: price dips into OB and closes above

Bearish: price wicks into OB and closes below

Plots entry markers for these mitigations.

🔹 5. Liquidity Sweeps

Detects equal highs/lows (liquidity zones)

Marks Buy SL when price dips below an equal low then closes above

Marks Sell SL when price breaks above an equal high then closes below

🔹 6. Fair Value Gaps (FVGs)

FVG Up: Gap between candle 3 and candle 1 (low > high )

FVG Down: Gap between candle 3 and candle 1 (high < low )

Plots highlighted boxes on these gaps

📊 Visual Elements

Boxes: For OB zones and FVGs

Shapes:

Labels: OB Buy/Sell entries

Triangles: Buy SL / Sell SL liquidity sweeps

Lines: Equal Highs and Lows

🔔 Alerts

Built-in alerts to notify when:

OB entries are confirmed

Liquidity sweeps happen

Helps in automation or active monitoring

✅ Ideal For

Traders using SMC, ICT concepts, Wyckoff, or institutional trading models

Anyone wanting to automate detection of structural elements on their chart

Akkerman IMB + Targets IndicatorAkkerman IMB + Targets Indicator

The Akkerman IMB + Targets Indicator is a powerful tool for traders who use the Smart Money Concept (SMC) methodology for intraday trading. This indicator combines several key elements of technical analysis, such as IMB (Imbalance) zones, liquidity zones, and intraday targets, to help traders identify significant levels on the chart for potential entry and exit points.

Main Features of the Indicator:

IMB (Imbalance) Zones:

The indicator detects IMB zones (imbalances) on the chart, which are often significant for the market because these zones can signal unsupported price moves where the market may either retrace or continue the move.

Green box — indicates a bullish IMB, where the price moves downward but does not reach the previous "low" level.

Red box — indicates a bearish IMB, where the price moves upward but does not reach the previous "high" level.

Liquidity Zones:

The indicator automatically identifies liquidity zones, which are critical levels for potential retracements or breakouts. These zones are determined by equal highs and lows on the chart (where the price has made similar highs or lows).

Triangles or lines highlight levels where significant buy or sell orders might be gathered.

Intraday Target Lines:

The indicator generates targets for intraday trading based on support and resistance levels over the last 10 periods.

These target lines on the chart indicate potential entry or exit points based on the lowest and highest prices over the past 10 bars, which represent key points for trading within the current session.

Indicator Settings:

Show IMB: Toggle to show or hide IMB zones on the chart.

Show Liquidity Zones: Toggle to show or hide liquidity zones on the chart.

Show Targets (Intraday): Toggle to show or hide intraday target lines.

Max Targets (maxTargets): Set the maximum number of targets to display on the chart.

How to Use:

IMB Zones help identify potential retracement or breakout zones on the market. These zones are a critical part of Smart Money analysis, as markets often retrace to these areas after significant price moves.

Liquidity Zones provide clues about where large orders may be gathered, which could lead to a retracement or breakout.

Intraday Targets assist in identifying important levels for entering or exiting trades within the current session to take advantage of short-term price movements.

Important Notes:

This indicator works best on the 1-hour timeframe (H1) for more accurate and stable signals.

For maximum effectiveness, it is recommended to combine this indicator with other technical indicators and analysis methods.

Institutional Quantum Momentum Impulse [BullByte]## Overview

The Institutional Quantum Momentum Impulse (IQMI) is a sophisticated momentum oscillator designed to detect institutional-level trend strength, volatility conditions, and market regime shifts. It combines multiple advanced technical concepts, including:

- Quantum Momentum Engine (Hilbert Transform + MACD Divergence + Stochastic Energy)

- Fractal Volatility Scoring (GARCH + Keltner-based volatility)

- Dynamic Adaptive Bands (Self-adjusting thresholds based on efficiency)

- Market Phase Detection (Volume + Momentum alignment)

- Liquidity & Cumulative Delta Analysis

The indicator provides a Z-score normalized momentum reading, making it ideal for mean-reversion and trend-following strategies.

---

## Key Features

### 1. Quantum Momentum Core

- Combines Hilbert Transform, MACD divergence, and Stochastic Energy into a single composite momentum score.

- Normalized using a Z-score for statistical significance.

- Smoothed with EMA/WMA/HMA for cleaner signals.

### 2. Dynamic Adaptive Bands

- Upper/Lower bands adjust based on volatility and efficiency ratio .

- Acts as overbought/oversold zones when momentum reaches extremes.

### 3. Market Phase Detection

- Identifies bullish , bearish , or neutral phases using:

- Volume-Weighted MA alignment

- Fractal momentum extremes

### 4. Volatility & Liquidity Filters

- Fractal Volatility Score (0-100 scale) shows market instability.

- Liquidity Check ensures trades are taken in favorable spread conditions.

### 5. Dashboard & Visuals

- Real-time dashboard with key metrics:

- Momentum strength, volatility, efficiency, cumulative delta, and market regime.

- Gradient coloring for intuitive momentum visualization .

---

## Best Trade Setups

### 1. Trend-Following Entries

- Signal :

- QM crosses above zero + Market Phase = Bullish + ADX > 25

- Cumulative Delta rising (buying pressure)

- Confirmation :

- Efficiency > 0.5 (strong momentum quality)

- Liquidity = High (tight spreads)

### 2. Mean-Reversion Entries

- Signal :

- QM touches upper band + Volatility expanding

- Market Regime = Ranging (ADX < 25)

- Confirmation :

- Efficiency < 0.3 (weak momentum follow-through)

- Cumulative Delta divergence (price high but delta declining)

### 3. Breakout Confirmation

- Signal :

- QM holds above zero after a pullback

- Market Phase shifts to Bullish/Bearish

- Confirmation :

- Volatility rising (expansion phase)

- Liquidity remains high

---

## Recommended Timeframes

- Intraday (5M - 1H): Works well for scalping & swing trades.

- Swing Trading (4H - Daily): Best for trend-following setups.

- Position Trading (Weekly+): Useful for macro trend confirmation.

---

## Input Customization

- Resonance Factor (1.0 - 3.618 ): Adjusts MACD divergence sensitivity.

- Entropy Filter (0.382/0.50/0.618) : Controls stochastic damping.

- Smoothing Type (EMA/WMA/HMA) : Changes momentum responsiveness.

- Normalization Period : Adjusts Z-score lookback.

---

The IQMI is a professional-grade momentum indicator that combines institutional-level concepts into a single, easy-to-read oscillator. It works across all markets (stocks, forex, crypto) and is ideal for traders who want:

✅ Early trend detection

✅ Volatility-adjusted signals

✅ Institutional liquidity insights

✅ Clear dashboard for quick analysis

Try it on TradingView and enhance your trading edge! 🚀

Happy Trading!

- BullByte

Pivot S/R with Volatility Filter## *📌 Indicator Purpose*

This indicator identifies *key support/resistance levels* using pivot points while also:

✅ Detecting *high-volume liquidity traps* (stop hunts)

✅ Filtering insignificant pivots via *ATR (Average True Range) volatility*

✅ Tracking *test counts and breakouts* to measure level strength

---

## *⚙ SETTINGS – Detailed Breakdown*

### *1️⃣ ◆ General Settings*

#### *🔹 Pivot Length*

- *Purpose:* Determines how many bars to analyze when identifying pivots.

- *Usage:*

- *Low values (5-20):* More pivots, better for scalping.

- *High values (50-200):* Fewer but stronger levels for swing trading.

- *Example:*

- Pivot Length = 50 → Only the most significant highs/lows over 50 bars are marked.

#### *🔹 Test Threshold (Max Test Count)*

- *Purpose:* Sets how many times a level can be tested before being invalidated.

- *Example:*

- Test Threshold = 3 → After 3 tests, the level is ignored (likely to break).

#### *🔹 Zone Range*

- *Purpose:* Creates a price buffer around pivots (±0.001 by default).

- *Why?* Markets often respect "zones" rather than exact prices.

---

### *2️⃣ ◆ Volatility Filter (ATR)*

#### *🔹 ATR Period*

- *Purpose:* Smoothing period for Average True Range calculation.

- *Default:* 14 (standard for volatility measurement).

#### *🔹 ATR Multiplier (Min Move)*

- *Purpose:* Requires pivots to show *meaningful price movement*.

- *Formula:* Min Move = ATR × Multiplier

- *Example:*

- ATR = 10 pips, Multiplier = 1.5 → Only pivots with *15+ pip swings* are valid.

#### *🔹 Show ATR Filter Info*

- Displays current ATR and minimum move requirements on the chart.

---

### *3️⃣ ◆ Volume Analysis*

#### *🔹 Volume Change Threshold (%)*

- *Purpose:* Filters for *unusual volume spikes* (institutional activity).

- *Example:*

- Threshold = 1.2 → Requires *120% of average volume* to confirm signals.

#### *🔹 Volume MA Period*

- *Purpose:* Lookback period for "normal" volume calculation.

---

### *4️⃣ ◆ Wick Analysis*

#### *🔹 Wick Length Threshold (Ratio)*

- *Purpose:* Ensures rejection candles have *long wicks* (strong reversals).

- *Formula:* Wick Ratio = (Upper Wick + Lower Wick) / Candle Range

- *Example:*

- Threshold = 0.6 → 60% of the candle must be wicks.

#### *🔹 Min Wick Size (ATR %)*

- *Purpose:* Filters out small wicks in volatile markets.

- *Example:*

- ATR = 20 pips, MinWickSize = 1% → Wicks under *0.2 pips* are ignored.

---

### *5️⃣ ◆ Display Settings*

- *Show Zones:* Toggles support/resistance shaded areas.

- *Show Traps:* Highlights liquidity traps (▲/▼ symbols).

- *Show Tests:* Displays how many times levels were tested.

- *Zone Transparency:* Adjusts opacity of zones.

---

## *🎯 Practical Use Cases*

### *1️⃣ Liquidity Trap Detection*

- *Scenario:* Price spikes *above resistance* then reverses sharply.

- *Requirements:*

- Long wick (Wick Ratio > 0.6)

- High volume (Volume > Threshold)

- *Outcome:* *Short Trap* signal (▼) appears.

### *2️⃣ Strong Support Level*

- *Scenario:* Price bounces *3 times* from the same level.

- *Indicator Action:*

- Labels the level with test count (3/5 = 3 tests out of max 5).

- Turns *red* if broken (Break Count > 0).

Deep Dive: How This Indicator Works*

This indicator combines *four professional trading concepts* into one powerful tool:

1. *Classic Pivot Point Theory*

- Identifies swing highs/lows where price previously reversed

- Unlike basic pivot indicators, ours uses *confirmed pivots only* (filtered by ATR)

2. *Volume-Weighted Validation*

- Requires unusual trading volume to confirm levels

- Filters out "phantom" levels with low participation

3. *ATR Volatility Filtering*

- Eliminates insignificant price swings in choppy markets

- Ensures only meaningful levels are plotted

4. *Liquidity Trap Detection*

- Spots institutional stop hunts where markets fake out traders

- Uses wick analysis + volume spikes for high-probability signals

---

Deep Dive: How This Indicator Works*

This indicator combines *four professional trading concepts* into one powerful tool:

1. *Classic Pivot Point Theory*

- Identifies swing highs/lows where price previously reversed

- Unlike basic pivot indicators, ours uses *confirmed pivots only* (filtered by ATR)

2. *Volume-Weighted Validation*

- Requires unusual trading volume to confirm levels

- Filters out "phantom" levels with low participation

3. *ATR Volatility Filtering*

- Eliminates insignificant price swings in choppy markets

- Ensures only meaningful levels are plotted

4. *Liquidity Trap Detection*

- Spots institutional stop hunts where markets fake out traders

- Uses wick analysis + volume spikes for high-probability signals

---

## *📊 Parameter Encyclopedia (Expanded)*

### *1️⃣ Pivot Engine Settings*

#### *Pivot Length (50)*

- *What It Does:*

Determines how many bars to analyze when searching for swing highs/lows.

- *Professional Adjustment Guide:*

| Trading Style | Recommended Value | Why? |

|--------------|------------------|------|

| Scalping | 10-20 | Captures short-term levels |

| Day Trading | 30-50 | Balanced approach |

| Swing Trading| 50-200 | Focuses on major levels |

- *Real Market Example:*

On NASDAQ 5-minute chart:

- Length=20: Identifies levels holding for ~2 hours

- Length=50: Finds levels respected for entire trading day

#### *Test Threshold (5)*

- *Advanced Insight:*

Institutions often test levels 3-5 times before breaking them. This setting mimics the "probe and push" strategy used by smart money.

- *Psychology Behind It:*

Retail traders typically give up after 2-3 tests, while institutions keep testing until stops are run.

---

### *2️⃣ Volatility Filter System*

#### *ATR Multiplier (1.0)*

- *Professional Formula:*

Minimum Valid Swing = ATR(14) × Multiplier

- *Market-Specific Recommendations:*

| Market Type | Optimal Multiplier |

|------------------|--------------------|

| Forex Majors | 0.8-1.2 |

| Crypto (BTC/ETH) | 1.5-2.5 |

| SP500 Stocks | 1.0-1.5 |

- *Why It Matters:*

In EUR/USD (ATR=10 pips):

- Multiplier=1.0 → Requires 10 pip swings

- Multiplier=1.5 → Requires 15 pip swings (fewer but higher quality levels)

---

### *3️⃣ Volume Confirmation System*

#### *Volume Threshold (1.2)*

- *Institutional Benchmark:*

- 1.2x = Moderate institutional interest

- 1.5x+ = Strong smart money activity

- *Volume Spike Case Study:*

*Before Apple Earnings:*

- Normal volume: 2M shares

- Spike threshold (1.2): 2.4M shares

- Actual volume: 3.1M shares → STRONG confirmation

---

### *4️⃣ Liquidity Trap Detection*

#### *Wick Analysis System*

- *Two-Filter Verification:*

1. *Wick Ratio (0.6):*

- Ensures majority of candle shows rejection

- Formula: (UpperWick + LowerWick) / Total Range > 0.6

2. *Min Wick Size (1% ATR):*

- Prevents false signals in flat markets

- Example: ATR=20 pips → Min wick=0.2 pips

- *Trap Identification Flowchart:*

Price Enters Zone →

Spikes Beyond Level →

Shows Long Wick →

Volume > Threshold →

TRAP CONFIRMED

---

## *💡 Master-Level Usage Techniques*

### *Institutional Order Flow Analysis*

1. *Step 1:* Identify pivot levels with ≥3 tests

2. *Step 2:* Watch for volume contraction near levels

3. *Step 3:* Enter when trap signal appears with:

- Wick > 2×ATR

- Volume > 1.5× average

### *Multi-Timeframe Confirmation*

1. *Higher TF:* Find weekly/monthly pivots

2. *Lower TF:* Use this indicator for precise entries

3. *Example:*

- Weekly pivot at $180

- 4H shows liquidity trap → High-probability reversal

---

## *⚠ Critical Mistakes to Avoid*

1. *Using Default Settings Everywhere*

- Crude oil needs higher ATR multiplier than bonds

2. *Ignoring Trap Context*

- Traps work best at:

- All-time highs/lows

- Major psychological numbers (00/50 levels)

3. *Overlooking Cumulative Volume*

- Check if volume is building over multiple tests

Fib BB on VWMA*ATRThis TradingView Pine Script is designed to plot Fibonacci Bollinger Bands on a Volume Weighted Moving Average (VWMA) using the Average True Range (ATR). The script takes a higher timeframe (HTF) approach, allowing traders to analyze price action and volatility from a broader market perspective.

🔹 How It Works

Higher Timeframe Data Integration

Users can select a specific timeframe to calculate the VWMA and ATR.

This allows for a more macro perspective, avoiding the noise of lower timeframes.

Volume Weighted Moving Average (VWMA)

Unlike the Simple Moving Average (SMA), VWMA gives higher weight to price movements with larger volume.

Calculation Formula:

𝑉𝑊𝑀𝐴=∑(𝐶𝑙𝑜𝑠𝑒×𝑉𝑜𝑙𝑢𝑚𝑒) / ∑𝑉𝑜𝑙𝑢𝑚𝑒

Since VWMA accounts for volume, it is more reactive to price zones with high buying or selling activity, making it useful for identifying liquidity zones.

ATR-Based Fibonacci Bollinger Bands

The Average True Range (ATR) is used to measure market volatility.

Instead of standard deviation-based Bollinger Bands, Fibonacci multipliers (2.618, 3.0, 3.414) are applied to ATR.

These bands adjust dynamically with market volatility.

🔹 Key Findings from Exploration

Through testing and analysis, this indicator seems to effectively detect supply and demand zones, particularly at the Fibonacci levels of 2.618 to 3.414.

Price frequently reacts at these bands, indicating that they capture key liquidity zones.

Potential Order Block Detection:

The ends of the Fibonacci Bollinger Bands (especially at 2.618, 3.0, and 3.414) tend to align with order blocks—areas where institutional traders previously accumulated or distributed positions.

This is particularly useful for order flow traders who focus on unfilled institutional orders.

🔹 How to Use This Indicator?

Identifying Order Blocks

When price reaches the upper or lower bands, check if there was a strong reaction (rejection or consolidation).

If price rapidly moves away from a band, that level might be an order block.

Spotting Liquidity Pools

VWMA’s nature enhances liquidity detection since it emphasizes high-volume price action.

If a price level repeatedly touches the band without breaking through, it suggests institutional orders may be absorbing liquidity there.

Trend Confirmation

If VWMA is trending upwards and price keeps rejecting the lower bands, it confirms a strong bullish trend.

Conversely, constant rejection from the upper bands suggests a bearish market.

This script is designed for open-source publication and offers traders a refined approach to detecting order blocks and liquidity zones using Fibonacci-based volatility bands.

📌 한글 설명 (상세 설명)

이 트레이딩뷰 파인스크립트는 거래량 가중 이동평균(VWMA)과 평균 실제 범위(ATR)를 활용하여 피보나치 볼린저 밴드를 표시하는 지표입니다.

또한, 고차 타임프레임(HTF) 데이터를 활용하여 시장의 큰 흐름을 분석할 수 있도록 설계되었습니다.

🔹 지표 작동 방식

고차 타임프레임(HTF) 데이터 적용

사용자가 원하는 타임프레임을 선택하여 VWMA와 ATR을 계산할 수 있습니다.

이를 통해 더 큰 시장 흐름을 분석할 수 있으며, 저타임프레임의 노이즈를 줄일 수 있습니다.

거래량 가중 이동평균(VWMA) 적용

VWMA는 단순 이동평균(SMA)보다 거래량이 많은 가격 움직임에 더 큰 가중치를 부여합니다.

계산 공식:

𝑉𝑊𝑀𝐴=∑(𝐶𝑙𝑜𝑠𝑒×𝑉𝑜𝑙𝑢𝑚𝑒) / ∑𝑉𝑜𝑙𝑢𝑚𝑒

거래량이 많이 발생한 가격 구간을 강조하는 특성이 있어, 시장의 유동성 구간을 더 정확히 포착할 수 있습니다.

ATR 기반 피보나치 볼린저 밴드 생성

ATR(Average True Range)를 활용하여 변동성을 측정합니다.

기존의 표준편차 기반 볼린저 밴드 대신, 피보나치 계수(2.618, 3.0, 3.414)를 ATR에 곱하여 밴드를 생성합니다.

이 밴드는 시장 변동성에 따라 유동적으로 조정됩니다.

🔹 탐구 결과: 매물대 및 오더블록 감지

테스트를 통해 Fibonacci 2.618 ~ 3.414 구간에서 매물대 및 오더블록을 포착하는 경향이 있음을 확인했습니다.

가격이 피보나치 밴드(특히 2.618, 3.0, 3.414)에 닿을 때 반응하는 경우가 많음

VWMA의 특성을 통해 오더블록을 감지할 가능성이 높음

🔹 오더블록(Order Block) 감지 원리

Fibonacci 밴드 끄트머리(2.618 ~ 3.414)에서 가격이 강하게 반응

이 영역에서 가격이 강하게 튀어 오르거나(매수 압력) 급락하는(매도 압력) 경우,

→ 기관들이 포지션을 청산하거나 추가 매집하는 구간일 가능성이 큼.

과거에 대량 주문이 체결된 가격 구간(= 오더블록)일 수 있음.

VWMA를 통한 유동성 감지

VWMA는 거래량이 집중된 가격을 기준으로 이동하기 때문에, 기관 주문이 많이 들어온 가격대를 강조하는 특징이 있음.

따라서 VWMA와 피보나치 밴드가 만나는 지점은 유동성이 높은 핵심 구간이 될 가능성이 큼.

매물대 및 청산 구간 분석

가격이 밴드에 도달했을 때 강한 반등이 나오는지를 확인 → 오더블록 가능성

가격이 밴드를 여러 번 테스트하면서 돌파하지 못한다면, 해당 지점은 강한 매물대일 가능성

🔹 활용 방법

✅ 오더블록 감지:

가격이 밴드(2.618~3.414)에 닿고 강하게 튕긴다면, 오더블록 가능성

해당 지점에서 거래량 증가 및 강한 반등 발생 시 매수 고려

✅ 유동성 풀 확인:

VWMA와 피보나치 밴드가 만나는 구간에서 반복적으로 거래량이 터진다면, 해당 지점은 기관 유동성 구간일 가능성

✅ 추세 확인:

VWMA가 상승하고 가격이 밴드 하단(지지선)에서 튕긴다면 강한 상승 추세

VWMA가 하락하고 가격이 밴드 상단(저항선)에서 거부당하면 하락 추세 지속

Volume Profile & Smart Money Explorer🔍 Volume Profile & Smart Money Explorer: Decode Institutional Footprints

Master the art of institutional trading with this sophisticated volume analysis tool. Track smart money movements, identify peak liquidity windows, and align your trades with major market participants.

🌟 Key Features:

📊 Triple-Layer Volume Analysis

• Total Volume Patterns

• Directional Volume Split (Up/Down)

• Institutional Flow Detection

• Real-time Smart Money Tracking

• Historical Pattern Recognition

⚡ Smart Money Detection

• Institutional Trade Identification

• Large Block Order Tracking

• Smart Money Concentration Periods

• Whale Activity Alerts

• Volume Threshold Analysis

📈 Advanced Profiling

• Hourly Volume Distribution

• Directional Bias Analysis

• Liquidity Heat Maps

• Volume Pattern Recognition

• Custom Threshold Settings

🎯 Strategic Applications:

Institutional Trading:

• Track Big Player Movements

• Identify Accumulation/Distribution

• Follow Smart Money Flow

• Detect Institutional Trading Windows

• Monitor Block Orders

Risk Management:

• Identify High Liquidity Windows

• Avoid Thin Market Periods

• Optimize Position Sizing

• Track Market Participation

• Monitor Volume Quality

Market Analysis:

• Volume Pattern Recognition

• Smart Money Flow Analysis

• Liquidity Window Identification

• Institutional Activity Cycles

• Market Depth Analysis

💡 Perfect For:

• Professional Traders

• Volume Profile Traders

• Institutional Traders

• Risk Managers

• Algorithmic Traders

• Smart Money Followers

• Day Traders

• Swing Traders

📊 Key Metrics:

• Normalized Volume Profiles

• Institutional Thresholds

• Directional Volume Split

• Smart Money Concentration

• Historical Patterns

• Real-time Analysis

⚡ Trading Edge:

• Trade with Institution Flow

• Identify Optimal Entry Points

• Recognize Distribution Patterns

• Follow Smart Money Positioning

• Avoid Thin Markets

• Capitalize on Peak Liquidity

🎓 Educational Value:

• Understand Market Structure

• Learn Volume Analysis

• Master Institutional Patterns

• Develop Market Intuition

• Track Smart Money Flow

🛠️ Customization:

• Adjustable Time Windows

• Flexible Volume Thresholds

• Multiple Timeframe Analysis

• Custom Alert Settings

• Visual Preference Options

Whether you're tracking institutional flows in crypto markets or following smart money in traditional markets, the Volume Profile & Smart Money Explorer provides the deep insights needed to trade alongside the biggest players.

Transform your trading from retail guesswork to institutional precision. Know exactly when and where smart money moves, and position yourself ahead of major market shifts.

#VolumeProfile #SmartMoney #InstitutionalTrading #MarketAnalysis #TradingView #VolumeAnalysis #CryptoTrading #ForexTrading #TechnicalAnalysis #Trading #PriceAction #MarketStructure #OrderFlow #Liquidity #RiskManagement #TradingStrategy #DayTrading #SwingTrading #AlgoTrading #QuantitativeTrading

EBP Candle Marker### **EBP Candle Marker – TradingView Indicator**

The **EBP Candle Marker** is a specialized TradingView indicator designed to identify and highlight potential liquidity sweep candles. This indicator visually emphasizes key price action patterns where the market sweeps previous highs or lows and closes in the opposite direction, often signaling potential reversals or liquidity grabs.

---

### 📊 **Indicator Logic:**

1. **Bullish Sweep:**

- The current candle’s **low** is lower than the previous candle’s **low** (indicating a liquidity sweep).

- The **close** is above both the **open** and **close** of the previous candle.

2. **Bearish Sweep:**

- The current candle’s **high** is higher than the previous candle’s **high** (indicating a liquidity sweep).

- The **close** is below both the **open** and **close** of the previous candle.

---

### 🎨 **Visual Representation:**

- **Yellow Candle Body:** Highlights any candle meeting the bullish or bearish sweep conditions.

---

### 🔔 **Alert Functionality:**

The indicator supports setting custom alerts in TradingView for:

- **Bullish Sweep Detected** – Notifies when a bullish sweep occurs.

- **Bearish Sweep Detected** – Notifies when a bearish sweep occurs.

These alerts are compatible across any timeframe, providing flexibility to monitor key market conditions.

---

### 📈 **Use Cases:**

- **Liquidity Sweep Detection:** Identify areas where the market may be triggering stop-loss orders or liquidity hunts.

- **Reversal Confirmation:** Enhance trade confirmation by identifying potential reversal zones.

- **Scalping & Swing Trading:** Suitable for both short-term and long-term trading strategies across multiple timeframes.

CLS Patterns + Price Action Levels📌 Key Features:

✅ CLS Candle Patterns Detection:

CLS Type 1 (Sweeps & Closes Opposite) – Confirms liquidity sweeps with opposite direction close.

CLS Type 2 (Sweeps but No Opposite Close) – Identifies liquidity traps without full reversal.

CLS Type 3 (Engulfing Candles) – Strong momentum shifts with engulfing price action.

CLS Type 4 (Order Block Reversals) – Institutional order flow recognition.

✅ Institutional & Price Action Levels:

250 Pip Institutional Levels – Major S&R zones for Forex & Indices.

Minor Quarter Points (25 Pips) – Intraday precision for refined entries.

✅ Liquidity Imbalance & Order Flow Gaps:

Detects early impulse moves & liquidity voids

Highlights areas of market inefficiency & potential reversals

✅ Higher Timeframe EMA for Trend Confirmation:

Customizable Weekly 3 EMA Overlay

Dynamic color change based on price action

✅ Built-in Alerts for CLS Patterns:

Real-time alerts for CLS buy/sell signals

Configurable notifications for trade execution

🎯 How to Use:

1️⃣ Enable CLS Pattern Signals to spot liquidity sweep candles with directional confirmation.

2️⃣ Use Institutional & QP Levels to identify key areas where price is likely to react.

3️⃣ Monitor Liquidity Imbalances to detect inefficient price moves that may fill.

4️⃣ Confirm Trend with HTF EMA to trade with momentum.

5️⃣ Set Alerts for CLS patterns and key price levels to stay ahead of the market.

This indicator is ideal for Forex, Indices, and Crypto traders looking to refine their entries with precise price action confirmations.

Sniper Trade Pro (ES 15-Min) - Topstep Optimized🔹 Overview

Sniper Trade Pro is an advanced algorithmic trading strategy designed specifically for E-mini S&P 500 (ES) Futures on the 15-minute timeframe. This strategy is optimized for Topstep 50K evaluations, incorporating strict risk management to comply with their max $1,000 daily loss limit while maintaining a high probability of success.

It uses a multi-confirmation approach, integrating:

✅ Money Flow Divergence (MFD) → To track liquidity imbalances and institutional accumulation/distribution.

✅ Trend Confirmation (EMA + VWAP) → To identify strong trend direction and avoid choppy markets.

✅ ADX Strength Filter → To ensure entries only occur in trending conditions, avoiding weak setups.

✅ Break-Even & Dynamic Stop-Losses → To reduce drawdowns and protect profits dynamically.

This script automatically generates Buy and Sell signals and provides built-in risk management for automated trading execution through TradingView Webhooks.

🔹 How Does This Strategy Work?

📌 1. Trend Confirmation (EMA + VWAP)

The strategy uses:

✔ 9-EMA & 21-EMA: Fast-moving averages to detect short-term momentum.

✔ VWAP (Volume-Weighted Average Price): Ensures trades align with institutional volume flow.

How it works:

Bullish Condition: 9-EMA above 21-EMA AND price above VWAP → Confirms buy trend.

Bearish Condition: 9-EMA below 21-EMA AND price below VWAP → Confirms sell trend.

📌 2. Liquidity & Money Flow Divergence (MFD)

This indicator measures liquidity shifts by tracking momentum changes in price and volume.

✔ MFD Calculation:

Uses Exponential Moving Average (EMA) of Momentum (MOM) to detect changes in buying/selling pressure.

If MFD is above its moving average, it signals liquidity inflows → bullish strength.

If MFD is below its moving average, it signals liquidity outflows → bearish weakness.

Why is this important?

Detects when Smart Money is accumulating or distributing before major moves.

Filters out false breakouts by confirming momentum strength before entry.

📌 3. Trade Entry Triggers (Candlestick Patterns & ADX Filter)

To avoid random entries, the strategy waits for specific candlestick confirmations with ADX trend strength:

✔ Bullish Entry (Buy Signal) → Requires:

Bullish Engulfing Candle (Reversal confirmation)

ADX > 20 (Ensures strong trending conditions)

MFD above its moving average (Liquidity inflows)

9-EMA > 21-EMA & price above VWAP (Trend confirmation)

✔ Bearish Entry (Sell Signal) → Requires:

Bearish Engulfing Candle (Reversal confirmation)

ADX > 20 (Ensures strong trending conditions)

MFD below its moving average (Liquidity outflows)

9-EMA < 21-EMA & price below VWAP (Trend confirmation)

📌 4. Risk Management & Profit Protection

This strategy is built with strict risk management to maintain low drawdowns and maximize profits:

✔ Dynamic Position Sizing → Automatically adjusts trade size to risk a fixed $400 per trade.

✔ Adaptive Stop-Losses → Uses ATR-based stop-loss (0.8x ATR) to adapt to market volatility.

✔ Take-Profit Targets → Fixed at 2x ATR for a Risk:Reward ratio of 2:1.

✔ Break-Even Protection → Moves stop-loss to entry once price moves 1x ATR in profit, locking in gains.

✔ Max Daily Loss Limit (-$1,000) → Stops trading if total losses exceed $1,000, complying with Topstep rules.

Trading Sessions Highs/Lows | InvrsROBINHOODTrading Sessions Highs/Lows | InvrsROBINHOOD

🚀 A powerful indicator for tracking key trading sessions and the highs and lows of each session!

📌 Description

The Trading Sessions Highs/Lows indicator visually marks the most critical trading sessions—Asia, London, and New York—using small colored dots at the bottom of the candle. It also tracks and plots the highs and lows of each session, along with the Daily Open and Weekly Open levels.

This tool is designed to help traders identify session-based liquidity zones, price reactions, and potential trade setups with minimal chart clutter.

Key Features:

✅ Session markers (Asia, London, NY AM, NY Lunch, NY PM) plotted as small dots

✅ Plots session highs and lows for market structure insights

✅ Daily Open line for intraday reference

✅ Weekly Open line for higher timeframe bias

✅ Alerts for session high/low breaks to capture momentum shifts

✅ User-defined UTC offset for global traders

✅ Customizable session colors for personal preference

📖 How to Use the Indicator

1️⃣ Understanding the Sessions

Asia Session (Yellow Dot) → Marks liquidity buildup & pre-London moves

London Session (Blue Dot) → Strong volatility, breakout opportunities

New York AM Session (Green Dot) → Major trends & institutional participation

New York Lunch (Red Dot) → Low volume, ranging market

New York PM Session (Dark Green Dot) → End-of-day movements & reversals

2️⃣ Session Highs & Lows for Market Structure

Session Highs can act as resistance or breakout points.

Session Lows can act as support or stop-hunt zones.

Break of a session high/low with volume may indicate continuation or reversal.

3️⃣ Using the Daily & Weekly Open

The Daily Open (Black Line) helps gauge the intraday trend.

Above Daily Open → Bearish Bias

Below Daily Open → Bullish Bias

The Weekly Open (Red Line) sets the higher timeframe directional bias.

4️⃣ Alerts for Breakouts

The indicator will trigger alerts when price breaks session highs or lows.

Useful for setting stop-losses, breakout trades, and risk management.

💡 Why This Indicator is Important for Beginners

1️⃣ Avoids Overtrading:

Many beginners trade in low-volume periods (NY Lunch, Asia session) and get stuck in choppy price action.

This indicator highlights when volatility is high so traders focus on better opportunities.

2️⃣ Session-Based Liquidity Traps:

Market makers often run stops at session highs/lows before reversing.

Watching session breaks prevents traders from falling into liquidity grabs.

3️⃣ Reduces Emotional Trading:

If price is above the Daily Open, a beginner shouldn’t look for shorts.

If price is below a key session low, it may signal a fake breakout.

4️⃣ Aligns with Institutional Trading:

Smart money traders use session highs/lows to set stop hunts & reversals.

Beginners can use this indicator to spot these zones before entering trades.

🛡️ How to Mitigate Risk with This Indicator

✅ Wait for Confirmations – Don’t trade blindly at session highs/lows. Look for wicks, rejections, or break/retests.

✅ Use Stop-Loss Above/Below Session Levels – If you’re going long, set SL below a session low. If short, set SL above a session high.

✅ Watch Volume & News Events – Breakouts without strong volume or news may be fake moves.

✅ Combine with Other Strategies – Use price action, trendlines, or EMAs with this indicator for higher probability trades.

✅ Use the Weekly Open for Trend Bias – If price stays below the Weekly Open, avoid bullish setups unless key support holds.

🎯 Who is This Indicator For?

📌 Beginners who need clear session-based trading levels.

📌 Day traders & scalpers looking to refine their intraday setups.

📌 Smart money traders using liquidity concepts.

📌 Swing traders tracking higher timeframe momentum shifts.

🚀 Final Thoughts

This indicator is an essential tool for traders who want to understand market structure, liquidity, and volatility cycles. Whether you’re trading forex, stocks, or crypto, it helps you stay on the right side of the market and avoid unnecessary risks.

🔹 Set it up, customize your colors, define your UTC offset, and start trading smarter today! 🏆📈

Swing Breakout System (SBS)The Swing Breakout Sequence (SBS) is a trading strategy that focuses on identifying high-probability entry points based on a specific pattern of price swings. This indicator will identify these patterns, then draw lines and labels to show confirmation.

How To Use:

The indicator will show both Bullish and Bearish SBS patterns.

Bullish Pattern is made up of 6 points: Low (0), HH (1), LL (2 | but higher than initial Low), New HH (3), LL (5), LL again (5)

Bearish Patten is made up of 6 points: High (0), LL (1), HH (2 | but lower than initial high), New LL (3), HH (5), HH again (5)

A label with an arrow will appear at the end, showing the completion of a successful sequence

Idea behind the strategy:

The idea behind this strategy, is the accumulation and then manipulation of liquidity throughout the sequence. For example, during SBS sequence, liquidity is accumulated during step (2), then price will push away to make a new high/low (step 3), after making a minor new high/low, price will retrace breaking the key level set up in step (2). This is price manipulating taking liquidity from behind high/low from step (2). After taking liquidity price the idea is price will continue in the original direction.

Step 0 - Setting up initial direction

Step 1 - Setting up initial direction

Step 2 - Key low/high establishing liquidity

Step 3 - Failed New high/low

Step 4 - Taking liquidity from step (2)

Step 5 - Taking liquidity from step 2 and 4

Pattern Detection:

- Uses pivot high/low points to identify swing patterns

- Stores 6 consecutive swing points in arrays

- Identifies two types of patterns:

1. Bullish Pattern: A specific sequence of higher lows and higher highs

2. Bearish Pattern: A specific sequence of lower highs and lower lows

Note: Because the indicator is identifying a perfect sequence of 6 steps, set ups may not appear frequently.

Visualization:

- Draws connecting lines between swing points

- Labels each point numerically (optional)

- Shows breakout arrows (↑ for bullish, ↓ for bearish)

- Generates alerts on valid breakouts

User Input Settings:

Core Parameters

1. Pivot Lookback Period (default: 2)

- Controls how many bars to look back/forward for pivot point detection

- Higher values create fewer but more significant pivot points

2. Minimum Pattern Height % (default: 0.1)

- Minimum required height of the pattern as a percentage of price

- Filters out insignificant patterns

3. Maximum Pattern Width (bars) (default: 50)

- Maximum allowed width of the pattern in bars

- Helps exclude patterns that form over too long a period

LRLR [TakingProphets]LRLR (Low Resistance Liquidity Run) Indicator

This indicator identifies potential liquidity runs in areas of low resistance, based on ICT (Inner Circle Trader) concepts. It specifically looks for a series of unmitigated swing highs in a downtrend that form without any bearish fair value gaps (FVGs) between them.

What is an LRLR?

- A Low Resistance Liquidity Run occurs when price creates a series of lower highs without any bearish fair value gaps in between

- The absence of bearish FVGs indicates there is no significant resistance in the area

- These formations often become targets for smart money to collect liquidity above the swing highs

How to Use the Indicator:

1. The indicator will draw a diagonal line connecting a series of qualifying swing highs

2. A small "LRLR" label appears to mark the pattern

3. These areas often become targets for future price moves, as they represent zones of accumulated liquidity with minimal resistance

Key Points:

- Minimum of 4 consecutive lower swing highs

- No bearish fair value gaps can exist between these swing highs

- The diagonal line helps visualize the liquidity run formation

- Can be used for trade planning and identifying potential reversal zones

Settings:

- Show Labels: Toggle the "LRLR" label visibility

- LRLR Line Color: Customize the appearance of the diagonal line

Best Practices:

1. Use in conjunction with other ICT concepts and market structure analysis

2. Pay attention to how price reacts when returning to these levels

3. Consider these areas as potential targets for smart money liquidity grabs

4. Most effective when used on higher timeframes (4H and above)

Note: This is an educational tool and should be used as part of a complete trading strategy, not in isolation.

RSI Divergence + Sweep + Signal + Alerts Toolkit [TrendX_]The RSI Toolkit is a powerful set of tools designed to enhance the functionality of the traditional Relative Strength Index (RSI) indicator. By integrating advanced features such as Moving Averages, Divergences, and Sweeps, it helps traders identify key market dynamics, potential reversals, and newly-approach trading stragies.

The toolkit expands on standard RSI usage by incorporating features from smart money concepts (Just try to be creative 🤣 Hope you like it), providing a deeper understanding of momentum, liquidity sweeps, and trend reversals. It is suitable for RSI traders who want to make more informed and effective trading decisions.

💎 FEATURES

RSI Moving Average

The RSI Moving Average (RSI MA) is the moving average of the RSI itself. It can be customized to use various types of moving averages, including Simple Moving Average (SMA), Exponential Moving Average (EMA), Relative Moving Average (RMA), and Volume-Weighted Moving Average (VWMA).

The RSI MA smooths out the RSI fluctuations, making it easier to identify trends and crossovers. It helps traders spot momentum shifts and potential entry/exit points by observing when the RSI crosses above or below its moving average.

RSI Divergence

RSI Divergence identifies discrepancies between price action and RSI momentum. There are two types of divergences: Regular Divergence - Indicates a potential trend reversal; Hidden Divergence - Suggests the continuation of the current trend.

Divergence is a critical signal for spotting weakness or strength in a trend. Regular divergence highlights potential trend reversals, while hidden divergence confirms trend continuation, offering traders valuable insights into market momentum and possible trade setups.

RSI Sweep

RSI Sweep detects moments when the RSI removes liquidity from a trend structure by sweeping above or below the price at key momentum level crossing. These sweeps are overlaid on the RSI chart for easier visualized.

RSI Sweeps are significant because they indicate potential turning points in the market. When RSI sweeps occur: In an uptrend - they suggest buyers' momentum has peaked, possibly leading to a reversal; In a downtrend - they indicate sellers’ momentum has peaked, also hinting at a reversal.

(Note: This feature incorporates Liquidity Sweep concepts from Smart Money Concepts into RSI analysis, helping RSI traders identify areas where liquidity has been removed, which often precedes a trend reversal)

🔎 BREAKDOWN

RSI Moving Average

How MA created: The RSI value is calculated first using the standard RSI formula. The MA is then applied to the RSI values using the trader’s chosen type of MA (SMA, EMA, RMA, or VWMA). The flexibility to choose the type of MA allows traders to adjust the smoothing effect based on their trading style.

Why use MA: RSI by itself can be noisy and difficult to interpret in volatile markets. Applying moving average would provide a smoother, more reliable view of RSI trends.

RSI Divergence

How Regular Divergence created: Regular Divergence is detected when price forms HIGHER highs while RSI forms LOWER highs (bearish divergence) or when price forms LOWER lows while RSI forms HIGHER lows (bullish divergence).

How Hidden Divergence created: Hidden Divergence is identified when price forms HIGHER lows while RSI forms LOWER lows (bullish hidden divergence) or when price forms LOWER highs while RSI forms HIGHER highs (bearish hidden divergence).

Why use Divergence: Divergences provide early warning signals of a potential trend change. Regular divergence helps traders anticipate reversals, while hidden divergence supports trend continuation, enabling traders to align their trades with market momentum.

RSI Sweep

How Sweep created: Trend Structure Shift are identified based on the RSI crossing key momentum level of 50. To track these sweeps, the indicator pinpoints moments when liquidity is removed from the Trend Structure Shift. This is a direct application of Liquidity Sweep concepts used in Smart Money theories, adapted to RSI.

Why use Sweep: RSI Sweeps are created to help traders detect potential trend reversals. By identifying areas where momentum has exhausted during a certain trend direction, the indicator highlights opportunities for traders to enter trades early in a reversal or continuation phase.

⚙️ USAGES

Divergence + Sweep

This is an example of combining Devergence & Sweep in BTCUSDT (1 hour)

Wait for a divergence (regular or hidden) to form on the RSI. After the divergence is complete, look for a sweep to occur. A potential entry might be formed at the end of the sweep.

Divergences indicate a potential trend change, but confirmation is required to ensure the setup is valid. The RSI Sweep provides that confirmation by signaling a liquidity event, increasing the likelihood of a successful trade.

Sweep + MA Cross

This is an example of combining Devergence & Sweep in BTCUSDT (1 hour)

Wait for an RSI Sweep to form then a potential entry might be formed when the RSI crosses its MA.

The RSI Sweep highlights a potential turning point in the market. The MA cross serves as additional confirmation that momentum has shifted, providing a more reliable and more potential entry signal for trend continuations.

DISCLAIMER

This indicator is not financial advice, it can only help traders make better decisions. There are many factors and uncertainties that can affect the outcome of any endeavor, and no one can guarantee or predict with certainty what will occur. Therefore, one should always exercise caution and judgment when making decisions based on past performance.

16. SMC Strategy with SL - low TimeframeOverview

The "SMC Strategy with SL - low Timeframe" is a comprehensive trading strategy that uses key concepts from Smart Money Theory to identify favorable areas in the market for buying or selling. This strategy takes advantage of price imbalances, support and resistance zones, and swing highs/lows to generate high-probability trade signals.

The key features of this strategy include:

Swing High/Low Analysis: Used to determine the Premium, Equilibrium, and Discount Zones.

Order Block Integration: An added layer of confluence to identify valid buy and sell signals.

Trend Direction Confirmation: Using a Simple Moving Average (SMA) to determine the overall trend.

Entry and Exit Rules: Based on price position relative to key zones and moving average, along with optional stop-loss and take-profit levels.

Detailed Description

Swing High and Swing Low Analysis

The script calculates Swing High and Swing Low based on the most recent price highs and lows over a specified look-back period (swingHighLength and swingLowLength, set to 8 by default).

It then derives the Premium, Equilibrium, and Discount Zones:

Premium Zone: Represents potential resistance, calculated based on recent swing highs.

Discount Zone: Represents potential support, calculated based on recent swing lows.

Equilibrium: The midpoint between Swing High and Swing Low, dividing the price range into Premium (above equilibrium) and Discount (below equilibrium) areas.

Zone Visualization

The strategy plots the Premium Zone (resistance) in red, the Discount Zone (support) in green, and the Equilibrium level in blue on the chart. This helps visually assess the current price relative to these important areas.

Simple Moving Average (SMA)

A 50-period Simple Moving Average (SMA) is added to help identify the trend direction.

Buy signals are valid only if the price is above the SMA, indicating an uptrend.

Sell signals are valid only if the price is below the SMA, indicating a downtrend.

Entry Rules

The script generates buy or sell signals when certain conditions are met:

A buy signal is triggered when:

Price is below the Equilibrium and within the Discount Zone.

Price is above the SMA.

The buy signal is further confirmed by the presence of an Order Block (recent lowest price area).

A sell signal is triggered when:

Price is above the Equilibrium and within the Premium Zone.

Price is below the SMA.