Opening Range {basic}Introduction

Opening range {basic} is a clean and reliable indicator designed to help traders visualize the opening range of a trading session with minimal setup and visual clutter.

This version focuses on the core components of opening range analysis, making it ideal for traders who want a simple, effective framework for identifying early-session structure across futures, forex and crypto markets.

Description

The indicator automatically calculates the opening range high, low and midpoint over a user-defined opening window (5m, 15m, 30m or 60m) within a selected trading session (default: NY session).

During the opening range window, the indicator dynamically tracks price to form the range. Once the opening range is complete, the high, low and midpoint are extended forward for the remainder of the session, providing clear reference levels that can be used for bias, mean reversion or breakout-based decision making.

A shaded fill highlights the opening range area, with an optional size display showing the total range in price units. Styling and logic are intentionally simplified to keep the chart clean and easy to interpret.

Features

Configurable opening range length

Choose between 5m, 15m, 30m or 60m opening ranges.

Session-based calculation

Opening range is calculated only within the selected trading session.

Opening range levels

Opening range high, low and midpoint.

Range fill & size display

Shaded fill between the opening range high and low.

Text showing total opening range size.

Clean, minimal design

Fixed line styles and thickness for clarity.

Dark and light theme support.

Minimal settings for fast, intuitive use.

Optimized performance

Designed for intraday timeframes compatible with the selected opening range length.

Terms & Conditions

This indicator is provided for educational and informational purposes only and does not constitute financial advice.

Trading involves risk and past performance is not indicative of future results.

The user assumes full responsibility for any trading decisions made using this indicator.

"range"に関するスクリプトを検索

Statistcal Daily Profile & Ranges# Statistical Daily Profile & Ranges - TradingView Publication Guide

## Overview

The **Statistical Daily Profile & Ranges** indicator is a comprehensive tool designed to analyze intraday session behavior and daily range characteristics. It combines Average Daily Range (ADR) projection levels with detailed session-by-session statistics and probability-based trading insights derived from historical price action patterns.

## What This Indicator Does

This indicator provides traders with three core analytical components:

1. **ADR Projection Levels** - Dynamic support/resistance levels based on historical daily ranges

2. **Session Range Analysis** - Visual boxes and statistical breakdowns for four key trading sessions

3. **Dynamic Probability Display** - Real-time probability statistics based on overnight session relationships

## How It Works

### Average Daily Range (ADR) Calculation

The indicator calculates the average daily range over a user-defined lookback period (default: 10 days) and projects this range from each day's opening price. This creates two key levels:

- **ADR High**: Opening price + average daily range

- **ADR Low**: Opening price - average daily range

- **ADR Median**: The opening price (middle of the projected range)

These levels are recalculated at the start of each trading day and extend forward, providing dynamic support and resistance zones based on recent volatility characteristics.

### Session Tracking & Statistics

The indicator monitors four distinct trading sessions (times in Eastern Time):

1. **Asia Session** (8:00 PM - 2:00 AM)

2. **London Session** (2:00 AM - 8:00 AM)

3. **NY Open** (8:00 AM - 9:00 AM)

4. **NY Initial Balance** (9:30 AM - 10:30 AM)

For each session, the indicator:

- Draws a colored box showing the session's high-to-low range

- Tracks the opening price, high, and low

- Stores historical data for statistical analysis

- Calculates average ranges by day of week (Monday through Friday)

The session statistics are displayed in a customizable table showing average point ranges for each session across different weekdays, helping traders identify which sessions and days typically produce the most movement.

### Dynamic Probability System

The indicator analyzes the relationship between the Asia and London sessions to determine the current market setup. After the London session closes, it automatically detects one of four possible conditions:

**1. London Engulfs Asia**

- London session breaks both above Asia's high AND below Asia's low

- This indicates strong momentum during the European session

- Most common occurrence pattern

**2. Asia Engulfs London**

- Asia session range completely contains the London session range

- Indicates consolidation during London hours

- Relatively rare pattern (occurs approximately 5.36% of the time)

**3. London Partially Engulfs Upwards**

- London breaks above Asia's high but stays above Asia's low

- Suggests bullish momentum continuation from Asia into London

**4. London Partially Engulfs Downwards**

- London breaks below Asia's low but stays below Asia's high

- Suggests bearish momentum continuation from Asia into London

Once a condition is detected, the indicator displays a probability table showing historically observed outcomes for that specific setup, including:

- Probability of NY session taking out key levels (Asia high/low, London high/low)

- Probability of NY session engulfing the entire overnight range

- Directional bias for NY Cash session (9:30 AM - 4:00 PM)

## How to Use This Indicator

### Initial Setup

1. Add the indicator to your chart (works on any intraday timeframe below Daily)

2. Adjust the **ADR Days** setting (default: 10) to control the lookback period for range calculation

3. Adjust the **Session Lookback Days** setting (default: 50) to determine how much historical data feeds the statistics tables

### Reading the ADR Levels

- Use the **ADR High** and **ADR Low** lines as potential profit targets or areas where price may encounter resistance

- The **ADR Median** line represents the opening price and can act as a pivot point for intraday directional bias

- If price reaches the ADR High early in the session, it suggests strong bullish momentum; conversely for ADR Low

- These levels adapt daily based on recent volatility, making them more responsive than static levels

### Interpreting Session Boxes

- **Session boxes** visually highlight when each trading session is active and its price range

- Larger boxes indicate higher volatility during that session

- Compare current session ranges to the statistical averages shown in the table

- Sessions that are unusually quiet or active relative to historical averages may signal compression or expansion

### Using the Session Statistics Table

- The table shows average point ranges for each session broken down by weekday

- Identify which sessions typically produce the most movement on specific days

- For example, if London on Thursdays averages 40 points while Mondays average 25 points, you can adjust position sizing or expectations accordingly

- The **Total** column shows the overall average across all days

- Sample sizes (shown in brackets if enabled) indicate data reliability

### Trading with the Probability Table

The probability table updates dynamically after the London session closes and shows statistically probable outcomes based on 12 years of NQ futures data.

**Important Limitations:**

- **These probabilities are derived from NQ (Nasdaq E-mini futures) data only**

- **Do NOT apply these probability statistics to other instruments** (ES, stocks, forex, etc.)

- The probabilities represent historical frequencies, not guarantees

- Always combine with your own analysis, risk management, and market context

**How to Apply the Probabilities:**

When **London Engulfs Asia**:

- Watch for NY session to take out London's extremes (72.33% probability for high, 71.12% for low)

- Slight bullish bias in NY Cash session (54.80% vs 45.20%)

- Lower probability of complete overnight engulfment (44.13%)

When **Asia Engulfs London** (rare - 5.36% occurrence):

- Higher probability NY takes Asia's high (75.86%)

- Moderately high probability NY takes Asia's low (65.52%)

- Slight increase in bullish bias (58.42% vs 41.58%)

- Recognize this as an unusual setup

When **London Partially Engulfs Upwards**:

- Very high probability NY takes London high (81.51%)

- Strong probability NY takes London low (64.45%)

- Moderate probability NY takes Asian low (53.16%)

- Slight bullish bias (55.52%)

When **London Partially Engulfs Downwards**:

- Very high probability NY takes London low (75.29%)

- Strong probability NY takes London high (68.80%)

- Moderate probability NY takes Asian high (56.44%)

- Slight bullish bias maintained (52.99%)

### Practical Trading Applications

**Scenario 1: Range Projection**

If the ADR is 500 points and the market opens at 25,000:

- ADR High: 25,500 (potential resistance/target)

- ADR Low: 24,500 (potential support/target)

- Monitor how price interacts with these levels throughout the day

**Scenario 2: Session-Based Trading**

Using the statistics table, you notice London on Wednesdays averages 35 points. During a Wednesday London session:

- If London has already moved 30 points, the session may be exhausting its typical range

- If London has only moved 15 points with an hour remaining, there may be expansion potential

- Adjust stop losses and targets based on typical session behavior

**Scenario 3: Probability-Based Setup**

It's 8:05 AM ET and the indicator shows "London Partially Engulfs Upwards":

- You now know there's an 81.51% historical probability NY will take out London's high

- There's a 53.16% probability NY will reach down to Asia's low

- The NY Cash session has a slight bullish bias (55.52%)

- Consider this alongside your technical analysis for directional bias and level targeting

## Customization Options

### Visual Settings

- **Line Width**: Adjust thickness of ADR levels

- **ADR Color/Style**: Customize appearance of ADR projection lines (solid, dashed, dotted)

- **Median Line**: Toggle visibility and customize appearance separately

- **Session Box Colors**: Customize each session's box color independently

- **Show Session Boxes**: Toggle session box visibility on/off

### Label Settings

- **ADR Labels**: Show/hide labels for ADR High and ADR Low, adjust size

- **Median Label**: Separate control for median line label

- **Session Labels**: Show/hide session name labels, adjust size

- **Label Colors**: Customize text colors for all labels

### Table Settings

- **Session Stats Table**: Position (9 locations available), size (Tiny to Huge), toggle on/off

- **Sample Sizes**: Show/hide the number of historical samples used for each calculation

- **Probabilities Table**: Separate position and size controls, toggle on/off

### Session Times

- Each session's time range can be customized to fit different markets or preferences

- All times are in Eastern Time (America/New_York timezone)

## Technical Notes

### Data Requirements

- The indicator requires sufficient historical data based on your lookback settings

- Minimum recommended: 50+ days of intraday data for reliable statistics

- Works on any timeframe below Daily (1-minute, 5-minute, 15-minute, etc.)

### Calculation Methodology

- **ADR Calculation**: Simple average of absolute daily high-low ranges

- **Session Statistics**: Mean average of ranges for each session filtered by day of week

- **Condition Detection**: Boolean logic comparing session high/low relationships

- All calculations update in real-time as new bars form

### Probability Data Source

The probability statistics displayed in the dynamic table are derived from:

- **Dataset**: 12 years of NQ (Nasdaq E-mini futures) historical data

- **Methodology**: Frequency analysis of outcomes following specific setup conditions

- **Time Period**: Multiple market cycles including various volatility regimes

**Critical Warning**: These probabilities are specific to NQ and reflect that instrument's behavior patterns. Market microstructure, participant behavior, and volatility characteristics differ significantly across instruments. Do not apply these NQ-derived probabilities to other markets (ES, RTY, YM, individual stocks, forex, commodities, etc.).

## Best Practices

1. **Combine with Other Analysis**: Use this indicator as one component of a complete trading methodology, not a standalone system

2. **Respect Risk Management**: Probabilities are not certainties; always use proper position sizing and stop losses

3. **Context Matters**: High-impact news events, holiday trading, and extreme volatility can invalidate typical patterns

4. **Verify Statistics**: Monitor your own results and compare to the displayed probabilities

5. **Adapt Session Times**: If trading instruments with different active hours, adjust session times accordingly

6. **Regular Calibration**: Periodically review if the session averages and probabilities remain relevant to current market conditions

## Understanding Originality

This indicator is original in its approach to combining three analytical frameworks into a single tool:

1. **Dynamic ADR Projection**: Unlike static pivot points, these levels adapt daily based on recent volatility

2. **Session-Specific Statistics**: Goes beyond simple volume profiles by quantifying average ranges for specific time windows across weekdays

3. **Conditional Probability Display**: Automatically detects overnight session relationships and displays relevant probability data rather than showing all scenarios simultaneously

The conditional logic system that determines which probability set to display is a key differentiator—traders only see the statistics relevant to the current market setup, reducing information overload and improving decision-making clarity.

## Summary

The **Statistical Daily Profile & Ranges** indicator provides traders with a comprehensive framework for understanding daily range potential, session-specific behavior patterns, and probability-based setup analysis. By combining ADR projection levels with detailed session statistics and dynamic probability displays, traders gain multiple perspectives on potential price movement within the trading day.

The indicator is most effective when used to:

- Set realistic profit targets based on average daily range

- Identify which sessions typically produce movement on specific weekdays

- Understand probability-weighted outcomes for different overnight setup conditions (NQ only)

- Visualize session ranges and compare them to historical averages

Remember that all statistical analysis reflects historical patterns, and market behavior can change. Always combine indicator signals with sound risk management, proper position sizing, and your own market analysis.

Session Open Range, Breakout & Trap Framework - TrendPredator OBSession Open Range, Breakout & Trap Framework — TrendPredator Open Box

Stacey Burke’s trading approach combines concepts from George Douglas Taylor, Tony Crabel, Steve Mauro, and Robert Schabacker. His framework focuses on reading price behaviour across daily templates and identifying how markets move through recurring cycles of expansion, contraction, and reversal. While effective, much of this analysis requires real-time interpretation of session-based behaviour, which can be demanding for traders working on lower intraday timeframes.

The TrendPredator indicators formalize parts of this methodology by introducing mechanical rules for multi-timeframe bias tracking and session structure analysis. They aim to present the key elements of the system—bias, breakouts, fakeouts, and range behaviour—in a consistent and objective way that reduces discretionary interpretation.

The Open Box indicator focuses specifically on the opening behaviour of major trading sessions. It builds on principles found in classical Open Range Breakout (ORB) techniques described by Tony Crabel, where a defined time window around the session open forms a structural reference range. Price behaviour relative to this range—breaking out, failing back inside, or expanding—can highlight developing session bias, potential trap formation, and directional conviction.

This indicator applies these concepts throughout the major equity sessions. It automatically maps the session’s initial range (“Open Box”) and tracks how price interacts with it as liquidity and volatility increase. It also incorporates related structural references such as:

* the first-hour high and low of the futures session

* the exact session open level

* an anchored VWAP starting at the session open

* automated expansion levels projected from the Open Box

In combination, these components provide a unified view of early session activity, including breakout attempts, fakeouts, VWAP reactions, and liquidity targeting. The Open Box offers a structured lens for observing how price transitions through the major sessions (Asia → London → New York) and how these behaviours relate to higher-timeframe bias defined in the broader TrendPredator framework.

Core Features

Open Box (Session Structure)

The indicator defines an initial session range beginning at the selected session open. This “Open Box” represents a fixed time window—commonly the first 30 minutes, or any user-defined duration—that serves as a structural reference for analysing early session behaviour.

The range highlights whether price remains inside the box, breaks out, or rejects the boundaries, providing a consistent foundation for interpreting early directional tendencies and recognising breakout, continuation, or fakeout characteristics.

How it works:

* At the session open, the indicator calculates the high and low over the specified time window.

* This range is plotted as the initial structure of the session.

* Price behaviour at the boundaries can illustrate emerging bias or potential trap formation.

* An optional secondary range (e.g., 15-minute high/low) can be enabled to capture early volatility with additional precision.

Inputs / Options:

* Session specifications (Tokyo, London, New York)

* Open Box start and end times (e.g., equity open + first 30 minutes, or any custom length)

* Open Box colour and label settings

* Formatting options for Open Box high and low lines

* Optional secondary range per session (e.g., 15-minute high/low)

* Forward extension of Open Box high/low lines

* Number of historic Open Boxes to display

Session VWAPs

The indicator plots VWAPs for each major trading session—Asia, London, and New York—anchored to their respective session opens. These session-specific VWAPs assist in tracking how value develops through the day and how price interacts with session-based volume distributions.

How it works:

* At each session open, a VWAP is anchored to the open price.

* The VWAP updates throughout the session as new volume and price data arrive.

* Deviations above or below the VWAP may indicate balance, imbalance, or directional control.

* Viewed together, session VWAPs help identify transitions in value across sessions.

Inputs / Options:

* Enable or disable VWAP per session

* Adjustable anchor and end times (optionally to end of day)

* Line styling and label settings

* Number of historic VWAPs to draw

First Hour High/Low Extensions

The indicator marks the high and low formed during the first hour of each session. These reference points often function as early control levels and provide context for assessing whether the session is establishing bias, consolidating, or exhibiting reversal behaviour.

How it works:

* After the session starts, the indicator records the highest and lowest prices during the first hour.

* These levels are plotted and extended across the session.

* They provide a visual reference for observing reactions, targets, or rejection zones.

Inputs / Options:

* Enable or disable for each session

* Line style, colour, and label visibility

* Number of historic sessions displayed

EQO Levels (Equity Open)

The indicator plots the opening price of each configured session. These “Equity Open” levels represent short-term reference points that can attract price early in the session.

Once the level is revisited after the Open Box has formed, it is automatically cut to avoid clutter. If not revisited, the line remains as an untested reference, similar to a naked point of control.

How it works:

* At session open, the open price is recorded.

* The level is plotted as a local reference.

* If price interacts with the level after the Open Box completes, the line is cut.

* Untested EQOs extend forward until interacted with.

Inputs / Options:

* Enable/disable per session

* Line style and label settings

* Optional extension into the next day

* Option for cutting vs. hiding on revisit

* Number of historic sessions displayed

OB Range Expansions (Automatic)

Range expansions are calculated from the height of the Open Box. These levels provide structured reference zones for identifying potential continuation or exhaustion areas within a session.

How it works:

* After the Open Box is formed, multiples of the range (e.g., 1×, 2×, 3×) are projected.

* These expansion levels are plotted above and below the range.

* Price reactions near these areas can illustrate continuation, hesitation, or potential reversal.

Inputs / Options:

* Enable or disable per session

* Select number of multiples

* Line style, colour, and label settings

* Extension length into the session

Stacey Burke 12-Candle Window Marker

The indicator can highlight the 12-candle window often referenced in Stacey Burke’s session methodology. This window represents the key active period of each session where breakout attempts, volatility shifts, and reversal signatures often occur.

How it works:

* A configurable window (default 12 candles) is highlighted from each session open.

* This window acts as a guide for observing active session behaviour.

* It remains visible throughout the session for structural context.

Inputs / Options:

* Enable/disable per session

* Configurable window duration (default: 3 hours)

* Colour and transparency controls

Concept and Integration

The Open Box is built around the same multi-timeframe logic that underpins the broader TrendPredator framework.

While higher-timeframe tools track bias and setups across the H8–D–W–M levels, the Open Box focuses on the H1–M30 domain to define session structure and observe how early intraday behaviour aligns with higher-timeframe conditions.

The indicator integrates with the TrendPredator FO (Breakout, Fakeout & Trend Switch Detector), which highlights microstructure signals on lower timeframes (M15/M5). Together they form a layered workflow:

* Higher timeframes: context, bias, and developing setups

* TrendPredator OB: intraday and intra-session structure

* TrendPredator FO: microstructure confirmation (e.g., FOL/FOH, switches)

This alignment provides a structured way to observe how daily directional context interacts with intraday behaviour.

See the public open source indicator TP FO here (click on it for access):

Practical Application

Before Session Open

* Review previous session Open Box, Open level, and VWAPs

* Assess how higher-timeframe bias aligns with potential intraday continuation or reversal

* Note untested EQO levels or VWAPs that may function as liquidity attractors

During Session Open

* Observe behaviour around the first-hour high/low and higher-timeframe reference levels

* Monitor how the M15 and 30-minute ranges close

* Track reactions relative to the session open level and the session VWAP

After the Open Box completes

* Assess price interaction with Open Box boundaries and first-hour levels

* Use microstructure signals (e.g., FOH/FOL, switches) for potential confirmation

* Refer to expansion levels as reference zones for management or target setting

After Session

* Review how price behaved relative to the Open Box, EQO levels, VWAPs, and expansion zones

* Analyse breakout attempts, fakeouts, and whether intraday structure aligned with the broader daily move

Example Workflow and Trade

1. Higher-timeframe analysis signals a Daily Fakeout Low Continuation (bullish context).

2. The New York session forms an Open Box; price breaks above and holds above the first-hour high.

3. A Fakeout Low + Switch Bar appears on M5 (via FO), after retesting the session VWAP triggering the entry.

4. 1x expansion level serves as reference targets for take profit.

Relation to the TrendPredator Ecosystem

The Open Box is part of the TrendPredator Indicator Family, designed to apply multi-timeframe logic consistently across:

* higher-timeframe context and setups

* intraday and session structure (OB)

* microstructure confirmation (FO)

Together, these modules offer a unified structure for analysing how daily and intraday cycles interact.

Disclaimer

This indicator is for educational purposes only and does not guarantee profits.

It does not provide buy or sell signals but highlights structural and behavioural areas for analysis.

Users are solely responsible for their trading decisions and outcomes.

TPO[Fixed Range, Anchored, Bars Back]TPO Bars Back, Fixed Range and Anchored

Overview

The TPO Profile (Time Price Opportunity Profile) is a powerful market profile indicator that displays the amount of time price spent at different levels during a specified period. Unlike traditional volume profile indicators that show volume distribution, TPO Profile shows time distribution , providing insights into where price has spent the most time and identifying key support and resistance levels.

Key Advantages Over TradingView's Built-in TPO

Simplified Composite Creation : Automatically creates TPO profiles for any time range without manual split/merge operations

Instant Value Area Calculation : Immediately shows Value Area, POC, VAH, and VAL for your selected period

No Manual Assembly Required : TradingView's native TPO requires you to manually split sessions and merge them to create composites - this indicator does it automatically

Flexible Time Ranges : Create composites for any custom time period (multiple days, weeks, specific events) with a few clicks

Real-time Composite Updates : Anchor mode creates live composites that update as new data arrives

Multiple Composite Analysis : Easily compare different time periods without the tedious manual process

Key Features

Core Functionality

Time-Based Analysis : Shows time spent at each price level rather than volume

Configurable Time Blocks : Use any timeframe for TPO counting (30min, 1H, 4H, etc.)

Multiple Price Levels : Adjustable from 5 to 200 levels for granular analysis

Point of Control (POC) : Automatically identifies the price level with highest time activity

Value Area Calculation : Shows the price range containing 70% (configurable) of time activity

Automatic Composite Generation : Creates multi-session composites without manual intervention

Three Operating Modes

1. Bars Back Mode

Analyzes the last N bars from the current bar

Perfect for recent market activity analysis

Range: 10-500 bars

Use Case : Intraday analysis, recent session review

2. Fixed Range Mode

Analyzes a specific time period between start and end times

Ideal for historical analysis of specific events

Creates perfect composites for multi-day periods

Use Case : Earnings periods, news events, specific trading sessions, weekly/monthly composites

3. Anchor Mode (NEW)

Starts from a specific time and extends to the current bar

Dynamically updates as new bars form

Perfect for building live composites from any starting point

Use Case : Live session monitoring, event-based analysis from a specific point, growing composites

Visual Elements

TPO Bars

Horizontal bars showing time distribution at each price level

Longer bars = more time spent at that level

Color-coded to distinguish Value Area from outlying levels

Point of Control (POC)

Red line marking the price level with highest time activity

Most significant support/resistance level

Configurable line style (Solid/Dashed/Dotted) and width

Value Area High/Low (VAH/VAL)

Green and Orange lines marking the boundaries of the Value Area

Shows the price range containing the specified percentage of time activity

Optional display with customizable line styles

Single Print Detection

Identifies price levels touched by only one time block

Display options: Lines or Boxes

Purple color highlighting these significant levels

Often act as strong support/resistance in future trading

Customization Options

Time Block Configuration

Block Time : Choose timeframe for TPO counting (30min, 1H, 4H, etc.)

Allows analysis at different time granularities

Higher timeframes = broader perspective, Lower timeframes = finer detail

Visual Styling

Line Styles : Solid, Dashed, or Dotted for all line elements

Line Widths : 1-5 pixels for POC, VAH, and VAL lines

Colors : Fully customizable colors for all elements

Transparency : Adjustable transparency for better chart readability

Label Management

Show/Hide Labels : Toggle POC, VAH, VAL labels

Font Sizes : Tiny, Small, Normal, Large, Huge

Label Positioning : 8 different position options relative to lines

Offset Controls : Fine-tune label positioning

Line Extension

Level Offset Right : Controls how far lines extend

Smart extension logic:

Value ≤ 0: Infinite extension (extend.right)

Value ≥ 1: Extends exactly N bars ahead

Trading Applications

Support & Resistance

POC often acts as strong support/resistance

Value Area boundaries provide key levels

Single prints frequently become significant levels

Market Structure Analysis

Identify areas of price acceptance (thick TPO bars)

Spot areas of price rejection (thin TPO bars)

Understand where market participants are comfortable trading

Composite Profile Analysis

Create multi-day, weekly, or monthly composites instantly

Compare different composite periods without manual work

Analyze longer-term price acceptance levels

Build composites around specific events or announcements

Session Analysis

Monitor intraday session development in real-time

Compare different sessions (London, New York, Asia)

Track how profiles change throughout the trading day

Build live composites across multiple sessions

Event Analysis

Use Fixed Range mode for earnings, news events

Use Anchor mode to track price development from specific events

Compare pre/post event price acceptance levels

Create event-based composites automatically

Input Parameters

Mode Selection

Mode : Bars Back | Fixed Range | Anchor

Bars Back : Number of bars to analyze (10-500)

Start Time : Beginning time for Fixed Range and Anchor modes

End Time : Ending time for Fixed Range mode only

Analysis Configuration

Block Time : Timeframe for TPO blocks (e.g., "30" for 30-minute blocks)

TPO Levels : Number of price levels (5-200)

Value Area % : Percentage for Value Area calculation (50-95%)

Display Options

Show POC : Display Point of Control line

Show Value Area : Display Value Area box

Show VAH/VAL Lines : Display Value Area boundary lines

Show Single Prints : Display single print detection

Single Print Style : Lines or Boxes

Styling Controls

Colors : TPO, POC, Value Area, VAH, VAL, Single Print colors

Line Styles : POC, VAH, VAL line styles

Line Widths : POC, VAH, VAL line widths

Labels : Show/hide, font size, position, offset controls

Technical Details

Calculation Method

Divides the price range into equal levels based on TPO Levels setting

For each time block, determines which price levels it crosses

Adds +1 count to each crossed level

Identifies POC as the level with highest count

Calculates Value Area by expanding from POC until target percentage is reached

Performance Considerations

Historical data limited to prevent buffer overflow errors

Smart bounds checking for different timeframes

Optimized cleanup routines to prevent drawing object accumulation

Pine Script Version

Built on Pine Script v6

Uses modern Pine Script best practices

Efficient array handling and drawing object management

Best Practices

Timeframe Selection

Block Time = Chart Timeframe : Traditional TPO approach

Block Time > Chart Timeframe : Smoother, broader perspective

Block Time < Chart Timeframe : More granular, detailed analysis

Level Count Guidelines

Low levels (10-20) : Better for swing trading, major levels

High levels (50-100) : Better for scalping, precise entries

Very high levels (100+) : For very detailed analysis

Mode Selection

Bars Back : Daily analysis, recent activity

Fixed Range : Historical events, specific periods, manual composites

Anchor : Live monitoring, event-based analysis, growing composites

Composite Creation Workflow

Select Fixed Range or Anchor mode

Set your desired start time (and end time for Fixed Range)

Adjust TPO Levels for desired granularity

Enable VAH/VAL lines to see Value Area boundaries

The composite profile generates automatically with all key levels

This indicator eliminates the tedious manual process of creating composite TPO profiles in TradingView. Instead of splitting sessions and manually merging them, you get instant composite analysis with automatic Value Area calculation, POC identification, and single print detection. The combination of time-based analysis, multiple operating modes, and extensive customization options makes it a powerful tool for understanding market structure and price acceptance levels across any time period.

Consolidation Range [BigBeluga]A hybrid volatility-volume indicator that isolates periods of price equilibrium and reveals the directional force behind each range buildup.

Consolidation Range is a powerful tool designed to detect compression phases in the market using volatility thresholds while visualizing volume imbalance within those phases. By combining low-volatility detection with directional volume delta, it highlights where accumulation or distribution is occurring—giving traders the confidence to act when breakouts follow. This indicator is particularly valuable in choppy or sideways markets where range identification and sentiment context are key.

🔵 CONCEPTS

Volatility Compression: Uses ADX (Average Directional Index) to detect periods of low trend strength—specifically when ADX drops below a configurable threshold.

Range Structure: Upon a low-volatility trigger, the script dynamically anchors horizontal upper and lower bounds based on local highs and lows.

Directional Volume Delta: Inside each active range, it calculates the net difference between buy and sell volume, showing who controlled the range.

Sentiment Bias: A label appears in the center of the zone on breakout, showing the accumulated delta and bias direction (▲ for positive, ▼ for negative).

Range Validity Filter: Only ranges with more than 15 bars are considered valid—short-lived consolidations are auto-filtered.

🔵 KEY FEATURES

Detects low volatility market phases using ADX logic (crosses under "Volatility Threshold Input").

Automatically plots adaptive consolidation zones with upper and lower boundary lines.

Includes dynamic midline to visualize the price average inside the range.

Visual range is filled with a progressive gradient to reflect distance between highs and lows.

When the range is active, the indicator accumulates volume delta (Buy - Sell volume) .

Upon breakout, the total volume delta is displayed at the midpoint , providing insight into market sentiment during the consolidation phase.

Filters out weak or short-lived consolidations under 15 bars.

🔵 HOW TO USE

Spot ranging or compression zones with minimal effort.

Use breakouts with volume delta bias to assess the strength or weakness of moves.

Combine with trend-following tools or volume-based confirmation for stronger setups.

Apply to higher timeframes for macro consolidation tracking .

🔵 CONCLUSION

Consolidation Range now brings together volatility filtering and directional volume delta into one smart module. This hybrid logic allows traders to not only identify balance zones but also understand who was in control during the buildup—offering a sharper edge for breakout and trend continuation strategies.

RTH Session Range Position (0-100) with EMAA Pine Script indicator designed to help traders understand where the current price is located within the Regular Trading Hours (RTH) session range, from 0 (session low) to 100 (session high). It also plots a smoothed EMA of this position to provide insight into momentum or trend during the RTH session.

What the Indicator Does

Defines RTH (Regular Trading Hours):

Start: 9:30 AM

End: 4:00 PM

These are typical US equity market hours.

Tracks the session's high and low during RTH:

sessionHigh and sessionLow update only during RTH.

Calculates position of the current price within the RTH range:

Formula: ((close - sessionLow) / (sessionHigh - sessionLow)) * 100

Result is a percentage:

0 = at session low

100 = at session high

50 = middle of session range

Calculates an EMA of that position (posEMA):

Smooths out the raw position to help visualize momentum within the range.

Plots and table:

Plots pos and posEMA on a separate chart pane.

Adds horizontal lines at key levels (0, 30, 50, 70, 100).

Table shows current values for Position, EMA, and Range.

Visual cues:

bgcolor highlights when pos crosses over or under the EMA — potential momentum shifts.

Alerts:

Cross above/below 50 (session midpoint).

Cross above/below EMA.

How to Use It Effectively

1. Session Strength & Momentum

Position above 70: Price is near session highs — strong upward momentum.

Position below 30: Price is near session lows — strong downward momentum.

Use the EMA of position to filter out noise and identify trends.

2. Breakout or Reversal Detection

Cross above EMA: Momentum may be turning bullish.

Cross below EMA: Momentum may be turning bearish.

These crosses (especially near mid-levels like 50) can hint at session trend shifts.

3. Range Context for Entries

If you're a mean-reversion trader, look for:

Price > 70 + turning down below EMA → possible short.

Price < 30 + turning up above EMA → possible long.

For breakout traders, you might wait for:

Crosses above 70 with EMA support.

Crosses below 30 with EMA resistance.

4. Confirmation Tool

Use this indicator alongside others to confirm:

Whether price action has strength within the day.

Whether breakouts have real momentum or are extended already.

Balanced Price Range | Flux Charts💎 GENERAL OVERVIEW

Introducing our new Balanced Price Range (BPR) indicator! A Balanced Price Range is a trading concept used by price action traders. It is detected by finding overlapping area between two contrary Fair Value Gaps (FVGs). These areas can be used as entry points during market pullbacks. For more information about the process, please check the "HOW DOES IT WORK ?" section.

Balanced Price Range Features :

Balanced Price Range Detection : Identifies areas where bullish and bearish FVGs overlap, suggesting a zone of price equilibrium.

Customizable FVG & BPR Detection : You can fine-tune FVG detection and sensitivity for BPR detection to your liking.

Retest Labels : Bullish & Bearish retest labels will be rendered for BPRs.

Alerts : You can set alerts for Bullish & Bearish BPR detection and their retests.

🚩 UNIQUENESS

This indicator doesn't just detect standard FVGs but specifically looks for areas where bullish and bearish IFVGs (Invalidated Fair Value Gaps) overlap, defining a Balanced Price Range. It also actively manages and updates identified BPR zones, removing them when they are invalidated or remain untouched for a specified period. It highlights and alerts users to retests of established BPR zones, signaling potential trading opportunities. Users can tailor the appearance of the BPR zones and retest markers, as well as configure specific alerts for new BPR formations and retests.

📌 HOW DOES IT WORK ?

A Fair Value Gap generally occur when there is an imbalance in the market. They can be detected by specific formations within the chart. The indicator first detects bullish & bearish FVG zones according to their formations on chart. Then, they are dynamically tracked and flagged as invalidated if the price crosses them, turning them into IFVGs. When a FVG & IFVG of the same type overlaps, the indicator combines them into a single BPR of corresponding type. The detected BPR is updated as new data comes in, and renders retests labels as they occur. A bullish BPR can be used to find long trade entry opportunities, while a bearish BPR can be used to find short trade entry opportunities. Retests can also indicate potential movements in the corresponding direction of the BPR. Users can set-up alerts for BPR detection & BPR retests and will get notified as they occur.

⚙️ SETTINGS

Show Historic Zones: If enabled, invalidated or expired BPR zones will remain visible on the chart.

Balanced Price Range:

FVG Detection Method: Determines the criteria for the bar types forming the initial FVG.

Same: All three bars forming the FVG must be of the same type (all bullish or all bearish).

Mixed: The bar types must vary (a mix of bullish and bearish bars).

All: Bar types can vary or be the same.

FVG Invalidation Method: Determines which part of the candle (wick or close) invalidates the initial FVG.

BPR Invalidation Method: Determines which part of the candle (wick or close) invalidates the Balanced Price Range.

Sensitivity: Adjusts the sensitivity of FVG detection. Higher values may identify fewer, larger BPRs, while lower values may detect more, smaller BPRs.

Labels: Toggles the display of text labels on the identified zones.

Retests: Enables or disables the detection and visualization of BPR retests.

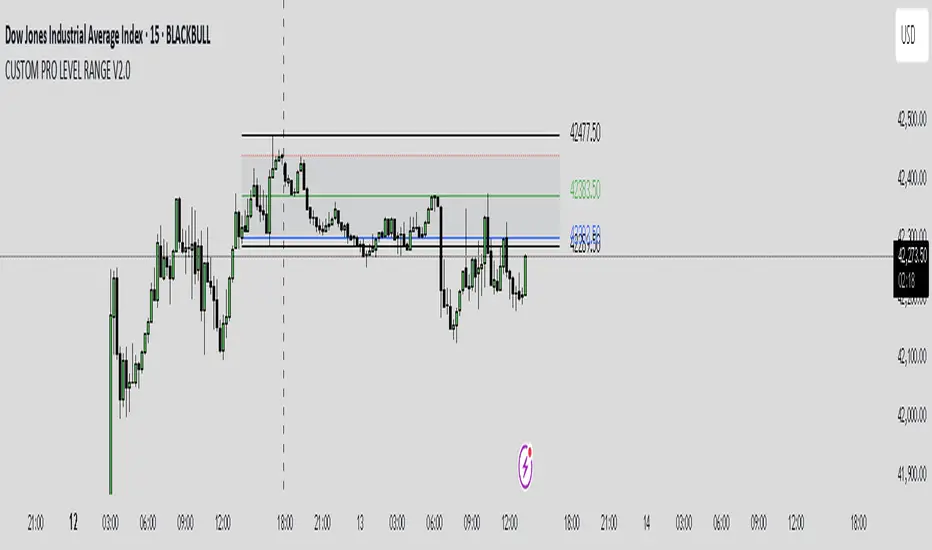

CUSTOM PRO RANGE V2.0 with AlertsCore Functions

Tracks High/Low Ranges

Daily (DR) or Initial (IDR) ranges within custom time windows (e.g., 9:30 AM–4:00 PM).

Optional extended hours (e.g., overnight).

Visual Tools

Draws boxes/lines for range boundaries, midpoints, and opening prices.

Custom colors/styles for clarity.

Smart Alerts

Notifies when price breaks high/low/mid of the range.

Avoids spam with once-per-bar alerts.

Flexible Timeframes

Works for intraday, daily, or even quarterly ranges with minor tweaks.

🎯 Who It Helps

Day Traders: Spot breakouts/reversals.

Swing Traders: Identify key support/resistance.

Analysts: Study price behavior in specific sessions.

Trading Sessions [BigBeluga]

This indicator brings Smart Money Concept (ICT) session logic to life by plotting key global trading sessions with volume and delta analytics. It not only highlights session ranges but also tracks their midpoints — which often act as intraday support/resistance levels.

🔵 KEY FEATURES

Visual session boxes: Plots boxes for Tokyo, London, New York, and Sydney sessions based on user-defined UTC+0 time ranges.

Volume & delta metrics: Displays total volume and delta volume (buy–sell difference) within each session.

Mid, High & Low Range Extension: Once a session ends, the high, low, and midpoint levels automatically extend — ideal for detecting SR zones.

Session labels: Each box includes a label with session name, time, volume, and delta for quick reference.

Custom session control: Enable or disable sessions individually and configure start/end times.

Clean aesthetics: Transparent shaded boxes with subtle borders make it easy to overlay without clutter.

Sessions Dashboard: Shows the time range of each session and tells you whether the session is currently active.

🔵 USAGE

Enable the sessions you want to monitor (e.g., New York or Tokyo) from the settings.

Use session volume and delta values to gauge the strength and direction of institutional activity.

Watch for price interaction with the extended range — it often acts as dynamic support/resistance after the session ends.

Overlay it with liquidity tools or breaker blocks for intraday strategy alignment.

🔵 EXAMPLES

Extended Future Range acted as resistance/support.

Delta value helped confirm bullish pressure during New York open.

Multiple sessions helped identify kill zone overlaps and high-volume turns.

Trading Sessions is more than just a visual scheduler — it's a precision tool for traders who align with session-based volume dynamics and ICT methodology. Use it to define high-probability zones, confirm volume shifts, and read deeper into the true intent behind market structure.

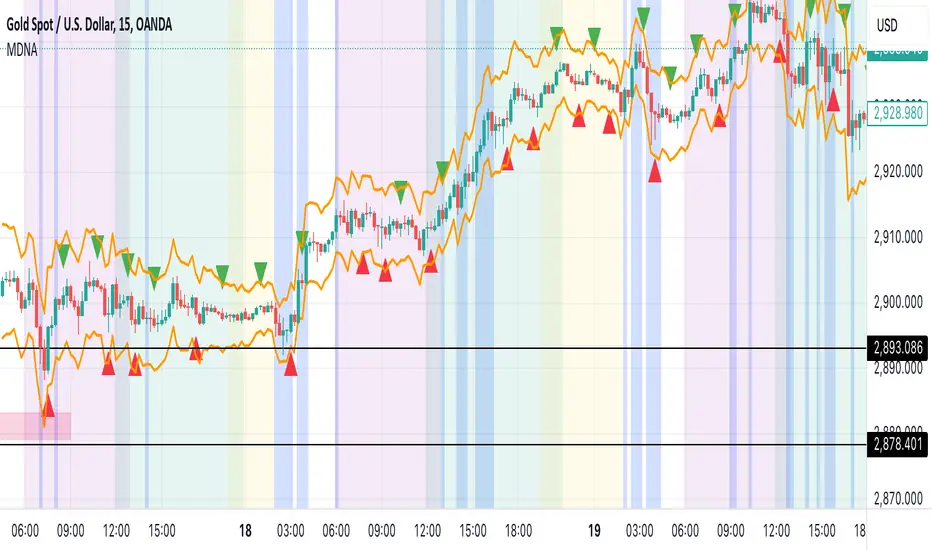

Market DNA: Structure, Volume, Range, and SessionsMarket DNA: Structure, Volume, Range, and Sessions**

The Market DNA indicator combines market structure, volume analysis, trading ranges, and global trading sessions into a single, comprehensive tool for traders. It helps identify key price levels, volume patterns, consolidation phases, and active market periods, enabling informed trading decisions.

Market Structure Detects swing highs and lows using `ta.pivothigh` and `ta.pivotlow`, plotting them as red/green triangles to highlight support/resistance and trend reversals.

- Fractal Volume Zones (FVG): Highlights areas of significant buying/selling pressure by comparing current volume to an average over a lookback period; high-volume zones are marked with a semi-transparent blue background.

- Trading Range: Defines a price channel using the Average True Range (ATR) and a multiplier, creating upper/lower bands to identify consolidation, breakouts, and potential trade levels.

- Market Sessions: Highlights major global trading sessions (Asia, Europe, US) with colored backgrounds (purple, teal, yellow) to indicate liquidity and volatility shifts.

How It Works

- Swing points help analyze trends and reversals.

- FVG confirms price movements with high volume for stronger signals.

- Trading range bands assist in identifying breakout opportunities and setting stops/take-profits.

- Session highlights allow traders to adapt strategies based on regional activity.

Customization

- Adjust `swing_length` for sensitivity in detecting turning points.

- Modify `volume_lookback` to control volume averaging.

- Tune `range_multiplier` for wider/narrower trading bands.

- Enable/disable session highlighting via `session_highlight`.

Use Cases

- Identify trends and key levels using swing points and FVG.

- Spot breakout opportunities with trading range bands.

- Adapt strategies to regional trading sessions for optimal timing.

This all-in-one indicator provides a clear, customizable view of the market, empowering traders to make data-driven decisions across asset classes and timeframes.

Peak Reaction Zones [BigBeluga]Peak Reaction Zones is an advanced Smart Money Concept (SMC) indicator that identifies the most recent swing high and swing low zones, helping traders determine premium and discount areas for optimal trade positioning.

🔵 Key Features:

Swing High & Low Zones:

Automatically detects the latest swing high and swing low levels.

Helps traders identify key reaction points where price is likely to respond.

Premium & Discount Concept:

The high zone represents a premium area, where price is overextended and may reverse.

The low zone represents a discount area, where price is undervalued and may bounce.

The midline dynamically marks the equilibrium of the range.

Adjustable Zone Width:

Users can fine-tune the width of the zones to match their trading style.

Wider zones capture broader reaction ranges, while narrower zones focus on precise levels.

Zone Retest Signals:

Blue markers appear when price retests the lower reaction zone, signaling potential support.

Orange markers appear when price retests the upper reaction zone, indicating possible resistance.

Price Labels for Key Levels:

Displays the price value of the swing high, swing low, and midline for quick reference.

Helps traders recognize major reaction points at a glance.

🔵 Usage:

Smart Money Trading: Utilize the premium and discount concept to align trades with institutional order flow.

Zone Reactions: Watch for price tests of reaction zones and use the retest signals to confirm potential reversals.

Midline Confirmation: If price holds above or below the midline, it can indicate directional bias.

Scalping & Swing Trading: Short-term traders can look for zone rejections, while swing traders can use the levels for trend continuation setups.

Peak Reaction Zones is a must-have tool for traders looking to trade with Smart Money Concepts, allowing for precise entries and exits based on key liquidity areas and market structure.

Alans Date Range CalculatorOverview

Setting a date range for backtesting enables you to evaluate your trading strategy under various market conditions. Traders can test a strategy’s performance during specific periods, such as economic downturns, bull markets, or periods of high volatility. This helps assess the trading strategy’s robustness and adaptability across different scenarios.

Specifying years of data instead of just inputting specific start and end dates offers several advantages:

1. **Consistency**: Using a fixed number of years ensures that the testing period is consistent across different strategies or iterations. This makes it easier to compare performance metrics and draw meaningful conclusions.

2. **Flexibility**: Specifying years allows for automatic adjustment of the start date based on the current date or selected end date. This is particularly useful when new data becomes available or when testing on different assets with varying historical data lengths.

3. **Efficiency**: It simplifies updating and retesting strategies. Instead of recalculating specific start dates each time, traders can quickly adjust the number of years to process, making it easier to test strategies over different timeframes.

4. **Comprehensive Analysis**: Broader timeframes defined by years help you evaluate how your strategy performs over multiple market cycles, providing insights into long-term viability and potential weaknesses.

Defining a date range by specifying years allows for more thorough and systematic backtesting, helping traders develop more reliable and effective trading systems.

Alan's Date Range Calculator: A TradingView Pine Script Indicator

Purpose

This Pine Script indicator calculates and displays a date range for backtesting trading strategies. It allows users to specify the number of years to analyze and an end date, then calculates the corresponding start date. Most importantly, users can copy the inputs and function into their own strategies to quickly add a time span feature for backtesting.

Key Features

User-defined input for the number of years to analyze

Customizable end date with a calendar input

Automatic calculation of the start date

Visual display of both start and end dates on the chart

How It Works

User Inputs

Years of Data to Process: An integer input allowing users to specify the number of years for analysis (default: 20, range: 1-100)

End Date: A calendar input for selecting the end date of the analysis period (default: December 31, 2024)

Date Calculation

The script uses a custom function calcStartDate() to determine the start date. It subtracts the specified number of years from the end date's year and sets the start date to January 1st of that year.

Visual Output

The indicator displays two labels on the chart:

Start Date Label: Shows the calculated start date

End Date Label: Displays the user-specified end date

Both labels are positioned horizontally at the bottom of the chart, with the end date label to the right of the start date label.

Applications

This indicator is particularly useful for traders who want to:

Define specific date ranges for backtesting strategies

Quickly visualize the time span of their analysis

Ensure consistent testing periods across different strategies or assets

Customization

Users can easily adjust the analysis period by changing the number of years or selecting a different end date. This flexibility allows for testing strategies across various market conditions and time frames.

Time Range### Indicator Name: **Time Range**

#### Description:

The **Time Range** indicator allows users to highlight specific time ranges on a chart for each day of the week. It uses customizable time inputs for every day (Monday to Sunday), allowing the user to define trading sessions or any time-based range. These sessions are visualized by shading the background of the chart within the defined periods.

#### Key Features:

- **Custom Sessions**: For each day of the week (Monday to Sunday), the user can define a unique time session by specifying the start time using the input fields.

- **Day-wise Session Activation**: The user can toggle the activation of sessions for each day by using checkboxes. If the session for a particular day is disabled, no background shading will appear for that day.

- **Background Highlighting**: When a session is active, the background of the chart during the specified session period will be shaded in gray with a 70% transparency. This helps the user visually identify active time ranges across multiple days.

#### Use Cases:

- **Highlighting Trading Sessions**: Traders can use this indicator to easily visualize specific market sessions such as the New York or London trading sessions.

- **Visualizing Custom Time Blocks**: Can be used to highlight any custom time blocks that are important for the trader, such as key trading hours, news release periods, or other time-based strategies.

#### Customizable Parameters:

- **Day Toggles**: Checkboxes to activate or deactivate sessions for each day of the week.

- **Time Range Inputs**: Time range inputs allow the user to set start times for each session, which are applied based on the user's selection for the day.

This indicator helps streamline chart analysis by giving clear visual markers for time-based events or trading windows.

ATR Gerchik LightAverage True Range ( ATR ) is a technical analysis indicator that measures volatility in the market. ATR is a moving average of the true range over a period of time.

ATR calculation procedure:

1. Determine the true maximum - this is the highest of the current maximum and yesterday's closing price of the day.

2. Determine the true minimum - this is the smallest of the current minimum and yesterday's closing price.

3. Determine the true range - this is the distance between the true maximum and minimum.

4. We exclude extremely large candles (> x2 ATR) and extremely small ones (< 0.5 ATR) from the obtained true ranges.

5. We calculate the average for the selected period based on the remaining range.

6. We calculate the percentage of the current True Range relative to the average ATR value for the previous period.

Description:

If you analyze it yourself, you will see that 75-80% of the time, the instrument moves only 1 ATR per day. You must understand that if an instrument has, for example, moved 80% of its daily range, it is not advisable to purchase it. This is comparable to a car's fuel tank: if the tank is almost empty, the car won't go far. Most indicators that calculate ATR include anomalous candles, which give unreliable results and lead to incorrect decisions. Because of this, many traders prefer to calculate ATR on their own.

However, the Gerchik ATR indicator accounts for anomalous candles and filters out extremely large candles (> 2x ATR) and extremely small ones (< 0.5x ATR). Additionally, this indicator immediately shows the consumed “fuel” of the instrument as a percentage, so you don't have to calculate the distance traveled yourself. This allows you to make quick, informed decisions. If we see that the tank is almost empty, it is logical not to get into that car today. When building any strategy, you must rely on the average movement.

Key Features:

Anomalous Candle Filtering: Excludes extremely large and small candles to provide more reliable ATR values.

Consumed Fuel Indicator: Shows the percentage of the ATR consumed, helping traders quickly assess the remaining potential movement.

Daily Timeframe Focus: Designed specifically for use on daily charts for accurate long-term analysis.

Practical Applications:

Entry and Exit Points: Use the ATR to determine optimal entry and exit points by assessing market volatility and potential price movement.

Stop-Loss Placement: Calculate stop-loss levels based on ATR to ensure they are placed at appropriate distances, accounting for current market volatility.

Trend Confirmation: Use the percentage of ATR consumed to confirm the strength of a trend and decide whether to enter or exit trades.

Examples of Use:

Trend Following: During strong trends, ATR helps identify periods of increased volatility, signaling potential breakouts or reversals.

Range Trading: In ranging markets, ATR can highlight periods of low volatility, indicating consolidation and potential breakout zones.

Note: The indicator is displayed and works only on the daily timeframe!

The indicator was created according to the instructions, description of the functionality, and strategy of Mr. Gerchik. Thank you so much, Chief!

________________________

Average True Range ( ATR , средний истинный диапазон) – это индикатор технического анализа, который измеряет волатильность на рынке. ATR представляет собой скользящее среднее истинного диапазона за определенный период времени.

Порядок расчета ATR:

1. Определяем истинный максимум – это наивысшее из текущего максимума и вчерашней цены закрытия дня.

2. Определяем истинный минимум – это наименьшее из текущего минимума и вчерашней цены закрытия.

3. Определяем истинный диапазон – это расстояние между истинным максимумом и минимумом.

4. Исключаем из полученных истинных диапазонов экстремально большие свечи (> x2 ATR) и экстремально маленькие (< 0.5 ATR).

5. Рассчитываем среднее за выбранный период исходя из оставшегося диапазона.

6 . Рассчитываем процент текущего истинного диапазона (True Range) относительно среднего значения ATR за предыдущий период.

Описание:

Если вы сами проанализируете, то увидите, что 75-80% времени инструмент ходит только 1 ATR. И вы должны понимать, что если инструмент внутри дня прошел, к примеру, 80% своего движения, то этот инструмент больше нельзя покупать. Это можно сравнить с баком машины: если бак почти пустой, машина далеко не уедет. Большинство индикаторов, которые рассчитывают ATR, производят расчет с паранормальными свечами. Это дает недостоверный результат и приводит к неверным решениям. Многие трейдеры из-за этого не используют готовые индикаторы и предпочитают считать ATR самостоятельно. Но индикатор ATR Gerchik учитывает паранормальные свечи и фильтрует экстремально большие свечи (> x2 ATR) и экстремально маленькие (< 0.5 ATR). Также этот индикатор сразу показывает израсходованный "бензин" инструмента в процентах. И вам не надо самостоятельно высчитывать пройденный путь. Вы можете быстро принимать правильные решения. Если мы видим, что бак почти пустой, логично не садиться в эту машину сегодня. Когда вы строите какую-то стратегию, вы должны обязательно полагаться на среднестатистическое движение.

Существует много стратегий, завязанных на ATR, которые учитывают волатильность инструмента, запас хода, точки разворота, места выставления стоп-лоссов (SL) и тейк-профитов (TP) и другие факторы. Я не буду останавливаться на них, так как каждый может найти описание этих стратегий и использовать их на свой выбор.

Индикатор отображается и работает только на дневном таймфрейме!

Индикатор создан по наставлениям, описанию функционала и стратегии господина Герчика. Огромное спасибо, Шеф!

Price Range Volume Profile [Pt]█ Introduction

The Price Range Volume Profile (PRVP) is a revolutionary indicator. This tool stands out from its peers due to its unique ability to capture the entire price chart history, thus providing a comprehensive volume profile of the entire asset's trading history, as available on TradingView chart. It's worth noting that I believe this tool is the first of its kind to accomplish such a feat. A much recommended tool if you are a volume profile trader.

█ Main Features

► Historical Lookback: This feature dives deep into the past, grasping all the historical data of an asset. It's equipped to handle up to 20,000 bars, although users without a premium TradingView account are advised to keep it at a maximum of 10,000 bars, or just use the "Full Historical Lookback" feature.

► Volume Profile / POC: Displays the distribution of volume across price levels for the selected price range. The Point of Control (POC), which is the price level with the highest traded volume, is also highlighted.

► Customization: Users have the flexibility to adjust the profile's appearance, including profile width, horizontal offset, and the option to fill the background of the profile range.

► Time Weighting: This feature allows users to give more weight to recent trading activity, which can be especially useful for intraday traders or during times of high volatility. Note that this feature will impact the volume profile and POC level.

► Settings Table: A settings table is displayed on the chart for users to quickly reference their input parameters.

█ Input Parameters

► Lookback Timeframe: Determines the period for which the volume profile is generated.

► Price Range: The percentage distance to consider for the profile, adjusted above and below the current closing price.

► Profile Step size: The granularity of the volume profile. Users can opt for automatic step size based on a predefined calculation or set their preferred tick step size.

► Historical Bars Lookback: Determines the number of bars to include in the volume profile calculation.

► Profile Visuals: Adjust the appearance and layout of the volume profile on the chart.

► Extra: Additional settings including the display of a settings table and its location.

█ Basic Understanding of Volume Profile - How to use PRVP?

Volume Profile is a valuable tool for traders who want insights into where the majority of trading activity has occurred. Here are some tips to make the most of it:

► Understand the Basics: Before using the Volume Profile, ensure you understand the difference between it and the standard volume histogram. While both represent volume, the former displays it against price while the latter shows it against time.

► Identify High Volume Nodes (HVN) and Low Volume Nodes (LVN):

◊ HVN: Areas where there's a lot of trading activity and where the price has spent a lot of time. These areas can act as strong support or resistance.

◊ LVN: Areas where there's a lack of trading activity. Prices might move quickly through these areas, and they can act as potential breakpoints or accelerators for price movement.

► Locate the Point of Control (POC): This is the price level with the highest traded volume for a specified period. It often acts as a magnet for price, and it can serve as a pivot or reference point.

► Trend Confirmation: A shift in the volume profile from one price level to another can confirm a trend. For instance, if higher volume starts to build at higher price levels, it may indicate a strong uptrend.

► Watch for Volume Gaps: If there's a significant gap in the volume profile, prices may move quickly through these levels as there's little historical trading activity to act as support or resistance.

█ Other Usage Tips

◊ For optimal performance, ensure that the chosen timeframe aligns closely with the chart timeframe. Differences in timeframes may lead to minor discrepancies in the volume profile.

◊ To address any errors arising from too many levels displayed on the volume profile, consider increasing the Profile Step size or reducing the Price Range.

Balance of Force (BOF)The script "Balance of Force" is an indicator that aims to provide insight into the bullish and bearish forces present in the market by analyzing the relationship between bullish and bearish true ranges. The indicator first calculates the bearish and bullish true ranges by taking the absolute difference between the open and close prices for each period and summing these values over a user-specified length. It then calculates the ratio of the bullish true range to the bearish true range and takes the natural logarithm of this value, resulting in the "bullish-bearish ratio".

The script then calculates the standard deviation of this ratio over a user-specified length to create a measure of volatility. Using this deviation and the dominant cycle, it then applies an exponential moving average to smooth the ratio. The indicator plots the smoothed ratio, the raw ratio, and the deviation of the ratio multiplied by 1, 2 and 3 in addition to filling the area between the deviation multiplied by 3 and the log(1) with red and green. The user can use the indicator to identify potential bullish or bearish market conditions by analyzing the relationship between the smoothed ratio and the log(1) and the deviation of the ratio.

Squeeze Range: Bollinger Bands / Keltner Channels [Whvntr]Presenting Squeeze Range: Bollinger Bands / Keltner Channels

TTMSqueeze method is a volatility and momentum indicator introduced by John Carter of Simpler Trading, which capitalizes on the tendency for price to break out strongly after consolidating in a tight trading range.

How did I make this indicator? The Bollinger Bands & Keltner Channels base scripts are from the standard indicators of their class in the Technicals section... I made this indicator first then noticed there were 3 others with a similar concept, but this differs in it's unique features and application of the TTMSqueeze strategy. This indicator plots the True Range of the Keltner Channel (Customizable in 'Bands Style" in the Inputs Menu) the instances the Bollinger Bands are within the range of the Keltner channel (the market just entered a squeeze).

Featuring: customizable Moving Averages

1. Exponential (Default for both BB & KC)

2. Simple

3. RMA (MA used in RSI )

Keltner channels have a multiplier of 2 & 3 on the Chart (3 being the outer).

How do I use this indicator? Once the teal dots are inside the solid red lines this would indicate that TTMperiod of low market volatility (the market is preparing itself for an explosive move up or down). Do some research and study how to use the TTMSqueeze method by John Carter. Disclaimer: not a guarantee of future favorable results.

Daily/Weekly ExtremesBACKGROUND

This indicator calculates the daily and weekly +-1 standard deviation of the S&P 500 based on 2 methodologies:

1. VIX - Using the market's expectation of forward volatility, one can calculate the daily expectation by dividing the VIX by the square root of 252 (the number of trading days in a year) - also know as the "rule of 16." Similarly, dividing by the square root of 50 will give you the weekly expected range based on the VIX.

2. ATR - We also provide expected weekly and daily ranges based on 5 day/week ATR.

HOW TO USE

- This indicator only has 1 option in the settings: choosing the ATR (default) or the VIX to plot the +-1 standard deviation range.

- This indicator WILL ONLY display these ranges if you are looking at the SPX or ES futures. The ranges will not be displayed if you are looking at any other symbols

- The boundaries displayed on the chart should not be used on their own as bounce/reject levels. They are simply to provide a frame of reference as to where price is trading with respect to the market's implied expectations. It can be used as an indicator to look for signs of reversals on the tape.

- Daily and Weekly extremes are plotted on all time frames (even on lower time frames).

Box Range AlertSimple Script for getting alerts on the crossing of Upper & Lower levels either way.

Good for Free users as they can only use 1 alert at a time. So this indicator will be useful to get alerts on both Breakout Or Breakdowns.

Just add input Price manually and set alerts.

SuperTrendRange by DGTSuperTrendRange study attempts to determine the state of the market

• whether a well-established bull/bear trend is present

• whether the market is trading in a range

SuperTrendRange (STR) takes into account the volatility of the market - further details regarding volatility can be found in the description of “Volatility Bands by DGT” study

Due to its similarities to SupertTrend (ST) and Parabolic SAR (SAR), I will try to explain by stating differences between them

SuperTrendRange uses both the ATR (Average True Range) and STDEV (Standard Deviation) as part of its calculations - unlike ST and SAR where they use only ATR

Sensitivity of the indicator is adjusted using the multiplier setting of both ATR and STDEV

Additionally, unlike ST, the source of the basis of SuperTrendRange can be selected among the assets price value or its moving average

Source and Length are adjustable too

The SuperTrendRange, like Parabolic SAR indicator, appears on a chart as a series of dots, either above, below or unlike Parabolic SAR both above and below of the asset's price

A dot placed

- below the price when the market is trending upward

- above the price when it is trending downward

- both above and below when the price starts moving sideways – this is a feature that both SuperTrend and Parabolic SAR misses, where they are known to produce false signals and losing trades, whereas SuperTrendRange emphasis the zones of the ranges occurring and in most cases are considered no trade recommended zones. Please note that the range width may vary depending on how the market is volatile. It is up to the users to trade if it fits their trading strategies

Dots plotted above and below can be assumed as Support and Resistance levels

Example usages – with trading opportunities

Gold Monthly Chart

Bitcoin Daily Chart

Disclaimer:

Trading success is all about following your trading strategy and the indicators should fit within your trading strategy, and not to be traded upon solely

The script is for informational and educational purposes only. Use of the script does not constitute professional and/or financial advice. You alone have the sole responsibility of evaluating the script output and risks associated with the use of the script. In exchange for using the script, you agree not to hold dgtrd TradingView user liable for any possible claim for damages arising from any decision you make based on use of the script

ORB 369 - Opening Range Breakout The ORB 369 is a professional-grade momentum indicator designed to capture the volatility of the New York market open. While many Opening Range Breakout (ORB) scripts simply draw lines, this script integrates time-segmented price action with Supply and Demand (S/D) theory to filter out "fakeouts" and identify high-probability institutional entries.

💡 The Core Concept: Why 3-6-9?

The strategy is rooted in the "Market Open Volatility" principle. The first 15 minutes (9:30–9:45 AM EST) represent the period where institutional orders are processed and "price discovery" is most aggressive.

The Range: We define the 15-minute high and low as the "Battlefield."

The 369 Logic: This script focuses on the 3rd 5-minute candle of the session (completing the 15m range) and monitors the subsequent 5m and 15m cycles for a definitive trend shift.

🛠️ How It Works

The script utilizes Pine Script v6 high-precision time-tracking and state-handling to ensure accuracy even on historical data.

1. Dynamic Session Anchoring

Unlike static indicators, this script uses America/New_York timezone anchoring. It identifies the Opening Range (OR) regardless of your local time, ensuring you are aligned with the NYSE floor traders.

2. Supply & Demand Detection

The script doesn't just look at the high/low; it analyzes the micro-structure within that 15-minute window.

It identifies unmitigated zones (areas where price moved so fast it left "imbalances").

If a breakout occurs but price immediately hits an internal S/D zone, it warns the trader of a potential "Look Above and Fail" scenario.

3. Breakout Confirmation (5m Logic)

A common mistake is entering on a "wick." This script uses Closing Logic:

Bullish Signal: A 5-minute candle must close entirely above the 15m High.

Bearish Signal: A 5-minute candle must close entirely below the 15m Low.

The script then repaints the candle body (defaulting to Blue/Red) to provide an instant visual cue that the "Breakout is Confirmed."

📈 How to Use It

Wait for the Box: At 9:45 AM EST, the script will automatically lock in the High, Low, and Midpoint (Mean) of the range.

Monitor the Midpoint: The Midpoint acts as the "Line in the Sand." If a breakout occurs but price stays near the Midpoint, the trend is weak. If price stays in the upper half of the range, the Bullish bias is stronger.

The Entry: Wait for the Candle Color Change. A blue candle above the range suggests a long entry; a red candle below suggests a short.

Supply/Demand Zones: If the script highlights a "Demand Zone" at the bottom of the range and price bounces off it before breaking the top, this provides a "double-confluence" setup.

⚙️ Technical Features

Customizable Aesthetics: Use the Settings menu to change the breakout colors (Green/Blue/Red) to match your personal chart theme.

Smart Tooltips: Hover over the inputs in the settings to see detailed explanations of what each parameter does.

Alert Ready: Built-in alerts for "Bullish Breakout" and "Bearish Breakout" that can be sent directly to your phone or desktop via TradingView.

DLR - Daily Liquidity Range Framework (v1.3)Daily Level Ranges

This strategy targets discounted premiums for buying Call/Put Options in discounted areas based on liquidity levels that form ranges.

Opening Range creates the strongest liquidity for the day.

Premarket Highs/Lows are strong liquidity points.

Previous Day Highs/Lows are reliable liquidity points.

PMH/PML and PDH/PDL may alternate positions relative to OR.

* Discounted Calls are taken under the OR in Bullish conditions

* Discounted Puts are taken above the OR in bearish conditions.

- Momentum Calls are taken at the OR in Bullish Conditions

- Momentum Puts are taken at the OR in Bearish Conditions

Auction Session Ranges (AMT Edition) [ Alerts] Auction Session Ranges (AMT Edition)

► Overview

The Session Ranges ( AMT Edition) is a session-based market structure and auction analysis tool designed to visually reveal acceptance, rejection, imbalance, and continuation across the Asia, London, and New York CME trading sessions.

Unlike typical indicators, this script is grounded in Auction Market Theory (AMT) and session-based structure, focusing on how price behaves at session extremes rather than relying on lagging calculations, oscillators, or predictive algorithms. Its purpose is to highlight areas where the market has earned the right to be traded, providing traders with a clear, rules-based framework for high-probability directional trades.

Important for backtesting: To properly backtest session extremes, Interaction Lines, and Closest Opposite Extreme Lines, you must use TradingView’s replay mode, as real-time bar-by-bar progression is required to observe how the market interacts with session extremes over time.

► Key Innovations

This is not a conventional session high/low indicator. Its originality comes from several unique design elements: