TMA + OSMA Scalping SystemSystem is based on TMA Bands + OSMA + EMA Zone. Signal is generated when:

- price recently touched lower or upper band

- price is crossing EMA Zone

- OSMA is aligned in direction of trade to be taken

Natural Target would be opposite band set by TMA.

"scalp"に関するスクリプトを検索

Ultimate VWAP Bands- Ultimate VWAP Bands is a script that helps to decide and further clarify areas of oversold and overbought conditions.

- For example, when the price is in the lowest band it is extremely oversold relative to the VWAP . Hence it should be considered a good place to buy with a high risk to reward payoff.

- Each band is set at a fixed offset away from the VWAP . The "VWAP Band Multiplier" adjusts this and is a key part of the script. This allows the indicator to be adjusted based on the assets volatility . For example, with Crypto. A multiplier of 1 would be strongly advised. Whilst a multiplier of 0.1-0.25 would be useful for currency pairs.

- This indicator can be used for all manners of trading. However, it is most effective when used for scalping and swing trading.

Full strategy AllinOne with risk management MACD RSI PSAR ATR MAHey, I am glad to present you one of the strategies where I put a lot of time in it.

This strategy can be adapted to all type of timecharts like scalping, daytrading or swing.

The context is the next one :

First we have the ATR to calculate our TP/SL points. At the same time we have another rule once we enter(we enter based on % risk from total equity, in this example 1%, at the same time, lowest ammount for this example is 0.1 lots, but can be modified to 0.01), so we can exit both by tp/sl points, or by losing 1% of our equity or winning 1% of our total equity. It's dinamic.

The strategy is made from

Trend direction :

PSAR

First confirmation point :

Crossover between 10EMA and Bollinger bands middle point

Second confirmation

MACD histogram

Third confirmation

RSI overbought/oversold levels

For entries : we check trend with psar, then once ema cross bb middle point, we confirm together with rsi level for overbought/oversold and macd histogram ( > 0 or <0).

We exit, when we have opposite sign, like from buy to sell or sell to buy, or when we reach tp/sl points, or when we reach % basaed equity points.

It can be changed to be fixed lots, or fixed tp/sl , you just have to uncomment the size from entries, and tp/sl lines.

At the same time, it has the possibility if one desires, to trade only concrete forex session like european, asian and so on for intraday trading.

Hope you enjoy it.

Let me know how it goes.

Candle checker for long/short for scalping/day tradingHey.

This strategy is still in working.

For it I check a x amount of candles in the past if they been for example all red/green in row, and based on that I enter. For example candle 7 < candle 6 .... candle 3 < candle 2 .... candle 1 < candle current for long and viceversa for short.

After that,once the trade is initiated, I exit based on 2 possibilities : candle color is different than the color of candle when entry, or based tp/sl.

Let me know what you think of it.

I will try to make the process to calculate automatically and input the number of candles to check like 5-10-15 and so on.

mForex - Keltner channel + EMA Scalping systemTransaction setup parameters

Time frame: M5, M15

Currency pair: EUR / USD , GPB / USD

Transaction: London, USA

Number of orders / day: 10 - 15 orders

Trading strategies

=== BUY ===

Candles close on the upper Keltner

EMA10 crosses the upper Keltner range from below

Stop loss in the middle band or up to 12 pips

Profit target: 15-25 pips

=== SELL ===

Candles close below Keltner below

EMA10 crosses the Keltner range below from above

Stop loss in the middle band or up to 12 pips

Profit target: 15-25 pips

mForex - Bollinger Bands - Pinbar scalping systemTransaction setup parameters

Time frame: M5, M15

Currency pair: Any except XAU/USD

Trading strategies

=== BUY ===

Price break out of the lower Bollinger Bands

The Pinbar reversal candlestick appears and closes the candle on the lower Bollinger Bands

Stop loss: Nearest bottom + 3-5 pips

Profit target: 10-20 pips

=== SELL ===

Price break out of the upper Bollinger Bands

The Pinbar reversal candle appeared and closed below the upper

Stop loss: Nearest peak + 3-5 pips

Profit target: 10-20 pips

* If you have any questions or suggestions for this strategy, feel free to ask us.

ADD for SPX intraday (NYSE Adv-Decl) -Tom1traderThis is the NYSE Advancers - decliners which the SPX pretty much follows. You can chart it like any index (ADD -NYSE $ADV MINUS $DECL) but I find it more useful in a separate panel with colors for direction.

The level gives an idea of days move (example: plus or minus 500 is not much movement through the session) but I follow the direction as when more stocks advance (green) or decline (red) the index tends to track it pretty closely.

On SPX, SPY and correlateds - very useful for intra-day trading (Scalping or 0DTE option trades) but not for higher time frames at all. If you chart the ADD in a chart and compare 5 minute to daily you will see what I mean.

I left it at 5 minutes timeframe which displays well on any intraday chart. You can change it by changing the "5" in the security function on line 13 to what you want ("1" 1 minute, "15" 15 minutes) or change it to timeframe.period (no quotes) so that it will follow the timeframe of the current chart. I like 5 min as it displays better on higher timeframes i.e. 15 min. or hour.

A simple moving average with a length of 10 is added to help gauge momemtum.

Hope this helps with trading or scripting ideas, questions or feed back welcome. Keep Smiling.

BTC Co-Relation v1Calculate Pearson-correlation-coefficient of selected cryptocurrency with Bitcoin average price of 10 different exchanges.

This is helpful in scalping(at least for me), by using this we can find co-relation between a cryptocurrency and Bitcoin .

Here we are using Bitcoin average price of 10 different exchanges.

It is an oscillator with minimum value -1 and maximum value +1.

👉-1 means current selected cryptocurrency price is completely out of relation with Bitcoin price, means Bitcoin price increasing and it's price decreasing or Bitcoin price decreasing and it's price increasing in selected time-frame.

👉+1 means current selected cryptocurrency price is completely in co-relation with Bitcoin price, means Bitcoin price increasing and it's price also increasing or Bitcoin price decreasing and it's price also decreasing in selected time-frame.

Happy trading 👍.

DB-X + DSMAJust a quick hack to combine both studies. Could be used for scalping or whatever you find it useful for... ;)

Alerts should work but no backtesting done on it.

First time coding - a 5min forex Scalping strategy This is my first attempt at producing a strategy in Pine Script.

I am NOT a professional coder. I'm not even a good coder at that. I've only started Pine Script coding since September 2019. I am teaching myself.

This script is far from finished. I need to tweak a number of things about this script. Namely:

Add a validity window to the 'trigger bar' condition. Ie, I want to shut down the condition when the price closes above EMA21

Change the order entry so they are stop orders, using the stop entry price derived from the signals

Make changes to lot sizing

Add a trailing stop condition

Comments welcome, but do not expect me to reply to any questions or requests. In fact, don't expect any replies from me. I consider myself notoriously bad at replies.

I do welcome any feedback from any seasoned coders out there, as I am still a novice coder, and have so much to learn!

As to anyone who wants to criticise me - constructive and helpful criticism are most welcome, criticism to make yourself feel superior to me - you kind can eat a dk.

For the strategy rules, google the user ForexSignals TV account and look for the video "SIMPLE and PROFITABLE Forex Scalping Strategy".

Share, learn, prosper

Peace to y'all

Serialhenry

6/11/19

M waves Mk3 'Magical M's v1

V2

V3

So I forgot this existed so here is the Opened sourced code (pm me for older sorce code there are 600+ Saves)(pm me for other scrips course code too lazy to republish everything)

Changes: Simplified and annotated code/upgraded to v4 format

as always adjust before using

i use this indicator combined with the other frequency one to help me identify time and direction of next move.

Pair with rsi

Pair with detrended tsi (have unpublished script might share later)

‘Redraw’ safe

Slightly detrented(adjustable) to avoid traps

quick how to use:

Meant as and adjustable indicator to “tune" to personal risk/reward preference

Green means buy red means sell

arrow indicators for long term sell and buy

Highly customizable (candles too)

Check out my profile for previous versions they are less customizable but also easier to get started with

similar to rsi you want to buy/sell when the indicator turns green/red and lines are as pinched as posible (the lines that are being filled).

keep an eye on the other line that moves around ;) if its not matching the other 2 moving averages and the main color indicator chances are its a trap(works both ways)

use the candles to help you keep your eye on the indicator when scalping (look at the original post for some color ideas)

TradingView's Technical AnalysisAll indicators used on the Technical Analysis Summary from TradingView, composed with oscillators and moving averages. Sell and strong sell will represent more indicators showing sell signals. Buy and strong buy will represent more indicators showing buy signals. A white bar will show neutral signal (don't trade). This can be good for binary options or scalping on small time frames, but also very good on higher times for forex. The signal will appear on the candle before, so wait for the new candle to appear to see what direction the signal will indicate.

Multi Timeframe Moving Average Collection | Scalp [aamonkey]This is a Multi Timeframe Moving Average Collection (Scalp Edition).

Why use it?

- Spot cluster of MAs on one chart

- See support and resistance

- Spot "freefall zones"

In the default settings you will get:

20, 100 and 200 MA of the 15min, 1h, 4h, and the 1D chart.

The color indicates significance!

From weaker to stronger support/resistance:

white(15min), green(1h),yellow(4h),red(1D)

- Length of the MAs is modifiable

- Timeframes of the MAs is modifiable

- Which MAs you want to see

- Colors

Mossy PopMossy Pop is a variation on the CM Chris Moody Pop 1 that is on the public library.

Bars are colored to show when the Pop is red crossing over the blue line turning bullish (Green Buy Bar)

or when it is overbought in green turning into blue going bearish (Red Sell Bar)

Use with other indicators but can work well on confirming a position on its own.

I find it worked best with Heikin Ashi but candles are fine.

Use with Mossy ADX DI for quick scalping profit and to confirm Buy/Sell signals!

[Delphi] Power Tools Scalping MA Power Tools Scalping MA

Inner Version 1.0 01/01/2019

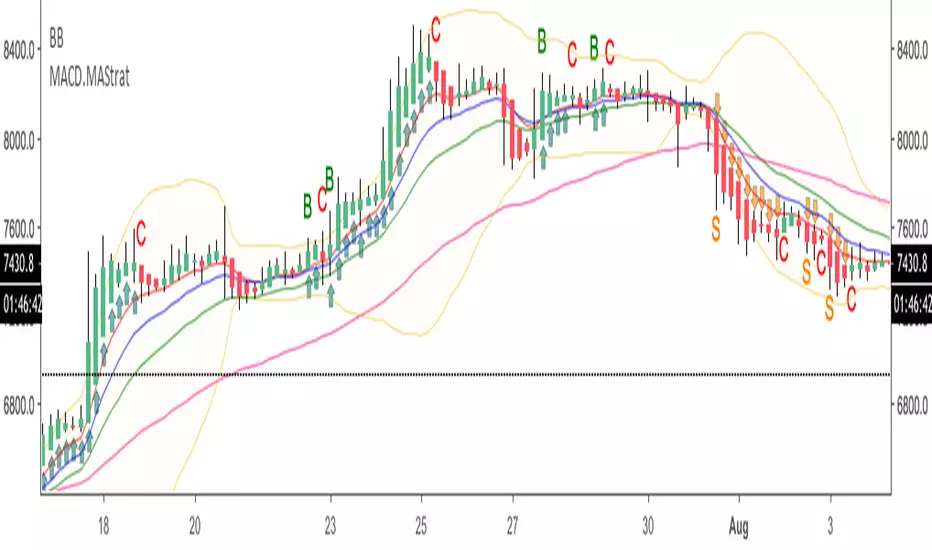

Developer: iDelphi

01/01/2019 Added Multi EMA Channel

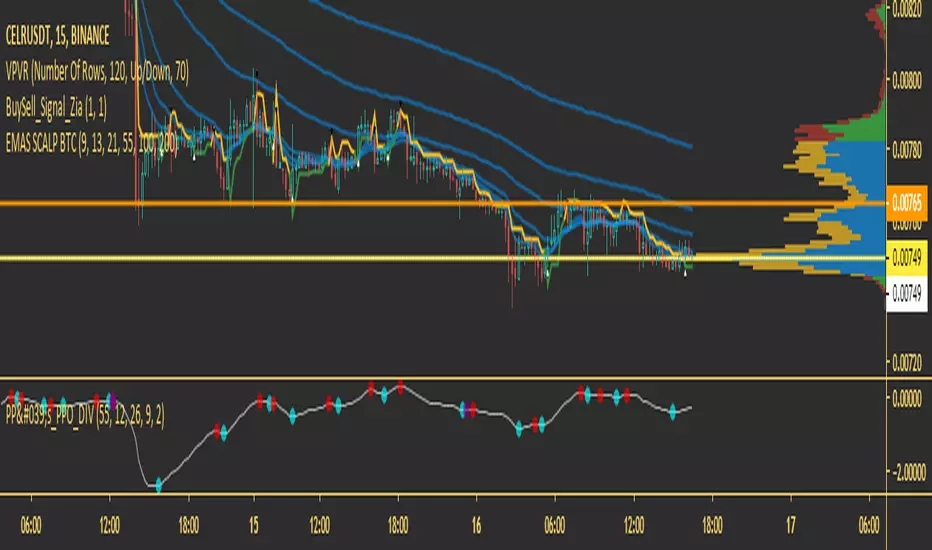

HA.MACD.MA.TradeSetupsHi probably trade setups indicator intended to be used with Heikin Ashi candles. It uses fibo EMAs and MACD to signal longs/shorts. Intended for scalping high cap coin with high volume on lower time frames.