RRG Relative Strength# RRG Relative Strength (RRG RS)

Compare any symbol to a benchmark using two RRG-style lines: **RS-Ratio** (trend of relative strength) and **RS-Momentum** (momentum of that trend). Both are centered at **100**:

- **RS-Ratio > 100** → outperforming the benchmark

- **RS-Ratio < 100** → underperforming

- **RS-Momentum** often **leads** RS-Ratio (crosses 100 earlier)

# How it works

1) Relative Strength (RS): RS = Close(symbol) / Close(benchmark)

2) Normalize around 100: smooth RS with EMA and divide RS by that EMA

3) RS-Ratio: EMA( RS / EMA(RS, Length), LenSmooth ) * 100

4) RS-Momentum: RS-Ratio / EMA(RS-Ratio, LenSmooth) * 100

# Inputs

- Length (default 14): normalization window for RS

- Length Smooth (default 20): smoothing window for RS-Ratio & RS-Momentum

# Benchmark (auto)

- US: SP:SPX (S&P 500)

- Vietnam: HOSE:VNINDEX

- Crypto: INDEX:BTCUSD

(Modify the mapping if needed, or replace with your own input.symbol().)

# How to read

- Improving: RS-Momentum crosses above 100 while RS-Ratio turns up

- Leading: RS-Ratio > 100 with RS-Momentum ≥ 100

- Weakening: RS-Momentum drops below 100; RS-Ratio often follows

# Timeframes & presets

- Works on Daily and Weekly charts

- Daily (fast): 14 / 20

- Approx. weekly behavior on Daily: 50 / 60

Note: Values usually hover near 100 (e.g., ~90–110) but are not strictly bounded. Ensure your symbol and benchmark trade in comparable sessions/currencies.

"spx"に関するスクリプトを検索

Adaptive Correlation Engine (ACE)🧠 Adaptive Correlation Engine (ACE)

Quantify inter-asset relationships with adaptive lag detection and actionable insights.

📌 What is ACE?

The Adaptive Correlation Engine (ACE) is a precision tool for seeking to uncover meaningful relationships between two assets — not just raw correlation, but also lag dynamics, leader detection, and alignment vs. divergence classification.

Unlike static correlation tools, ACE intelligently scans multiple lag windows to find:

✅ The maximum correlation between the base asset and a comparison symbol

⏱️ The optimal lag (if any) at which the correlation is strongest

🧭 Whether the assets are Aligned (positive correlation) or Divergent (inverse)

🔁 Which symbol is leading, and by how many bars

📈 Actionable signal strength based on a user-defined correlation threshold

⚙️ How It Works

Correlation Scan:

For each bar, ACE checks the correlation between the charted asset (close) and a lagged version of the comparison asset across a sliding window of lookback periods.

Lag Optimization:

The engine searches from lag 0 up to your specified Max Lag to find where the correlation (positive or negative) is most significant.

Relationship Classification:

The indicator classifies the relationship as:

Aligned: Positive correlation above the threshold

Divergent: Negative correlation above the threshold

Synchronous: No lag detected

Low Signal: Correlation is weak or noisy

Visual & Tabular Insights:

ACE plots the highest detected correlation on the chart and shows an insight table displaying:

- Correlation value

- Detected lag

- Direction type (aligned/divergent)

- Leading asset

- Suggested action (e.g., “Likely continuation” or “Possible mean reversion”)

💡 How to Use It

Use ACE to identify leadership patterns between assets (e.g., ETH leads altcoins, SPX leads crypto, etc.)

Spot potential lagging trade setups where one asset’s move may soon echo in another

Confirm or challenge correlation-based trading assumptions with data

Combine with technical indicators or price action to time entries and exits more confidently

🔔 Alerts

Built-in alerts notify you when correlation strength crosses your actionable threshold, classified by alignment or divergence.

🛠️ Inputs

Compare Symbol: The asset to compare against (e.g., INDEX:ETHUSD)

Correlation Lookback: Rolling window for calculating correlation

Max Lag Bars: Maximum lag shift to test

Minimum Actionable Correlation: Signal threshold for trade-worthy insights

⚠️ Disclaimer

This tool is for research and informational purposes only. It does not constitute financial advice or a trading signal. Always perform your own due diligence and consult a financial advisor before making investment decisions.

Dynamic 5DMA/EMA with Color for Multiple Products🔹 Dynamic 5DMA/EMA with Slope-Based Coloring (All Timeframes)

This indicator plots a dynamic 5-period moving average that adapts intelligently to your chart's timeframe and product type — giving you a clean, slope-sensitive visual edge across intraday, daily, and weekly views.

✅ Key Features:

📈 Dynamic MA Length Scaling:

On intraday timeframes, the MA adjusts for your selected market session (RTH, ETH, VIX, or Futures), calculating a true 5-day average based on actual session length — not just a flat bar count.

🔄 Automatic Timeframe Detection:

Daily Chart: Uses standard 5DMA or 5EMA.

Weekly Chart: Applies a true 5-week MA.

Intraday Charts: Converts 5 days into bar-length equivalent dynamically.

🎨 Color-Coded Slope Logic:

Green = Rising MA (bullish slope)

Red = Falling MA (bearish slope)

Neutral slope = previous color held for visual continuity

No more guessing — direction is instantly clear.

⚠️ Built-In Slope Flip Alerts:

Set alerts when the slope of the MA turns up or down. Ideal for timing pullback entries or exits across any product.

⚙️ Session Settings for Proper Scaling:

Choose your product's market structure to ensure accurate 5-day conversion on intraday charts:

Stocks - RTH: 390 mins/day

Stocks - ETH: 780 mins/day

VIX: 855 mins/day

Futures: 1440 mins/day

This ensures the MA reflects 5 full trading days, regardless of session irregularities or bar interval.

📌 Why Use This Indicator?

Most MAs misrepresent trend direction on intraday charts because they assume static daily bar counts. This tool corrects that, then adds slope-based coloring to give you a fast, visual read on short-term momentum. Whether you’re swing trading SPY, scalping VIX, or position trading futures, this indicator keeps your view aligned with how institutions see moving averages across timeframes.

🔧 Best For:

VIX & volatility traders

Short-term SPY/SPX traders

Swing traders who value clean setups

Anyone wanting a true 5-day trend anchor on any chart

NDX Levels Adjusted to Active TickerThis indicator allows you to plot custom NDX levels directly on the NQ1! (E-mini NASDAQ-100 Futures) chart, automatically adjusting for the spread between NDX and NQ1!. This is particularly useful for traders who perform technical analysis on NDX but execute trades on NQ1!.

Features:

Input up to three NDX key levels to track (e.g., 23000, 24000, 25000).

The script adjusts these levels in real-time based on the current spread between NDX and NQ1!

Displays the spread in the chart header for quick reference

Plots updated horizontal lines that move with the spread

Includes optional labels showing the spread periodically to reduce clutter

Supports Multiple Tickers: NQ1!, QQQ, NAS100 and NAS100USD.

Ideal for futures traders who want SPX context while trading NQ1!, QQQ, NAS100 or NAS100USD..

IV PercentileIV Percentile Indicator - Brief Description

What It Does

The IV Percentile Indicator measures where current implied volatility ranks compared to the past year, showing what percentage of time volatility was lower than today's level.

How It Works

Data Collection:

Tracks implied volatility (or historical volatility as proxy) for each trading day

Stores the last 252 days (1 year) of volatility readings

Uses VIX data for SPY/SPX, historical volatility for other stocks

Calculation:

IV Percentile = (Days with IV below current level) ÷ (Total days) × 100

Example: If IV Percentile = 75%, it means current volatility is higher than 75% of the past year's readings.

Visual Output

Main Display:

Blue line showing percentile (0-100%)

Reference lines at key levels (20%, 30%, 50%, 70%, 80%)

Color-coded backgrounds for quick identification

Info table with current readings

Key Levels:

80%+ (Red): Very high IV → Sell premium

70-79% (Orange): High IV → Consider selling

30-20% (Green): Low IV → Consider buying

<20% (Bright Green): Very low IV → Buy premium

Trading Application

When IV Percentile is HIGH (70%+):

Options are expensive relative to recent history

Good time to sell premium (iron condors, credit spreads)

Expect volatility to decrease toward normal levels

When IV Percentile is LOW (30%-):

Options are cheap relative to recent history

Good time to buy premium (straddles, long options)

Expect volatility to increase from compressed levels

Core Logic

The indicator helps answer: "Is this a good time to buy or sell options based on how expensive/cheap they are compared to recent history?" It removes the guesswork from volatility timing by providing historical context for current option prices.

Reversal Signal avec TICK + RSIThis indicator is a potential reversal indicator for SCALPING, don't use it for swing. It's base on TICK and on an overbrought/oversold condition of the RSI. You can play with the setting, typicaly I like my TICK to be over reacting an 800/-800 and my rsi over 20 and 80, but it give not enough signal. So I set the TICK signal at 651/-651 and the RSI at 25/75. This indicator is made for SP500 and Nasdaq, so SPY/QQQ/SPX/ES/NQ should work well. It's the first version of it, so maybe I'll add so more data to it to increase signal and lower false one. For now I've test it on live market yet(26/7/25).

The RSI is Fast(5 period), I like to use it on the 1 or 5 min chart.

Please not that it only work during 9h30am to 4pm EST.(Because of the TICK)

Feel free to try and even comment. Don't be harsh on me, it's my first try!

(Sorry for my 'english' it's not my first language)

FAUCON

Orthogonal Projections to Latent Structures (O-PLS)Version 0.1

Orthogonal Projections to Latent Structures (O-PLS) Indicator for TradingView

This indicator, named "Orthogonal Projections to Latent Structures (O-PLS)", is designed to help traders understand the relevance or predictive power of various market variables on the future close price of the asset it's applied to. Unlike standard correlation coefficients that show a simple linear relationship, O-PLS aims to separate variables into "predictive" (relevant to Y) and "orthogonal" (irrelevant noise) components. This Pine Script indicator provides a simplified proxy of the relevance score derived from O-PLS principles.

Purpose of the Indicator

The primary purpose of this indicator is to identify which technical factors (such as price, volume, and other indicators) have the strongest relationship with the future price movement of the current trading instrument. By providing a "relevance score" for each input variable, it helps traders focus on the most influential data points, potentially leading to more informed trading decisions.

Inputs

The indicator offers the following user-definable inputs:

* **Lookback Period:** This integer input (default: 100, min: 10, max: 500) determines the number of past bars used to calculate the relevance scores for each variable. A longer lookback period considers more historical data, which can lead to smoother, less reactive scores but might miss recent shifts in variable importance.

* **External Asset Symbol:** This symbol input (default: `BINANCE:BTCUSDT`) allows you to specify an external asset (e.g., `BINANCE:ETHUSDT`, `NASDAQ:TSLA`) whose close price will be included in the analysis as an additional variable. This is useful for cross-market analysis to see how other assets influence the current chart.

* **Plot Visibility Checkboxes (e.g., "Plot: Open Price Relevance", "Plot: Volume Relevance", etc.):** These boolean checkboxes allow you to toggle the visibility of individual relevance score plots on the chart, helping to declutter the display and focus on specific variables.

Outputs

The indicator provides two main types of output:

Relevance Score Plots: These are lines plotted in a separate pane below the main price chart. Each line corresponds to a specific market variable (Open Price, Close Price, High Price, Low Price, Volume, various RSIs, SMAs, MFI, and the External Asset Close). The value of each line represents the calculated "relevance score" for that variable, typically scaled between 0 and 10. A higher score indicates a stronger predictive relationship with the future close price.

Sorted Relevance Table : A table displayed in the top-right corner of the chart provides a clear, sorted list of all analyzed variables and their corresponding relevance scores. The table is sorted in descending order of relevance, making it easy to identify the most influential factors at a glance. Each variable name in the table is colored according to its plot color, and the external asset's name is dynamically displayed without the "BINANCE:" prefix.

How to Use the Indicator

1. **Add to Chart:** Apply the "Orthogonal Projections to Latent Structures (O-PLS)" indicator to your desired trading chart (e.g., ETH/USDT).

2. **Adjust Inputs:**

* **Lookback Period:** Experiment with different lookback periods to see how the relevance scores change. A shorter period might highlight recent correlations, while a longer one might show more fundamental relationships.

* **External Asset Symbol:** If you trade BTC/USDT, you might add ETH/USDT or SPX as an external asset to see its influence.

3. **Analyze Relevance Scores:**

* **Plots:** Observe the individual relevance score plots over time. Are certain variables consistently high? Do scores change before significant price moves?

* **Table:** Refer to the sorted table on the latest confirmed bar to quickly identify the top-ranked variables.

4. **Incorporate into Strategy:** Use the insights from the relevance scores to:

* Prioritize certain indicators or price actions in your trading strategy. For example, if "Volume" has a high relevance score, it suggests volume confirmation is critical for future price moves.

* Understand the influence of inter-market relationships (via the External Asset Close).

How the Indicator Works

The indicator works by performing the following steps on each bar:

1. **Data Fetching:** It gathers historical data for various price components (open, high, low, close), volume, and calculated technical indicators (SMA, RSI, MFI) for the specified `lookback` period. It also fetches the close price of an `External Asset Symbol` .

2. **Standardization (Z-scoring):** All collected raw data series are standardized by converting them into Z-scores. This involves subtracting the mean of each series and dividing by its standard deviation . Standardization is crucial because it brings all variables to a common scale, preventing variables with larger absolute values from disproportionately influencing the correlation calculations.

3. **Correlation Calculation (Proxy for O-PLS Relevance):** The indicator then calculates a simplified form of correlation between each standardized input variable and the standardized future close price (Y variable) . This correlation is a proxy for the relevance that O-PLS would identify. A high absolute correlation indicates a strong linear relationship.

4. **Relevance Scaling:** The calculated correlation values are then scaled to a range of 0 to 10 to provide an easily interpretable "relevance score" .

5. **Output Display:** The relevance scores are presented both as time-series plots (allowing observation of changes over time) and in a real-time sorted table (for quick identification of top factors on the current bar) .

How it Differs from Full O-PLS

This indicator provides a *simplified proxy* of O-PLS principles rather than a full, mathematically rigorous O-PLS model. Here's why and how it differs:

* **Dimensionality Reduction:** A full O-PLS model would involve complex matrix factorization techniques to decompose the independent variables (X) into components that are predictive of Y and components that are orthogonal (unrelated) to Y but still describe X's variance. Pine Script's array capabilities and computational limits make direct implementation of these matrix operations challenging.

* **Orthogonal Components:** A true O-PLS model explicitly identifies and removes orthogonal components (noise) from the X data that are unrelated to Y. This indicator, in its simplified form, primarily focuses on the direct correlation (relevance) between each X variable and Y after standardization, without explicitly modeling and separating these orthogonal variations.

* **Predictive Model:** A full O-PLS model is ultimately a predictive model that can be used for regression (predicting Y). This indicator, however, focuses solely on **identifying the relevance/correlation of inputs to Y**, rather than building a predictive model for Y itself. It's more of an analytical tool for feature importance than a direct prediction engine.

* **Computational Intensity:** Full O-PLS involves Singular Value Decomposition (SVD) or Partial Least Squares (PLS) algorithms, which are computationally intensive. The indicator uses simpler statistical measures (mean, standard deviation, and direct correlation calculation over a lookback window) that are feasible within Pine Script's execution limits.

In essence, this Pine Script indicator serves as a practical tool for gaining insights into variable relevance, inspired by the spirit of O-PLS, but adapted for the constraints and common use cases of a TradingView environment.

Spread AnalysisSpread Analysis - Futures vs Spot Price Analysis

Advanced spread analysis tool that compares futures/perp prices with spot prices across multiple exchanges, providing insights into market sentiment and potential trading opportunities.

Multi-Asset Support: Automatically detects and analyzes crypto perpetual vs spot spreads, index futures vs cash indices (ES/SPX, NQ/NDX, YM/DJI), and commodity futures vs spot prices (GC/GOLD, CL/USOIL)

Multi-Exchange Aggregation: For crypto, aggregates prices from Binance, BitMEX, Kraken, Bybit, OKX, and Coinbase to calculate mean perp and spot prices

Z-Score Based Alerts: Uses statistical Z-score analysis to identify extreme spread conditions that may signal potential reversals or continuation patterns

Visual Histogram Display: Shows spread differences as colored columns - green for futures premium, red for futures discount

Flexible Calculation Methods: Supports absolute price differences, percentage spreads, or basis point calculations

Trading Applications: Identify market sentiment divergence, spot potential reversal opportunities, and confirm trend strength

Risk Management: Use extreme Z-scores to identify overvalued conditions and potential mean reversion setups

Market Analysis: Understand the relationship between futures and spot markets across different asset classes

Timing Tool: Spread momentum often precedes price moves, providing early signals for entry/exit decisions

Perfect for traders who want to understand the relationship between futures and spot markets, identify divergences, and spot potential reversal opportunities across crypto, indices, and commodities.

Key Features:

• Automatic asset detection and appropriate spread calculation

• Configurable Z-score alerts for extreme conditions

• Comprehensive tooltips and information guide

• Multiple calculation methods (absolute, percentage, basis points)

• Clean, customizable visual display

Use Cases:

• Crypto traders analyzing perp vs spot relationships

• Futures traders monitoring basis relationships

• Mean reversion strategies using extreme spreads

• Trend confirmation using spread momentum

• Market sentiment analysis across asset classes

NY Open Breakout [ATR-5000]# **New York Open Breakout Indicator **

## **📌 Overview**

This **Pine Script** indicator identifies high-probability breakout opportunities at the **New York market open (13:30 UTC)** based on **volatility filters** using **customizable ATR periods and thresholds**.

### **🔹 Key Features**

✅ **Fully Customizable ATR Periods** (2 to **5000** bars)

✅ **Adjustable Thresholds** (0.01% to 5.00%)

✅ **Opening Range (OR) Filter** (0.01% to 5.00%)

✅ **Clean Visuals** – Only highlights the **13:30 UTC candle** when conditions are met

✅ **Real-Time Info Panel** – Displays current ATR & threshold settings

✅ **Automatic Daily Reset** – Fresh signals every trading day

---

## **📊 How It Works**

### **1️⃣ Volatility Check (13:25 UTC)**

- Calculates **two ATR values** (user-defined periods)

- Compares them against **custom % thresholds**

- Only proceeds if **both ATRs exceed** their required volatility levels

### **2️⃣ Opening Range Confirmation (13:30 UTC)**

- Measures the **high-low range** of the 13:30 candle

- Validates if the range meets the **minimum % threshold**

- If all conditions pass → **Highlights the candle** in your chosen color

### **3️⃣ Visual Feedback**

- **🟣 Colored Candle** → Valid breakout signal

- **📊 Info Table** → Shows current ATR settings & thresholds

---

## **⚙️ Customization Options**

| **Setting** | **Default** | **Adjustable Range** |

|---------------------------|------------|----------------------|

| **First ATR Period** | 14 | **2–5000** bars |

| **Second ATR Period** | 161 | **2–5000** bars |

| **First ATR Threshold** | 0.42% | **0.01%–5.00%** |

| **Second ATR Threshold** | 0.40% | **0.01%–5.00%** |

| **OR Range Threshold** | 0.42% | **0.01%–5.00%** |

| **Candle Color** | Purple | **Any color** |

---

## **📈 Best Use Cases**

✔ **Forex (EURUSD, GBPUSD)** – Captures NY session momentum

✔ **Indices (SPX, NASDAQ)** – Works well with opening volatility

✔ **Commodities (Gold, Oil)** – Filters out low-energy days

---

## **🔧 How to Adjust Settings**

1. **Click the gear icon (⚙️)** on your TradingView chart

2. **Modify ATR periods & thresholds** as needed

3. **Change the candle color** for better visibility

---

## **🚀 Why This Indicator?**

- **No repainting** – Signals lock in after candle close

- **No clutter** – Only marks valid 13:30 candles

- **Adaptable** – Works on **any market & timeframe**

- **Fully automated** – No manual adjustments needed

---

### **📥 Apply & Start Trading!**

Simply **load the script** on TradingView and customize it to fit your strategy! 🚀

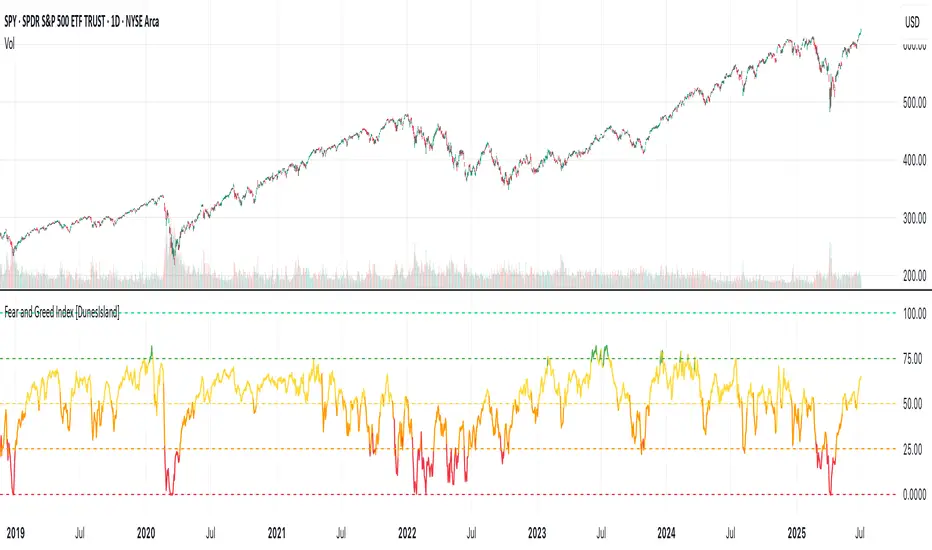

Fear and Greed Index [DunesIsland]The Fear and Greed Index is a sentiment indicator designed to measure the emotions driving the stock market, specifically investor fear and greed. Fear represents pessimism and caution, while greed reflects optimism and risk-taking. This indicator aggregates multiple market metrics to provide a comprehensive view of market sentiment, helping traders and investors gauge whether the market is overly fearful or excessively greedy.How It WorksThe Fear and Greed Index is calculated using four key market indicators, each capturing a different aspect of market sentiment:

Market Momentum (30% weight)

Measures how the S&P 500 (SPX) is performing relative to its 125-day simple moving average (SMA).

A higher value indicates that the market is trading well above its moving average, signaling greed.

Stock Price Strength (20% weight)

Calculates the net number of stocks hitting 52-week highs minus those hitting 52-week lows on the NYSE.

A greater number of net highs suggests strong market breadth and greed.

Put/Call Options (30% weight)

Uses the 5-day average of the put/call ratio.

A lower ratio (more call options being bought) indicates greed, as investors are betting on rising prices.

Market Volatility (20% weight)

Utilizes the VIX index, which measures market volatility.

Lower volatility is associated with greed, as investors are less fearful of large market swings.

Each component is normalized using a z-score over a 252-day lookback period (approximately one trading year) and scaled to a range of 0 to 100. The final Fear and Greed Index is a weighted average of these four components, with the weights specified above.Key FeaturesIndex Range: The index value ranges from 0 to 100:

0–25: Extreme Fear (red)

25–50: Fear (orange)

50–75: Neutral (yellow)

75–100: Greed (green)

Dynamic Plot Color: The plot line changes color based on the index value, visually indicating the current sentiment zone.

Reference Lines: Horizontal lines are plotted at 0, 25, 50, 75, and 100 to represent the different sentiment levels: Extreme Fear, Fear, Neutral, Greed, and Extreme Greed.

How to Interpret

Low Values (0–25): Indicate extreme fear, which may suggest that the market is oversold and could be due for a rebound.

High Values (75–100): Indicate greed, which may signal that the market is overbought and could be at risk of a correction.

Neutral Range (25–75): Suggests a balanced market sentiment, neither overly fearful nor greedy.

This indicator is a valuable tool for contrarian investors, as extreme readings often precede market reversals. However, it should be used in conjunction with other technical and fundamental analysis tools for a well-rounded view of the market.

Daily Trading Barometer (DTB) with DJIA OverlayThe "Daily Trading Barometer (DTB) with DJIA Overlay" is a custom technical indicator designed to identify intermediate-term overbought and oversold conditions in the stock market, inspired by Edson Gould's original DTB methodology. This indicator combines three key components:

A 7-day advance-decline oscillator, a 20-day volume oscillator, and a 28-day DJIA price ratio, normalized into a composite index scaled around 110–135. Values below 110 signal potential oversold conditions, while values above 135 indicate overbought territory, aiding in timing market reversals.

The overlay of a normalized DJIA plot allows for visual correlation with the broader market trend. Use this tool to anticipate turning points in oscillating markets, though it’s best combined with other indicators for confirmation. Ideal for traders seeking probabilistic insights into bear or bull market transitions.

How to use -

If the DTB line (blue) and normalized DJIA (orange) are under the green dashed line, high probability for a long and reversal.

Use with the symbol SPX/QQQ

Dow Jones Industrial Average - DJIA

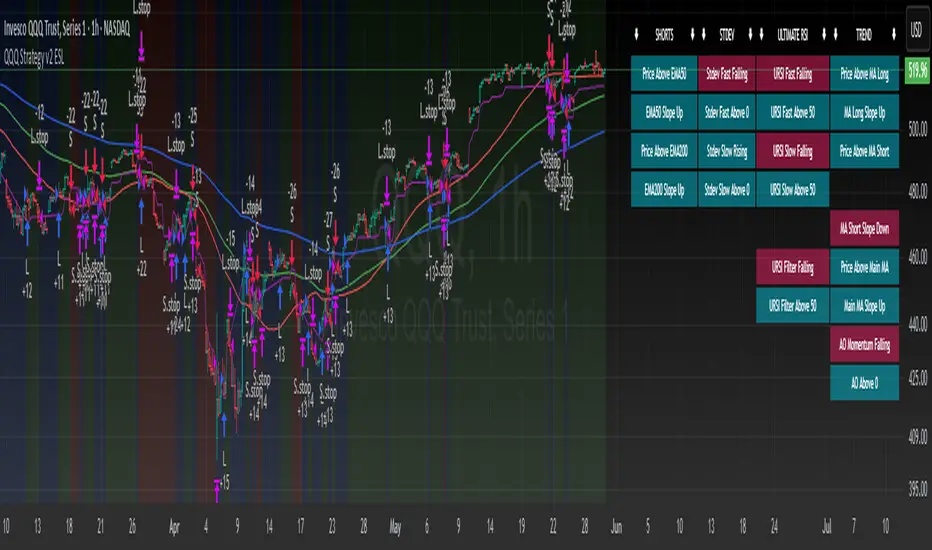

QQQ Strategy v2 ESL | easy-peasy-x This is a strategy optimized for QQQ (and SPY) for the 1H timeframe. It significantly outperforms passive buy-and-hold approach. With settings adjustments, it can be used on various assets like stocks and cryptos and various timeframes, although the default out of the box settings favor QQQ 1H.

The strategy uses various triggers to take both long and short trades. These can be adjusted in settings. If you try a different asset, see what combination of triggers works best for you.

Some of the triggers employ LuxAlgo's Ultimate RSI - shoutout to him for great script, check it out here .

Other triggers are based on custom signed standard deviation - basically the idea is to trade Bollinger Bands expansions (long to the upside, short to the downside) and fade or stay out of contractions.

There are three key moving averages in the strategy - LONG MA, SHORT MA, BASIC MA. Long and Short MAs are guides to eyes on the chart and also act as possible trend filters (adjustable in settings). Basic MA acts as guide to eye and a possible trade trigger (adjustable in settings).

There are a few trend filters the strategy can use - moving average, signed standard deviation, ultimate RSI or none. The filters act as an additional condition on triggers, making the strategy take trades only if both triggers and trend filter allows. That way one can filter out trades with unfavorable risk/reward (for instance, don't long if price is under the MA200). Different trade filters can be used for long and short trades.

The strategy employs various stop loss types, the default of which is a trailing %-based stop loss type. ATR-based stop loss is also available. The default 1.5% trailing stop loss is suitable for leveraged trading.

Lastly, the strategy can trigger take profit orders if certain conditions are met, adjustable in settings. Also, it can hold onto winning trades and exit only after stop out (in which case, consecutive triggers to take other positions will be ignored until stop out).

Let me know if you like it and if you use it, what kind of tweaks would you like to see.

With kind regards,

easy-peasy-x

S&P 500 & Normalized CAPE Z-Score AnalyzerThis macro-focused indicator visualizes the historical valuation of the U.S. equity market using the CAPE ratio (Shiller P/E), normalized over its long-term average and standard deviations. It helps traders and investors identify overvaluation and undervaluation zones over time, combining both statistical signals and historical context.

💡 Why It’s Useful

This indicator is ideal for macro traders and long-term investors looking to contextualize equity valuations across decades. It helps identify statistical extremes in valuation by referencing the standard deviation of the CAPE ratio relative to its long-term mean. The overlay of S&P 500 price with valuation zones provides a visual confirmation tool for macro decisions or timing insights.

It includes:

✅ Three display modes:

-S&P 500 (color-coded by CAPE valuation zone)

-Normalized CAPE (vs. long-term mean)

-CAPE Z-Score (standardized measure)

🎯 How to Interpret

Dynamic coloring of the S&P 500 price based on CAPE valuation:

🔴 Z > +2σ → Highly Overvalued

🟠 Z > +1σ → Overvalued

⚪ -1σ < Z < +1σ → Neutral

🟢 Z < -1σ → Undervalued

✅ Z < -2σ → Strong Buy Zone

-Live valuation label showing the current CAPE, Z-score, and zone.

-Macro event shading: major historical events (e.g. Great Depression, Oil Crisis, Dot-com Bubble, COVID Crash) are shaded on the chart for context.

✅ Built-in alerts:

CAPE > +2σ → Potential risk zone

CAPE < -2σ → Potential opportunity zone

📊 Use Cases

This indicator is ideal for:

🧠 Macro traders seeking long-term valuation extremes.

📈 Portfolio managers monitoring systemic valuation risk.

🏛️ Long-term investors timing strategic allocation shifts.

🧪 How It Works

CAPE ratio (Shiller PE) is retrieved from Quandl (MULTPL/SHILLER_PE_RATIO_MONTH).

The script calculates the long-term average and standard deviation of CAPE.

The Z-score is computed as:

(CAPE - Mean) / Standard Deviation

Users can switch between:

S&P 500 chart, color-coded by CAPE valuation zones.

Normalized CAPE, centered around zero (historic mean).

CAPE Z-score, showing statistical positioning directly.

Visual bands represent +1σ, +2σ, -1σ, -2σ thresholds.

You can switch between modes using the “Display” dropdown in the settings panel.

📊 Data Sources

CAPE: MULTPL/SHILLER_PE_RATIO_MONTH via Quandl

S&P 500: Monthly close prices of SPX (TradingView data)

All data updated on monthly resolution

This is not a repackaged built-in or autogenerated script. It’s a custom-built and interactive indicator designed for educational and analytical use in macroeconomic valuation studies.

SOFR Spread (proxy: FEDFUNDS - US03MY)📊 SOFR Spread (Proxy: FEDFUNDS - US03MY) – Monitoring USD Money Market Liquidity

In 2008, the spread exhibits a sharp vertical spike, signaling a severe liquidity dislocation: investors rushed into short-term U.S. Treasuries, pushing their yields down dramatically, while the FEDFUNDS rate remained relatively high.

This behavior indicates extreme systemic stress in the interbank lending market, preceding massive Federal Reserve interventions such as rate cuts, emergency liquidity operations, and the launch of quantitative easing (QE).

Description:

This indicator plots the spread between the Effective Federal Funds Rate (FEDFUNDS) and the 3-Month US Treasury Bill yield (US03MY), used here as a proxy for the SOFR spread.

It serves as a simple yet powerful tool to detect liquidity dislocations and stress signals in the US short-term funding markets.

Interpretation:

🔴 Spread > 0.20% → Possible liquidity stress: elevated repo rates, cash shortage, interbank distrust.

🟡 Spread ≈ 0% → Normal market conditions, balanced liquidity.

🟢 Spread < 0% → Excess liquidity: strong demand for T-Bills, “flight to safety”, or distortion due to expansionary monetary policy.

Ideal for:

Monitoring Fed policy impact

Anticipating market-wide liquidity squeezes

Correlation with DXY, SPX, VIX, MOVE Index, and risk sentiment

🧠 Note: As SOFR is not directly available on TradingView, FEDFUNDS is used as a reliable proxy, closely tracking the same trends in most macro conditions.

Index Futures vs Cash ArbitrageThis indicator measures the statistical spread between major stock index futures and their corresponding cash indices (e.g., ES vs SPX, NQ vs NDX) using Z-score normalization. It automatically detects commonly traded index pairs (S&P 500, Nasdaq, Dow Jones, Russell 2000) and calculates a smoothed spread between futures and spot prices. A Z-score is then derived from this spread to highlight potential overpricing or underpricing conditions.

Traders can use customizable thresholds to identify mean-reversion opportunities where the futures contract may be temporarily overvalued or undervalued relative to the index. The histogram highlights the direction of the Z-score (green = futures > index, red = futures < index), while built-in alerts notify users of key threshold breaches or zero-line crosses.

This tool is designed for discretionary traders, pairs traders, or anyone exploring statistical arbitrage strategies between futures and spot markets. It is not a buy/sell signal by itself and should be used with additional confluence or risk management techniques.

Divergence Macro Sentiment Indicator (DMSI)The Divergence Macro Sentiment Indicator (DMSI)

Think of DMSI as your daily “mood ring” for the markets. It boils down the tug-of-war between growth assets (S&P 500, copper, oil) and safe havens (gold, VIX) into one clear histogram—so you instantly know if the bulls have broad backing or are charging ahead with one foot tied behind.

🔍 What You’re Seeing

Green bars (above zero): Risk-on conviction.

Equities and commodities are rallying while gold and volatility retreat.

Red bars (below zero): Risk-off caution.

Gold or VIX are climbing even as stocks rise—or stocks aren’t fully joined by oil/copper.

Zero line: The line in the sand between “full-steam ahead” and “proceed with care.”

📈 How to Read It

Cross-Zero Signals

Bullish trigger: DMSI flips up through zero after a red stretch → fresh long entries.

Bearish trigger: DMSI tumbles below zero from green territory → tighten stops or go defensive.

Divergence Warnings

If SPX makes new highs but DMSI is rolling over (lower green bars or red), that’s your early red flag—rallies may fizzle.

Strength Confirmation

On pullbacks, only buy dips when DMSI ≥ 0. When DMSI is deeply positive, you can be more aggressive on position size or add leverage.

💡 Trade Guidance & Use Cases

Trend Filter: Only take your S&P or sector-ETF long setups when DMSI is non-negative—avoids hollow rallies.

Macro Pair Trades:

Deep red DMSI: go long gold or gold miners (GLD, GDX).

Strong green DMSI: lean into cyclicals, industrials, even energy names.

Risk Management:

Scale out as DMSI fades into negative territory mid-trade.

Scale in or add to winners when it stays bullish.

Swing Confirmation: Overlay on any oscillator or price-pattern system—accept signals only when the macro tide is flowing in your favour.

🚀 Why It Works

Markets don’t move in a vacuum. When stocks rally but the “real-economy” metals and volatility aren’t cooperating, something’s off under the hood. DMSI catches those cross-asset cracks before price alone can—and gives you an early warning system for smarter entries, tighter risk, and bigger gains when the macro trend really kicks in.

UM Dual MA with Price Bar Color change & Fill

Description

This is a dual moving average indicator with colored bars and moving averages. I wrote this indicator to keep myself on the right side of the market and trends. It plots two moving averages, (length and type of MA are user-defined) and colors the MAs green when trending higher or red when trending lower. The price bars are green when both MAs are green, red when both MAs are red, and orange when one MA is green and the other is red. The idea behind the indicator is to be extremely visual. If I am buying a red bar, I ask myself "why?" If I am selling a green bar, again, "why?"

Recommended Usage

Configure your tow favorite Moving averages. Consider long positions when one or both turn green. Scale into a position with a portion upon the first MA turning green, and then more when the second turns green. Consider scaling out when the bars are orange after an up move.

Orange bars are either areas of consolidation or prior to major turns.

You can also look for MA crossovers.

The indicator works on any timeframe and any security. I use it on daily, hourly, 2 day charts.

Default settings

The defaults are the author's preferred settings:

- 8 period WMA and 16 period WMA.

- Bars are green when both MAs are trending higher, red when both MAs are trending lower, and orange when one MA is trending higher and the other is trending lower.

Moving average types, lengths, and colors are user-configurable. Bar colors are also user-configurable.

Alerts

Alerts can be set by right-clicking the indicator and selecting the dropdown:

- Bullish Trend Both MAs turning green

- Bearish Trend Both MAs turning red

- Mixed Trend, 1 green 1 red MA

Helpful Hints:

Look for bullish areas when both MAs turn green after a sustained downtrend

Look for bearish areas when both MAs turn red

Careful in areas of orange bars, this could be a consolidation or a warning to a potential trend direction change.

Switch up your timeframes, I toggle back and forth between 1 and 2 days.

Stretch your timeframe over a lower time frame; for example, I like the 8 and 16 daily WMA. With most securities I get 16 bars with pre and post market. This translates into 128 and 256 MAs on the hourly chart. This slows down moves and color transitions for better manageability.

Author's Subjective Observations

I like the 128/256 WMA on the hourly charts for leveraged and inverse ETFs such as SPXL/SPXS, TQQQ/SQQQ, TNA/TZA. Or even the volatility ETFs/ETNS: UVXY, VXX.

Here is a one-hour chart example:

I have noticed that as volatility increases, I should begin looking at higher timeframes. This seems counterintuitive, but higher volatility increases the level of noise or swings.

I question myself when I short a green bar or buy a red bar; "Why am I doing this?" The colors help me visually stay on the right side of trend. If I am going to speculate on a market turn, at least do it when the bars are orange (MA trends differ)

My last observation is a 2-day chart of leveraged ETFs with the 8 and 16 WMAs. I frequently trade SPXL, FNGA, and TNA. If you are really dissecting this indicator,

look at a few 2-day charts. 2-day charts seem to catch the major swings nicely up and down. They also weed out the daily sudden big swings such as a panic move from economic data

or tweets. When both the MAs turn red on a 2-day chart the same day or same bar, beware; this could be a rough ride or short opportunity. I found weekly charts too long for my style but good

to review for direction. Less decisions on longer charts equate to less brain damage for myself.

These are just my thoughts, of course you do you and what suits your style best! Happy Trading.

OverUnder Yield Spread🗺️ OverUnder is a structural regime visualizer , engineered to diagnose the shape, tone, and trajectory of the yield curve. Rather than signaling trades directly, it informs traders of the world they’re operating in. Yield curve steepening or flattening, normalizing or inverting — each regime reflects a macro pressure zone that impacts duration demand, liquidity conditions, and systemic risk appetite. OverUnder abstracts that complexity into a color-coded compression map, helping traders orient themselves before making risk decisions. Whether you’re in bonds, currencies, crypto, or equities, the regime matters — and OverUnder makes it visible.

🧠 Core Logic

Built to show the slope and intent of a selected rate pair, the OverUnder Yield Spread defaults to 🇺🇸US10Y-US2Y, but can just as easily compare global sovereign curves or even dislocated monetary systems. This value is continuously monitored and passed through a debounce filter to determine whether the curve is:

• Inverted, or

• Steepening

If the curve is flattening below zero: the world is bracing for contraction. Policy lags. Risk appetite deteriorates. Duration gets bid, but only as protection. Stocks and speculative assets suffer, regardless of positioning.

📍 Curve Regimes in Bull and Bear Contexts

• Flattening occurs when the short and long ends compress . In a bull regime, flattening may reflect long-end demand or fading growth expectations. In a bear regime, flattening often precedes or confirms central bank tightening.

• Steepening indicates expanding spread . In a bull context, this may signal healthy risk appetite or early expansion. In a bear or crisis context, it may reflect aggressive front-end cuts and dislocation between short- and long-term expectations.

• If the curve is steepening above zero: the world is rotating into early expansion. Risk assets behave constructively. Bond traders position for normalization. Equities and crypto begin trending higher on rising forward expectations.

🖐️ Dynamically Colored Spread Line Reflects 1 of 4 Regime States

• 🟢 Normal / Steepening — early expansion or reflation

• 🔵 Normal / Flattening — late-cycle or neutral slowdown

• 🟠 Inverted / Steepening — policy reversal or soft landing attempt

• 🔴 Inverted / Flattening — hard contraction, credit stress, policy lag

🍋 The Lemon Label

At every bar, an anchored label floats directly on the spread line. It displays the active regime (in plain English) and the precise spread in percent (or basis points, depending on resolution). Colored lemon yellow, neither green nor red, the label is always legible — a design choice to de-emphasize bias and center the data .

🎨 Fill Zones

These bands offer spatial, persistent views of macro compression or inversion depth.

• Blue fill appears above the zero line in normal (non-inverted) conditions

• Red fill appears below the zero line during inversion

🧪 Sample Reading: 1W chart of TLT

OverUnder reveals a multi-year arc of structural inversion and regime transition. From mid-2021 through late 2023, the spread remains decisively inverted, signaling persistent flattening and credit stress as bond prices trended sharply lower. This prolonged inversion aligns with a high-volatility phase in TLT, marked by lower highs and an accelerating downtrend, confirming policy lag and macro tightening conditions.

As of early 2025, the spread has crossed back above the zero baseline into a “Normal / Steepening” regime (annotated at +0.56%), suggesting a macro inflection point. Price action remains subdued, but the shift in yield structure may foreshadow a change in trend context — particularly if follow-through in steepening persists.

🎭 Different Traders Respond Differently:

• Bond traders monitor slope change to anticipate policy pivots or recession signals.

• Equity traders use regime shifts to time rotations, from growth into defense, or from contraction into reflation.

• Currency traders interpret curve steepening as yield compression or divergence depending on region.

• Crypto traders treat inversion as a liquidity vacuum — and steepening as an early-phase risk unlock.

🛡️ Can It Compare Different Bond Markets?

Yes — with caveats. The indicator can be used to compare distinct sovereign yield instruments, for example:

• 🇫🇷FR10Y vs 🇩🇪DE10Y - France vs Germany

• 🇯🇵JP10Y vs 🇺🇸US10Y - BoJ vs Fed policy curves

However:

🙈 This no longer visualizes the domestic yield curve, but rather the differential between rate expectations across regions

🙉 The interpretation of “inversion” changes — it reflects spread compression across nations , not within a domestic yield structure

🙊 Color regimes should then be viewed as relative rate positioning , not absolute curve health

🙋🏻 Example: OverUnder compares French vs German 10Y yields

1. 🇫🇷 Change the long-duration ticker to FR10Y

2. 🇩🇪 Set the short-duration ticker to DE10Y

3. 🤔 Interpret the result as: “How much higher is France’s long-term borrowing cost vs Germany’s?”

You’ll see steepening when the spread rises (France decoupling), flattening when the spread compresses (convergence), and inversions when Germany yields rise above France’s — historically rare and meaningful.

🧐 Suggested Use

OverUnder is not a signal engine — it’s a context map. Its value comes from situating any trade idea within the prevailing yield regime. Use it before entries, not after them.

• On the 1W timeframe, OverUnder excels as a macro overlay. Yield regime shifts unfold over quarters, not days. Weekly structure smooths out rate volatility and reveals the true curvature of policy response and liquidity pressure. Use this view to orient your portfolio, define directional bias, or confirm long-duration trend turns in assets like TLT, SPX, or BTC.

• On the 1D timeframe, the indicator becomes tactically useful — especially when aligning breakout setups or trend continuations with steepening or flattening transitions. Daily views can also identify early-stage regime cracks that may not yet be visible on the weekly.

• Avoid sub-daily use unless you’re anchoring a thesis already built on higher timeframe structure. The yield curve is a macro construct — it doesn’t oscillate cleanly at intraday speeds. Shorter views may offer clarity during event-driven spikes (like FOMC reactions), but they do not replace weekly context.

Ultimately, OverUnder helps you decide: What kind of world am I trading in? Use it to confirm macro context, avoid fighting the curve, and lean into trades aligned with the broader pressure regime.

JPMorgan Collar LevelsThis indicator visualizes the current JPMorgan Hedging Collar strategy commonly used by institutional funds like JHEQX. It plots three key levels:

– Short Call strike (upper bound)

– Long Put strike (protection level)

– Short Put strike (cost reduction)

The area between the long put and short call is shaded to represent the active hedging zone. This setup is updated quarterly and can influence SPX market behavior near expiration dates.

Inputs are customizable to reflect the latest collar configuration. Useful for traders tracking institutional hedging flows or analyzing market structure near key option expirations.

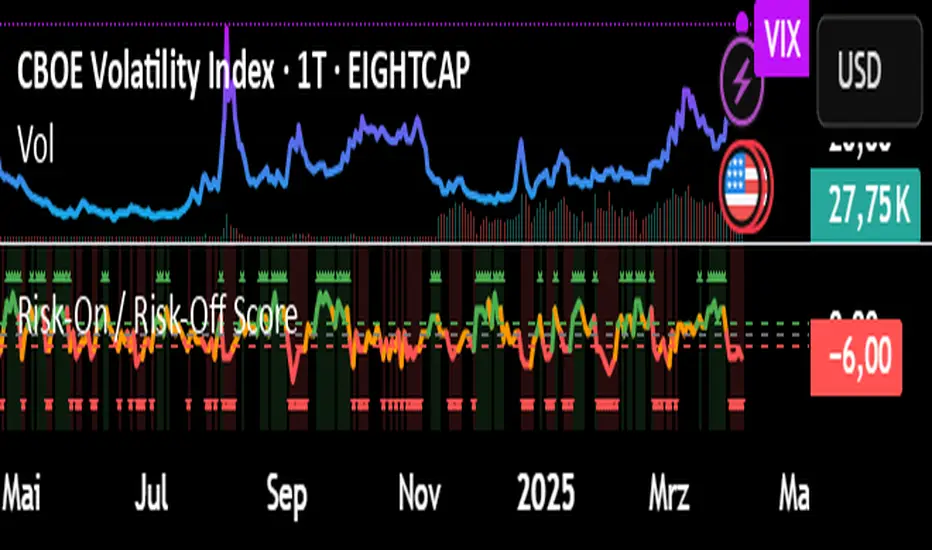

Risk-On / Risk-Off ScoreRisk-On / Risk-Off Score (Macro Sentiment Indicator)

This indicator calculates a custom Risk-On / Risk-Off Score to objectively assess the current market risk sentiment using a carefully selected basket of macroeconomic assets and intermarket relationships.

🧠 What does this indicator do?

The score is based on 14 key components grouped into three categories:

🟢 Risk-On Assets (rising = appetite for risk)

(+1 if performance over X days is positive, otherwise –1)

NASDAQ 100 (NAS100USD)

S&P 500 (SPX)

Bitcoin (BTCUSD)

Copper (HG1!)

WTI Crude Oil (CLK2025)

🔴 Risk-Off Assets (rising = flight to safety)

(–1 if performance is positive, otherwise +1)

Gold (XAUUSD)

US Treasury Bonds (TLT ETF) (TLT)

US Dollar Index (DXY)

USD/CHF

USD/JPY

US 10Y Yields (US10Y) (yields are interpreted inversely)

⚖️ Risk Spreads / Relative Indicators

(+1 if rising, –1 if falling)

Copper/Gold Ratio → HG1! / XAUUSD

NASDAQ/VIX Ratio → NAS100USD / VIX

HYG/TLT Ratio → HYG / TLT

📏 Score Calculation

Total score = sum of all components

Range: from –14 (extreme Risk-Off) to +14 (strong Risk-On)

Color-coded output:

🟢 Score > 2 = Risk-On

🟠 –2 to +2 = Neutral

🔴 Score < –2 = Risk-Off

Displayed as a line plot with background color and signal markers

🧪 Timeframe of analysis:

Default: 5 days (adjustable via input)

Calculated using Rate of Change (% change)

🧭 Use Cases:

Quickly assess macro sentiment

Filter for position sizing, hedging, or intraday bias

Especially useful for:

Swing traders

Day traders with macro filters

Volatility and options traders

📌 Note:

This is not a buy/sell signal indicator, but a contextual sentiment tool designed to help you stay aligned with overall market conditions.

Panic Drop Stock Market Bull/Bear Market Panic Drop Bull/Bear

What It Does:

This indicator identifies bull and bear markets for the S&P 500 (or any stock/index) using the 50-period and 150-period Simple Moving Averages (SMAs). A green background signals a confirmed bull market when the 50 SMA is above the 150 SMA and the 150 SMA slope is flat or upward. A red background signals a confirmed bear market when the 50 SMA is below the 150 SMA and the 150 SMA slope is downward. The background color persists until a new confirmed state is detected, ensuring no gaps—perfect for spotting long-term market trends whether you’re a beginner, trend trader, or long-term investor.

Key Features:

Plots 50 SMA (default: blue line) and 150 SMA (default: orange line).

Background highlights: green for bull markets, red for bear markets.

Persistent background color—no gaps during unconfirmed periods.

Alerts for confirmed bull and bear market transitions.

Fully adjustable: MA periods, slope lookback, and more.

How to Use It:

Add to your S&P 500 chart (e.g., SPX or SPY) on a daily or weekly timeframe (daily default recommended for long-term trends).

Watch for background color changes:

Green background: Confirmed bull market—consider long positions or holding.

Red background: Confirmed bear market—consider shorting or exiting longs.

Customize via settings:

Adjust MA periods (default: 50 and 150).

Set slope lookback (default: 5 bars) to control slope sensitivity.

Change MA colors if desired.

Set alerts: Right-click on the chart > "Add Alert" > Select "Bull Market Confirmed" or "Bear Market Confirmed."

Trade smart: Use the background to confirm market regimes—e.g., go long during green (bull) phases above key support levels, or protect capital during red (bear) phases.

Why It’s Great:

Beginners: Simple background colors make market trends easy to spot.

Trend Traders: 50/150 SMA crossover with slope confirmation catches major market shifts.

Long-Term Investors: Persistent background ensures you stay in the trend without noise.

Created by Timothy Assi (Panic Drop), eToro’s elite investor. Test it, tweak it, and trade with confidence!

OPEX & VIX Expiry Markers (Past, Present, Future)Expiry Date Indicator for Options & Index Traders

Track Key Expiration Dates Automatically

For traders focused on options, indices, and expiration-based strategies, staying aware of key expiration dates is essential. This TradingView indicator automatically plots OPEX, VIX Expiry, and Quarterly Expirations on your charts—helping you plan trades more effectively without manual tracking.

Features:

✔ OPEX Expiration Markers – Highlights the third Friday of each month, when equity and index options expire.

✔ VIX Expiration Tracking – Marks Wednesday VIX expirations, useful for volatility-based trades.

✔ Quarterly Expiration Highlights – Identifies major market expiration cycles for better trade management.

✔ Live Countdown to Next OPEX – Displays how many days remain until the next expiration.

✔ Works on Any Timeframe – Past, present, and future expiration dates update dynamically.

✔ Customizable Settings – Enable or disable specific features based on your trading style.

Ideal for Traders Who Use:

📈 SPX / SPY / NDX / VIX Options Strategies

📅 Iron Condors, Credit Spreads, and Expiration-Based Trades

This tool helps traders stay ahead of expiration cycles, ensuring they never miss an important date. Simple, effective, and built for seamless integration into your trading workflow.

This keeps it professional and to the point without overhyping it. Let me know if you'd like any further refinements! 🚀

IBS (Internal Bar Strength) Trading Strategy for SPY and NDQImplementation by AlgoTradeKit

Overview

The IBS Trading Strategy is a daily bars long-only trading system, based on the concept of Internal Bar Strength (IBS). The strategy aims to identify potential reversals by monitoring how the previous bar’s close positions itself within its high-low range. It is suitable for stock and US indices. The default parameters are optimized for SPY/SPX and NDQ/QQQ

Strategy Concept

The Internal Bar Strength (IBS) is calculated using the formula:

IBS = (Previous Close - Previous Low) / (Previous High - Previous Low)

This value always lies between 0 and 1. An IBS value below 0.2 is typically interpreted as an oversold condition, while a value above 0.9 suggests an overbought state.

Trading Rules

- Long Entry :

- Condition 1 : IBS is below the user-defined entry threshold (default is 0.2).

- Condition 2 : The current price is above an N-period Exponential Moving Average (EMA) (default period is 252).

- Note : You can disable the EMA condition by setting the EMA period to 0.

- Long Exit

- The position is closed when IBS rises above the user-defined exit threshold (default is 0.9).

Customization Options

- IBS Entry Threshold : Adjust to set the sensitivity for entering a long trade based on oversold conditions.

- IBS Exit Threshold : Customize to define the exit point when the market becomes overbought.

- EMA Period : Set the lookback period for the EMA to align with your trend bias; disable this condition by setting the period to 0.

Risk Management & Trading Considerations

- Designed for daily charts, the strategy captures higher timeframe trends and minimizes noise.

- The entry and exit conditions are straightforward, aiming to avoid over-trading while letting clear signals dictate trade management.

- Always use proper risk management techniques and test the strategy thoroughly on historical data and in a simulated environment before applying it in live markets.

Disclaimer

This strategy is for educational and informational purposes only and does not constitute financial advice. Trading involves risk, and past performance is not indicative of future results. Always conduct your own research and consider your risk tolerance before making any trades.