BKLevelsThis displays levels from a text input, levels from certain times on the previous day, and high/low/close from previous day. The levels are drawn for the date in the first line of the text input. Newlines are required between each level

Example text input:

2024-12-17

SPY,606,5,1,Lower Hvol Range,FIRM

SPY,611,1,1,Last 20K CBlock,FIRM

SPY,600,2,1,Last 20K PBlock,FIRM

SPX,6085,1,1,HvolC,FIRM

SPX,6080,2,1,HvolP,FIRM

SPX,6095,3,1,Upper PDVR,FIRM

SPX,6060,3,1,Lower PDVR,FIRM

For each line, the format is ,,,,,

For color, there are 9 possible user- configurable colors- so you can input numbers 1 through 9

For line style, the possible inputs are:

"FIRM" -> solid line

"SHORT_DASH" -> dotted line

"MEDIUM_DASH" -> dashed line

"LONG_DASH" -> dashed line

"spx"に関するスクリプトを検索

Correlation Coefficient [Giang]### **Introduction to the "Correlation Coefficient" Indicator**

#### **Idea behind the Indicator**

The "Correlation Coefficient" indicator was developed to analyze the linear relationship between Bitcoin (**BTCUSD**) and other important economic indices or financial assets, such as:

- **SPX** (S&P 500 Index): Represents the U.S. stock market.

- **DXY** (Dollar Index): Reflects the strength of the USD against major currencies.

- **SPY** (ETF representing the S&P 500): A popular trading instrument.

- **GOLD** (Gold price): A traditional safe-haven asset.

The correlation between these assets can help traders understand how Bitcoin reacts to market movements of traditional financial instruments, providing opportunities for more effective trading decisions.

Additionally, the indicator allows users to **customize asset symbols for comparison**, not limited to the default indices (SPX, DXY, SPY, GOLD). This flexibility enables traders to tailor their analysis to specific goals and portfolios.

---

#### **Significance and Use of Correlation in Trading**

**Correlation** is a measure of the linear relationship between two data series. In the context of this indicator:

- **The correlation coefficient ranges from -1 to 1**:

- **1**: Perfect positive relationship (both increase or decrease together).

- **0**: No linear relationship.

- **-1**: Perfect negative relationship (one increases while the other decreases).

- **Use in trading**:

- Identify **strong relationships or unusual divergences** between Bitcoin and other assets.

- Help determine **market sentiment**: For example, if Bitcoin has a negative correlation with DXY, traders might expect Bitcoin to rise when the USD weakens.

- Provide a foundation for hedging strategies or investments based on inter-asset relationships.

---

#### **Components of the Indicator**

The "Correlation Coefficient" indicator consists of the following key components:

1. **Main Data (BTCUSD)**:

- The closing price of Bitcoin is used as the central asset for calculations.

2. **Comparison Data**:

- Users can select different asset symbols for comparison. By default, the indicator supports:

- **SPX**: Stock market index.

- **DXY**: Dollar Index.

- **SPY**: Popular ETF.

- **GOLD**: Gold price.

3. **Correlation Coefficients**:

- Calculated between BTC and each comparison index, based on a Weighted Moving Average (WMA) over a user-defined period.

4. **Graphical Representation**:

- Displays individual correlation coefficients with each comparison index, making it easier for traders to track and analyze.

---

#### **How to Analyze and Use the Indicator**

**1. Identify Key Correlations:**

- Observe the correlation lines between BTC and the indices to determine positive or negative relationships.

- Example:

- If the **Correlation Coefficient (BTC-DXY)** sharply declines to -1, this indicates that when USD strengthens, Bitcoin tends to weaken.

**2. Analyze the Strength of Correlations:**

- **Strong Correlations**: If the coefficient is close to 1 or -1, the relationship between the two assets is very clear.

- **Weak Correlations**: If the coefficient is near 0, Bitcoin may be influenced by other factors outside the compared index.

**3. Develop Trading Strategies:**

- Use correlations to predict Bitcoin's price movements:

- If BTC has an inverse relationship with **DXY**, traders might consider selling BTC when the USD strengthens.

- If BTC and **SPX** are strongly correlated, traders can monitor the stock market to predict Bitcoin's trend.

**4. Evaluate Changes Over Time:**

- Use different timeframes (daily, weekly) to track the correlation's fluctuations.

- Look for unusual signals, such as a breakdown or shift from positive to negative relationships.

---

#### **Conclusion**

The "Correlation Coefficient" indicator is a powerful tool that helps traders analyze the relationship between Bitcoin and major financial indices. The ability to customize asset symbols for comparison makes the indicator flexible and suitable for various trading strategies. When used correctly, this indicator not only provides insights into market sentiment but also supports the development of intelligent trading strategies and optimized profits.

Scaled Historical ATR [SS]Hello again everyone,

This is the Scaled ATR Range indicator. This was done in response to an article/analysis I posted regarding the expected high and range on SPX. I would encourage you to read it here:

Essentially, I took SPX data, scaled it to correct for inflation, then calculated the ATR for Bullish years to get our average range to expect and our close range to expected.

I accomplished this analysis using Excel; however, I figured Pinescript would handle this type of task more elegantly, and I was correct!

This indicator is the result.

What it does:

This indicator permits the analyst to select a historic period in time. The indicator will then scale the period into returns and convert the range to a corrected range based on the current position of the ticker. How it does this is by converting the returns of the historic period selected, then multiplying the returns by the current period open, to ensure that the range amounts are corrected for inflation and natural growth of a ticker.

I say analyst because this indicator is intended to be used by both professional and recreational analysts, to give them an easy way to:

a) Scale historic data and correct it based on the current rate; and

b) Offer insight into a ticker’s ATR and behaviour during bullish and bearish periods.

Prior to this indicator, the only way to do this would be manually or the use of statistical software.

How to use?

The indicator’s use is quite simple. Once launched, the indicator will ask the user to input a timeframe period that the user is interested in assessing. In the main chart above, I chose SPX between 1995 and 2001.

The user can further filter down the data using the settings menu. In the settings menu, there is an option to filter by “All”, “Bullish Periods” or “Bearish Periods”.

Filtering by “All”

Filtering by “All” will include all candles selected within the timeframe. This includes both bearish and bullish candles. It will give you the averaged out range for the entire period of time, including both bearish and bullish instances.

Filtering by “Bullish”

Filtering by “Bullish” will omit any red candles from the analysis. It will only return the ATR ranges for green, bullish candles.

Filtering by “Bearish”

Inverse to filtering by Bullish, if you filter by Bearish, it will only include the red, bearish candles in the analysis.

My suggestion? If you are trying to determine t he likely outcome of a bullish year, filter by Bullish instances. If you want the likely outcome of a bearish year, filter by Bearish.

Other features of the Indicator:

The indicator will display the current period statistics. In the main chart above, you can see that the current ranges for this year are displayed. This allows you to do a side by side comparison of the current period vs. the historic period you are looking at. This can alert you to further upside, further downside and the anticipated close range. It can also alert you to whether or not we are following a similar trajectory as the historical periods you are looking at.

As well, the indicator will list target prices for the current period based on the historical periods you are looking at. This helps to put things into perspective.

Concluding Remarks

And that is the indicator in a nutshell! I encourage you to read the article I linked above to see how you may use it in an analysis. This would be the best example of a real world application of this indicator!

Otherwise, I hope you enjoy and, as always, safe trades!

[dharmatech] Area Under Yield Curve : USThis indicator displays the area under the U.S. Treasury Securities yield curve.

If you compare this to SP:SPX , you'll see that there are large periods where they are inversely related. Other times, they track together. When the move together, watch out for the expected and eventual divergence.

By default, this indicator will show up in a separate pane. If you move it to an existing pane (e.g. along side SP:SPX ) you'll need to move it to a different price scale.

The area under the yield curve is a quick way to see if the overall yield curve moved up or down. Generally speaking, increasing yields isn't good for markets, unless there is some other stimulus going on simultaneously.

The following treasury securities are used in this calculation:

FRED:DGS1MO (1 month)

FRED:DGS3MO (3 month)

FRED:DGS6MO (6 month)

FRED:DGS1 (1 year)

FRED:DGS2 (2 year)

FRED:DGS3 (3 year)

FRED:DGS5 (5 year)

FRED:DGS7 (7 year)

FRED:DGS10 (10 year)

FRED:DGS20 (20 year)

FRED:DGS30 (30 year)

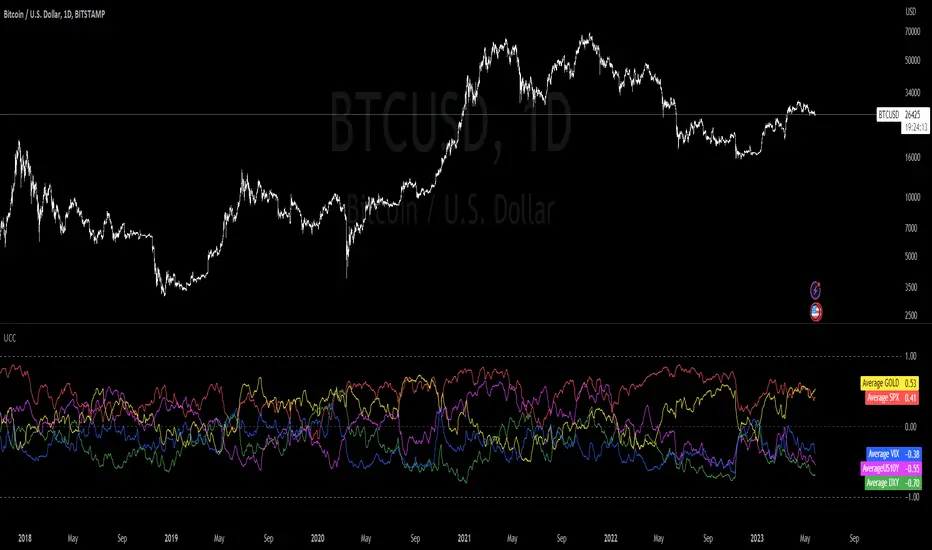

Ultimate Correlation CoefficientIt contains the Correlations for SP:SPX , TVC:DXY , CURRENCYCOM:GOLD , TVC:US10Y and TVC:VIX and is intended for INDEX:BTCUSD , but works fine for most other charts as well.

Don't worry about the colored mess, what you want is to export your chart ->

TradingView: How can I export chart data?

and then use the last line in the csv file to copy your values into a correlation table.

Order is:

SPX

DXY

GOLD

US10Y

VIX

Your last exported line should look like this:

2023-05-25T02:00:00+02:00 26329.56 26389.12 25873.34 26184.07 0 0.255895534 -0.177543633 0.011944815 0.613678565 0.387705043 0.696003298 0.566425278 0.877838156 0.721872645 0 -0.593674719 -0.839538073 -0.662553817 -0.873684242 -0.695764534 -0.682759656 -0.54393749 -0.858188808 -0.498548691 0 0.416552489 0.424444345 0.387084882 0.887054782 0.869918437 0.88455388 0.694720993 0.192263269 -0.138439783 0 -0.39773255 -0.679121698 -0.429927048 -0.780313396 -0.661460134 -0.346525721 -0.270364046 -0.877208139 -0.367313687 0 -0.615415111 -0.226501775 -0.094827955 -0.475553396 -0.408924242 -0.521943234 -0.426649404 -0.266035908 -0.424316191

The zeros are thought as a demarcation for ease of application :

2023-05-25T02:00:00+02:00 26329.56 26389.12 25873.34 26184.07 0 -> unused

// 15D 30D 60D 90D 120D 180D 360D 600D 1000D

0.255895534 -0.177543633 0.011944815 0.613678565 0.387705043 0.696003298 0.566425278 0.877838156 0.721872645 -> SPX

0

-0.593674719 -0.839538073 -0.662553817 -0.873684242 -0.695764534 -0.682759656 -0.54393749 -0.858188808 -0.498548691 -> DXY

0

0.416552489 0.424444345 0.387084882 0.887054782 0.869918437 0.88455388 0.694720993 0.192263269 -0.138439783 -> GOLD

0

-0.39773255 -0.679121698 -0.429927048 -0.780313396 -0.661460134 -0.346525721 -0.270364046 -0.877208139 -0.367313687 -> US10Y

0

-0.615415111 -0.226501775 -0.094827955 -0.475553396 -0.408924242 -0.521943234 -0.426649404 -0.266035908 -0.424316191 -> VIX

VIX Rule of 16There’s an interesting aspect of VIX that has to do with the number 16. (approximately the square root of the number of trading days in a year).

In any statistical model, 68.2% of price movement falls within one standard deviation (1 SD ). The rest falls into the “tails” outside of 1 SD .

When you divide any implied volatility (IV) reading (such as VIX ) by 16, the annualized number becomes a daily number

The essence of the “rule of 16.” Once you get it, you can do all sorts of tricks with it.

If the VIX is trading at 16, then one-third of the time, the market expects the S&P 500 Index (SPX) to trade up or down by more than 1% (because 16/16=1). A VIX at 32 suggests a move up or down of more than 2% a third of the time, and so on.

• VIX of 16 – 1/3 of the time the SPX will have a daily change of at least 1%

• VIX of 32 – 1/3 of the time the SPX will have a daily change of at least 2%

• VIX of 48 – 1/3 of the time the SPX will have a daily change of at least 3%

Volatility barometerIt is the indicator that analyzes the behaviour of VIX against CBOE volaility indices (VIX3M, VIX6M and VIX1Y) and VIX futures (next contract to the front one - VX!2). Because VIX is a derivate of SPX, the indicator shall be used on the SPX chart (or equivalent like SPY).

When the readings get above 90 / below 10, it means the market is overbought / oversold in terms of implied volatility. However, it does not mean it will reverse - if the price go higher along with the indicator readings then everything is fine. There is an alarming situation when the SPX is diverging - e.g. the price go higher, the readings lower. It means the SPX does not play in the same team as IVOL anymore and might reverse.

You can use it in conjunction with other implied volatility indicators for stronger signals: the Correlation overlay ( - the indicator that measures the correlation between VVIX and VIX) and VVIX/VIX ratio (it generates a signal the ratio makes 50wk high).

VIX-VXV-Ratio-Buschi

English:

This script shows the ratio between the VIX (implied volatility of SPX options over the next month) and the VXV (implied volatility of SPX options over the next three months). Since in normal "Contango" mode, the VXV should be higher than the VIX, the crossing under 1.0 or maybe 0.95 after a volatility spike could be a sign for a calming market or at least a calming volatility.

Deutsch:

Dieses Skript zeigt das Verhältnis zwischen dem VIX (implizite Volatilität der SPX-Optionen über den nächsten Monat) und dem VXV (implizite Volatilität der SPX-Optionen über die nächsten drei Monate). Da im normalen "Contango"-Modus der VXV höher als der VIX liegen sollte, kann das Abfallen unter 1,0 oder 0,95 nach einer Volatilitätsspitze ein Anzeichen für einen ruhiger werdenden Markt oder zumindest eine ruhiger werdende Volatilität sein.

Volatility Radar Volatility Radar

A comprehensive VIX-based dashboard for volatility regime analysis and trade bias confirmation. Designed for options traders who use VIX levels to inform directional bias and identify potential traps in market positioning.

Dashboard Columns

1. 10-Min Rule

Displays your current directional bias based on VIX zone positioning with time-based confirmation.

CALLS (Green): VIX is below the Bullish Chop level — conditions favor call buying / bullish stock positioning

PUTS (Red): VIX is above the Bearish Chop level — conditions favor put buying / bearish stock positioning

CHOP (Yellow): VIX is between the two chop levels — no clear directional edge

Confirmation Logic: The bias must hold for a configurable period (default: 10 minutes) before showing "✓ CONFIRMED". A countdown timer shows time remaining until confirmation. High-velocity moves (spikes or crushes) trigger immediate confirmation. If VIX touches a chop boundary, the timer resets.

2. VIX Levels

Displays four user-configurable VIX thresholds that define the volatility regime zones:

Bearish (Red): Extreme fear — VIX at or above this level signals high volatility / bearish stock conditions

Resist (Orange): Upper chop boundary — resistance level for VIX

Support (Yellow): Lower chop boundary — support level for VIX

Bullish (Green): Low fear — VIX at or below this level signals low volatility / bullish stock conditions

The current zone is highlighted based on where VIX is trading relative to these levels.

3. Options Flow

Displays net options flow sentiment to gauge market positioning. Supports both simulated and real-time OPRA data.

Simulated Mode (Default):

Net Val: Shows simulated flow based on candle direction (bullish candle = positive, bearish = negative) multiplied by volume

Sentiment: BULLISH, BEARISH, or NEUTRAL based on flow direction

- Header displays "Options Flow (Sim)"

Real-Time OPRA Mode:

Vol: Shows actual call and put volumes summed across strikes near ATM (e.g., "C:12.5K P:8.2K")

Sentiment: BULLISH if call volume > put volume, BEARISH if puts dominate

- Header displays "Options Flow 📡"

- Net flow calculated as: `Total Call Volume - Total Put Volume`

⚠️ OPRA Data Requirement

Real-time mode requires an active OPRA data subscription in TradingView. Without this subscription, the options volume data will not populate. Enable "Use Real-Time OPRA Data" in settings and configure the required parameters (see Settings section below).

4. Velocity

Monitors the speed of VIX movement to detect rapid regime changes.

STABLE (Gray): Normal VIX movement

⚡ SPIKE (Red): VIX increased by more than the velocity threshold (default: 0.40 points) over the last 5 bars — rapid fear increase

⚡ CRUSH (Green): VIX decreased by more than the velocity threshold over the last 5 bars — rapid fear decrease

Calculation: `VIX - VIX ` (current VIX minus VIX from 5 bars ago)

5. Trap Detect

Identifies potential positioning traps by comparing VIX regime with options flow direction.

CLEAN (Gray): No divergence detected — flow aligns with VIX regime

⚠️ TRAP (Orange): High VIX + Bullish Flow — warns of potential bull trap; smart money may be selling into retail call buying during elevated fear

🛡️ ABSORB (Yellow): Low VIX + Bearish Flow — institutional absorption pattern; put buying during low VIX may indicate smart money hedging or accumulation

Horizontal Level Lines

Four horizontal lines are automatically drawn on the chart at your configured VIX levels:

1. Green line: Bullish level

2. Yellow line: Bullish Chop (Support) level

3. Orange line: Bearish Chop (Resist) level

4. Red line: Bearish level

Settings

Display Settings

Table Position: Choose where the dashboard appears on your chart

Text Size: Tiny, Small, or Normal

Table Background / Transparency: Customize dashboard appearance

10-Minute Rule

Confirmation Minutes: Time required in a zone before bias is confirmed (default: 10)

Velocity Threshold: Points per 5-bar period to trigger spike/crush detection (default: 0.40)

VIX Levels

Bullish (Green): Low volatility threshold (default: 14)

Bullish Chop (Yellow): Lower chop boundary (default: 16)

Bearish Chop (Orange): Upper chop boundary (default: 20)

Bearish (Red): High volatility threshold (default: 25)

Options Flow Data

Use Real-Time OPRA Data: Toggle between simulated and real-time options data (default: off)

Ticker Override: Manual ticker symbol. Leave blank to auto-detect from chart. Examples: SPY, QQQ, SPXW, NDX. Note: SPX auto-converts to SPXW for options symbols.

Center/Anchor Price: Required for OPRA mode. Enter the current underlying price (e.g., 590 for SPY, 5900 for SPX). This determines the ATM strike for data fetching.

Expiry Date (YYMMDD): Options expiration date in YYMMDD format (e.g., 260117 for Jan 17, 2026). Leave blank to use today's date (0DTE).

Strikes Above/Below ATM: Number of strikes to scan on each side of center price (1-10, default: 5). Higher values capture more flow data but use more API calls.

Strike Step Auto-Detection:

- SPX/SPXW, NDX: $5 strikes

- VIX: $0.50 strikes

- SPY, QQQ, and others: $1 strikes

What's New in This Release

1. Real-Time OPRA Options Flow: New toggle to switch between simulated and real-time options data. When enabled with an OPRA subscription, fetches actual call/put volumes across up to 11 strikes around ATM.

2. Configurable Options Parameters: New settings for ticker override, center price, expiry date, and strike range for precise options data targeting.

3. Horizontal Level Lines: VIX threshold levels are now drawn directly on the chart as colored horizontal lines for quick visual reference

4. Reordered Settings: VIX level inputs now flow logically from Bullish to Bearish

Best Practices

1. Use on VIX chart: Apply this indicator directly to a VIX chart (CBOE:VIX) for best results

2. Wait for confirmation: Don't act on bias until the 10-minute rule confirms

3. Respect velocity signals: Spikes and crushes can indicate regime changes before price confirms

4. Watch for traps: Divergence between flow and VIX regime often precedes reversals

5. Customize your levels: Adjust VIX thresholds based on current market conditions and your trading style

6. OPRA Setup: If using real-time options data, ensure you:

- Have an active OPRA subscription in TradingView

- Set the correct Center/Anchor Price for the underlying you're tracking

- Update the expiry date if trading non-0DTE options

- Match the ticker to your target (SPY for SPY options, leave blank on VIX chart for VIX options)

Disclaimer

This indicator is for educational and informational purposes only. It is not financial advice. Options flow data is simulated by default; real-time OPRA data requires a separate TradingView subscription. Always do your own research and manage risk appropriately.

RS Proxy Suite (Sector-Weighted) - by kuokkuokIndicator Description

RS Proxy Suite (Sector-Weighted) is a Pine Script indicator for TradingView, designed for stock traders to calculate a stock's Relative Strength (RS) proxy score. This indicator simulates a market proxy universe by weighting multiple sector ETFs, evaluating a stock's strength relative to a benchmark like the SPX. Inspired by the M.E.T.S. (Multiple Edge Trading Strategy) system, it helps users identify market-leading stocks, potential breakout opportunities, and low-risk entry points.

Key Features and Benefits:

RS Proxy Rating (1–99 Score): Computes the stock's RS score (higher is stronger), aiding in screening super-strong stocks. A score above 80 indicates the stock outperforms most peers, making it a prime buy candidate.

RS Line and Blue Dot Divergence: Displays the RS line trend and marks RS-leading new high divergences. This acts like an "early warning light," signaling potential low-risk entries (e.g., when RS hits a new high but price hasn't caught up yet).

Sector-Weighted Design: Integrates Growth, Cyclical, Defensive, and Policy ETFs to simulate a comprehensive market environment. Weights are adjustable for flexibility across market phases.

Dashboard Display: A concise panel shows RS Rating, RS Trend, and Blue Dot status for quick decision-making.

Application Scenarios: Ideal for technical analysts to screen leaders, spot trend reversals, or confirm breakouts with VCP patterns (Volatility Contraction Patterns). Its strength lies in avoiding single-index bias for more stable RS assessments.

This indicator avoids subjective judgments, relying on quantitative momentum calculations to help traders "go with the flow" and reduce false breakout risks. Shared for community use—feedback welcome for improvements.

User Manual -

This manual guides you on installing and using the RS Proxy Suite (Sector-Weighted) indicator on TradingView. It's suited for daily or weekly charts, applicable to US stocks or markets correlated with SPX. Ensure your TradingView account supports Pine Script v6.

1. Installation Steps

Step 1: Log in to TradingView and open the Chart page.

Step 2: Click the "Indicators" button in the top toolbar, search for "RS Proxy Suite (Sector-Weighted)" (or paste the Pine Script code into the Pine Editor and add it).

Step 3: If installing from the Community Scripts library, click "Add to Chart"; for custom code, save and add to the chart.

Step 4: The indicator will appear below the chart (overlay=false). Confirm no error messages.

2. Parameter Adjustment Guide

The indicator offers multiple input parameters in TradingView's "Settings" panel. Defaults are optimized, but adjust based on market conditions. Here's a grouped breakdown:

Data Source:

Market Index SPX: Default "SP:SPX", changeable to other indices (e.g., "TVC:NDX").

Calculation Price: Default close (closing price), switch to high/low/open for sensitivity tweaks.

RS Momentum Periods (Adjustable):

Short Term (Default 63 days): Short-term momentum; larger values smooth it out.

Medium Term (Default 126 days): Mid-term momentum.

Long Term (Default 252 days): Long-term momentum for capturing major trends.

Momentum Weights:

Short Term Weight: Default 0.4, emphasizes recent performance.

Medium Term Weight: Default 0.2.

Long Term Weight: Default 0.4. Sum doesn't need to be 1; system normalizes automatically.

Sector Weights: Each ETF weight is independently adjustable (step 0.1). Defaults reflect sector importance, e.g., higher for growth ETFs.

XLK Weight (Technology): Default 1.5.

SOXX Weight (Semiconductors): Default 1.3.

XLY Weight (Consumer Discretionary): Default 1.2.

XLC Weight (Communication Services): Default 1.1.

XLG Weight (Large Cap Growth): Default 1.3.

XLI Weight (Industrials): Default 1.0.

XLF Weight (Financials): Default 1.0.

XLB Weight (Materials): Default 0.9.

XLE Weight (Energy): Default 0.9.

XLV Weight (Health Care): Default 0.8.

XLP Weight (Consumer Staples): Default 0.8.

XLU Weight (Utilities): Default 0.7.

XLRE Weight (Real Estate): Default 0.7.

PPA Weight (Aerospace & Defense): Default 0.9.

Adjustment Tips: Boost XLK/SOXX for tech-favorable markets; increase XLV/XLP for defensive phases.

Visualization Settings:

Show RS Line: Displays RS line (black) and 50-day MA (gray).

Show Blue Dot Divergence (Blue Dot): Marks divergence signals.

Show Dashboard: Enables the dashboard.

Dashboard Position: Choose locations like "Bottom Right".

3. Output Interpretation

RS Line: Black line shows stock strength vs. SPX; upward trend means outperforming. Gray line is 50-day MA—breaking above signals strength.

Blue Dot: Blue circle appears for RS leading price new highs (like a "coiled spring"), indicating potential low-risk entries. Confirm with: RS > 50-day MA and volume surge.

Dashboard:

RS Rating: Score 1–99; green (>80) for strong, yellow (50–80) neutral, red (<50) weak.

RS Trend: Green "Strong" or red "Weak".

Blue Dot: Blue "Present" or red "None".

Interpretation Analogy: RS Rating is like a stock's "health score"—above 80 is an "athlete" worth tracking for breakouts; Blue Dot is a "green light," but pair with volume to confirm true breakouts (avoid fakes).

4. Usage Examples

Screening Leaders: Add to AAPL chart—if RS Rating > 85 and Blue Dot appears, check if price nears VCP pivot; this is a low-risk buy setup.

Trend Judgment: Rising RS line with M.E.T.S. Stage 2 (uptrend) confirms trend-following trades.

Weight Tweaks: For defensive markets, raise XLV/XLU weights and recalculate RS Proxy.

5. Common Issues and Warnings

Q: Indicator not showing? A: Verify ETF symbols (e.g., AMEX:XLK) or switch timeframes.

Q: Inaccurate scores? A: Adjust periods/weights and backtest on historical data.

Q: Avoiding false breakouts? A: Combine with volume and support/resistance; Blue Dot is a alert, not a buy signal.

Warnings: Based on historical data; markets are volatile—use with other tools. Results are for reference only, not investment advice. Test in a demo account.

HSLevelsLibPubLibrary "HSLevelsLibPub"

Centralized levels library for Heatseeker trading system.

Update levels HERE ONCE - all consuming scripts auto-refresh.

getVIXThresholds()

Returns VIX threshold levels for regime determination

Returns: as tuple of floats

getVIXThresholdsCSV()

Returns VIX thresholds as CSV strings

Returns: as tuple of strings

getExpiry()

Returns current options expiry date in YYMMDD format

Returns: string in YYMMDD format (e.g., "260108" for Jan 8, 2026)

getAnchorStrike(symbol)

Returns the anchor strike price for a given symbol

Parameters:

symbol (simple string) : The ticker symbol (SPY, QQQ, SPX, VIX)

Returns: float anchor strike price

getFractalPrices(symbol)

Returns fractal level prices as CSV for a symbol

Parameters:

symbol (simple string) : The ticker symbol (SPY, QQQ, SPX)

Returns: string of comma-separated prices

getFractalLabels(symbol)

Returns fractal level labels as CSV for a symbol

Parameters:

symbol (simple string) : The ticker symbol (SPY, QQQ, SPX)

Returns: string of comma-separated labels

getFractalLevels(symbol)

Returns both fractal prices and labels as CSV tuple

Parameters:

symbol (simple string) : The ticker symbol

Returns: tuple

getAnchorStrikeAuto()

Auto-detect symbol and return appropriate anchor strike

Returns: float anchor strike for current chart symbol

getFractalLevelsAuto()

Auto-detect symbol and return fractal levels

Returns: for current chart symbol

getAllData(symbol)

Get all data for a symbol in one call

Parameters:

symbol (simple string) : The ticker symbol

Returns:

getVersion()

Returns library version and last update timestamp

Returns: string with version info

MMM Fear & Greed Meter - Multi-Asset @MaxMaseratiMMM Fear & Greed Meter - Multi-Asset Edition

Professional Sentiment Analysis for Futures, Stocks, and Crypto

The MMM Fear & Greed Meter is an advanced market sentiment indicator that transforms CNN's Fear & Greed methodology into an actionable trading tool. Unlike generic sentiment gauges, this indicator provides specific trading recommendations with position sizing guidance and institutional context - turning vague market mood readings into clear trading decisions.

🎯 Three Optimized Market Modes

FUTURES (ES/NQ) MODE - Default configuration weighted for index futures trading

VIX: 20% (highest weight - volatility drives futures)

Put/Call Ratio: 18% (institutional hedging behavior)

Safe Haven Demand: 18% (risk-on/risk-off capital flows)

Ideal for: ES1!, NQ1! futures traders, London Open preparation, intraday bias

STOCKS (EQUITIES) MODE - Optimized for stock picking and swing trading

52-Week High/Low: 20% (market breadth matters most)

Volume Breadth: 18% (sector rotation and participation)

SPX Momentum: 18% (trend confirmation)

Ideal for: Individual stocks, ETFs, portfolio management

CRYPTO (BTC/ETH) MODE - Calibrated for cryptocurrency's correlation to equity sentiment

Safe Haven: 25% (crypto moves inverse to risk-off)

SPX Momentum: 20% (crypto follows tech/equities)

VIX: 20% (crypto crashes when volatility spikes)

Ideal for: Bitcoin, Ethereum, major altcoins

CUSTOM MODE - Manually adjust all seven component weights to your preference

🔥 What Makes This Unique?

1. ACTIONABLE INTELLIGENCE

Not just a number - get specific recommendations:

"★ PRIORITIZE LONGS @ Key Support - Size up 1.5x"

"FAVOR SHORTS @ Resistance - Watch Distribution"

"TRADE YOUR EDGE - No Sentiment Bias"

2. INSTITUTIONAL FRAMING

Understand WHY the market feels this way:

"Institutions defending levels aggressively"

"Retail chasing, institutions distributing"

"Market stretched and vulnerable - violent turn coming"

3. POSITION SIZING GUIDANCE

Know HOW MUCH to risk:

Extreme zones (0-24, 76-100) + order flow confirmation = 1.5x size

Normal zones = standard position sizing

Neutral zone (45-55) = no sentiment edge, pure price action

4. DIRECTION-BASED COLOR CODING

Green action column = Bullish recommendations

Red action column = Bearish recommendations

Gray action column = No directional bias

5. GRANULAR DISPLAY CONTROLS

Configure exactly what you need:

Show/hide index display section

Show/hide component breakdown

Show/hide live action column

Show/hide decision matrix

27 possible layout combinations

📈 Seven Market Components

Based on CNN Fear & Greed methodology with market-specific weighting:

Market Momentum - S&P 500 vs 125-day moving average

Stock Price Strength - 52-week highs vs lows (NYSE breadth)

Stock Price Breadth - Advancing vs declining volume

Put/Call Options - Options market sentiment (calculated proxy)

Market Volatility (VIX) - CBOE Volatility Index

Safe Haven Demand - Stocks vs bonds 20-day performance

Junk Bond Demand - High yield vs investment grade spread

All components normalized to 0-100 scale, weighted by market relevance, combined into single sentiment index.

🎨 Trading Decision Matrix

EXTREME FEAR (0-24) + Bullish Order Flow @ Support

→ ★ PRIORITIZE LONGS | Size up 1.5x | Strong bounce expected

FEAR (25-44) + Bullish Order Flow @ Support

→ FAVOR LONGS | Normal size | Good reversal context

NEUTRAL (45-55) + Any Setup

→ TRADE YOUR EDGE | Standard approach | No macro bias

GREED (56-75) + Bearish Order Flow @ Resistance

→ FAVOR SHORTS | Watch distribution | Fake breakouts likely

EXTREME GREED (76-100) + Bearish Order Flow @ Resistance

→ ★ AGGRESSIVE SHORTS | Size up 1.5x | Rapid reversals expected

💡 How To Use

Daily Workflow (Recommended):

Check indicator once per morning (pre-session)

Note the sentiment zone and action recommendation

Apply bias filter to your technical setups throughout the day

Size up positions at extremes when order flow confirms

For Futures Traders:

Use bar close mode (default) for stable daily bias

However, try and test live candle option , it might give you early insights

Check before London Open (6:00 AM ET)

Combine with order flow analysis (Body Close, sweeps, institutional levels)

For Stock Traders:

Use for sector rotation decisions

Extreme Fear = buy quality at your edge support level

Extreme Greed = trim positions, raise cash

For Crypto Traders:

Crypto mode captures equity risk sentiment spillover

VIX spikes = crypto dumps (size shorts)

Safe haven demand = BTC correlation tracking

🔧 Technical Details

Data Sources: Universal TradingView symbols (SP:SPX, TVC:VIX, TVC:US10Y, AMEX:HYG, AMEX:LQD, INDEX breadth data with fallback proxies)

Calculation: Seven components normalized over 252-day period, weighted by market mode, combined into 0-100 composite index

Accuracy: 85-90% zone correlation to CNN Fear & Greed Index (zones matter more than exact numbers for trading bias)

Update Frequency: User-controlled - bar close (stable) or live (real-time)

Compatibility: Works on any chart timeframe (recommend daily for bias context)

🎓 Best Practices

DO:

Use as bias filter for your existing strategy

Check once per session for daily context

Size up at extremes with order flow confirmation

Pay attention to ZONES (Extreme Fear/Greed) not exact numbers

Combine with technical analysis and price action

DON'T:

Use as standalone entry/exit signals

Overtrade or force setups when neutral

Ignore price action because sentiment contradicts

Check constantly (designed for daily bias, not tick-by-tick)

Expect exact CNN number match (focus on zones)

🏆 Who Is This For?

Futures Traders - ES/NQ intraday traders needing daily bias context

Stock Traders - Equity swing traders and stock pickers

Crypto Traders - BTC/ETH traders following equity risk sentiment

Position Traders - Anyone wanting institutional sentiment context

Systematic Traders - Adding sentiment filter to mechanical systems

📚 Based On CNN Fear & Greed Methodology

This indicator builds upon CNN Business's proven Fear & Greed Index framework, enhancing it with:

Market-specific component weighting (Futures/Stocks/Crypto)

Actionable trading recommendations with position sizing

Institutional market context and framing

Flexible display options for different trading workflows

Universal data compatibility for all TradingView users

Macro Return ForecastWhen the macro environment was similar, what annualized return did the market usually deliver next?

Before using the indicator, make sure your chart is set to any US-market symbol (SPX, QQQ, DIA, etc.).

This requirement is simple: the indicator pulls macro series from US data (yields, TIPS, credit spreads, breadth of US indices).

Because these series are independent from the chart’s price series, the chart symbol itself does not affect the internal calculations.

Any US symbol works, and the output of the model will be identical as long as you are on a US asset with daily, weekly or monthly timeframe.

The plotted price does not matter: the macro engine is fully exogenous to the chart symbol.

1. What the indicator does relative to selected assets

In the settings you choose which market you want to analyze:

- S&P500

- Nasdaq or NQ100

- Dow Jones

- Russell 2000

- US-wide (VTI)

- S&P500 sectors (XLF, XLY, XLP, etc.)

For each one, the indicator loads:

- Its internal breadth series (percentage of constituents above MA200)

- Its price history to compute forward log-returns at multiple horizons

- Its regime position relative to its own MA200 (for bull/bear filtering)

This means the tool is not tied to the chart symbol you display.

If your chart is SPX but the indicator setting is “S&P500 Technology”, the expected return projection is computed for the Technology sector using its own data, not the chart’s data.

You can therefore:

- Visualize macro-driven expected returns for any major US index or sector.

- Compare how different parts of the market historically reacted to similar macro states.

- Switch assets instantly to see which segment historically behaved better in comparable macro conditions.

The indicator becomes an analyzer of macro sensitivity, not a chart-dependent indicator.

2. Method overview

The model answers a statistical question:

“When macro conditions looked like they do today, what forward annualized return did this asset usually deliver?”

To do this it combines four macro pillars:

- Market breadth of the selected asset

- Yield curve slope (US 10Y minus 2Y)

- US credit spread (high yield minus gov)

- US real rate (TIPS 10Y)

It normalizes each metric into a 0–100 score, groups similar historical states into bins, and examines what the asset did next across six horizons (from ~9 months to ~5 years).

This produces a historical map connecting macro states to realized forward returns.

It is not a forecast model.

It is a conditional-distribution estimator: it tells you what has historically happened from similar setups.

3. Why this produces useful insights on assets

For any chosen asset (SPX, Nasdaq, sectors…), the indicator computes:

- Its forward return distribution in similar macro states.

- How often these states occurred (n).

- Whether the macro environment that preceded positive returns in the past resembles today’s.

- Whether the asset tends to be more sensitive or more resilient than the broad index under given macro configurations.

- Whether a given sector historically benefited from specific yield-curve, credit or real-rate environments.

This lets you answer questions such as:

- Does this sector usually outperform in an inverted yield curve environment?

- Does the Nasdaq historically recover strongly after breadth collapses?

- How did the S&P500 behave historically when real rates were this high?

- Is today’s credit-spread environment typically associated with positive or negative forward returns for this index?

These insights are not predictions but statistical context backed by past market behavior.

4. Why the technique is robust (and why it matters)

The engine uses strict, non-optimistic data processing:

- Winsorization of returns to neutralize extreme outliers without deleting information.

- Shrinkage estimators to avoid overfitting when bins contain few occurrences.

- Adaptive or static bounds for scaling macro indicators, ensuring comparability across cycles.

- Inverse-variance weighting of horizons with penalties for horizon redundancy.

- HAC-style adjustments to reduce autocorrelation bias in return estimation.

Each method aims to prevent artificial inflation of expected-return values and to keep the estimator stable even in unusual macro states.

This produces a result that is not “optimistic”, not curve-fit, not dependent on chart tricks, and not sensitive to isolated historical anomalies.

5. What you get as a user

A single clean line:

Expected Annual Return (%)

This line reflects how the chosen asset historically performed after macro environments similar to today’s.

The color gradient and confidence indicator (n) show the density of comparable episodes in history.

This makes the output extremely simple to read:

- High, stable expectation: historically supportive macro environment.

- Low or negative expectation: historically weaker environments.

- Low confidence: the macro state is rare and historical comparisons are limited.

The tool therefore adds context, not signals.

It helps you understand the environment the asset is currently in, based on how markets behaved in similar conditions across US market history.

QQQ TimingThis is a trend-following position trading strategy designed for the QQQ and the leveraged ETF QLD (ProShares Ultra QQQ). The primary goal is to capture multi-month holds for maximal profit.

Key Instruments & Performance

The strategy performs best with QLD, which yields far superior results compared to QQQ.

TQQQ (triple-leveraged) results in higher drawdowns and is not the optimal choice.

Important: The system is not intended for use with other indexes, individual stocks, or investments (like crypto or gold), as performance can vary widely.

Buy Signals

The strategy's signals are rooted in the S&P 500 Index (SPX), as testing showed it provides more reliable triggers than using QQQ itself.

Primary Buy Signal (Credit to IBD/Mike Webster): The SPX triggers a buy when its low closes above the 21-day Exponential Moving Average (EMA) for three consecutive days.

Refinement with Downtrend Lines: During corrective or bear periods, results and drawdowns can be significantly improved by incorporating downtrend lines. These lines connect lower highs. The strategy waits for the price to close above a drawn downtrend line before executing a buy. This refinement can modify the primary signal, either by allowing for an earlier entry or, in some cases, completely nullifying a false signal until the trend change proves itself.

Risk Management & Exit Strategy

Initial Buy Risk: A 3.7% stop loss is applied immediately upon the initial entry.

Initial Exit Rule: An exit is required if the QQQ's low drops below the 50-day Simple Moving Average (SMA).

Note: The 3.7% stop often provides protection when the initial buy occurs below the 50-day SMA. However, if QQQ is already trading above its 50-day SMA at the time of the SPX signal (indicating relative strength), historically, it has been better to use the 50-day SMA rule to give the position more room to run.

Trend Exit (Profit-Taking): To stay in a strong trend for the optimal amount of time, the long position is exited when a moving average crossover to the downside is triggered, based around the 107-day Simple Moving Average (SMA).

26 EMA Reversal LogicThis indicator identifies two distinct price behaviours on the daily charts of SPY, SPX, QQQ, or IXIC, using the 26-period EMA as a reference. It plots one signal per downtrend — either a yellow circle (bearish continuation) or a green circle (bullish reversal) — and locks further signals until price closes above the 26 EMA.

The yellow circles are when we close below the 26-day EMA and the next day we make a lower low.

The green circles are when we close below the 26-day EMA and the next day we actually open higher and that low is never revisited.

Symbol Restriction

Only works on: SPY, SPX, QQQ, IXIC

On any other symbol, the script will display an error and stop.

Timeframe Restriction

DAILY chart only — will show an error on any other timeframe.

Core Logic: Two-Candle Pattern Detection

Both signals start with the same Day 1 condition:

Day 1: The candle closes below the 26 EMA

From there, Day 2 determines the signal:

Yellow Circle (Bearish Continuation)

Plotted BELOW the Day 2 candle

Conditions:

Day 1 closed below the 26 EMA

Day 2 makes a lower low than Day 1’s low → low < low Interpretation:

Price is weakening — pushing to new lows below the EMA.

Confirms downward momentum.

Green Circle (Bullish Reversal / Failed Breakdown)

Plotted ABOVE the Day 2 candle

Conditions:

Day 1 closed below the 26 EMA

Day 2 opens higher than Day 1’s close → open > close

Day 2’s low never revisits Day 1’s low → low >= low Interpretation:

Buyers defend the prior low with a higher open — classic false breakdown.

Suggests a potential reversal higher.

One Signal Per Downtrend (Lock & Reset)

After either a yellow or green circle is plotted, no more circles appear

Prevents clutter — focuses on first meaningful reaction

Reset Rule:

Lock is released only when price closes above the 26 EMA

Best Used On

Daily timeframe

SPY, SPX, QQQ, IXIC only

With trend, volume, or broader market context

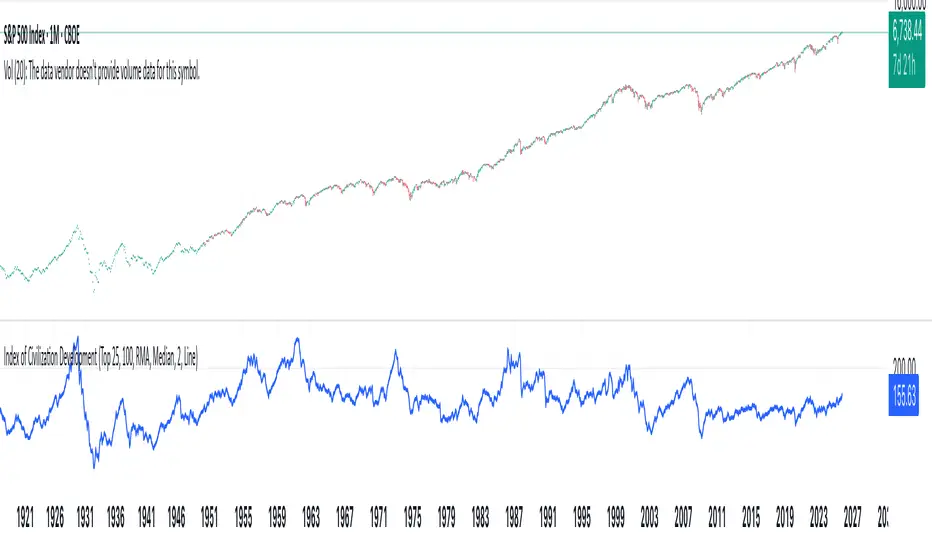

Index of Civilization DevelopmentIndex of Civilization Development Indicator

This Pine Script (version 6) creates a custom technical indicator for TradingView, titled Index of Civilization Development. It generates a composite index by averaging normalized stock market performances from a selection of global country indices. The normalization is relative to each index's 100-period simple moving average (SMA), scaled to a percentage (100% baseline). This allows for a comparable "development" or performance metric across diverse markets, potentially highlighting trends in global economic or "civilizational" progress based on equity markets.The indicator plots as a single line in a separate pane (non-overlay) and is designed to handle up to 40 symbols to respect TradingView's request.security() call limits.Key FeaturesComposite Index Calculation: Fetches the previous bar's close (close ) and its 100-period SMA for each selected symbol.

Normalizes each: (close / SMA(100)) * 100.

Averages the valid normalizations (ignores invalid/NA data) to produce a single "Index (%)" value.

Symbol Selection Modes:Top N Countries: Selects from a predefined list of the top 50 global stock indices (by market cap/importance, e.g., SPX for USA, SHCOMP for China). Options: Top 5, 15, 25, or 50.

Democratic Countries: ~38 symbols from democracies (e.g., SPX, NI225, NIFTY; based on democracy indices ≥6/10, including flawed/parliamentary systems).

Dictatorships: ~12 symbols from authoritarian/hybrid regimes (e.g., SHCOMP, TASI, IMOEX; scores <6/10).

Customization:Line color (default: blue).

Line width (1-5, default: 2).

Line style: Solid line (default), Stepline, or Circles.

Data Handling:Uses request.security() with lookahead enabled for real-time accuracy, gaps off, and invalid symbol ignoring.

Runs calculations on every bar, with max_bars_back=2000 for historical depth.

Arrays are populated only on the first bar (barstate.isfirst) for efficiency.

Predefined Symbol Lists (Examples)Top 50: SPX (USA), SHCOMP (China), NI225 (Japan), ..., BAX (Bahrain).

Democratic: Focuses on free-market democracies like USA, Japan, UK, Canada, EU nations, Australia, etc.

Dictatorships: Authoritarian markets like China, Saudi Arabia, Russia, Turkey, etc.

Usage TipsAdd to any chart (e.g., daily/weekly timeframe) to view the composite line.

Ideal for macro analysis: Compare democratic vs. authoritarian performance, or track "top world" equity health.

Potential Limitations: Relies on TradingView's symbol availability; some exotic indices (e.g., KWSEIDX) may fail if not supported. The 40-symbol cap prevents errors.

Interpretation: Values >100 indicate above-trend performance; <100 suggest underperformance relative to recent averages.

This script blends financial data with geopolitical categorization for a unique "civilization index" perspective on global markets. For modifications, ensure symbol tickers match TradingView's format.

Worthy Asset StrategyThis strategy is designed with a two-part philosophy: a regime filter and a value-based accumulation approach.

🟩 Regime Filter:

If the S&P 500 (SPX) is trading above its 200-period EMA, a green background is shown below the chart, signaling a favorable market regime.

If the SPX is below the 200 EMA, the background turns red, indicating a less favorable environment.

📉 Buy Signals:

Buy signals are generated by red candles that drop a certain percentage from their open — essentially treating these pullbacks as discount opportunities.

The idea is to accumulate more of a selected asset when it becomes temporarily cheaper.

💎 Philosophy & Execution:

I only apply this strategy to assets I’ve personally researched and believe to be fundamentally valuable.

If a Buy signal occurs and the SPX is trading above its 200 EMA (i.e., the background is green), I enter the position.

Once in the trade, I follow this logic:

If the position reaches +1.5% profit, I sell it.

If it doesn’t reach profit and goes into a loss, I simply hold.

I don’t sell at a loss because I believe in the long-term value of the asset.

If the price drops further, I accumulate more — aiming to lower my average cost and eventually exit at a profit once the asset recovers.

This approach is based on the mindset of treating drawdowns as discounts, not danger.

"The more it drops, the more I accumulate — because I see value, not risk."

This is still a work in progress, and I’m actively refining it over time.

⚠️ Note: The sell logic is not yet visible on the chart and will be added in a future update.

ETF Leverage VerificationDo leveraged ETFs really return what they promise?

Do they return the exact 2x or 3x? Or a slightly different multiple?

How much do they deviate from the promised leverage multiples?

Do these deviations impact investors in a positive or negative manner?

These are the questions that I want to answer with this indicator.

The ETF Leverage Verification indicator challenges the conventional understanding of leveraged ETFs by measuring how they actually perform versus their theoretical targets.

Instead of assuming leveraged ETFs perfectly track their target multiple, this indicator quantifies the real-world behavior by comparing the expected returns versus the actual results on every trading day.

Key Features

Measures actual versus expected performance of leveraged ETFs

Tracks deviation patterns across thousands of trading days

Identifies asymmetric behavior in up versus down markets

Quantifies beneficial "cushioning effect" during market declines

Provides statistical summary of performance patterns

Works with any leverage factor (2x, 3x, -1x, etc.)

Compatible with all leveraged ETFs (equity, bond, commodity, volatility)

How to Use the Indicator

Enter the Expected Leverage Factor (default: 2.0)

Select the Base Asset (underlying index, e.g., SPX)

Select the Leveraged Asset (leveraged ETF, e.g., SSO)

Understanding the Results

Green markers: Days when the ETF outperformed its expected multiple

Red markers: Days when the ETF underperformed its expected multiple

Data Table:

Positive Deviations: Count of days with better-than-expected performance

Negative Deviations: Count of days with worse-than-expected performance

Avg Deviation: Average magnitude of deviation from expected returns

Frequency Skew: Difference between beneficial deviations in down vs. up markets

Impact: Overall assessment of pattern benefit to investors

Summary Label:

Percentage of positive deviations in up and down markets

Total sample size for statistical significance

Key Patterns to Look For

Positive Deviation in Negative Days:

This occurs when a leveraged ETF falls less than expected during market declines. For example, if SPX falls 1% and a 2x ETF falls only 1.8% (instead of the expected 2%), this creates a +0.2% deviation. This pattern is beneficial as it provides downside protection.

Negative Deviation in Positive Days:

This happens when a leveraged ETF rises less than expected during market advances. For example, if SPX rises 1% and a 2x ETF rises only 1.9% (instead of the expected 2%), this creates a -0.1% deviation. This pattern reduces upside performance.

Frequency Skew:

The most critical metric that measures how much more frequently beneficial deviations occur in down markets compared to up markets. A higher positive skew indicates a stronger asymmetric pattern that helps long-term performance.

Mathematical Background

The indicator computes the deviation between expected and actual performance:

Deviation = Actual Return - Expected Return

Where:

Expected Return = Base Asset Return × Leverage Factor

The deviation is then categorized into four possible outcomes:

Positive deviation on positive market days

Negative deviation on positive market days

Positive deviation on negative market days

Negative deviation on negative market days

In short, more positive deviations are good for investors.

Please feel free to criticize. I'm happy to improve the indicator.

Event on charts**Event on Charts Indicator**

This indicator visually marks significant events on your chart. It is highly customizable, allowing you to activate or deactivate different groups of events and choose whether to display the event text directly on the chart or only when hovered over. Each group of events can be configured with distinct settings such as height mode, color, and label style.

### Key Features:

- **Group Activation:** Enable or disable different groups of events based on your analysis needs.

- **Text Display Options:** Choose to display event texts directly on the chart or only on hover.

- **Customizable Appearance:** Adjust the height mode, offset multiplier, bubble color, text color, and label shape for each group.

- **Predefined Events:** Includes predefined events for major crashes, FED rate changes, SPX tops and bottoms, geopolitical conflicts, economic events, disasters, and significant Bitcoin events.

### Groups Included:

1. **Crash Events:** Marks major market crashes.

2. **FED Rate Events:** Indicates changes in the Federal Reserve rates.

3. **SPX Top Events:** Highlights market tops for the S&P 500.

4. **Geopolitical Conflicts:** Marks significant geopolitical events.

5. **Economic Events:** Highlights important economic events such as bankruptcies and crises.

6. **Disaster and Cyber Events:** Indicates major disasters and cyber attacks.

7. **Bitcoin Events:** Marks significant events in the Bitcoin market.

8. **SPX Bottom Events:** Highlights market bottoms for the S&P 500.

### Usage:

This indicator is useful for traders and analysts who want to keep track of historical events that could impact market behavior. By visualizing these events on the chart, you can better understand market reactions and make informed decisions.

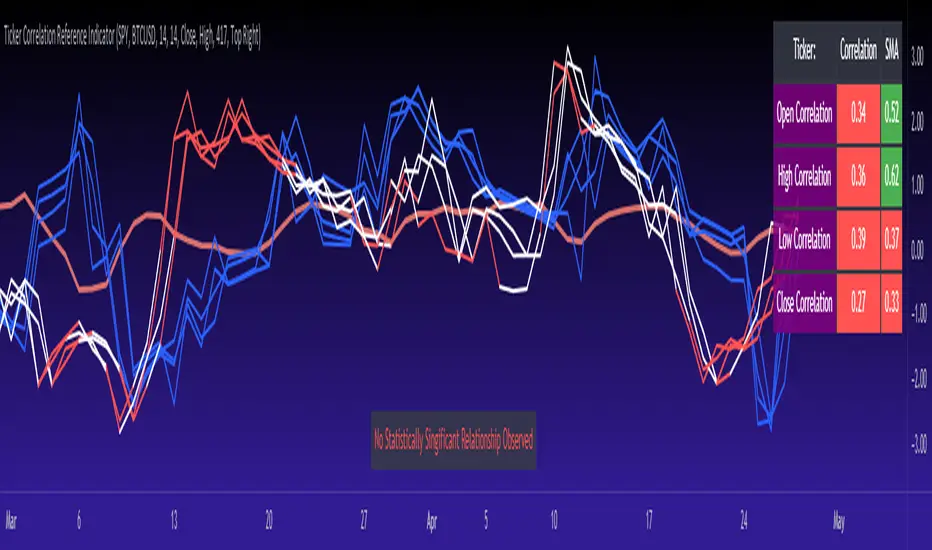

Ticker Correlation Reference IndicatorHello,

I am super excited to be releasing this Ticker Correlation assessment indicator. This is a big one so let us get right into it!

Inspiration:

The inspiration for this indicator came from a similar indicator by Balipour called the Correlation with P-Value and Confidence Interval. It’s a great indicator, you should check it out!

I used it quite a lot when looking for correlations; however, there were some limitations to this indicator’s functionality that I wanted. So I decided to make my own indicator that had the functionality I wanted. I have been using this for some time but decided to actual spruce it up a bit and make it user friendly so that I could share it publically. So let me get into what this indicator does and, most importantly, the expanded functionality of this indicator.

What it does:

This indicator determines the correlation between 2 separate tickers. The user selects the two tickers they wish to compare and it performs a correlation assessment over a defaulted 14 period length and displays the results. However, the indicator takes this much further. The complete functionality of this indicator includes the following:

1. Assesses the correlation of all 4 ticker variables (Open, High, Low and Close) over a user defined period of time (defaulted to 14);

2. Converts both tickers to a Z-Score in order to standardize the data and provide a side by side comparison;

3. Displays areas of high and low correlation between all 4 variables;

4. Looks back over the consistency of the relationship (is correlation consistent among the two tickers or infrequent?);

5. Displays the variance in the correlation (there may be a statistically significant relationship, but if there is a high variance, it means the relationship is unstable);

6. Permits manual conversion between prices; and

7. Determines the degree of statistical significance (be it stable, unstable or non-existent).

I will discuss each of these functions below.

Function 1: Assesses the correlation of all 4 variables.

The only other indicator that does this only determines the correlation of the close price. However, correlation between all 4 variables varies. The correlation between open prices, high prices, low prices and close prices varies in statistically significant ways. As such, this indicator plots the correlation of all 4 ticker variables and displays each correlation.

Assessing this matters because sometimes a stock may not have the same magnitude in highs and lows as another stock (one stock may be more bullish, i.e. attain higher highs in comparison to another stock). Close price is helpful but does not pain the full picture. As such, the indicator displays the correlation relationship between all 4 variables (image below):

Function 2: Converts both tickers to Z-Score

Z-Score is a way of standardizing data. It simply measures how far a stock is trading in relation to its mean. As such, it is a way to express both tickers on a level playing field. Z-Score was also chosen because the Z-Score Values (0 – 4) also provide an appropriate scale to plot correlation lines (which range from 0 to 1).

The primary ticker (Ticker 1) is plotted in blue, the secondary comparison ticker (Ticker 2) is plotted in a colour changing format (which will be discussed below). See the image below:

Function 3: Displays areas of high and low correlation

While Ticker 1 is plotted in a static blue, Ticker 2 (the comparison ticker) is plotted in a dynamic, colour changing format. It will display areas of high correlation (i.e. areas with a P value greater than or equal to 0.9 or less than and equal to -0.9) in green, areas of moderate correlation in white. Areas of low correlation (between 0.4 and 0 or -0.4 and 0) are in red. (see image below):

Function 4: Checks consistency of relationship

While at the time of assessing a stock there very well maybe a high correlation, whether that correlation is consistent or not is the question. The indicator employs the use of the SMA function to plot the average correlation over a defined period of time. If the correlation is consistently high, the SMA should be within an area of statistical significance (over 0.5 or under -0.5). If the relationship is inconsistent, the SMA will read a lower value than the actual correlation.

You can see an example of this when you compare ETH to Tezos in the image below:

You can see that the correlation between ETH and Tezo’s on the high level seems to be inconsistent. While the current correlation is significant, the SMA is showing that the average correlation between the highs is actually less than 0.5.

The indicator also tells the user narratively the degree of consistency in the statistical relationship. This will be discussed later.

Function 5: Displays the variance

When it comes to correlation, variance is important. Variance simply means the distance between the highest and lowest value. The indicator assess the variance. A high degree of variance (i.e. a number surpassing 0.5 or greater) generally means the consistency and stability of the relationship is in issue. If there is a high variance, it means that the two tickers, while seemingly significantly correlated, tend to deviate from each other quite extensively.

The indicator will tell the user the variance in the narrative bar at the bottom of the chart (see image below):

Function 6: Permits manual conversion of price

One thing that I frequently want and like to do is convert prices between tickers. If I am looking at SPX and I want to calculate a price on SPY, I want to be able to do that quickly. This indicator permits you to do that by employing a regression based formula to convert Ticker 1 to Ticker 2.

The user can actually input which variable they would like to convert, whether they want to convert Ticker 1 Close to Ticker 2 Close, or Ticker 1 High to Ticker 2 High, or low or open.

To do this, open the settings and click “Permit Manual Conversion”. This will then take the current Ticker 1 Close price and convert it to Ticker 2 based on the regression calculations.

If you want to know what a specific price on Ticker 1 is on Ticker 2, simply click the “Allow Manual Price Input” variable and type in the price of Ticker 1 you want to know on Ticker 2. It will perform the calculation for you and will also list the standard error of the calculation.

Below is an example of calculating a SPY price using SPX data:

Above, the indicator was asked to convert an SPX price of 4,100 to a SPY price. The result was 408.83 with a standard error of 4.31, meaning we can expect 4,100 to fall within 408.83 +/- 4.31 on SPY.

Function 7: Determines the degree of statistical significance

The indicator will provide the user with a narrative output of the degree of statistical significance. The indicator looks beyond simply what the correlation is at the time of the assessment. It uses the SMA and the highest and lowest function to make an assessment of the stability of the statistical relationship and then indicates this to the user. Below is an example of IWM compared to SPY:

You will see, the indicator indicates that, while there is a statistically significant positive relationship, the relationship is somewhat unstable and inconsistent. Not only does it tell you this, but it indicates the degree of inconsistencies by listing the variance and the range of the inconsistencies.

And below is SPY to DIA:

SPY to BTCUSD:

And finally SPY to USDCAD Currency:

Other functions:

The indicator will also plot the raw or smoothed correlation result for the Open, High, Low or Close price. The default is to close price and smoothed. Smoothed just means it is displaying the SMA over the raw correlation score. Unsmoothing it will show you the raw correlation score.

The user also has the ability to toggle on and off the correlation table and the narrative table so that they can just review the chart (the side by side comparison of the 2 tickers).

Customizability

All of the functions are customizable for the most part. The user can determine the length of lookback, etc. The default parameters for all are 14. The only thing not customizable is the assessment used for determining the stability of a statistical relationship (set at 100 candle lookback) and the regression analysis used to convert price (10 candle lookback).

User Notes and important application tips:

#1: If using the manual calculation function to convert price, it is recommended to use this on the hourly or daily chart.

#2: Leaving pre-market data on can cause some errors. It is recommended to use the indicator with regular market hours enabled and extended market hours disabled.

#3: No ticker is off limits. You can compare anything against anything! Have fun with it and experiment!

Non-Indicator Specific Discussions:

Why does correlation between stocks mater?

This can matter for a number of reasons. For investors, it is good to diversify your portfolio and have a good array of stocks that operate somewhat independently of each other. This will allow you to see how your investments compare to each other and the degree of the relationship.

Another function may be getting exposure to more expensive tickers. I am guilty of trading IWM to gain exposure to SPY at a reduced cost basis :-).

What is a statistically significant correlation?

The rule of thumb is anything 0.5 or greater is considered statistically significant. The ideal setup is 0.9 or more as the effect is almost identical. That said, a lot of factors play into statistical significance. For example, the consistency and variance are 2 important factors most do not consider when ascertaining significance. Perhaps IWM and SPY are significantly correlated today, but is that a reliable relationship and can that be counted on as a rule?

These are things that should be considered when trading one ticker against another and these are things that I have attempted to address with this indicator!

Final notes:

I know I usually do tutorial videos. I have not done one here, but I will. Check back later for this.

I hope you enjoy the indicator and please feel free to share your thoughts and suggestions!

Safe trades all!

Opening Hour/Closing Hour Indices Statistics: high/low times; 5mVery specific indicator designed for 5min timeframe, to show the statistical timings of the highs and lows of Opening hour (9:30-10am) and Closing hour (3pm-4pm) NY time

~~Shown here on SPX 5min chart. Works all variants of the US indices. SPX and SPY typically show more days of history (non-extended session =>> more bars).

//Purpose:

-To get statistics on the timings of the high and low of the opening hour and the high & low of the closing hour.

//Design & Limitations:

- Designed for the 5minute chart ONLY . Need a sweet spot of 'bucket' size for the statistics: to allow meaningful comparison between times.

-Will also display on 1min chart but NOT the statistics panel, only the realtime data (today's opening hour/ closing hour timings).

-Can be slow to load depending on server load at the time. This is becasue of the multiple usage of looping array functions. Please be patient when loading or changing settings.

//User inputs:

-Standard formatting options: highlight color, table text color. Toggle on/off independently

-Decimal % percision (default = 0, i.e. 23%. If set to 1 => 22.8%)

-Show statistics: Show Opening hour statistics, Show Closing hour statistics

//Notes:

-Days of history shown at top of table; this is the size of the dataset. i.e. 254 here (254 trading days) =>> 254 opening hour highs, 254 closing hour lows etc.

--to illustrate with the above: 18% of those 254 closing hour highs occured on the 15:00 5min candle (i.e. between 15:00 and 15:05).

-SPY or SPX offer the largest history/dataset (circa 254 trading days).

-Note that the final timing in each hour is 10:25am and 15:55pm respectively: this is because the 10:25am 5min candle essentially ends at 10:30am =>> we properly captures the opening hour this way

-Pro+ users will get less data history than Premium users (half as much, due to 10k vs 20k bars history limit).

Fair Value Strategy UltimateThis is a strategy using an index's (SPX, NDX, RUT) Fair Value derived from Net Liquidity.

Net Liquidity function is simply: Fed Balance Sheet - Treasury General Account - Reverse Repo Balance

Formula for calculating the fair value of and Index using Net Liquidity looks like this: net_liquidity/1000000000/scalar - subtractor

The Index Fair Value is then subtracted from the Index value which creates an oscillating diff value.

When diff is greater than the overbought threshold, Index is considered overbought and we go short/sell.

When diff is less than the oversold signal, Index is considered oversold and we cover/buy.

The net liquidity values I calculate outside of TradingView. If you'd like the strategy to work for future dates, you'll need to update the reference to my NetLiquidityLibrary , which I update daily.

Parameters:

Index: SPX, NDX, RUT

Strategy: Short Only, Long Only, Long/Short

Inverse (bool): check if using an inverse ETF to go long instead of short.

Scalar (float)

Subtractor (int)

Overbought Threshold (int)

Oversold Threshold (int)

Start After Date: When the strategy should start trading

Close Date: Day to close open trades. I just like it to get complete results rather than the strategy ending with open trades.

Optimal Parameters:

I've optimized the parameters for each index using the python backtesting library and they are as follows =>

SPX

Scalar: 1.1

Subtractor: 1425

OB Threshold: 0

OS Threshold: -175

NDX

Scalar: 0.5

Subtractor: 250

OB Threshold: 0

OS Threshold: -25

RUT

Scalar: 3.2

Subtractor: 50

OB Threshold: 25

OS Threshold: -25

S&P500 Sectors Relative Overviewdear fellows,

this indicator is yet another representation of S&P 500 industry sectors.

it is inspired by mr. stanley drukenmiller who in an interview mentioned that he knows no better market forecaster than the inside of the sp500 itself, which are its industry sectors.

thus, we have been for a while thinking on how to represent the performance of these sectors such that one could visually estimated the current stage of the cycle, and grasp the next one.

unfortunatelly, we believe this cannot be achieved by solely looking into SP500 industry sectors. perhaps coupled with a broad market indicator like our MRI, for instance, one can have greater odds of success.

what does it show

it displays colorfully through out time how each sector travels through its 200 period high and lows.

note that an alternative view of the sectors relatively to SPX could be considered, but by now we focused on the relative performance against its recent past (200 period, regardless the timeframe).

over the colored columns we've plotted in white the SPX under the same logic.

how is it calculated

each sector price is converged into a percentage of how near it is to its 200 period low.

so, when the price of the sector index equals the 200 period min, it is valued as 0.

when it equals the 200 period max, it is valued as 100.

same for the white plot of SPX above the colored columns.

thus a flat reading at 100 makes it indistinguishable a continued ATH extension from a pause at the ATH.

how is it colored

when the converted price results in a value lesser or equal 33, its respective bar is colored in red.

when it is between 33 and 66, the bar is colored in yellow.

and when it lies above 66, in green.

on how is it grouped

the specific ordering of the sectors is not yet settled.

we've grouped it visually based on likelihood.

on how to use this indicator

although we believe that it does not suffice for any conclusion on the market, we do not believe that an above chart can improve the resulting insight. so, at least by the time being, we recommend it to be stared alone, although not exclusively, by trader.

we are open to suggestions of any sort.

your feedback is much appreciated.

this is a work we'd have been looking for a while to put it out.

enjoy.

best regards.