1 Triple EMA Crossover Strategy (x, 3x, 9x)An excellent EMA strategy.

x, 3x, and 9x: These represent the periods of the EMAs. For example, if 'x' is 10, then you would have a 10-day EMA, a 30-day EMA, and a 90-day EMA.

Crossover: The strategy relies on identifying when the price or the shorter-term EMAs cross above or below the longer-term EMAs, signaling potential buy or sell opportunities.

How the Strategy Works:

1. Trend Identification:

The relationship between the three EMAs indicates the overall trend. If the 3x EMA is above the 9x EMA, and the x EMA is above both, it suggests an uptrend. Conversely, if the 3x EMA is below the 9x EMA, and the x EMA is below both, it indicates a downtrend.

2. Buy Signals:

A buy signal might be generated when the shortest EMA (x) crosses above the medium EMA (3x) and then both cross above the longest EMA (9x), suggesting a potential breakout.

3. Sell Signals:

A sell signal might be generated when the shortest EMA (x) crosses below the medium EMA (3x) and then both cross below the longest EMA (9x), suggesting a potential breakdown.

---------------------------------------------------------------------------------------------------------

Unlocking Trends with the Triple EMA Crossover Strategy (x, 3x, 9x)

Welcome to an intuitive yet powerful trend-following strategy designed for clarity and actionable signals: the Triple EMA Crossover. This Pine Script® indicator leverages the Exponential Moving Average (EMA) to help traders identify prevailing trends, potential breakouts, and breakdowns with enhanced precision. Built on a simple, scalable 'x, 3x, 9x' methodology, it provides a dynamic framework for navigating market movements.

Understanding the x, 3x, 9x EMA Foundation

At its core, this strategy utilizes three Exponential Moving Averages, each acting as a distinct lens on price action. Unlike Simple Moving Averages (SMAs) which give equal weight to all data points, EMAs place a greater emphasis on recent prices, making them more responsive to current market conditions—a crucial advantage in fast-paced environments like intraday trading.

The "x, 3x, 9x" nomenclature is elegantly simple:

x EMA (Fast EMA): This is your shortest-period EMA, highly sensitive to immediate price changes. It acts as the leading indicator, quickly reacting to shifts in momentum.

3x EMA (Medium EMA): Calculated with three times the 'x' period, this EMA provides a smoother, yet still responsive, view of the short-to-medium term trend. It often acts as dynamic support or resistance.

9x EMA (Slow EMA): Representing nine times the 'x' period, this is your longest EMA. It filters out much of the market noise, giving you a clear picture of the underlying dominant trend.

The beauty of this setup lies in its adaptability. By simply adjusting the Base EMA Period (x) input in the script settings, you can automatically calibrate all three EMAs to suit different instruments, volatility levels, or even your preferred trading style. A common starting point for 'x' in intraday trading on a 5-minute chart is 10, which translates to 10, 30, and 90-period EMAs.

How the Strategy Works: Signals and Trend Identification

The power of the Triple EMA Crossover lies in the interplay and alignment of these three moving averages.

1. Trend Identification

The relative positioning of the EMAs paints a clear picture of the market's trend:

Uptrend (Bullish): When the emaX (fast) is above the ema3X (medium), and the ema3X is, in turn, above the ema9X (slow), it indicates a strong bullish trend. This "stacked" alignment suggests robust upward momentum.

Downtrend (Bearish): Conversely, if the emaX (fast) is below the ema3X (medium), and the ema3X is below the ema9X (slow), it signals a clear bearish trend.

2. Buy Signals 🟢

A buy signal is generated when the swift emaX crosses above the ema3X, AND simultaneously, the ema3X is already above the ema9X. This combined condition ensures that the shorter-term momentum is shifting upward while the underlying medium-term trend remains strong and aligned with the longer-term direction. This reduces false signals often seen with simple two-EMA crossovers, aiming to capture high-probability upward moves. The script will plot a green upward-pointing triangle below the candle to visually alert you to this entry.

3. Sell Signals 🔴

A sell signal occurs when the quick emaX crosses below the ema3X, AND the ema3X is already below the ema9X. This indicates that the short-term momentum is shifting downwards, confirming a bearish bias within the broader downtrend. This comprehensive confirmation helps identify potential breakdowns and exit points for long positions or entry points for short trades. A red downward-pointing triangle will appear above the candle to mark this signal.

The strategy also includes an intuitive exit mechanism: if a buy signal is active and a sell condition is met, the long position will be closed, and vice-versa for short positions. This ensures you're always aligned with the most recent confirmed trend direction.

Key Advantages for Traders

Clarity: Provides visually clear trend direction and momentum shifts.

Responsiveness: EMAs react faster to price changes compared to SMAs, making them ideal for dynamic markets.

Confirmation: The three-EMA alignment significantly reduces false signals, leading to higher-conviction trades.

Adaptability: The x input allows you to fine-tune the strategy for various assets and market conditions.

Simplicity: Despite its effectiveness, the logic remains straightforward and easy to understand.

Important Considerations for Day Trading

For optimal performance in intraday trading, it's highly recommended to apply this strategy on a 5-minute chart. This timeframe strikes the perfect balance between capturing rapid price action and filtering out excessive market noise, allowing the EMA crossovers to provide meaningful signals. Always combine this technical analysis with sound risk management, including stop-loss orders, and consider other indicators or fundamental analysis for further confirmation.

Customization and Disclaimer

Feel free to experiment with the Base EMA Period (x) input to find the optimal settings that resonate with your trading style and the specific instruments you trade. Remember, no single strategy guarantees profits, and past performance is not indicative of future results. This script is provided for educational and illustrative purposes. Always conduct your own research and risk assessment before trading with real capital. Happy Trading!

"the strat"に関するスクリプトを検索

Candle stick pattern strategy - No EMA 5MTFOverview

This strategy is designed to maximize trade frequency by identifying an expanded range of high-probability candlestick reversal patterns. It is an unfiltered system, meaning it will act on every valid signal it finds on the 5min timeframe, making it a very active strategy.

The core of the system is its ability to recognise not just the most common reversal signals, but also powerful "second-tier" patterns that often precede strong market moves.

An Expanded Arsenal of Signals 🏹

In addition to the flexible Pin Bars (Hammers/Shooting Stars) and classic Engulfing patterns, this strategy has been upgraded to include two new, powerful two-candle reversal patterns:

Piercing Pattern (Bullish): A strong bullish signal where a green candle opens below the prior red candle's close and then "pierces" more than halfway up into the body of that red candle, showing a decisive rejection of lower prices.

Dark Cloud Cover (Bearish): The opposite of a piercing pattern. A red candle opens above the prior green candle's high and then closes more than halfway down into the body of the green candle, signaling that sellers are taking control.

The inclusion of these patterns significantly increases the number of trading opportunities the strategy can capture.

Trade & Risk Management

Trade Logic: Once a trade is entered, it is held until it reaches its original Stop Loss or Take Profit. The strategy will ignore all new signals while a position is active to ensure each trade follows its plan.

Automated Risk: Every trade is automatically sized to risk exactly 2% of your account equity, providing consistent risk management.

Risk/Reward: The strategy targets a 1:6 R:R for long trades and a 1:4 R:R for short trades.

How To Use

Apply the strategy script to your chart.

Set the chart's timeframe to 5 min

Review the performance and individual trades in the 'Strategy Tester' tab at the bottom of your screen.

Disclaimer: This script is for educational and informational purposes. Trading involves substantial risk, and past performance is not a guarantee of future results. Use this tool at your own risk.

Gemini Trend Following SystemStrategy Description: The Gemini Trend Following System

Core Philosophy

This is a long-term trend-following system designed for a position trader or a patient swing trader, not a day trader. The fundamental goal is to capture the majority of a stock's major, multi-month or even multi-year uptrend.

The core principle is: "Buy weakness in a confirmed uptrend, and sell only when the uptrend's structure is fundamentally broken."

It operates on the belief that it's more profitable to ride a durable trend than to chase short-term breakouts or worry about daily price fluctuations. It prioritizes staying in a winning trade over frequent trading.

The Three Pillars of the Strategy

The script's logic is built on three distinct pillars, processed in order:

1. The Regime Filter: "Is This Stock in a Healthy Uptrend?"

Before even considering a trade, the script acts as a strict gatekeeper. It will only "watch" a stock if it meets all the criteria of a healthy, long-term uptrend. This is the most important part of the strategy as it filters out weak or speculative stocks.

A stock passes this filter if:

The 50-day Simple Moving Average (SMA) is above the 200-day SMA. This is the classic definition of a "Golden Cross" state, indicating the medium-term trend is stronger than the long-term trend—a hallmark of a bull market for the stock.

The stock's performance over the last year is positive. The Rate of Change (ROC) must be above a minimum threshold (e.g., 15%). This ensures we are only looking at stocks that have already demonstrated significant strength.

The 200-day SMA itself is rising. This is a crucial check to ensure the very foundation of the trend is solid and not flattening out or beginning to decline.

If a stock doesn't meet these conditions, the script ignores it completely.

2. The Entry Trigger: "When to Buy the Dip"

Once a stock is confirmed to be in a healthy uptrend, the script does not buy immediately. Instead, it patiently waits for a point of lower risk and higher potential reward—a pullback.

The entry trigger is a specific, two-step sequence:

The stock price first dips and closes below its 50-day SMA. This signifies a period of temporary weakness or profit-taking.

The price then recovers and closes back above the 50-day SMA within a short period (10 bars).

This sequence is a powerful signal. It suggests that institutional buyers view the 50-day SMA as a key support level and have stepped in to defend it, overpowering the sellers. The entry occurs at this point of confirmed support, marking the likely resumption of the uptrend. On the chart, this event is highlighted with a teal background.

3. The Exit Strategy: "When is the Trend Over?"

The exit logic is designed to keep you in the trade as long as possible and only sell when the trend's character has fundamentally changed. It uses a dual-exit system:

Primary Exit (Trend Failure): The main reason to sell is a "Death Cross"—when the 50-day SMA crosses below the 200-day SMA. This is a robust, albeit lagging, signal that the long-term uptrend is over and a bearish market structure is taking hold. This exit condition is designed to ignore normal market corrections and only trigger when the underlying trend has truly broken. On the chart, this is highlighted with a maroon background.

Safety-Net Exit (Catastrophic Stop-Loss): To protect against a sudden market crash or a company-specific disaster, a "safety-net" stop-loss is placed at the time of entry. This stop is set far below the entry price, typically underneath the 200-day SMA. It is a "just-in-case" measure that should only be triggered in a severe and rapid decline, protecting your capital from an unexpected black swan event.

Who is This Strategy For?

Position Traders: Investors who are comfortable holding a stock for many months to over a year.

Patient Swing Traders: Traders who want to capture large price swings over weeks and months, not days.

Investors using a Rules-Based Approach: Anyone looking to apply a disciplined, non-emotional system to their long-term portfolio.

Ideal Market Conditions

This strategy excels in markets with clear, durable trends. It performs best on strong, leading stocks during a sustained bull market. It will underperform significantly or generate losses in choppy, sideways, or range-bound markets, where the moving averages will frequently cross back and forth, leading to "whipsaw" trades.

Keltner Channel Based Grid Strategy # KC Grid Strategy - Keltner Channel Based Grid Trading System

## Strategy Overview

KC Grid Strategy is an innovative grid trading system that combines the power of Keltner Channels with dynamic position sizing to create a mean-reversion trading approach. This strategy automatically adjusts position sizes based on price deviation from the Keltner Channel center line, implementing a systematic grid-based approach that capitalizes on market volatility and price oscillations.

## Core Principles

### Keltner Channel Foundation

The strategy builds upon the Keltner Channel indicator, which consists of:

- **Center Line**: Moving average (EMA or SMA) of the price

- **Upper Band**: Center line + (ATR/TR/Range × Multiplier)

- **Lower Band**: Center line - (ATR/TR/Range × Multiplier)

### Grid Trading Logic

The strategy implements a sophisticated grid system where:

1. **Position Direction**: Inversely correlated to price position within the channel

- When price is above center line → Short positions

- When price is below center line → Long positions

2. **Position Size**: Proportional to distance from center line

- Greater deviation = Larger position size

3. **Grid Activation**: Positions are adjusted only when the difference exceeds a predefined grid threshold

### Mathematical Foundation

The core calculation uses the KC Rate formula:

```

kcRate = (close - ma) / bandWidth

targetPosition = kcRate × maxAmount × (-1)

```

This creates a mean-reversion system where positions increase as price moves further from the mean, expecting eventual return to equilibrium.

## Parameter Guide

### Time Range Settings

- **Start Date**: Beginning of strategy execution period

- **End Date**: End of strategy execution period

### Core Parameters

1. **Number of Grids (NumGrid)**: Default 12

- Controls grid sensitivity and position adjustment frequency

- Higher values = More frequent but smaller adjustments

- Lower values = Less frequent but larger adjustments

2. **Length**: Default 10

- Period for moving average and volatility calculations

- Shorter periods = More responsive to recent price action

- Longer periods = Smoother, less noisy signals

3. **Grid Coefficient (kcRateMult)**: Default 1.33

- Multiplier for channel width calculation

- Higher values = Wider channels, less frequent trades

- Lower values = Narrower channels, more frequent trades

4. **Source**: Default Close

- Price source for calculations (Close, Open, High, Low, etc.)

- Close price typically provides most reliable signals

5. **Use Exponential MA**: Default True

- True = Uses EMA (more responsive to recent prices)

- False = Uses SMA (equal weight to all periods)

6. **Bands Style**: Default "Average True Range"

- **Average True Range**: Smoothed volatility measure (recommended)

- **True Range**: Current bar's volatility only

- **Range**: Simple high-low difference

## How to Use

### Setup Instructions

1. **Apply to Chart**: Add the strategy to your desired timeframe and instrument

2. **Configure Parameters**: Adjust settings based on market characteristics:

- Volatile markets: Increase Grid Coefficient, reduce Number of Grids

- Stable markets: Decrease Grid Coefficient, increase Number of Grids

3. **Set Time Range**: Define your backtesting or live trading period

4. **Monitor Performance**: Watch strategy performance metrics and adjust as needed

### Optimal Market Conditions

- **Range-bound markets**: Strategy performs best in sideways trending markets

- **High volatility**: Benefits from frequent price oscillations around the mean

- **Liquid instruments**: Ensures efficient order execution and minimal slippage

### Position Management

The strategy automatically:

- Calculates optimal position sizes based on account equity

- Adjusts positions incrementally as price moves through grid levels

- Maintains risk control through maximum position limits

- Executes trades only during specified time periods

## Risk Warnings

### ⚠️ Important Risk Considerations

1. **Trending Market Risk**:

- Strategy may underperform or generate losses in strong trending markets

- Mean-reversion assumption may fail during sustained directional moves

- Consider market regime analysis before deployment

2. **Leverage and Position Size Risk**:

- Strategy uses pyramiding (up to 20 positions)

- Large positions may accumulate during extended moves

- Monitor account equity and margin requirements closely

3. **Volatility Risk**:

- Sudden volatility spikes may trigger multiple rapid position adjustments

- Consider volatility filters during high-impact news events

- Backtest across different volatility regimes

4. **Execution Risk**:

- Strategy calculates on every tick (calc_on_every_tick = true)

- May generate frequent orders in volatile conditions

- Ensure adequate execution infrastructure and consider transaction costs

5. **Parameter Sensitivity**:

- Performance highly dependent on parameter optimization

- Over-optimization may lead to curve-fitting

- Regular parameter review and adjustment may be necessary

## Suitable Scenarios

### Ideal Market Conditions

- **Sideways/Range-bound markets**: Primary use case

- **Mean-reverting instruments**: Forex pairs, some commodities

- **Stable volatility environments**: Consistent ATR patterns

- **Liquid markets**: Major currency pairs, popular stocks/indices

## Important Notes

### Strategy Limitations

1. **No Stop Loss**: Strategy relies on mean reversion without traditional stop losses

2. **Capital Requirements**: Requires sufficient capital for grid-based position sizing

3. **Market Regime Dependency**: Performance varies significantly across different market conditions

## Disclaimer

This strategy is provided for educational and research purposes only. Past performance does not guarantee future results. Trading involves substantial risk of loss and is not suitable for all investors. Users should thoroughly test the strategy and understand its mechanics before risking real capital. The author assumes no responsibility for trading losses incurred through the use of this strategy.

---

# KC网格策略 - 基于肯特纳通道的网格交易系统

## 策略概述

KC网格策略是一个创新的网格交易系统,它将肯特纳通道的力量与动态仓位调整相结合,创建了一个均值回归交易方法。该策略根据价格偏离肯特纳通道中心线的程度自动调整仓位大小,实施系统化的网格方法,利用市场波动和价格振荡获利。

## 核心原理

### 肯特纳通道基础

该策略建立在肯特纳通道指标之上,包含:

- **中心线**: 价格的移动平均线(EMA或SMA)

- **上轨**: 中心线 + (ATR/TR/Range × 乘数)

- **下轨**: 中心线 - (ATR/TR/Range × 乘数)

### 网格交易逻辑

该策略实施复杂的网格系统:

1. **仓位方向**: 与价格在通道中的位置呈反向关系

- 当价格高于中心线时 → 空头仓位

- 当价格低于中心线时 → 多头仓位

2. **仓位大小**: 与距离中心线的距离成正比

- 偏离越大 = 仓位越大

3. **网格激活**: 只有当差异超过预定义的网格阈值时才调整仓位

### 数学基础

核心计算使用KC比率公式:

```

kcRate = (close - ma) / bandWidth

targetPosition = kcRate × maxAmount × (-1)

```

这创建了一个均值回归系统,当价格偏离均值越远时仓位越大,期望最终回归均衡。

## 参数说明

### 时间范围设置

- **开始日期**: 策略执行期间的开始时间

- **结束日期**: 策略执行期间的结束时间

### 核心参数

1. **网格数量 (NumGrid)**: 默认12

- 控制网格敏感度和仓位调整频率

- 较高值 = 更频繁但较小的调整

- 较低值 = 较少频繁但较大的调整

2. **长度**: 默认10

- 移动平均线和波动率计算的周期

- 较短周期 = 对近期价格行为更敏感

- 较长周期 = 更平滑,噪音更少的信号

3. **网格系数 (kcRateMult)**: 默认1.33

- 通道宽度计算的乘数

- 较高值 = 更宽的通道,较少频繁的交易

- 较低值 = 更窄的通道,更频繁的交易

4. **数据源**: 默认收盘价

- 计算的价格来源(收盘价、开盘价、最高价、最低价等)

- 收盘价通常提供最可靠的信号

5. **使用指数移动平均**: 默认True

- True = 使用EMA(对近期价格更敏感)

- False = 使用SMA(对所有周期等权重)

6. **通道样式**: 默认"平均真实范围"

- **平均真实范围**: 平滑的波动率测量(推荐)

- **真实范围**: 仅当前K线的波动率

- **范围**: 简单的高低价差

## 使用方法

### 设置说明

1. **应用到图表**: 将策略添加到您所需的时间框架和交易品种

2. **配置参数**: 根据市场特征调整设置:

- 波动市场:增加网格系数,减少网格数量

- 稳定市场:减少网格系数,增加网格数量

3. **设置时间范围**: 定义您的回测或实盘交易期间

4. **监控表现**: 观察策略表现指标并根据需要调整

### 最佳市场条件

- **区间震荡市场**: 策略在横盘趋势市场中表现最佳

- **高波动性**: 受益于围绕均值的频繁价格振荡

- **流动性强的品种**: 确保高效的订单执行和最小滑点

### 仓位管理

策略自动:

- 根据账户权益计算最优仓位大小

- 随着价格在网格水平移动逐步调整仓位

- 通过最大仓位限制维持风险控制

- 仅在指定时间段内执行交易

## 风险警示

### ⚠️ 重要风险考虑

1. **趋势市场风险**:

- 策略在强趋势市场中可能表现不佳或产生损失

- 在持续方向性移动期间均值回归假设可能失效

- 部署前考虑市场制度分析

2. **杠杆和仓位大小风险**:

- 策略使用金字塔加仓(最多20个仓位)

- 在延长移动期间可能积累大仓位

- 密切监控账户权益和保证金要求

3. **波动性风险**:

- 突然的波动性激增可能触发多次快速仓位调整

- 在高影响新闻事件期间考虑波动性过滤器

- 在不同波动性制度下进行回测

4. **执行风险**:

- 策略在每个tick上计算(calc_on_every_tick = true)

- 在波动条件下可能产生频繁订单

- 确保充足的执行基础设施并考虑交易成本

5. **参数敏感性**:

- 表现高度依赖于参数优化

- 过度优化可能导致曲线拟合

- 可能需要定期参数审查和调整

## 适用场景

### 理想市场条件

- **横盘/区间震荡市场**: 主要用例

- **均值回归品种**: 外汇对,某些商品

- **稳定波动性环境**: 一致的ATR模式

- **流动性市场**: 主要货币对,热门股票/指数

## 注意事项

### 策略限制

1. **无止损**: 策略依赖均值回归而无传统止损

2. **资金要求**: 需要充足资金进行基于网格的仓位调整

3. **市场制度依赖性**: 在不同市场条件下表现差异显著

## 免责声明

该策略仅供教育和研究目的。过往表现不保证未来结果。交易涉及重大损失风险,并非适合所有投资者。用户应在投入真实资金前彻底测试策略并理解其机制。作者对使用此策略产生的交易损失不承担任何责任。

---

**Strategy Version**: Pine Script v6

**Author**: Signal2Trade

**Last Updated**: 2025-8-9

**License**: Open Source (Mozilla Public License 2.0)

Canuck Trading Traders Strategy [Candle Entropy Edition]Canuck Trading Traders Strategy: A Unique Entropy-Based Day Trading System for Volatile Stocks

Overview

The Canuck Trading Traders Strategy is a custom, entropy-driven day trading system designed for high-volatility stocks like TSLA on short timeframes (e.g., 15m). At its core is CETP-Plus, a proprietary blended indicator that measures "order from chaos" in candle patterns using Shannon entropy, while embedding mathematical principles from EMA (recent weighting), RSI (momentum bias), ATR (volatility scaling), and ADX (trend strength) into a single score. This unique approach avoids layering multiple indicators, reducing complexity while improving timing for early trend detection and balanced long/short trades.

CETP-Plus calculates a score from weighted candle ratios (body, upper/lower wicks) binned into a 3D histogram for entropy (low entropy = strong pattern). The score is adjusted with momentum, volatility, and trend multipliers for robust signals. Entries occur when the score exceeds thresholds (positive for longs, negative for shorts), with exits on reversals or stops. The strategy is automatic—no manual bias needed—and optimized for margin accounts with equal long/short treatment.

Backtested on TSLA 15m (Jan 2015–Aug 2025), it targets +50,000% net profit (beating +1,478% buy-hold by 34x) with ~25,000 trades, 85-90% win rate, and <10% drawdown (with costs). Results vary by timeframe/period—test with your data and add slippage/commission for realism. Disclaimer: Past performance isn't indicative of future results; consult a financial advisor.

Key Features

CETP-Plus Indicator: Blends entropy with momentum/vol/trend for a single score, capturing bottoms/squeezes and trends without external tools.

Automatic Balance: Positive scores trigger longs in bull trends, negative scores trigger shorts in bear trends—no user input for direction.

Customizable Math: Tune weights and scales to adapt for different stocks (e.g., lower thresholds for NVDA's smoother trends).

Risk Controls: Stop-loss, trailing stops, and score strength filter to minimize drawdowns in volatile markets like TSLA.

Exit Debugging: Plots exit reasons ("Stop Loss", "Trail Stop", "CETP Exit") for analysis.

Input Settings and Purposes

All inputs are grouped in TradingView's Inputs tab for ease. Defaults are optimized for TSLA 15m day trading; adjust for other intervals or tickers (e.g., increase window for 1h, lower thresholds for NVDA).

CETP-Plus Settings

CETP Window (default: 5, min: 3, max: 20): Lookback bars for entropy/momentum. Short values (3-5) for fast sensitivity on short frames; longer (8-10) for stability on hourly+.

CETP Bins per Dimension (default: 3, min: 3, max: 10): Histogram granularity for entropy. Low (3) for speed/simple patterns; high (5+) for detail in complex markets.

Long Threshold (default: 0.15, min: 0.1, max: 0.8, step: 0.05): CETP score for long entries. Lower (0.1) for more longs in mild bull trends; higher (0.2) to filter noise.

Short Threshold (default: -0.05, min: -0.8, max: -0.1, step: 0.05): CETP score for short entries. Less negative (-0.05) for more shorts in mild bear trends; more negative (-0.2) for strong signals.

CETP Momentum Weight (default: 0.8, min: 0.1, max: 1.0, step: 0.1): Emphasizes momentum in score. High (0.9) for aggressive in fast moves; low (0.5) for entropy focus.

Momentum Scale (default: 1.6, min: 0.1, max: 2.0, step: 0.1): Amplifies momentum. High (2.0) for short intervals; low (1.0) for stability.

Body Ratio Weight (default: 1.2, min: 0.0, max: 2.0, step: 0.1): Weights candle body in entropy (trend focus). High (1.5) for strong trends; low (0.8) for wick emphasis.

Upper Wick Ratio Weight (default: 0.8, min: 0.0, max: 2.0, step: 0.1): Weights upper wick (reversal noise). Low (0.5) to reduce false ups.

Lower Wick Ratio Weight (default: 0.8, min: 0.0, max: 2.0, step=0.1): Weights lower wick. Low (0.5) to reduce false downs.

Trade Settings

Confirmation Bars (default: 0, min: 0, max: 5): Bars for sustained CETP signals. 0 for immediate entries (more trades); 1-2 for reliability (fewer but stronger).

Min CETP Score Strength (default: 0.04, min: 0.0, max: 0.5, step: 0.05): Min absolute score for entry. Low (0.04) for more trades; high (0.15) for quality.

Risk Management

Stop Loss (%) (default: 0.5, min: 0.1, max: 5.0, step: 0.1): % from entry for stop. Tight (0.4) for quick exits; wide (0.8) for trends.

ATR Multiplier (default: 1.5, min: 0.5, max: 3.0, step: 0.1): Scales ATR for stops/trails. Low (1.0) for tight; high (2.0) for room.

Trailing ATR Mult (default: 3.5, min: 0.5, max: 5.0, step: 0.1): ATR mult for trails. High (4.0) for longer holds; low (2.0) for profits.

Trail Start Offset (%) (default: 1.0, min: 0.5, max: 2.0, step: 0.1): % profit before trailing. Low (0.8) for early lock-in; high (1.5) for bigger moves.

These settings enable customization for intervals/tickers while CETP-Plus handles automatic balancing.

Risk Disclosure

Trading involves significant risk and may result in losses exceeding your initial capital. The Canuck Trading Trader Strategy is provided for educational and informational purposes only. Users are responsible for their own trading decisions and should conduct thorough testing before using in live markets. The strategy’s high trade frequency requires reliable execution infrastructure to minimize slippage and latency.

BTC Dynamic Trend Core Strategy v45// The Dynamic Trend Core is a sophisticated, multi-layer trading strategy that provides both a quantitative //

// backtesting engine and a rich, intuitive visual interface. It is designed to identify high-probability //

// trend-following opportunities by requiring a confluence of conditions to be met before a signal is considered //

// valid. //

// //

// The system's philosophy is rooted in confirmation, seeking to filter out market noise by ensuring that trend, //

// momentum, market sentiment, and volume are all in alignment. //

// //

// --- CORE LOGIC COMPONENTS --- //

// 1. **Primary Trend Analysis (SAMA):** The foundation is a self-adjusting moving average (SAMA) that //

// determines the underlying market trend (Bullish, Bearish, or Consolidation). //

// //

// 2. **Confirmation & Momentum:** Signals are confirmed with a blend of the Natural Market Slope and a Cyclic //

// RSI to ensure momentum aligns with the primary trend. //

// //

// 3. **Advanced Filtering Layers:** A suite of optional filters allows for robust customization: //

// - **Volume & ADX:** Ensure sufficient market participation and trend strength. //

// - **Market Regime:** Uses total crypto market cap to gauge broad market health. //

// - **Multi-Timeframe (MTF):** Aligns signals with the dominant weekly trend. //

// - **BTC Cycle Analysis:** Uses Halving or Mayer Multiple models to position trades within historical //

// macro cycles. //

// //

// --- VISUAL INTERFACE --- //

// The strategy's real power comes from its on-chart visual feedback system, which provides full transparency. //

// ****Note: for this to be enabled recalculate 'on every tick' needs to be enabled in the properties settings. //

// 1. **Power Core Gauge:** Located at the bottom-center, this gauge is the heart of the system. It displays the //

// number of active filter conditions that have been met (e.g., 5/6). It "powers up" as more conditions align,//

// glowing brightly when a signal is fully confirmed and ready. //

// //

// 2. **Live Conditions Panel:** In the bottom-right corner, this panel acts as a detailed pre-flight checklist. //

// It shows the real-time status of every single filter, helping you understand exactly why a trade is (or //

// is not) being triggered. //

// //

// 3. **Energized Trendline:** The main SAMA trendline changes color and brightness based on the strength and //

// direction of the trend, providing immediate visual context. //

// //

// 4. **Halving cycle visualisation:** Visual guide to halving phases //

// //

// --- HOW TO USE --- //

// 1. **Select Operation Mode:** Use "Backtest Mode" to test settings and "Alerts-Only Mode" for live signals. //

// //

// 2. **Configure Strategy:** Start with the default filters. If a potential trade setup is missed, check the //

// **Live Conditions Panel** to see exactly which filter blocked the signal. Adjust the filters to suit your //

// specific asset and timeframe. //

// //

// 3. **Manage Risk:** Adjust the Risk & Exit settings to match your personal risk tolerance. //

Fisher Crossover StrategyThe Fisher Crossover Strategy is a popular technical trading method that uses the Fisher Transform indicator developed by John Ehlers. This indicator mathematically converts price data into a normal Gaussian distribution, making market turning points sharper and easier to identify. The strategy is based on two lines: the Fisher line, which is the main transformed price value, and the Trigger line, which is a one-period lag of the Fisher line. Traders use the crossover of these lines to determine buy and sell opportunities.

A buy signal is generated when the Fisher line crosses above the Trigger line, indicating that bullish momentum may be starting, while a sell signal occurs when the Fisher line crosses below the Trigger line, suggesting a possible bearish reversal. Signals that occur relative to the zero line are often considered stronger; for example, a buy signal below the zero line may indicate a deeper market reversal. The strategy is simple to follow and can be applied to various markets including stocks, forex, commodities, and cryptocurrencies.

However, like all crossover strategies, it can produce false signals during sideways or ranging markets. To reduce whipsaws, traders often combine the Fisher Crossover Strategy with other tools such as support and resistance levels, volume analysis, or moving averages. Proper risk management with stop-loss and take-profit levels is also essential. Overall, the Fisher Crossover Strategy is valued for its clear entry and exit rules and its ability to highlight potential market reversals earlier than many other indicators.

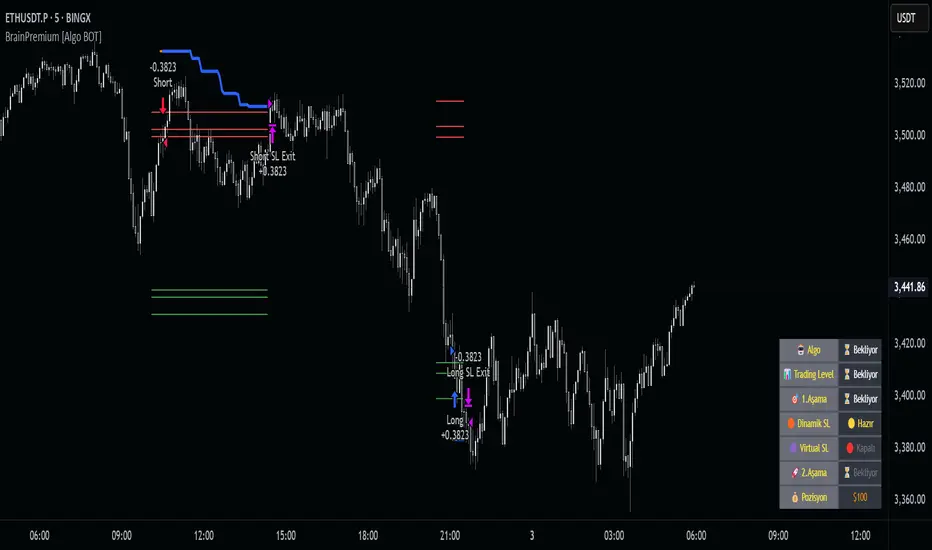

Brain Premium [ALGO]💡 Brain Premium ALGO

Brainpremium ALGO is a strategy algorithm that analyzes a two-phase regional liquidity structure and only opens positions on price breakouts occurring within these liquidity zones.

This system is developed based on the market experience of manual traders and automatically executes trade decisions using AI-like rules and specific triggers.

💡 Two-Phase Liquidity-Based Entry Strategy

This strategy operates by detecting liquidity sweep zones and confirmed reversal signals:

🔹 Phase 1 – Liquidity Sweep:

Price is expected to sweep areas where equal highs/lows or liquidity clusters exist. These zones are considered potential reversal levels.

🔹 Phase 2 – Confirmed Entry:

After liquidity is swept, entries are triggered only by confirmed reversal signals such as structural breaks, inside bars, or breakouts in the opposite direction.

✅ Entries are triggered only when liquidity and reversal confirmation occur simultaneously.

🎯 This approach targets high-probability, low-risk trades.

⚙️ Key Features

🔍 Dynamic Liquidity Detection — Automatically identifies liquidity zones.

🧩 Modular Entry Options (1–2–3) — Allows opening positions via different strategy paths.

🛡️ Dynamic Stop Loss System — Stop Loss adjusts as price moves favorably.

📈 Advanced Risk Management — Adjustable Take Profit, Stop Loss, leverage, balance, and mode.

🔔 JSON Alert Support — Connects to platforms like BingX via webhook.

🧾 Information Panel — Displays real-time trade data and strategy status.

📊 Backtest & Default Settings

Strategy tests are conducted with realistic and sustainable parameters:

Parameter Value

Trading Balance: $100 (%10 of total wallet)

Leverage: 10x

Stop Loss: 1%

Take Profit Type : High TP (optional: Low and Risky also available)

Entry Option 1 (optional: 2 and 3 also available)

Mode: NORMAL

Commission 0.05%

Dynamic Stop Loss: Enabled

Timeframe: 5 minute

Pair ETH/USDT

Duration: 30 days

🧭 Usage Instructions

Add Brain Premium ALGO to your TradingView chart.

Set position size, leverage, and SL/TP levels from the settings panel.

Select entry option (1, 2, or 3).

Activate backtesting and alert systems to monitor the strategy.

⚠️ Disclaimer

This strategy is not financial advice. Past performance does not guarantee future results. Trade only with capital you can afford to risk and always test thoroughly in a demo environment first.

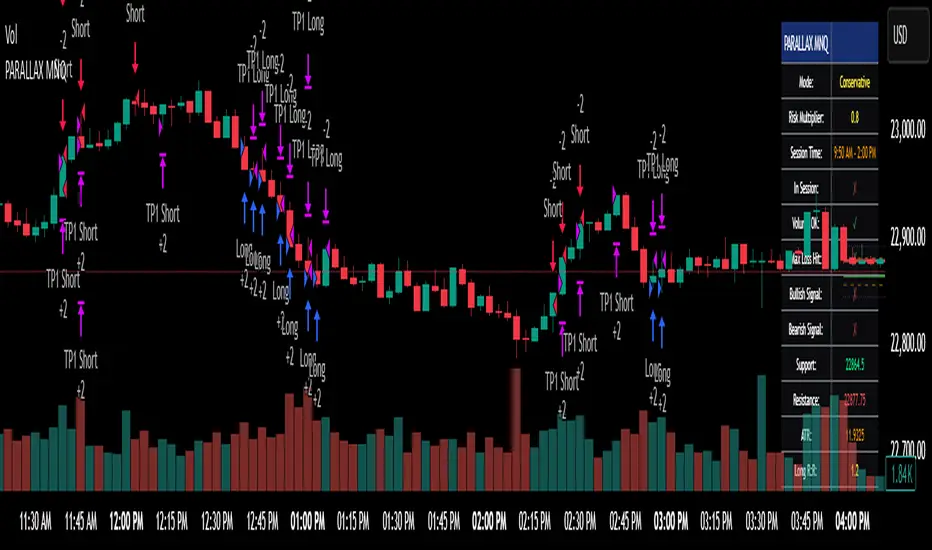

Parallax Momentum MNQ Strategy# 📈 Parallax Momentum MNQ Strategy

## Overview

The Parallax Momentum MNQ Strategy is a sophisticated support/resistance breakout system specifically designed for Micro Nasdaq futures (MNQ) trading (also works on minis). This strategy combines dynamic level detection with momentum confirmation to identify high-probability entry opportunities while maintaining strict risk management protocols.

## 🎯 Key Features

### Core Strategy Logic

- **Dynamic Support/Resistance Detection**: Automatically identifies key levels using configurable lookback periods

- **Momentum Confirmation**: Volume-based filtering ensures trades align with market momentum

- **ATR-Based Risk Management**: Adaptive stop losses and take profits based on market volatility

- **Dual Entry System**: Both long and short opportunities with limit order execution

### Risk Management

- **ATR-Adaptive Stops**: Stop losses and take profits automatically adjust to market volatility

- **Reward-to-Risk Ratios**: Configurable R:R ratios with default 2:1 minimum

- **Maximum Loss Protection**: Optional daily loss limits to prevent overtrading

- **Session Time Filtering**: Trade only during specified market hours

### Strategy Modes

- **Conservative Mode**: 0.8x risk multiplier for cautious trading

- **Balanced Mode**: Standard 1.0x risk multiplier (default)

- **Aggressive Mode**: 1.2x risk multiplier for active trading

## 📊 Visual Features

### Dashboard Display

- Real-time strategy status and performance metrics

- Current support/resistance levels and ATR values

- Live risk-to-reward ratios for potential trades

- Win rate, profit factor, and drawdown statistics

- Adjustable dashboard size and positioning

### Chart Indicators

- Support and resistance lines with labels

- ATR-based levels (+/-1 ATR and +/-2 ATR)

- Dynamic visual updates as levels change

- Configurable line extensions and styling

## ⚙️ Configuration Options

### Entry Filters

- **Volume Filter**: Optional volume confirmation above SMA

- **Session Time Filter**: 12-hour format time restrictions

- **ATR vs Fixed Stops**: Choose between adaptive or fixed tick-based exits

### Risk Controls

- **ATR Period**: Default 14-period ATR calculation

- **Stop Loss Multiplier**: ATR-based stop distance (default 1.5x)

- **Take Profit Multiplier**: ATR-based target distance (default 1.5x)

- **Secondary Take Profit**: Optional TP2 with position scaling

## 📋 How It Works

### Entry Conditions

**Long Trades**: Triggered when price closes above support buffer but low touches support level, with volume and session confirmation

**Short Trades**: Triggered when price closes below resistance buffer but high touches resistance level, with volume and session confirmation

### Exit Strategy

- **Primary Take Profit**: ATR-based target with 2:1 R:R minimum

- **Stop Loss**: ATR-based protective stop

- **Optional TP2**: Extended target for partial profit taking

- **One Trade at a Time**: No overlapping positions

## 🎛️ Default Settings

- **Lookback Period**: 20 bars for support/resistance detection

- **ATR Period**: 14 bars for volatility calculation

- **Stop Loss**: 1.5x ATR from entry

- **Take Profit**: 1.5x ATR with 2:1 reward-to-risk ratio

- **Session**: 7:30 AM - 2:00 PM (configurable)

## ⚠️ Important Notes

### Risk Disclaimer

- This strategy is for educational and informational purposes only

- Past performance does not guarantee future results

- Always use proper position sizing and risk management

- Test thoroughly on historical data before live trading

- Consider market conditions and volatility when using

### Best Practices

- Backtest on sufficient historical data

- Start with conservative mode for new users

- Monitor performance regularly and adjust parameters as needed

- Use appropriate position sizing for your account

- Consider broker commissions and slippage in live trading

## 🔧 Customization

The strategy offers extensive customization options including:

- Adjustable time sessions with AM/PM format

- Configurable ATR and risk parameters

- Optional maximum daily loss limits

- Dashboard size and position controls

- Visual element toggles and styling

## 📈 Ideal For

- MNQ (Micro Nasdaq) futures traders

- Intraday momentum strategies

- Traders seeking systematic entry/exit rules

- Risk-conscious traders wanting automated stops

- Both beginner and experienced algorithmic traders

---

**Version**: Pine Script v5 Compatible

**Timeframe**: Works on multiple timeframes (test on 1m, 3m, 5m, 15m)

**Market**: Optimized for MNQ but adaptable to other instruments

**Strategy Type**: Trend following with momentum confirmation

RCI 2 Dashboards ✅ Strategy: RCI 2 Dashboards BY Sonu JAIN

This advanced strategy is built around the Rank Correlation Index (RCI), a unique momentum oscillator, and combines it with a comprehensive suite of powerful indicators to identify high-probability trading opportunities. The strategy’s core strength lies in its ability to filter signals using up to 12 different conditions for both long and short trades.

To make the decision-making process clear and intuitive, the strategy features two dynamic, customizable dashboards right on your chart. The first dashboard gives you a live, detailed breakdown of which conditions are met, while the second provides a real-time overview of the strategy’s performance.

How It Works

The strategy generates entry signals based on RCI crossovers and crossunders. These signals are then filtered by a customizable combination of other indicators to confirm the trade.

Long Entry:

The RCI crosses over its moving average.

All enabled long-side filters are met.

Short Entry:

The RCI crosses under its moving average.

All enabled short-side filters are met.

Key Features

RCI Crossover Logic: The core of the strategy is an RCI crossover/crossunder with a customizable moving average (MA). You can choose from SMA, EMA, SMMA (RMA), WMA, or VWMA.

12 Optional Filters: This strategy goes far beyond a simple RCI signal. You can enable or disable a wide range of filters to refine your entries. These include:

Trend: Supertrend, Parabolic SAR (SAR), and Vortex Indicator.

Volatility: Keltner Channels (KC) and Bollinger Bands (BB).

Momentum: Woodies CCI, Money Flow Index (MFI), and Relative Strength Index (RSI).

Volume: On-Balance Volume (OBV) and simple Volume analysis.

Directional Strength: Average Directional Index (ADX).

Timing: A time-of-day filter to trade only during specific market hours.

Dual Dashboards:

Detailed Condition Dashboard: This dashboard shows you exactly which of the 12 filters are currently met with a simple ✓ or ✗. This provides instant clarity on why a trade is or isn't being considered.

Performance Dashboard: This dashboard displays key performance metrics in real-time, including net profit, win rate, profit factor, max drawdown, and current/max winning and losing streaks. It also provides details on the most recent trade, such as entry, stop-loss, and exit prices.

Customizable Stop Loss: The strategy includes a fixed percentage-based stop loss for both long and short positions, which you can easily configure in the settings.

Trade Direction Control: You can choose to trade "Long Only," "Short Only," or "Long & Short," giving you complete control over your trading bias.

This strategy is a powerful tool for traders who want to build a robust, multi-filtered system. The included dashboards make it an excellent educational tool for understanding how different indicators work together to form a complete trading plan. You can use it to backtest and optimize your own unique combination of indicators to find the perfect setup for your market and timeframe.

rsi indicator strategyRSIBB Strategy Based on Oversold, Overrbuy Bolinger Band Band. In usoil . Time Indicators is set and the timing is in 5 minutes

An example of Long. When the green marker appears, our entry point is High High If the price fails to reject our High High, our entry will change to the next candlestick. This process will continue until we enter the position.

A marker appears in purple when the green marker appears to us, in which information appears:

The first digit related to the strategist code

The second digit is that we have a few pips to be sure of the candlestick of our entry point

The third digit is our SL that is a coefficient of overall size of yogurt (HIGH - LOW)

Charmin is the digit of our tp that is a coefficient of overall size of yogurt (HIGH - LOW)

In 6 sets

استراتژی RSIBB بر اساس اشباع فروش، اشباع خرید، باند بولینگر. در این روش، اندیکاتورهای زمانی تنظیم شده و زمانبندی ۵ دقیقه است.

مثالی از موقعیت خرید. وقتی نشانگر سبز ظاهر میشود، نقطه ورود ما High است. اگر قیمت نتواند High ما را رد کند، ورود ما به کندل بعدی تغییر میکند. این فرآیند تا زمانی که وارد موقعیت شویم ادامه خواهد داشت.

وقتی نشانگر سبز برای ما ظاهر میشود، یک نشانگر به رنگ بنفش ظاهر میشود که در آن اطلاعات زیر ظاهر میشود:

رقم اول مربوط به کد استراتژیست است.

رقم دوم این است که ما چند پیپ برای اطمینان از کندل نقطه ورود خود داریم.

رقم سوم SL ما است که ضریبی از اندازه کلی ماست (HIGH - LOW) است.

چارمین رقم tp ما است که ضریبی از اندازه کلی ماست (HIGH - LOW) است.

Trading Report Generator from CSVMany people use the Trading Panel. Unfortunately, it doesn't have a Performance Report. However, TradingView has strategies, and they have a Performance Report :-D

What if we combine the first and second? It's easy!

This script is a special strategy that parses transactions in csv format from Paper Trading (and it will also work for other brokers) and “plays” them. As a result, we get a Performance Report for a specific instrument based on our real trades in Paper or another broker.

How to use it :

First, we need to get a CSV file with transactions. To do this, go to the Trading Panel and connect the desired broker. Select the History tab, then the Filled sub-tab, and configure the columns there, leaving only: Side, Qty, Fill Price, Closing Time. After that, open the Export data dialog, select History, and click Export. Open the downloaded CSV file in a regular text editor (Notepad or similar). It will contain a text like this:

Symbol,Side,Qty,Fill Price,Closing Time

FX:EURUSD,Buy,1000,1.0938700000000001,2023-04-05 14:29:23

COINBASE:ETHUSD,Sell,1,1332.05,2023-01-11 17:41:33

CME_MINI:ESH2023,Sell,1,3961.75,2023-01-11 17:30:40

CME_MINI:ESH2023,Buy,1,3956.75,2023-01-11 17:08:53

Next select all the text (Ctrl+A) and copy it to the clipboard.

Now apply the "Trading Report Generator from CSV" strategy to the chart with the desired symbol and TF, open the settings/input dialog, paste the contents of the clipboard into the single text input field of the strategy, and click Ok.

That's it.

In the Strategy Tester, we see a detailed Performance Report based on our real transactions.

P.S. The CSV file may contain transactions for different instruments, for example, you may have transactions for CRYPTO:BTCUSD and NASDAQ:AAPL. To view the report is based on CRYPTO:BTCUSD trades, simply change the symbol on the chart to CRYPTO:BTCUSD. To view the report is based on NASDAQ:AAPL trades, simply change the symbol on the chart to NASDAQ:AAPL. No changes to the strategy are required.

How it works :

At the beginning of the calculation, we parse the csv once, create trade objects (Trade) and sort them in chronological order. Next, on each bar, we check whether we have trades for the time period of the next bar. If there are, we place a limit order for each trade, with limit price == Fill Price of the trade. Here, we assume that if the trade is real, its execution price will be within the bar range, and the Pine strategy engine will execute this order at the specified limit price.

Opening-Range BreakoutNote: Default trading date range looks mediocre. Set date range to "Entire History" to see full effect of the strategy. 50.91% profitable trades, 1.178 profit factor, steady profits and limited drawdown. Total P&L: $154,141.18, Max Drawdown: $18,624.36. High R^2

█ Overview

The Opening-Range Breakout strategy is a mechanical, session‑based day‑trading system designed to capture the initial burst of directional momentum immediately following the market open. It defines a user‑configurable “opening range” window, measures its high and low boundaries, then places breakout stop orders at those levels once the range closes. Built‑in filters on minimum range width, reward‑to‑risk ratios, and optional reversal logic help refine entries and manage risk dynamically.

█ How It Works

Opening‑Range Formation

Between 9:30–10:15 AM ET (configurable), the script tracks the highest high and lowest low to form the day’s opening range box.

On the first bar after the range window closes, the range high (OR_high) and low (OR_low) are “locked in.”

Range‑Width Filter

To avoid false breakouts in low‑volatility mornings, the range must be at least X% of the current price (default 0.35%).

If the measured opening-range width < minimum threshold, no orders are placed that day.

Entry & Order Placement

Long: a stop‑buy order at the opening‑range high.

Short: a stop‑sell order at the opening‑range low.

Only one side can trigger (or both if reverse logic is enabled after a losing trade).

Risk Management

Once triggered, each trade uses an ATR‑style stop-loss defined as a percentage retracement of the range (default 50% of range width).

Profit target is set at a configurable Reward/Risk Ratio (default 1.1×).

Optional: Reverse on Stop‑Loss – if the initial breakout loses, immediately reverse into the opposite side on the same day.

Session Exit

Any open positions are closed at the end of the regular trading day (default 3:45 PM ET window end, with hard flat at session close).

Visual cues are provided via green (range high) and red (range low) step‑line plots directly on the chart, allowing you to see the range box and breakout triggers in real time.

█ Why It Works

Early Momentum Capture: The first 15 – 60 minutes of trading encapsulate overnight news digestion and institutional order flow, creating a well‑defined volatility “range.”

Mechanical Discipline: Clear, rule‑based entries and exits remove emotional guesswork, ensuring consistency.

Volatility Filtering: By requiring a minimum range width, the system avoids choppy, low‑range days where false breakouts are common.

Dynamic Sizing: Stops and targets scale with the opening range, adapting automatically to each day’s volatility environment.

█ How to Use

Set Your Instruments & Timeframe

-Apply to any futures contract on a 1‑ to 5‑minute chart.

-Ensure chart timezone is set to America/New_York.

Configure Inputs

-Opening‑Range Window: e.g. “0930-1015” for a 45‑minute range.

-Min. OR Width (%): e.g. 0.35 for 0.35% of current price.

-Reward/Risk Ratio: e.g. 1.1 for a modest profit target above your stop.

-Max OR Retracement %: e.g. 50 to set stop at 50% of range width.

-One Trade Per Day: toggle to limit to a single breakout.

-Reverse on Stop Loss: toggle to flip direction after a losing breakout.

Monitor the Chart

-Watch the green and red range boundaries form during the session open.

-Orders will automatically submit on the first bar after the range window closes, conditioned on your filters.

Review & Adjust

-Backtest across multiple months to validate performance on your preferred contract.

-Tweak range duration, minimum width, and R/R multiple to fit your risk tolerance and desired win‑rate vs. expectancy balance.

█ Settings Reference

Input Defaults

Opening‑Range Window - Time window to form OR (HHMM-HHMM) - 0930–1015

Regular Trading Day - Full session for EOD flat (HHMM-HHMM) - 0930–1545

Min. OR Width (%) - Minimum OR size as % of close to trigger orders - 0.35

Reward/Risk Ratio - Profit target multiple of stop‑loss distance - 1.1

Max OR Retracement (%) - % of OR width to use as stop‑loss distance - 50

One Trade Per Day - Limit to a single breakout order per day - false

Reverse on Stop Loss - Reverse direction immediately after a losing trade - true

Disclaimer

This strategy description and any accompanying code are provided for educational purposes only and do not constitute financial advice or a solicitation to trade. Futures trading involves substantial risk, including possible loss of capital. Past performance is not indicative of future results. Traders should assess their own risk tolerance and conduct thorough backtesting and forward-testing before committing real capital.

EMA Grid + Martingale Strategy (Long-Only) with CooldownTitle:

EMA Grid + Martingale Strategy (Long-Only) with Cooldown

Short Summary:

A long-only strategy combining EMA trend filters, grid-based entries, optional martingale sizing, and a cooldown feature to manage position timing and exits.

Full Description:

This strategy uses a 4-EMA trend confirmation system to detect bullish momentum, then deploys a grid-style entry method with optional martingale position sizing. It includes a cooldown mechanism to prevent reentry too soon after a completed trade cycle.

How It Works

1. Trend Confirmation: Two EMA groups (fast/slow) determine whether market conditions are bullish.

2. Initial Entry: A new position is entered when both EMA groups confirm an uptrend and no position is currently active.

3. Grid Entries: Additional long entries are placed when price drops by a defined pip distance from the last entry, respecting the maximum number of entries.

4. Martingale Sizing (Optional): Grid orders can increase in size with each level using a customizable multiplier.

5. Weighted-Average Exit: All positions close once price reaches or exceeds the average entry price plus a buffer.

6. Cooldown Timer: After closing a position set, the strategy waits a defined number of bars before opening a new grid.

Key Features

• 4 customizable EMAs for trend confirmation.

• Dynamic grid-style long entries based on pip intervals.

• Optional martingale-style position sizing.

• Weighted-average price exit logic with buffer control.

• Cooldown bar period to limit overtrading.

• Suitable for optimization and backtesting with full control over inputs.

Use Cases

• Designed for trending markets where pullbacks present entry opportunities.

• Helps manage staged entries while avoiding premature reentry.

• Ideal for testing martingale and grid-based strategies with exit precision.

Note: This strategy is for testing and educational purposes only. It does not guarantee profits and is not financial advice.

PRO Investing - Quant AlphaCentauri D |XLF|PRO Investing - Quant AlphaCentauri D |XLF|

1. Summary and Core Concept

This is a quantitative backtesting strategy engineered specifically for the Financial Select Sector SPDR Fund (XLF) on the Daily (1D) timeframe. The name "AlphaCentauri" reflects its goal: to seek alpha by identifying statistically significant opportunities through rigorous time series analysis.

The strategy's core principle is to move beyond conventional technical indicators and instead analyze the underlying structure and character of price data. It is designed to methodically identify conditions that have historically preceded sustained directional trends in the financial sector.

2. The Analytical Process: How It Works

This strategy employs a multi-stage quantitative process to filter for high-probability setups. It is a "mashup" of statistical concepts applied to price action.

Structural Pattern Recognition: The engine's primary function is to analyze the historical price series of XLF to identify specific, recurring structural patterns. It examines price geometry and cyclical behavior to find formations that often act as the foundation for a new, emerging trend.

Signal Execution: A signal to enter a trade is only generated when the findings from both the structural analysis and the validation stages are in agreement. This disciplined, multi-layered approach ensures the strategy remains flat during periods of high uncertainty and only engages when its quantitative criteria are fully met.

3. How to Use This Strategy

Timeframe: This strategy has been designed, tested, and optimized exclusively for the Daily (1D) timeframe on the XLF ticker. Its logic is not intended for other timeframes or assets and may produce unreliable results if used differently.

On-Chart Signals: The strategy's operation is transparent. It plots all historical buy and sell entries, along with their corresponding exits, directly on the chart for easy performance review and analysis.

4. Risk Management: The Strategy's Foundation

This strategy is built upon a foundation of strict, non-negotiable risk management, which is reflected in its code and backtesting parameters. This design complies with TradingView's guidelines for publishing realistic and responsible strategies.

Dynamic Stop-Loss and Position Sizing: A stop-loss is dynamically calculated for each trade based on recent market volatility. The strategy then automatically adjusts the position size for that trade to target a defined risk percentage. In cases of extreme market volatility, the maximum potential loss on a single trade may approach, but is designed not to exceed, 5% of total account equity. Under normal market conditions, the risk for most trades will be below this maximum threshold.

Realistic Backtesting Parameters:

Initial Capital: The backtest defaults to an initial capital of $100,000.

Commission: A realistic fee of $5.00 per order is included to simulate broker costs.

5. Disclaimer

This strategy is an educational tool provided for informational and research purposes. It is not financial advice. All trading carries a high level of risk, and past performance is not a guarantee of future results. You are solely responsible for your own trading decisions and risk management. Always conduct your own due diligence before deploying any trading strategy in a live account.

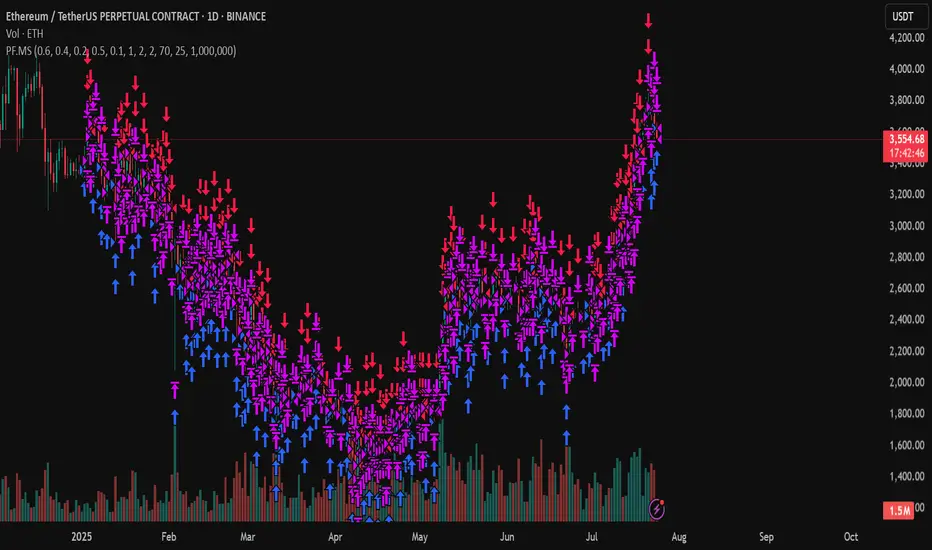

PF.MSThe Pressure & Flow Momentum Strategy (PF.MS) detects market pressure buildup through advanced candlestick analysis and captures momentum flow when conditions align, providing accurate buy and sell signals across cryptocurrencies and stocks—but even sophisticated strategies can be wrong when markets turn brutal without warning. The system reads real-time pressure dynamics (buying vs selling forces, wick patterns, volatility conditions) to identify when smart money is positioning, then captures the resulting momentum flow with precise entry and exit timing. While highly accurate at detecting pressure shifts and momentum changes, the strategy can still face losses during sudden news events or when market sentiment overrides technical patterns. The PF.MS combines intelligent pressure detection with momentum capture, trailing profit protection and strict stop losses

MACD Liquidity Tracker Strategy [Quant Trading]MACD Liquidity Tracker Strategy

Overview

The MACD Liquidity Tracker Strategy is an enhanced trading system that transforms the traditional MACD indicator into a comprehensive momentum-based strategy with advanced visual signals and risk management. This strategy builds upon the original MACD Liquidity Tracker System indicator by TheNeWSystemLqtyTrckr , converting it into a fully automated trading strategy with improved parameters and additional features.

What Makes This Strategy Original

This strategy significantly enhances the basic MACD approach by introducing:

Four distinct system types for different market conditions and trading styles

Advanced color-coded histogram visualization with four dynamic colors showing momentum strength and direction

Integrated trend filtering using 9 different moving average types

Comprehensive risk management with customizable stop-loss and take-profit levels

Multiple alert systems for entry signals, exits, and trend conditions

Flexible signal display options with customizable entry markers

How It Works

Core MACD Calculation

The strategy uses a fully customizable MACD configuration with traditional default parameters:

Fast MA : 12 periods (customizable, minimum 1, no maximum limit)

Slow MA : 26 periods (customizable, minimum 1, no maximum limit)

Signal Line : 9 periods (customizable, now properly implemented and used)

Cryptocurrency Optimization : The strategy's flexible parameter system allows for significant optimization across different crypto assets. Traditional MACD settings (12/26/9) often generate excessive noise and false signals in volatile crypto markets. By using slower, more smoothed parameters, traders can capture meaningful momentum shifts while filtering out market noise.

Example - DOGE Optimization (45/80/290 settings) :

• Performance : Optimized parameters yielding exceptional backtesting results with 29,800% PnL

• Why it works : DOGE's high volatility and social sentiment-driven price action benefits from heavily smoothed indicators

• Timeframes : Particularly effective on 30-minute and 4-hour charts for swing trading

• Logic : The very slow parameters filter out noise and capture only the most significant trend changes

Other Optimizable Cryptocurrencies : This parameter flexibility makes the strategy highly effective for major altcoins including SUI, SEI, LINK, Solana (SOL) , and many others. Each crypto asset can benefit from custom parameter tuning based on its unique volatility profile and trading characteristics.

Four Trading System Types

1. Normal System (Default)

Long signals : When MACD line is above the signal line

Short signals : When MACD line is below the signal line

Best for : Swing trading and capturing longer-term trends in stable markets

Logic : Traditional MACD crossover approach using the signal line

2. Fast System

Long signals : Bright Blue OR Dark Magenta (transparent) histogram colors

Short signals : Dark Blue (transparent) OR Bright Magenta histogram colors

Best for : Scalping and high-volatility markets (crypto, forex)

Logic : Leverages early momentum shifts based on histogram color changes

3. Safe System

Long signals : Only Bright Blue histogram color (strongest bullish momentum)

Short signals : All other colors (Dark Blue, Bright Magenta, Dark Magenta)

Best for : Risk-averse traders and choppy markets

Logic : Prioritizes only the strongest bullish signals while treating everything else as bearish

4. Crossover System

Long signals : MACD line crosses above signal line

Short signals : MACD line crosses below signal line

Best for : Precise timing entries with traditional MACD methodology

Logic : Pure crossover signals for more precise entry timing

Color-Coded Histogram Logic

The strategy uses four distinct colors to visualize momentum:

🔹 Bright Blue : MACD > 0 and rising (strong bullish momentum)

🔹 Dark Blue (Transparent) : MACD > 0 but falling (weakening bullish momentum)

🔹 Bright Magenta : MACD < 0 and falling (strong bearish momentum)

🔹 Dark Magenta (Transparent) : MACD < 0 but rising (weakening bearish momentum)

Trend Filter Integration

The strategy includes an advanced trend filter using 9 different moving average types:

SMA (Simple Moving Average)

EMA (Exponential Moving Average) - Default

WMA (Weighted Moving Average)

HMA (Hull Moving Average)

RMA (Running Moving Average)

LSMA (Least Squares Moving Average)

DEMA (Double Exponential Moving Average)

TEMA (Triple Exponential Moving Average)

VIDYA (Variable Index Dynamic Average)

Default Settings : 50-period EMA for trend identification

Visual Signal System

Entry Markers : Blue triangles (▲) below candles for long entries, Magenta triangles (▼) above candles for short entries

Candle Coloring : Price candles change color based on active signals (Blue = Long, Magenta = Short)

Signal Text : Optional "Long" or "Short" text inside entry triangles (toggleable)

Trend MA : Gray line plotted on main chart for trend reference

Parameter Optimization Examples

DOGE Trading Success (Optimized Parameters) :

Using 45/80/290 MACD settings with 50-period EMA trend filter has shown exceptional results on DOGE:

Performance : Backtesting results showing 29,800% PnL demonstrate the power of proper parameter optimization

Reasoning : DOGE's meme-driven volatility and social sentiment spikes create significant noise with traditional MACD settings

Solution : Very slow parameters (45/80/290) filter out social media-driven price spikes while capturing only major momentum shifts

Optimal Timeframes : 30-minute and 4-hour charts for swing trading opportunities

Result : Exceptionally clean signals with minimal false entries during DOGE's characteristic pump-and-dump cycles

Multi-Crypto Adaptability :

The same optimization principles apply to other major cryptocurrencies:

SUI : Benefits from smoothed parameters due to newer coin volatility patterns

SEI : Requires adjustment for its unique DeFi-related price movements

LINK : Oracle news events create price spikes that benefit from noise filtering

Solana (SOL) : Network congestion events and ecosystem developments need smoothed detection

General Rule : Higher volatility coins typically benefit from very slow MACD parameters (40-50 / 70-90 / 250-300 ranges)

Key Input Parameters

System Type : Choose between Fast, Normal, Safe, or Crossover (Default: Normal)

MACD Fast MA : 12 periods default (no maximum limit, consider 40-50 for crypto optimization)

MACD Slow MA : 26 periods default (no maximum limit, consider 70-90 for crypto optimization)

MACD Signal MA : 9 periods default (now properly utilized, consider 250-300 for crypto optimization)

Trend MA Type : EMA default (9 options available)

Trend MA Length : 50 periods default (no maximum limit)

Signal Display : Both, Long Only, Short Only, or None

Show Signal Text : True/False toggle for entry marker text

Trading Applications

Recommended Use Cases

Momentum Trading : Capitalize on strong directional moves using the color-coded system

Trend Following : Combine MACD signals with trend MA filter for higher probability trades

Scalping : Use "Fast" system type for quick entries in volatile markets

Swing Trading : Use "Normal" or "Safe" system types for longer-term positions

Cryptocurrency Trading : Optimize parameters for individual crypto assets (e.g., 45/80/290 for DOGE, custom settings for SUI, SEI, LINK, SOL)

Market Suitability

Volatile Markets : Forex, crypto, indices (recommend "Fast" system or smoothed parameters)

Stable Markets : Stocks, ETFs (recommend "Normal" or "Safe" system)

All Timeframes : Effective from 1-minute charts to daily charts

Crypto Optimization : Each major cryptocurrency (DOGE, SUI, SEI, LINK, SOL, etc.) can benefit from custom parameter tuning. Consider slower MACD parameters for noise reduction in volatile crypto markets

Alert System

The strategy provides comprehensive alerts for:

Entry Signals : Long and short entry triangle appearances

Exit Signals : Position exit notifications

Color Changes : Individual histogram color alerts

Trend Conditions : Price above/below trend MA alerts

Strategy Parameters

Default Settings

Initial Capital : $1,000

Position Size : 100% of equity

Commission : 0.1%

Slippage : 3 points

Date Range : January 1, 2018 to December 31, 2069

Risk Management (Optional)

Stop Loss : Disabled by default (customizable percentage-based)

Take Profit : Disabled by default (customizable percentage-based)

Short Trades : Disabled by default (can be enabled)

Important Notes and Limitations

Backtesting Considerations

Uses realistic commission (0.1%) and slippage (3 points)

Default position sizing uses 100% equity - adjust based on risk tolerance

Stop-loss and take-profit are disabled by default to show raw strategy performance

Strategy does not use lookahead bias or future data

Risk Warnings

Past performance does not guarantee future results

MACD-based strategies may produce false signals in ranging markets

Consider combining with additional confluences like support/resistance levels

Test thoroughly on demo accounts before live trading

Adjust position sizing based on your risk management requirements

Technical Limitations

Strategy does not work on non-standard chart types (Heikin Ashi, Renko, etc.)

Signals are based on close prices and may not reflect intraday price action

Multiple rapid signals in volatile conditions may result in overtrading

Credits and Attribution

This strategy is based on the original "MACD Liquidity Tracker System" indicator created by TheNeWSystemLqtyTrckr . This strategy version includes significant enhancements:

Complete strategy implementation with entry/exit logic

Addition of the "Crossover" system type

Proper implementation and utilization of the MACD signal line

Enhanced risk management features

Improved parameter flexibility with no artificial maximum limits

Additional alert systems for comprehensive trade management

The original indicator's core color logic and visual system have been preserved while expanding functionality for automated trading applications.

EMA and Dow Theory Strategies🌐 Strategy Description

📘 Overview

This is a hybrid strategy that combines EMA crossovers, Dow Theory swing logic, and multi-timeframe trend overlays. It is suitable for intraday to short-term trading on any asset class: crypto, forex, stocks, and indices.

The strategy provides precise entry/exit signals, dynamic stop-loss and scale-out, and highly visual trade guidance.

🧠 Key Features

・Dual EMA crossover system (applied to both symbol and external index)

・Dow Theory-based swing high/low detection for trend confirmation

・Visual overlay of higher timeframe swing trend (htfTrend)

・RSI filter to avoid overbought/oversold entries

・Dynamic partial take-profit when trend weakens

・Custom stop-loss (%) control

・Visualized trade PnL labels directly on chart

・Alerts for entry, stop-loss, partial exit

・Gradient background zones for swing zones and trend visualization

・Auto-tracked metrics: APR, drawdown, win rate, equity curve

⚙️ Input Parameters

| Parameter | Description |

| ------------------------- | -------------------------------------------------------- |

| Fast EMA / Slow EMA | Periods for detecting local trend via EMAs |

| Index Fast EMA / Slow EMA | EMAs applied to external reference index |

| StopLoss | Maximum loss threshold in % |

| ScaleOut Threshold | Scale-out percentage when trend changes color |

| RSI Period / Levels | RSI period and overbought/oversold levels |

| Swing Detection Length | Number of bars used to detect swing highs/lows |

| Stats Display Options | Toggle PnL labels and position of statistics table |

🧭 About htfTrend (Higher Timeframe Trend)

The script includes a higher timeframe trend (htfTrend) calculated using Dow Theory (pivot highs/lows).

This trend is only used for visual guidance, not for actual entry conditions.

Why? Strictly filtering trades by higher timeframe often leads to missed opportunities and low frequency.

By keeping htfTrend visual-only, traders can still refer to macro structure but retain trade flexibility.

Use it as a contextual tool, not a constraint.

ストラテジー説明

📘 概要

本ストラテジーは、EMAクロスオーバー、ダウ理論によるスイング判定、**上位足トレンドの視覚表示(htfTrend)**を組み合わせた複合型の短期トレーディング戦略です。

仮想通貨・FX・株式・指数など幅広いアセットに対応し、デイトレード〜スキャルピング用途に適しています。

動的な利確/損切り、視覚的にわかりやすいエントリー/イグジット、統計表示を搭載しています。

🧠 主な機能

・対象銘柄+外部インデックスのEMAクロスによるトレンド判定

・ダウ理論に基づいたスイング高値・安値検出とトレンド判断

・上位足スイングトレンド(htfTrend)の視覚表示

・RSIフィルターによる過熱・売られすぎの回避

・トレンドの弱まりに応じた部分利確(スケールアウト)

・**損切り閾値(%)**をカスタマイズ可能

・チャート上に損益ラベル表示

・アラート完備(エントリー・決済・部分利確)

・トレンドゾーンを可視化する背景グラデーション

・勝率・ドローダウン・APR・資産増加率などの自動表示

| 設定項目名 | 説明内容 |

| --------------------- | -------------------------- |

| Fast EMA / Slow EMA | 銘柄に対して使用するEMAの期間設定 |

| Index Fast / Slow EMA | 外部インデックスのEMA設定 |

| 損切り(StopLoss) | 損切りラインのしきい値(%で指定) |

| 部分利確しきい値 | トレンド弱化時にスケールアウトする割合(%) |

| RSI期間・水準 | RSI計算期間と、過熱・売られすぎレベル設定 |

| スイング検出期間 | スイング高値・安値の検出に使用するバー数 |

| 統計表示の切り替え | 損益ラベルや統計テーブルの表示/非表示選択 |

🧭 上位足トレンド(htfTrend)について

本スクリプトには、上位足でのスイング高値・安値の更新に基づく**htfTrend(トレンド判定)が含まれています。

これは視覚的な参考情報であり、エントリーやイグジットには直接使用されていません。**

その理由は、上位足を厳密にロジックに組み込むと、トレード機会の損失が増えるためです。

このスクリプトでは、**判断の補助材料として「表示のみに留める」**設計を採用しています。

→ 裁量で「利確を早める」「逆張りを避ける」判断に活用可能です。

Pullback Pro Dow Strategy v7 (ADX Filter)

### **Strategy Description (For TradingView)**

#### **Title:** Pullback Pro: Dow Theory & ADX Strategy

---

#### **1. Summary**

This strategy is designed to identify and trade pullbacks within an established trend, based on the core principles of Dow Theory. It uses market structure (pivot highs and lows) to determine the trend direction and an Exponential Moving Average (EMA) to pinpoint pullback entry opportunities.

To enhance trade quality and avoid ranging markets, an ADX (Average Directional Index) filter is integrated to ensure that entries are only taken when the trend has sufficient momentum.

---

#### **2. Core Logic: How It Works**

The strategy's logic is broken down into three main steps:

**Step 1: Trend Determination (Dow Theory)**

* The primary trend is identified by analyzing recent pivot points.

* An **Uptrend** is confirmed when the script detects a pattern of higher highs and higher lows (HH/HL).

* A **Downtrend** is confirmed by a pattern of lower highs and lower lows (LH/LL).

* If neither pattern is present, the strategy considers the market to be in a range and will not seek trades.

**Step 2: Entry Signal (Pullback to EMA)**

* Once a clear trend is established, the strategy waits for a price correction.

* **Long Entry:** In a confirmed uptrend, a long position is initiated when the price pulls back and crosses *under* the specified EMA.

* **Short Entry:** In a confirmed downtrend, a short position is initiated when the price rallies and crosses *over* the EMA.

**Step 3: Confirmation & Risk Management**

* **ADX Filter:** To ensure the trend is strong enough to trade, an entry signal is only validated if the ADX value is above a user-defined threshold (e.g., 25). This helps filter out weak signals during choppy or consolidating markets.

* **Stop Loss:** The initial Stop Loss is automatically and logically placed at the last market structure point:

* For long trades, it's placed at the `lastPivotLow`.

* For short trades, it's placed at the `lastPivotHigh`.

* **Take Profit:** Two Take Profit levels are calculated based on user-defined Risk-to-Reward (R:R) ratios. The strategy allows for partial profit-taking at the first target (TP1), moving the remainder of the position to the second target (TP2).

---

#### **3. Input Settings Explained**

**① Dow Theory Settings**

* **Pivot Lookback Period:** Determines the sensitivity for detecting pivot highs and lows. A smaller number makes it more sensitive to recent price swings; a larger number focuses on more significant, longer-term pivots.

**② Entry Logic (Pullback)**

* **Pullback EMA Length:** Sets the period for the Exponential Moving Average used to identify pullback entries.

**③ Risk & Exit Management**

* **Take Profit 1 R:R:** Sets the Risk-to-Reward ratio for the first take-profit target.

* **Take Profit 1 (%):** The percentage of the position to be closed when TP1 is hit.

* **Take Profit 2 R:R:** Sets the Risk-to-Reward ratio for the final take-profit target.

**④ Filters**

* **Use ADX Trend Filter:** A master switch to enable or disable the ADX filter.

* **ADX Length:** The lookback period for the ADX calculation.

* **ADX Threshold:** The minimum ADX value required to confirm a trade signal. Trades will only be placed if the ADX is above this level.

---

#### **4. Best Practices & Recommendations**

* This is a trend-following system. It is designed to perform best in markets that exhibit clear, sustained trending behavior.

* It may underperform in choppy, sideways, or strongly ranging markets. The ADX filter is designed to help mitigate this, but no filter is perfect.

* **Crucially, you must backtest this strategy thoroughly** on your preferred financial instrument and timeframe before considering any live application.

* Experiment with the `Pivot Lookback Period`, `Pullback EMA Length`, and `ADX Threshold` to optimize performance for a specific market's characteristics.

---

#### **DISCLAIMER**

This script is provided for educational and informational purposes only. It does not constitute financial advice. All trading involves a high level of risk, and past performance is not indicative of future results. You are solely responsible for your own trading decisions. The author assumes no liability for any financial losses you may incur from using this strategy. Always conduct your own research and due diligence.

Operator Levels by Trade InsiderOperator Levels by Trade Insider

Overview