"williams"に関するスクリプトを検索

Williams Fractals by Sheridan Sadewa modif untuk menggunakan fractal yang ukurannya lebih kecil dan deket

Williams %R - Multi TimeframeThis indicator implements the William %R multi-timeframe. On the 1H chart, the curves for 1H (with signal), 4H, and 1D are displayed. On the 4H chart, the curves for 4H (with signal) and 1D are shown. On all other timeframes, only the %R and signal are displayed. The indicator is useful to use on 1H and 4H charts to find confluence among the different curves and identify better entries based on their alignment across all timeframes. Signals above 80 often indicate a potential bearish reversal in price, while signals below 20 often suggest a bullish price reversal.

Williams %R SKGThis is William% R indicator alongwith EMA and RSI overbought and oversold background

Williams Alligator Trend Filter HeatmapHello I've decided that the alligator lines can be used to find a trend. This script expands on that and checks 10 different multipliers to see trend over the long term and have 10 values. Those 10 values each give a color to one of the 10 lines in turn giving this Fire like plotting. I personaly use this to see if there is fear (red) in the markets or greed (blue), plotted 9 different crypto coins on the chart and have 4 columns in my setup to see the values on different timeframes. In the chart preview this is 1H,30M,10M,1M to see current environment. The colors use alot of data to generate especialy the bottom part, that colors based on a very long time zone.

Williams %R Color MapThis script is used to have a quick view for my triple screen trading system.

I use it in 1 hour chart so that the higher timeframe is 5-hour and daily.

Visual for the current price on which fib area of 5-hour and daily chart.

Williams Gator Oscillator// The Gator Oscillator histogram above zero shows the absolute difference between blue and red lines of Alligator indicator,

// while histogram below zero shows the absolute difference between red and green lines.

//

// There are green and red bars on the Gator Oscillator histograms.

// A green bar appears when its value is higher than the value of the previous bar.

// A red bars appears when its value is lower than the value of the previous bar.

//

// Gator Oscillator helps to better visualize the upcoming changes in the trends: to know when Alligator sleeps, eats, fills //out and is about to go to sleep.

CCO_LibraryLibrary "CCO_Library"

Contrarian Crowd Oscillator (CCO) Library - Multi-oscillator consensus indicator for contrarian trading signals

@author B3AR_Trades

calculate_oscillators(rsi_length, stoch_length, cci_length, williams_length, roc_length, mfi_length, percentile_lookback, use_rsi, use_stochastic, use_williams, use_cci, use_roc, use_mfi)

Calculate normalized oscillator values

Parameters:

rsi_length (simple int) : (int) RSI calculation period

stoch_length (int) : (int) Stochastic calculation period

cci_length (int) : (int) CCI calculation period

williams_length (int) : (int) Williams %R calculation period

roc_length (int) : (int) ROC calculation period

mfi_length (int) : (int) MFI calculation period

percentile_lookback (int) : (int) Lookback period for CCI/ROC percentile ranking

use_rsi (bool) : (bool) Include RSI in calculations

use_stochastic (bool) : (bool) Include Stochastic in calculations

use_williams (bool) : (bool) Include Williams %R in calculations

use_cci (bool) : (bool) Include CCI in calculations

use_roc (bool) : (bool) Include ROC in calculations

use_mfi (bool) : (bool) Include MFI in calculations

Returns: (OscillatorValues) Normalized oscillator values

calculate_consensus_score(oscillators, use_rsi, use_stochastic, use_williams, use_cci, use_roc, use_mfi, weight_by_reliability, consensus_smoothing)

Calculate weighted consensus score

Parameters:

oscillators (OscillatorValues) : (OscillatorValues) Individual oscillator values

use_rsi (bool) : (bool) Include RSI in consensus

use_stochastic (bool) : (bool) Include Stochastic in consensus

use_williams (bool) : (bool) Include Williams %R in consensus

use_cci (bool) : (bool) Include CCI in consensus

use_roc (bool) : (bool) Include ROC in consensus

use_mfi (bool) : (bool) Include MFI in consensus

weight_by_reliability (bool) : (bool) Apply reliability-based weights

consensus_smoothing (int) : (int) Smoothing period for consensus

Returns: (float) Weighted consensus score (0-100)

calculate_consensus_strength(oscillators, consensus_score, use_rsi, use_stochastic, use_williams, use_cci, use_roc, use_mfi)

Calculate consensus strength (agreement between oscillators)

Parameters:

oscillators (OscillatorValues) : (OscillatorValues) Individual oscillator values

consensus_score (float) : (float) Current consensus score

use_rsi (bool) : (bool) Include RSI in strength calculation

use_stochastic (bool) : (bool) Include Stochastic in strength calculation

use_williams (bool) : (bool) Include Williams %R in strength calculation

use_cci (bool) : (bool) Include CCI in strength calculation

use_roc (bool) : (bool) Include ROC in strength calculation

use_mfi (bool) : (bool) Include MFI in strength calculation

Returns: (float) Consensus strength (0-100)

classify_regime(consensus_score)

Classify consensus regime

Parameters:

consensus_score (float) : (float) Current consensus score

Returns: (ConsensusRegime) Regime classification

detect_signals(consensus_score, consensus_strength, consensus_momentum, regime)

Detect trading signals

Parameters:

consensus_score (float) : (float) Current consensus score

consensus_strength (float) : (float) Current consensus strength

consensus_momentum (float) : (float) Consensus momentum

regime (ConsensusRegime) : (ConsensusRegime) Current regime classification

Returns: (TradingSignals) Trading signal conditions

calculate_cco(rsi_length, stoch_length, cci_length, williams_length, roc_length, mfi_length, consensus_smoothing, percentile_lookback, use_rsi, use_stochastic, use_williams, use_cci, use_roc, use_mfi, weight_by_reliability, detect_momentum)

Calculate complete CCO analysis

Parameters:

rsi_length (simple int) : (int) RSI calculation period

stoch_length (int) : (int) Stochastic calculation period

cci_length (int) : (int) CCI calculation period

williams_length (int) : (int) Williams %R calculation period

roc_length (int) : (int) ROC calculation period

mfi_length (int) : (int) MFI calculation period

consensus_smoothing (int) : (int) Consensus smoothing period

percentile_lookback (int) : (int) Percentile ranking lookback

use_rsi (bool) : (bool) Include RSI

use_stochastic (bool) : (bool) Include Stochastic

use_williams (bool) : (bool) Include Williams %R

use_cci (bool) : (bool) Include CCI

use_roc (bool) : (bool) Include ROC

use_mfi (bool) : (bool) Include MFI

weight_by_reliability (bool) : (bool) Apply reliability weights

detect_momentum (bool) : (bool) Calculate momentum and acceleration

Returns: (CCOResult) Complete CCO analysis results

calculate_cco_default()

Calculate CCO with default parameters

Returns: (CCOResult) CCO result with standard settings

cco_consensus_score()

Get just the consensus score with default parameters

Returns: (float) Consensus score (0-100)

cco_consensus_strength()

Get just the consensus strength with default parameters

Returns: (float) Consensus strength (0-100)

is_panic_bottom()

Check if in panic bottom condition

Returns: (bool) True if panic bottom signal active

is_euphoric_top()

Check if in euphoric top condition

Returns: (bool) True if euphoric top signal active

bullish_consensus_reversal()

Check for bullish consensus reversal

Returns: (bool) True if bullish reversal detected

bearish_consensus_reversal()

Check for bearish consensus reversal

Returns: (bool) True if bearish reversal detected

bearish_divergence()

Check for bearish divergence

Returns: (bool) True if bearish divergence detected

bullish_divergence()

Check for bullish divergence

Returns: (bool) True if bullish divergence detected

get_regime_name()

Get current regime name

Returns: (string) Current consensus regime name

get_contrarian_signal()

Get contrarian signal

Returns: (string) Current contrarian trading signal

get_position_multiplier()

Get position size multiplier

Returns: (float) Recommended position sizing multiplier

OscillatorValues

Individual oscillator values

Fields:

rsi (series float) : RSI value (0-100)

stochastic (series float) : Stochastic value (0-100)

williams (series float) : Williams %R value (0-100, normalized)

cci (series float) : CCI percentile value (0-100)

roc (series float) : ROC percentile value (0-100)

mfi (series float) : Money Flow Index value (0-100)

ConsensusRegime

Consensus regime classification

Fields:

extreme_bearish (series bool) : Extreme bearish consensus (<= 20)

moderate_bearish (series bool) : Moderate bearish consensus (20-40)

mixed (series bool) : Mixed consensus (40-60)

moderate_bullish (series bool) : Moderate bullish consensus (60-80)

extreme_bullish (series bool) : Extreme bullish consensus (>= 80)

regime_name (series string) : Text description of current regime

contrarian_signal (series string) : Contrarian trading signal

TradingSignals

Trading signals

Fields:

panic_bottom_signal (series bool) : Extreme bearish consensus with high strength

euphoric_top_signal (series bool) : Extreme bullish consensus with high strength

consensus_reversal_bullish (series bool) : Bullish consensus reversal

consensus_reversal_bearish (series bool) : Bearish consensus reversal

bearish_divergence (series bool) : Bearish price-consensus divergence

bullish_divergence (series bool) : Bullish price-consensus divergence

strong_consensus (series bool) : High consensus strength signal

CCOResult

Complete CCO calculation results

Fields:

consensus_score (series float) : Main consensus score (0-100)

consensus_strength (series float) : Consensus strength (0-100)

consensus_momentum (series float) : Rate of consensus change

consensus_acceleration (series float) : Rate of momentum change

oscillators (OscillatorValues) : Individual oscillator values

regime (ConsensusRegime) : Regime classification

signals (TradingSignals) : Trading signals

position_multiplier (series float) : Recommended position sizing multiplier

Markov Chain [3D] | FractalystWhat exactly is a Markov Chain?

This indicator uses a Markov Chain model to analyze, quantify, and visualize the transitions between market regimes (Bull, Bear, Neutral) on your chart. It dynamically detects these regimes in real-time, calculates transition probabilities, and displays them as animated 3D spheres and arrows, giving traders intuitive insight into current and future market conditions.

How does a Markov Chain work, and how should I read this spheres-and-arrows diagram?

Think of three weather modes: Sunny, Rainy, Cloudy.

Each sphere is one mode. The loop on a sphere means “stay the same next step” (e.g., Sunny again tomorrow).

The arrows leaving a sphere show where things usually go next if they change (e.g., Sunny moving to Cloudy).

Some paths matter more than others. A more prominent loop means the current mode tends to persist. A more prominent outgoing arrow means a change to that destination is the usual next step.

Direction isn’t symmetric: moving Sunny→Cloudy can behave differently than Cloudy→Sunny.

Now relabel the spheres to markets: Bull, Bear, Neutral.

Spheres: market regimes (uptrend, downtrend, range).

Self‑loop: tendency for the current regime to continue on the next bar.

Arrows: the most common next regime if a switch happens.

How to read: Start at the sphere that matches current bar state. If the loop stands out, expect continuation. If one outgoing path stands out, that switch is the typical next step. Opposite directions can differ (Bear→Neutral doesn’t have to match Neutral→Bear).

What states and transitions are shown?

The three market states visualized are:

Bullish (Bull): Upward or strong-market regime.

Bearish (Bear): Downward or weak-market regime.

Neutral: Sideways or range-bound regime.

Bidirectional animated arrows and probability labels show how likely the market is to move from one regime to another (e.g., Bull → Bear or Neutral → Bull).

How does the regime detection system work?

You can use either built-in price returns (based on adaptive Z-score normalization) or supply three custom indicators (such as volume, oscillators, etc.).

Values are statistically normalized (Z-scored) over a configurable lookback period.

The normalized outputs are classified into Bull, Bear, or Neutral zones.

If using three indicators, their regime signals are averaged and smoothed for robustness.

How are transition probabilities calculated?

On every confirmed bar, the algorithm tracks the sequence of detected market states, then builds a rolling window of transitions.

The code maintains a transition count matrix for all regime pairs (e.g., Bull → Bear).

Transition probabilities are extracted for each possible state change using Laplace smoothing for numerical stability, and frequently updated in real-time.

What is unique about the visualization?

3D animated spheres represent each regime and change visually when active.

Animated, bidirectional arrows reveal transition probabilities and allow you to see both dominant and less likely regime flows.

Particles (moving dots) animate along the arrows, enhancing the perception of regime flow direction and speed.

All elements dynamically update with each new price bar, providing a live market map in an intuitive, engaging format.

Can I use custom indicators for regime classification?

Yes! Enable the "Custom Indicators" switch and select any three chart series as inputs. These will be normalized and combined (each with equal weight), broadening the regime classification beyond just price-based movement.

What does the “Lookback Period” control?

Lookback Period (default: 100) sets how much historical data builds the probability matrix. Shorter periods adapt faster to regime changes but may be noisier. Longer periods are more stable but slower to adapt.

How is this different from a Hidden Markov Model (HMM)?

It sets the window for both regime detection and probability calculations. Lower values make the system more reactive, but potentially noisier. Higher values smooth estimates and make the system more robust.

How is this Markov Chain different from a Hidden Markov Model (HMM)?

Markov Chain (as here): All market regimes (Bull, Bear, Neutral) are directly observable on the chart. The transition matrix is built from actual detected regimes, keeping the model simple and interpretable.

Hidden Markov Model: The actual regimes are unobservable ("hidden") and must be inferred from market output or indicator "emissions" using statistical learning algorithms. HMMs are more complex, can capture more subtle structure, but are harder to visualize and require additional machine learning steps for training.

A standard Markov Chain models transitions between observable states using a simple transition matrix, while a Hidden Markov Model assumes the true states are hidden (latent) and must be inferred from observable “emissions” like price or volume data. In practical terms, a Markov Chain is transparent and easier to implement and interpret; an HMM is more expressive but requires statistical inference to estimate hidden states from data.

Markov Chain: states are observable; you directly count or estimate transition probabilities between visible states. This makes it simpler, faster, and easier to validate and tune.

HMM: states are hidden; you only observe emissions generated by those latent states. Learning involves machine learning/statistical algorithms (commonly Baum–Welch/EM for training and Viterbi for decoding) to infer both the transition dynamics and the most likely hidden state sequence from data.

How does the indicator avoid “repainting” or look-ahead bias?

All regime changes and matrix updates happen only on confirmed (closed) bars, so no future data is leaked, ensuring reliable real-time operation.

Are there practical tuning tips?

Tune the Lookback Period for your asset/timeframe: shorter for fast markets, longer for stability.

Use custom indicators if your asset has unique regime drivers.

Watch for rapid changes in transition probabilities as early warning of a possible regime shift.

Who is this indicator for?

Quants and quantitative researchers exploring probabilistic market modeling, especially those interested in regime-switching dynamics and Markov models.

Programmers and system developers who need a probabilistic regime filter for systematic and algorithmic backtesting:

The Markov Chain indicator is ideally suited for programmatic integration via its bias output (1 = Bull, 0 = Neutral, -1 = Bear).

Although the visualization is engaging, the core output is designed for automated, rules-based workflows—not for discretionary/manual trading decisions.

Developers can connect the indicator’s output directly to their Pine Script logic (using input.source()), allowing rapid and robust backtesting of regime-based strategies.

It acts as a plug-and-play regime filter: simply plug the bias output into your entry/exit logic, and you have a scientifically robust, probabilistically-derived signal for filtering, timing, position sizing, or risk regimes.

The MC's output is intentionally "trinary" (1/0/-1), focusing on clear regime states for unambiguous decision-making in code. If you require nuanced, multi-probability or soft-label state vectors, consider expanding the indicator or stacking it with a probability-weighted logic layer in your scripting.

Because it avoids subjectivity, this approach is optimal for systematic quants, algo developers building backtested, repeatable strategies based on probabilistic regime analysis.

What's the mathematical foundation behind this?

The mathematical foundation behind this Markov Chain indicator—and probabilistic regime detection in finance—draws from two principal models: the (standard) Markov Chain and the Hidden Markov Model (HMM).

How to use this indicator programmatically?

The Markov Chain indicator automatically exports a bias value (+1 for Bullish, -1 for Bearish, 0 for Neutral) as a plot visible in the Data Window. This allows you to integrate its regime signal into your own scripts and strategies for backtesting, automation, or live trading.

Step-by-Step Integration with Pine Script (input.source)

Add the Markov Chain indicator to your chart.

This must be done first, since your custom script will "pull" the bias signal from the indicator's plot.

In your strategy, create an input using input.source()

Example:

//@version=5

strategy("MC Bias Strategy Example")

mcBias = input.source(close, "MC Bias Source")

After saving, go to your script’s settings. For the “MC Bias Source” input, select the plot/output of the Markov Chain indicator (typically its bias plot).

Use the bias in your trading logic

Example (long only on Bull, flat otherwise):

if mcBias == 1

strategy.entry("Long", strategy.long)

else

strategy.close("Long")

For more advanced workflows, combine mcBias with additional filters or trailing stops.

How does this work behind-the-scenes?

TradingView’s input.source() lets you use any plot from another indicator as a real-time, “live” data feed in your own script (source).

The selected bias signal is available to your Pine code as a variable, enabling logical decisions based on regime (trend-following, mean-reversion, etc.).

This enables powerful strategy modularity : decouple regime detection from entry/exit logic, allowing fast experimentation without rewriting core signal code.

Integrating 45+ Indicators with Your Markov Chain — How & Why

The Enhanced Custom Indicators Export script exports a massive suite of over 45 technical indicators—ranging from classic momentum (RSI, MACD, Stochastic, etc.) to trend, volume, volatility, and oscillator tools—all pre-calculated, centered/scaled, and available as plots.

// Enhanced Custom Indicators Export - 45 Technical Indicators

// Comprehensive technical analysis suite for advanced market regime detection

//@version=6

indicator('Enhanced Custom Indicators Export | Fractalyst', shorttitle='Enhanced CI Export', overlay=false, scale=scale.right, max_labels_count=500, max_lines_count=500)

// |----- Input Parameters -----| //

momentum_group = "Momentum Indicators"

trend_group = "Trend Indicators"

volume_group = "Volume Indicators"

volatility_group = "Volatility Indicators"

oscillator_group = "Oscillator Indicators"

display_group = "Display Settings"

// Common lengths

length_14 = input.int(14, "Standard Length (14)", minval=1, maxval=100, group=momentum_group)

length_20 = input.int(20, "Medium Length (20)", minval=1, maxval=200, group=trend_group)

length_50 = input.int(50, "Long Length (50)", minval=1, maxval=200, group=trend_group)

// Display options

show_table = input.bool(true, "Show Values Table", group=display_group)

table_size = input.string("Small", "Table Size", options= , group=display_group)

// |----- MOMENTUM INDICATORS (15 indicators) -----| //

// 1. RSI (Relative Strength Index)

rsi_14 = ta.rsi(close, length_14)

rsi_centered = rsi_14 - 50

// 2. Stochastic Oscillator

stoch_k = ta.stoch(close, high, low, length_14)

stoch_d = ta.sma(stoch_k, 3)

stoch_centered = stoch_k - 50

// 3. Williams %R

williams_r = ta.stoch(close, high, low, length_14) - 100

// 4. MACD (Moving Average Convergence Divergence)

= ta.macd(close, 12, 26, 9)

// 5. Momentum (Rate of Change)

momentum = ta.mom(close, length_14)

momentum_pct = (momentum / close ) * 100

// 6. Rate of Change (ROC)

roc = ta.roc(close, length_14)

// 7. Commodity Channel Index (CCI)

cci = ta.cci(close, length_20)

// 8. Money Flow Index (MFI)

mfi = ta.mfi(close, length_14)

mfi_centered = mfi - 50

// 9. Awesome Oscillator (AO)

ao = ta.sma(hl2, 5) - ta.sma(hl2, 34)

// 10. Accelerator Oscillator (AC)

ac = ao - ta.sma(ao, 5)

// 11. Chande Momentum Oscillator (CMO)

cmo = ta.cmo(close, length_14)

// 12. Detrended Price Oscillator (DPO)

dpo = close - ta.sma(close, length_20)

// 13. Price Oscillator (PPO)

ppo = ta.sma(close, 12) - ta.sma(close, 26)

ppo_pct = (ppo / ta.sma(close, 26)) * 100

// 14. TRIX

trix_ema1 = ta.ema(close, length_14)

trix_ema2 = ta.ema(trix_ema1, length_14)

trix_ema3 = ta.ema(trix_ema2, length_14)

trix = ta.roc(trix_ema3, 1) * 10000

// 15. Klinger Oscillator

klinger = ta.ema(volume * (high + low + close) / 3, 34) - ta.ema(volume * (high + low + close) / 3, 55)

// 16. Fisher Transform

fisher_hl2 = 0.5 * (hl2 - ta.lowest(hl2, 10)) / (ta.highest(hl2, 10) - ta.lowest(hl2, 10)) - 0.25

fisher = 0.5 * math.log((1 + fisher_hl2) / (1 - fisher_hl2))

// 17. Stochastic RSI

stoch_rsi = ta.stoch(rsi_14, rsi_14, rsi_14, length_14)

stoch_rsi_centered = stoch_rsi - 50

// 18. Relative Vigor Index (RVI)

rvi_num = ta.swma(close - open)

rvi_den = ta.swma(high - low)

rvi = rvi_den != 0 ? rvi_num / rvi_den : 0

// 19. Balance of Power (BOP)

bop = (close - open) / (high - low)

// |----- TREND INDICATORS (10 indicators) -----| //

// 20. Simple Moving Average Momentum

sma_20 = ta.sma(close, length_20)

sma_momentum = ((close - sma_20) / sma_20) * 100

// 21. Exponential Moving Average Momentum

ema_20 = ta.ema(close, length_20)

ema_momentum = ((close - ema_20) / ema_20) * 100

// 22. Parabolic SAR

sar = ta.sar(0.02, 0.02, 0.2)

sar_trend = close > sar ? 1 : -1

// 23. Linear Regression Slope

lr_slope = ta.linreg(close, length_20, 0) - ta.linreg(close, length_20, 1)

// 24. Moving Average Convergence (MAC)

mac = ta.sma(close, 10) - ta.sma(close, 30)

// 25. Trend Intensity Index (TII)

tii_sum = 0.0

for i = 1 to length_20

tii_sum += close > close ? 1 : 0

tii = (tii_sum / length_20) * 100

// 26. Ichimoku Cloud Components

ichimoku_tenkan = (ta.highest(high, 9) + ta.lowest(low, 9)) / 2

ichimoku_kijun = (ta.highest(high, 26) + ta.lowest(low, 26)) / 2

ichimoku_signal = ichimoku_tenkan > ichimoku_kijun ? 1 : -1

// 27. MESA Adaptive Moving Average (MAMA)

mama_alpha = 2.0 / (length_20 + 1)

mama = ta.ema(close, length_20)

mama_momentum = ((close - mama) / mama) * 100

// 28. Zero Lag Exponential Moving Average (ZLEMA)

zlema_lag = math.round((length_20 - 1) / 2)

zlema_data = close + (close - close )

zlema = ta.ema(zlema_data, length_20)

zlema_momentum = ((close - zlema) / zlema) * 100

// |----- VOLUME INDICATORS (6 indicators) -----| //

// 29. On-Balance Volume (OBV)

obv = ta.obv

// 30. Volume Rate of Change (VROC)

vroc = ta.roc(volume, length_14)

// 31. Price Volume Trend (PVT)

pvt = ta.pvt

// 32. Negative Volume Index (NVI)

nvi = 0.0

nvi := volume < volume ? nvi + ((close - close ) / close ) * nvi : nvi

// 33. Positive Volume Index (PVI)

pvi = 0.0

pvi := volume > volume ? pvi + ((close - close ) / close ) * pvi : pvi

// 34. Volume Oscillator

vol_osc = ta.sma(volume, 5) - ta.sma(volume, 10)

// 35. Ease of Movement (EOM)

eom_distance = high - low

eom_box_height = volume / 1000000

eom = eom_box_height != 0 ? eom_distance / eom_box_height : 0

eom_sma = ta.sma(eom, length_14)

// 36. Force Index

force_index = volume * (close - close )

force_index_sma = ta.sma(force_index, length_14)

// |----- VOLATILITY INDICATORS (10 indicators) -----| //

// 37. Average True Range (ATR)

atr = ta.atr(length_14)

atr_pct = (atr / close) * 100

// 38. Bollinger Bands Position

bb_basis = ta.sma(close, length_20)

bb_dev = 2.0 * ta.stdev(close, length_20)

bb_upper = bb_basis + bb_dev

bb_lower = bb_basis - bb_dev

bb_position = bb_dev != 0 ? (close - bb_basis) / bb_dev : 0

bb_width = bb_dev != 0 ? (bb_upper - bb_lower) / bb_basis * 100 : 0

// 39. Keltner Channels Position

kc_basis = ta.ema(close, length_20)

kc_range = ta.ema(ta.tr, length_20)

kc_upper = kc_basis + (2.0 * kc_range)

kc_lower = kc_basis - (2.0 * kc_range)

kc_position = kc_range != 0 ? (close - kc_basis) / kc_range : 0

// 40. Donchian Channels Position

dc_upper = ta.highest(high, length_20)

dc_lower = ta.lowest(low, length_20)

dc_basis = (dc_upper + dc_lower) / 2

dc_position = (dc_upper - dc_lower) != 0 ? (close - dc_basis) / (dc_upper - dc_lower) : 0

// 41. Standard Deviation

std_dev = ta.stdev(close, length_20)

std_dev_pct = (std_dev / close) * 100

// 42. Relative Volatility Index (RVI)

rvi_up = ta.stdev(close > close ? close : 0, length_14)

rvi_down = ta.stdev(close < close ? close : 0, length_14)

rvi_total = rvi_up + rvi_down

rvi_volatility = rvi_total != 0 ? (rvi_up / rvi_total) * 100 : 50

// 43. Historical Volatility

hv_returns = math.log(close / close )

hv = ta.stdev(hv_returns, length_20) * math.sqrt(252) * 100

// 44. Garman-Klass Volatility

gk_vol = math.log(high/low) * math.log(high/low) - (2*math.log(2)-1) * math.log(close/open) * math.log(close/open)

gk_volatility = math.sqrt(ta.sma(gk_vol, length_20)) * 100

// 45. Parkinson Volatility

park_vol = math.log(high/low) * math.log(high/low)

parkinson = math.sqrt(ta.sma(park_vol, length_20) / (4 * math.log(2))) * 100

// 46. Rogers-Satchell Volatility

rs_vol = math.log(high/close) * math.log(high/open) + math.log(low/close) * math.log(low/open)

rogers_satchell = math.sqrt(ta.sma(rs_vol, length_20)) * 100

// |----- OSCILLATOR INDICATORS (5 indicators) -----| //

// 47. Elder Ray Index

elder_bull = high - ta.ema(close, 13)

elder_bear = low - ta.ema(close, 13)

elder_power = elder_bull + elder_bear

// 48. Schaff Trend Cycle (STC)

stc_macd = ta.ema(close, 23) - ta.ema(close, 50)

stc_k = ta.stoch(stc_macd, stc_macd, stc_macd, 10)

stc_d = ta.ema(stc_k, 3)

stc = ta.stoch(stc_d, stc_d, stc_d, 10)

// 49. Coppock Curve

coppock_roc1 = ta.roc(close, 14)

coppock_roc2 = ta.roc(close, 11)

coppock = ta.wma(coppock_roc1 + coppock_roc2, 10)

// 50. Know Sure Thing (KST)

kst_roc1 = ta.roc(close, 10)

kst_roc2 = ta.roc(close, 15)

kst_roc3 = ta.roc(close, 20)

kst_roc4 = ta.roc(close, 30)

kst = ta.sma(kst_roc1, 10) + 2*ta.sma(kst_roc2, 10) + 3*ta.sma(kst_roc3, 10) + 4*ta.sma(kst_roc4, 15)

// 51. Percentage Price Oscillator (PPO)

ppo_line = ((ta.ema(close, 12) - ta.ema(close, 26)) / ta.ema(close, 26)) * 100

ppo_signal = ta.ema(ppo_line, 9)

ppo_histogram = ppo_line - ppo_signal

// |----- PLOT MAIN INDICATORS -----| //

// Plot key momentum indicators

plot(rsi_centered, title="01_RSI_Centered", color=color.purple, linewidth=1)

plot(stoch_centered, title="02_Stoch_Centered", color=color.blue, linewidth=1)

plot(williams_r, title="03_Williams_R", color=color.red, linewidth=1)

plot(macd_histogram, title="04_MACD_Histogram", color=color.orange, linewidth=1)

plot(cci, title="05_CCI", color=color.green, linewidth=1)

// Plot trend indicators

plot(sma_momentum, title="06_SMA_Momentum", color=color.navy, linewidth=1)

plot(ema_momentum, title="07_EMA_Momentum", color=color.maroon, linewidth=1)

plot(sar_trend, title="08_SAR_Trend", color=color.teal, linewidth=1)

plot(lr_slope, title="09_LR_Slope", color=color.lime, linewidth=1)

plot(mac, title="10_MAC", color=color.fuchsia, linewidth=1)

// Plot volatility indicators

plot(atr_pct, title="11_ATR_Pct", color=color.yellow, linewidth=1)

plot(bb_position, title="12_BB_Position", color=color.aqua, linewidth=1)

plot(kc_position, title="13_KC_Position", color=color.olive, linewidth=1)

plot(std_dev_pct, title="14_StdDev_Pct", color=color.silver, linewidth=1)

plot(bb_width, title="15_BB_Width", color=color.gray, linewidth=1)

// Plot volume indicators

plot(vroc, title="16_VROC", color=color.blue, linewidth=1)

plot(eom_sma, title="17_EOM", color=color.red, linewidth=1)

plot(vol_osc, title="18_Vol_Osc", color=color.green, linewidth=1)

plot(force_index_sma, title="19_Force_Index", color=color.orange, linewidth=1)

plot(obv, title="20_OBV", color=color.purple, linewidth=1)

// Plot additional oscillators

plot(ao, title="21_Awesome_Osc", color=color.navy, linewidth=1)

plot(cmo, title="22_CMO", color=color.maroon, linewidth=1)

plot(dpo, title="23_DPO", color=color.teal, linewidth=1)

plot(trix, title="24_TRIX", color=color.lime, linewidth=1)

plot(fisher, title="25_Fisher", color=color.fuchsia, linewidth=1)

// Plot more momentum indicators

plot(mfi_centered, title="26_MFI_Centered", color=color.yellow, linewidth=1)

plot(ac, title="27_AC", color=color.aqua, linewidth=1)

plot(ppo_pct, title="28_PPO_Pct", color=color.olive, linewidth=1)

plot(stoch_rsi_centered, title="29_StochRSI_Centered", color=color.silver, linewidth=1)

plot(klinger, title="30_Klinger", color=color.gray, linewidth=1)

// Plot trend continuation

plot(tii, title="31_TII", color=color.blue, linewidth=1)

plot(ichimoku_signal, title="32_Ichimoku_Signal", color=color.red, linewidth=1)

plot(mama_momentum, title="33_MAMA_Momentum", color=color.green, linewidth=1)

plot(zlema_momentum, title="34_ZLEMA_Momentum", color=color.orange, linewidth=1)

plot(bop, title="35_BOP", color=color.purple, linewidth=1)

// Plot volume continuation

plot(nvi, title="36_NVI", color=color.navy, linewidth=1)

plot(pvi, title="37_PVI", color=color.maroon, linewidth=1)

plot(momentum_pct, title="38_Momentum_Pct", color=color.teal, linewidth=1)

plot(roc, title="39_ROC", color=color.lime, linewidth=1)

plot(rvi, title="40_RVI", color=color.fuchsia, linewidth=1)

// Plot volatility continuation

plot(dc_position, title="41_DC_Position", color=color.yellow, linewidth=1)

plot(rvi_volatility, title="42_RVI_Volatility", color=color.aqua, linewidth=1)

plot(hv, title="43_Historical_Vol", color=color.olive, linewidth=1)

plot(gk_volatility, title="44_GK_Volatility", color=color.silver, linewidth=1)

plot(parkinson, title="45_Parkinson_Vol", color=color.gray, linewidth=1)

// Plot final oscillators

plot(rogers_satchell, title="46_RS_Volatility", color=color.blue, linewidth=1)

plot(elder_power, title="47_Elder_Power", color=color.red, linewidth=1)

plot(stc, title="48_STC", color=color.green, linewidth=1)

plot(coppock, title="49_Coppock", color=color.orange, linewidth=1)

plot(kst, title="50_KST", color=color.purple, linewidth=1)

// Plot final indicators

plot(ppo_histogram, title="51_PPO_Histogram", color=color.navy, linewidth=1)

plot(pvt, title="52_PVT", color=color.maroon, linewidth=1)

// |----- Reference Lines -----| //

hline(0, "Zero Line", color=color.gray, linestyle=hline.style_dashed, linewidth=1)

hline(50, "Midline", color=color.gray, linestyle=hline.style_dotted, linewidth=1)

hline(-50, "Lower Midline", color=color.gray, linestyle=hline.style_dotted, linewidth=1)

hline(25, "Upper Threshold", color=color.gray, linestyle=hline.style_dotted, linewidth=1)

hline(-25, "Lower Threshold", color=color.gray, linestyle=hline.style_dotted, linewidth=1)

// |----- Enhanced Information Table -----| //

if show_table and barstate.islast

table_position = position.top_right

table_text_size = table_size == "Tiny" ? size.tiny : table_size == "Small" ? size.small : size.normal

var table info_table = table.new(table_position, 3, 18, bgcolor=color.new(color.white, 85), border_width=1, border_color=color.gray)

// Headers

table.cell(info_table, 0, 0, 'Category', text_color=color.black, text_size=table_text_size, bgcolor=color.new(color.blue, 70))

table.cell(info_table, 1, 0, 'Indicator', text_color=color.black, text_size=table_text_size, bgcolor=color.new(color.blue, 70))

table.cell(info_table, 2, 0, 'Value', text_color=color.black, text_size=table_text_size, bgcolor=color.new(color.blue, 70))

// Key Momentum Indicators

table.cell(info_table, 0, 1, 'MOMENTUM', text_color=color.purple, text_size=table_text_size, bgcolor=color.new(color.purple, 90))

table.cell(info_table, 1, 1, 'RSI Centered', text_color=color.purple, text_size=table_text_size)

table.cell(info_table, 2, 1, str.tostring(rsi_centered, '0.00'), text_color=color.purple, text_size=table_text_size)

table.cell(info_table, 0, 2, '', text_color=color.blue, text_size=table_text_size)

table.cell(info_table, 1, 2, 'Stoch Centered', text_color=color.blue, text_size=table_text_size)

table.cell(info_table, 2, 2, str.tostring(stoch_centered, '0.00'), text_color=color.blue, text_size=table_text_size)

table.cell(info_table, 0, 3, '', text_color=color.red, text_size=table_text_size)

table.cell(info_table, 1, 3, 'Williams %R', text_color=color.red, text_size=table_text_size)

table.cell(info_table, 2, 3, str.tostring(williams_r, '0.00'), text_color=color.red, text_size=table_text_size)

table.cell(info_table, 0, 4, '', text_color=color.orange, text_size=table_text_size)

table.cell(info_table, 1, 4, 'MACD Histogram', text_color=color.orange, text_size=table_text_size)

table.cell(info_table, 2, 4, str.tostring(macd_histogram, '0.000'), text_color=color.orange, text_size=table_text_size)

table.cell(info_table, 0, 5, '', text_color=color.green, text_size=table_text_size)

table.cell(info_table, 1, 5, 'CCI', text_color=color.green, text_size=table_text_size)

table.cell(info_table, 2, 5, str.tostring(cci, '0.00'), text_color=color.green, text_size=table_text_size)

// Key Trend Indicators

table.cell(info_table, 0, 6, 'TREND', text_color=color.navy, text_size=table_text_size, bgcolor=color.new(color.navy, 90))

table.cell(info_table, 1, 6, 'SMA Momentum %', text_color=color.navy, text_size=table_text_size)

table.cell(info_table, 2, 6, str.tostring(sma_momentum, '0.00'), text_color=color.navy, text_size=table_text_size)

table.cell(info_table, 0, 7, '', text_color=color.maroon, text_size=table_text_size)

table.cell(info_table, 1, 7, 'EMA Momentum %', text_color=color.maroon, text_size=table_text_size)

table.cell(info_table, 2, 7, str.tostring(ema_momentum, '0.00'), text_color=color.maroon, text_size=table_text_size)

table.cell(info_table, 0, 8, '', text_color=color.teal, text_size=table_text_size)

table.cell(info_table, 1, 8, 'SAR Trend', text_color=color.teal, text_size=table_text_size)

table.cell(info_table, 2, 8, str.tostring(sar_trend, '0'), text_color=color.teal, text_size=table_text_size)

table.cell(info_table, 0, 9, '', text_color=color.lime, text_size=table_text_size)

table.cell(info_table, 1, 9, 'Linear Regression', text_color=color.lime, text_size=table_text_size)

table.cell(info_table, 2, 9, str.tostring(lr_slope, '0.000'), text_color=color.lime, text_size=table_text_size)

// Key Volatility Indicators

table.cell(info_table, 0, 10, 'VOLATILITY', text_color=color.yellow, text_size=table_text_size, bgcolor=color.new(color.yellow, 90))

table.cell(info_table, 1, 10, 'ATR %', text_color=color.yellow, text_size=table_text_size)

table.cell(info_table, 2, 10, str.tostring(atr_pct, '0.00'), text_color=color.yellow, text_size=table_text_size)

table.cell(info_table, 0, 11, '', text_color=color.aqua, text_size=table_text_size)

table.cell(info_table, 1, 11, 'BB Position', text_color=color.aqua, text_size=table_text_size)

table.cell(info_table, 2, 11, str.tostring(bb_position, '0.00'), text_color=color.aqua, text_size=table_text_size)

table.cell(info_table, 0, 12, '', text_color=color.olive, text_size=table_text_size)

table.cell(info_table, 1, 12, 'KC Position', text_color=color.olive, text_size=table_text_size)

table.cell(info_table, 2, 12, str.tostring(kc_position, '0.00'), text_color=color.olive, text_size=table_text_size)

// Key Volume Indicators

table.cell(info_table, 0, 13, 'VOLUME', text_color=color.blue, text_size=table_text_size, bgcolor=color.new(color.blue, 90))

table.cell(info_table, 1, 13, 'Volume ROC', text_color=color.blue, text_size=table_text_size)

table.cell(info_table, 2, 13, str.tostring(vroc, '0.00'), text_color=color.blue, text_size=table_text_size)

table.cell(info_table, 0, 14, '', text_color=color.red, text_size=table_text_size)

table.cell(info_table, 1, 14, 'EOM', text_color=color.red, text_size=table_text_size)

table.cell(info_table, 2, 14, str.tostring(eom_sma, '0.000'), text_color=color.red, text_size=table_text_size)

// Key Oscillators

table.cell(info_table, 0, 15, 'OSCILLATORS', text_color=color.purple, text_size=table_text_size, bgcolor=color.new(color.purple, 90))

table.cell(info_table, 1, 15, 'Awesome Osc', text_color=color.blue, text_size=table_text_size)

table.cell(info_table, 2, 15, str.tostring(ao, '0.000'), text_color=color.blue, text_size=table_text_size)

table.cell(info_table, 0, 16, '', text_color=color.red, text_size=table_text_size)

table.cell(info_table, 1, 16, 'Fisher Transform', text_color=color.red, text_size=table_text_size)

table.cell(info_table, 2, 16, str.tostring(fisher, '0.000'), text_color=color.red, text_size=table_text_size)

// Summary Statistics

table.cell(info_table, 0, 17, 'SUMMARY', text_color=color.black, text_size=table_text_size, bgcolor=color.new(color.gray, 70))

table.cell(info_table, 1, 17, 'Total Indicators: 52', text_color=color.black, text_size=table_text_size)

regime_color = rsi_centered > 10 ? color.green : rsi_centered < -10 ? color.red : color.gray

regime_text = rsi_centered > 10 ? "BULLISH" : rsi_centered < -10 ? "BEARISH" : "NEUTRAL"

table.cell(info_table, 2, 17, regime_text, text_color=regime_color, text_size=table_text_size)

This makes it the perfect “indicator backbone” for quantitative and systematic traders who want to prototype, combine, and test new regime detection models—especially in combination with the Markov Chain indicator.

How to use this script with the Markov Chain for research and backtesting:

Add the Enhanced Indicator Export to your chart.

Every calculated indicator is available as an individual data stream.

Connect the indicator(s) you want as custom input(s) to the Markov Chain’s “Custom Indicators” option.

In the Markov Chain indicator’s settings, turn ON the custom indicator mode.

For each of the three custom indicator inputs, select the exported plot from the Enhanced Export script—the menu lists all 45+ signals by name.

This creates a powerful, modular regime-detection engine where you can mix-and-match momentum, trend, volume, or custom combinations for advanced filtering.

Backtest regime logic directly.

Once you’ve connected your chosen indicators, the Markov Chain script performs regime detection (Bull/Neutral/Bear) based on your selected features—not just price returns.

The regime detection is robust, automatically normalized (using Z-score), and outputs bias (1, -1, 0) for plug-and-play integration.

Export the regime bias for programmatic use.

As described above, use input.source() in your Pine Script strategy or system and link the bias output.

You can now filter signals, control trade direction/size, or design pairs-trading that respect true, indicator-driven market regimes.

With this framework, you’re not limited to static or simplistic regime filters. You can rigorously define, test, and refine what “market regime” means for your strategies—using the technical features that matter most to you.

Optimize your signal generation by backtesting across a universe of meaningful indicator blends.

Enhance risk management with objective, real-time regime boundaries.

Accelerate your research: iterate quickly, swap indicator components, and see results with minimal code changes.

Automate multi-asset or pairs-trading by integrating regime context directly into strategy logic.

Add both scripts to your chart, connect your preferred features, and start investigating your best regime-based trades—entirely within the TradingView ecosystem.

References & Further Reading

Ang, A., & Bekaert, G. (2002). “Regime Switches in Interest Rates.” Journal of Business & Economic Statistics, 20(2), 163–182.

Hamilton, J. D. (1989). “A New Approach to the Economic Analysis of Nonstationary Time Series and the Business Cycle.” Econometrica, 57(2), 357–384.

Markov, A. A. (1906). "Extension of the Limit Theorems of Probability Theory to a Sum of Variables Connected in a Chain." The Notes of the Imperial Academy of Sciences of St. Petersburg.

Guidolin, M., & Timmermann, A. (2007). “Asset Allocation under Multivariate Regime Switching.” Journal of Economic Dynamics and Control, 31(11), 3503–3544.

Murphy, J. J. (1999). Technical Analysis of the Financial Markets. New York Institute of Finance.

Brock, W., Lakonishok, J., & LeBaron, B. (1992). “Simple Technical Trading Rules and the Stochastic Properties of Stock Returns.” Journal of Finance, 47(5), 1731–1764.

Zucchini, W., MacDonald, I. L., & Langrock, R. (2017). Hidden Markov Models for Time Series: An Introduction Using R (2nd ed.). Chapman and Hall/CRC.

On Quantitative Finance and Markov Models:

Lo, A. W., & Hasanhodzic, J. (2009). The Heretics of Finance: Conversations with Leading Practitioners of Technical Analysis. Bloomberg Press.

Patterson, S. (2016). The Man Who Solved the Market: How Jim Simons Launched the Quant Revolution. Penguin Press.

TradingView Pine Script Documentation: www.tradingview.com

TradingView Blog: “Use an Input From Another Indicator With Your Strategy” www.tradingview.com

GeeksforGeeks: “What is the Difference Between Markov Chains and Hidden Markov Models?” www.geeksforgeeks.org

What makes this indicator original and unique?

- On‑chart, real‑time Markov. The chain is drawn directly on your chart. You see the current regime, its tendency to stay (self‑loop), and the usual next step (arrows) as bars confirm.

- Source‑agnostic by design. The engine runs on any series you select via input.source() — price, your own oscillator, a composite score, anything you compute in the script.

- Automatic normalization + regime mapping. Different inputs live on different scales. The script standardizes your chosen source and maps it into clear regimes (e.g., Bull / Bear / Neutral) without you micromanaging thresholds each time.

- Rolling, bar‑by‑bar learning. Transition tendencies are computed from a rolling window of confirmed bars. What you see is exactly what the market did in that window.

- Fast experimentation. Switch the source, adjust the window, and the Markov view updates instantly. It’s a rapid way to test ideas and feel regime persistence/switch behavior.

Integrate your own signals (using input.source())

- In settings, choose the Source . This is powered by input.source() .

- Feed it price, an indicator you compute inside the script, or a custom composite series.

- The script will automatically normalize that series and process it through the Markov engine, mapping it to regimes and updating the on‑chart spheres/arrows in real time.

Credits:

Deep gratitude to @RicardoSantos for both the foundational Markov chain processing engine and inspiring open-source contributions, which made advanced probabilistic market modeling accessible to the TradingView community.

Special thanks to @Alien_Algorithms for the innovative and visually stunning 3D sphere logic that powers the indicator’s animated, regime-based visualization.

Disclaimer

This tool summarizes recent behavior. It is not financial advice and not a guarantee of future results.

BW MFI fixed v6Bill Williams MFI

Sure! Here’s an English description of the indicator you have:

---

### Bill Williams Market Facilitation Index (MFI) — Indicator Description

This indicator implements the **Market Facilitation Index (MFI)** as introduced by Bill Williams. The MFI measures the market's willingness to move the price by comparing the price range to the volume.

---

### How it works:

* **MFI Calculation:**

The MFI is calculated as the difference between the current bar’s high and low prices divided by the volume of that bar:

$$

\text{MFI} = \frac{\text{High} - \text{Low}}{\text{Volume}}

$$

* **Color Coding Logic:**

The indicator compares the current MFI and volume values to their previous values and assigns colors to visualize market conditions according to Bill Williams’ methodology:

| Color | Condition | Market Interpretation |

| ----------- | ------------------ | --------------------------------------------------------------------------------------------- |

| **Green** | MFI ↑ and Volume ↑ | Strong trend continuation or acceleration (increased price movement supported by volume) |

| **Brown** | MFI ↓ and Volume ↓ | Trend weakening or possible pause (both price movement and volume are decreasing) |

| **Blue** | MFI ↑ and Volume ↓ | Possible false breakout or lack of conviction (price moves but volume decreases) |

| **Fuchsia** | MFI ↓ and Volume ↑ | Market indecision or battle between bulls and bears (volume rises but price movement shrinks) |

| **Gray** | None of the above | Neutral or unchanged market condition |

* **Display:**

The indicator plots the MFI values as colored columns on a separate pane below the price chart, providing a visual cue of the market’s behavior.

---

### Purpose:

This tool helps traders identify changes in market momentum and the strength behind price moves, providing insight into when trends might accelerate, weaken, or potentially reverse.

---

If you want, I can help you write a more detailed user guide or trading strategy based on this indicator!

COT IndexReference:

Trade Stocks and Commodities with the Insiders

Secrets of the COT Report by Larry Williams pg34

The equation is as below:

Current week's value- Lowest value of last three years

---------------------------------------------------------------------------- X 100%

Highest high of last three years-Lowest low of last three years

According to Larry Williams, traders should follow commercials direction. When the commercial index line (yellow line) is above 80, this indicates commercials are bullish. Hence, traders can look for potential buy setup. Conversely, when commercials index line (yellow line) is below 20, this indicates commercials are bearish, we can look for sell setup.

Do note that this is only applicable on Weekly chart as COT reports come out on weekly basis.

Modification from the original COT index from Larry Williams:

1) I've added 1year and 6months period, so traders maybe can look for pullback using shorter period. By default, Larry Williams uses 3 years Commercial index.

2) I've added non-commercials and retail traders index, they basically trade opposite way of commercials.

This indicator should not be used as a timing tool or entry tool, you can use it as your weekly or monthly bias tool. For more information, please read the books. Feel free to modify the code, if u have a better version of this, you may share to me if you want, I will be very grateful!

Student Wyckoff Target Shooter

**Target Shooter — Equal Move Target Tool (Larry Williams idea)**

**1. What this indicator does**

Target Shooter is a tool that measures the last meaningful price swing and projects an **equal move target** in the direction of the breakout.

The logic is simple:

* The market makes a move from point A to point B (a swing high to a swing low, or vice versa).

* Then price breaks out above or below this swing range.

* Target Shooter takes the size of that swing and **adds it in the direction of the breakout**, showing a logical **price target zone** where the move may:

* slow down,

* react,

* or potentially reverse.

This is a practical implementation of the “Equal Moves” idea often referenced by Larry Williams.

---

**2. Core idea (example)**

Example from the classic explanation:

* Price drops from **80 down to 20** → the move is **60 points**.

* The swing range is now: **High = 80, Low = 20**.

* Later, price **breaks above 80**.

Target Shooter assumes:

> “If the market could move 60 points in one direction, after a breakout it may travel another 60 points in the opposite direction.”

So the upside target becomes:

* Move size: 80 − 20 = 60

* Breakout above 80

* **Target = 80 + 60 = 140**

The indicator finds such swings automatically and draws:

* **UT (Upper Target)** on upside breakouts

* **DT (Down Target)** on downside breakouts

---

**3. What you see on the chart**

1. **Target lines**

* When price breaks **above** a previous swing range, the indicator plots a horizontal **UT (Upper Target)** line — the projected equal move target.

* When price breaks **below** the previous swing range, it plots a **DT (Down Target)** line — the downside target.

* Each line is drawn from the breakout bar and extended to the right for a user-defined number of bars.

2. **Price labels**

* A small label “UT” or “DT” is shown at the end of the line with the exact target price.

* This makes it easy to see where the projected target is without checking the scale.

3. **Optional swing range (debug view)**

* There is an option to display the **swing range** that the target is based on (similar to a Donchian channel on previous bars).

* This shows the upper (swing high) and lower (swing low) boundaries the indicator used to define the last move.

---

**4. Key inputs (plain language)**

* **Swing window length (bars)**

How many bars back the indicator looks to find the last meaningful swing (highest high and lowest low).

This is like the length of a Donchian channel used to define the previous range.

Smaller values → more frequent, shorter targets.

Larger values → bigger swings and more distant targets.

* **Minimum move size (in ticks)**

This is a noise filter.

If the distance between the swing high and swing low is smaller than this threshold, no targets are drawn.

The indicator will only react to moves that are big enough to matter for your trading.

* **Breakout type: Close vs High/Low**

* **Breakout by Close**:

The target appears only when the **bar closes** above/below the swing range.

More conservative and fewer false signals.

* **Breakout by High/Low**:

The target appears as soon as the **high** or **low** of the bar breaks the swing range.

Faster and more aggressive, but more sensitive to noise.

* **Target line length (bars)**

How far to the right the UT/DT lines should be extended.

Shorter length → local target zones.

Longer length → important levels visible far into the future.

* **Appearance settings**

* Separate color, width and style for **UT** and **DT** lines.

* Option to show or hide labels with price and “UT/DT” text.

---

**5. How to use Target Shooter in trading**

> Important: this is **not** an entry signal indicator.

> Target Shooter is a **targeting and context tool**, not a standalone system.

Typical uses:

1. **Planning take-profit zones**

* You already have an entry signal from your own strategy (Wyckoff, Larry Williams patterns, levels, volume, whatever you use).

* Target Shooter shows a **logical equal move target** where the current wave can reasonably “shoot”.

* You can:

* place your main take-profit around the target,

* scale out part of the position,

* tighten stops when price approaches the target.

2. **Finding potential reaction / reversal areas**

* Equal move targets often act as **zones of interest**.

* If price reaches a UT/DT level and then shows weakness/absorption/volume spikes or reversal candles, this might be a good place to take profits or look for counter-trend opportunities (for experienced traders).

3. **Assessing trend strength**

* If price **easily exceeds** the equal move target and keeps going without any reaction, it suggests a very strong trend.

* If price **fails to reach** the target and reverses early, the move is weaker than expected.

---

**6. Timeframes**

Target Shooter can be used on:

* **Intraday** (M5, M15, M30, H1) — for shorter-term targets within the day,

* **Higher timeframes** (H4, D1 and above) — for swing and position trades.

General rule:

The **higher the timeframe and the larger the swing**, the **more important** the target level tends to be.

---

**7. Notes and limitations**

* The indicator does **not** predict the future.

It simply projects a geometric equal move from the last swing.

* It should be combined with your own trading framework:

* support/resistance,

* Wyckoff / VSA,

* trend tools,

* volume/flow, etc.

* Always keep proper risk management.

A target is a **scenario**, not a guarantee.

.

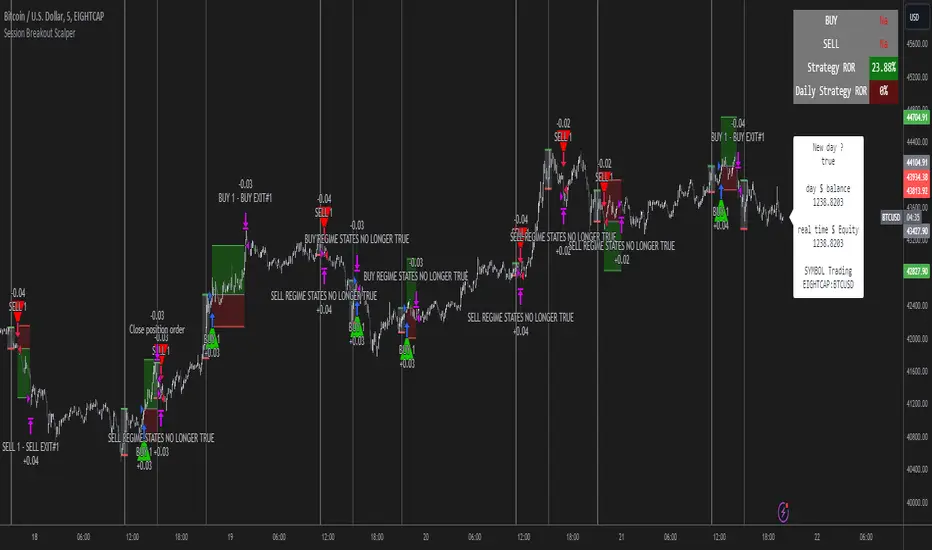

Session Breakout Scalper Trading BotHi Traders !

Introduction:

I have recently been exploring the world of automated algorithmic trading (as I prefer more objective trading strategies over subjective technical analysis (TA)) and would like to share one of my automation compatible (PineConnecter compatible) scripts “Session Breakout Scalper”.

The strategy is really simple and is based on time conditional breakouts although has more ”relatively” advanced optional features such as the regime indicators (Regime Filters) that attempt to filter out noise by adding more confluence states and the ATR multiple SL that takes into account volatility to mitigate the down side risk of the trade.

What is Algorthmic Trading:

Firstly what is algorithmic trading? Algorithmic trading also known as algo-trading, is a method of using computer programs (in this case pine script) to execute trades based on predetermined rules and instructions (this trading strategy). It's like having a robot trader who follows a strict set of commands to buy and sell assets automatically, without any human intervention.

Important Note:

For Algorithmic trading the strategy will require you having an essential TV subscription at the minimum (so that you can set alerts) plus a PineConnecter subscription (scroll down to the .”How does the strategy send signals” headings to read more)

The Strategy Explained:

Is the Time input true ? (this can be changed by toggling times under the “TRADE MEDIAN TIMES” group for user inputs).

Given the above is true the strategy waits x bars after the session and then calculates the highest high (HH) to lowest low (LL) range. For this box to form, the user defined amount of bars must print after the session. The box is symmetrical meaning the HH and LL are calculated over a lookback that is equal to the sum of user defined bars before and after the session (+ 1).

The Strategy then simultaneously defines the HH as the buy level (green line) and the LL as the sell level (red line). note the strategy will set stop orders at these levels respectively.

Enter a buy if price action crosses above the HH, and then cancel the sell order type (The opposite is true for a stop order).

If the momentum based regime filters are true the strategy will check for the regime / regimes to be true, if the regime if false the strategy will exit the current trade, as the regime filter has predicted a slowing / reversal of momentum.

The image below shows the strategy executing these trading rules ( Regime filters, "Trades on chart", "Signal & Label" and "Quantity" have been omitted. "Strategy label plots" has been switched to true)

Other Strategy Rules:

If a new session (time session which is user defined) is true (blue vertical line) and the strategy is currently still in a trade it will exit that trade immediately.

It is possible to also set a range of percentage gain per day that the strategy will try to acquire, if at any point the strategy’s profit is within the percentage range then the position / trade will be exited immediately (This can be changed in the “PERCENT DAY GAIN” group for user inputs)

Stops and Targets:

The strategy has either static (fixed) or variable SL options. TP however is only static. The “STRAT TP & TP” group of user inputs is responsible for the SL and TP values (quoted in pips). Note once the ATR stop is set to true the SL values in the above group no longer have any affect on the SL as expected.

What are the Regime Filters:

The Larry Williams Large Trade Index (LWLTI): The Larry Williams Large Trade Index (LWTI) is a momentum-based technical indicator developed by iconic trader Larry Williams. It identifies potential entries and exits for trades by gauging market sentiment, particularly the buying and selling pressure from large market players. Here's a breakdown of the LWTI:

LWLTI components and their interpretation:

Oscillator: It oscillates between 0 and 100, with 50 acting as the neutral line.

Sentiment Meter: Values above 75 suggest a bearish market dominated by large selling, while readings below 25 indicate a bullish market with strong buying from large players.

Trend Confirmation: Crossing above 75 during an uptrend and below 25 during a downtrend confirms the trend's continuation.

The Andean Oscillator (AO) : The Andean Oscillator is a trend and momentum based indicator designed to measure the degree of variations within individual uptrends and downtrends in the prices.

Regime Filter States:

In trading, a regime filter is a tool used to identify the current state or "regime" of the market.

These Regime filters are integrated within the trading strategy to attempt to lower risk (equity volatility and/or draw down). The regime filters have different states for each market order type (buy and sell). When the regime filters are set to true, if these regime states fail to be true the trade is exited immediately.

For Buy Trades:

LWLTI positive momentum state: Quotient of the lagged trailing difference and the ATR > 50

AO positive momentum state: Bull line > Bear line (signal line is omitted)

For Sell Trades:

LWLTI negative momentum stat: Quotient of the lagged trailing difference and the ATR < 50

AO negative momentum state: Bull line < Bear line (signal line is omitted)

How does the Strategy Send Signals:

The strategy triggers a TV alert (you will neet to set a alert first), TV then sends a HTTP request to the automation software (PineConnecter) which receives the request and then communicates to an MT4/5 EA to automate the trading strategy.

For the strategy to send signals you must have the following

At least a TV essential subscription

This Script added to your chart

A PineConnecter account, which is paid and not free. This will provide you with the expert advisor that executes trades based on these strategies signals.

For more detailed information on the automation process I would recommend you read the PineConnecter documentation and FAQ page.

Dashboard:

This Dashboard (top right by defualt) lists some simple trading statistics and also shows when a trade is live.

Important Notice:

- USE THIS STRATEGY AT YOUR OWN RISK AND ALWAYS DO YOUR OWN RESEARCH & MANUAL BACKTESTING !

- THE STRATEGY WILL NOT EXHIBIT THE BACKTEST PERFORMANCE SEEN BELOW IN ALL MARKETS !

Setup Max e Min Larry WilliansLarry Williams used this system to win the trading championship

Hello friends, I bring a script with a trading strategy to be used in futures such as Index, Forex and Commodities. Developed by famous trader Larry Williams.

In them we use two 3-period Simple Moving Averages (Arithmetic) (one with the high price, the other with the low price), and a 21-period Moving Average (Arithmetic) to determine the trend. This will form an average channel with the prices of the maximums and minimums of the last three candles.

Best time charts use the strategy: from 5 minutes to 60 minutes.

This strategy is quite simple. The 21 Moving Average will color according to the trend (Green for bullish, Red for bearish and Gray for transitions). The Script will signal the entry according to the trend by the colors of the candles and also by the signal:

When green, the buy will be on the crossing of the lower Moving Average crossing the candlestick, and the exit will be on the crossing of the candlestick on the next Upper Moving Average.

When red, the sell will be at the crossing of the Upper Moving Average crossing the candlestick, and the exit will be at the crossing of the candlestick on the next Lower Moving Average.

When the Script signals the candle with a purple X, it means that the trend is changing and the entire open operation must be closed.

This system has no Stop, so be careful when using it.

Na linguagem do autor:

Larry Williams usou esse sistema ganhar campeonato de trade

Olá amigos, trago um script com uma estratégia de trade pra ser usada em futuros como Índice, Forex e Commodities. Desenvolvido pelo famoso trader Larry Willians.

Neles usamos duas Médias Móveis Simples (Aritmética) de 3 períodos (uma com o preço da máxima, outra com o preço da mínima), e uma Média Móvel (Aritmética) de 21 períodos para determinar a tendência. Nisso vai formar uma canal de médias com os preços das máximas e mínimas dos últimos três candles.

Melhores tempos gráficos usar a estratégia: de 5 minutos até 60 minutos.

Essa estratégia é bem simples. A Média Móvel de 21 irá colorir de acordo com a tendência (Green pra alta, Red para baixa e Gray para transições). O Script irá sinalizar a entrada de acordo com a tendência pela cores dos candles e também pela sinalização:

Quando green, a compra será no cruzamento da Média Móvel inferior cruzando o candle, e a saida será no cruzamento do candle na Média Móvel Superior seguinte.

Quando red, a venda será no cruzamento da Média Móvel Superior cruzando o candle, e a saida será no cruzamento do candle na Média Móvel Inferior seguinte.

Quando o Script sinaliza o candle com X purple, significa que a tendência está em mudança e deve ser fechada toda a operação em aberto.

Este sistema não possui Stop, portando cuidado quanto a seu uso.

IndicatorsLibrary "Indicators"

cmf(lookback, n_to_smooth)

Calculates the Chaikin's Money Flow.

Parameters:

lookback (simple int)

n_to_smooth (simple int)

Returns: float The Money Flow value.

cmma(lookback, atr_length)

Calculates the CMMA (Close Minus Moving Average) indicator.

Parameters:

lookback (simple int)

atr_length (simple int)

Returns: float The CMMA value.

macd(fast_length, slow_length, n_to_smooth)

Calculates the normalized and scaled MACD.

Parameters:

fast_length (simple int)

slow_length (simple int)

n_to_smooth (simple int)

Returns: A tuple containing .

stochK(length, n_to_smooth)

Calculates a simplified Stochastic Oscillator.

Uses: 100 * ta.sma((close - lowest_low) / (highest_high - lowest_low), n_to_smooth)

Parameters:

length (simple int)

n_to_smooth (simple int)

Returns: float The Stochastic %K value.

williamsR(length)

Calculates the Williams %R using the stochK function.

Uses: -1 * (100 - stoch(length, 1))

Parameters:

length (simple int)

Returns: float The Williams %R value.

MACD Willy StrategyThis strategy is mainly developed for scalping / intraday trading. It could potentially be used to identify entry/exit signals for short term options trading. It performs decently well on popular stocks when used on time frames between 5 min to 15 min using regular session bar data. It combines 3 popular indicators, EMA, MACD, and William %range, to generate both long and short signals.

EMA:

Default is 200 EMA line.

MACD:

Default is 12/26 lengths for fast/slow signal inputs.

William %R - Smoothed (Published):

This is a custom indicator that generates two moving average lines from the original William %R line.

How it works:

Entry conditions:

1. Long/short entries when bar closes above/below EMA line

2. Long/short entries when MACD line is above/below signal line (histogram > 0 for long, < 0 for short)

3. Long/short entries when William %R fast MA line is above/below slow MA line

Exit conditions:

1. Exit long when MACD line is below signal line, vise versa for exit short

2. Exit long when William %R fast MA line is below slow MA line, vise versa for exit short

3. Exit long when William %R fast MA line must in below the overbought (-20) limit, exit short when above the oversold (-80) limit.

***Note that parameters are NOT optimized for any particular stocks / instruments.

Enjoy~~!!

100PipsADay third screen / triple screen strategy MACD and W%RThird Screen Strategy

This particular script is specifically designed around this strategy. D1 MACD & H1 Williams %.

I coded the script in a way that you automatically get the signal that is calculated taking in consideration both the indicators (macd and w%R)

Green means that the daily MACD histogram is above 0 (crowd is bullish) but w%R shows that momentarily there is a lower price (W%R is oversold),

Red is vice versa.

Quote from original post :

Below is how I would normally take a trade using my strategy.

As you can see below in my chart, I look on the D1 chart for the MACD to cross over.

Once it is clear that it has crossed over, I will enter positions on the H1 chart using Williams %.

end quote.

This Script i coded in a way that automatically account for both the indicators, so you don't have to switch between timeframes.

3 Important rules :

To get the indicator set correctly you need to use on 1 Hour time frame

-----------------------

You should wait 6 hours when signal appear to open an other position on the same pair

-----------------------

I coded an alarm that gets triggered when the pair meet both condition (when the bar and/or the background is green) so you can just set it by right clicking the indicator and be relaxed!

Italiano :

Strategia Third screen

Questo particolare script è specificamente progettato attorno a questa strategia. D1 MACD e H1 Williams%.

Ho codificato lo script in modo da ottenere automaticamente il segnale calcolato tenendo conto di entrambi gli indicatori (macd e w% R)

Verde indica che l'istogramma MACD giornaliero è superiore a 0 (la folla è rialzista) ma w% R mostra che momentaneamente esiste un prezzo inferiore (W% R è sotto il livello di oversold),

Il rosso è viceversa.

Ho codificato questo script in un modo che tiene conto automaticamente di entrambi gli indicatori, quindi non è necessario passare da un intervallo di tempo all'altro.

3 Regole importanti:

Per impostare correttamente l'indicatore è necessario utilizzare nel periodo di 1 ora

-----------------------

Dovresti aspettare 6 ore una volta che arriva il segnale per aprire un'altra posizione sullo stessa moneta

-----------------------

Ho codificato un allarme che viene attivato quando sono soddisfatte entrambe le condizioni (ossia quando lo sfondo è verde), quindi puoi semplicemente impostarlo facendo clic con il pulsante destro del mouse sull'indicatore ed essere rilassato!

$MTF Fractal Echo DetectorMIL:MTVFR FRACTAL ECHO DETECTOR by Timmy741

The first public multi-timeframe fractal convergence system that actually works.

Market makers don’t move price randomly.

They test the same fractal structure on lower timeframes first → then execute the real move on higher timeframes.

This indicator catches the “echo” — when 3–5 timeframes are printing fractals at almost the exact same price level.

That’s not coincidence. That’s preparation.

FEATURES

• 5 simultaneous timeframes (1min → 4H by default)

• Real Williams Fractal detection (configurable period)

• Dynamic echo tolerance & minimum TF alignment

• Visual S/R zones from every timeframe

• Bullish / Bearish echo convergence signals

• Strength meter (3/5, 4/5, 5/5 TF alignment)

• Zero repainting — uses proper lookahead=off

• Fully Pine v6 typed + optimized

USE CASE

When you see a 4/5 or 5/5 echo:

→ That level is being defended or attacked with intent

→ 80%+ chance the next real move comes from there

→ Trade the breakout or reversal at that exact fractal cluster

Works insane on:

• BTC / ETH (all timeframes)

• Nasdaq / SPX futures

• Forex majors (especially GBP & gold)

• 2025 small-cap rotation setups

100% Open Source • MPL 2.0 • Built by Timmy741 • December 2024

If you know about fractal echoes… you already know.

#fractal #mtf #echo #williamsfractal #multitimeframe #smartmoney #ict #smc #orderflow #convergence #timmy741 #snr #structure

Profitunity - Beginner [TC]This indicator aggregates the knowledges of the first level of the Trading Chaos approach by Bill Williams. It uses the Market Facilitation Index (MFI) in conjunction with the type of bar(candle) to generate strong long and strong short signals.

General information

Bars numeration

All bars or candles could be numbered with the following algorithm. If we divide the candle for 3 equal parts from high to low. The highest third have the number 1, the middle one - 2, the lowest one - 3. Hence we can define the first number as the number of the third where the price opened, second - where the price closed. For example, if the price opened at the highest third and closed at the lowest one this candle has the number 13.

Trend defining

Also candles could be divided into three groups according to the trend condition: uptrend, downtrend, sideways. If the middle of the candle's trading range is above the high of the previous candle - it's uptrend candle, if below the low of the previous candle - it's downtrend candle, sideways in other candles.

Profitunity windows

According to Bill Williams MFI has 4 windows - fake, green, fade and squat. I am not going to describe here the methodology of MFI, but one thing you should know that the most valuable windows are green and squat. Green state is an indication of the true move on the market. Squat the sign that the increase in volume have not triggered the trend continuation and reverse is about to happen.

How to use?

You can use this script as the helper in automatic defining the type of candle. Indicator shows only green (green candle color) and squat (red candle color) MFI states. Add script to any timeframe and asset chart to see labels.

The "strong long" label flashes when 3 conditions are met:

1. Squat candle

2. Candle number 13

3. Downtrend candle

"Strong short" label flashes when:

1. Squat candle

2. Candle number 31

3. Uptrend candle

This indicator helps to find the trend reversal points, can be used in conjunction with other TA tools to find the entry points.

taLibrary "ta"

█ OVERVIEW

This library holds technical analysis functions calculating values for which no Pine built-in exists.

Look first. Then leap.

█ FUNCTIONS

cagr(entryTime, entryPrice, exitTime, exitPrice)

It calculates the "Compound Annual Growth Rate" between two points in time. The CAGR is a notional, annualized growth rate that assumes all profits are reinvested. It only takes into account the prices of the two end points — not drawdowns, so it does not calculate risk. It can be used as a yardstick to compare the performance of two instruments. Because it annualizes values, the function requires a minimum of one day between the two end points (annualizing returns over smaller periods of times doesn't produce very meaningful figures).

Parameters:

entryTime : The starting timestamp.

entryPrice : The starting point's price.

exitTime : The ending timestamp.

exitPrice : The ending point's price.

Returns: CAGR in % (50 is 50%). Returns `na` if there is not >=1D between `entryTime` and `exitTime`, or until the two time points have not been reached by the script.

█ v2, Mar. 8, 2022

Added functions `allTimeHigh()` and `allTimeLow()` to find the highest or lowest value of a source from the first historical bar to the current bar. These functions will not look ahead; they will only return new highs/lows on the bar where they occur.

allTimeHigh(src)

Tracks the highest value of `src` from the first historical bar to the current bar.

Parameters:

src : (series int/float) Series to track. Optional. The default is `high`.

Returns: (float) The highest value tracked.

allTimeLow(src)

Tracks the lowest value of `src` from the first historical bar to the current bar.

Parameters:

src : (series int/float) Series to track. Optional. The default is `low`.

Returns: (float) The lowest value tracked.

█ v3, Sept. 27, 2022

This version includes the following new functions:

aroon(length)

Calculates the values of the Aroon indicator.

Parameters:

length (simple int) : (simple int) Number of bars (length).

Returns: ( [float, float ]) A tuple of the Aroon-Up and Aroon-Down values.

coppock(source, longLength, shortLength, smoothLength)

Calculates the value of the Coppock Curve indicator.

Parameters:

source (float) : (series int/float) Series of values to process.

longLength (simple int) : (simple int) Number of bars for the fast ROC value (length).

shortLength (simple int) : (simple int) Number of bars for the slow ROC value (length).

smoothLength (simple int) : (simple int) Number of bars for the weigted moving average value (length).

Returns: (float) The oscillator value.

dema(source, length)

Calculates the value of the Double Exponential Moving Average (DEMA).

Parameters:

source (float) : (series int/float) Series of values to process.

length (simple int) : (simple int) Length for the smoothing parameter calculation.

Returns: (float) The double exponentially weighted moving average of the `source`.

dema2(src, length)

An alternate Double Exponential Moving Average (Dema) function to `dema()`, which allows a "series float" length argument.

Parameters:

src : (series int/float) Series of values to process.

length : (series int/float) Length for the smoothing parameter calculation.

Returns: (float) The double exponentially weighted moving average of the `src`.