Adaptive RSI Oscillator📌 Adaptive RSI Oscillator

This indicator transforms the classic RSI into a fully adaptive, self-optimizing oscillator — normalized between -1 and 1, dynamically smoothed, and enhanced with divergence detection.

🔧 Key Features

Self-Optimizing RSI: Automatically selects the optimal RSI lookback length based on return stability (no hardcoded periods).

Dynamic Smoothing: Adapts to market conditions using a fraction of the optimized length.

Normalized Output : Converts traditional RSI to a consistent scale across all assets and timeframes.

Divergence Detection: Compares RSI behavior vs. price percentile ranks and scales the signal accordingly.

Gradient Visualization: Color-coded background and plot lines reflect the strength and direction of the signal with soft transitions.

Neutral Zone Adaptation: Dynamically widens or narrows the zone of inaction based on volatility, reducing noise.

🎯 Use Cases

Identify extreme momentum zones without relying on fixed 70/30 RSI levels

Detect divergences early with adaptive filtering

Highlight potential exhaustion or continuation

⚠️ Disclaimer: This indicator is for informational and educational purposes only. It does not constitute financial advice or a recommendation to buy or sell any security. Always conduct your own research and consult a licensed financial advisor before making investment decisions. Use at your own risk.

標準偏差

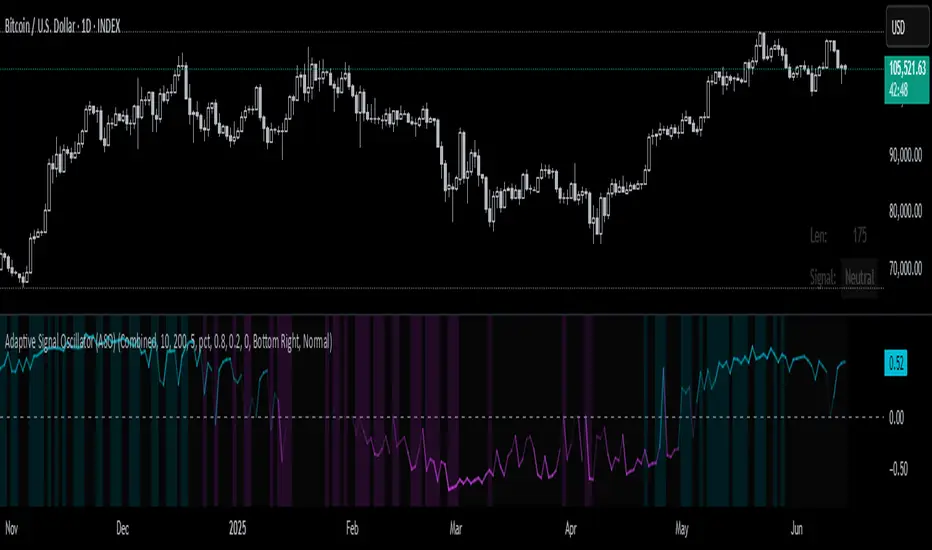

Adaptive Signal Oscillator (ASO)📘 Adaptive Signal Oscillator (ASO)

A fully dynamic, self-calibrating oscillator that adapts to any asset or timeframe by optimizing for real-time signal stability and volatility structure — without relying on static parameters or hardcoded thresholds.

🔍 Overview

The Adaptive Signal Oscillator (ASO) is a next-generation technical analysis tool designed to provide context-aware long/short signals across crypto, equities, or forex markets. Unlike traditional oscillators (RSI, Stochastics, MACD), ASO requires no manual tuning of lookback periods or overbought/oversold zones — it self-optimizes based on current market behavior.

🧠 How It Works

✅ 1. Dynamic Lookback Optimization

ASO evaluates a range of lookback lengths between user-defined minLen and maxLen. For each length, it calculates the standard deviation of returns and finds the one with the least volatility change (i.e., the most stable structure). This length is dynamically assigned as bestLen, recalculated on every bar.

✅ 2. Multi-Layer Signal Composition

Four independent signal layers are computed using bestLen:

RSI Layer: Measures relative price strength via a custom dynamic RSI.

Z-Score Layer: Standardized deviation of price from its mean.

Volatility Layer: Standard deviation of log or percent returns.

Price Position Layer: Current price percentile within the lookback window.

Each of these layers is transformed into a percentile score scaled to the range .

✅ 3. Volatility-Based Weighting

The standard deviation (volatility) of each signal layer is computed. Less volatile layers are weighted more heavily, ensuring the final composite signal prioritizes stable, consistent inputs.

Weights are normalized and combined to form a composite score, representing a dynamically blended, noise-weighted signal across the four layers.

✅ 4. Optional Adaptive Smoothing

A boolean toggle lets users apply smoothing to the final score. The smoothing window scales proportionally to bestLen, preserving adaptiveness even during trend transitions.

✅ 5. Percentile-Based Thresholding

Rather than using arbitrary fixed thresholds, ASO converts the composite score into a ranked percentile. Long/short signals are then generated based on user-defined percentile bands, adapting naturally to each asset’s behavior.

📈 Interpreting ASO

Score > Threshold → Strong long signal (highlighted in aqua).

Score < Threshold → Strong short signal (highlighted in fuchsia).

Crossing h_thresh (e.g., 0) → Neutral-to-bias change; useful for early trend cues.

The background and label update in real time to reflect the current regime and bestLen.

⚙️ Inputs

minLen, maxLen, step: Define the search range for optimal lookback length.

retMethod: Choose between log or percent return calculations.

threshHigh, threshLow: Define signal zones using percentiles.

smooth: Enable dynamic score smoothing.

h_thresh: Midline crossover zone for directional context.

⚠️ Disclaimer

This tool is designed for exploratory and educational purposes only. It does not offer financial advice or trading recommendations. Past performance is not indicative of future results.

Always consult a licensed financial advisor before making investment decisions.

VWAP %BVWAP %B - Volume Weighted Average Price Percent B

The VWAP %B indicator combines the reliability of VWAP (Volume Weighted Average Price) with the analytical power of %B oscillators, similar to Bollinger Bands %B but using volume-weighted statistics.

## How It Works

This indicator calculates where the current price sits relative to VWAP-based standard deviation bands, expressed as a percentage from 0 to 1:

• **VWAP Calculation**: Uses volume-weighted average price as the center line

• **Standard Deviation Bands**: Creates upper and lower bands using standard deviation around VWAP

• **%B Formula**: %B = (Price - Lower Band) / (Upper Band - Lower Band)

## Key Levels & Interpretation

• **Above 1.0**: Price is trading above the upper VWAP band (strong bullish momentum)

• **0.8 - 1.0**: Overbought territory, potential resistance

• **0.5**: Price exactly at VWAP (equilibrium)

• **0.2 - 0.0**: Oversold territory, potential support

• **Below 0.0**: Price is trading below the lower VWAP band (strong bearish momentum)

## Trading Applications

**Trend Following**: During strong trends, breaks above 1.0 or below 0.0 often signal continuation rather than reversal.

**Mean Reversion**: In ranging markets, extreme readings (>0.8 or <0.2) may indicate potential reversal points.

**Volume Context**: Unlike traditional %B, this incorporates volume weighting, making it more reliable during high-volume periods.

## Parameters

• **Length (20)**: Period for standard deviation calculation

• **Standard Deviation Multiplier (2.0)**: Controls band width

• **Source (close)**: Price input for calculations

## Visual Features

• Reference lines at key levels (0, 0.2, 0.5, 0.8, 1.0)

• Background highlighting for extreme breaks

• Real-time values table

• Clean oscillator format below price chart

Perfect for intraday traders and swing traders who want to combine volume analysis with momentum oscillators.

COV Bands ~ C H I P ACOV Bands ~ C H I P A is a custom volatility and trend identification tool designed to capture directional shifts using the Coefficient of Variation (COV), calculated from standard deviation relative to a mean price baseline.

Key features include:

A configurable SMA-based mean baseline to anchor volatility measurements clearly.

Adjustable upper and lower band multipliers to independently calibrate sensitivity and responsiveness for bullish or bearish breakouts.

Dynamic bands derived from price-relative volatility (COV), enabling adaptive identification of significant price deviations.

User-controlled standard deviation length to manage sensitivity and smoothness of volatility signals.

Direct candle coloring, providing immediate visual feedback using vibrant electric blue for bullish momentum and bright red for bearish momentum.

This indicator is particularly useful for detecting meaningful price movements, breakout signals, and potential reversals when the market moves significantly beyond its typical volatility boundaries.

Note: This indicator has not undergone formal robustness or optimization testing. Therefore, future performance in live trading environments isn't guaranteed.

Interpolated Median Volatility LSMA | OttoThis indicator combines trend-following and volatility analysis by enhancing traditional LSMA with percentile-based linear interpolation applied to both the Least Squares Moving Average (LSMA) and standard deviation. Rather than relying on raw values, it uses the interpolated median (50th percentile) to smooth out noise while preserving sensitivity to significant price shifts. This approach produces a cleaner trend signal that remains responsive to real market changes, adapts to evolving volatility conditions, and improves the accuracy of breakout detection.

Core Concept

The indicator builds on these core components:

LSMA (Least Squares Moving Average): A linear regression-based moving average that fits line using user selected source over user defined period. It offers a smoother and more reactive trend signal compared to standard moving averages.

Standard Deviation shows how much price varies from the mean. In this indicator, it’s used to measure market volatility.

Volatility Bands: Instead of traditional Bollinger-style bands, this script calculates custom upper and lower bands using percentile-based linear interpolation on both the LSMA and standard deviation. This method produces smoother bands that filter out noise while remaining adaptive to meaningful price movements, making them more aligned with real market behavior and helping reduce false signals.

Percentile interpolation estimates a specific percentile (like the median — the 50th percentile) from a set of values — even when that percentile doesn't fall exactly on one data point. Instead of selecting a single nearest value, it calculates a smoothed value between nearby points. In this script, it’s used to find the median of past LSMA and standard deviation values, reducing the impact of outliers and smoothing the trend and volatility signals for more robust results.

Signal Logic: A long signal is identified when close price goes above the upper band, and a short signal when close price goes below the lower band.

⚙️ Inputs

Source: The price source used in calculations

LSMA Length: Period for calculating LSMA

Standard Deviation Length: Period for calculating volatility

Percentile Length: Period used for interpolating percentile values of LSMA and standard deviation

Multiplier: Controls the width of the bands by scaling the interpolated standard deviation

📈 Visual Output

Colored LSMA Line: Changes color based on signal (green for bullish, purple for bearish)

Upper & Lower Bands: Volatility bands calculated using interpolated values (green for bullish, purple for bearish)

Bar Coloring: Price bars are colored to reflect signal state (green for bullish, purple for bearish)

Optional Candlestick Overlay: Enhances visual context by coloring candles to match the signal state (green for bullish, purple for bearish)

How to Use

Add the indicator to your chart and look for signals when close price goes above or below the bands.

Long Signal: close Price goes above the upper band

Short Signal: close Price goes below the lower band

🔔 Alerts:

This script supports alert conditions for long and short signals. You can set alerts based on band crossovers to be notified of potential entries/exits.

⚠️ Disclaimer:

This indicator is intended for educational and informational purposes only. Trading/investing involves risk, and past performance does not guarantee future results. Always test and evaluate strategies before applying them in live markets. Use at your own risk.

Neural Adaptive VWAPNeural Adaptive VWAP with ML Features is an advanced trading indicator that enhances traditional Volume Weighted Average Price (VWAP) calculations through machine learning-inspired adaptive algorithms and predictive volume modeling.

🌟 Key Features:

🧠 Machine Learning-Inspired Adaptation

Dynamic weight adjustment system that learns from prediction errors

Multi-feature volume prediction using time-of-day patterns, price momentum, and volatility

Adaptive learning mechanism that improves accuracy over time

📊 Enhanced VWAP Calculation

Combines actual and predicted volume for forward-looking VWAP computation

Session-based reset with proper daily anchoring

Confidence bands based on rolling standard deviation for dynamic support/resistance

🎯 Advanced Signal Generation

Volume-confirmed crossover signals to reduce false entries

Color-coded candle visualization based on VWAP position

Multi-level strength indicators (strong/weak bullish/bearish zones)

⚙️ Intelligent Feature Engineering

Normalized volume analysis with statistical z-score

Time-series pattern recognition for intraday volume cycles

Price momentum and volatility integration

Sigmoid activation functions for realistic predictions

📈 How It Works:

The indicator employs a sophisticated feature engineering approach that extracts meaningful patterns from:

Volume Patterns: Normalized volume analysis and historical comparisons

Temporal Features: Time-of-day and minute-based cyclical patterns

Market Dynamics: Price momentum, volatility, and rate of change

Adaptive Learning: Error-based weight adjustment similar to neural network training

Unlike static VWAP indicators, this system continuously adapts its calculation methodology based on real-time market feedback, making it more responsive to changing market conditions while maintaining the reliability of traditional VWAP analysis.

🔧 Customizable Parameters:

VWAP Length (1-200 bars)

Volume Pattern Lookback (5-50 periods)

Learning Rate (0.001-0.1) for adaptation speed

Prediction Horizon (1-10 bars ahead)

Adaptation Period for weight updates

📊 Visual Elements:

Blue Line: Adaptive VWAP with predictive elements

Red/Green Bands: Dynamic confidence zones

Colored Candles: Position-based strength visualization

Signal Arrows: Volume-confirmed entry points

Info Table: Real-time performance metrics and weight distribution

🎯 Best Use Cases:

Intraday Trading: Enhanced execution timing with volume prediction

Institutional-Style Execution: Improved VWAP-based order placement

Trend Following: Adaptive trend identification with confidence zones

Support/Resistance Trading: Dynamic levels that adjust to market conditions

OA - Sigma BandsDescription:

The OA - Sigma Bands indicator is a fully adaptive, volatility-sensitive dynamic band system designed to detect price expansion and potential breakouts. Unlike traditional fixed-width Bollinger Bands, OA - Sigma Bands adjust their boundaries based on a combination of standard deviation (σ) and Average Daily Range (ADR), making them more responsive to real market behavior and shifts in volatility.

Key Concepts & Logic

This tool constructs three distinct band regions:

Sigma Bands (±σ):

Calculated using the standard deviation of the closing price over a user-defined lookback period. This acts as the core volatility filter to identify statistically significant price deviations.

ADR Zones (±ADR):

These zones provide an additional layer based on the percentage average of daily price ranges over the last 20 bars. They help visualize intraday or short-term expected volatility.

Dynamic Adjustment Logic:

When price breaks outside the upper/lower sigma or ADR boundaries for a defined number of bars (user input), the system recalibrates. This ensures that the bands evolve with volatility and don’t remain outdated in trending markets.

Inputs & Customization

Sigma Multiplier: Set how wide the sigma bands should be (default: 1.5).

Lookback Period: Controls how many bars are used to calculate the standard deviation (default: 200).

Break Confirmation Bars: Determines how many candles must close beyond a boundary to trigger band recalibration.

ADR Period: Internally fixed at 20 bars for stable short-term volatility measurement.

Full Color Customization: Customize the band colors and fill transparency to suit your chart style.

Benefits & Use Cases

Breakout Trading: Detect when price exits statistically significant ranges, confirming trend expansion.

Mean Reversion: Use the outer bands as potential reversion zones in sideways or low-volatility markets.

Volatility Awareness: Visually identify when price is compressed or expanding.

Dynamic Structure: The auto-updating nature makes it more reliable than static historical zones.

Overlay-Ready: Designed to sit directly on price charts with minimal clutter.

Disclaimer

This script is intended for educational and informational purposes only. It does not constitute investment advice, financial guidance, or a recommendation to buy or sell any security. Always perform your own research and apply proper risk management before making trading decisions.

If you enjoy this script or find it useful, feel free to give it or leave a comment!

Full Day Midpoint Line with Dynamic StdDev Bands (ETH & RTH)A Pine Script indicator designed to plot a midpoint line based on the high and low prices of a user-defined trading session (typically Extended Trading Hours, ETH) and to add dynamic standard deviation (StdDev) bands around this midpoint.

Session Midpoint Line:

The midpoint is calculated as the average of the session's highest high and lowest low during the defined ETH period (e.g., 4:00 AM to 8:00 PM).

This line represents a central tendency or "fair value" for the session, similar to a pivot point or volume-weighted average price (VWAP) anchor.

Interpretation:

Prices above the midpoint suggest bullish sentiment, while prices below indicate bearish sentiment.

The midpoint can act as a dynamic support/resistance level, where price may revert to or react at this level during the session.

Dynamic StdDev Bands:

The bands are calculated by adding/subtracting a multiple of the standard deviation of the midpoint values (tracked in an array) from the midpoint.

The standard deviation is dynamically computed based on the historical midpoint values within the session, making the bands adaptive to volatility.

Interpretation:

The upper and lower bands represent potential overbought (upper) and oversold (lower) zones.

Prices approaching or crossing the bands may indicate stretched conditions, potentially signaling reversals or breakouts.

Trend Identification:

Use the midpoint as a reference for the session’s trend. Persistent price action above the midpoint suggests bullishness, while below indicates bearishness.

Combine with other indicators (e.g., moving averages, RSI) to confirm trend direction.

Support/Resistance Trading:

Treat the midpoint as a dynamic pivot point. Price rejections or consolidations near the midpoint can be entry points for mean-reversion trades.

The StdDev bands can act as secondary support/resistance levels. For example, price reaching the upper band may signal a potential short entry if accompanied by reversal signals.

Breakout/Breakdown Strategies:

A strong move beyond the upper or lower band may indicate a breakout (bullish above upper, bearish below lower). Confirm with volume or momentum indicators to avoid false breakouts.

The dynamic nature of the bands makes them useful for identifying significant price extensions.

Volatility Assessment:

Wider bands indicate higher volatility, suggesting larger price swings and potentially riskier trades.

Narrow bands suggest consolidation, which may precede a breakout. Traders can prepare for volatility expansions in such scenarios.

The "Full Day Midpoint Line with Dynamic StdDev Bands" is a versatile and visually intuitive indicator well-suited for day traders focusing on session-specific price action. Its dynamic midpoint and volatility-adjusted bands provide valuable insights into support, resistance, and potential reversals or breakouts.

(FVC) Fractal Volatility Compression (DAFE) (FVC) Fractal Volatility Compression

See the Market’s Volatility DNA.

The Fractal Volatility Compression (FVC) is a next-generation tool for traders who want to see volatility compression and expansion across multiple timeframes and volatility engines—not just price, but the very structure of volatility itself.

What Makes FVC Unique?

Dual-Engine Volatility:

Plots both classic price-based (Stdev) and meta-volatility (VoVix) compression/expansion, so you can see when the market is “coiling” or “exploding” on multiple levels.

Fractal, Multi-Timeframe Analysis:

Measures volatility on short, medium, and long timeframes, then normalizes each as a Z-score. The result: a true “coiled spring” detector that works on any asset, any timeframe.

Threshold Lines You Control:

Yellow center line: Your neutral baseline.

Green compression line: When crossed, the market is “spring-loading.”

Red expansion line: When crossed, volatility is breaking out.

All lines are solid, clean, and end before the dashboard for a professional look.

Agreement Fill: When both engines agree (both above or both below the center line), a bright fill highlights the zone—red for expansion, green for compression.

Signature Dashboard & Info Line:

Dashboard (right-middle) shows all Z-scores and FVC values, color-coded for instant clarity.

Compact info label for mobile or minimalist users.

Inputs & Customization

Thresholds: Set the yellow, green, and red lines to match your asset, timeframe, and risk tolerance.

Timeframes & Lengths: Tune the short, medium, and long volatility windows for your style.

Toggle Lines: Show/hide Stdev or VoVix FVC lines independently.

Dashboard & Info Line: Toggle for your workflow and screen size.

How to Use

Compression (below green): Market is “coiling” across timeframes—watch for explosive moves.

Expansion (above red): Volatility is breaking out—expect regime shifts or trend acceleration.

Agreement Fill: When both lines agree, the signal is strongest.

Not a Buy/Sell Signal: These are regime and structure signals—combine with your own

strategy and risk management.

Why should you use FVC?

See what others can’t:

Most tools show only one dimension of volatility. FVC reveals the fractal DNA of market compression and expansion. Works on any asset, any timeframe. Professional, clean, and fully customizable.

Fractal Volatility Compression (FVC):

Because the next big move is born in the market’s hidden compression.

For educational purposes only. Not financial advice. Always use proper risk management

Use with discipline. Trade your edge.

— Dskyz, for DAFE Trading Systems

(MVD) Meta-Volatility Divergence (DAFE) Meta-Volatility Divergence (MVD)

Reveal the Hidden Tension in Volatility.

The Meta-Volatility Divergence (MVD) indicator is a next-generation tool designed to expose the disagreement between multiple volatility measures—helping you spot when the market’s “volatility engines” are out of sync, and a regime shift or volatility event may be brewing.

What Makes MVD Unique?

Multi-Source Volatility Analysis:

Unlike traditional volatility indicators that rely on a single measure, MVD fuses four distinct volatility signals:

ATR (Average True Range): Captures the average range of price movement.

Stdev (Standard Deviation): Measures the dispersion of closing prices.

Range: The average difference between high and low.

VoVix: A proprietary “volatility of volatility” metric, quantifying the difference between fast and slow ATR, normalized by ATR’s own volatility.

Divergence Engine:

The core MVD line (yellow) represents the mean absolute deviation (MAD) of these volatility measures from their average. When the line is flat, all volatility measures are in agreement. When the line rises, it means the market’s volatility signals are diverging—often a precursor to regime shifts, volatility expansions, or hidden stress.

Dynamic Z-Score Normalization:

The MVD line is normalized as a Z-score, so you can easily spot when current divergence is rare or extreme compared to recent history.

Visual Clarity:

Yellow center line: Tracks the real-time divergence of volatility measures.

Green dashed thresholds: Mark the ±2.00 Z-score levels, highlighting when divergence is unusually high and action may be warranted.

Dashboard: Toggleable panel shows all key metrics (ATR, Stdev, VoVix, MVD Z) and your custom branding.

Compact Info Label : For mobile or minimalist users, a single-line summary keeps you informed without clutter.

What Makes The MVD line move?

- The MVD line rises when the included volatility measures (ATR, Stdev, Range, VoVix) are moving in different directions or at different magnitudes. For example, if ATR is rising but Stdev is falling, the line will move up, signaling disagreement.

- The line falls or flattens when all volatility measures are in sync, indicating a consensus in the market’s volatility regime.

- VoVix adds a unique dimension, making the indicator especially sensitive to sudden changes in volatility structure that most tools miss.

Inputs & Settings

ATR Length: Sets the lookback for ATR calculation. Shorter = more sensitive, longer = smoother.

Stdev Length: Sets the lookback for standard deviation. Adjust for your asset’s volatility.

Range Length: Sets the lookback for the average high-low range.

MVD Lookback: Controls the window for Z-score normalization. Higher values = more historical context, lower = more responsive.

Show Dashboard: Toggle the full dashboard panel on/off.

Show Compact Info Label: Toggle the mobile-friendly info line on/off.

Tip:

Adjust these settings to match your asset’s volatility and your trading timeframe. There is no “one size fits all”—tuning is key to extracting the most value from MVD.

How to make MVD work for you:

Threshold Crosses: When the MVD line crosses above or below the green dashed thresholds (±2.00), it signals that volatility measures are diverging more than usual. This is a heads-up that a volatility event, regime shift, or hidden market stress may be developing.

Not a Buy/Sell Signal: A threshold cross is not a direct buy or sell signal. It is an indication that the market’s volatility structure is changing. Use it as a filter, confirmation, or alert in combination with your own strategy and risk management.

Dashboard & Info Line: Use the dashboard for a full view of all metrics, or the info label for a quick glance—especially useful on mobile.

Chart: MNQ! on 5min frames

ATR: 14

StDev L: 11

Range L: 13

MDV LB: 13

Important Note

MVD is a market structure and volatility regime tool.

It is designed to alert you to potential changes in market conditions, not to provide direct trade entries or exits. Always combine with your own analysis and risk management.

Meta-Volatility Divergence:

See the market’s hidden tension. Anticipate the next wave.

For educational purposes only. Not financial advice. Always use proper risk management.

Use with discipline. Trade your edge.

— Dskyz, for DAFE Trading Systems

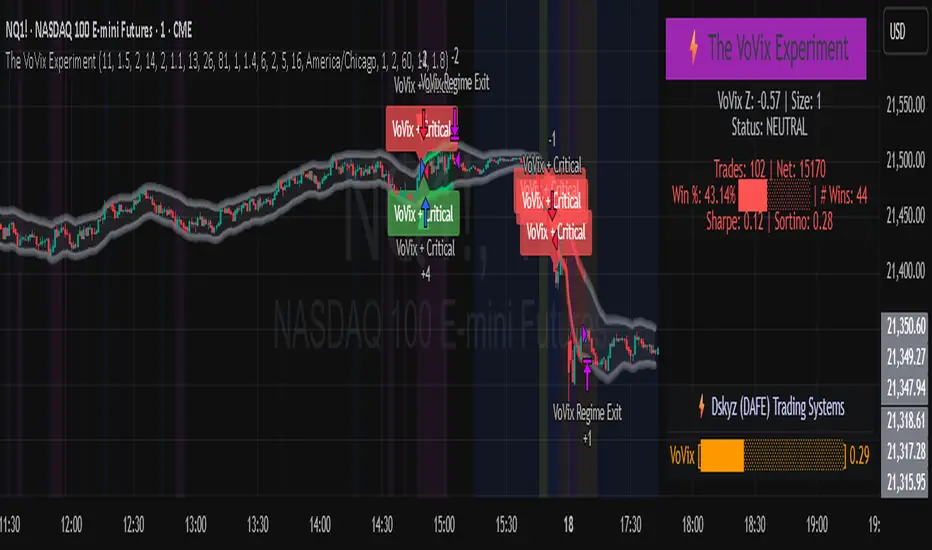

The VoVix Experiment The VoVix Experiment

The VoVix Experiment is a next-generation, regime-aware, volatility-adaptive trading strategy for futures, indices, and more. It combines a proprietary VoVix (volatility-of-volatility) anomaly detector with price structure clustering and critical point logic, only trading when multiple independent signals align. The system is designed for robustness, transparency, and real-world execution.

Logic:

VoVix Regime Engine: Detects pre-move volatility anomalies using a fast/slow ATR ratio, normalized by Z-score. Only trades when a true regime spike is detected, not just random volatility.

Cluster & Critical Point Filters: Price structure and volatility clustering must confirm the VoVix signal, reducing false positives and whipsaws.

Adaptive Sizing: Position size scales up for “super-spikes” and down for normal events, always within user-defined min/max.

Session Control: Trades only during user-defined hours and days, avoiding illiquid or high-risk periods.

Visuals: Aurora Flux Bands (From another Original of Mine (Options Flux Flow): glow and change color on signals, with a live dashboard, regime heatmap, and VoVix progression bar for instant insight.

Backtest Settings

Initial capital: $10,000

Commission: Conservative, realistic roundtrip cost:

15–20 per contract (including slippage per side) I set this to $25

Slippage: 3 ticks per trade

Symbol: CME_MINI:NQ1!

Timeframe: 15 min (but works on all timeframes)

Order size: Adaptive, 1–2 contracts

Session: 5:00–15:00 America/Chicago (default, fully adjustable)

Why these settings?

These settings are intentionally strict and realistic, reflecting the true costs and risks of live trading. The 10,000 account size is accessible for most retail traders. 25/contract including 3 ticks of slippage are on the high side for MNQ, ensuring the strategy is not curve-fit to perfect fills. If it works here, it will work in real conditions.

Forward Testing: (This is no guarantee. I've provided these results to show that executions perform as intended. Test were done on Tradovate)

ALL TRADES

Gross P/L: $12,907.50

# of Trades: 64

# of Contracts: 186

Avg. Trade Time: 1h 55min 52sec

Longest Trade Time: 55h 46min 53sec

% Profitable Trades: 59.38%

Expectancy: $201.68

Trade Fees & Comm.: $(330.95)

Total P/L: $12,576.55

Winning Trades: 59.38%

Breakeven Trades: 3.12%

Losing Trades: 37.50%

Link: www.dropbox.com

Inputs & Tooltips

VoVix Regime Execution: Enable/disable the core VoVix anomaly detector.

Volatility Clustering: Require price/volatility clusters to confirm VoVix signals.

Critical Point Detector: Require price to be at a statistically significant distance from the mean (regime break).

VoVix Fast ATR Length: Short ATR for fast volatility detection (lower = more sensitive).

VoVix Slow ATR Length: Long ATR for baseline regime (higher = more stable).

VoVix Z-Score Window: Lookback for Z-score normalization (higher = smoother, lower = more reactive).

VoVix Entry Z-Score: Minimum Z-score for a VoVix spike to trigger a trade.

VoVix Exit Z-Score: Z-score below which the regime is considered decayed (exit).

VoVix Local Max Window: Bars to check for local maximum in VoVix (higher = stricter).

VoVix Super-Spike Z-Score: Z-score for “super” regime events (scales up position size).

Min/Max Contracts: Adaptive position sizing range.

Session Start/End Hour: Only trade between these hours (exchange time).

Allow Weekend Trading: Enable/disable trading on weekends.

Session Timezone: Timezone for session filter (e.g., America/Chicago for CME).

Show Trade Labels: Show/hide entry/exit labels on chart.

Flux Glow Opacity: Opacity of Aurora Flux Bands (0–100).

Flux Band EMA Length: EMA period for band center.

Flux Band ATR Multiplier: Width of bands (higher = wider).

Compliance & Transparency

* No hidden logic, no repainting, no pyramiding.

* All signals, sizing, and exits are fully explained and visible.

* Backtest settings are stricter than most real accounts.

* All visuals are directly tied to the strategy logic.

* This is not a mashup or cosmetic overlay; every component is original and justified.

Disclaimer

Trading is risky. This script is for educational and research purposes only. Do not trade with money you cannot afford to lose. Past performance is not indicative of future results. Always test in simulation before live trading.

Proprietary Logic & Originality Statement

This script, “The VoVix Experiment,” is the result of original research and development. All core logic, algorithms, and visualizations—including the VoVix regime detection engine, adaptive execution, volatility/divergence bands, and dashboard—are proprietary and unique to this project.

1. VoVix Regime Logic

The concept of “volatility of volatility” (VoVix) is an original quant idea, not a standard indicator. The implementation here (fast/slow ATR ratio, Z-score normalization, local max logic, super-spike scaling) is custom and not found in public TradingView scripts.

2. Cluster & Critical Point Logic

Volatility clustering and “critical point” detection (using price distance from a rolling mean and standard deviation) are general quant concepts, but the way they are combined and filtered here is unique to this script. The specific logic for “clustered chop” and “critical point” is not a copy of any public indicator.

3. Adaptive Sizing

The adaptive sizing logic (scaling contracts based on regime strength) is custom and not a standard TradingView feature or public script.

4. Time Block/Session Control

The session filter is a common feature in many strategies, but the implementation here (with timezone and weekend control) is written from scratch.

5. Aurora Flux Bands (From another Original of Mine (Options Flux Flow)

The “glowing” bands are inspired by the idea of volatility bands (like Bollinger Bands or Keltner Channels), but the visual effect, color logic, and integration with regime signals are original to this script.

6. Dashboard, Watermark, and Metrics

The dashboard, real-time Sharpe/Sortino, and VoVix progression bar are all custom code, not copied from any public script.

What is “standard” or “common quant practice”?

Using ATR, EMA, and Z-score are standard quant tools, but the way they are combined, filtered, and visualized here is unique. The structure and logic of this script are original and not a mashup of public code.

This script is 100% original work. All logic, visuals, and execution are custom-coded for this project. No code or logic is directly copied from any public or private script.

Use with discipline. Trade your edge.

— Dskyz, for DAFE Trading Systems

REVELATIONS (VoVix - PoC) REVELATIONS (VoVix - POC): True Regime Detection Before the Move

Let’s not sugarcoat it: Most strategies on TradingView are recycled—RSI, MACD, OBV, CCI, Stochastics. They all lag. No matter how many overlays you stack, every one of these “standard” indicators fires after the move is underway. The retail crowd almost always gets in late. That’s never been enough for my team, for DAFE, or for anyone who’s traded enough to know the real edge vanishes by the time the masses react.

How is this different?

REVELATIONS (VoVix - POC) was engineered from raw principle, structured to detect pre-move regime change—before standard technicals even light up. We built, tested, and refined VoVix to answer one hard question:

What if you could see the spike before the trend?

Here’s what sets this system apart, line-by-line:

o True volatility-of-volatility mathematics: It’s not just "ATR of ATR" or noise smoothing. VoVix uses normalized, multi-timeframe v-vol spikes, instantly detecting orderbook stress and "outlier" market events—before the chart shows them as trends.

o Purist regime clustering: Every trade is enabled only during coordinated, multi-filter regime stress. No more signals in meaningless chop.

o Nonlinear entry logic: No trade is ever sent just for a “good enough” condition. Every entry fires only if every requirement is aligned—local extremes, super-spike threshold, regime index, higher timeframe, all must trigger in sync.

o Adaptive position size: Your contracts scale up with event strength. Tiny size during nominal moves, max leverage during true regime breaks—never guesswork, never static exposure.

o All exits governed by regime decay logic: Trades are closed not just on price targets but at the precise moment the market regime exhausts—the hardest part of systemic trading, now solved.

How this destroys the lag:

Standard indicators (RSI, MACD, OBV, CCI, and even most “momentum” overlays) simply tell you what already happened. VoVix triggers as price structure transitions—anyone running these generic scripts will trade behind the move while VoVix gets in as stress emerges. Real alpha comes from anticipation, not confirmation.

The visuals only show what matters:

Top right, you get a live, live quant dashboard—regime index, current position size, real-time performance (Sharpe, Sortino, win rate, and wins). Bottom right: a VoVix "engine bar" that adapts live with regime stress. Everything you see is a direct function of logic driving this edge—no cosmetics, no fake momentum.

Inputs/Signals—explained carefully for clarity:

o ATR Fast Length & ATR Slow Length:

These are the heart of VoVix’s regime sensing. Fast ATR reacts to sharp volatility; Slow ATR is stability baseline. Lower Fast = reacts to every twitch; higher Slow = requires more persistent, “real” regime shifts.

Tip: If you want more signals or faster markets, lower ATR Fast. To eliminate noise, raise ATR Slow.

o ATR StdDev Window: Smoothing for volatility-of-volatility normalization. Lower = more jumpy, higher = only the cleanest spikes trigger.

Tip: Shorten for “jumpy” assets, raise for indices/futures.

o Base Spike Threshold: Think of this as your “minimum event strength.” If the current move isn’t volatile enough (normalized), no signal.

Tip: Higher = only biggest moves matter. Lower for more signals but more potential noise.

o Super Spike Multiplier: The “are you sure?” test—entry only when the current spike is this multiple above local average.

Tip: Raise for ultra-selective/swing-trading; lower for more active style.

Regime & MultiTF:

o Regime Window (Bars):

How many bars to scan for regime cluster “events.” Short for turbo markets, long for big swings/trends only.

o Regime Event Count: Only trade when this many spikes occur within the Regime Window—filters for real stress, not isolated ticks.

Tip: Raise to only ever trade during true breakouts/crashes.

o Local Window for Extremes:

How many bars to check that a spike is a local max.

Tip: Raise to demand only true, “clearest” local regime events; lower for early triggers.

o HTF Confirm:

Higher timeframe regime confirmation (like 45m on an intraday chart). Ensures any event you act on is visible in the broader context.

Tip: Use higher timeframes for only major moves; lower for scalping or fast regimes.

Adaptive Sizing:

o Max Contracts (Adaptive): The largest size your system will ever scale to, even on extreme event.

Tip: Lower for small accounts/conservative risk; raise on big accounts or when you're willing to go big only on outlier events.

o Min Contracts (Adaptive): The “toe-in-the-water.” Smallest possible trade.

Tip: Set as low as your broker/exchange allows for safety, or higher if you want to always have meaningful skin in the game.

Trade Management:

o Stop %: Tightness of your stop-loss relative to entry. Lower for tighter/safer, higher for more breathing room at cost of greater drawdown.

o Take Profit %: How much you'll hold out for on a win. Lower = more scalps. Higher = only run with the best.

o Decay Exit Sensitivity Buffer: Regime index must dip this far below the trading threshold before you exit for “regime decay.”

Tip: 0 = exit as soon as stress fails, higher = exits only on stronger confirmation regime is over.

o Bars Decay Must Persist to Exit: How long must decay be present before system closes—set higher to avoid quick fades and whipsaws.

Backtest Settings

Initial capital: $10,000

Commission: Conservative, realistic roundtrip cost:

15–20 per contract (including slippage per side) I set this to $25

Slippage: 3 ticks per trade

Symbol: CME_MINI:NQ1!

Timeframe: 1 min (but works on all timeframes)

Order size: Adaptive, 1–3 contracts

No pyramiding, no hidden DCA

Why these settings?

These settings are intentionally strict and realistic, reflecting the true costs and risks of live trading. The 10,000 account size is accessible for most retail traders. 25/contract including 3 ticks of slippage are on the high side for NQ, ensuring the strategy is not curve-fit to perfect fills. If it works here, it will work in real conditions.

Tip: Set to 1 for instant regime exit; raise for extra confirmation (less whipsaw risk, exits held longer).

________________________________________

Bottom line: Tune the sensitivity, selectivity, and risk of REVELATIONS by these inputs. Raise thresholds and windows for only the best, most powerful signals (institutional style); lower for activity (scalpers, fast cryptos, signals in constant motion). Sizing is always adaptive—never static or martingale. Exits are always based on both price and regime health. Every input is there for your control, not to sell “complexity.” Use with discipline, and make it your own.

This strategy is not just a technical achievement: It’s a statement about trading smarter, not just more.

* I went back through the code to make sure no the strategy would not suffer from repainting, forward looking, or any frowned upon loopholes.

Disclaimer:

Trading is risky and carries the risk of substantial loss. Do not use funds you aren’t prepared to lose. This is for research and informational purposes only, not financial advice. Backtest, paper trade, and know your risk before going live. Past performance is not a guarantee of future results.

Expect more: We’ll keep pushing the standard, keep evolving the bar until “quant” actually means something in the public code space.

Use with clarity, use with discipline, and always trade your edge.

— Dskyz , for DAFE Trading Systems

Deviation over Deviation (DoD) (DAFE) Deviation over Deviation (DoD)

Let’s call it out: The vast majority of “volatility” tools on TradingView are just new wrappers on old math—ATR, bands, and basic deviation, all chasing the same tired after-the-fact moves. They’re built to describe the aftermath, not the ignition. If you’re still relying on these, you’re trading in the rearview mirror while the real edge is already gone. That’s not our game, and it shouldn’t be yours.

Deviation over Deviation (DoD) is built for one purpose:

To expose the hidden regime shifts—the moments when volatility itself becomes volatile, when the market’s “normal” deviation is no longer normal, and when the next move is about to erupt. This isn’t just another overlay. This is a quant-grade anomaly detector, engineered to show you the probability surface before the crowd even knows it’s changed.

What sets this apart:

Deviation over Deviation (DoD):

Not just “how much did price move,” but “how unusual is the current volatility compared to its own history?” This is the Z-score of Z-scores—a true rarity detector for market stress, lull, or impending breakout.

VoVix Integration:

Select VoVix as your source and you’re not just tracking price, but the volatility of volatility—the same math that powers institutional regime models. This is the edge that front-runs the move, not follows it.

Multi-Timeframe Comparative Engine:

Instantly compare current and higher timeframe DoD Z-scores. See when the micro and macro regimes align—or when they’re about to collide.

Professional, Adaptive Dashboard:

No cosmetic fluff, always showing you the real quant state: current DoD Z, HTF DoD Z, and regime warnings. Every color, every plot, every signal is a direct function of the logic—no distractions, no lag.

How this destroys the lag:

Standard deviation, ATR, and “volatility bands” are always late. They tell you what just happened. DoD and VoVix show you when the nature of volatility itself is changing—when the market is about to leave the old regime behind. This is the difference between trading the past and trading the future.

Inputs/Signals—explained for clarity:

Deviation Lookback & DoD Lookback:

Control the sensitivity and selectivity of the regime detector. Shorter = more signals, longer = only the rarest events.

Source Selection:

Choose from price, volume, volatility, or VoVix. Each source gives you a different lens on market stress. VoVix is for those who want to see the “regime quake” before the aftershocks.

HTF (Comparative Timeframe):

Set your higher timeframe for macro regime confirmation. When both DoD Z-scores align, you’re seeing a true market inflection.

VoVix Parameters:

Fine-tune the volatility-of-volatility engine for your market. Lower ATR Fast = more responsive; higher ATR Slow = more selective. Adjust for your asset, your timeframe, your edge.

Bottom line:

This isn’t just another “volatility” script. This is a regime anomaly detector, built for traders who want to anticipate, not react. Every input is there for a reason. Every plot is a direct readout of the quant logic. Use it to filter your entries, to time your exits, or to simply see the market’s hidden structure in real time.

Disclaimer:

Trading is risky. This script is for research and informational purposes only, not financial advice. Backtest, paper trade, and know your risk before going live. Past performance is not a guarantee of future results.

*Updated the Dashboard/Metrics Display for better visibility

Use with discipline. Trade your edge.

— Dskyz, for DAFE Trading Systems

(DAFE) DEVMA - Crossover (Deviation Moving Average) (DAFE) DEVMA - Crossover (Deviation Moving Average)

Let’s keep pushing the edge. After the breakthrough of Deviation over Deviation (DoD)—which gave traders a true lens into volatility’s hidden regime shifts—many asked: “What’s next?” The answer is DEVMA: a crossover engine built not on price, but on the heartbeat of the market itself.

Why is this different?

DEVMA isn’t just a moving average crossover. It’s a regime detector that tracks the expansion and contraction of deviation—giving you a real-time readout of when the market’s energy is about to shift. This is the next step for anyone who wants to anticipate volatility, not just react to it.

What sets DEVMA apart:

Volatility-First Logic:Both fast and slow lines are moving averages of deviation, not price. You’re tracking the market’s “energy,” not just its direction. This is the quant edge that most scripts miss.

Regime-Colored Lines:

The fast and slow DEVMA lines change color in real time—green/aqua for expansion, maroon/orange for contraction—so you can see regime shifts at a glance.

Quant-Pro Visuals:

Subtle glow, clean cross markers, and a minimalist dashboard keep your focus on what matters: the regime, not the noise.

Static Regime Thresholds:

Reference lines at 1.5 and 0.5 (custom colors) give you instant context for “normal” vs. “extreme” volatility states.

No Price Chasing:

This isn’t about following price. It’s about anticipating the next volatility regime—before the crowd even knows what’s coming.

How this builds on DoD:

DoD showed you when volatility itself was about to change. DEVMA takes that insight and turns it into a crossover engine—so you can see, filter, and act on regime shifts in real time. If DoD was the radar, DEVMA is the navigation system.

Inputs/Signals—explained for clarity:

Deviation Lookback:

Controls the sensitivity of the regime detector. Shorter = more signals, longer = only the rarest events.

Fast/Slow DEVMA Lengths:

Fine-tune how quickly the regime lines react. Fast for scalping, slow for swing trading.

Source Selection:

Choose from price, volume, volatility, or VoVix. Each source gives you a different lens on market stress. VoVix is for those who want to see the “regime quake” before the aftershocks.

VoVix Parameters:

Fine-tune the volatility-of-volatility engine for your market. Lower ATR Fast = more responsive; higher ATR Slow = more selective.

Bottom line:

DEVMA is for those who want to see the market’s heartbeat, not just its shadow. Use it to filter your trades, time your entries, or simply understand the market’s true rhythm. Every input is there for a reason. Every plot is a direct readout of the quant logic. Use with discipline, and make it your own.

Disclaimer:

Trading is risky. This script is for research and informational purposes only, not financial advice. Backtest, paper trade, and know your risk before going live. Past performance is not a guarantee of future results.

*Updated the Dashboard/Metrics Display for better visibility

Use with discipline. Trade your edge.

— Dskyz, for DAFE Trading Systems

Harmony in Havoc - The Entropy of VoVix Harmony in Havoc – The Entropy of VoVix

There are moments in the market when chaos and order are not opposites, but partners in a dance.

Harmony in Havoc is not just an indicator—it’s a window into that dance.

Most tools try to tame the market by smoothing it, boxing it in, or chasing after what’s already happened. This script does the opposite: it listens for the music beneath the noise, the rare moments when volatility and unpredictability align, and the market’s next movement is about to begin.

What is Harmony in Havoc?

VoVix Spike:

The pulse of volatility-of-volatility. Not just how much the market is moving, but how violently its own heartbeat is changing.

Entropy:

A real-time measure of surprise. When entropy is high, the market is not just moving—it’s breaking its own patterns, rewriting its own rules.

Progression Bar & Status:

The yellow bar is your visual gauge of tension. As it fills, the market is winding up.

Wait: The world is calm.

Get ready!: The storm is building.

Take Action!!: The probability of a regime eruption is at its peak.

Yellow Background:

When the background glows, the market is at its most unstable—this is not a buy or sell signal, but a quant alert.

How does it work?

Every tick, Harmony in Havoc measures the distance between the market’s current volatility and its own unpredictability. When the VoVix spike approaches or exceeds the entropy threshold, the system knows:

“This is the moment when the improbable becomes possible.”

Why is this different?

It doesn’t tell you what to do.

It doesn’t chase price.

It doesn’t care about trends, bands, or the past.

Instead, it gives you a quantitative sense of anticipation—a way to see when the market is most likely to break from its own history, and when the edge is at its sharpest.

How to use it:

Watch for the yellow background and “Take Action!!” status.

Use it as a regime filter, a volatility dashboard, or a warning system for your own strategies.

Tune the inputs for your asset and timeframe—make it your own.

Inputs—explained for you:

VoVix Fast/Slow ATR & Stdev:

Control how sensitive the system is to volatility shocks. Lower = more signals, higher = only the rarest events.

Entropy Window & Bins:

Control how “surprised” the entropy engine is by current volatility. Shorter window = more responsive, more bins = finer detail.

Show/Hide Controls:

Toggle the VoVix spike, entropy line, and their glows to customize your visual experience.

Bottom line:

This is not a buy or sell script.

This is a quant regime detector for those who want to feel the market’s tension—to sense when harmony and havoc are about to collide.

Disclaimer:

Trading is risky. This script is for research and informational purposes only, not financial advice. Backtest, paper trade, and know your risk before going live. Past performance is not a guarantee of future results.

*I've only tested this on 1 and 5 min frames.

Use with discipline. Trade your edge.

— Dskyz, for DAFE Trading Systems

3 days ago

Release Notes

* Now mobile friendly. I've added a toggle to switch the dashboard on/off, and added a mobile information line that shows the same information on the dashboard. This is to allow the script to stay visually in balance and this also has a toggle.

* Background color added that coresponds with Buy or Sell areas.

Kernel Regression Bands SuiteMulti-Kernel Regression Bands

A versatile indicator that applies kernel regression smoothing to price data, then dynamically calculates upper and lower bands using a wide variety of deviation methods. This tool is designed to help traders identify trend direction, volatility, and potential reversal zones with customizable visual styles.

Key Features

Multiple Kernel Types: Choose from 17+ kernel regression styles (Gaussian, Laplace, Epanechnikov, etc.) for smoothing.

Flexible Band Calculation: Select from 12+ deviation types including Standard Deviation, Mean/Median Absolute Deviation, Exponential, True Range, Hull, Parabolic SAR, Quantile, and more.

Adaptive Bands: Bands are calculated around the kernel regression line, with a user-defined multiplier.

Signal Logic: Trend state is determined by crossovers/crossunders of price and bands, coloring the regression line and band fills accordingly.

Custom Color Modes: Six unique color palettes for visual clarity and personal preference.

Highly Customizable Inputs: Adjust kernel type, lookback, deviation method, band source, and more.

How to Use

Trend Identification: The regression line changes color based on the detected trend (up/down)

Volatility Zones: Bands expand/contract with volatility, helping spot breakouts or mean-reversion opportunities.

Visual Styling: Use color modes to match your chart theme or highlight specific market states.

Credits:

Kernel regression logic adapted from:

ChartPrime | Multi-Kernel-Regression-ChartPrime (Link in the script)

Disclaimer

This script is for educational and informational purposes only. Not financial advice. Use at your own risk.

Percentage SDThis TradingView indicator, called "Percentage SD," measures how much the price of an asset is fluctuating (its volatility) and shows this as a percentage.

You can choose which price to track (like the closing price) and the period over which to measure this volatility.

The indicator then draws a yellow line in a separate panel below your main chart. When this line is higher, it means the price is more volatile relative to its current level. A lower line suggests less volatility. This can help you see when price movements are becoming more or less active.

Price Lag Factor (PLF)📊 Price Lag Factor (PLF) for Crypto Traders: A Comprehensive Breakdown

The Price Lag Factor (PLF) is a momentum indicator designed to identify overextended price movements and gauge market momentum. It is particularly optimized for the crypto market, which is known for its high volatility and rapid trend shifts.

🔎 What is the Price Lag Factor (PLF)?

The PLF measures the difference between long-term and short-term price momentum and scales it dynamically based on recent volatility. This helps traders identify when the market might be overbought or oversold while filtering out noise.

The formula used in the PLF calculation is:

PLF = (Z-Long - Z-Short) / Stdev(PLF)

Where:

Z-long: Z-score of the long-term moving average (50-period by default).

Z-short: Z-score of the short-term moving average (14-period by default).

Stdev(PLF): Standard deviation of the PLF over a longer period (50-period by default).

🧠 How to Interpret the PLF:

1. Trend Direction:

Positive PLF (Green Bars): Indicates bullish momentum. The long-term trend is up, and short-term movements are confirming it.

Negative PLF (Red Bars): Indicates bearish momentum. The long-term trend is down, and short-term movements are consistent with it.

2. Momentum Strength:

PLF near Zero (±0.5): Low momentum; trend direction is not strong.

PLF between ±1 and ±2: Moderate momentum, indicating that the market is moving with strength but not in an overextended state.

PLF beyond ±2: High momentum (overbought/oversold), indicating potential trend exhaustion and a possible reversal.

📈 Trading Strategies:

1. Trend Following:

Bullish Signal:

Enter long when PLF crosses above 0 and remains green.

Confirm with other indicators like RSI or MACD to reduce false signals.

Bearish Signal:

Enter short when PLF crosses below 0 and remains red.

Use trend confirmation (e.g., moving average crossover) for better accuracy.

2. Reversal Trading:

Overbought Signal:

If PLF rises above +2, look for signs of bearish divergence or a reversal pattern to consider a short entry.

Oversold Signal:

If PLF falls below -2, watch for bullish divergence or a support bounce to consider a long entry.

3. Momentum Divergence:

Bullish Divergence:

Price makes a lower low while PLF makes a higher low.

Indicates weakening bearish momentum and a potential bullish reversal.

Bearish Divergence:

Price makes a higher high while PLF makes a lower high.

Signals weakening bullish momentum and a potential bearish reversal.

💡 Best Practices:

Combine with Volume:

Volume spikes during high PLF readings can confirm trend continuation.

Low volume during PLF extremes may hint at false breakouts.

Watch for Extreme Levels:

PLF beyond ±2 suggests overextended price action. Use caution when entering new positions.

Confirm with Other Indicators:

Use with Relative Strength Index (RSI) or Bollinger Bands to get a better sense of overbought/oversold conditions.

Overlay with a moving average to gauge trend consistency.

🚀 Why the PLF Works for Crypto:

Crypto markets are highly volatile and prone to rapid trend changes. The PLF's adaptive scaling ensures it remains relevant regardless of market conditions.

It highlights momentum shifts more accurately than static indicators because it accounts for changing volatility in its calculation.

🚨 Disclaimer for Traders Using the Price Lag Factor (PLF) Indicator:

The Price Lag Factor (PLF) indicator is designed as a technical analysis tool to gauge momentum and identify potential overbought or oversold conditions. However, it should not be relied upon as a sole decision-making factor for trading or investing.

Important Points to Consider:

Market Risk: Trading cryptocurrencies and other financial assets involves significant risk. The PLF may not accurately predict future price movements, especially during unexpected market events.

Indicator Limitations: No technical indicator, including the PLF, is infallible. False signals can occur, particularly in low-volume or highly volatile conditions.

Supplementary Analysis: Always combine PLF insights with other technical indicators, fundamental analysis, and risk management strategies to make informed decisions.

Personal Judgment: Traders should use their own discretion when interpreting PLF signals and never trade based solely on this indicator.

No Guarantees: The PLF is designed for educational and informational purposes only. Past performance is not indicative of future results.

Always perform thorough research and consider consulting with a professional financial advisor before making any trading decisions.

VolVolVolVol: Volatility & Volume

The indicator consists of 3 oscillating components that are all represented on a positive/negative percentage scale.

Direction : Green/Red shaded area

Smoothened distance between Close and EMA of Close relative to StDev of Close

Intensity : Turquoise line

If direction = bullish: Smoothened distance between Low and EMA of Low relative to StDev of Low

If direction = bearish: Smoothened distance between High and EMA of High relative to StDev of High

Momentum : Fuchsia line

Double exponential average of bullish closing volume - bearish closing volume

The indicator provides the following signals on the candlestick charts based on the above components' movements.

Bullish position signals: Below candles

Bearish position signals: Above candles

Entry signal : Increase in all 3 factors or sharp increase in Intensity + Momentum

Add signal : Trend slowdown because of volume drop or retracement following a temporary consolidation

Exit signal : Increase in Intensity and Momentum against the prevailing trend direction

There may be simultaneous Bullish and Bearish signals. These should be treated as hedges for existing positions.

Day’s Open ForecastOverview

This Pine Script indicator combines two primary components:

1. Day’s Open Forecast:

o Tracks historical daily moves (up and down) from the day’s open.

o Calculates average up and down moves over a user-defined lookback period.

o Optionally includes standard deviation adjustments to forecast potential intraday levels.

o Plots lines on the chart for the forecasted up and down moves from the current day's open.

2. Session VWAP:

o Allows you to specify a custom trading session (by time range and UTC offset).

o Calculates and plots a Volume-Weighted Average Price (VWAP) during that session.

By combining these two features, you can gauge potential intraday moves relative to historical behavior from the open, while also tracking a session-specific VWAP that can act as a dynamic support/resistance reference.

How the Code Works

1. Collect Daily Moves

o The script detects when a new day starts using time("D").

o Once a new day is detected, it stores the previous day’s up-move (dayHigh - dayOpen) and down-move (dayOpen - dayLow) into arrays.

o These arrays keep track of the last N days (default: 126) of up/down move data.

2. Compute Statistics

o The script computes the average (f_average()) of up-moves and down-moves over the stored period.

o It also computes the standard deviation (f_stddev()) of up/down moves for optional “forecast bands.”

3. Forecast Lines

o Plots the current day’s open.

o Plots the average forecast lines above and below the open (Avg Up Move Level and Avg Down Move Level).

o If standard deviation is enabled, plots additional lines (Avg+StdDev Up and Avg+StdDev Down).

4. Session VWAP

o The script detects the start of a user-defined session (via input.session) and resets accumulation of volume and the numerator for VWAP.

o As each bar in the session updates, it accumulates volume (vwapCumulativeVolume) and a price-volume product (vwapCumulativeNumerator).

o The session VWAP is then calculated as (vwapCumulativeNumerator / vwapCumulativeVolume) and plotted.

5. Visualization Options

o Users can toggle standard deviation usage, historical up/down moves plotting, and whether to show the forecast “bands.”

o The vwapSession and vwapUtc inputs let you adjust which session (and time zone offset) the VWAP is calculated for.

________________________________________

How to Use This Indicator on TradingView

1. Create a New Script

o Open TradingView, then navigate to Pine Editor (usually found at the bottom of the chart).

o Copy and paste the entire code into the editor.

2. Save and Add to Chart

o Click Save (give it a relevant title if you wish), then click Add to chart.

o The indicator will appear on your chart with the forecast lines and VWAP.

o By default, it is overlayed on the price chart (because of overlay=true).

3. Customize Inputs

o In the indicator’s settings, you can:

Change lookback days (default: 126).

Enable or disable standard deviation (Include Standard Deviation in Forecast?).

Adjust the standard deviation multiplier.

Choose whether to plot bands (Plot Bands with Averages/StdDev?).

Plot historical moves if desired (Plot Historical Up/Down Moves for Reference?).

Set your custom session and UTC offset for the VWAP calculation.

4. Interpretation

o “Current Day Open” is simply today’s open price on your chart.

o Up/Down Move Lines: Indicate a potential forecast based on historical averages.

If standard deviation is enabled, the second set of lines acts as an extended range.

o VWAP: Helpful for determining intraday price equilibrium over the specified session.

Important Notes / Best Practices

• The script only updates the historical up/down move data once per day (when a new day starts).

• The VWAP portion resets at the start of the specified session each day.

• Standard deviation multiplies the average up/down range, giving you a sense of “volatility range” around the day’s open.

• Adjust the lookback length (dayCount) to balance how many days of data you want to average. More days = smoother but possibly slower to adapt; fewer days = more reactive but potentially less reliable historically.

Educational & Liability Disclaimers

1. Educational Disclaimer

o The information provided by this indicator is for educational and informational purposes only. It is a technical analysis tool intended to demonstrate how to use historical data and basic statistics in Pine Script.

2. No Financial Advice

o This script does not constitute financial or investment advice. All examples and explanations are solely illustrative. You should always do your own analysis before making any investment decisions.

3. No Liability

o The author of this script is not liable for any losses or damages—monetary or otherwise—that may occur from the application of this script.

o Past performance does not guarantee future results, and you should never invest money you cannot afford to lose.

By adding this indicator to your TradingView chart, you acknowledge and accept that you alone are responsible for your own trading decisions.

Enjoy using the “Day’s Open Forecast” and Session VWAP for better market insights!

Spent Output Profit Ratio (SOPR) Z-Score | [DeV]SOPR Z-Score

The Spent Output Profit Ratio (SOPR) is an advanced on-chain metric designed to provide deep insights into Bitcoin market dynamics by measuring the ratio between the combined USD value of all Bitcoin outputs spent on a given day and their combined USD value at the time of creation (typically, their purchase price). As a member of the Realized Profit/Loss family of metrics, SOPR offers a window into aggregate seller behavior, effectively representing the USD amount received by sellers divided by the USD amount they originally paid. This indicator enhances this metric by normalizing it into a Z-Score, enabling a statistically robust analysis of market sentiment relative to historical trends, augmented by a suite of customizable features for precision and visualization.

SOPR Settings -

Lookback Length (Default: 150 days): Determines the historical window for calculating the Z-Score’s mean and standard deviation. A longer lookback captures broader market cycles, providing a stable baseline for identifying extreme deviations, which is particularly valuable for long-term strategic analysis.

Smoothing Period (Default: 100 days): Applies an EMA to the raw SOPR, balancing responsiveness to recent changes with noise reduction. This extended smoothing period ensures the indicator focuses on sustained shifts in seller behavior, ideal for institutional-grade trend analysis.

Moving Average Settings -

MA Lookback Length (Default: 90 days): Sets the period for the Z-Score’s moving average, offering a shorter-term trend signal relative to the 150-day Z-Score lookback. This contrast enhances the ability to detect momentum shifts within the broader context.

MA Type (Default: EMA): Provides six moving average types, from the simple SMA to the volume-weighted VWMA. The default EMA strikes an optimal balance between smoothness and responsiveness, while alternatives like HMA (Hull) or VWMA (volume-weighted) allow for specialized applications, such as emphasizing recent price action or incorporating volume dynamics.

Display Settings -

Show Moving Average (Default: True): Toggles the visibility of the Z-Score MA plot, enabling users to focus solely on the raw Z-Score when preferred.

Show Background Colors (Default: True): Activates dynamic background shading, enhancing visual interpretation of market regimes.

Background Color Source (Default: SOPR): Allows users to tie the background color to either the SOPR Z-Score’s midline (reflecting adjustedZScore > 0) or the MA’s trend direction (zScoreMA > zScoreMA ). This dual-source option provides flexibility to align the visual context with the primary analytical focus.

Analytical Applications -

Bear Market Resistance: When the Z-Score approaches or exceeds zero (raw SOPR near 1), it often signals resistance as sellers rush to exit at break-even, a pattern historically observed during downtrends. A rising Z-Score MA crossing zero can confirm this pressure.

Bull Market Support: Conversely, a Z-Score dropping below zero in uptrends indicates reluctance to sell at a loss, forming support as sell pressure diminishes. The MA’s bullish coloring reinforces confirmation of renewed buying interest.

Extreme Deviations: Values significantly above or below zero highlight overbought or oversold conditions, respectively, offering opportunities for contrarian positioning when paired with other on-chain or price-based metrics.

Sharpe Ratio ScreenerThe original code was created by tim_amblard , and the modifications were made by Mr_Rakun for the purpose of adapting the script into a screener format.

The Sharpe ratio is a popular metric used to measure the risk-adjusted return of an asset or portfolio, which allows traders and investors to assess whether the returns they are receiving are worth the risk they are taking. In this script, the Sharpe ratio is calculated over a 180-day period (approximately 6 months), and several valuation zones are defined based on the ratio to help assess whether an asset is overvalued, undervalued, or critically undervalued.

Key Features:

1. Risk-Free Rate Input: The user can define the risk-free rate (usually the return of government bonds or a similar safe asset) for Sharpe ratio calculation.

2. Lookback Period (180 Days): The default lookback period is set to 180 days (approximately 6 months) to calculate the mean and standard deviation of the asset’s daily returns.

3. Valuation Zones:

• Overvalued Zone: If the Sharpe ratio is greater than 5.

• Undervalued Zone: If the Sharpe ratio is between -1 and 5.

• Critically Undervalued Zone: If the Sharpe ratio is below -3.

• Neutral Zone: If the Sharpe ratio does not meet any of the above conditions.

4. Table View: The script pulls a list of symbols from the user (e.g., cryptocurrency or stock tickers) and displays their latest price, Sharpe ratio, and whether they are in an overvalued, undervalued, or neutral zone in a table format.

5. Custom Symbol Input: The user can input a list of symbols (separated by commas) to track.

6. Daily Timeframe Check: The script warns the user to ensure they are using a daily timeframe, as this indicator is designed specifically for it.

How It Works:

• The script calculates the daily returns for each symbol over the specified lookback period.

• It then calculates the mean and standard deviation of the returns to derive the Sharpe ratio.

• The Sharpe ratio is annualized, and it’s compared to the defined thresholds to categorize the symbol into different valuation zones.

• A table is generated on the chart to show the symbols, their current prices, and their Sharpe ratios, with color-coded background to easily identify whether they are overvalued (red), undervalued (green), or critically undervalued (blue).

This tool is useful for screening multiple assets for their Sharpe ratio to find investment opportunities with optimal risk-adjusted returns.

Original code credit: This code was originally written by tim_amblard and modified by Mr_Rakun for use as a screener.

Türkçe Açıklama:

Orijinal kod tim_amblard tarafından yazılmıştır ve Mr_Rakun tarafından, bu script’in tarayıcı formatına dönüştürülmesi amacıyla değiştirilmiştir.

Sharpe oranı, bir varlığın veya portföyün risk düzeltilmiş getirisini ölçmek için yaygın olarak kullanılan bir metriktir. Bu metrik, yatırımcıların aldıkları risk karşılığında aldıkları getirinin ne kadar verimli olduğunu değerlendirmelerine olanak tanır. Bu script’te, Sharpe oranı 180 günlük bir periyot (yaklaşık 6 ay) boyunca hesaplanır ve oranı baz alarak varlıkların değerleme bölgeleri tanımlanır: aşırı değerli, değerli ve kritik şekilde değersiz.

Ana Özellikler:

1. Risk-Free Rate (Risk-Free Oranı) Girişi: Kullanıcı, Sharpe oranı hesaplaması için risk-free (risksiz) oranı (genellikle devlet tahvilleri veya benzeri güvenli bir varlık getirisi) tanımlayabilir.

2. Lookback (Geribildirim) Periyodu (180 Gün): Varsayılan geribildirim periyodu, varlığın günlük getirilerinin ortalama ve standart sapmalarını hesaplamak için 180 gün (yaklaşık 6 ay) olarak ayarlanmıştır.

3. Değerleme Bölgeleri:

• Aşırı Değerli Bölge: Sharpe oranı 5’ten büyükse.

• Değerli Bölge: Sharpe oranı -1 ile 5 arasında ise.

• Kritik Derecede Değersiz Bölge: Sharpe oranı -3’ten küçükse.

• Nötr Bölge: Sharpe oranı yukarıdaki hiçbir koşulu karşılamıyorsa.

4. Tablo Görünümü: Script, kullanıcıdan alınan semboller listesine göre (örneğin, kripto para veya hisse senedi sembolleri) her bir sembolün son fiyatını, Sharpe oranını ve değerleme bölgesini tablo şeklinde gösterir.

5. Özel Sembol Girişi: Kullanıcı, izlemek istediği semboller listesini (virgülle ayrılmış) girebilir.

6. Günlük Zaman Çerçevesi Kontrolü: Script, kullanıcının doğru sonuçlar almak için günlük zaman çerçevesinde işlem yapması gerektiğini hatırlatır.

Nasıl Çalışır:

• Script, her sembol için belirtilen geribildirim periyodu boyunca günlük getirileri hesaplar.

• Ardından, getirilerin ortalama ve standart sapmasını hesaplayarak Sharpe oranını çıkarır.

• Sharpe oranı yıllıklaştırılır ve tanımlanan eşiklerle karşılaştırılarak sembol, farklı değerleme bölgelerine kategorize edilir.

• Grafik üzerinde, semboller, mevcut fiyatları ve Sharpe oranları gösteren bir tablo oluşturulur. Bu tablo, hangi sembollerin aşırı değerli (kırmızı), değerli (yeşil) veya kritik derecede değersiz (mavi) olduğunu kolayca görmek için renk kodlu arka planlar kullanır.

Bu araç, yatırım fırsatlarını daha verimli bir şekilde değerlendirebilmek için risk düzeltilmiş getiri açısından optimal fırsatları bulmak için birden fazla varlığın Sharpe oranlarını taramak için kullanışlıdır.

Volatility BandsThe Volatility Bands script is a custom indicator designed to help traders visualize volatility levels in the market. It calculates dynamic bands around a central moving average, providing insights into potential support and resistance levels based on recent price action.

The script calculates multiple volatility bands (u0, u1, u2, d0, d1, d2) that adjust based on recent price movements. The outer bands (u2 and d2) represent extreme volatility levels, while the inner bands (u0, u1, d0, d1) indicate more immediate support and resistance.

Look for price reactions at the band levels. A touch of the upper bands may indicate overbought conditions, while a touch of the lower bands may indicate oversold conditions.

Central Moving Average: A smoothed moving average that adapts to price changes, providing a clear trend direction.

The script has no input parameters.

Script Functions:

erf(x): Calculates the error function for a given input x. Used in the calculation of the smoothing factor for the UMA.

uma(input): Provides a smoothed average that adapts to recent price changes, reducing lag compared to traditional moving averages.

dev(input, mu): Used to calculate the volatility bands around the central moving average.