RPT Position Sizer🎯 Purpose

This indicator is a position sizing and stop-loss calculator designed to help traders instantly determine:

How many shares/contracts to buy,

How much risk (₹) they are taking per trade,

How much capital will be deployed, and

The precise stop-loss price level based on user-defined parameters.

It displays all key values in a compact on-chart table (bottom-left corner) for quick trade planning.

💡 Use Case

Perfect for discretionary swing traders, systematic position traders, and risk managers who want instant visual feedback of trade sizing metrics directly on the chart — eliminating manual calculations and improving discipline.

⚙️ Key Features

Dynamic Inputs

Trading Capital (₹) — total available capital for trading.

RPT % — risk-per-trade as a percentage of total capital.

SL % — stop-loss distance in percent below CMP (Current Market Price).

CMP Source — can be linked to close, hl2, etc.

Rounding Style — round position size to Nearest, Floor, or Ceil.

Decimals Show — control number formatting precision in the table.

Core Calculations

SL Points: CMP × SL%

SL Price: CMP − SL Points

Risk Amount (₹): Capital × RPT%

Position Size: Risk ÷ SL Points

Capital Used: Position Size × CMP

Clean On-Chart Table Display

Displays:

Trading Capital

RPT %

Risk Amount (₹)

Position Size (shares/contracts)

Capital Required (₹)

Stop-Loss % & SL Price

The table uses a minimalistic white-on-black design with clear labeling and rupee formatting for quick reference.

Data Window Integration

Plots hidden values (Position Size, Risk Amount, SL Points, Capital Used) for use in TradingView’s Data Window—ideal for strategy testing and exporting values.

Statistics

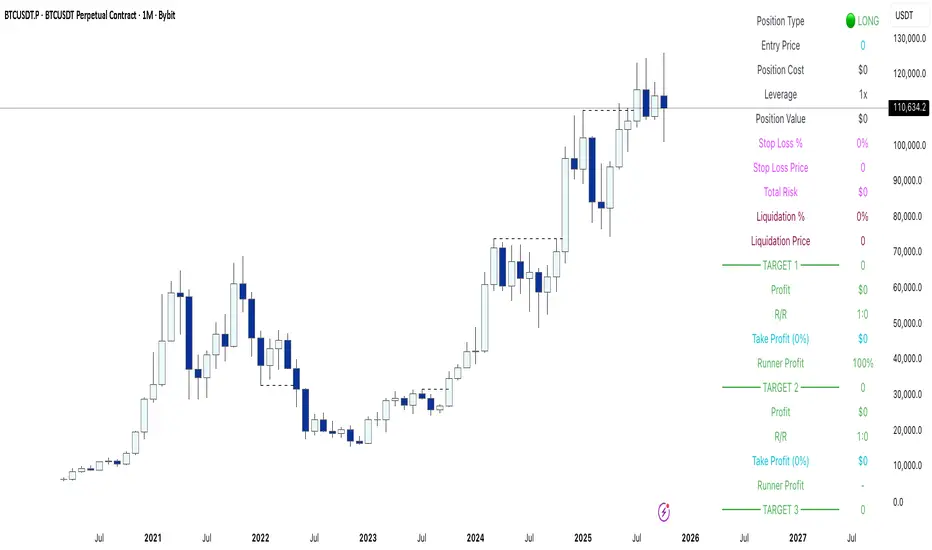

Yuki Leverage RR Calculator**YUKI LEVERAGE RR CALCULATOR**

A professional-grade risk/reward calculator for leveraged crypto or forex trades.

Instantly visualizes entry, stop loss, targets, leverage, and risk-to-reward ratios — helping you plan precise positions with confidence.

──────────────────────────────

**WHAT IT DOES**

Calculates position value, quantity, stop-loss price, liquidation estimate, and per-target profit.

Displays everything in an on-chart table with optional price tags and alerts.

──────────────────────────────

**KEY FEATURES**

• Long / Short toggle (only one active at a time)

• Leverage-aware position sizing based on Position Cost ($) and Leverage

• Dynamic Stop Loss: input % → auto price + $ risk

• Up to 3 Take-Profit Targets with scaling logic

• Instant R:R ratios per target

• Liquidation estimate (approximation only)

• ENTRY / SL / T1 / T2 / T3 / LIQ visual tags

• Dark/Light mode, adjustable table and tag size

• Built-in alerts for Targets and Stop Loss

──────────────────────────────

**INPUTS**

• Long or Short selection

• Entry Price, Stop Loss %

• Target 1 / Target 2 / Target 3 + Take Profit %

• Position Cost ($), Leverage

• Visual preferences: show/hide table, table corner, font size, tag offset, text size

──────────────────────────────

**TABLE OUTPUTS**

Position Info: Type, Entry, Position Cost, Leverage, Value

Risk Section: Stop Loss %, Stop Loss Price, Total Risk ($), Liquidation % & Price

Targets 1–3: Profit ($), R:R, Take Profit ($), Runner % or PnL

──────────────────────────────

**ALERTS**

• Target 1 Hit – when price crosses T1

• Target 2 Hit – when price crosses T2

• Target 3 Hit – when price crosses T3

• Stop Loss Hit – triggers based on direction

(Use TradingView Alerts → Condition → Indicator → select desired alert)

──────────────────────────────

**HOW TO USE**

1. Choose Long or Short

2. Enter Entry Price, Stop Loss %, Position Cost, and Leverage

3. Add Targets 1–3 with optional Take Profit %

4. Adjust visuals as desired

5. Monitor table + alerts for live trade planning

──────────────────────────────

**NOTES**

• Liquidation values are estimates only

• Fees, slippage, and funding not included

• Designed for educational and planning purposes

──────────────────────────────

⚠️ **DISCLAIMER**

For educational use only — not financial advice.

Trading leveraged products involves high risk of loss.

Always confirm calculations with your exchange and trade responsibly.

Z-Score Momentum | MisinkoMasterThe Z-Score Momentum is a new trend analysis indicator designed to catch reversals, and shifts in trends by comparing the "positive" and "negative" momentum by using the Z-Score.

This approach helps traders and investors get unique insight into the market of not just Crypto, but any market.

A deeper dive into the indicator

First, I want to cover the "Why?", as I believe it will ease of the part of the calculation to make it easier to understand, as by then you will understand how it fits the puzzle.

I had an attempt to create a momentum oscillator that would catch reversals and provide high tier accuracy while maintaining the main part => the speed.

I thought back to many concepts, divergences between averages?

- Did not work

Maybe a MACD rework?

- Did not work with what I tried :(

So I thought about statistics, Standard Deviation, Z-Score, Sharpe/Sortino/Omega ratio...

Wait, was that the Z-Score? I only tried the For Loop version of it :O

So on my way back from school I formulated a concept (originaly not like this but to that later) that would attempt to use the Z-Score as an accurate momentum oscillator.

Many ideas were falling out of the blue, but not many worked.

After almost giving up on this, and going to go back to developing my strategies, I tried one last thing:

What if we use divergences in the average, formulated like a Z-score?

Surprise-surprise, it worked!

Now to explain what I have been so passionately yapping about, and to connect the pieces of the puzzle once and for all:

The indicator compares the "strength" of the bullish/bearish factors (could be said differently, but this is my "speach bubble", and I think this describes it the best)

What could we use for the "bullish/bearish" factors?

How about high & low?

I mean, these are by definitions the highest and lowest points in price, which I decided to interpret as: The highest the bull & bear "factors" achieved that bar.

The problem here is comparison, I mean high will ALWAYS > low, unless the asset decided to unplug itself and stop moving, but otherwise that would be unfair.

Now if I use my Z-score, it will get higher while low is going up, which is the opposite of what I want, the bearish "factor" is weaker while we go up!

So I sat on my ret*rded a*s for 25 minutes, completly ignoring the fact the number "-1" exists.

Surprise surprise, multiplying the Z-Score of the low by -1 did what I wanted!

Now it reversed itself (magically). Now while the low keeps going down, the bear factor increases, and while it goes up the bear factor lowers.

This was btw still too noisy, so instead of the classic formula:

a = current value

b = average value

c = standard deviation of a

Z = (a-b)/c

I used:

a = average value over n/2 period

b = average value over n period

c = standard deviation of a

Z = (a-b)/c

And then compared the Z-Score of High to the Z-Score of Low by basic subtraction, which gives us final result and shows us the strength of trend, the direction of the trend, and possibly more, which I may have not found.

As always, this script is open source, so make sure to play around with it, you may uncover the treasure that I did not :)

Enjoy Gs!

IB range + Breakout fibsThe IB High / Low + Auto-Fib indicator automatically plots the Initial Balance range and a Fibonacci projection for each trading day.

Define your IB start and end times (e.g., 09:30–10:30).

The indicator marks the IB High and IB Low from that session and extends them to the session close.

It keeps the last N days visible for context.

When price breaks outside the IB range, it automatically plots a Fibonacci retracement/extension from the opposite IB side to the breakout, using levels 0, 0.236, 0.382, 0.5, 0.618, 0.88, 1.

The Fib updates dynamically as the breakout extends, and labels are neatly aligned on the right side of the chart for clarity.

Ideal for traders who monitor Initial Balance breaks, range expansions, and Fibonacci reaction levels throughout the trading session.

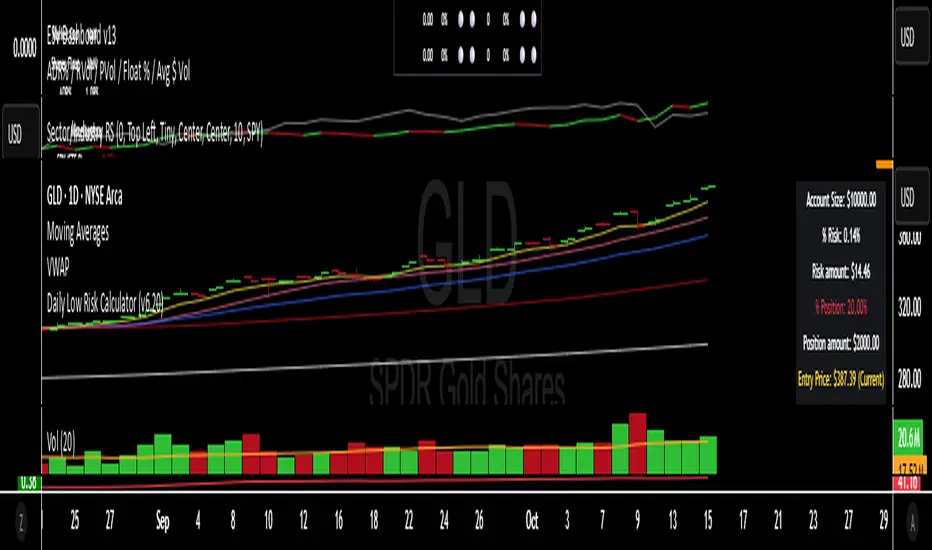

Risk sizing toolHelps you manage risk per trade accurately.

Automatically adjusts position size if the stop-loss or account constraints are exceeded.

Gives a clear visual summary directly on your stock chart.

Prevents taking trades that are too large relative to your account.

Volume v4 (Dollar Value) by Koenigsegg📊 Volume v3 (Dollar Value) by Koenigsegg

🎯 Purpose:

Volume v3 (Dollar Value) by Koenigsegg transforms traditional raw-unit volume into dollar-denominated volume, revealing how much money actually flows through each candle.

Instead of measuring how many coins or contracts were traded, this version calculates the total traded value = volume × average price (hlc3), allowing traders to visually assess capital intensity and market participation within each move.

⚙️ Core Features

- Converts raw volume into USD-based traded value for each candle.

- Color-coded bars show bullish (green/teal) vs. bearish (red) activity.

- Built-in SMA and SMMA overlays highlight sustained shifts in value flow.

- Designed for visual clarity to support momentum, exhaustion, and divergence studies.

📖 How to Read It

Rising Dollar Volume — indicates growing market participation and strong capital flow, often aligning with impulsive waves in trend direction.

Falling Dollar Volume — signals waning interest or reduced participation, potentially hinting at correction or exhaustion phases.

Comparing Legs — when price makes new highs/lows but dollar volume weakens, it can reveal divergences between price movement and actual capital commitment.

SMA / SMMA Lines — use them to identify longer-term accumulation or depletion of market activity, separating short bursts from sustained inflows or outflows.

The goal is to visualize the strength of market moves in terms of capital energy, not just tick activity. This distinction helps traders interpret whether a trend is being driven by genuine money flow or low-liquidity drift.

⚠️ Disclaimer

This script is provided for research and educational purposes only.

It does not constitute financial advice, investment recommendations, or trading signals.

Always conduct your own analysis and manage your own risk when trading live markets.

The author accepts no liability for financial losses incurred from use of this tool.

🧠 Credits

Developed and published by Koenigsegg.

Written in Pine Script® v6, fully compliant with TradingView’s House Rules for Pine Scripts.

Licensed under the Mozilla Public License 2.0.

Cumulative Volume Delta Z Score [BackQuant]Cumulative Volume Delta Z Score

The Cumulative Volume Delta Z Score indicator is a sophisticated tool that combines the cumulative volume delta (CVD) with Z-Score normalization to provide traders with a clearer view of market dynamics. By analyzing volume imbalances and standardizing them through a Z-Score, this tool helps identify significant price movements and market trends while filtering out noise.

Core Concept of Cumulative Volume Delta (CVD)

Cumulative Volume Delta (CVD) is a popular indicator that tracks the net difference between buying and selling volume over time. CVD helps traders understand whether buying or selling pressure is dominating the market. Positive CVD signals buying pressure, while negative CVD indicates selling pressure.

The addition of Z-Score normalization to CVD makes it easier to evaluate whether current volume imbalances are unusual compared to past behavior. Z-Score helps in detecting extreme conditions by showing how far the current CVD is from its historical mean in terms of standard deviations.

Key Features

Cumulative Volume Delta (CVD): Tracks the net buying vs. selling volume, allowing traders to gauge the overall market sentiment.

Z-Score Normalization: Converts CVD into a standardized value to highlight extreme movements in volume that are statistically significant.

Divergence Detection: The indicator can spot bullish and bearish divergences between price and CVD, which can signal potential trend reversals.

Pivot-Based Divergence: Identifies price and CVD pivots, highlighting divergence patterns that are crucial for predicting price changes.

Trend Analysis: Colors bars according to trend direction, providing a visual indication of bullish or bearish conditions based on Z-Score.

How It Works

Cumulative Volume Delta (CVD): The CVD is calculated by summing the difference between buying and selling volume for each bar. It represents the net buying or selling pressure, giving insights into market sentiment.

Z-Score Normalization: The Z-Score is applied to the CVD to normalize its values, making it easier to compare current conditions with historical averages. A Z-Score greater than 0 indicates a bullish market, while a Z-Score less than 0 signals a bearish market.

Divergence Detection: The indicator detects regular and hidden bullish and bearish divergences between price and CVD. These divergences often precede trend reversals, offering traders a potential entry point.

Pivot-Based Analysis: The indicator uses pivot highs and lows in both price and CVD to identify divergence patterns. A bullish divergence occurs when price makes a lower low, but CVD fails to follow, suggesting weakening selling pressure. Conversely, a bearish divergence happens when price makes a higher high, but CVD doesn't confirm the move, indicating potential selling pressure.

Trend Coloring: The bars are colored based on the trend direction. Green bars indicate an uptrend (CVD is positive), and red bars indicate a downtrend (CVD is negative). This provides an easy-to-read visualization of market conditions.

Standard Deviation Levels: The indicator plots ±1σ, ±2σ, and ±3σ levels to indicate the degree of deviation from the average CVD. These levels act as thresholds for identifying extreme buying or selling pressure.

Customization Options

Anchor Timeframe: The user can define an anchor timeframe to aggregate the CVD, which can be customized based on the trader’s needs (e.g., daily, weekly, custom lower timeframes).

Z-Score Period: The period for calculating the Z-Score can be adjusted, allowing traders to fine-tune the indicator's sensitivity.

Divergence Detection: The tool offers controls to enable or disable divergence detection, with the ability to adjust the lookback periods for pivot detection.

Trend Coloring and Visuals: Traders can choose whether to color bars based on trend direction, display standard deviation levels, or visualize the data as a histogram or line plot.

Display Options: The indicator also allows for various display options, including showing the Z-Score values and divergence signals, with customizable colors and line widths.

Alerts and Signals

The Cumulative Volume Delta Z Score comes with pre-configured alert conditions for:

Z-Score Crossovers: Alerts are triggered when the Z-Score crosses the 0 line, indicating a potential trend reversal.

Shifting Trend: Alerts for when the Z-Score shifts direction, signaling a change in market sentiment.

Divergence Detection: Alerts for both regular and hidden bullish and bearish divergences, offering potential reversal signals.

Extreme Imbalances: Alerts when the Z-Score reaches extreme positive or negative levels, indicating overbought or oversold market conditions.

Applications in Trading

Trend Identification: Use the Z-Score to confirm bullish or bearish trends based on cumulative volume data, filtering out noise and false signals.

Reversal Signals: Divergences between price and CVD can help identify potential trend reversals, making it a powerful tool for swing traders.

Volume-Based Confirmation: The Z-Score allows traders to confirm price movements with volume data, providing more reliable signals compared to price action alone.

Divergence Strategy: Use the divergence signals to identify potential points of entry, particularly when regular or hidden divergences appear.

Volatility and Market Sentiment: The Z-Score provides insights into market volatility by measuring the deviation of CVD from its historical mean, helping to predict price movement strength.

The Cumulative Volume Delta Z Score is a powerful tool that combines volume analysis with statistical normalization. By focusing on volume imbalances and applying Z-Score normalization, this indicator provides clear, reliable signals for trend identification and potential reversals. It is especially useful for filtering out market noise and ensuring that trades are based on significant price movements driven by substantial volume changes.

This indicator is perfect for traders looking to add volume-based analysis to their strategy, offering a more robust and accurate way to gauge market sentiment and trend strength.

Triple SuperTrend + RSI + Fib BBTriple SuperTrend + RSI + Fibonacci Bollinger Bands Strategy

📊 Overview

This advanced trading strategy combines the power of three SuperTrend indicators with RSI confirmation and Fibonacci Bollinger Bands to generate high-probability trade signals. The strategy is designed to capture strong trending moves while filtering out false signals through multi-indicator confluence.

🔧 Core Components

Three SuperTrend Indicators

The strategy uses three SuperTrend indicators with progressively longer periods and multipliers:

SuperTrend 1: 10-period ATR, 1.0 multiplier (fastest, most sensitive)

SuperTrend 2: 11-period ATR, 2.0 multiplier (medium sensitivity)

SuperTrend 3: 12-period ATR, 3.0 multiplier (slowest, most stable)

This layered approach ensures that all three timeframe perspectives align before generating a signal, significantly reducing false entries.

RSI Confirmation (7-period)

The Relative Strength Index acts as a momentum filter:

Long signals require RSI > 50 (bullish momentum)

Short signals require RSI < 50 (bearish momentum)

This prevents entries during weak or divergent price action.

Fibonacci Bollinger Bands (200, 2.618)

Uses a 200-period Simple Moving Average with 2.618 standard deviation bands (Fibonacci ratio). These bands serve dual purposes:

Visual representation of price extremes

Automatic exit trigger when price reaches overextended levels

📈 Entry Logic

LONG Entry (BUY Signal)

A LONG position is opened when ALL of the following conditions are met simultaneously:

All three SuperTrend indicators turn green (bullish)

RSI(7) is above 50

This is the first bar where all conditions align (no repainting)

SHORT Entry (SELL Signal)

A SHORT position is opened when ALL of the following conditions are met simultaneously:

All three SuperTrend indicators turn red (bearish)

RSI(7) is below 50

This is the first bar where all conditions align (no repainting)

🚪 Exit Logic

Positions are automatically closed when ANY of these conditions occur:

SuperTrend Color Change: Any one of the three SuperTrend indicators changes direction

Fibonacci BB Touch: Price reaches or exceeds the upper or lower Fibonacci Bollinger Band (2.618 standard deviations)

This dual-exit approach protects profits by:

Exiting quickly when trend momentum shifts (SuperTrend change)

Taking profits at statistical price extremes (Fib BB touch)

🎨 Visual Features

Signal Arrows

Green Up Arrow (BUY): Appears below the bar when long entry conditions are met

Red Down Arrow (SELL): Appears above the bar when short entry conditions are met

Yellow Down Arrow (EXIT): Appears above the bar when exit conditions are met

Background Coloring

Light Green Tint: All three SuperTrends are bullish (uptrend environment)

Light Red Tint: All three SuperTrends are bearish (downtrend environment)

SuperTrend Lines

Three colored lines plotted with varying opacity:

Solid line (ST1): Most responsive to price changes

Semi-transparent (ST2): Medium-term trend

Most transparent (ST3): Long-term trend structure

Dashboard

Real-time information panel showing:

Individual SuperTrend status (UP/DOWN)

Current RSI value and color-coded status

Current position (LONG/SHORT/FLAT)

Net Profit/Loss

⚙️ Customizable Parameters

SuperTrend Settings

ATR periods for each SuperTrend (default: 10, 11, 12)

Multipliers for each SuperTrend (default: 1.0, 2.0, 3.0)

RSI Settings

RSI length (default: 7)

RSI source (default: close)

Fibonacci Bollinger Bands

BB length (default: 200)

BB multiplier (default: 2.618)

Strategy Options

Enable/disable long trades

Enable/disable short trades

Initial capital

Position sizing

Commission settings

💡 Strategy Philosophy

This strategy is built on the principle of confluence trading - waiting for multiple independent indicators to align before taking a position. By requiring three SuperTrend indicators AND RSI confirmation, the strategy filters out the majority of low-probability setups.

The multi-timeframe SuperTrend approach ensures that short-term, medium-term, and longer-term trends are all in agreement, which typically occurs during strong, sustainable price moves.

The exit strategy is equally important, using both trend-following logic (SuperTrend changes) and mean-reversion logic (Fibonacci BB touches) to adapt to different market conditions.

📊 Best Use Cases

Trending Markets: Works best in markets with clear directional bias

Higher Timeframes: Designed for 15-minute to daily charts

Volatile Assets: SuperTrend indicators excel in assets with clear trends

Swing Trading: Hold times typically range from hours to days

⚠️ Important Notes

No Repainting: All signals are confirmed and will not change on historical bars

One Signal Per Setup: The strategy prevents duplicate signals on consecutive bars

Exit Protection: Always exits before potentially taking an opposite position

Visual Clarity: All three SuperTrend lines are visible simultaneously for transparency

🎯 Recommended Settings

While default parameters are optimized for general use, consider:

Crypto/Volatile Markets: May benefit from slightly higher multipliers

Forex: Default settings work well for major pairs

Stocks: Consider longer BB periods (250-300) for daily charts

Lower Timeframes: Reduce all periods proportionally for scalping

📝 Alerts

Built-in alert conditions for:

BUY signal triggered

SELL signal triggered

EXIT signal triggered

Set up notifications to never miss a trade opportunity!

Disclaimer: This strategy is for educational and informational purposes only. Past performance does not guarantee future results. Always backtest thoroughly and practice proper risk management before live trading.

Background Trend Follower by exp3rtsThe Background Trend Follower indicator visually highlights the market’s daily directional bias using subtle background colors. It calculates the price change from the daily open and shades the chart background according to the current intraday momentum.

🟢 Green background → Price is significantly above the daily open (strong bullish trend)

🔴 Red background → Price is significantly below the daily open (strong bearish trend)

🟡 Yellow background → Price is trading near the daily open (neutral or consolidating phase)

The script automatically detects each new trading day.

It records the opening price at the start of the day.

As the session progresses, it continuously measures how far the current price has moved from that open.

When the move exceeds ±50 points (custom threshold), the background color adapts to reflect the trend strength.

Perfect for traders who want a quick visual sense of intraday bias — bullish, bearish, or neutral — without cluttering the chart with extra indicators.

HTF Live View - GSK-VIZAG-AP-INDIA📘 HTF Live View — GSK-VIZAG-AP-INDIA

🧩 Overview

The HTF Live View indicator provides a real-time visual representation of higher-timeframe (HTF) candle structures — such as 15min, 30min, 1H, 4H, and Daily — all derived directly from live 1-minute data.

This allows traders to see how higher timeframe candles are forming within the current session — without switching chart timeframes.

⚙️ Core Features

📊 Live Multi-Timeframe OHLC Tracking

Continuously calculates and displays Open, High, Low, and Close values for each key timeframe (15m, 30m, 1H, 4H, and Daily) based on the ongoing session.

⏱ Session-Aware Calculation

Automatically syncs with market hours defined by user-selected start and end times. Works across multiple timezones for global compatibility.

🕹 Visual Candle Representation

Draws mini-candles on the chart for each higher timeframe to represent their current body and wick — updated live.

Green body → bullish development

Red body → bearish development

📅 Informative Table Panel

Displays a summary table showing:

Timeframe label

Period (start–end time)

Live OHLC values

Color-coded close values

🌍 Timezone Support

Fully compatible with common regions such as Asia/Kolkata, New York, London, Tokyo, and Sydney.

🔧 User Inputs

Parameter Description

Market Start Hour/Minute Define session start time (default: 09:15)

Session End Hour/Minute Define market close (default: 15:30)

Timezone Select your preferred timezone for session alignment

💡 How It Works

The indicator uses a rolling OHLC calculation function that dynamically computes candle values based on elapsed session time.

Each timeframe (15m, 30m, 1H, 4H, and Daily) is built from 1-minute data to maintain precision even during intraday updates.

Both a visual representation (candles and wicks) and a data table (numeric summary) are displayed for clarity.

🧠 Use Cases

Monitor how HTF candles are forming live without switching chart intervals.

Understand intraday structure shifts (e.g., when 1H turns from red to green).

Confirm trend alignment across multiple timeframes visually.

Combine with your volume, delta, or liquidity tools for deeper confluence.

🪶 Signature

Developed by GSK-VIZAG-AP-INDIA

© prowelltraders — Educational and analytical use only.

⚠️ Disclaimer

This indicator is for educational and informational purposes only.

It does not provide financial advice or guaranteed trading results.

Always perform your own analysis before making investment decisions.

Volume Sampled Supertrend [BackQuant]Volume Sampled Supertrend

A Supertrend that runs on a volume sampled price series instead of fixed time. New synthetic bars are only created after sufficient traded activity, which filters out low participation noise and makes the trend much easier to read and model.

Original Script Link

This indicator is built on top of my volume sampling engine. See the base implementation here:

Why Volume Sampling

Traditional charts print a bar every N minutes regardless of how active the tape is. During quiet periods you accumulate many small, low information bars that add noise and whipsaws to downstream signals.

Volume sampling replaces the clock with participation. A new synthetic bar is created only when a pre-set amount of volume accumulates (or, in Dollar Bars mode, when pricevolume reaches a dollar threshold). The result is a non-uniform time series that stretches in busy regimes and compresses in quiet regimes. This naturally:

filters dead time by skipping low volume chop;

standardizes the information content per bar, improving comparability across regimes;

stabilizes volatility estimates used inside banded indicators;

gives trend and breakout logic cleaner state transitions with fewer micro flips.

What this tool does

It builds a synthetic OHLCV stream from volume based buckets and then applies a Supertrend to that synthetic price. You are effectively running Supertrend on a participation clock rather than a wall clock.

Core Features

Sampling Engine - Choose Volume buckets or Dollar Bars . Thresholds can be dynamic from a rolling mean or median, or fixed by the user.

Synthetic Candles - Plots the volume sampled OHLC candles so you can visually compare against regular time candles.

Supertrend on Synthetic Price - ATR bands and direction are computed on the sampled series, not on time bars.

Adaptive Coloring - Candle colors can reflect side, intensity by volume, or a neutral scheme.

Research Panels - Table shows total samples, current bucket fill, threshold, bars-per-sample, and synthetic return stats.

Alerts - Long and Short triggers on Supertrend direction flips for the synthetic series.

How it works

Sampling

Pick Sampling Method = Volume or Dollar Bars.

Set the dynamic threshold via Rolling Lookback and Filter (Mean or Median), or enable Use Fixed and type a constant.

The script accumulates volume (or pricevolume) each time bar. When the bucket reaches the threshold, it finalizes one or more synthetic candles and resets accumulation.

Each synthetic candle stores its own OHLCV and is appended to the synthetic series used for all downstream logic.

Supertrend on the sampled stream

Choose Supertrend Source (Open, High, Low, Close, HLC3, HL2, OHLC4, HLCC4) derived from the synthetic candle.

Compute ATR over the synthetic series with ATR Period , then form upperBand = src + factorATR and lowerBand = src - factorATR .

Apply classic trailing band and direction rules to produce Supertrend and trend state.

Because bars only come when there is sufficient participation, band touches and flips tend to align with meaningful pushes, not idle prints.

Reading the display

Synthetic Volume Bars - The non-uniform candles that represent equal information buckets. Expect more candles during active sessions and fewer during lulls.

Volume Sampled Supertrend - The main line. Green when Trend is 1, red when Trend is -1.

Markers - Small dots appear when a new synthetic sample is created, useful for aligning activity cycles.

Time Bars Overlay (optional) - Plot regular time candles to compare how the synthetic stream compresses quiet chop.

Settings you will use most

Data Settings

Sampling Method - Volume or Dollar Bars.

Rolling Lookback and Filter - Controls the dynamic threshold. Median is robust to outliers, Mean is smoother.

Use Fixed and Fixed Threshold - Force a constant bucket size for consistent sampling across regimes.

Max Stored Samples - Ring buffer limit for performance.

Indicator Settings

SMA over last N samples - A moving average computed on the synthetic close series. Can be hidden for a cleaner layout.

Supertrend Source - Price field from the synthetic candle.

ATR Period and Factor - Standard Supertrend controls applied on the synthetic series.

Visuals and UI

Show Synthetic Bars - Turn synthetic candles on or off.

Candle Color Mode - Green/Red, Volume Intensity, Neutral, or Adaptive.

Mark new samples - Puts a dot when a bucket closes.

Show Time Bars - Overlay regular candles for comparison.

Paint candles according to Trend - Colors chart candles using current synthetic Supertrend direction.

Line Width , Colors , and Stats Table toggles.

Some workflow notes:

Trend Following

Set Sampling Method = Volume, Filter = Median, and a reasonable Rolling Lookback so busy regimes produce more samples.

Trade in the direction of the Volume Sampled Supertrend. Because flips require real participation, you tend to avoid micro whipsaws seen on time bars.

Use the synthetic SMA as a bias rail and trailing reference for partials or re-entries.

Breakout and Continuation

Watch for rapid clustering of new sample markers and a clean flip of the synthetic Supertrend.

The compression of quiet time and expansion in busy bursts often makes breakouts more legible than on uniform time charts.

Mean Reversion

In instruments that oscillate, faded moves against the synthetic Supertrend are easier to time when the bucket cadence slows and Supertrend flattens.

Combine with the synthetic SMA and return statistics in the table for sizing and expectation setting.

Stats table (top right)

Method and Total Samples - Sampling regime and current synthetic history length.

Current Vol or Dollar and Threshold - Live bucket fill versus the trigger.

Bars in Bucket and Avg Bars per Sample - How much time data each synthetic bar tends to compress.

Avg Return and Return StdDev - Simple research metrics over synthetic close-to-close changes.

Why this reduces noise

Time based bars treat a 5 minute print with 1 percent of average participation the same as one with 300 percent. Volume sampling equalizes bar information content. By advancing the bar only when sufficient activity occurs, you skip low quality intervals that add variance but little signal. For banded systems like Supertrend, this often means fewer false flips and cleaner runs.

Notes and tips

Use Dollar Bars on assets where nominal price varies widely over time or across symbols.

Median filter can resist single burst outliers when setting dynamic thresholds.

If you need a stable research baseline, set Use Fixed and keep the threshold constant across tests.

Enable Show Time Bars occasionally to sanity check what the synthetic stream is compressing or stretching.

Link again for reference

Original Volume Based Sampling engine:

Bottom line

When you let participation set the clock, your Supertrend reacts to meaningful flow instead of idle prints. The result is a cleaner state machine, fewer micro whipsaws, and a trend read that respects when the market is actually trading.

Extreme Candle Pattern Visualizer🟠 OVERVIEW

This indicator compares the current candle's percentage change against historical data, then highlights past candles with equal or bigger magnitude of movement. Also, for all the highlighted past candles, it tracks how far price extends before recovering to its starting point. It also provides statistical context through percentile rankings.

IN SHORT: Quickly spot similar price movements in the past and understand how unusual the current candle is using percentile rankings.

🟠 CORE CONCEPT

The indicator operates on two fundamental principles:

1. Statistical Rarity Detection

The script calculates the percentage change (open to close) of every candle within a user-defined lookback period and determines where the current candle ranks in this distribution. A candle closing at -9% might fall in the bottom 5th percentile, indicating it's more extreme than 95% of recent candles. This percentile ranking helps traders identify statistically unusual moves that often precede reversals or extended trends.

2. Recovery Path Mapping

Once extreme candles are identified (those matching or exceeding the current candle's magnitude), the indicator tracks their subsequent price action. For bearish candles, it measures how far price dropped before recovering back to the candle's opening price. For bullish candles, it tracks how high price climbed before returning to the open. This reveals whether extreme moves typically extend further or reverse quickly.

🟠 PRACTICAL APPLICATIONS

Mean Reversion Trading:

Candles in extreme percentiles (below 10% or above 90%) often signal oversold/overbought conditions. The recovery lines show typical extension distances, helping traders set profit targets for counter-trend entries.

Momentum Continuation:

When extreme candles show small recovery percentages before price reverses back, it suggests strong directional momentum that may continue.

Stop Loss Placement:

Historical recovery data reveals typical extension ranges after extreme moves, informing more precise stop loss positioning beyond noise but before major reversals.

Pattern Recognition:

By visualizing how similar historical extremes resolved, traders gain context for current price action rather than trading in isolation.

🟠 VISUAL ELEMENTS

Orange Circles: Mark historical candles with similar or greater magnitude to current candle

Red Lines: Track downward extensions after bearish extreme candles

Green Lines: Track upward extensions after bullish extreme candles

Percentage Labels: Show exact extension distance from candle close to extreme point

Percentile Label: Color-coded box displaying current candle's statistical ranking

Hollow Candles: Background rendering for clean chart presentation

🟠 ORIGINALITY

This indicator uniquely combines statistical percentile analysis with forward-looking recovery tracking. While many indicators identify extreme moves, few show what happened next across multiple historical instances simultaneously. The dual approach provides both the "how rare is this?" question (percentile) and "what typically happens after?" answer (recovery paths) in a single visual framework.

Michal D. Lagless Moving Average | MisinkoMasterThe 𝕸𝖎𝖈𝖍𝖆𝖑 𝕯. 𝕷𝖆𝖌𝖑𝖊𝖘𝖘 𝕸𝖔𝖛𝖎𝖓𝖌 𝕬𝖛𝖊𝖗𝖆𝖌𝖊 is my latest creation of a trend following tool, which is a bit different from the rest. By trying to de-lag the classical moving average, it gives you fast signals on changes in trend as fast as possible, keeping traders & investors always in check for potential risks they might want to avoid.

How does it work?

First we need to calculate lengths. The lengths are calcuted using a user defined input called the "Length Multiplier" and we of course need as well the length input too.

The indicator uses 10 lengths, 5 for an average price, 5 for median price.

The length for the average is the following:

length_2_avg = length_1_avg * length_multiplier

length_3_avg = length_2_avg * length_multiplier

...

and for the median lengths:

length_1_median = length_2_avg

length_2_median = length_3_avg

Here applies this rule

length_x_median < length_x_avg

This is intentional, and it is because the average is a little more reactive, while the median is a bit slower. To make up for the "slowness" of the median, we simple reduce the length of it a bit more than the average.

Now that we have our length we are ready to calculate averages and medians over their respective period. This is the a normal average from elementary school, nothing too fancy.

Now that we have all of them we match the pairs using another user defined input called "Median Weight" like so:

(Average_x * (2-median_weight) + Median_x * median_weight)/2

This gives more weight to the average (also due to the max value limit set to avoid breaking the fundational logic behind it).

After doing it to all the pairs we now average those pairs using another input called "Exponential Weight Multiplier".

The Exponential Weight Multiplier is used for weights which I will cover soon:

weight1 = weight

weight2 = weight * weight

weight3 = weight * weight * weight....

This is done until we have all the weights calculated

This gives exponentially more weight to the less lagging indicators, which is how we delag the indicator.

Then we sum all the pairs like so:

sum = pair1 * weight1 + pair2 * weight2 + pair3 * weight3 + pair4 * weight4 + pair5 * weight5

Then the sum is divided by the sum of weights, this results in us getting the final value.

Methodology & What is the actual point & how was it made?

I want to cover this one a bit deeper:

The methodology behind this was creating an indicator that would not be lagging, and would be able to avoid lag while not producing signals too often.

In many attempts in the first part, I tried using EMA, RMA, DEMA, TEMA, HMA, SMA and so on, but they were too noisy (except for SMA & RMA, but those had their flaws), so I tried the classical average taught in elementary school. This one worked better, but the noise was too high still after all this time. This made me include the median, which helped the noise, but made it far too lagging.

Here came the idea of making the median length lower and adding weights to counter the lag of the median, but it was still too lagging. This made me make the weights for lengths more exponential, while previously they were calculated using a little bit amplified sums that were alright, but nowhere near my desired result.

Using the new weights I got further, and after a bit of testing I was sattisfied with the results.

The logic for the trend was a big part in my development part, there were many I could think of, but not enough time to try them, so I stuck to the usual one, and I leave it up to YOU to beat my trend logic and get even better results.

Use Cases:

- Price/MA Crossovers

Simple, effective, useful

- Source for other indicators

This I tried myself, and it worked in a cool way, making the signals of for example RSI much smoother, so definitely try it out if you know how to code, or just simply put it in the source of the RSI.

- ROC

This trend logic stuck with me, I think you could find a way to make it good, but mainly for the people that can code in pine, trying out to combine the trend logic with ROC could work very well, do not sleep on it!

- Education

This concept is not really that complex, so for people looking for new ideas, inspiration, or just watching how trend following tools behave in general this is something that could benefit anyone, as the concept can be applied to ANYTHING, even the classical RSI, MACD, you could try even the Parabolic SAR, maybe STC or VZO, there is no limit to imagination.

- Strategy creation

Filtering this indicator with "and" conditions, or maybe even "or" or anything really could be very useful in a strategy that desires fast signals.

- Price Distance from bands

I noticed this while looking at past performance:

The stronger the trend the higher the distance from the Moving Average.

Final Notes

Watch out for mean reverting markets, as this is trend following you could get easily screwed in them.

Play around with this if it fits your desired outcome, you might find something I did not.

Hope you find it useful,

See you next time!

Stochastic %K Colored by VolumeDescription:

"Stochastic %K Colored by Volume is a technical indicator that combines the traditional Stochastic %K oscillator with volume-based coloring. It highlights periods of high, low, and neutral trading volume by changing the color of the %K line. Additionally, it identifies bullish and bearish divergences between price and the %K oscillator, helping traders spot potential reversals and trend changes. The indicator also includes key levels for overbought, oversold, and extreme zones to guide trading decisions."

Opening Range Fibonacci Extensions (ATR Adjusted)this script displays daily, weekly, or monthly range extensions as a function of ATR in a Fibonacci retracement

SJA WINFUT B3-10

INDICATOR FOR WINFUT B3 – 5-minute chart.

This indicator was designed to trade the Bovespa index futures contract (WINFUT) on the 5-minute chart.

It integrates technical analysis and macroeconomic context elements.

It combines several indicators in which the system calculates a score weighted by color and intensity for each indicator, generating a metric called “STRENGTH %,” which reflects the dominance of buyers (green), sellers (red), or sideways movement (orange) at the moment.

The calculation is adapted to market hours:

Between 9:00 a.m. and 9:59 a.m., it considers only the available indicators; after 10:00 a.m., it uses all data.

The panel displays real-time information, including divergences between strength and price, providing robust decision support for short-term operations on the mini index.

Buying trend.

The more green indicators (at the top of the panel) and dark blue indicators (at the bottom of the panel) and the higher the strength percentage, the greater the probability of buying.

Selling trend.

The more red indicators (at the top of the panel) and dark blue indicators (at the bottom of the panel) and the higher the strength percentage, the greater the probability of selling.

Translated with DeepL.com (free version)

JK_Traders_Reality_LibLibrary "JK_Traders_Reality_Lib"

This library contains common elements used in Traders Reality scripts

calcPvsra(pvsraVolume, pvsraHigh, pvsraLow, pvsraClose, pvsraOpen, redVectorColor, greenVectorColor, violetVectorColor, blueVectorColor, darkGreyCandleColor, lightGrayCandleColor)

calculate the pvsra candle color and return the color as well as an alert if a vector candle has apperared.

Situation "Climax"

Bars with volume >= 200% of the average volume of the 10 previous chart TFs, or bars

where the product of candle spread x candle volume is >= the highest for the 10 previous

chart time TFs.

Default Colors: Bull bars are green and bear bars are red.

Situation "Volume Rising Above Average"

Bars with volume >= 150% of the average volume of the 10 previous chart TFs.

Default Colors: Bull bars are blue and bear are violet.

Parameters:

pvsraVolume (float) : the instrument volume series (obtained from request.sequrity)

pvsraHigh (float) : the instrument high series (obtained from request.sequrity)

pvsraLow (float) : the instrument low series (obtained from request.sequrity)

pvsraClose (float) : the instrument close series (obtained from request.sequrity)

pvsraOpen (float) : the instrument open series (obtained from request.sequrity)

redVectorColor (simple color) : red vector candle color

greenVectorColor (simple color) : green vector candle color

violetVectorColor (simple color) : violet/pink vector candle color

blueVectorColor (simple color) : blue vector candle color

darkGreyCandleColor (simple color) : regular volume candle down candle color - not a vector

lightGrayCandleColor (simple color) : regular volume candle up candle color - not a vector

@return

adr(length, barsBack)

Parameters:

length (simple int) : how many elements of the series to calculate on

barsBack (simple int) : starting possition for the length calculation - current bar or some other value eg last bar

@return adr the adr for the specified lenght

adrHigh(adr, fromDo)

Calculate the ADR high given an ADR

Parameters:

adr (float) : the adr

fromDo (simple bool) : boolean flag, if false calculate traditional adr from high low of today, if true calcualte from exchange midnight

@return adrHigh the position of the adr high in price

adrLow(adr, fromDo)

Parameters:

adr (float) : the adr

fromDo (simple bool) : boolean flag, if false calculate traditional adr from high low of today, if true calcualte from exchange midnight

@return adrLow the position of the adr low in price

splitSessionString(sessXTime)

given a session in the format 0000-0100:23456 split out the hours and minutes

Parameters:

sessXTime (simple string) : the session time string usually in the format 0000-0100:23456

@return

calcSessionStartEnd(sessXTime, gmt)

calculate the start and end timestamps of the session

Parameters:

sessXTime (simple string) : the session time string usually in the format 0000-0100:23456

gmt (simple string) : the gmt offset string usually in the format GMT+1 or GMT+2 etc

@return

drawOpenRange(sessXTime, sessXcol, showOrX, gmt)

draw open range for a session

Parameters:

sessXTime (simple string) : session string in the format 0000-0100:23456

sessXcol (simple color) : the color to be used for the opening range box shading

showOrX (simple bool) : boolean flag to toggle displaying the opening range

gmt (simple string) : the gmt offset string usually in the format GMT+1 or GMT+2 etc

@return void

drawSessionHiLo(sessXTime, showRectangleX, showLabelX, sessXcolLabel, sessXLabel, gmt, sessionLineStyle)

Parameters:

sessXTime (simple string) : session string in the format 0000-0100:23456

showRectangleX (simple bool)

showLabelX (simple bool)

sessXcolLabel (simple color) : the color to be used for the hi/low lines and label

sessXLabel (simple string) : the session label text

gmt (simple string) : the gmt offset string usually in the format GMT+1 or GMT+2 etc

sessionLineStyle (simple string) : the line stile for the session high low lines

@return void

calcDst()

calculate market session dst on/off flags

@return indicating if DST is on or off for a particular region

timestampPreviousDayOfWeek(previousDayOfWeek, hourOfDay, gmtOffset, oneWeekMillis)

Timestamp any of the 6 previous days in the week (such as last Wednesday at 21 hours GMT)

Parameters:

previousDayOfWeek (simple string) : Monday or Satruday

hourOfDay (simple int) : the hour of the day when psy calc is to start

gmtOffset (simple string) : the gmt offset string usually in the format GMT+1 or GMT+2 etc

oneWeekMillis (simple int) : the amount if time for a week in milliseconds

@return the timestamp of the psy level calculation start time

getdayOpen()

get the daily open - basically exchange midnight

@return the daily open value which is float price

newBar(res)

new_bar: check if we're on a new bar within the session in a given resolution

Parameters:

res (simple string) : the desired resolution

@return true/false is a new bar for the session has started

toPips(val)

to_pips Convert value to pips

Parameters:

val (float) : the value to convert to pips

@return the value in pips

rLabel(ry, rtext, rstyle, rcolor, valid, labelXOffset)

a function that draws a right aligned lable for a series during the current bar

Parameters:

ry (float) : series float the y coordinate of the lable

rtext (simple string) : the text of the label

rstyle (simple string) : the style for the lable

rcolor (simple color) : the color for the label

valid (simple bool) : a boolean flag that allows for turning on or off a lable

labelXOffset (int) : how much to offset the label from the current position

rLabelOffset(ry, rtext, rstyle, rcolor, valid, labelOffset)

a function that draws a right aligned lable for a series during the current bar

Parameters:

ry (float) : series float the y coordinate of the lable

rtext (string) : the text of the label

rstyle (simple string) : the style for the lable

rcolor (simple color) : the color for the label

valid (simple bool) : a boolean flag that allows for turning on or off a lable

labelOffset (int)

rLabelLastBar(ry, rtext, rstyle, rcolor, valid, labelXOffset)

a function that draws a right aligned lable for a series only on the last bar

Parameters:

ry (float) : series float the y coordinate of the lable

rtext (string) : the text of the label

rstyle (simple string) : the style for the lable

rcolor (simple color) : the color for the label

valid (simple bool) : a boolean flag that allows for turning on or off a lable

labelXOffset (int) : how much to offset the label from the current position

drawLine(xSeries, res, tag, xColor, xStyle, xWidth, xExtend, isLabelValid, xLabelOffset, validTimeFrame)

a function that draws a line and a label for a series

Parameters:

xSeries (float) : series float the y coordinate of the line/label

res (simple string) : the desired resolution controlling when a new line will start

tag (simple string) : the text for the lable

xColor (simple color) : the color for the label

xStyle (simple string) : the style for the line

xWidth (simple int) : the width of the line

xExtend (simple string) : extend the line

isLabelValid (simple bool) : a boolean flag that allows for turning on or off a label

xLabelOffset (int)

validTimeFrame (simple bool) : a boolean flag that allows for turning on or off a line drawn

drawLineDO(xSeries, res, tag, xColor, xStyle, xWidth, xExtend, isLabelValid, xLabelOffset, validTimeFrame)

a function that draws a line and a label for the daily open series

Parameters:

xSeries (float) : series float the y coordinate of the line/label

res (simple string) : the desired resolution controlling when a new line will start

tag (simple string) : the text for the lable

xColor (simple color) : the color for the label

xStyle (simple string) : the style for the line

xWidth (simple int) : the width of the line

xExtend (simple string) : extend the line

isLabelValid (simple bool) : a boolean flag that allows for turning on or off a label

xLabelOffset (int)

validTimeFrame (simple bool) : a boolean flag that allows for turning on or off a line drawn

drawPivot(pivotLevel, res, tag, pivotColor, pivotLabelColor, pivotStyle, pivotWidth, pivotExtend, isLabelValid, validTimeFrame, levelStart, pivotLabelXOffset)

draw a pivot line - the line starts one day into the past

Parameters:

pivotLevel (float) : series of the pivot point

res (simple string) : the desired resolution

tag (simple string) : the text to appear

pivotColor (simple color) : the color of the line

pivotLabelColor (simple color) : the color of the label

pivotStyle (simple string) : the line style

pivotWidth (simple int) : the line width

pivotExtend (simple string) : extend the line

isLabelValid (simple bool) : boolean param allows to turn label on and off

validTimeFrame (simple bool) : only draw the line and label at a valid timeframe

levelStart (int) : basically when to start drawing the levels

pivotLabelXOffset (int) : how much to offset the label from its current postion

@return the pivot line series

getPvsraFlagByColor(pvsraColor, redVectorColor, greenVectorColor, violetVectorColor, blueVectorColor, lightGrayCandleColor)

convert the pvsra color to an internal code

Parameters:

pvsraColor (color) : the calculated pvsra color

redVectorColor (simple color) : the user defined red vector color

greenVectorColor (simple color) : the user defined green vector color

violetVectorColor (simple color) : the user defined violet vector color

blueVectorColor (simple color) : the user defined blue vector color

lightGrayCandleColor (simple color) : the user defined regular up candle color

@return pvsra internal code

updateZones(pvsra, direction, boxArr, maxlevels, pvsraHigh, pvsraLow, pvsraOpen, pvsraClose, transperancy, zoneupdatetype, zonecolor, zonetype, borderwidth, coloroverride, redVectorColor, greenVectorColor, violetVectorColor, blueVectorColor)

a function that draws the unrecovered vector candle zones

Parameters:

pvsra (int) : internal code

direction (simple int) : above or below the current pa

boxArr (array) : the array containing the boxes that need to be updated

maxlevels (simple int) : the maximum number of boxes to draw

pvsraHigh (float) : the pvsra high value series

pvsraLow (float) : the pvsra low value series

pvsraOpen (float) : the pvsra open value series

pvsraClose (float) : the pvsra close value series

transperancy (simple int) : the transparencfy of the vecor candle zones

zoneupdatetype (simple string) : the zone update type

zonecolor (simple color) : the zone color if overriden

zonetype (simple string) : the zone type

borderwidth (simple int) : the width of the border

coloroverride (simple bool) : if the color overriden

redVectorColor (simple color) : the user defined red vector color

greenVectorColor (simple color) : the user defined green vector color

violetVectorColor (simple color) : the user defined violet vector color

blueVectorColor (simple color) : the user defined blue vector color

cleanarr(arr)

clean an array from na values

Parameters:

arr (array) : the array to clean

@return if the array was cleaned

calcPsyLevels(oneWeekMillis, showPsylevels, psyType, sydDST)

calculate the psy levels

4 hour res based on how mt4 does it

mt4 code

int Li_4 = iBarShift(NULL, PERIOD_H4, iTime(NULL, PERIOD_W1, Li_0)) - 2 - Offset;

ObjectCreate("PsychHi", OBJ_TREND, 0, Time , iHigh(NULL, PERIOD_H4, iHighest(NULL, PERIOD_H4, MODE_HIGH, 2, Li_4)), iTime(NULL, PERIOD_W1, 0), iHigh(NULL, PERIOD_H4,

iHighest(NULL, PERIOD_H4, MODE_HIGH, 2, Li_4)));

so basically because the session is 8 hours and we are looking at a 4 hour resolution we only need to take the highest high an lowest low of 2 bars

we use the gmt offset to adjust the 0000-0800 session to Sydney open which is at 2100 during dst and at 2200 otherwize. (dst - spring foward, fall back)

keep in mind sydney is in the souther hemisphere so dst is oposite of when london and new york go into dst

Parameters:

oneWeekMillis (simple int) : a constant value

showPsylevels (simple bool) : should psy levels be calculated

psyType (simple string) : the type of Psylevels - crypto or forex

sydDST (bool) : is Sydney in DST

@return

adrHiLo(length, barsBack, fromDO)

Parameters:

length (simple int) : how many elements of the series to calculate on

barsBack (simple int) : starting possition for the length calculation - current bar or some other value eg last bar

fromDO (simple bool) : boolean flag, if false calculate traditional adr from high low of today, if true calcualte from exchange midnight

@return adr, adrLow and adrHigh - the adr, the position of the adr High and adr Low with respect to price

drawSessionHiloLite(sessXTime, showRectangleX, showLabelX, sessXcolLabel, sessXLabel, gmt, sessionLineStyle, sessXcol)

Parameters:

sessXTime (simple string) : session string in the format 0000-0100:23456

showRectangleX (simple bool)

showLabelX (simple bool)

sessXcolLabel (simple color) : the color to be used for the hi/low lines and label

sessXLabel (simple string) : the session label text

gmt (simple string) : the gmt offset string usually in the format GMT+1 or GMT+2 etc

sessionLineStyle (simple string) : the line stile for the session high low lines

sessXcol (simple color) : - the color for the box color that will color the session

@return void

msToHmsString(ms)

converts milliseconds into an hh:mm string. For example, 61000 ms to '0:01:01'

Parameters:

ms (int) : - the milliseconds to convert to hh:mm

@return string - the converted hh:mm string

countdownString(openToday, closeToday, showMarketsWeekends, oneDay)

that calculates how much time is left until the next session taking the session start and end times into account. Note this function does not work on intraday sessions.

Parameters:

openToday (int) : - timestamps of when the session opens in general - note its a series because the timestamp was created using the dst flag which is a series itself thus producing a timestamp series

closeToday (int) : - timestamp of when the session closes in general - note its a series because the timestamp was created using the dst flag which is a series itself thus producing a timestamp series

@return a countdown of when next the session opens or 'Open' if the session is open now

showMarketsWeekends (simple bool)

oneDay (simple int)

countdownStringSyd(sydOpenToday, sydCloseToday, showMarketsWeekends, oneDay)

that calculates how much time is left until the next session taking the session start and end times into account. special case of intraday sessions like sydney

Parameters:

sydOpenToday (int)

sydCloseToday (int)

showMarketsWeekends (simple bool)

oneDay (simple int)

Swing Data - SimplifiedThe swing data indicator by jfsrev but simplified. Thank you jfsrev for your work!

Aladin Pair Trading System v1Aladin Pair Trading System v1

What is This Indicator?

The Aladin Pair Trading System is a sophisticated tool designed to help traders identify profitable opportunities by comparing two related stocks that historically move together. Think of it as finding when one twin is running ahead or lagging behind the other - these moments often present trading opportunities as they tend to return to moving together.

Who Should Use This?

Beginners: Learn about statistical arbitrage and pair trading

Intermediate Traders: Execute mean-reversion strategies with confidence

Advanced Traders: Fine-tune parameters for optimal pair relationships

Portfolio Managers: Implement market-neutral strategies

💡 What is Pair Trading?

Imagine two ice cream shops next to each other. They usually have similar customer traffic because they're in the same area. If one day Shop A is packed while Shop B is empty, you might expect this imbalance to correct itself soon.

Pair trading works the same way:

You find two stocks that normally move together (like TCS and Infosys)

When one stock moves too far from the other, you trade expecting them to realign

You buy the lagging stock and sell the leading stock

When they come back together, you profit from both sides

Key Features

1. Z-Score Analysis

What it is: A statistical measure showing how far the price relationship has deviated from normal

What it means:

Z-Score near 0 = Normal relationship

Z-Score at +2 = Stock A is expensive relative to Stock B (Sell A, Buy B)

Z-Score at -2 = Stock A is cheap relative to Stock B (Buy A, Sell B)

2. Multiple Timeframe Analysis

Long-term Z-Score (300 bars): Shows the big picture trend

Short-term Z-Score (100 bars): Shows recent movements

Signal Z-Score (20 bars): Generates quick trading signals

3. Statistical Validation

The indicator checks if the pair is suitable for trading:

Correlation (must be > 0.7): Confirms the stocks move together

1.0 = Perfect positive correlation

0.7 = Strong correlation

Below 0.7 = Warning: pair may not be reliable

ADF P-Value (should be < 0.05): Tests if the relationship is stable

Low value = Good for pair trading

High value = Relationship may be random

Cointegration: Confirms long-term equilibrium relationship

YES = Pair tends to revert to mean

NO = Pair may drift apart permanently

Visual Elements Explained

Chart Zones (Color-Coded Areas)

Yellow Zone (-1.5 to +1.5)

Normal Zone: Relationship is stable

Action: Wait for better opportunities

Blue Zone (±1.5 to ±2.0)

Entry Zone: Deviation is significant

Action: Prepare for potential trades

Green/Red Zone (±2.0 to ±3.0)

Opportunity Zone: Strong deviation

Action: High-probability trade setups

Beyond ±3.0

Risk Limit: Extreme deviation

Action: Either maximum opportunity or structural break

Signal Arrows

Green Arrow Up (Buy A + Sell B):

Stock A is undervalued relative to B

Buy Stock A, Short Stock B

Red Arrow Down (Sell A + Buy B):

Stock A is overvalued relative to B

Sell Stock A, Buy Stock B

Settings Guide

Symbol Inputs

Pair Symbol (Symbol B): Choose the second stock to compare

Default: NSE:INFY (Infosys)

Example pairs: TCS/INFY, HDFCBANK/ICICIBANK, RELIANCE/ONGC

Z-Score Parameters

Long Z-Score Period (300): Historical context

Short Z-Score Period (100): Recent trend

Signal Period (20): Trading signals

Z-Score Threshold (2.0): Entry trigger level

Higher = Fewer but stronger signals

Lower = More frequent signals

Statistical Parameters

Correlation Period (240): How many bars to check correlation

Hurst Exponent Period (50): Measures mean-reversion tendency

Probability Lookback (100): Historical probability calculations

Trading Parameters

Entry Threshold (0.0): Minimum Z-score for entry

Risk Threshold (1.5): Warning level

Risk Limit (3.0): Maximum deviation to trade

How to Use (Step-by-Step)

Step 1: Choose Your Pair

Add the indicator to your chart (this becomes Stock A)

In settings, select Stock B (the comparison stock)

Choose stocks from the same sector for best results

Step 2: Verify Pair Quality

Check the Statistics Table (top-right corner):

✅ Correlation > 0.70 (Green = Good)

✅ ADF P-value < 0.05 (Green = Good)

✅ Cointegrated = YES (Green = Good)

If all three are green, the pair is suitable for trading!

Step 3: Wait for Signals

BUY SIGNAL (Green Arrow Up)

Z-Score crosses above -2.0

Action: Buy Stock A, Sell Stock B

Exit: When Z-Score returns to 0

SELL SIGNAL (Red Arrow Down)

Z-Score crosses below +2.0

Action: Sell Stock A, Buy Stock B

Exit: When Z-Score returns to 0

Step 4: Risk Management

Yellow Zone: Monitor only

Blue Zone: Prepare for entry

Green/Red Zone: Active trading zone

Beyond ±3.0: Maximum risk - use caution

⚠️ Important Warnings

Not All Pairs Work: Always check the statistics table first

Market Conditions Matter: Correlation can break during market stress

Use Stop Losses: Set stops at Z-Score ±3.5 or beyond

Position Sizing: Trade both legs with appropriate hedge ratios

Transaction Costs: Factor in brokerage and slippage for both stocks

Example Trade

Scenario: TCS vs INFOSYS

Correlation: 0.85 ✅

Z-Score: -2.3 (TCS is cheap vs INFY)

Action to be taken:

Buy 1lot of TCS Future

Sell 1lot of INFOSYS Future

Expected Outcome:

As Z-Score moves toward 0, TCS outperforms INFOSYS

Close both positions when Z-Score crosses 0

Profit from the convergence

Best Practices

Test Before Trading: Use paper trading first

Sector Focus: Choose pairs from the same industry

Monitor Statistics: Check correlation daily

Avoid News Events: Don't trade pairs during earnings/major news

Size Appropriately: Start small, scale with experience

Be Patient: Wait for high-quality setups (±2.0 or beyond)

What Makes This Indicator Unique?

Multi-timeframe Z-Score analysis: Three different perspectives

Statistical validation: Built-in correlation and cointegration tests

Visual risk zones: Easy-to-understand color-coded areas

Real-time statistics: Live pair quality monitoring

Beginner-friendly: Clear signals with educational zones

Technical Background

The indicator uses:

Engle-Granger Cointegration Test: Validates pair relationship

ADF (Augmented Dickey-Fuller) Test: Tests stationarity

Pearson Correlation: Measures linear relationship

Z-Score Normalization: Standardizes deviations

Log Returns: Handles price differences properly

Support & Community

For questions, suggestions, or to share your pair trading experiences:

Comment below the indicator

Share your successful pair combinations

Report any issues for quick fixes

Disclaimer

This indicator is for educational and informational purposes only. It does not constitute financial advice. Pair trading involves risk, including the risk of loss.

Always:

Do your own research

Understand the risks

Trade with money you can afford to lose

Consider consulting a financial advisor

📌 Quick Reference Card

Z-ScoreInterpretationAction-3.0 to -2.0A very cheap vs BStrong Buy A, Sell B-2.0 to -1.5A cheap vs BBuy A, Sell B-1.5 to +1.5Normal rangeHold/Wait+1.5 to +2.0A expensive vs BSell A, Buy B+2.0 to +3.0A very expensive vs BStrong Sell A, Buy B

Good Pair Statistics:

Correlation: > 0.70

ADF P-value: < 0.05

Cointegration: YES

Version: 1.0

Last Updated: 10th October 2025

Compatible: TradingView Pine Script v6

Happy Trading!

Date Marker📅 Date Marker

Date Marker is a simple, lightweight indicator that draws a single vertical line on a chosen date — ideal for quickly comparing how different charts looked at the same point in time.

Switch between symbols or timeframes, and the line automatically stays fixed at your selected date.

Perfect for studying market reactions to key events, earnings, announcements, or macro shifts.

Multi Brownian Forecast📊 Multi Brownian Forecast (Time-Adaptive, Probabilistic)

This indicator uses a sophisticated Geometric Brownian Motion (GBM) Monte Carlo simulation to project future price paths. It adapts to any chart timeframe and provides quantitative, multi-period probability signals.

---

🧠 Core Mathematical Methodology

The model relies on GBM, which is a continuous-time stochastic process that models asset prices.

1. Historical Analysis (Drift & Volatility):

* The script first calculates Logarithmic Returns over a user-defined Historical Lookback (Hours) .

* Drift ($\mu$): Computed as the average of the log returns.

* Volatility ($\sigma$): Computed as the standard deviation of the log returns.

* These values are then time-adapted to an hourly step, compensating for the chart's current timeframe (e.g., 5-minute, 1-hour).

2. Monte Carlo Simulation:

* It runs a specified Number of Simulations (e.g., 1000).

* For each simulation, the price is stepped forward hourly using the GBM formula, which incorporates the calculated drift and a random shock drawn from a normal distribution (generated via the Box-Muller transform ).

---

✨ Key Features

Probabilistic Quartile Forecast: Plots a dynamic "cone" of probability on the chart. It shows key price percentiles (Q1, Q2/Median, Q3, and Q4/Outer Bound) at the forecast's expiration, visualizing the expected range of price outcomes based on the simulations.

Multi-Period Probability Signals: This is the core signal feature. Users can define multiple, independent forecast periods (e.g., 4h, 16h, 48h) in a comma-separated list.

* For each period, a Probability Up and Probability Down is calculated based on hitting a custom Target Price Change (%) (e.g., 2%) at a certain confidence level given a simulation over the historical backlook.

* The probabilities are displayed in a chart table. The cell text turns white if the calculated probability exceeds the user-defined Signal Confidence (%) .

Conditional Fibonacci Retracement: Optionally displays a Fibonacci Retracement on the chart. This feature is only activated when one of the multi-period signals reaches its minimum confidence threshold, providing a contextual technical level when a probabilistic edge is found.