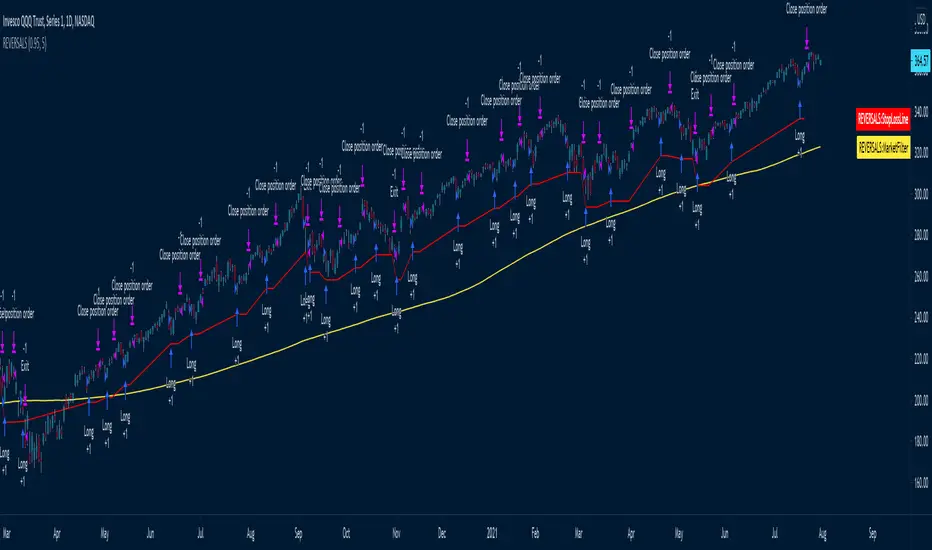

8 Whittle DownThe system is designed to short on directionally negative instruments like VXX & SQQQ

The system only shorts, no longs

It enters a pilot position if the system has no trades open at the time is in the late afternoon

It uses a 200-day moving average as a filter and will only short if the price is below the 200 day moving average

The pilot position will only enter with 1/3 ( one third ) of the total expected position size

StopLossPerc sets the stop loss, (1.15) means it is set to a 15% stop loss. -- The Red Line

The system will buy additional shares for a full position if the pilot piston profit target was not reached

The full shares position is set to purchase at a higher price. T2EntTrgPerc sets the buy percentage target for the additional shares. -- The Yellow Line

Each entry has different settable profit targets. T1ProfTrgPerc sets the profit target for the first trade (0.95) is basically set to a 5% profit.

T2ProfTrgPerc sets the profit target for the second trade (0.90) is basically set to a 10% profit. -- The White Line

RED LINE == STOP LOSS LINE

GREENLINE == PROFIT TARGET FOR THE 1ST TRADE

YELLOW LINE == ADD ON SHARES TO THE TRADE

WHITE LINE == PROFIT TARGET FOR THE 1st & 2nd TRADE COMBINED

Let me know if you have any questions and I'll try to clarify

Pine Script® ストラテジー