OPEN-SOURCE SCRIPT

更新済 MY_CME Open Interest

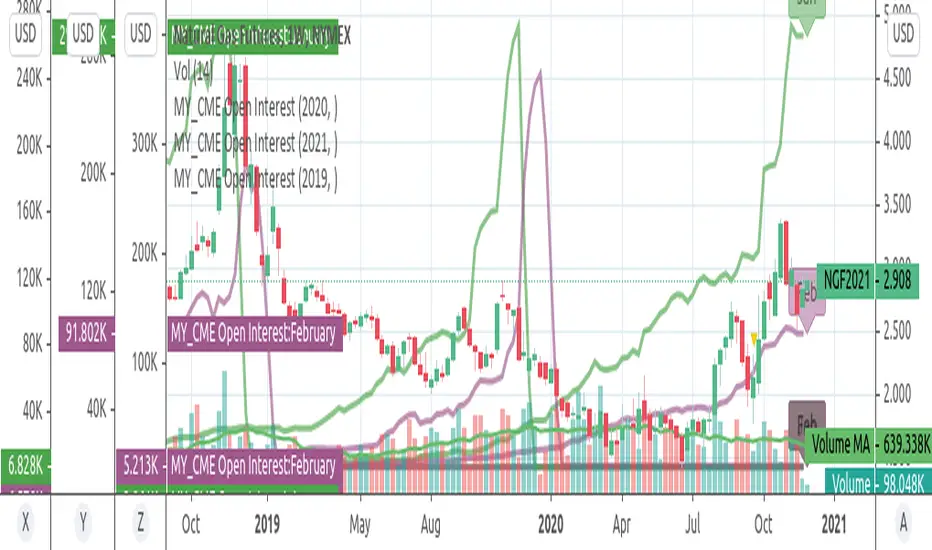

end-of-day Open Interest as provided by CME for D interval.

Can select Commodity (Gold.Silver,Crude), year, contract (Feb,April,June,AugOct,Dec)

Can select Commodity (Gold.Silver,Crude), year, contract (Feb,April,June,AugOct,Dec)

リリースノート

Now uses QUANDL/CHRIS/CME_GCn continuous datasetActual dataset is #2 (eg SI2 silver), previous contract is #1 (eg SI1)

Automatically selects actual future from chart ticket,

can be overriden with a different commodity contract, eg.: GC3

リリースノート

Plot e-o-d CME Open Interest + CFTC weekly COT Open Interest (optional) for contracts (Feb/Jun/Aug/Oct/Dec) years (2016/17/18/19) Gold/Silver/WTIリリースノート

Select the year via config. Select the contracts months via config

Scripts tries to take ticker as base. Overridable via config, eg "GC" or "ES" or"CL"or "EC" etc

Dunno where to get all these codes thou, there's some mess out there

Database used is the CHRIS continuous by quandl, exported to tradingview:

quandl.com/data/CHRIS-Wiki-Continuous-Futures

(use previous link to search datasets and codes)

Load indicator multiple times to compare contracts over multiple years

Added codess for all 12 months contracts

CFTC total OI can also be plotted

リリースノート

fixed needed confirmation for Year&Prod on startupリリースノート

better chart attached+fixed def val for Year

リリースノート

CFTC Open Interest fixed, now for Fut+Optリリースノート

added more future years till 2023, source is there anywayThese are my five public views I use for trading:

オープンソーススクリプト

TradingViewの精神に則り、このスクリプトの作者はコードをオープンソースとして公開してくれました。トレーダーが内容を確認・検証できるようにという配慮です。作者に拍手を送りましょう!無料で利用できますが、コードの再公開はハウスルールに従う必要があります。

免責事項

この情報および投稿は、TradingViewが提供または推奨する金融、投資、トレード、その他のアドバイスや推奨を意図するものではなく、それらを構成するものでもありません。詳細は利用規約をご覧ください。

オープンソーススクリプト

TradingViewの精神に則り、このスクリプトの作者はコードをオープンソースとして公開してくれました。トレーダーが内容を確認・検証できるようにという配慮です。作者に拍手を送りましょう!無料で利用できますが、コードの再公開はハウスルールに従う必要があります。

免責事項

この情報および投稿は、TradingViewが提供または推奨する金融、投資、トレード、その他のアドバイスや推奨を意図するものではなく、それらを構成するものでもありません。詳細は利用規約をご覧ください。