OPEN-SOURCE SCRIPT

更新済 Fractal Regression Bands [DW]

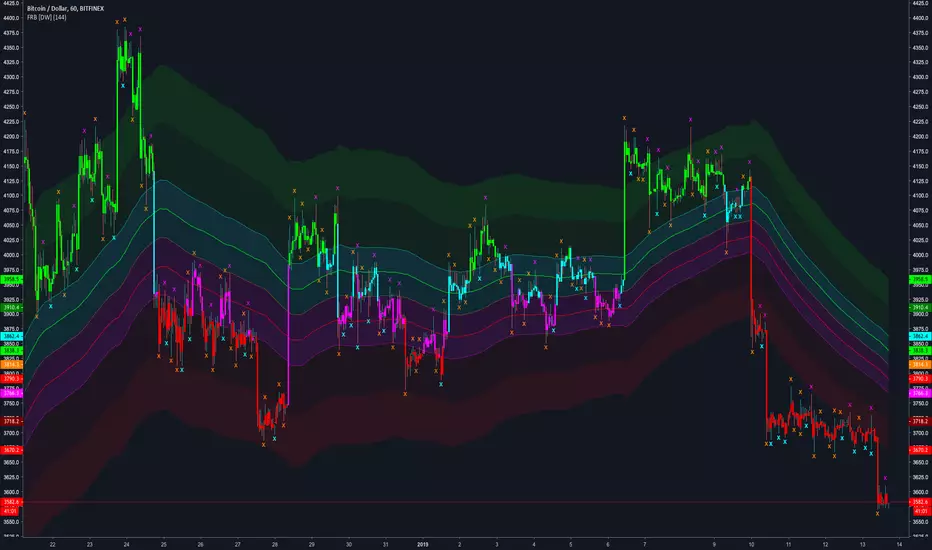

This study is an experimental regression curve built around fractal and ATR calculations.

First, Williams Fractals are calculated, and used as anchoring points.

Next, high anchor points are connected to negative sloping lines, and low anchor points to positive sloping lines. The slope is a specified percentage of the current ATR over the sampling period.

The median between the positive and negative sloping lines is then calculated, then the best fit line (linear regression) of the median is calculated to generate the basis line.

Lastly, a Golden Mean ATR is taken of price over the sampling period and multiplied by 1/2, 1, 2, and 3. The results are added and subtracted from the basis line to generate the bands.

Williams Fractals are included in the plots. The color scheme indicated whether each fractal is engulfing or non-engulfing.

Custom bar color scheme is included.

First, Williams Fractals are calculated, and used as anchoring points.

Next, high anchor points are connected to negative sloping lines, and low anchor points to positive sloping lines. The slope is a specified percentage of the current ATR over the sampling period.

The median between the positive and negative sloping lines is then calculated, then the best fit line (linear regression) of the median is calculated to generate the basis line.

Lastly, a Golden Mean ATR is taken of price over the sampling period and multiplied by 1/2, 1, 2, and 3. The results are added and subtracted from the basis line to generate the bands.

Williams Fractals are included in the plots. The color scheme indicated whether each fractal is engulfing or non-engulfing.

Custom bar color scheme is included.

リリースノート

Updates:Due to inefficiencies and its arbitrary nature, the slope factor calculation has been removed from the script.

Due to the linear regression's significant amount of overshoot, especially at greater sampling lengths, the basis line is now calculated using exponential smoothing, which fits the price series much better with minimal overshoot.

Changed the size of the fractal signals.

オープンソーススクリプト

TradingViewの精神に則り、このスクリプトの作者はコードをオープンソースとして公開してくれました。トレーダーが内容を確認・検証できるようにという配慮です。作者に拍手を送りましょう!無料で利用できますが、コードの再公開はハウスルールに従う必要があります。

For my full list of premium tools, check the blog:

wallanalytics.com/

Reach out on Telegram:

t.me/DonovanWall

wallanalytics.com/

Reach out on Telegram:

t.me/DonovanWall

免責事項

この情報および投稿は、TradingViewが提供または推奨する金融、投資、トレード、その他のアドバイスや推奨を意図するものではなく、それらを構成するものでもありません。詳細は利用規約をご覧ください。

オープンソーススクリプト

TradingViewの精神に則り、このスクリプトの作者はコードをオープンソースとして公開してくれました。トレーダーが内容を確認・検証できるようにという配慮です。作者に拍手を送りましょう!無料で利用できますが、コードの再公開はハウスルールに従う必要があります。

For my full list of premium tools, check the blog:

wallanalytics.com/

Reach out on Telegram:

t.me/DonovanWall

wallanalytics.com/

Reach out on Telegram:

t.me/DonovanWall

免責事項

この情報および投稿は、TradingViewが提供または推奨する金融、投資、トレード、その他のアドバイスや推奨を意図するものではなく、それらを構成するものでもありません。詳細は利用規約をご覧ください。