OPEN-SOURCE SCRIPT

更新済 Volatility Adjusted EMA - by Crunchster

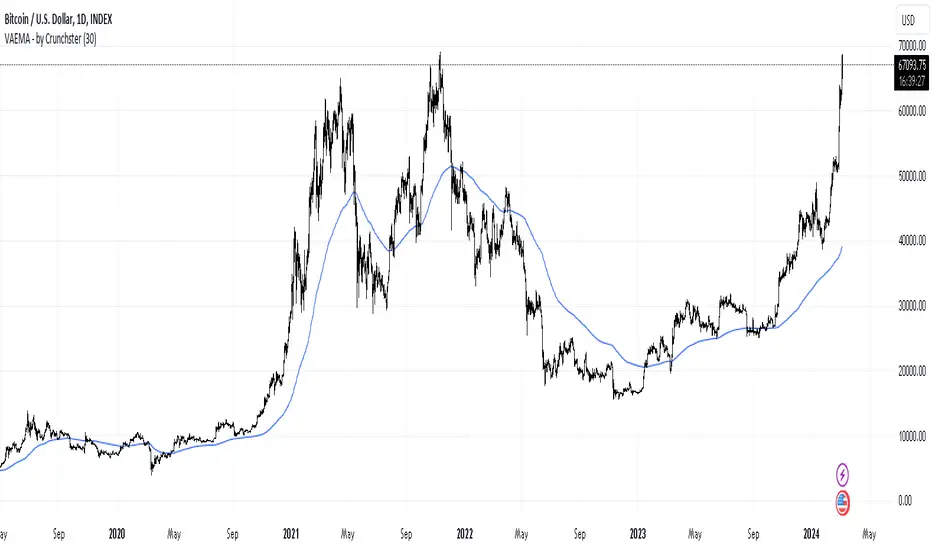

Applies recent volatility adjustment to the exponential moving average, where the smoothing factor is 2/(N + 1) - N being the lookback period or span

Volatility of recent 30 days returns is calculated using standard deviation with a thirty day lookback.

Increased smoothing compared to a standard EMA, which also adjusts to market conditions, as first described by Chande in 1991.

Volatility of recent 30 days returns is calculated using standard deviation with a thirty day lookback.

Increased smoothing compared to a standard EMA, which also adjusts to market conditions, as first described by Chande in 1991.

リリースノート

Minor code updateオープンソーススクリプト

TradingViewの精神に則り、このスクリプトの作者はコードをオープンソースとして公開してくれました。トレーダーが内容を確認・検証できるようにという配慮です。作者に拍手を送りましょう!無料で利用できますが、コードの再公開はハウスルールに従う必要があります。

Join me on Mizar.com and trade my strategies

免責事項

この情報および投稿は、TradingViewが提供または推奨する金融、投資、トレード、その他のアドバイスや推奨を意図するものではなく、それらを構成するものでもありません。詳細は利用規約をご覧ください。

オープンソーススクリプト

TradingViewの精神に則り、このスクリプトの作者はコードをオープンソースとして公開してくれました。トレーダーが内容を確認・検証できるようにという配慮です。作者に拍手を送りましょう!無料で利用できますが、コードの再公開はハウスルールに従う必要があります。

Join me on Mizar.com and trade my strategies

免責事項

この情報および投稿は、TradingViewが提供または推奨する金融、投資、トレード、その他のアドバイスや推奨を意図するものではなく、それらを構成するものでもありません。詳細は利用規約をご覧ください。