OPEN-SOURCE SCRIPT

更新済 VWAP Market Session Anchored

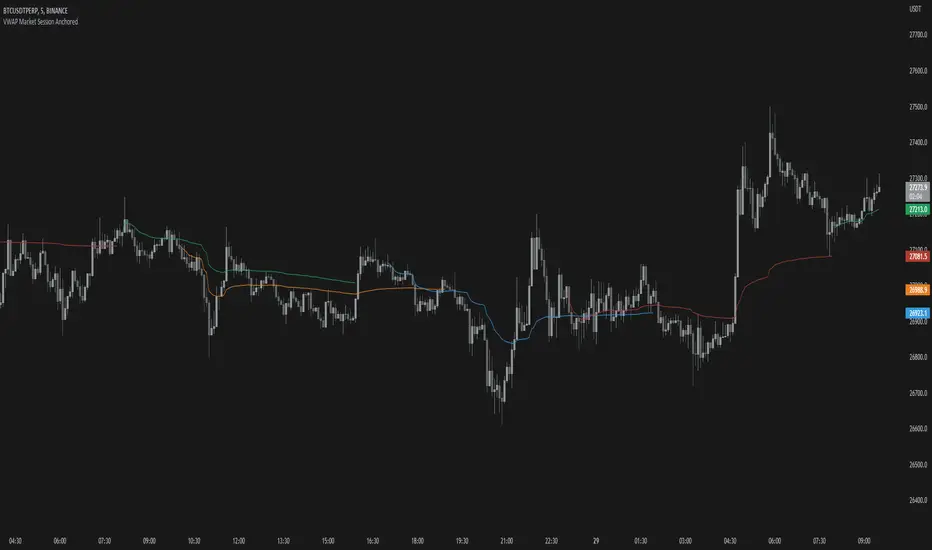

VWAP Market Session Anchored differs from the traditional VWAP or VWAP Auto Anchored indicator in that the Volume Weighted Average Price calculation is automatically anchored to four major market session starts: Sydney, London, Tokyo, New York.

Settings

Usage

Similar to the traditional VWAP, VWAP Market Session Anchored is a technical analysis tool used to measure the average price weighted by volume. VWAP Market Session Anchored can be used to identify the trend during a specific market session.

Limitations

When setting a custom session, be mindful that calculations are based off of the Coordinated Universal Time (UTC) time, you must convert your local time zone to UTC in order to have an accurate representation of your custom session.

It is not recommended to use this indicator on timeframes above 1 hour as market sessions only last a few hours.

Settings

- Source: the source for the VWAP calculation.

- Offset: changing this number will move the VWAP either Forwards or Backwards, relative to the current market. Zero is the default.

- Band: enabling this will show Standard Deviation bands.

- Band Multiplier: the value the Standard Deviation bands will be multiplied by before being plotted on the chart.

- Sessions: enabling the sessions will plot the respective anchored VWAP on chart.

- Custom: enabling this will show a custom user-defined session.

- Custom UTC: the custom session is defined by a starting UTC hour followed by the ending UTC hour.

Usage

Similar to the traditional VWAP, VWAP Market Session Anchored is a technical analysis tool used to measure the average price weighted by volume. VWAP Market Session Anchored can be used to identify the trend during a specific market session.

Limitations

When setting a custom session, be mindful that calculations are based off of the Coordinated Universal Time (UTC) time, you must convert your local time zone to UTC in order to have an accurate representation of your custom session.

It is not recommended to use this indicator on timeframes above 1 hour as market sessions only last a few hours.

リリースノート

- Updated colors

- Updated chart

オープンソーススクリプト

TradingViewの精神に則り、このスクリプトの作者はコードをオープンソースとして公開してくれました。トレーダーが内容を確認・検証できるようにという配慮です。作者に拍手を送りましょう!無料で利用できますが、コードの再公開はハウスルールに従う必要があります。

免責事項

この情報および投稿は、TradingViewが提供または推奨する金融、投資、トレード、その他のアドバイスや推奨を意図するものではなく、それらを構成するものでもありません。詳細は利用規約をご覧ください。

オープンソーススクリプト

TradingViewの精神に則り、このスクリプトの作者はコードをオープンソースとして公開してくれました。トレーダーが内容を確認・検証できるようにという配慮です。作者に拍手を送りましょう!無料で利用できますが、コードの再公開はハウスルールに従う必要があります。

免責事項

この情報および投稿は、TradingViewが提供または推奨する金融、投資、トレード、その他のアドバイスや推奨を意図するものではなく、それらを構成するものでもありません。詳細は利用規約をご覧ください。