SuperTrend AI (Clustering) [LuxAlgo]The SuperTrend AI indicator is a novel take on bridging the gap between the K-means clustering machine learning method & technical indicators. In this case, we apply K-Means clustering to the famous SuperTrend indicator.

🔶 USAGE

Users can interpret the SuperTrend AI trailing stop similarly to the regular SuperTrend indicator. Using higher minimum/maximum factors will return longer-term signals.

The displayed performance metrics displayed on each signal allow for a deeper interpretation of the indicator. Whereas higher values could indicate a higher potential for the market to be heading in the direction of the trend when compared to signals with lower values such as 1 or 0 potentially indicating retracements.

In the image above, we can notice more clear examples of the performance metrics on signals indicating trends, however, these performance metrics cannot perform or predict every signal reliably.

We can see in the image above that the trailing stop and its adaptive moving average can also act as support & resistance. Using higher values of the performance memory setting allows users to obtain a longer-term adaptive moving average of the returned trailing stop.

🔶 DETAILS

🔹 K-Means Clustering

When observing data points within a specific space, we can sometimes observe that some are closer to each other, forming groups, or "Clusters". At first sight, identifying those clusters and finding their associated data points can seem easy but doing so mathematically can be more challenging. This is where cluster analysis comes into play, where we seek to group data points into various clusters such that data points within one cluster are closer to each other. This is a common branch of AI/machine learning.

Various methods exist to find clusters within data, with the one used in this script being K-Means Clustering , a simple iterative unsupervised clustering method that finds a user-set amount of clusters.

A naive form of the K-Means algorithm would perform the following steps in order to find K clusters:

(1) Determine the amount (K) of clusters to detect.

(2) Initiate our K centroids (cluster centers) with random values.

(3) Loop over the data points, and determine which is the closest centroid from each data point, then associate that data point with the centroid.

(4) Update centroids by taking the average of the data points associated with a specific centroid.

Repeat steps 3 to 4 until convergence, that is until the centroids no longer change.

To explain how K-Means works graphically let's take the example of a one-dimensional dataset (which is the dimension used in our script) with two apparent clusters:

This is of course a simple scenario, as K will generally be higher, as well the amount of data points. Do note that this method can be very sensitive to the initialization of the centroids, this is why it is generally run multiple times, keeping the run returning the best centroids.

🔹 Adaptive SuperTrend Factor Using K-Means

The proposed indicator rationale is based on the following hypothesis:

Given multiple instances of an indicator using different settings, the optimal setting choice at time t is given by the best-performing instance with setting s(t) .

Performing the calculation of the indicator using the best setting at time t would return an indicator whose characteristics adapt based on its performance. However, what if the setting of the best-performing instance and second best-performing instance of the indicator have a high degree of disparity without a high difference in performance?

Even though this specific case is rare its however not uncommon to see that performance can be similar for a group of specific settings (this could be observed in a parameter optimization heatmap), then filtering out desirable settings to only use the best-performing one can seem too strict. We can as such reformulate our first hypothesis:

Given multiple instances of an indicator using different settings, an optimal setting choice at time t is given by the average of the best-performing instances with settings s(t) .

Finding this group of best-performing instances could be done using the previously described K-Means clustering method, assuming three groups of interest (K = 3) defined as worst performing, average performing, and best performing.

We first obtain an analog of performance P(t, factor) described as:

P(t, factor) = P(t-1, factor) + α * (∆C(t) × S(t-1, factor) - P(t-1, factor))

where 1 > α > 0, which is the performance memory determining the degree to which older inputs affect the current output. C(t) is the closing price, and S(t, factor) is the SuperTrend signal generating function with multiplicative factor factor .

We run this performance function for multiple factor settings and perform K-Means clustering on the multiple obtained performances to obtain the best-performing cluster. We initiate our centroids using quartiles of the obtained performances for faster centroids convergence.

The average of the factors associated with the best-performing cluster is then used to obtain the final factor setting, which is used to compute the final SuperTrend output.

Do note that we give the liberty for the user to get the final factor from the best, average, or worst cluster for experimental purposes.

🔶 SETTINGS

ATR Length: ATR period used for the calculation of the SuperTrends.

Factor Range: Determine the minimum and maximum factor values for the calculation of the SuperTrends.

Step: Increments of the factor range.

Performance Memory: Determine the degree to which older inputs affect the current output, with higher values returning longer-term performance measurements.

From Cluster: Determine which cluster is used to obtain the final factor.

🔹 Optimization

This group of settings affects the runtime performances of the script.

Maximum Iteration Steps: Maximum number of iterations allowed for finding centroids. Excessively low values can return a better script load time but poor clustering.

Historical Bars Calculation: Calculation window of the script (in bars).

AI

AI Trend Navigator [K-Neighbor]█ Overview

In the evolving landscape of trading and investment, the demand for sophisticated and reliable tools is ever-growing. The AI Trend Navigator is an indicator designed to meet this demand, providing valuable insights into market trends and potential future price movements. The AI Trend Navigator indicator is designed to predict market trends using the k-Nearest Neighbors (KNN) classifier.

By intelligently analyzing recent price actions and emphasizing similar values, it helps traders to navigate complex market conditions with confidence. It provides an advanced way to analyze trends, offering potentially more accurate predictions compared to simpler trend-following methods.

█ Calculations

KNN Moving Average Calculation: The core of the algorithm is a KNN Moving Average that computes the mean of the 'k' closest values to a target within a specified window size. It does this by iterating through the window, calculating the absolute differences between the target and each value, and then finding the mean of the closest values. The target and value are selected based on user preferences (e.g., using the VWAP or Volatility as a target).

KNN Classifier Function: This function applies the k-nearest neighbor algorithm to classify the price action into positive, negative, or neutral trends. It looks at the nearest 'k' bars, calculates the Euclidean distance between them, and categorizes them based on the relative movement. It then returns the prediction based on the highest count of positive, negative, or neutral categories.

█ How to use

Traders can use this indicator to identify potential trend directions in different markets.

Spotting Trends: Traders can use the KNN Moving Average to identify the underlying trend of an asset. By focusing on the k closest values, this component of the indicator offers a clearer view of the trend direction, filtering out market noise.

Trend Confirmation: The KNN Classifier component can confirm existing trends by predicting the future price direction. By aligning predictions with current trends, traders can gain more confidence in their trading decisions.

█ Settings

PriceValue: This determines the type of price input used for distance calculation in the KNN algorithm.

hl2: Uses the average of the high and low prices.

VWAP: Uses the Volume Weighted Average Price.

VWAP: Uses the Volume Weighted Average Price.

Effect: Changing this input will modify the reference values used in the KNN classification, potentially altering the predictions.

TargetValue: This sets the target variable that the KNN classification will attempt to predict.

Price Action: Uses the moving average of the closing price.

VWAP: Uses the Volume Weighted Average Price.

Volatility: Uses the Average True Range (ATR).

Effect: Selecting different targets will affect what the KNN is trying to predict, altering the nature and intent of the predictions.

Number of Closest Values: Defines how many closest values will be considered when calculating the mean for the KNN Moving Average.

Effect: Increasing this value makes the algorithm consider more nearest neighbors, smoothing the indicator and potentially making it less reactive. Decreasing this value may make the indicator more sensitive but possibly more prone to noise.

Neighbors: This sets the number of neighbors that will be considered for the KNN Classifier part of the algorithm.

Effect: Adjusting the number of neighbors affects the sensitivity and smoothness of the KNN classifier.

Smoothing Period: Defines the smoothing period for the moving average used in the KNN classifier.

Effect: Increasing this value would make the KNN Moving Average smoother, potentially reducing noise. Decreasing it would make the indicator more reactive but possibly more prone to false signals.

█ What is K-Nearest Neighbors (K-NN) algorithm?

At its core, the K-NN algorithm recognizes patterns within market data and analyzes the relationships and similarities between data points. By considering the 'K' most similar instances (or neighbors) within a dataset, it predicts future price movements based on historical trends. The K-Nearest Neighbors (K-NN) algorithm is a type of instance-based or non-generalizing learning. While K-NN is considered a relatively simple machine-learning technique, it falls under the AI umbrella.

We can classify the K-Nearest Neighbors (K-NN) algorithm as a form of artificial intelligence (AI), and here's why:

Machine Learning Component: K-NN is a type of machine learning algorithm, and machine learning is a subset of AI. Machine learning is about building algorithms that allow computers to learn from and make predictions or decisions based on data. Since K-NN falls under this category, it is aligned with the principles of AI.

Instance-Based Learning: K-NN is an instance-based learning algorithm. This means that it makes decisions based on the entire training dataset rather than deriving a discriminative function from the dataset. It looks at the 'K' most similar instances (neighbors) when making a prediction, hence adapting to new information if the dataset changes. This adaptability is a hallmark of intelligent systems.

Pattern Recognition: The core of K-NN's functionality is recognizing patterns within data. It identifies relationships and similarities between data points, something akin to human pattern recognition, a key aspect of intelligence.

Classification and Regression: K-NN can be used for both classification and regression tasks, two fundamental problems in machine learning and AI. The indicator code is used for trend classification, a predictive task that aligns with the goals of AI.

Simplicity Doesn't Exclude AI: While K-NN is often considered a simpler algorithm compared to deep learning models, simplicity does not exclude something from being AI. Many AI systems are built on simple rules and can be combined or scaled to create complex behavior.

No Explicit Model Building: Unlike traditional statistical methods, K-NN does not build an explicit model during training. Instead, it waits until a prediction is required and then looks at the 'K' nearest neighbors from the training data to make that prediction. This lazy learning approach is another aspect of machine learning, part of the broader AI field.

-----------------

Disclaimer

The information contained in my Scripts/Indicators/Ideas/Algos/Systems does not constitute financial advice or a solicitation to buy or sell any securities of any type. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

My Scripts/Indicators/Ideas/Algos/Systems are only for educational purposes!

Wick-to-Body Ratio Trend Forecast | Flux ChartsThe Wick-to-Body Ratio Trend Forecast Indicator aims to forecast potential movements following the last closed candle using the wick-to-body ratio. The script identifies those candles within the loopback period with a ratio matching that of the last closed candle and provides an analysis of their trends.

➡️ USAGE

Wick-to-body ratios can be used in many strategies. The most common use in stock trading is to discern bullish or bearish sentiment. This indicator extends candle ratios, revealing previous patterns that follow a candle with a similar ratio. The most basic use of this indicator is the single forecast line.

➡️ FORECASTING SYSTEM

This line displays a compilation of the averages of all the previous trends resulting from those historical candles with a matching ratio. It shows the average movements of the trends as well as the 'strength' of the trend. The 'strength' of the trend is a gradient that is blue when the trend deviates more from the average and red when it deviates less.

Chart: AMEX:SPY 30 min; Indicator Settings: Loopback 700, Previous Trends ON

The color-coded deviation is visible in this image of the indicator with the default settings (except for Forecast Lines > Previous Trends ), and the trend line grows bluer as the past patterns deviate more.

➡️ ADAPTIVE ACCEPTABLE RANGE

The algorithm looks back at every candle within the loopback period to find candles that match the last closed candle. The algorithm adaptively changes the acceptable range to which a candle can differ from the ratio of the last closed candle. The algorithm will never have more than 15 historical points used, as it will lower its sensitivity before it reaches that point.

Chart: BITSTAMP:BTCUSD 5 min; Indicator Settings: Loopback 700

Here is the BTC chart on 7/6/23 with default settings except for the loopback period at 700.

Chart: BITSTAMP:BTCUSD 5 min; Indicator Settings: Loopback 200

Here is the exact same chart with a loopback period of 200. While the first ratio for both is the same, a new ratio is revealed for the chart with a loopback of only 200 because the adaptive range is adjusted in the algorithm to find an acceptable number of reference points. Note the table in the top right however, while the algorithm adapts the acceptable range between the current ratio and historical ones to find reference points, there is a threshold at which candles will be considered too inaccurate to be considered. This prevents meaningless associations between candles due to a particularly rare ratio. This threshold can be adjusted in the settings through "Default Accuracy".

Order Block Scanner - Institutional ActivityIntroducing the Order Block Scanner: Unleash the Power of Institutional Insight!

Unlock a whole new realm of trading opportunities with the Order Block Scanner, your ultimate weapon in the dynamic world of financial markets. This cutting-edge indicator is meticulously designed to empower you with invaluable insights into potential Institutional and Hedge Funds activity like never before. Prepare to harness the intelligence that drives the giants of the industry and propel your trading success to new heights.

Institutional trading has long been veiled in secrecy, an exclusive realm accessible only to the chosen few. But with the Order Block Scanner, the doors to this realm swing open, inviting you to step inside and seize the advantage. Our revolutionary technology employs advanced algorithms to scan and analyze market data, pinpointing the telltale signs of institutional activity that can make or break your trades.

Imagine having the power to identify key levels where Institutional and Hedge Funds are initiating significant trades. With the Order Block Scanner, these hidden order blocks are unveiled, allowing you to ride the coattails of the market giants. This game-changing tool decodes their strategies, offering you a window into their actions and allowing you to align your trading decisions accordingly.

Forget the guesswork and uncertainty that plague so many traders. The Order Block Scanner empowers you with precision and clarity, helping you make informed decisions based on real-time data. Identify when the big players enter or exit the market, recognize their accumulation or distribution patterns, and position yourself for maximum profit potential.

Step into the realm of trading mastery and unleash your potential with the Order Block Scanner. Elevate your trading game, tap into the world of institutional trading, and take your profits to soaring heights. Don't let opportunity pass you by – invest in the Order Block Scanner today and embark on a thrilling journey toward trading success like never before.

The algorithm operates on data from Options and Darkpool markets, which is first exported to Quandl DB and then imported to TradingView using an API. The indicator also identifies patterns based on volume, volatility, and market movements, increasing the number of identified institutional activities on the markets.

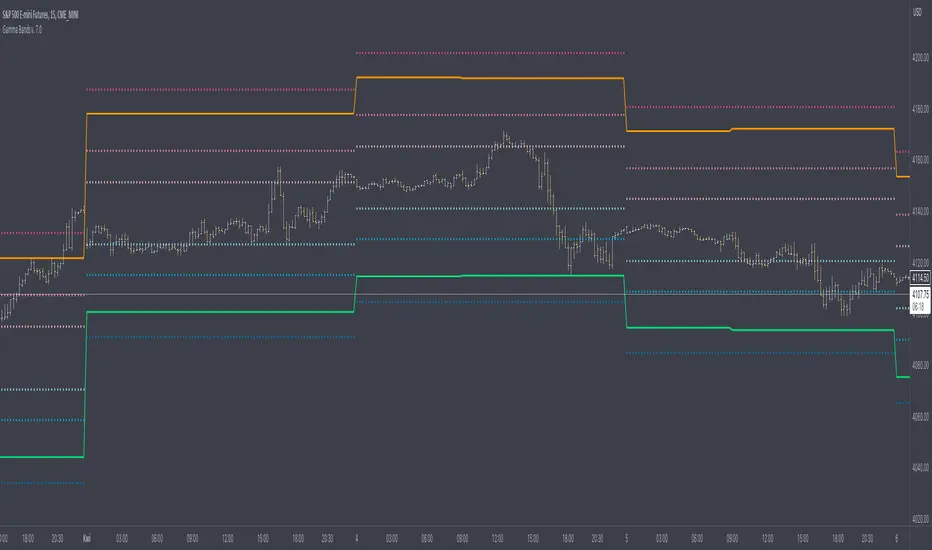

Gamma Bands v. 7.0Gamma Bands are based on previous day data of base intrument, Volatility , Options flow (imported from external source Quandl via TradingView API as TV is not supporting Options as instruments) and few other additional factors to calculate intraday levels. Those levels in correlation with even pure Price Action works like a charm what is confirmed by big orders often placed exactly on those levels on Futures Contracts. We have levels +/- 0.25, 0.5 and 1.0 that are calculated from Pivot Point and are working like Support and Resistance. Higher the number of Gamma, stronger the level. Passing Gamma +1/-1 would be good entry point for trades as almost everytime it is equal to Trend Day. Levels are calculated by Machine Learning algorithm written in Python which downloads data from Options and Darkpool markets, process and calculate levels, export to Quandl and then in PineScript I import the data to indicator. Levels are refreshed each day and are valid for particular trading day.

There's possibility also to enable display of Initial Balance range (High and Low range of bars/candles from 1st hour of regular cash session). Breaking one of extremes of Initial Balance is very often driving sentiment for rest of the session.

Volatility Reversal Levels

They're calculated taking into account Options flow imported to TV (Strikes, Call/Put types & Expiration dates) in combination with Volatility, Volume flow. Based on that we calculate on daily basis Significant Close level and "Stop and Reversal level".

Very often reaching area close to those levels either trigger immediate reversal of previous trend or at least push price into consolidation range.

[UPRIGHT Trading] Volatility Trend Filter (VTF) AlgoHello Traders,

As some of you know, I have had this in Beta for a long while now and it's finally time for a full release.

I originally designed this to be an Unreal Algo add-on to track & stay in the trade a little better, but the VTF Algo has become a full Algorithm and can be used standalone with supreme accuracy.

It's for beginners and advanced traders alike. I've made the settings very customizable, but also easy to just jump right in.

How it works:

It uses volatility , deviations, and tons of statistical calculations, confirmations, moving averages, and filters to bring you the most accurate Supply & Demand predictive algorithm possible. The VTF Algo will automatically normalize different volatility in any type of market to help avoid getting Chopped up and give a forward-looking approach to accurate Price Action and confirmation. It will automatically show support and resistance in real-time. The channel that The VTF Algo creates will help traders confirm whether they should stay in the trade or get out fast. As the green top grows it naturally acts as Supply and as the red bottom grows it acts as Demand, when one of them far exceeds the other the direction price will proceed to is clear to see.

Features:

-Easy-to-read Price Action & Trend channel.

-Exceptional Chop Filter (grayed center).

-Accurate Buy/Sell and Topline Continuation Signals.

-Rejection Signals.

-Multiple-Timeframe Customizable Trend Table. Showing Directional Arrows (see bottom right of picture).

-Bullish / Bearish Growing Blocks.

-Fully Customizable with Clean and Cleaner Mode.

The VTF Algo was made with all different types of traders in mind.

Some like things Ultra Crispy Clean:

Others like things a little more clean but can move their focus to where it's needed:

Lastly, there are those who don't mind things looking a little busy:

Topline Continuation Signals, Auto-Supply/Demand, and a Real-Time Multiple Timeframe Trend Table (in the bottom-right) corner:

Meshes perfectly as an Algo Add-on for Unreal Algo © (as originally designed) to enhance "The Simple Strat" © :

I tried to make everything as customizable as possible. So adding or removing or color-changing is super easy.

Happy Trading.

Cheers,

Mike

Universal Moving Average Convergence DivergenceI changed MACD formula to divergence of (MA26/MA12 - 1).

And its make it more useful.

Cuz:

1) comparability with all other coins with different prices.

2) fix small numbers in low price coines like shiba

3) making a good indicator like RSI to use it for optimization and ML/AI projects as a variable

Most important thing about this indicator is that its Universal

Now you can compare the UMACD of Shiba with Bitcoin without any problem in matamatics space.No need to use virtuality and its important in Optimization problems that we rediuse the problem from a picture to a number(A plot to a list of numbers)

If we don't care about exagrated pumps and dumps, we can say to it Normalized-MACD too. Cuz in normal situations its MAX ≈ 0.1 and MIN ≈ -0.1

Tesla Coil MLThis is a re-implementation of @veryfid's wonderful Tesla Coil indicator to leverage basic Machine Learning Algorithms to help classify coil crossovers. The original Tesla Coil indicator requires extensive training and practice for the user to develop adequate intuition to interpret coil crossovers. The goal for this version is to help the user understand the underlying logic of the Tesla Coil indicator and provide a more intuitive way to interpret the indicator. The signals should be interpreted as suggestions rather than as a hard-coded set of rules.

NOTE: Please do NOT trade off the signals blindly. Always try to use your own intuition for understanding the coils and check for confluence with other indicators before initiating a trade.

MoonFlag DailyThis is a useful indicator as it shows potential long and short regions by coloring the AI wavecloud green or red.

There is an option to show a faint white background in regions where the green/red cloud parts are failing as a trade from the start position of each region.

Its a combination of 3 algos I developed, and there is an option to switch to see these individually, although this has lots of info and is a bit confusing.

It does have alerts and there are text boxes in the indicator settings where a comment can be input - this is useful for webhooks bots auto trading.

Most useful in this indicator is that at the end of each green/long or red/short region there is a label that shows the % gain or loss for a trade.

The label at the end of the chart shows the % of winning longs/shorts and the average % gain or loss for all the longs/shorts within the set test period (set in settings)

So, I generally set the chart initially on a 15min timeframe with the indicator timeframe (in settings) set to run on say 30min or 1hour. I then select a long test period (several plus months) and then optimize the wavelcloud length (in settings) to give the best %profit per trade. (Longs always seem to give better results than shorts)

I then, change the chart timeframe to much faster, say 1min or 5min, but leave the indicator timeframe at 1 hour. In this manner - the label only shows a few trades however, the algo is run at every bar close and when this is set to 1min, this means that losses will be minimised at the bot exits quickly. In comparison - if the chart is on a 15min timeframe - it can take this amount before the bot will exit a trade and by then there could be catastrophic losses.

It is quite hard to get a positive result - although with a bit of playing around - just as a background indicator - I find this useful. I generally set-up on say 4charts all with different timeframes and then look for consistency between the long/short signal positions. (Although when I run as a bot I use a fast timeframe)

Please do leave some comments and get in touch.

MoonFlag (Josef Tainsh PhD)

Unreal Algo [UPRIGHT] (cc)Hello Traders,

It's finally that time, I'm releasing my baby out into the world.

Unreal Algo is the answer to the question you didn't know you were asking.

It's for beginners and advanced traders alike. I've made the settings very customizable, but also easy to just jump right in.

How it works:

It uses tons of calculations, confirmations, and filters to bring you the most accurate predictive algorithm possible. The algo will automatically adjust to different volatility in the market to still provide accurate signals and confirmation. It will automatically show support and resistance in real-time. A Moving Average cloud with speeds varying from extra fast to slow; they will help traders confirm whether they should stay in the trade. Also, I added 2 stoplosses, because the importance of risk management should always be emphasized even with strong accuracy.

Features:

---The Most Accurate Signals on the planet.

--------Buy/Sell, Up/Down direction change, and Red/Green arrows.

--- MA cloud with beautiful color blend that can act as a confirmation of direction.

-------- 17 different types/versions of moving Averages to choose from.

--------Easy line transparency and toggle adjustments.

--------Easy cloud transparency adjustments.

--- Support and Resistance .

--- Advanced PSAR that will show red when bearish while in a bullish trend, and visa-versa.

---Potential Orderblocks that can be extended to show a grid (adding additional support/resistance information).

--- Fibonacci Lines.

--- Pivot bar that changes colors based on pivot direction.

---Resistance Breakout and Support Breakdown Signals .

--- Relative volume & momentum bar coloring.

---Two Separate Stoplosses .

--------Circles change color and flip to top and red for Short, bottom and green for long.

--------Horizontal stoploss that tracks the price and flags to take profit. White for Long and Yellow for short.

---As always... Fully customizable .

Different customization options:

Without stoplosses and Support/Resistance.

Without Support/Resistance, arrows and psar removed.

Added back Support/Resistance, lightened MA cloud

Fully loaded (minus trailing stoploss)

neutronix community bot ML + Alerts 4h-daily (mod. capissimo)Gm traders,

i have been a python programmer for some years studying artificial intelligence for general purpose; after some time i finally decided to have a look at some finance related stuff and scripts.

Moved by curiosity i've decided to make some but decisive modifications to a script i tried to use initially but without success: the LVQ machine learning strategy.

So after studying the charts and indicators, i have rewritten this script made by Capissimo and added heavy filtering thanks to vwap and vwma, then fixed repaint and other issues.

I hope you enjoy it and that it could increase your possibilities of success in trading.

HOW TO USE THE SCRIPT

Add the script to 3h+ charts like for example BTC 4h, 6h, 8h, 12h, daily. (In order for it to work on shorter timeframes charts you can try to change to lookback window but i dont advise it).

Change only rsi and volfilter(volume filtering) settings to try to find the best winrate. Leave dataset to open. Fyi the winrate isn't 100% accurate but can give you a raw vision of final results.

Use alerts included for trading and and in options click on 'Once per bar'. If you have checked 'Reverse Signals' in the control panel you have got more 'risky' signals so be advised if trading futures and stocks.

Exit trade signals not provided, so it is recommended the use of take profits and stop loss (1.5:1 ratio)

As always, the script is for study purposes. Do not risk more than you can spend!

Original LVQ-based strategy made by capissimo

Modified by gravisxv 13/10/2021

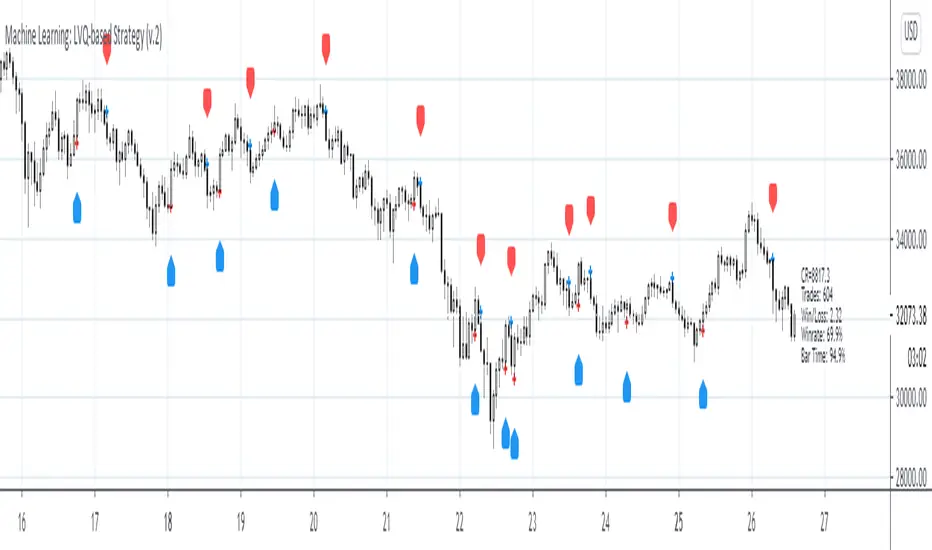

Machine Learning: LVQ-based StrategyLVQ-based Strategy (FX and Crypto)

Description:

Learning Vector Quantization (LVQ) can be understood as a special case of an artificial neural network, more precisely, it applies a winner-take-all learning-based approach. It is based on prototype supervised learning classification task and trains its weights through a competitive learning algorithm.

Algorithm:

Initialize weights

Train for 1 to N number of epochs

- Select a training example

- Compute the winning vector

- Update the winning vector

Classify test sample

The LVQ algorithm offers a framework to test various indicators easily to see if they have got any *predictive value*. One can easily add cog, wpr and others.

Note: TradingViews's playback feature helps to see this strategy in action. The algo is tested with BTCUSD/1Hour.

Warning: This is a preliminary version! Signals ARE repainting.

***Warning***: Signals LARGELY depend on hyperparams (lrate and epochs).

Style tags: Trend Following, Trend Analysis

Asset class: Equities, Futures, ETFs, Currencies and Commodities

Dataset: FX Minutes/Hours+++/Days

Machine Learning: Logistic RegressionMulti-timeframe Strategy based on Logistic Regression algorithm

Description:

This strategy uses a classic machine learning algorithm that came from statistics - Logistic Regression (LR).

The first and most important thing about logistic regression is that it is not a 'Regression' but a 'Classification' algorithm. The name itself is somewhat misleading. Regression gives a continuous numeric output but most of the time we need the output in classes (i.e. categorical, discrete). For example, we want to classify emails into “spam” or 'not spam', classify treatment into “success” or 'failure', classify statement into “right” or 'wrong', classify election data into 'fraudulent vote' or 'non-fraudulent vote', classify market move into 'long' or 'short' and so on. These are the examples of logistic regression having a binary output (also called dichotomous).

You can also think of logistic regression as a special case of linear regression when the outcome variable is categorical, where we are using log of odds as dependent variable. In simple words, it predicts the probability of occurrence of an event by fitting data to a logit function.

Basically, the theory behind Logistic Regression is very similar to the one from Linear Regression, where we seek to draw a best-fitting line over data points, but in Logistic Regression, we don’t directly fit a straight line to our data like in linear regression. Instead, we fit a S shaped curve, called Sigmoid, to our observations, that best SEPARATES data points. Technically speaking, the main goal of building the model is to find the parameters (weights) using gradient descent.

In this script the LR algorithm is retrained on each new bar trying to classify it into one of the two categories. This is done via the logistic_regression function by updating the weights w in the loop that continues for iterations number of times. In the end the weights are passed through the sigmoid function, yielding a prediction.

Mind that some assets require to modify the script's input parameters. For instance, when used with BTCUSD and USDJPY, the 'Normalization Lookback' parameter should be set down to 4 (2,...,5..), and optionally the 'Use Price Data for Signal Generation?' parameter should be checked. The defaults were tested with EURUSD.

Note: TradingViews's playback feature helps to see this strategy in action.

Warning: Signals ARE repainting.

Style tags: Trend Following, Trend Analysis

Asset class: Equities, Futures, ETFs, Currencies and Commodities

Dataset: FX Minutes/Hours/Days

Machine Learning: Perceptron-based strategyPerceptron-based strategy

Description:

The Learning Perceptron is the simplest possible artificial neural network (ANN), consisting of just a single neuron and capable of learning a certain class of binary classification problems. The idea behind ANNs is that by selecting good values for the weight parameters (and the bias), the ANN can model the relationships between the inputs and some target.

Generally, ANN neurons receive a number of inputs, weight each of those inputs, sum the weights, and then transform that sum using a special function called an activation function. The output of that activation function is then either used as the prediction (in a single neuron model) or is combined with the outputs of other neurons for further use in more complex models.

The purpose of the activation function is to take the input signal (that’s the weighted sum of the inputs and the bias) and turn it into an output signal. Think of this activation function as firing (activating) the neuron when it returns 1, and doing nothing when it returns 0. This sort of computation is accomplished with a function called step function: f(z) = {1 if z > 0 else 0}. This function then transforms any weighted sum of the inputs and converts it into a binary output (either 1 or 0). The trick to making this useful is finding (learning) a set of weights that lead to good predictions using this activation function.

Training our perceptron is simply a matter of initializing the weights to zero (or random value) and then implementing the perceptron learning rule, which just updates the weights based on the error of each observation with the current weights. This has the effect of moving the classifier’s decision boundary in the direction that would have helped it classify the last observation correctly. This is achieved via a for loop which iterates over each observation, making a prediction of each observation, calculating the error of that prediction and then updating the weights accordingly. In this way, weights are gradually updated until they converge. Each sweep through the training data is called an epoch.

In this script the perceptron is retrained on each new bar trying to classify this bar by drawing the moving average curve above or below the bar.

This script was tested with BTCUSD, USDJPY, and EURUSD.

Note: TradingViews's playback feature helps to see this strategy in action.

Warning: Signals ARE repainting.

Style tags: Trend Following, Trend Analysis

Asset class: Equities, Futures, ETFs, Currencies and Commodities

Dataset: FX Minutes/Hours+/Days

Machine Learning: kNN-based Strategy (mtf)This is a multi-timeframe version of the kNN-based strategy.

GreenCrypto Swing Trade Indicator - GC02Overview: This is a swing trading Indictor works using support & resistance and market trend, it is designed for all type of markets (crypto, forex, stock etc.) and works on all commonly used timeframes (preferably on 1H, 4H Candles).

How it works:

Core logic behind this indicator is to finding the Support and Resistance, we find the Lower High (LH) and Higher Low (HL) to find the from where the price reversed(bounced back) and also we use a custom logic for figuring out the peak price in the last few candles (based on the input "Strength" ). Based on the multiple previous Support and Resistance (HH, HL, LL LH) we calculate a price level, this price level is used a major a factor for entering the trade. Once we have the price level we check if the current price crosses that price level, if it crossed then we consider that as a long/short entry (based on whether it crosses resistance or support line that we calculated). Once we have pre long/short signals we further filter it based on the market trend to prevent too early/late signals, this trend is calculated based on the value from the input field "Factor". Along with this if we don't see a clear trend we do the filtering by checking how many support or resistance level the price has bounced off.

Stop Loss and Take Profit : We have also added printing SL and TP levels on the chart to make the it easier for everyone to find the SL/TP values. Script calculates the SL value by checking the previous support level for LONG trade and previous resistance level for SHORT trades. Take profit are calculated in 1:1 ratio as of now.

Available Inputs:

Strength : Define the strength of the support resistance that we calculate. The lower value means less number of candles used for calculating the support & resistance and vice versa

Factor : Specify what level of trend to use. Using higher value will result script looking using the larger trend (zoomed out trend) and using lesser value will result in using the short trends

Note: For most of the charts you don’t need to change the default values. However, feel free to try it out.

How to use:

Add the script to the chart and once the indicator is load it will display the "long" and "short" entry points along with the stopLoss and takeProfit points.

How to get access:

Send a DM to us for getting access to the script.

Machine Learning: kNN-based StrategykNN-based Strategy (FX and Crypto)

Description:

This strategy uses a classic machine learning algorithm - k Nearest Neighbours (kNN) - to let you find a prediction for the next (tomorrow's, next month's, etc.) market move. Being an unsupervised machine learning algorithm, kNN is one of the most simple learning algorithms.

To do a prediction of the next market move, the kNN algorithm uses the historic data, collected in 3 arrays - feature1, feature2 and directions, - and finds the k-nearest

neighbours of the current indicator(s) values.

The two dimensional kNN algorithm just has a look on what has happened in the past when the two indicators had a similar level. It then looks at the k nearest neighbours,

sees their state and thus classifies the current point.

The kNN algorithm offers a framework to test all kinds of indicators easily to see if they have got any *predictive value*. One can easily add cog, wpr and others.

Note: TradingViews's playback feature helps to see this strategy in action.

Warning: Signals ARE repainting.

Style tags: Trend Following, Trend Analysis

Asset class: Equities, Futures, ETFs, Currencies and Commodities

Dataset: FX Minutes/Hours+++/Days

KBL PLAY-ZONE PLOTTER - MCX CRUDE OIL

► How To Use This Indicator ?

• New Intraday Trading Levels Will Be Generated At 09:30 AM (UTC +05:30)

• Buy If 5 Minutes Candle Close Above '' BreakOut Buy Here '' Level.

• Sell If 5 Minutes Candle Close Below '' BreakOut Sell Here '' Level.

• Book Profits At Breakout Buy or BreakOut Sell Targets.

• If 1st Call Target Hit , Then Do Not Trade More On That Day.

• If 1st Call StopLoss Hit , Then Only Trade On 2nd Call.

PM us to obtain access.

Candlesticks ANN for Stock Markets TF : 1WHello, this script consists of training candlesticks with Artificial Neural Networks (ANN).

In addition to the first series, candlesticks' bodies and wicks were also introduced as training inputs.

The inputs are individually trained to find the relationship between the subsequent historical value of all candlestick values 1.(High,Low,Close,Open)

The outputs are adapted to the current values with a simple forecast code.

Once the OHLC value is found, the exponential moving averages of 5 and 20 periods are used.

Reminder : OHLC = (Open + High + Close + Low ) / 4

First version :

Script is designed for S&P 500 Indices,Funds,ETFs, especially S&P 500 Stocks,and for all liquid Stocks all around the World.

NOTE: This script is only suitable for 1W time-frame for Stocks.

The average training error rates are less than 5 per thousand for each candlestick variable. (Average Error < 0.005 )

I've just finished it and haven't tested it in detail.

So let's use it carefully as a supporter.

Best regards !

ANN Next Coming Candlestick Forecast SPX 1D v1.0WARNING:

Experimental and incomplete.

Script is open to development and will be developed.

This is just version 1.0

STRUCTURE

This script is trained according to the open, close, high and low values of the bars.

It is tried to predict the future values of opening, closing, high and low values.

A few simple codes were used to correlate expectation with current values. (You can see between line 129 - 159 )

Therefore, they are all individually trained.

You can see in functions.

The average training error of each variable is less than 0.011.

NOTE :

This script is designed for experimental use on S & P 500 and connected instruments only on 1-day bars.

The Plotcandle function is inspired by the following script of alexgrover :

Since we estimate the next values, our error rates should be much lower for all candlestick values. This is just first version to show logic.

I will continue to look for other variables to reach average error = 0.001 - 0.005 for each candlestick status.

Feel free to use and improve , this is open-source.

Best regards.

ANN BTC MTF Golden Cross Period MACDHi, this is the MACD version of the ANN BTC Multi Timeframe Script.

The MACD Periods were approximated to the Golden Cross values.

MACD Lengths :

Signal Length = 25

Fast Length = 50

Slow Length = 200

Regards.

ANN BTC MTF CM Sling Shot SystemHi all, this script was created as a result of ANN training in all time frames of bitcoin data.

Trained data is built on Chris Moody's Sling Shot system.

CM Sling Shot System :

This system automatically generates the ANN output for all time periods.

Therefore, it has multi-time-frame feature.

Artificial Neural Networks training details:

Average Errors

1 minute = 0.005570

3 minutes = 0.006674

5 minutes = 0.007067

15 minutes = 0.010000

30 minutes = 0.009398

45 minutes = 0.010000

1 Hour = 0.006848

2 Hours = 0.006901

3 Hours = 0.009608

4 Hours = 0.009774

1 Day = 0.010000

1 Week = 0.010000

The results look good (All Average Error <= 0.01 ), the Sling Shot Method is also good, but you can also refer to historically slower period averages to filter these arrows a bit more. I leave the decision to you.

Best regards.

Relativity Adaptive Stop-LossRelativity Adaptive Stop-Loss is a stop-loss technique that uses the Relativity Autonomous Distribution Blocks algorithm.

For detailed info about Relativity Autonomous Distribution Blocks :

*** Features

This structure is different from standard stop-losses.

The base frame is based on "Market Adaptive Stop-Loss" script.

For detailed information about Market Adaptive Stop-Loss:

This script uses the Relativity Autonomous Distribution Blocks as cross method.

Tradeable / Non Tradeable Region Detector :

This script separates tradeable and non-tradeable regions with a coloring method.

Plotting Rules :

* Maroon : Uncorfirmed Short Positions

* Teal : Unconfirmed Long Positions

* Green : Confirmed Long Positions

* Red : Confirmed Short Positions

This script can be used in only 1W time frame. (TF = 1W )

Does not repaint on 1W and larger time frames. ( Source = close )

*** Settings :

The only option here is the ATR multiplier.

The default use value of this ATR multiplier, which is of the standard of stop-loss, is 2.You can set it from the menu.

No alert is set.

Because the positive and negative regions are the same as Relativity Autonomous Distribution Blocks.

Since the traders can trade according to the support and resistance outside the definite regions, the unnecessary signal was confused and the alerts were removed.

*** USAGE

The Stop-Loss indicator can slide on the chart.

So you have to make sure you put it in right place.

Using this script in a new pane below will radically solve slip problems.

Stop-Loss values do not slip definitely.The values can select from the alignment.

NOTE :

Some structures (Market Adaptive Stop-Loss) and design in this script are inspired by everget's Chandelier Exit script :

Best regards.