Elder Ray (Bull Power) Strategy Backtest Developed by Dr Alexander Elder, the Elder-ray indicator measures buying

and selling pressure in the market. The Elder-ray is often used as part

of the Triple Screen trading system but may also be used on its own.

Dr Elder uses a 13-day exponential moving average (EMA) to indicate the

market consensus of value. Bull Power measures the ability of buyers to

drive prices above the consensus of value. Bear Power reflects the ability

of sellers to drive prices below the average consensus of value.

Bull Power is calculated by subtracting the 13-day EMA from the day's High.

Bear power subtracts the 13-day EMA from the day's Low.

You can use in the xPrice any series: Open, High, Low, Close, HL2, HLC3, OHLC4 and ect...

You can change long to short in the Input Settings

Please, use it only for learning or paper trading. Do not for real trading.

Algotrading

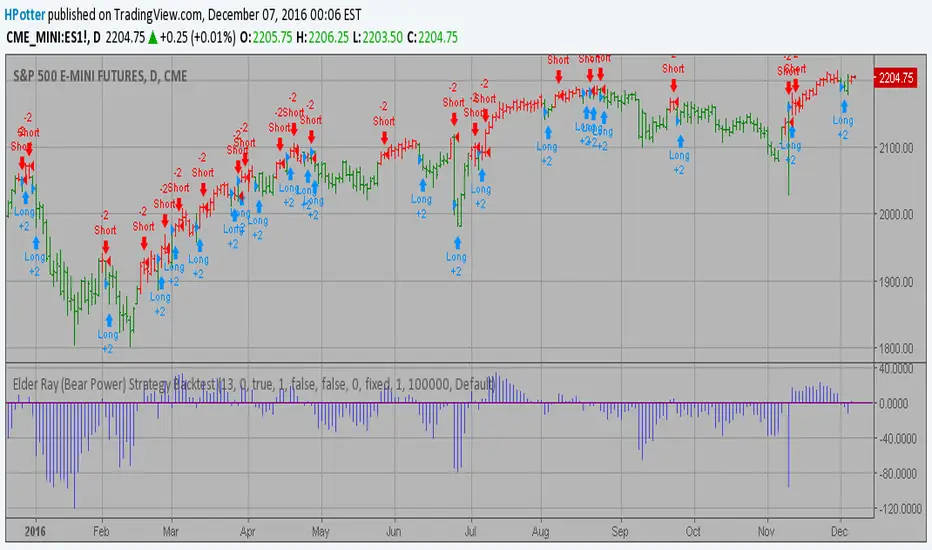

Elder Ray (Bear Power) Strategy Backtest Developed by Dr Alexander Elder, the Elder-ray indicator measures buying

and selling pressure in the market. The Elder-ray is often used as part

of the Triple Screen trading system but may also be used on its own.

Dr Elder uses a 13-day exponential moving average (EMA) to indicate the

market consensus of value. Bear Power measures the ability of sellers to

drive prices below the consensus of value. Bear Power reflects the ability

of sellers to drive prices below the average consensus of value.

Bull Power is calculated by subtracting the 13-day EMA from the day's High.

Bear power subtracts the 13-day EMA from the day's Low.

You can use in the xPrice any series: Open, High, Low, Close, HL2, HLC3, OHLC4 and ect...

You can change long to short in the Input Settings

Please, use it only for learning or paper trading. Do not for real trading.

ECO Strategy Backtest We call this one the ECO for short, but it will be listed on the indicator list

at W. Blau’s Ergodic Candlestick Oscillator. The ECO is a momentum indicator.

It is based on candlestick bars, and takes into account the size and direction

of the candlestick "body". We have found it to be a very good momentum indicator,

and especially smooth, because it is unaffected by gaps in price, unlike many other

momentum indicators.

We like to use this indicator as an additional trend confirmation tool, or as an

alternate trend definition tool, in place of a weekly indicator. The simplest way

of using the indicator is simply to define the trend based on which side of the "0"

line the indicator is located on. If the indicator is above "0", then the trend is up.

If the indicator is below "0" then the trend is down. You can add an additional

qualifier by noting the "slope" of the indicator, and the crossing points of the slow

and fast lines. Some like to use the slope alone to define trend direction. If the

lines are sloping upward, the trend is up. Alternately, if the lines are sloping

downward, the trend is down. In this view, the point where the lines "cross" is the

point where the trend changes.

When the ECO is below the "0" line, the trend is down, and we are qualified only to

sell on new short signals from the Hi-Lo Activator. In other words, when the ECO is

above 0, we are not allowed to take short signals, and when the ECO is below 0, we

are not allowed to take long signals.

You can change long to short in the Input Settings

Please, use it only for learning or paper trading. Do not for real trading.

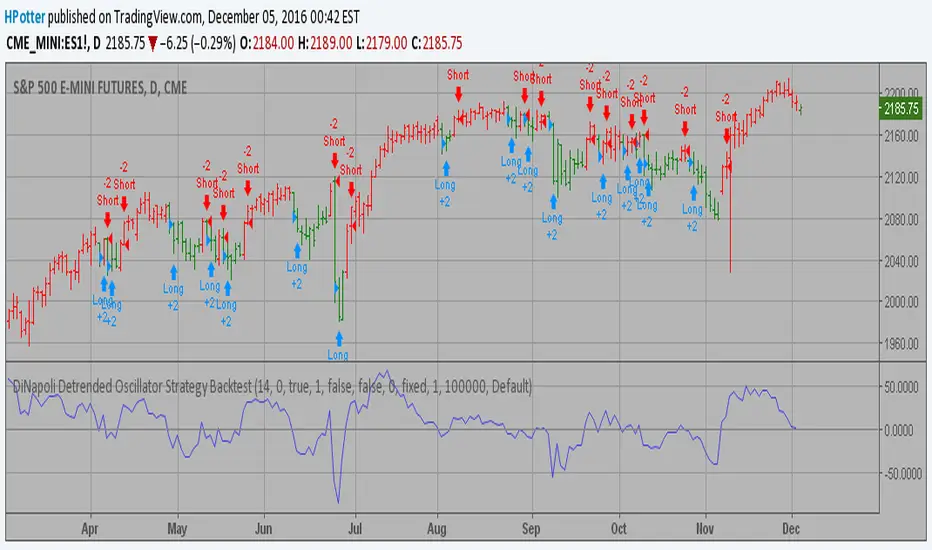

DiNapoli Detrended Oscillator Strategy Backtest DiNapoli Detrended Oscillator Strategy

You can change long to short in the Input Settings

Please, use it only for learning or paper trading. Do not for real trading.

DAPD - Strategy Backtest This indicator is similar to Bollinger Bands. It based on DAPD - Daily

Average Price Delta. DAPD is based upon a summation for each of the

highs (hod) for the 21 days prior to today minus the summation for

each of the lows (lod) for the last 21 days prior to today. The result

of this calculation would then be divided by 21.

It will be buy when high above previos DAPD high and sell if low below previos DAPD low

You can change long to short in the Input Settings

Please, use it only for learning or paper trading. Do not for real trading.

Chaikin Volatility Strategy Backtest Chaikin's Volatility indicator compares the spread between a security's

high and low prices. It quantifies volatility as a widening of the range

between the high and the low price.

You can use in the xPrice1 and xPrice2 any series: Open, High, Low, Close, HL2,

HLC3, OHLC4 and ect...

You can change long to short in the Input Settings

Please, use it only for learning or paper trading. Do not for real trading.

CCI Strategy Reversed Backtest The Commodity Channel Index (CCI) is best used with markets that display cyclical or

seasonal characteristics, and is formulated to detect the beginning and ending of these

cycles by incorporating a moving average together with a divisor that reflects both possible

and actual trading ranges. The final index measures the deviation from normal, which indicates

major changes in market trend.

To put it simply, the Commodity Channel Index (CCI) value shows how the instrument is trading

relative to its mean (average) price. When the CCI value is high, it means that the prices are

high compared to the average price; when the CCI value is down, it means that the prices are low

compared to the average price. The CCI value usually does not fall outside the -300 to 300 range

and, in fact, is usually in the -100 to 100 range.

You can change long to short in the Input Settings

Please, use it only for learning or paper trading. Do not for real trading.

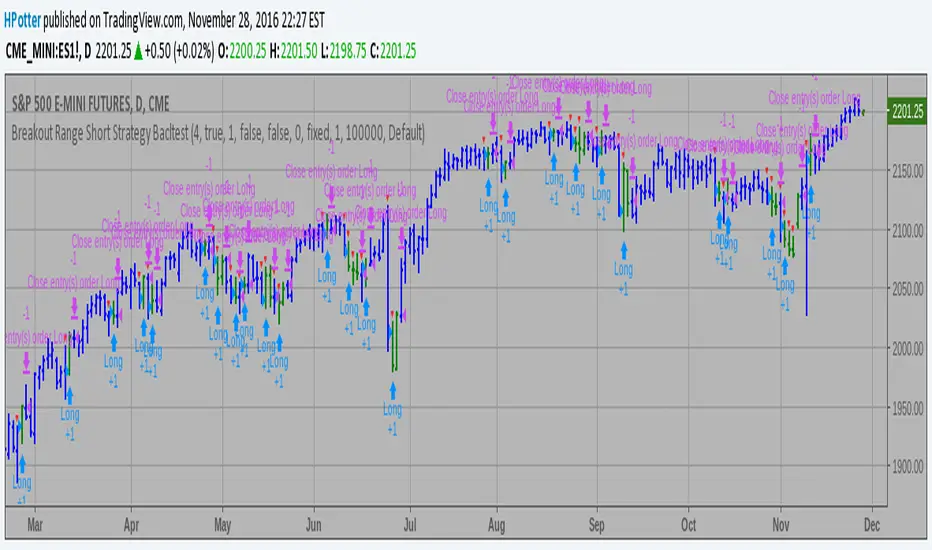

Breakout Range Short Strategy BacktestBreakout Range Short Strategy

You can change long to short in the Input Settings

Please, use it only for learning or paper trading. Do not for real trading.

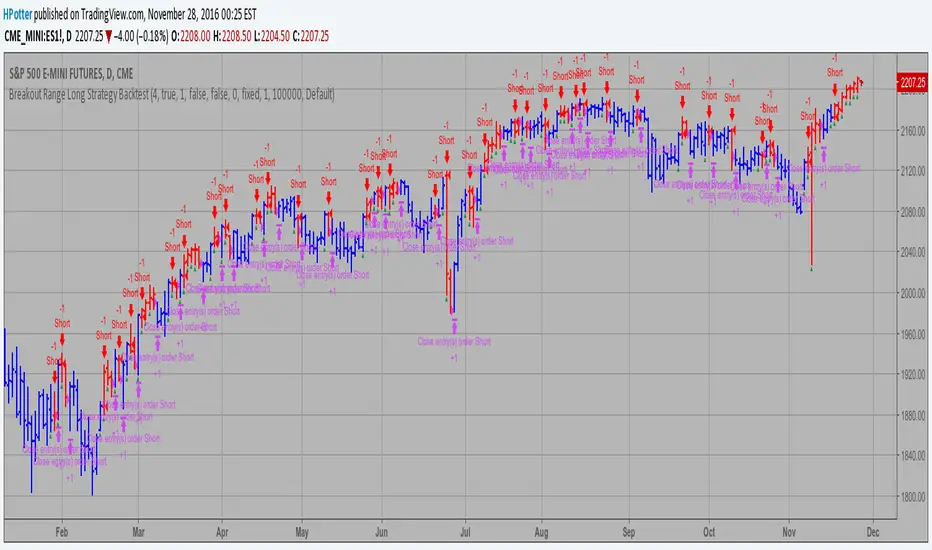

Breakout Range Long Strategy Backtest Breakout Range Long Strategy

You can change long to short in the Input Settings

Please, use it only for learning or paper trading. Do not for real trading.

Bill Williams. Awesome Oscillator (AC) Strategy Backtest This indicator plots the oscillator as a histogram where blue denotes

periods suited for buying and red . for selling. If the current value

of AO (Awesome Oscillator) is above previous, the period is considered

suited for buying and the period is marked blue. If the AO value is not

above previous, the period is considered suited for selling and the

indicator marks it as red.

You can make changes in the property for set calculating strategy MA, EMA, WMA

Please, use it only for learning or paper trading. Do not for real trading.

Bandpass Filter Reversed Strategy BacktestThe related article is copyrighted material from

Stocks & Commodities Mar 2010

You can use in the xPrice any series: Open, High, Low, Close, HL2, HLC3, OHLC4 and ect...

Please, use it only for learning or paper trading. Do not for real trading.

Average True Range Reversed Strategy Average True Range Trailing Stops Strategy, by Sylvain Vervoort

The related article is copyrighted material from Stocks & Commodities Jun 2009

Please, use it only for learning or paper trading. Do not for real trading.

3-Bar-Reversal-Pattern Strategy Backtest This startegy based on 3-day pattern reversal described in "Are Three-Bar

Patterns Reliable For Stocks" article by Thomas Bulkowski, presented in

January, 2000 issue of Stocks&Commodities magazine.

That pattern conforms to the following rules:

- It uses daily prices, not intraday or weekly prices;

- The middle day of the three-day pattern has the lowest low of the three days, with no ties allowed;

- The last day must have a close above the prior day's high, with no ties allowed;

- Each day must have a nonzero trading range.

Please, use it only for learning or paper trading. Do not for real trading.

2/20 Exponential Moving Average StrategyThis indicator plots 2/20 exponential moving average. For the Mov

Avg X 2/20 Indicator, the EMA bar will be painted when the Alert criteria is met.

Please, use it only for learning or paper trading. Do not for real trading.

MACD, backtest 2015+ only, cut in half and doubledThis is only a slight modification to the existing "MACD Strategy" strategy plugin!

found the default MACD strategy to be lacking, although impressive for its simplicity. I added "year>2014" to the IF buy/sell conditions so it will only backtest from 2015 and beyond ** .

I also had a problem with the standard MACD trading late, per se. To that end I modified the inputs for fast/slow/signal to double. Example: my defaults are 10, 21, 10 so I put 20, 42, 20 in. This has the effect of making a 30min interval the same as 1 hour at 10,21,10. So if you want to backtest at 4hr, you would set your time interval to 2hr on the main chart. This is a handy way to make shorter time periods more useful even regardless of strategy/testing, since you can view 15min with alot less noise but a better response.

Used on BTCCNY OKcoin, with the chart set at 45 min (so really 90min in the strategy) this gave me a percent profitable of 42% and a profit factor of 1.998 on 189 trades.

Personally, I like to set the length/signals to 30,63,30. Meaning you need to triple the time, it allows for much better use of shorter time periods and the backtests are remarkably profitable. (i.e. 15min chart view = 45min on script, 30min= 1.5hr on script)

** If you want more specific time periods you need to try plugging in different bar values: replace "year" with "n" and "2014" with "5500". The bars are based on unix time I believe so you will need to play around with the number for n, with n being the numbers of bars.