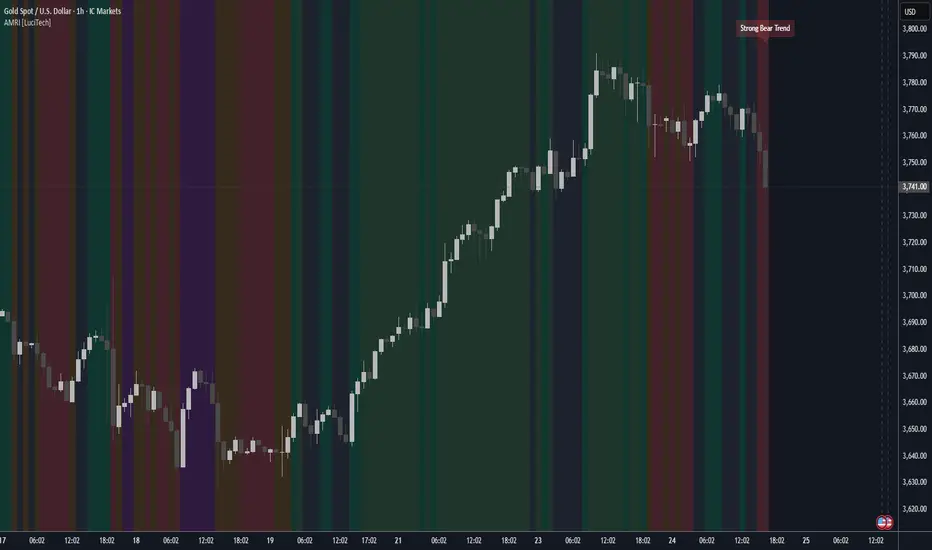

Regime Switching [Pointalgo]Regime Switching

Regime Switching is a market condition classifier designed to automatically detect whether price is in a Trending, Ranging (Mean Reversion), or Neutral/Noise environment.

Instead of applying one strategy to all conditions, this script adapts its visual tools and signals based on the detected regime.

How It Works:

1. ADX (Trend Strength)

Measures directional strength. Higher values indicate stronger trends.

2. Efficiency Ratio (Kaufman Concept)

Compares net price movement to total movement.

High efficiency → directional move

Low efficiency → choppy movement

Using these two inputs, the script classifies the market into:

TRENDING → Strong ADX + Efficient movement

RANGING → Weak ADX + Inefficient movement

NOISE → Transitional / unclear conditions

Adaptive Visual System:

The indicator automatically switches tools depending on the regime:

Trending Mode

Displays Donchian Channel (20-period highs/lows)

Highlights breakout conditions

Green background shading

Ranging Mode

Displays Bollinger Bands (20, 2 standard deviations)

Highlights fade/reversal conditions

Blue background shading

Noise Mode

1.Neutral background

2.No active channel emphasis

Signal Logic:

Breakout above previous Donchian high

Breakdown below previous Donchian low

Range Mode:

Buy when price crosses above lower Bollinger Band

Sell when price crosses below upper Bollinger Band

Signals are informational and intended for study and research.

Dashboard:

The built-in table shows:

1. Current detected regime

2. Efficiency value

3. State color coding

This allows quick interpretation of market condition at a glance.

Disclaimer:

This script is for educational and research purposes only.

It does not constitute financial advice or a trading recommendation.

Always test and validate strategies before live trading.

Pine Script® インジケーター