Mean Reversion Mirror📌 Mean Reversion Mirror — Multi‑Level Mean Reversion Strategy

Mean Reversion Mirror is an advanced modular mean‑reversion strategy built around dynamic and static deviation levels from a moving average.

The strategy automatically scales into positions across six levels (LONG and SHORT), using both dynamic MA‑based deviation levels and static levels that lock in after entry.

🔍 Core Concept

Price tends to revert toward its mean.

This strategy exploits that behavior by opening an initial base entry at the first deviation and adding positions as the imbalance grows.

Each additional level improves the average entry price and increases the probability of exiting profitably.

⚙️ Key Features

📈 Six Dynamic Deviation Levels

Levels are calculated as percentage deviations from a selected MA (WMA, SMA, EMA, RMA, HMA).

This makes the strategy adaptive to volatility and market structure.

📉 Six Static Levels

Once triggered, each level becomes fixed and no longer changes.

This creates a stable averaging grid independent of future MA movement.

🎯 Flexible Take‑Profit System

fixed take‑profit

or trailing take‑profit with dynamic offset

🖐 Manual Entry Support

You can manually set a price for LONG or SHORT, and the strategy will execute the base entry automatically.

📊 Rich Visualization

dynamic deviation levels

static levels

dotted “last chance” levels

average position price

take‑profit line

compact mini‑table with key position metrics

📦 Two Operating Modes

STK Mode — fixed unit size

Classic Mode — quantity calculated from USD value

🧠 Entry Logic

The strategy uses sequences B1–B6 (LONG) and S1–S6 (SHORT):

B1/S1 — base entry

B2–B6 / S2–S6 — averaging entries as deviation increases

L6/S6 — “last chance” level with its own size

Each level activates only after the previous one.

📌 Who This Strategy Is For

mean‑reversion traders

grid/averaging system users

pullback‑based investors

traders who want clear visual levels

users who prefer manual control over entry points

⚠️ Disclaimer

This strategy is not financial advice.

Always backtest and adjust parameters according to your risk tolerance before using it in live markets.

Martingale

Trade Manager + MOST RSI📌 Trade Manager + MOST RSI — Adaptive Position Management Strategy

Overview

This strategy combines the MOST‑RSI trend‑reversal model with a fully customizable position management system.

It is designed for traders who want a flexible, visual, and systematic approach to scaling into positions, managing risk, and automating exits.

The script supports both automatic entries (based on MOST‑RSI signals) and manual entries (user‑defined price levels), making it suitable for hybrid discretionary + algorithmic trading.

✨ Key Features

MOST‑RSI Entry Logic

Adaptive RSI‑based trend detection

VAR‑smoothed moving average

Automatic LONG/SHORT signal generation

Configurable sensitivity through MOST Percent, MA Type, and RSI Length

Smart Position Management

Initial order + cascading Safety Orders (SO)

Adjustable deviation, step scaling, and volume scaling

Independent LONG and SHORT deviation settings

Breakeven after N safety orders

Automatic TP placement based on average entry price

Clean Visual Structure

TP lines visible only when a position is open

NEXT SO level with dynamic labeling

Average price line with subtle styling

Transparent background zones for TP, SO, and AVG

Real‑time mini‑table showing position metrics

Manual Entry Mode

Set custom LONG/SHORT entry levels

Automatic line drawing

One‑click reset

Perfect for discretionary setups

📊 Recommended Timeframes

1H — balanced

4H — conservative

MOST‑RSI adapts well across different market conditions.

🔧 Optimization Recommendations

1. Deviation (%)

Trending markets: 4–7%

Ranging markets: 2–3%

Optimize LONG and SHORT separately

2. Safety Order Volume Scale

Typical range: 1.3–1.6

Higher = faster averaging, higher risk

3. Safety Order Step Scale

1.4–1.7 for safer spacing

1.1–1.3 for tighter spacing

4. Take‑Profit

Volatile assets: 2–5%

Stable assets: 1.5–2%

5. Risk Management

Max SO: 5–10 depending on volatility

More SO = safer but more capital required

6. MOST‑RSI Parameters

RSI Length: 14

MA Length: 5

MOST Percent: 7–12%

7. Backtesting

Use at least 1 year of data

Include high‑volatility periods

8. Drawdown Control

If drawdown is too high:

Lower SO volume scale

Reduce max SO

Increase SO step scale

📌 Disclaimer

This script does not guarantee profits and is not financial advice.

Always test strategies on historical data and use proper risk management.

Trade Manager + DivergenceTrade Manager + Divergence — Smart Entry & Automated Risk Control

Trade Manager + Divergence is a versatile trading strategy that combines automated RSI divergence detection, manual level entries, and a multi‑layered safety‑order system with advanced risk management.

It is designed for traders who want precise technical entries supported by fully automated position handling.

🔍 Key Features

1. RSI Divergence Entry Module

The strategy automatically detects:

Bullish divergence (Higher Low on RSI + Lower Low on price)

Bearish divergence (Lower High on RSI + Higher High on price)

Additional options include:

Divergence strength filtering

MA200 trend filter

Visual divergence markers on the chart

2. Manual Entry Levels

You can define:

A manual LONG entry price

A manual SHORT entry price

Automatic removal of the level after entry

Perfect for traders who prefer to work from key zones they identify themselves.

3. Multi‑Level Safety Order System

The strategy supports:

Initial base order

Up to 8 safety orders

Volume scaling

Step scaling

All parameters are fully customizable:

Order size

Distance between orders

Scaling coefficients

Maximum number of safety orders

4. Automated Take Profit

Take profit is calculated from the average position price:

Separate TP settings for LONG and SHORT

TP levels displayed directly on the chart

5. Breakeven Mechanism

After a specified number of safety orders, the strategy can:

Automatically close the position at breakeven

Include exchange fees in the calculation

6. Mini Status Panel

A compact table in the top‑right corner shows:

Position size

Position value

Number of open trades

Current PnL

Equity

This makes monitoring your position simple and intuitive.

⚙️ Clean and Organized Settings

All inputs are grouped into clear sections:

General

Entry Mode

Divergence Settings

Manual Levels

Risk Management

Each parameter includes a tooltip explaining its purpose.

📌 Disclaimer

This script does not guarantee profits and is not financial advice.

Always test strategies on historical data and use proper risk management.

Dips Oleg Adaptive Dip‑Buying Strategy with Lot Precision & Smart Averaging

📘 Description

This strategy is a personalized adaptation of an idea originally developed by the respected author fullmax.

I reworked the concept to suit my own trading approach, adding lot‑precision rounding to avoid exchange quantity errors when using webhooks, and enhancing the visual and analytical components of the script.

🔧 What’s New in This Version

Configurable lot precision to ensure clean, exchange‑safe order sizes

Improved UI elements: base‑order labels, compact mini‑table, grouped settings

Dynamic safety‑order pricing based on price drops and scaling factors

Flexible date‑range filtering for controlled backtesting

Clear visualization of SMA threshold, safety levels, breakeven, and take‑profit

Adaptive threshold logic that adjusts depending on trend conditions

🎯 Core Logic

The strategy monitors how far price deviates from a short‑term SMA.

When the deviation crosses a user‑defined threshold, the script opens a base position.

If price continues to dip, the system deploys safety orders with:

scalable volume

scalable distance

precise rounding for compatibility with webhook automation

Once the position is built, the strategy manages exits using a fixed take‑profit target.

A breakeven reference line and auto‑cleanup logic help maintain clarity and prevent stale orders.

⚙️ Feature Overview

Dip‑based entry logic with bull/bear threshold switching

Safety orders with volume and step scaling

Take‑profit management

Breakeven visualization

Mini‑table showing real‑time position metrics

Clean chart overlays for easier interpretation

📝 Disclaimer

This script is intended for educational and analytical use.

It does not guarantee profits and should be tested thoroughly before being used in live trading.

RSI + martingaleТорговая стратегия основанная на совмещении торговой системы Мартингейл и индекса относительной сила RSI.

Скрипт входит в сделку после пересечения заданных уровней перекупленности и перепроданности RSI. Набирает позицию, по умолчанию умнажая размер каждой докупки x2. Закрывается по тейк-профиту.

A trading strategy based on combining the Martingale trading system and the Relative Strength Index (RSI).

The script enters the trade after crossing the set overbought and oversold levels of the RSI. It takes a position, by default multiplying the size of each additional purchase by x2. It closes with a take profit.

Martingale Strategy Simulator [BackQuant]Martingale Strategy Simulator

Purpose

This indicator lets you study how a martingale-style position sizing rule interacts with a simple long or short trading signal. It computes an equity curve from bar-to-bar returns, adapts position size after losing streaks, caps exposure at a user limit, and summarizes risk with portfolio metrics. An optional Monte Carlo module projects possible future equity paths from your realized daily returns.

What a martingale is

A martingale sizing rule increases stake after losses and resets after a win. In its classical form from gambling, you double the bet after each loss so that a single win recovers all prior losses plus one unit of profit. In markets there is no fixed “even-money” payout and returns are multiplicative, so an exact recovery guarantee does not exist. The core idea is unchanged:

Lose one leg → increase next position size

Lose again → increase again

Win → reset to the base size

The expectation of your strategy still depends on the signal’s edge. Sizing does not create positive expectancy on its own. A martingale raises variance and tail risk by concentrating more capital as a losing streak develops.

What it plots

Equity – simulated portfolio equity including compounding

Buy & Hold – equity from holding the chart symbol for context

Optional helpers – last trade outcome, current streak length, current allocation fraction

Optional diagnostics – daily portfolio return, rolling drawdown, metrics table

Optional Monte Carlo probability cone – p5, p16, p50, p84, p95 aggregate bands

Model assumptions

Bar-close execution with no slippage or commissions

Shorting allowed and frictionless

No margin interest, borrow fees, or position limits

No intrabar moves or gaps within a bar (returns are close-to-close)

Sizing applies to equity fraction only and is capped by your setting

All results are hypothetical and for education only.

How the simulator applies it

1) Directional signal

You pick a simple directional rule that produces +1 for long or −1 for short each bar. Options include 100 HMA slope, RSI above or below 50, EMA or SMA crosses, CCI and other oscillators, ATR move, BB basis, and more. The stance is evaluated bar by bar. When the stance flips, the current trade ends and the next one starts.

2) Sizing after losses and wins

Position size is a fraction of equity:

Initial allocation – the starting fraction, for example 0.15 means 15 percent of equity

Increase after loss – multiply the next allocation by your factor after a losing leg, for example 2.00 to double

Reset after win – return to the initial allocation

Max allocation cap – hard ceiling to prevent runaway growth

At a high level the size after k consecutive losses is

alloc(k) = min( cap , base × factor^k ) .

In practice the simulator changes size only when a leg ends and its PnL is known.

3) Equity update

Let r_t = close_t / close_{t-1} − 1 be the symbol’s bar return, d_{t−1} ∈ {+1, −1} the prior bar stance, and a_{t−1} the prior bar allocation fraction. The simulator compounds:

eq_t = eq_{t−1} × (1 + a_{t−1} × d_{t−1} × r_t) .

This is bar-based and avoids intrabar lookahead. Costs, slippage, and borrowing costs are not modeled.

Why traders experiment with martingale sizing

Mean-reversion contexts – if the signal often snaps back after a string of losses, adding size near the tail of a move can pull the average entry closer to the turn

Behavioral or microstructure edges – some rules have modest edge but frequent small whipsaws; size escalation may shorten time-to-recovery when the edge manifests

Exploration and stress testing – studying the relationship between streaks, caps, and drawdowns is instructive even if you do not deploy martingale sizing live

Why martingale is dangerous

Martingale concentrates capital when the strategy is performing worst. The main risks are structural, not cosmetic:

Loss streaks are inevitable – even with a 55 percent win rate you should expect multi-loss runs. The probability of at least one k-loss streak in N trades rises quickly with N.

Size explodes geometrically – with factor 2.0 and base 10 percent, the sequence is 10, 20, 40, 80, 100 (capped) after five losses. Without a strict cap, required size becomes infeasible.

No fixed payout – in gambling, one win at even odds resets PnL. In markets, there is no guaranteed bounce nor fixed profit multiple. Trends can extend and gaps can skip levels.

Correlation of losses – losses cluster in trends and in volatility bursts. A martingale tends to be largest just when volatility is highest.

Margin and liquidity constraints – leverage limits, margin calls, position limits, and widening spreads can force liquidation before a mean reversion occurs.

Fat tails and regime shifts – assumptions of independent, Gaussian returns can understate tail risk. Structural breaks can keep the signal wrong for much longer than expected.

The simulator exposes these dynamics in the equity curve, Max Drawdown, VaR and CVaR, and via Monte Carlo sketches of forward uncertainty.

Interpreting losing streaks with numbers

A rough intuition: if your per-trade win probability is p and loss probability is q=1−p , the chance of a specific run of k consecutive losses is q^k . Over many trades, the chance that at least one k-loss run occurs grows with the number of opportunities. As a sanity check:

If p=0.55 , then q=0.45 . A 6-loss run has probability q^6 ≈ 0.008 on any six-trade window. Across hundreds of trades, a 6 to 8-loss run is not rare.

If your size factor is 1.5 and your base is 10 percent, after 8 losses the requested size is 10% × 1.5^8 ≈ 25.6% . With factor 2.0 it would try to be 10% × 2^8 = 256% but your cap will stop it. The equity curve will still wear the compounded drawdown from the sequence that led to the cap.

This is why the cap setting is central. It does not remove tail risk, but it prevents the sizing rule from demanding impossible positions

Note: The p and q math is illustrative. In live data the win rate and distribution can drift over time, so real streaks can be longer or shorter than the simple q^k intuition suggests..

Using the simulator productively

Parameter studies

Start with conservative settings. Increase one element at a time and watch how the equity, Max Drawdown, and CVaR respond.

Initial allocation – lower base reduces volatility and drawdowns across the board

Increase factor – set modestly above 1.0 if you want the effect at all; doubling is aggressive

Max cap – the most important brake; many users keep it between 20 and 50 percent

Signal selection

Keep sizing fixed and rotate signals to see how streak patterns differ. Trend-following signals tend to produce long wrong-way streaks in choppy ranges. Mean-reversion signals do the opposite. Martingale sizing interacts very differently with each.

Diagnostics to watch

Use the built-in metrics to quantify risk:

Max Drawdown – worst peak-to-trough equity loss

Sharpe and Sortino – volatility and downside-adjusted return

VaR 95 percent and CVaR – tail risk measures from the realized distribution

Alpha and Beta – relationship to your chosen benchmark

If you would like to check out the original performance metrics script with multiple assets with a better explanation on all metrics please see

Monte Carlo exploration

When enabled, the forecast draws many synthetic paths from your realized daily returns:

Choose a horizon and a number of runs

Review the bands: p5 to p95 for a wide risk envelope; p16 to p84 for a narrower range; p50 as the median path

Use the table to read the expected return over the horizon and the tail outcomes

Remember it is a sketch based on your recent distribution, not a predictor

Concrete examples

Example A: Modest martingale

Base 10 percent, factor 1.25, cap 40 percent, RSI>50 signal. You will see small escalations on 2 to 4 loss runs and frequent resets. The equity curve usually remains smooth unless the signal enters a prolonged wrong-way regime. Max DD may rise moderately versus fixed sizing.

Example B: Aggressive martingale

Base 15 percent, factor 2.0, cap 60 percent, EMA cross signal. The curve can look stellar during favorable regimes, then a single extended streak pushes allocation to the cap, and a few more losses drive deep drawdown. CVaR and Max DD jump sharply. This is a textbook case of high tail risk.

Strengths

Bar-by-bar, transparent computation of equity from stance and size

Explicit handling of wins, losses, streaks, and caps

Portable signal inputs so you can A–B test ideas quickly

Risk diagnostics and forward uncertainty visualization in one place

Example, Rolling Max Drawdown

Limitations and important notes

Martingale sizing can escalate drawdowns rapidly. The cap limits position size but not the possibility of extended adverse runs.

No commissions, slippage, margin interest, borrow costs, or liquidity limits are modeled.

Signals are evaluated on closes. Real execution and fills will differ.

Monte Carlo assumes independent draws from your recent return distribution. Markets often have serial correlation, fat tails, and regime changes.

All results are hypothetical. Use this as an educational tool, not a production risk engine.

Practical tips

Prefer gentle factors such as 1.1 to 1.3. Doubling is usually excessive outside of toy examples.

Keep a strict cap. Many users cap between 20 and 40 percent of equity per leg.

Stress test with different start dates and subperiods. Long flat or trending regimes are where martingale weaknesses appear.

Compare to an anti-martingale (increase after wins, cut after losses) to understand the other side of the trade-off.

If you deploy sizing live, add external guardrails such as a daily loss cut, volatility filters, and a global max drawdown stop.

Settings recap

Backtest start date and initial capital

Initial allocation, increase-after-loss factor, max allocation cap

Signal source selector

Trading days per year and risk-free rate

Benchmark symbol for Alpha and Beta

UI toggles for equity, buy and hold, labels, metrics, PnL, and drawdown

Monte Carlo controls for enable, runs, horizon, and result table

Final thoughts

A martingale is not a free lunch. It is a way to tilt capital allocation toward losing streaks. If the signal has a real edge and mean reversion is common, careful and capped escalation can reduce time-to-recovery. If the signal lacks edge or regimes shift, the same rule can magnify losses at the worst possible moment. This simulator makes those trade-offs visible so you can calibrate parameters, understand tail risk, and decide whether the approach belongs anywhere in your research workflow.

EMA Grid + Martingale Strategy (Long-Only) with CooldownTitle:

EMA Grid + Martingale Strategy (Long-Only) with Cooldown

Short Summary:

A long-only strategy combining EMA trend filters, grid-based entries, optional martingale sizing, and a cooldown feature to manage position timing and exits.

Full Description:

This strategy uses a 4-EMA trend confirmation system to detect bullish momentum, then deploys a grid-style entry method with optional martingale position sizing. It includes a cooldown mechanism to prevent reentry too soon after a completed trade cycle.

How It Works

1. Trend Confirmation: Two EMA groups (fast/slow) determine whether market conditions are bullish.

2. Initial Entry: A new position is entered when both EMA groups confirm an uptrend and no position is currently active.

3. Grid Entries: Additional long entries are placed when price drops by a defined pip distance from the last entry, respecting the maximum number of entries.

4. Martingale Sizing (Optional): Grid orders can increase in size with each level using a customizable multiplier.

5. Weighted-Average Exit: All positions close once price reaches or exceeds the average entry price plus a buffer.

6. Cooldown Timer: After closing a position set, the strategy waits a defined number of bars before opening a new grid.

Key Features

• 4 customizable EMAs for trend confirmation.

• Dynamic grid-style long entries based on pip intervals.

• Optional martingale-style position sizing.

• Weighted-average price exit logic with buffer control.

• Cooldown bar period to limit overtrading.

• Suitable for optimization and backtesting with full control over inputs.

Use Cases

• Designed for trending markets where pullbacks present entry opportunities.

• Helps manage staged entries while avoiding premature reentry.

• Ideal for testing martingale and grid-based strategies with exit precision.

Note: This strategy is for testing and educational purposes only. It does not guarantee profits and is not financial advice.

EMA Grid + Martingale Indicator (Long-Only)Title:

EMA Grid + Martingale Indicator (Long-Only)

Short Summary:

A 4-EMA trend filter combined with a grid-based entry system and optional martingale sizing to visualize staged long entries and exits in bullish markets.

Full Description:

This indicator combines a 4-EMA trend filter with a grid-based entry system and optional martingale-style position sizing to help traders visualize staged long entries and exits in trending markets.

How It Works

1. Trend Detection: Uses two sets of EMAs (fast/slow pairs) to confirm bullish momentum. A long signal is generated when both EMA groups align in an uptrend.

2. Grid Entries: After the initial long entry, additional grid levels are triggered every time price drops by the specified grid step (in pips).

3. Martingale Sizing (Optional): Each subsequent entry can increase in size based on the defined martingale factor.

4. Weighted-Average Exit: Calculates the weighted average of all grid entries and signals an exit when the price reaches or surpasses this level plus an optional buffer.

Key Features

• 4 EMA Trend Filter with fully customizable lengths.

• Dynamic grid entries with visual labels (L1, L2, etc.).

• Optional martingale position sizing.

• Weighted-average exit with adjustable buffer.

• Customizable parameters for EMAs, grid steps, max entries, and buffer pips.

• Clear chart visualization of EMAs and entry/exit levels.

Use Cases

• For traders using cost-averaging or grid strategies in bullish markets.

• Visualizes multiple entry levels and profit targets.

• Useful for backtesting and strategy planning.

Note: This indicator is for visualization and planning purposes only. It does not execute trades automatically. It does not guarantee profits and is not financial advice.

Buysell Martingale Signal - CustomBuysell Martingale Signal - Custom Indicator

Introduction:

This indicator provides a dynamic buy and sell signal system incorporating an adaptive Martingale logic. Built upon the signalLib_yashgode9/2 library, it is designed for use across various markets and timeframes.

Key Features:

Primary Buy & Sell Signals: Identifies initial buy and sell opportunities based on directional changes derived from the signalLib.

Martingale Signals:

For Short (Sell) Positions: A Martingale Sell signal is triggered when the price moves against the existing short position by a specified stepPercent from the last entry price, indicating a potential opportunity to average down or increase position size.

For Long (Buy) Positions: Similarly, a Martingale Buy signal is triggered when the price moves against the existing long position by a stepPercent from the last entry price.

On-Chart Labels: Displays clear, customizable labels on the chart for primary Buy, Sell, Martingale Buy, and Martingale Sell signals.

Customizable Colors: Allows users to set distinct colors for primary signals and Martingale signals for better visual distinction.

Adjustable Sensitivity: Features configurable parameters (DEPTH_ENGINE, DEVIATION_ENGINE, BACKSTEP_ENGINE) to fine-tune the sensitivity of the underlying signal generation.

Webhook Support (Static Message Alerts): This indicator provides alerts with static messages for both primary and Martingale buy/sell signals. These alerts can be leveraged for automation by external systems (such as trading bots or exchange-provided Webhook Signal Trading services).

Important Note: When using these alerts for automation, an external system is required to handle the complex Martingale logic and position management (e.g., tracking steps, PnL calculation, hedging, dynamic quantity sizing), as this indicator solely focuses on signal generation and sending predefined messages.

How to Use:

Add the indicator to your desired chart.

Adjust the input parameters in the indicator's settings to match your specific trading symbol and timeframe.

For automation, you can set up TradingView alerts for the Buy Signal (Main/Martingale) and Sell Signal (Main/Martingale) conditions, pointing them to your preferred Webhook URL.

Configurable Parameters:

DEPTH_ENGINE: (e.g., 30) Controls the depth of analysis for the signal algorithm.

DEVIATION_ENGINE: (e.g., 5) Defines the allowable deviation for signal generation.

BACKSTEP_ENGINE: (e.g., 5) Specifies the number of historical bars to look back.

Martingale Step Percent: (e.g., 0.5) The percentage price movement against the current position that triggers a Martingale signal.

Labels Transparency: Adjusts the transparency of the on-chart signal labels.

Buy-Color / Sell-Color: Sets the color for primary Buy and Sell signal labels.

Martingale Buy-Color / Martingale Sell-Color: Sets the color for Martingale Buy and Sell signal labels.

Label size: Controls the visual size of the labels.

Label Offset: Adjusts the vertical offset of the labels from the candlesticks.

Risk Warning:

Financial trading inherently carries significant risk. Martingale strategies are particularly high-risk and can lead to substantial losses or even complete liquidation of capital if the market moves strongly and persistently against your position. Always backtest thoroughly and practice with a demo account, fully understanding the associated risks, before engaging with real capital.

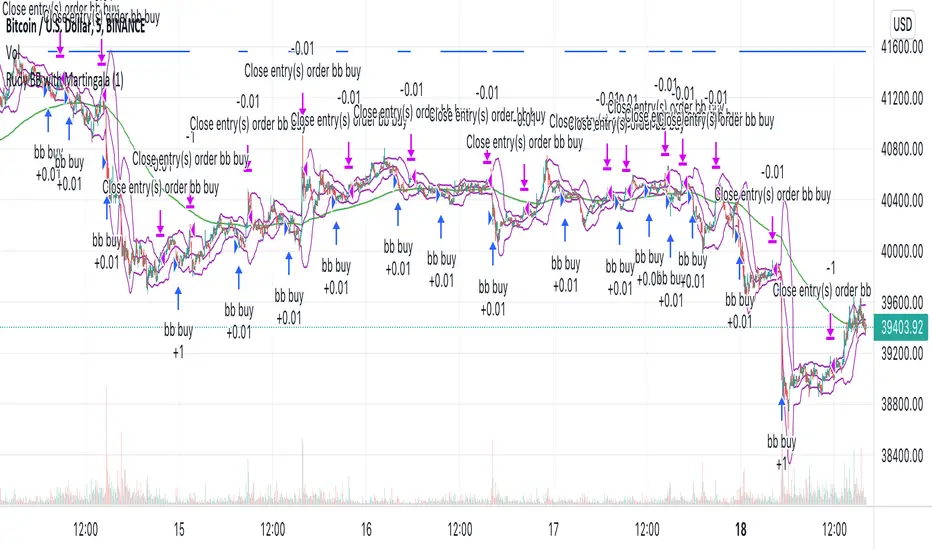

Rudy's BB with MartingaleMy first strategy script that uses Bollinger Bands and Martingale to increase contract size after negative profit.

Loft Strategy V4This strategy is an advanced version of the Loft Strategy V1, I shared earlier. (Loft Strategy V1 consists of a kalman filter (by alexgrover ) and a "stop and reverse" line which is following and the kalman filter. If the price goes in the same direction as the position side, the "stop and reverse" line approaches the kalman filter as set on the "Approach Decrease Step" parameter.)

In addition to the previous version, it includes a martingale like deviation and multiple take-profit.

Here it is some parameters definitions of the strategy:

Kalman Filter: The higher this parameter, the faster and more aggressive the filter. Otherwise the filter goes very smoothly

Beginning Approach: First approximation as a percentage of stop-n-reverse line

Final Approach: Minimum approximation of stop-n-reverse line

Approach Decrease Step: If the price moves in the same direction as the strategy, the approach percentage is reduced by this parameter. Otherwise nothing do

Base Order Quantity: Initial capital of position

Max Safe Order Attempt: This parameter determines the maximum number of times the strategy will raise the bet after losing in a row.

Safe Order Deviation: if the last trade is loss, multiply the bet by this parameter (aka. martingale factor)

Profit Deviation: if last trade in loss, multiply the take-profit points

Max Order Quantity: Maximum capital allowed for a position

TP1, TP2, TP3 : Take profit spots in percentage

QT1, QT2, QT3: Amount of take-profit spots

Stop Loss: Maximum stop loss allowed for a trade

Long Entry, Short Entry: Only long side, only short side or both side

Safe Stop After TP2: If the price reaches the TP2 point, move the stop-loss point to the entry price.

Safe Stop After TP1: If the price reaches TP1, move the stop-loss point to the stop-n-reverse line.

Alferow_pnl_up_shortThis script allows you to determine the leverage required to enter one position based on the set entry price, the price of the expected take profit, stop loss and risk per transaction. It also allows you to schedule this transaction for 5 possible transactions, with different shoulders and a martingale coefficient for each subsequent gain at the same risk, allowing you to qualitatively improve the pnl of the transaction with price fluctuations after entering the transaction. The script is designed for short positions.

Alferow_pnl_up_longThis script allows you to determine the leverage required to enter one position based on the set entry price, the price of the expected take profit, stop loss and risk per transaction. It also allows you to schedule this transaction for 5 possible transactions, with different shoulders and a martingale coefficient for each subsequent gain at the same risk, allowing you to qualitatively improve the pnl of the transaction with price fluctuations after entering the transaction. The script is designed for long positions.

Martingale TemplateA template example on how to apply the famous Martingale gambling strategy. When your strategy gets an exit signal for your long position that leaves you without profit, you re-enter on the next entry long condition with double the capital of the previous amount entered with. You keep doubling the amount of capital entered with until you finally exit with a profit. If the strategy isn't sound enough then it could take several attempts and it can take only as much as a dozen tries to eat away at all your capital as the capital required to double on the next entry increases greatly over time by consecutive products of 2.

The strategy used is just a simple moving average crossover, above the moving average is going long, below the moving average is going short. It can be replaced with whatever strategy that you want. The colored vertical bars show long and short positions and exits. The default option on the tick box under the settings show the number of attempts at entering before finally exiting with a profit, the other option shows the amount of capital it took starting from 1.

Grid System With Fake MartingaleThe proposed strategy is based on a grid system with a money management that tries to replicate the effect of a martingale without having to double your position size after each loss, hence the name "fake martingale". Note that a balance using this strategy is still subject to exponential decay, the risk is not minimized, as such, it would be dangerous to use this strategy.

For more information on the martingale and grid systems see:

Strategy Settings

Point determines the "grid" size and should be adjusted accordingly to the scale of the security you are applying the strategy to. Higher value would require larger price movements in order to trigger a trade, generating fewer trades as a result.

The order size determines the number of contracts/shares to purchase.

The martingale multiplier determines the factor by which the position size is multiplied after a loss, using values higher to 2 will "squarify" your balance, while a value of 1 would use a constant position sizing.

Finally, the anti-martingale parameter determines whether the strategy uses a reverse martingale or not, if set to true then the position size is multiplied after each win.

How It Works

Let's illustrate how we replicate a martingale without doubling our exposure with a simple casino example. Imagine you are playing roulette, and that you are betting on colors (black/red), your payout is 1 to 1, in the case you win, you will have your initial stake back plus a profit equal to your initial stake.

If your strategy is to recover any previous losses, you can double your stake each time you lose, once you win you will get back the previous losses plus a profit equal to your original stake, this is the martingale system. So how can we win back previous losses without having to double our stake? We could do that by doubling the payout ratio after a loss, so after a loss, we must use a payout ratio of 2:1, if we lose once again we must use a payout of 4:1...etc, our payout ratio would be subject to exponential growth instead of our stake.

Of course, the payout ratio is fixed with casino games, but in trading, we can manipulate the position of our take profit in order to replicate such effect, this is what this strategy is doing. So after a loss, we place our take profit such that a win recover our losses back plus generate a profit.

Advantages

The advantage of this approach is that unlike the martingale we don't double our position size, which instead can remain constant, this is a huge advantage as a martingale will require a significant capital in order to tank a series of losses.

Disadvantages

The main disadvantage of this method is that the price might never reach our take profit after a long losing streak, our balance would remain in the red and we couldn't do anything about it except reset the strategy.

Frictional costs are still a disadvantage, as such, we would need to place our take profits in order to account for them, while this is still better than purchasing additional shares, it minimizes the chances of the price reaching the take profit.

Conclusions

An alternative money management system replicating the effect of a martingale as been presented, we can see that such a system is far from being perfect, and it would be foolish to use it, however, it stills offer a convenient alternative to less aggressive progressive position sizing systems.

I have been receiving some messages from users criticizing me for exposing the martingale money management system, and I understand why but I can't agree, talking about it allow me to warn users against it, the grid-martingale methodology is will create more harm than anything else, the reward is only one side of the story and should always be compared against the risk, so always take a look at all the statics in a backtest.

Thanks for reading!

Shout-Out

This post was made possible thanks to my patrons:

@Happymono, @AmariMars, @kkhaial, @Nugehe, @LucF, @Nosmok, @iflostio, @DankBeans, @ecletv, @Neverstorm, @alex.crown.jr, @uk503, @xkingshotss, @vsov, @jbelka, @yatrader2, @hughza, @ganh

Grid Like StrategyIt is possible to use progressive position sizing in order to recover from past losses, a well-known position sizing system being the "martingale", which consists of doubling your position size after a loss, this allows you to recover any previous losses in a losing streak + winning an extra. This system has seen a lot of attention from the trading community (mostly from beginners), and many strategies have been designed around the martingale, one of them being "grid trading strategies".

While such strategies often shows promising results on paper, they are often subjects to many frictions during live trading that makes them totally unusable and dangerous to the trader. The motivations behind posting such a strategy isn't to glorify such systems, but rather to present the problems behind them, many users come to me with their ideas and glorious ways to make money, sometimes they present strategies using the martingale, and it is important to present the flaws of this methodology rather than blindly saying "you shouldn't use it".

Strategy Settings

Point determines the "grid" size and should be adjusted accordingly to the scale of the symbol you are applying the strategy to. Higher value would require larger price movements in order to trigger a trade, as such higher values will generate fewer trades.

The order size determines the number of contracts/shares to purchase.

The martingale multiplier determines the factor by which the position size is multiplied after a loss, using values higher to 2 will "squarify" your balance, while a value of 1 would use a constant position sizing.

Finally, the anti-martingale parameter determines whether the strategy uses a reverse martingale or not, if set to true then the position size is multiplied after any wins.

The Grid

Grid strategies are commons and do not present huge problems until we use certain position sizing methods such as the martingale. A martingale is extremely sensitive to any kind of friction (frictional costs, slippage...etc), the grid strategy aims to provide a stable and simple environment where a martingale might possibly behave well.

The goal of a simple grid strategy is to go long once the price crossover a certain level, a take profit is set at the level above the current one and stop loss is placed at the level below the current one, in a winning scenario the price reach the take profit, the position is closed and a new one is opened with the same setup. In a losing scenario, the price reaches the stop loss level, the position is closed and a short one is opened, the take profit is set at the level below the current one, and a stop loss is set at the level above the current one. Note that all levels are equally spaced.

It follows from this strategy that wins and losses should be constant over time, as such our balance would evolve in a linear fashion. This is a great setup for a martingale, as we are theoretically assured to recover all the looses in a losing streak.

Martingale - Exponential Decays - Risk/Reward

By using a martingale we double our position size (exposure) each time we lose a trade, if we look at our balance when using a martingale we see significant drawdowns, with our balance peaking down significantly. The martingale sequence is subject to exponential growth, as such using a martingale makes our balance exposed to exponential decays, that's really bad, we could basically lose all the initially invested capital in a short amount of time, it follows from this that the theoretical success of a martingale is determined by what is the maximum losing streak you can endure

Now consider how a martingale affects our risk-reward ratio, assuming unity position sizing our martingale sequence can be described by 2^(x-1) , using this formula we would get the amount of shares/contracts we need to purchase at the x trade of a losing streak, we would need to purchase 256 contracts in order to recover from a losing streak of size 9, this is enormous when you take into account that your wins are way smaller, the risk-reward ratio is totally unfair.

Of course, some users might think that a losing streak of size 9 is pretty unlikely, if the probability of winning and losing are both equal to 0.5, then the probability of 9 consecutive losses is equal to 0.5^9 , there are approximately 0.2% of chance of having such large losing streak, note however that under a ranging market such case scenario could happen, but we will see later that the length of a losing streak is not the only problem.

Other Problems

Having a capital large enough to tank 9any number of consecutive losses is not the only thing one should focus on, as we have to take into account market prices and trading dynamics, that's where the ugly part start.

Our first problem is frictional costs, one example being the spread, but this is a common problem for any strategy, however here a martingale is extra sensitive to it, if the strategy does not account for it then we will still double our positions costs but we might not recover all the losses of a losing streak, instead we would be recovering only a proportion of it, under such scenario you would be certain to lose over time.

Another problem are gaps, market price might open under a stop-loss without triggering it, and this is a big no-no.

Equity of the strategy on AMD, in a desired scenario the equity at the second arrow should have been at a higher position than the equity at the first arrow.

In order for the strategy to be more effective, we would need to trade a market that does not close, such as the cryptocurrency market. Finally, we might be affected by slippage, altho only extreme values might drastically affect our balance.

The Anti Martingale

The strategy lets you use an anti-martingale, which double the position size after a win instead of a loss, the goal here is not to recover from a losing strike but instead to profit from a potential winning streak.

Here we are exposing your balance to exponential gross but you might also lose a trade at the end a winning streak, you will generally want to reinitialize your position size after a few wins instead of waiting for the end of a streak.

Alternative

You can use other-kind of progressions for position sizing, such as a linear one, increasing your position size by a constant number each time you lose. More gentle progressions will recover a proportion of your losses in a losing streak.

You can also simulate the effect of a martingale without doubling your position size by doubling your target profit, if for example you have a 10$ profit-target/stop-loss and lose a trade, you can use a 20$ profit target to recover from the lost trade + gain a profit of 10$. While this approach does not introduce exponential decay in your balance, you are betting on the market reaching your take profits, considering the fact that you are doubling their size you are expecting market volatility to increase drastically over time, as such this approach would not be extremely effective for high losing streak.

Conclusion

You will see a lot of auto-trading strategies that are based on a grid approach, they might even use a martingale. While the backtests will look appealing, you should think twice before using such kind of strategy, remember that frictional costs will be a huge challenge for the strategy, and that it assumes that the trader has an important initial capital. We have also seen that the risk/reward ratio is theoretically the worst you can have on a strategy, having a low reward and a high risk. This does not mean that progressive position sizing is bad, but it should not be pushed to the extreme.

It is nice to note that the martingale is originally a betting system designed for casino games, which unlike trading are not subject to frictional costs, but even casino players don't use it, so why would you?

Thx for reading

MMP Indicator 4-step WeeklyFading levels using martingale (limit orders, rebate venue) with no stop-loss orders, long the wings at the end of Support and Resist levels from prior week Friday right before the close. Re-hedge the order book units when there is a breakout.

inwCoin Martingale Strategy ( for Bitcoin )** Same as my previous martingale script but this version = opensource **

inwCoin Martingale Strategy is the proof of concept strategy that in the end, anyone who using martingale strategy will kaboom their portfolio.

For those who don't know what is "martingale".. it's a simple double down strategy in the hope to cover the loss in previous entry.

Example

In the game that if you win, you'll get 100% of your bet money back.

1st loss = 1$

2nd loss = bet 2$ : if win, get 2$ / real profit = 1$ ( 2-1 )

3rd loss = bet 4$ : if win, get 4$ / real profit = 1$ ( 4 - ( 2+1) )

4th loss = bet 8$ : if win, get 8$ / real profit = 1$ ( 8 - ( 4+2+1 ) )

...

...

10th loss = bet 512$ : if win, get 512$ / real profit = 1$ ( 512 - ( 256+128+64+32+16+8+4+2+1) )

as you can see, the next bet will be first bet x 2^(n-1)

and the profit will equal to your first bet.

==================

In trading and forex EA ( Expert Advisor or bot ) people use this strategy to fool newbies that their martingale system will generate steady income for eternity.

But in reality, this strategy will destroy your whole portfolio eventually some time in the future. Because there will be some "Blackswan event" in market at some point in time. And one who ignore this fact, will lose everything.

But, if you using low risk strategy and generate some profit from your low-risk portfolio. You can take small chunk of that profit and put it in riskier strategy like this martingale, to accerelate your profit snowball.

===================

Parameter Explaination

====================

Price = datasource for indicator calculation

Fixed position size option = if uncheck, the "Start position size" parameter will be % of your initial capital. If checked, it will fixed position size ( like 1 BTC )

Start Position Logic = condition to enter first trade

- MACD singal > 0 : Self explanatory, default macd value

- Stochastic RSI cross up : enter when sto line cross up from bottom ( 20 )

- ATR channel : enter trade if price cross above 2.3 ATR

Take Profit Percent = take profit target % from average entry

Start martingale ..= if price compare to average position entry less than this %, it will start to double down ( martingale )

Martingale Multiplier = you can specific how big you'll double down, default is 2

Trade Direction = long only for now

Use date rang = self explanatory

** make sure to setup your initial capital in properties tab **

On chart

=======

White Line = Average position price

Orange Line = your current equity

If equity less than 0, it will close any remaining positions ( It's mean your position got liquidated )

If price > equity line for "take profit percent" it will close any remaining positions.

=======

As you can see, this strategy survive 2018 drop and pump profit to 1000+% ( Check in the strategy tester tab > list of trades )

But in May 2020 -50% drop in just 3 days, your whole portfolio got liquidated.

Actually, after some digging in profit and backtest result.

This strategy, when it can survive a shape drop, can generate a lot of profit.

So, if you want to use martingale. Make sure to use only small chunk of your profit from "low-risk" strategy to accelerate your profit generation ( aka degen port )

DO NOT greedy and use all of your initial capital or borrowed money to use with this strategy!

Bilateral Stochastic Oscillator StrategyIntroduction

Strategy based on the bilateral stochastic oscillator, this oscillator aim to detect trends and possible reversal points of the current trend. The oscillator is composed of 1 bull line in blue and 1 bear line in red as well as a signal line in orange, the strategy have many options such as two different strategy framework and a martingale mode. If you require more information about the indicator go check it into my uploaded indicators.

Strategy Frameworks

There are two frameworks available that can be selected from the strategy settings window. Both have the same closing conditions, the "Bull/Bear Cross" entry conditions are :

Buy : when the bull line cross over the bear line

Sell : when the bear line cross over the bull line

The "Signal Cross" entry conditions are :

Buy : when the bull line cross over the signal line

Sell : when the bear line cross over the signal line

Both have the same close conditions that is : close when bull/bear cross under the signal line.

Introduction To Martingale

The martingale money management system consist to double the order size after a loosing trade and can be described as a 2^x where x is the current number of loosing trades since the last win trade, when we win a trade the order size return to the default order size. Therefore our order size function is based on exponential growth.

This system enable the trader to win back his previous losses plus a potential profit, martingales must always be used with stops and sometimes take profits in order to get control in a strategy.

It must always be taken into account that in a series of losses the balance can exponentially decay thus ending to 0 in a matter of trades, this is why it is not recommended to use such system. The strategy allow you to select a martingale multiplier that can be inferior to 2 thus limiting risks, a multiplied of 1 disable the martingale.

Results

Those are the some statistics of the strategy applied to some forex majors by using the default settings in a time frames of 15 minutes.

//-------------------------------------------------------

EURUSD - Order Size 1000 - Spread 0.0002

Profit : $ 21.08

Trades : 19

PP : 57.89 %

Profit Factor : 3.228

Max Drawdown : -$ 3.81

Average Trade : $ 1.11

//-------------------------------------------------------

GBPUSD - Order Size 1000 - Spread 0.0002

Profit : $ 2.31

Trades : 20

PP : 55 %

Profit Factor : 0.938

Max Drawdown : -$ 20.29

Average Trade : $ 0.12

//-------------------------------------------------------

EURAUD - Order Size 1000 - Spread 0.0002

Profit : -$ 9.22

Trades : 20

PP : 40 %

Profit Factor : 0.698

Max Drawdown : -$ 23.44

Average Trade : $ 0.46

//-------------------------------------------------------

EURCHF - Order Size 1000 - Spread 0.0002

Profit : $ 1.58

Trades : 24

PP : 54.17 %

Profit Factor : 1.103

Max Drawdown : -$ 7.23

Average Trade : $ 0.07

//-------------------------------------------------------

Conclusions

Based on the results the strategy does not posses the sufficient performance in order to apply a martingale or any other growth systems as order size. Parameters might be subject to drastic changes depending on the market/time-frame in order to return long-term positive results. I let you draw your conclusions.

Decent Martingale Strategy [Pinescript v3]In my experimentation to add some sort of hedging to trades, I stumbled on the Martingale roulette betting strategy.

If it works in the casino, why not here?

The principle is simple:

If you lose a trade, immediately go the opposite direction and double your bet.

In this case, we're just applying a multiplier.

The strategy is a simple EMA crossover - defaulted to my favorite periods 8 and 62.

Enjoy :) I'll make a new one that's contained in a function, so you can simply implement it in your own strategy and have it monitor winning/losing trades automatically.

Cheers,

DasanC

[RS]Function Martingale Multiplier - MA Crossover Bias V1EXPERIMENTAL:

WARNING: Martingale is subject to HUGE drawdown spikes, use at your own risk!

updated function to also double(aply multiplier) on even trades, example with a MA's crossover.

[RS]Function Martingale Multiplier V0EXPERIMENTAL:

WARNING:Martingale is susceptible to huge drawdown spikes, use at your own risk.

simple functions for martingale wins and losses, multiplier can be adjusted manually to increase/decrease performance/drawdown.

[STRATEGY][RS]Roulette Martingale V0a solid strategy all across the majors.

double the profits :p

WARNING: use at your own discretion.