Round Strike Price, Levels Options Series➤ Strike Price Range Mode:

➤ Exact Strike Price Mode:

⭐ Overview and How It Works

Round Strike Price or Levels is a precision-focused visual tool designed for options and index traders.

It dynamically plots round strike levels around the current price and presents them either as:

⠀ — Exact strike prices, or

⠀ — Strike price ranges, where each zone represents the midpoint between two adjacent strikes.

The indicator continuously recalculates the base strike using the current price and aligns all surrounding levels using a fixed step size.

All lines and labels are updated only on the last bar for optimal performance and stability.

This makes StrikePrice ideal for:

🔹 Identifying key option strikes.

🔹 Visualizing price acceptance zones.

🔹 Understanding strike-to-strike movement during intraday trading.

⭐ Key Features and Functionality

Strike Price Range:

⠀ — Treats each pair of strike lines as a price zone.

⠀ — Labels are plotted at the midpoint between two lines.

⠀ — Last label is intentionally hidden (no upper range exists)

Exact Strike Price:

⠀ — Labels are plotted directly on each strike line.

⠀ — Useful for precise strike-based analysis.

Dynamic Base Calculation:

⠀ — Automatically snaps price to the nearest round strike.

⠀ — Re-centers the entire grid as price moves.

⠀ — No manual adjustment required.

Efficient Object Management:

⠀ — Uses persistent arrays for lines and labels.

⠀ — Objects are reused instead of recreated.

⠀ — Prevents flickering and avoids TradingView object limits.

🎨 Visualizations and User Experience

Clean horizontal strike grid with configurable:

⠀ — Line width, Line color, Line style (Solid / Dashed / Dotted), Extension direction (Left / Right / Both / None).

Labels are:

⠀ — Positioned to the right of price, Size-adjustable, Fully customizable in text color and background color.

Designed to stay visually clear even on:

⠀ — Fast-moving intraday charts, Options-focused layouts, Multi-indicator setups.

Tip: Increase Right Bars Margin in chart settings to give labels proper spacing.

⭐ Settings and Customization

🔹 Strike Settings:

⠀ — Step (points): Distance between adjacent strike levels (e.g., 50, 100)

⠀ — Levels per side: Number of strike levels plotted above and below the base.

⠀ — Strike Mode: Strike Price Range, Exact Strike Price.

🔹 Line Settings:

⠀ — Line width, Line color, Line style (Solid / Dashed / Dotted), Line extension direction.

🔹 Label Settings:

⠀ — Show / hide labels, Label distance (bars to the right), Label size, Label text color, Label background color.

All label properties are updated dynamically, allowing real-time UI tuning without reloading the script.

⭐ Uniqueness of the Concept:

Unlike generic round-number indicators, StrikePrice:

⠀ — Understands option-style strike structure.

⠀ — Separates range-based thinking from exact price levels.

⠀ — Uses midpoint logic to visualize strike-to-strike movement.

⠀ — Maintains strict performance discipline by updating only when necessary.

This makes it especially useful for:

⠀ • NIFTY / BANKNIFTY options.

⠀ • Index and futures traders.

⠀ • Intraday strike rotation analysis.

⠀ • Premium decay and range-bound setups.

🚀 Conclusion:

StrikePrice is a focused, professional-grade indicator for traders who think in strikes, ranges, and levels rather than arbitrary prices.

It offers:

⠀ • Clear structure

⠀ • Accurate strike alignment

⠀ • Clean visuals

⠀ • Zero repainting logic

Optionstrading

IV vs Realised Volatility (VIX/HV Comparator)VIX / HV Comparator – Implied vs Realised Volatility

This indicator compares Implied Volatility (IV) from a volatility index (VIX, India VIX, etc.) with the Realised / Historical Volatility (HV) of the current chart symbol.

It helps you see whether options are pricing volatility as rich or cheap relative to what the underlying is actually doing.

What it does

Pulls IV from any user-selected vol index symbol (e.g. CBOE:VIX for SPX, NSEINDIA:INDIAVIX for Nifty).

Calculates realised volatility from the chart’s price data using returns over a user-defined lookback.

Annualises HV so IV and HV are displayed on the same percentage scale, on any timeframe (intraday or higher).

Optionally shows an IV/HV ratio in a separate pane to highlight when options are rich or cheap relative to realised volatility.

How to read it

Main panel:

Orange line – Implied Volatility (IV) from your chosen vol index.

Aqua line – Realised / Historical Volatility (HV) of the current chart symbol.

Fill between lines:

Green shading -> IV > HV -> options are priced richer than what the underlying is currently realising.

Red shading -> HV > IV -> realised vol is higher than the options market is implying.

Sub-panel (optional):

IV / HV ratio

- Above 1 -> IV > HV (vol rich).

- Below 1 -> IV < HV (vol cheap).

- Horizontal guides (for example 1.2 / 0.8) help frame “significantly rich/cheap” zones.

A small label on the latest bar displays the current IV, HV and their difference in vol points.

Inputs (key ones)

IV Index Symbol – choose the volatility index that corresponds to your underlying (VIX, India VIX, etc.).

Realised Vol Lookback – number of bars used to compute HV (for example 20).

Trading Days per Year and Active Hours per Day – used for annualising HV so it stays consistent across timeframes.

IV Scale Factor – adjust if your IV index is quoted in decimals (0.15) instead of points (15).

Practical uses

Context for options trades – Quickly see if current IV is high or low relative to realised volatility when deciding on strategies (premium selling vs buying, spreads, hedges).

Vol regime analysis – Track shifts where HV starts to rise above IV (real stress building) or IV spikes far above HV (fear premium / insurance bid).

Cross-timeframe checks – Use on intraday charts for short-term trading context, or on daily/weekly charts for bigger picture vol regimes.

This tool is not a stand-alone signal generator. It is meant to be a volatility dashboard you combine with your usual price action, trend, and options strategy rules to understand how the options market is pricing risk vs what the underlying is actually delivering.

GexView📈 OVERVIEW

GexView indicator plots the Historical Gamma Exposure (GEX) profile, directly on the chart. It enables traders and analysts to observe how GEX profile evolve across multiple days/sessions.

🧲 CONCEPT

Today everybody uses Gamma Exposure. Gamma is the ROC (Rate of Change) for an option’s delta. GEX is crucial for all traders, not just intraday traders, because it helps assess market stability and potential volatility shifts driven by options positioning.

High positive GEX generally implies a mean-reverting market, where big price swings are dampened, while negative GEX signals increased volatility and potential large moves.

Understanding GEX allows traders to anticipate liquidity-driven price action, identify key support and resistance levels, and adjust strategies accordingly. In today’s market, where options flow heavily influences underlying assets, ignoring GEX can mean missing critical market dynamics that impact both short-term and long-term positions.

💡 UNIQUENESS

This indicator is a unique tool and offers a groundbreaking way to visualize market dynamics by plotting Historical Gamma Exposure (GEX), like a Volume Profile across multiple days or sessions. For the first time, traders can clearly see how GEX levels evolve over time, revealing how certain price zones gain or lose importance as market conditions change. This multi-session GEX profile allows users to identify persistent areas of dealer positioning and potential support or resistance that develop and shift over days. Unlike traditional GEX tools designed primarily for intraday use, this indicator provides valuable insight for both short-term traders and medium-term investors seeking to understand how option market flows influence price behaviour over extended periods.

⚙️ FEATURES

• Historical Gamma Exposure

The GexView indicator by default plots the last 6 days of the GEX profile, providing a framework for understanding the bigger picture.

• GEX profile

Displays the 10 largest GEX levels across all expirations (thick lines), as well as the 10 largest GEX levels for the next expiration (thin lines, 0DTE or upcoming).

• Update

Daily, after market close, based on new open interest. No more manual level imports.

Just one-click update.

• Settings

Option to plot total sum GEX for all expirations, or only net GEX for next expiration.

• Watchlist

SPX, NDX, DIA, SPY, QQQ, VIX, VXX, IBIT

(Additional tickers coming soon)

• Mapping

The indicator automatically detects and maps the underlying ticker on your chart, or lets you plot any symbol from the available watchlist.

🔍 HOW TO USE

• Identify intraday support and resistance levels shaped by option market dynamics

• Quickly spot significant GEX levels and compare how they relate to other key levels.

• Compare current vs. past GEX distributions for contextual trend analysis

• Observe structural GEX shifts that may align with volatility or mean-reversion setups

• Easily understanding if an asset trading on positive gamma (around green lines), or negative gamma (around red lines)

Examples:

1. DIA ETF

2. QQQ and VIX

📚 NOTES

• Calculation

GEX for All Expirations: This is the total sum (Call+Put) of gamma exposure of all expirations.

GEX for Nearest Expirations: This is the net sum (Call-Put) of gamma exposure of next expirations (0DTE if available).

• Trading Session - RTH & ETH

The indicator can include the extended trading hours when activated on the chart.

✅ VISUALIZATION

• Vertical implementation of gamma exposure profile.

• Thick lines represent the total gamma exposure across all expiration contracts.

• Thin lines represent the gamma exposure of next expiration only.

• All Expirations: Green colour if Calls > Puts, Red colour if Calls < Puts

• Next Expiration: Lime colour if Calls > Puts, Maroon colour if Calls < Puts

⚠️ DISCLAIMER

This indicator is provided for informational and educational purposes only.

It does not constitute financial advice or a recommendation to buy or sell any financial instrument.

Historical Gamma patterns and analytical interpretations do not guarantee future performance.

All analysis should be combined with independent research and risk management.

TradeUniv.com Expected MovesTradeUniv.com Expected Moves

See where the market expects stocks to move based on options pricing data. This indicator shows you upper and lower price levels that help identify potential support, resistance, and overextended moves.

What Are Expected Moves?

Expected moves are calculated from option prices and show where the market thinks a stock is likely to trade by the end of the day or week. Think of them as probability zones - when price reaches or crosses these levels, it may signal an unusual

move or potential reversal opportunity.

What You'll See on Your Chart:

• Upper Level (Green) - Expected high for the period

• Lower Level (Red) - Expected low for the period• Midpoint (Gray) - Previous day's closing price (your reference point)

• Shaded Area - The expected trading range between levels

How to Use:

1. Visit www.tradeuniv.com

2. Select your favorite tickers

3. Click "Generate Script" and copy the TradingView input

4. Paste it into this indicator's settings

5. The indicator automatically shows the expected moves for whatever chart you're viewing

Perfect For:

• Day traders planning entry and exit zones

• Identifying when price has moved "too far too fast"

• Spotting potential reversal areas

• Understanding daily volatility expectations

• Planning option strategies around expected ranges

Features:

• Automatically detects daily vs weekly expirations (SPY, IWM, QQQ use daily; others use weekly)

• Customizable colors and line styles

• Price crossing alerts (get notified when price breaks above/below expected levels)

• Works on any timeframe

• Clean, minimal chart display

Important:

• Requires TradeUniv.com free account to generate data

• Refresh your data daily for accurate calculations

• Only shows levels for tickers you selected when generating

ATM Pulse (Arjo)ATM Pulse (Arjo) — Real-Time ATM Options Sentiment & Trend Strength Indicator

Overview

ATM Pulse (Arjo) is an options analytics and trend overlay tool that automatically detects the At-The-Money (ATM) strike for NIFTY, BANKNIFTY , or any selected stock.

It merges Call–Put Volume Ratio (CPVR) sentiment analysis with a Chandelier Exit trend overlay to help traders visualize both market bias and trend direction in a single chart.

Concepts & Logic

ATM Auto Detection

The script calculates the current ATM strike by rounding the underlying’s price to the nearest strike interval (e.g., 50 for NIFTY, 100 for BANKNIFTY). It then requests live option-chain data for that strike.

Call–Put Volume Ratio (CPVR)

The Call-Put Volume Ratio (CPVR) is calculated as the call volume divided by the put volume.

CPVR > 1.25 → Bullish dominance (Calls stronger)

CPVR < 0.75 → Bearish dominance (Puts stronger)

0.75–1.25 → Neutral sentiment

This ratio helps interpret real-time option-market positioning.

Chandelier Exit Trend Overlay

Using Average True Range (ATR) , the overlay plots dynamic trailing stops and visual trend zones:

🟢 Green: Uptrend continuation zone

🔴 Red: Downtrend continuation zone

A color change signals possible momentum reversal.

Combination of CPVR and Chandelier Exit

CPVR gauges option-market sentiment

Chandelier Exit confirms price-action direction

When both align (e.g., bullish CPVR + green Chandelier zone), it strengthens directional conviction. Divergent readings may signal indecision or early reversals.

How to Use

Open any NIFTY, BANKNIFTY , or stocks chart.

Add ATM Pulse (Arjo) to the chart.

Select your expiry date — the script auto-detects the ATM strike and displays:

C: Call LTP

P: Put LTP

CPVR: Call/Put Volume Ratio label

Watch the Chandelier Exit colors:

🟢 Green = Bullish trend

🔴 Red = Bearish trend

Combine CPVR bias + trend color for confirmation.

If CPVR is above 1.25 and trend color green → More bullish activity (Calls stronger).

If CPVR is below 0.75, and trend color red→ More bearish activity (Puts stronger).

If CPVR is between 0.75 and 1.25 and the trend color is gray/mixed → Neutral

Practical Use Case

The script continuously updates the ATM strike, CPVR , and trend overlay in real time.

It provides a clear visual snapshot of how option volumes align with price momentum , ideal for intraday or short-term directional traders.

Disclaimer

This tool is for educational and analytical purposes only.

It does not provide financial advice or guaranteed trading signals.

Happy Trading. ARJO

Option Chain-Based Call & Put Momentum VisualizerOption Chain-Based Call & Put Momentum Visualizer

invite-only by @JjpTradingAcademy

Overview

The Option Chain-Based CE/PE Momentum Visualizer is a powerful analytical tool designed to track real-time momentum and sentiment shifts between Call (CE) and Put (PE) options directly on the chart. It offers deep insight into option buyers’ and sellers’ behavior by analyzing multiple strikes, dynamically calculating cumulative CE/PE strength, and correlating it with underlying index price movements.

How to Use

The bottom pane of the indicator displays the decay data for both Call and Put options at every candle, green shows positive, red shows negative, and orange shows neutral. At the centre, it shows difference between Call and Put decay data, if the difference is less than 35 then it indicates with lime color otherwise it appears with purple color, When the trend changes between from lime and purple, the indicator plots a purple bar representing strong candles that often precede high momentum moves.

High/Low ranges are automatically plotted once the middle value drops below 10.

A breakout/breakdown of purple candle at the range indicates a strong directional movement on either side.

Reference images for visual guidance:

Inputs

To ensure proper functionality, fill in all fields correctly - Index/Stock Symbol Name, Pre-Market 's ATM Level, Options Type (OTM, ITM, OTM+ITM), Options Expiry Date, Options Symbol Prefix, Strike Interval If these are not set correctly, runtime errors may occur.

CE/PE Candle Strength – Displays CE/PE strength % for each candle

Highlight Prior Range – Marks previous High/Low zones for visual confirmation

Show Historical Entry Zone – Displays earlier High/Low ranges with color fills to highlight zone strength

Alerts

Purple Bar Signal

(Setup: Add Alert → Condition: "Option Chain-Based Call & Put Momentum Visualizer" → "Purple Bar Signal")

Security Call

All signals are calculated on bar close.

The script uses security () calls to fetch individual option OHLC data for accurate CE/PE momentum analysis.

Access

Invite-Only.

Request access via TradingView PM to @JjpTradingAcademy

Redistribution, reselling, or code extraction is strictly prohibited.

Disclaimer

This indicator is for educational purposes only.

It does not constitute financial advice or a guaranteed system of profitability.

Trading options involves significant risk - always conduct your own research and apply sound risk management.

PCP Arbitrage Monitor (Math by Thomas)Live monitor for Put–Call Parity (C + PV(K) = P + S) showing drift, arbitrage direction, and opportunity strength.

The PCP Arbitrage Monitor helps traders visualize and quantify deviations from the Put–Call Parity (PCP) relationship:

𝐶+𝐾𝑒−𝑟𝑇 = 𝑃+𝑆

When this equation drifts, it indicates a potential arbitrage opportunity between call, put, and underlying (spot or future).

This indicator plots the left-hand side (LHS) and right-hand side (RHS) of the PCP equation on your chart, computes the drift, and automatically highlights and displays actionable trade combinations when the deviation exceeds a set threshold.

⚙️ How It Works

Inputs

Call & Put Symbols – Select matching call and put options (same strike & expiry).

Strike (K) – The strike price for those options.

Expiry (UTC) – Option expiry date/time (used to calculate 𝑇 and PV(K)).

Risk-free Rate (r) – Annualized rate used for discounting the strike.

Lot Size / Tick Value – Used to calculate profit in INR.

Arbitrage Threshold – Minimum drift (in points) to trigger signals (default 200).

Displayed Data

LHS = C + PV(K) (Call + discounted Strike)

RHS = P + S (Put + Spot/Future)

Drift = LHS – RHS

Bookable Profit (INR)

Action Suggestion (only when |drift| ≥ threshold)

Background Highlight

🟩 Green – Call side expensive → Sell Call + Buy Put + Buy Fut

🟥 Red – Call side cheap → Buy Call + Sell Put + Sell Fut

Table

Displays all key values live in the top-right corner:

Option prices

LHS, RHS

Drift (points)

Time to expiry

Lot size

Bookable profit (INR)

Trade action (only if |drift| ≥ threshold)

📈 How to Use

Open a NIFTY Spot or Futures chart (works on both).

Enter the exact option symbols (e.g., NSE:NIFTY24DEC21900CE and NSE:NIFTY24DEC21900PE).

Adjust Strike (K) and Expiry to match those options.

Observe:

The green/red background highlights large deviations (≥ threshold).

The Action cell displays the arbitrage combination and expected profit.

A drift beyond the threshold suggests a potential risk-free arbitrage if executed simultaneously across all legs.

Hold positions till expiry if margin allows; the profit is theoretically locked in.

💡 Tips

Works on both Spot and Futures charts — the script auto-uses the chart’s close as 𝑆

Set smoothing to 0 to see raw parity values.

Adjust threshold based on costs and margin — e.g., 150–200 points for NIFTY is practical.

Only valid when options are European (no early exercise risk).

Ensure both option symbols are liquid and from the same expiry.

⚠️ Disclaimer

This tool is for educational and analytical purposes.

Real arbitrage execution depends on liquidity, bid-ask spread, slippage, and margin requirements.

Always validate prices with your broker before trading.

Institutional Zones: Opening & Closing Trend HighlightsDescription / Content:

Track key institutional trading periods on Nifty/Bank Nifty charts with dynamic session zones:

Opening Volatility Zone: 9:15 AM – 9:45 AM IST (Green)

Closing Institutional Zone: 1:30 PM – 3:30 PM IST (Orange)

Both zones are bounded by the day’s high and low to help visualize institutional activity and price behavior.

Key Observations:

Breakout in both closing trend and opening trends often occurs on uptrending days.

Breakdown in both closing range and opening range usually happens on downside trending days.

Price opening above the previous closing trend is often a sign of a strong opening.

This script helps traders identify trend strength, breakout/breakdown zones, and institutional participation during critical market hours.

Disclaimer:

This indicator is for educational and informational purposes only. It is not a financial advice or recommendation to buy or sell any instrument. Always confirm with your own analysis before taking any trade.

Pine Script Features:

Dynamic boxes for opening and closing sessions

Boxes adjust to the day’s high and low

Optional labels at session start

Works on intraday charts (1m, 5m, 15m, etc.)

Usage Tip:

Use this indicator in combination with trend analysis and volume data to spot strong breakout/breakdown opportunities in Nifty and Bank Nifty.

Gamma Exposure Levels by OMG (Oh My Gamma)OMG (Oh My Gamma) - Daily GEX Levels

An operational framework for Gamma analysis with daily data.

Indicator's Purpose & Demo Data

This indicator plots key strategic levels derived from Gamma Exposure (GEX) analysis. It showcases the operational logic of OhMyGamma analytical engine.

IMPORTANT: The levels plotted by this public script are based on a past date's snapshot for demonstration purposes. They are not valid for live trading and will not update automatically.

The real edge comes from using the fresh data structure provided daily.

How to Read the Levels

This indicator is designed to provide actionable intelligence, not just data. Here's how to read it:

The Levels: Each line represents a key strategic zone (Zero Gamma, Call/Put Walls, etc.) where a market reaction is statistically probable due to dealer hedging flows.

Line Thickness = Strategic Importance: The thickness of each line directly corresponds to its strategic rating. Thicker, solid lines represent higher-conviction zones.

Labels & Tooltips: Hover over a level's label on your chart to see its full description, confluences, and strategic rating.

Pro Tip: The Power of Confluence

This indicator is not a standalone "system". It's an institutional-grade intelligence layer. Its predictive power increases exponentially when used to find confluence with your own analysis.

The highest-probability trades occur when a key Gamma level aligns with:

Price Action: Key support/resistance zones, order blocks, or liquidity pools.

Volumetric Indicators: High/Low Volume Nodes (HVN/LVN) from Volume Profile, VWAP, and Anchored VWAP.

Use these levels to confirm your setups and gain the conviction to act.

How to Get the Daily Updated Script

This indicator requires a new Pine Script code each day to load the current session's data.

To get the daily updated code feel free to visit www.ohmygamma.com

Feedback & Suggestions

This tool is built for the community. Suggestions for improvements and new features are highly welcome and help the project evolve. Feel free to get in touch via the contact form on the website.

Disclaimer: This tool is for informational and educational purposes only. Trading involves significant risk. The authors assume no responsibility for any trading decisions.

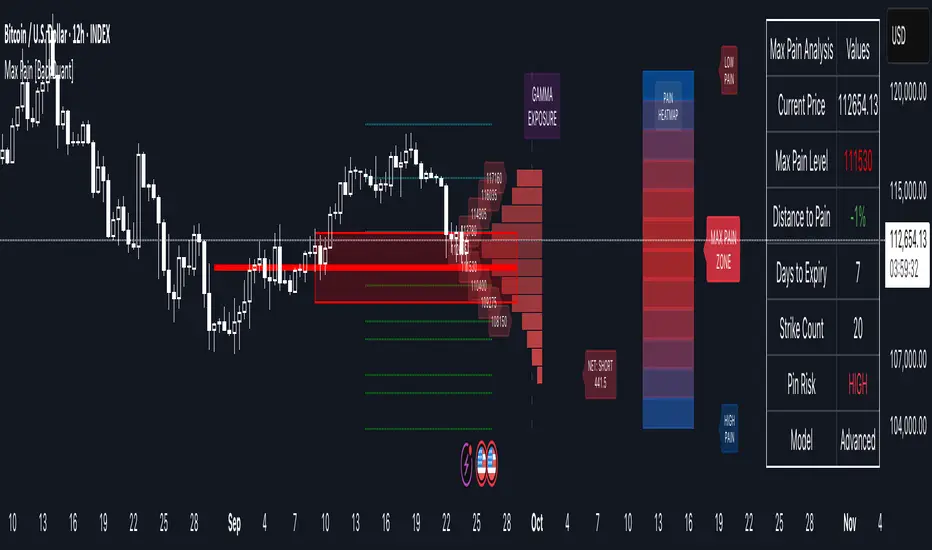

Options Max Pain Calculator [BackQuant]Options Max Pain Calculator

A visualization tool that models option expiry dynamics by calculating "max pain" levels, displaying synthetic open interest curves, gamma exposure profiles, and pin-risk zones to help identify where market makers have the least payout exposure.

What is Max Pain?

Max Pain is the theoretical expiration price where the total dollar value of outstanding options would be minimized. At this price level, option holders collectively experience maximum losses while option writers (typically market makers) have minimal payout obligations. This creates a natural gravitational pull as expiration approaches.

Core Features

Visual Analysis Components:

Max Pain Line: Horizontal line showing the calculated minimum pain level

Strike Level Grid: Major support and resistance levels at key option strikes

Pin Zone: Highlighted area around max pain where price may gravitate

Pain Heatmap: Color-coded visualization showing pain distribution across prices

Gamma Exposure Profile: Bar chart displaying net gamma at each strike level

Real-time Dashboard: Summary statistics and risk metrics

Synthetic Market Modeling**

Since Pine Script cannot access live options data, the indicator creates realistic synthetic open interest distributions based on configurable market parameters including volume patterns, put/call ratios, and market maker positioning.

How It Works

Strike Generation:

The tool creates a grid of option strikes centered around the current price. You can control the range, density, and whether strikes snap to realistic market increments.

Open Interest Modeling:

Using your inputs for average volume, put/call ratios, and market maker behavior, the indicator generates synthetic open interest that mirrors real market dynamics:

Higher volume at-the-money with decay as strikes move further out

Adjustable put/call bias to reflect current market sentiment

Market maker inventory effects and typical short-gamma positioning

Weekly options boost for near-term expirations

Pain Calculation:

For each potential expiry price, the tool calculates total option payouts:

Call options contribute pain when finishing in-the-money

Put options contribute pain when finishing in-the-money

The strike with minimum total pain becomes the Max Pain level

Gamma Analysis:

Net gamma exposure is calculated at each strike using standard option pricing models, showing where hedging flows may be most intense. Positive gamma creates price support while negative gamma can amplify moves.

Key Settings

Basic Configuration:

Number of Strikes: Controls grid density (recommended: 15-25)

Days to Expiration: Time until option expiry

Strike Range: Price range around current level (recommended: 8-15%)

Strike Increment: Spacing between strikes

Market Parameters:

Average Daily Volume: Baseline for synthetic open interest

Put/Call Volume Ratio: Market sentiment bias (>1.0 = bearish, <1.0 = bullish) It does not work if set to 1.0

Implied Volatility: Current option volatility estimate

Market Maker Factors: Dealer positioning and hedging intensity

Display Options:

Model Complexity: Simple (line only), Standard (+ zones), Advanced (+ heatmap/gamma)

Visual Elements: Toggle individual components on/off

Theme: Dark/Light mode

Update Frequency: Real-time or daily calculation

Reading the Display

Dashboard Table (Top Right):

Current Price vs Max Pain Level

Distance to Pain: Percentage gap (smaller = higher pin risk)

Pin Risk Assessment: HIGH/MEDIUM/LOW based on proximity and time

Days to Expiry and Strike Count

Model complexity level

Visual Elements:

Red Line: Max Pain level where payout is minimized

Colored Zone: Pin risk area around max pain

Dotted Lines: Major strike levels (green = support, orange = resistance)

Color Bar: Pain heatmap (blue = high pain, red = low pain/max pain zones)

Horizontal Bars: Gamma exposure (green = positive, red = negative)

Yellow Dotted Line: Gamma flip level where hedging behavior changes

Trading Applications

Expiration Pinning:

When price is near max pain with limited time remaining, there's increased probability of gravitating toward that level as market makers hedge their positions.

Support and Resistance:

High open interest strikes often act as magnets, with max pain representing the strongest gravitational pull.

Volatility Expectations:

Above gamma flip: Expect dampened volatility (long gamma environment)

Below gamma flip: Expect amplified moves (short gamma environment)

Risk Assessment:

The pin risk indicator helps gauge likelihood of price manipulation near expiry, with HIGH risk suggesting potential range-bound action.

Best Practices

Setup Recommendations

Start with Model Complexity set to "Standard"

Use realistic strike ranges (8-12% for most assets)

Set put/call ratio based on current market sentiment

Adjust implied volatility to match current levels

Interpretation Guidelines:

Small distance to pain + short time = high pin probability

Large gamma bars indicate key hedging levels to monitor

Heatmap intensity shows strength of pain concentration

Multiple nearby strikes can create wider pin zones

Update Strategy:

Use "Daily" updates for cleaner visuals during trading hours

Switch to "Every Bar" for real-time analysis near expiration

Monitor changes in max pain level as new options activity emerges

Important Disclaimers

This is a modeling tool using synthetic data, not live market information. While the calculations are mathematically sound and the modeling realistic, actual market dynamics involve numerous factors not captured in any single indicator.

Max pain represents theoretical minimum payout levels and suggests where natural market forces may create gravitational pull, but it does not guarantee price movement or predict exact expiration levels. Market gaps, news events, and changing volatility can override these dynamics.

Use this tool as additional context for your analysis, not as a standalone trading signal. The synthetic nature of the data makes it most valuable for understanding market structure and potential zones of interest rather than precise price prediction.

Technical Notes

The indicator uses established option pricing principles with simplified implementations optimized for Pine Script performance. Gamma calculations use standard financial models while pain calculations follow the industry-standard definition of minimized option payouts.

All visual elements use fixed positioning to prevent movement when scrolling charts, and the tool includes performance optimizations to handle real-time calculation without timeout errors.

Implied Volatility RangeThe Implied Volatility Range is a forward-looking tool that transforms option market data into probability ranges for future prices. Based on the lognormal distribution of asset prices assumed in modern option pricing models, it converts the implied volatility curve into a volatility cone with dynamic labels that show the market’s expectations for the price distribution at a specific point in time. At the selected future date, it displays projected price levels and their percentage change from today’s close across 1, 2, and 3 standard deviation (σ) ranges:

1σ range = ~68.2% probability the price will remain within this range.

2σ range = ~95.4% probability the price will remain within this range.

3σ range = ~99.7% probability the price will remain within this range.

What makes this indicator especially useful is its ability to incorporate implied volatility skew. When only ATM IV (%) is entered, the indicator displays the standard Black–Scholes lognormal distribution. By adding High IV (%) and Low IV (%) values tied to strikes above and below the current price, the indicator interpolates between these inputs to approximate the implied volatility skew. This adjustment produces a market-implied probability distribution that indicates whether the option market is leaning bullish or bearish, based on the data entered in the menu:

ATM IV (%) = Implied volatility at the current spot price (at-the-money).

High IV (%) = Implied volatility at a strike above the current spot price.

High Strike = Strike price corresponding to the High IV input (OTM call).

Low IV (%) = Implied volatility at a strike below the current spot price.

Low Strike = Strike price corresponding to the Low IV input (OTM put).

Expiration (Day, Month, Year) = Option expiration date for the projection.

Once these inputs are entered, the indicator calculates implied probability ranges and, if both High IV and Low IV values are provided, adjusts for skew to approximate the option market’s distribution. If no implied volatility data is supplied, the indicator defaults to a lognormal distribution based on historical volatility, using past realized volatility over the same forward horizon. This keeps the tool functional even without implied volatility inputs, though in that case the output represents only an approximation of ATM IV, not the actual market view.

In summary, the Implied Volatility Range is a powerful tool that translates implied volatility inputs into a clear and practical estimate of the market’s expectations for future prices. It allows traders to visualize the probability of price ranges while also highlighting directional bias, a dimension often difficult to interpret from traditional implied volatility charts. It should be emphasized, however, that this tool reflects only the market’s expectations at a specific point in time, which may change as new information and trading activity reshape implied volatility.

Multi-Timeframe Options Strategy with Dynamic Scoring System## Multi-Timeframe Options Strategy with Dynamic Scoring System

### Overview

This indicator combines 12 technical analysis tools using a proprietary 30-point scoring system to generate options trading signals (CALL/PUT). It's designed for traders seeking confluence-based entries with multiple confirmation layers.

### How the Scoring System Works

The indicator evaluates market conditions across three categories:

**Trend Analysis (9 points maximum):**

- EMA Alignment (9, 21, 50, 200): Checks if moving averages are properly stacked (3 points)

- ADX Trend Strength: Confirms trend momentum above 25 threshold (3 points)

- Higher Timeframe Confirmation: Validates signals against larger timeframe trend (3 points)

**Momentum Indicators (7 points maximum):**

- RSI Position & Direction: Optimal zones 40-65 for buys, 35-60 for sells (2 points)

- MACD Signal Line Cross: Momentum confirmation (2 points)

- Stochastic Oscillator: Overbought/oversold conditions (2 points)

- Bollinger Band Position: Price relative to middle band (1 point)

**Market Quality Filters (4 points maximum):**

- Volume Confirmation: 1.5x average volume requirement (2 points)

- VWAP Position: Trend alignment check (1 point)

- ATR Volatility: Ensures adequate price movement (1 point)

### Key Features

**1. Fair Value Gaps (FVG)**

- Identifies price inefficiencies between candles

- Bullish FVG: Current low > high (potential support)

- Bearish FVG: Current high < low (potential resistance)

- Visual representation with colored boxes on chart

**2. Three Operating Modes**

- Normal Mode: Minimum 10 points - balanced signal frequency

- High Mode: Minimum 15 points - fewer but stronger signals

- Ultra Mode: Minimum 20 points - only highest quality setups

**3. Protection Mechanisms**

- Bollinger Band squeeze detection avoids ranging markets

- Prevents conflicting signals (no simultaneous CALL/PUT)

- 5-bar minimum cooldown between signals

- Filters extreme RSI readings (>75 or <25)

**4. Risk Management**

- Three profit targets: 0.5%, 1%, 1.5%

- Stop loss: 0.5% or ATR-based

- Visual target lines with entry/exit levels

### How Components Work Together

The indicator creates a comprehensive market analysis by combining:

- **EMAs** provide the trend structure framework

- **Oscillators** (RSI, Stochastic) identify optimal entry timing

- **ADX** confirms trend strength to filter weak signals

- **Volume** validates institutional participation

- **Higher timeframe** acts as a directional filter

Each component contributes points to either bullish or bearish scoring. Signals only generate when one direction significantly outweighs the other and meets minimum thresholds.

### Usage Instructions

1. **Select Mode**: Choose Normal/High/Ultra based on your trading style

2. **Monitor Dashboard**: Check real-time scoring and market conditions

3. **Wait for Signals**: Main BUY/SELL labels appear when criteria met

4. **Follow Targets**: Use automated TP and SL levels for risk management

5. **Candle Labels**: Optional CALL/PUT labels show building momentum

### Dashboard Information

The dashboard displays:

- Current trend direction and HTF confirmation

- ADX strength and direction

- RSI status with divergence detection

- MACD momentum state

- Volume multiplier

- Market condition (trending/ranging)

- Live scoring for both directions

### Important Notes

- This is a technical analysis tool, not financial advice

- Past performance does not guarantee future results

- Always use proper risk management

- Test thoroughly on demo before live trading

### Originality

This indicator's unique value comes from:

1. The 30-point weighted scoring system that prioritizes different factors

2. Integration of Fair Value Gaps with traditional indicators

3. Multi-mode operation allowing traders to adjust signal frequency

4. Higher timeframe validation system

5. Comprehensive filtering to reduce false signals

The combination creates a systematic approach to options trading that goes beyond simple indicator mashups by providing clear, scored reasoning for each signal.

---

### Updates and Support

For questions or suggestions, please comment below. The indicator will be updated based on community feedback while maintaining compliance with all platform rules.

🧠 STWP Options Strategy Dashboard (Strangle)________________________________________

🧠 STWP Options Strategy Dashboard (Long/Short Strangle)

Author: simpletradewithpatience

Markets: NSE (India)

Best timeframe: 1-second chart

Built with: Pine Script v5

________________________________________

📌 Overview

A real-time options strategy dashboard tailored for NSE Strangles:

✅ Long Strangle → Buy OTM CE + Buy OTM PE

✅ Short Strangle → Sell OTM CE + Sell OTM PE

This tool offers a tick-by-tick visual dashboard to monitor:

Live premiums, PnL, breakeven levels, expiry decay, and Greeks.

It is designed **for manual use only** — no trade automation.

Ideal for strategy tracking, education, and decision support.

________________________________________

📌 Key Features

✅ Long & Short Strangle support

✅ Real-time tracking of CE & PE legs (LTPs, PnL, Premium)

✅ Max Loss / Profit calculator

✅ Breakeven range calculator

✅ Risk:Reward verdict (dynamic logic)

✅ Smart Exit logic with trade-specific warnings

✅ Reversal Exit logic based on spot compression

✅ Optional manual Greeks input (Delta, Gamma, Theta, IV)

✅ Greek-based bias: Bullish / Bearish / Neutral

✅ Days to Expiry (DTE) calculator

✅ Clean dashboard UI (emoji-labeled)

✅ Built for Indian NSE Options

✅ Designed to run on **1-second chart only**

________________________________________

📌 Option Symbol Inputs (LTP Tracking)

✅ Call Symbol: OTM CE (above spot)

✅ Put Symbol: OTM PE (below spot)

🎯 Symbol Tips: Use NSE format like `NSE:RELIANCE25JUL3050CE` and `PE`

⚠️ Valid option symbols are critical for accurate PnL tracking

________________________________________

📌 Strategy Parameters

- Call & Put Strike Prices

- Buy/Sell Premiums for both legs

- Lot Size & Number of Lots

- Loss Bearable Amount (₹)

- Expiry Date & Time (used for DTE tracking)

________________________________________

📌 Smart Exit Logic

🧠 A dynamic assistant that checks:

✅ Profit Target Hit

❌ Loss Threshold Breach

⏳ Expiry nearing with no breakout

🟡 Partial Profit Zone

📉 Guides the trader to avoid emotional decisions.

All messages are suggestive only — no trade recommendations.

________________________________________

📌 Reversal Exit Logic (Strangle Specific)

🔁 Detects if spot is trapped between the call/put strikes

➡️ If no breakout from the average strike zone, exit is suggested

⚠️ Helps prevent theta decay trap in Long Strangles

________________________________________

📌 Greeks (Optional Input)

🔹 Manual input for Delta, Gamma, Theta, and IV for both legs

🔍 Dashboard shows:

- Net Delta: Directional Bias

- Net Gamma: Volatility Risk

- Net Theta: Time Decay Risk

- Avg IV: Vol Crush or Low IV Warning

- Verdict: 🟢 Strong / 🟡 Moderate / ❌ Risky

________________________________________

📌 Dashboard Display

📈 Strategy Type: Long or Short Strangle

💹 Call & Put Premiums (Entry vs LTP)

📊 Total Net Premium

📉 Real-time PnL

📐 Breakeven Range (Lower & Upper)

🧠 Smart Exit verdict

🔁 Reversal Exit guidance

📆 Days to Expiry (DTE)

📊 R:R Ratio & Quality Verdict

📐 Greeks Summary + Risk Flags (if enabled)

________________________________________

⚠️ Important Notes

✅ Built for NSE Options only

✅ Designed for Long/Short Strangle strategies

✅ Use on 1-second chart only

❌ Will not function correctly on higher timeframes

✅ This is a manual dashboard — **no orders or automation**

✅ For educational, research, and tracking use only

❌ Not financial advice or a trading recommendation

________________________________________

💬 How to Use This Dashboard

1️⃣ Choose your strategy: Long or Short Strangle

2️⃣ Enter valid CE & PE symbols (OTM strikes)

3️⃣ Fill in strike prices and premiums (Buy/Sell)

4️⃣ Optionally enter Greeks (Delta, Gamma, etc.)

5️⃣ Set your expiry date

6️⃣ Monitor PnL, risk zones, exit suggestions

7️⃣ Use alerts (if enabled) for major thresholds

________________________________________

🤝 Final Note

This tool was built with patience and care by simpletradewithpatience to help fellow options traders trade more objectively, systematically, and confidently.

Feel free to share feedback on Tradingview.

Happy Trading! 📈

Stay disciplined. Stay smart.

________________________________________

🔠 Glossary

PnL – Profit & Loss

LTP – Last Traded Price

IV – Implied Volatility

DTE – Days to Expiry

ROI – Return on Investment

R:R – Risk to Reward Ratio

CE / PE – Call / Put Option

SEBI – Securities and Exchange Board of India

________________________________________

⚠️ Disclaimer

This script is for educational and research purposes only.

I am not a SEBI-registered advisor.

No buy or sell recommendations are made.

Trading options involves significant risk.

Use proper risk management and always consult a licensed advisor if in doubt.

The author is not responsible for any financial losses incurred.

By using this tool, you agree to these terms.

________________________________________

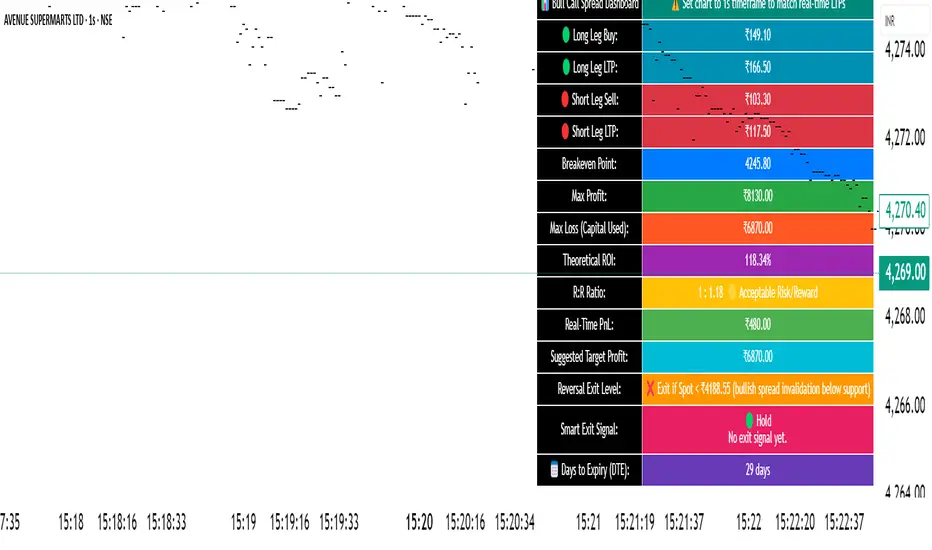

🧠 STWP Dashboard (Bull Call Spread / Bear Put Spread)________________________________________

🧠 STWP Options Strategy Dashboard (Bull Call Spread/ Bear Put Spread)

Author: @simpletradewithpatience

Markets: NSE (India)

Best timeframe: 1-second chart

Built with: Pine Script v5

________________________________________

📌 Overview

A real-time options strategy dashboard tailored for NSE traders, designed for two-leg spreads:

✅ Bull Call Spread → Buy Lower Strike CE, Sell Higher Strike CE

✅ Bear Put Spread → Buy Higher Strike PE, Sell Lower Strike PE

This tool gives you a real-time, color-coded visual interface with:

Entry premiums & breakeven levels

Live LTPs & PnL

ROI & Risk: Reward

Smart Exit logic

Alerts for expiry, Greeks, and PnL events

It’s fully manual, for educational and tracking use only — not for automated trading.

________________________________________

📌 Key Features

✅ Track Bull Call & Bear Put Spreads

✅ Live LTP tracking via symbol input

✅ Real-time PnL, breakeven, max profit/loss

✅ ROI & Risk:Reward calculation

✅ Smart Exit logic with trade verdicts

✅ Invalidation logic with Reversal Exit

✅ Manual input of Greeks (Delta, Gamma, Theta, IV%)

✅ Greek-based alerts for Gamma Risk, IV Crush, Theta Decay

✅ Days to Expiry (DTE) tracking

✅ Fully customizable alert system

✅ Clean, emoji-labelled dashboard UI

✅ Built for Indian NSE options only

✅ Requires 1-second chart for correct data

________________________________________

📌 Option Symbol Inputs (LTP Tracking)

✅ Long Leg Symbol (Buy): Lower strike CE (Bull Call) or higher strike PE (Bear Put)

✅ Short Leg Symbol (Sell): Higher strike CE (Bull Call) or lower strike PE (Bear Put)

✅ Symbol Tips: Use TradingView's dropdown to select NSE option symbols like NSE:RELIANCE25JUL3000CE

⚠️ Providing valid option symbols is crucial — it powers all live tracking and calculations.

________________________________________

📌 Trade Setup Parameters

Spot Price at Entry

Long & Short Strike Prices

Buy Price (Long Leg)

Sell Price (Short Leg)

Lot Size & Number of Lots

Loss Bearable Amount (₹) → Used by Smart Exit logic to issue early warnings

________________________________________

📌 Expiry Date Input

Expiry Year, Month, and Day

🎯 Used to calculate Days to Expiry (DTE) and enable:

⏱️ Expiry alerts like “Less than 2 Days”, “Theta Risk”, and more

📉 Smart Exit logic adjusts based on time decay

________________________________________

📌 Greeks (Optional)

🔹 Default Mode: Don’t Enter Greeks

🔹 Optional Mode: Enter Greeks for both legs (Delta, Gamma, Theta, IV%)

🔍 Enabling Greeks unlocks:

Net Delta, Gamma, Theta, IV

Greek-based warnings (e.g. Gamma Risk, Theta Risk)

A dashboard Greek Verdict:

🟢 Conservative 🟡 Moderate Risk 🔴 Aggressive Risk

________________________________________

📌 Dashboard Display

🎯 Strategy Type (Bull or Bear Spread)

📈 Entry Premiums & Live LTPs

💹 Breakeven, Max Profit/Loss, Net Premium

📊 ROI % & Risk:Reward (with verdict)

📉 Real-time PnL using tick-by-tick data

🚦 Smart Exit verdict: Hold, Exit Soon, or Book Profit

🔁 Reversal Exit Price (spread invalidation logic)

📆 Days to Expiry (DTE)

📐 Greek Data (if enabled) with Net & Average values

⚠️ Greek Risk Verdict for managing directional risk

________________________________________

📌 Alert System (Built-in Alerts)

🎯 Target Profit Hit

❌ Max Loss Reached

🛑 Loss Bearable Limit Breached

📍 Hold Signal

📉 Book Loss / Exit Soon

⏳ Expiry Nearing

⚠️ Spread Invalidation Alert (via Reversal Price breach)

💥 High Gamma Risk (if Gamma > ±0.05)

📉 High IV Alert (if IV > 35%)

🚨 Combined Master Alert – fires if any key condition is triggered

________________________________________

📌 Smart Exit System

⚙️ Context-aware, dynamic trade assistant

✅ Analyses real-time market, PnL, expiry risk, reversal risk

✅ Gives exit suggestions based on:

Time decay

Price invalidation

Breach of defined loss/profit thresholds

✅ Keeps you objective — no emotional exits

________________________________________

📌 Reversal Exit Logic

🔁 Detects directional failure in spread structure

Bull Call Spread: Invalidation = Spot falls 25% of net premium below long strike

Bear Put Spread: Invalidation = Spot rises 25% of net premium above short strike

📉 Alerts you to exit even before loss appears

🎯 Designed for directional traders using spread logic

💡 Acts as a breakdown or breakout filter

________________________________________

⚠️ Important Notes

✅ Built for NSE Options – not for global exchanges

✅ Only for Bull Call & Bear Put spreads

✅ Use on 1-second chart only

❌ Will not work properly on higher timeframes

✅ Manual tool only – doesn’t place trades

✅ For educational and research use only

________________________________________

💬 How to Use This Dashboard

Choose Your Strategy

Bull Call or Bear Put

Input Symbols & Strikes

Use Tradingview dropdown to select accurate NSE option symbols

Enter Buy/Sell Prices

Add premiums, lot size, no. of lots

(Optional) Enable Greeks

Add Delta, Gamma, Theta, IV for both legs

Set Expiry Date

Year, Month, Day — activates DTE & expiry alerts

Monitor Dashboard

Live PnL, Max P/L, ROI, R:R, Smart Exit, Reversal Levels

(Optional) Enable Alerts

Get notified for PnL events, expiry risk, Greek risk, spread failure

________________________________________

🤝 Final Note

This tool was built with patience and care by @simpletradewithpatience to help fellow options traders trade more objectively, systematically, and confidently.

Feel free to share feedback on Tradingview.

Happy Trading! 📈

Stay disciplined. Stay smart.

________________________________________

🔠 Glossary

PnL – Profit & Loss

LTP – Last Traded Price

IV – Implied Volatility

DTE – Days to Expiry

ROI – Return on Investment

R:R – Risk to Reward Ratio

CE / PE – Call / Put Option

SEBI – Securities and Exchange Board of India

________________________________________

⚠️ Disclaimer

This script is for educational and research purposes only.

I am not a SEBI-registered advisor.

No buy or sell recommendations are made.

Trading options involves significant risk.

Use proper risk management and always consult a licensed advisor if in doubt.

The author is not responsible for any financial losses incurred.

By using this tool, you agree to these terms.

________________________________________

Simulated OI Proxy with Trend Table1. In Simple Terms

This script mimics open interest analysis using price and volume changes.

It visually marks possible bullish and bearish setups directly on your price chart.

It’s especially useful for markets where real OI data is not available (like Indian stocks)

=======================================================================

2. Calculating Price and Volume Changes

close - close: Calculates the change in closing price from the previous bar to the current bar.

volume - volume: Calculates the change in trading volume from the previous bar to the current bar.

Purpose:

These calculations help determine if price and volume are increasing or decreasing, which is used as a proxy for open interest (OI) since real OI data may not be available.

===================================================================

3. Proxy Logic for OI Signals

long_buildup: Both price and volume are rising. This suggests new buying interest (bullish signal).

short_buildup: Price is falling but volume is rising. This suggests new short positions are being opened (bearish signal).

short_covering: Price is rising but volume is falling. This suggests shorts are closing their positions, causing a price rise (cautiously bullish).

long_unwinding: Both price and volume are falling. This suggests long positions are being closed (cautiously bearish).

====================================================================

4. Plotting the Signals

plotshape(condition, ...): Draws a shape on the chart when the condition is true.

Long Buildup: Green triangle below the bar (bullish).

Short Buildup: Red triangle above the bar (bearish).

Short Covering: Blue circle below the bar (cautiously bullish).

Long Unwinding: Orange circle above the bar (cautiously bearish).

======================================================================

5. Signal Detection:

The script checks price and volume changes to determine which signal is active.

Trend Assignment:

It assigns a text label and color for the detected trend.

Table Display:

A table appears at the top-right of your chart, showing the current trend based on the latest bar.

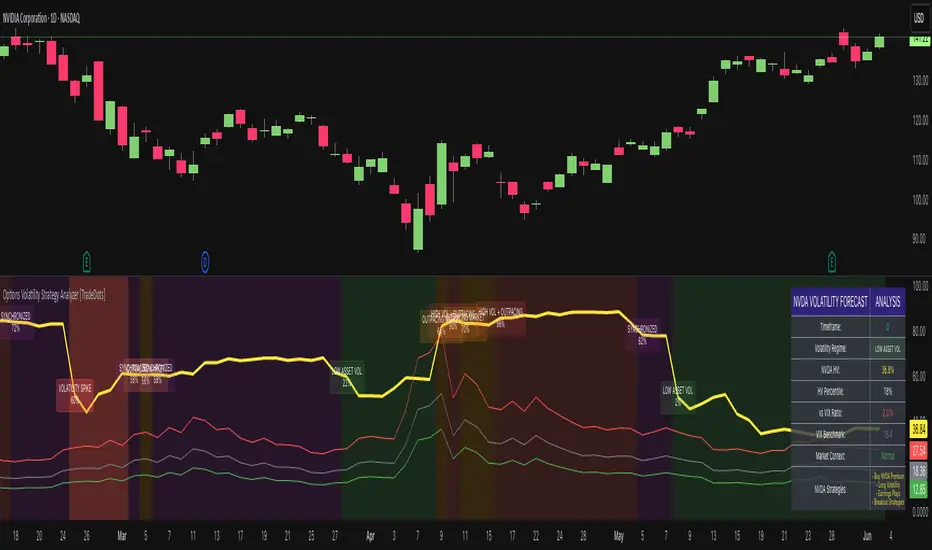

Options Volatility Strategy Analyzer [TradeDots]The Options Volatility Strategy Analyzer is a specialized tool designed to help traders assess market conditions through a detailed examination of historical volatility, market benchmarks, and percentile-based thresholds. By integrating multiple volatility metrics (including VIX and VIX9D) with color-coded regime detection, the script provides users with clear, actionable insights for selecting appropriate options strategies.

📝 HOW IT WORKS

1. Historical Volatility & Percentile Calculations

Annualized Historical Volatility (HV): The script automatically computes the asset’s historical volatility using log returns over a user-defined period. It then annualizes these values based on the chart’s timeframe, helping you understand the asset’s typical volatility profile.

Dynamic Percentile Ranks: To gauge where the current volatility level stands relative to past behavior, historical volatility values are compared against short, medium, and long lookback periods. Tracking these percentile ranks allows you to quickly see if volatility is high or low compared to historical norms.

2. Multi-Market Benchmark Comparison

VIX and VIX9D Integration: The script tracks market volatility through the VIX and VIX9D indices, comparing them to the asset’s historical volatility. This reveals whether the asset’s volatility is outpacing, lagging, or remaining in sync with broader market volatility conditions.

Market Context Analysis: A built-in term-structure check can detect market stress or relative calm by measuring how VIX compares to shorter-dated volatility (VIX9D). This helps you decide if the present environment is risk-prone or relatively stable.

3. Volatility Regime Detection

Color-Coded Background: The analyzer assigns a volatility regime (e.g., “High Asset Vol,” “Low Asset Vol,” “Outpacing Market,” etc.) based on current historical volatility percentile levels and asset vs. market ratios. A color-coded background highlights the regime, enabling traders to quickly interpret the market’s mood.

Alerts on Regime Changes & Spikes: Automated alerts warn you about any significant expansions or contractions in volatility, allowing you to react swiftly in changing conditions.

4. Strategy Forecast Table

Real-Time Strategy Suggestions: At the close of each bar, an on-chart table generates suggested options strategies (e.g., selling premium in high volatility or buying premium in low volatility). These suggestions provide a quick summary of potential tactics suited to the current regime.

Contextual Market Data: The table also displays key statistics, such as VIX levels, asset historical volatility percentile, or ratio comparisons, helping you confirm whether volatility conditions warrant more conservative or more aggressive strategies.

🛠️ HOW TO USE

1. Select Your Timeframe: The script supports multiple timeframes. For short-term trading, intraday charts often reveal faster shifts in volatility. For swing or position trading, daily or weekly charts may be more stable and produce fewer false signals.

2. Check the Volatility Regime: Observe the background color and on-chart labels to identify the current regime (e.g., “HIGH ASSET VOL,” “LOW VOL + LAGGING,” etc.).

3. Review the Forecast Table: The table suggests strategy ideas (e.g., iron condors, long straddles, ratio spreads) depending on whether volatility is elevated, subdued, or spiking. Use these as a starting point for designing trades that match your risk tolerance.

4. Combine with Additional Analysis: For optimal results, confirm signals with your broader trading plan, technical tools (moving averages, price action), and fundamental research. This script is most effective when viewed as one component in a comprehensive decision-making process.

❗️LIMITATIONS

Directional Neutrality: This indicator analyzes volatility environments but does not predict price direction (up/down). Traders must combine with directional analysis for complete strategy selection.

Late or Missed Signals: Since all calculations require a bar to close, sharp intrabar volatility moves may not appear in real-time.

False Positives in Choppy Markets: Rapid changes in percentile ranks or VIX movements can generate conflicting or premature regime shifts.

Data Sensitivity: Accuracy depends on the availability and stability of volatility data. Significant gaps or unusual market conditions may skew results.

Market Correlation Assumptions: The system assumes assets generally correlate with S&P 500 volatility patterns. May be less effective for:

Small-cap stocks with unique volatility drivers

International stocks with different market dynamics

Sector-specific events disconnected from broad market

Cryptocurrency-related assets with independent volatility patterns

RISK DISCLAIMER

Options trading involves substantial risk and is not suitable for all investors. Options strategies can result in significant losses, including the total loss of premium paid. The complexity of options strategies requires thorough understanding of the risks involved.

This indicator provides volatility analysis for educational and informational purposes only and should not be considered as investment advice. Past volatility patterns do not guarantee future performance. Market conditions can change rapidly, and volatility regimes may shift without warning.

No trading system can guarantee profits, and all trading involves the risk of loss. The indicator's regime classifications and strategy suggestions should be used as part of a comprehensive trading plan that includes proper risk management, directional analysis, and consideration of broader market conditions.

Options Chart Lite [Pt]█ Options Chart Lite

────────────────────────────

█ Introduction

Options Chart Lite is a simplified version of the full Options Chart+ tool — created for traders who want a clean and easy way to visualize option volume around price without extra complexity.

It displays live call and put volume and pricing directly on your TradingView chart, centered around the most relevant strikes for the selected expiry.

────────────────────────────

█ What Is Options Chart Lite ?

Options Chart Lite is a tool that shows real-time call and put activity in a clean, strike-by-strike table.

It provides:

- Side-by-side call/put volume and pricing

- Live table centered on current price

- Total call and put volume summary

- Quick insight into flow without overlays or clutter

────────────────────────────

█ Key Features

Visual Option Table

- Volume and price for calls and puts

- Table auto-centers around current price

- Up to 20 strikes shown

Total Volume Summary

- Call vs put volume shown at the bottom

Formatted Expiry + Timeframe

- Full expiry display (e.g. “Fri Apr 11, 2025”)

- Fixed to 1D timeframe

Reset & Warnings

- Button to reset strike range

- Optional delayed data notice

────────────────────────────

█ Inputs

Option Expiry Date (YYMMDD): Must match a valid expiry

Strike Increment: Strike spacing (e.g., 1, 2.5, 5)

Reference Strike Denominator: Rounds price to valid strike

Font Size Option: Choose Auto, Tiny, Small, or Normal

Reset Button: Re-centers if price moves

Delayed Data Warning: Toggle display of warning

────────────────────────────

█ Use Cases

Spot Key Strikes

See which strikes have the most activity.

Quick Flow Insights

Volume bias without opening an option chain.

Prep Levels

Align price action with strike flow.

Volume Skew Snapshot

Check if calls or puts dominate.

────────────────────────────

█ Known Limitations

- Invalid Expiry or Strike Inputs Will Error

Inputs must match real listed options for the symbol.

- Options Data Must Be Available

Volume will appear as 0 if TradingView data isn’t accessible.

- Strike Range is Limited

Script renders ~20 strikes. Use Reset Indicator if price moves too far.

Options Chart+ [Pt]█ Introduction

Since the launch of options data support on TradingView, the landscape for retail options traders has started to shift. But until now, no tool in the public TradingView library has offered a full-featured, visual-first interface for reading option strike activity directly from your chart.

www.tradingview.com

Options Chart+ changes that — bringing an institutional-style strike analysis interface to TradingView.

It reads the option chain for any symbol and expiry, dynamically builds a strike-by-strike volume and price table, highlights top areas of market activity, and helps you interpret directional sentiment through both total and skew-adjusted implied moves.

────────────────────────────

█ What Is Options Chart+ ?

Options Chart+ is a premium script for analyzing call and put option volumes and pricing for any option chain that's readily available on TradingView.

It provides a real-time, on-chart display of:

- Strike-Level Volume and Price Table

- Gradient Heatmaps for Volume Activity

- Overlayed Top Strikes on the Chart

- Implied Move and Directional Bias Metrics

By visualizing where options traders are concentrating their positioning, this tool helps uncover potential support/resistance zones, directional bets, and key gamma levels — all from the flow.

────────────────────────────

█ Key Features

Visual Option Chain Table

- Centers around the current price

- Real-time volume and price per strike

- Clean formatting with total summaries

Gradient Volume Coloring

- Highlights activity using customizable color gradients

- Makes volume spikes obvious at a glance

Top Strike Overlays

- Automatically highlights top volume call/put strikes

- Overlays labeled lines on the chart for price context

Implied Move and Directional Bias

- ATM straddle = Total Implied Move

- Volume-weighted extrinsics = Directional Implied Move (DIM)

- Shows skew-based bias: bullish or bearish

────────────────────────────

█ Inputs & Customization

Option Expiry Date (YYMMDD): Must match valid options for the symbol

Strike Increment: Matches strike spacing (e.g., 1, 2.5, 5)

Reference Strike Denominator: Rounds the center strike

Volume Timeframe: Any valid chart timeframe

Gradient Volume Coloring: Toggle on/off

Call/Put Volume Colors: Fully customizable

Draw Top Strike Lines: Enables chart overlays

Start / End Offset: Customize overlay length

Font Size: Auto, Tiny, Small, or Normal

Delayed Data Warning: Adds footnote in the table

Reset Button: Re-centers the tool if price moves too far

────────────────────────────

█ Use Cases

1. Spotting High-Interest Strikes

Use gradient heatmaps and overlays to see where volume is clustering.

Example: Heavy calls at 4200 may act as a magnet or gamma level — perfect for breakout or fade setups.

2. Interpreting Sentiment with DIM

Gauge where the flow is leaning directionally.

Example: Bullish DIM = call extrinsics outweigh puts → sentiment skewed bullish.

3. Sizing Risk Around Implied Movement

Use Total Implied Move to set range boundaries.

Example: Avoid selling premium inside the expected move unless risk is tight.

4. Combining Volume and Price Action

Overlay strikes with price structure for confluence trades.

Example: A heavy put strike with price holding = potential bounce zone.

5. Structuring Straddles or Strangles

Use volume skew to inform multi-leg positions.

Example: If call side is bid up, lean strangle wider to the upside.

────────────────────────────

█ Known Limitations

- Invalid Expiry or Strike Inputs Will Error

You are responsible for selecting a valid expiry and strike increment that matches the symbol’s listed options.

- Options Data Must Be Available

This tool depends on TradingView's options feed. If you do not have access (delayed or real-time), the script will fail to load.

- Strike Range is Limited

Renders ~20 strikes max to preserve clarity. If price moves beyond that, use the Reset Indicator input.

────────────────────────────

█ Final Thoughts

Options Chart+ is built for traders who operate on flow, structure, and sentiment. It lets you trade with confidence by showing where the real positioning is happening — visually, clearly, and in real-time.

If you:

- Think in terms of option flow

- Trade around volume levels or gamma exposure

- Want faster access to skew and sentiment

- Or just need clarity over chaos in an options chain...

This tool is for you.

Opening Range Breakout (ORB)This is an Opening Range Break indicator. Best if used on a 5 minute chart. It plots the opening 30 minutes high and low of a ticker. (meaning mostly for stocks, options, etfs) and then it alerts a buy signal upon break of opening high and a sell signal upon break of opening low. This is a day trading type of indicator and there is a new opening range everyday.

Monthly Options Expiration 2025Monthly Options Expiration 2025

Plots the monthly options expiration dates in advance for the year 2025.

Happy trading and all the best.

Option Time ValueThis TradingView script calculates and visualizes the time value of an option (Call or Put) based on its market price and intrinsic value. The time value represents the premium paid for the option above its intrinsic value, and it is a key metric for analyzing the cost of holding an option.

This script is suitable for traders analyzing options on indices or stocks, such as the NIFTY 50, and supports both Call and Put options. By dynamically extracting the strike price and option type from the input symbol, it adapts seamlessly to the selected instrument.

Key Features:

Dynamic Instrument Selection:

Users can input the underlying asset (e.g., NSE:NIFTY) and the specific option instrument (e.g., NSE:NIFTY250327C24000 for a Call or NSE:NIFTY250327P24000 for a Put).

Automatic Option Type Detection:

The script detects whether the option is a Call or a Put by parsing the input symbol for the characters "C" (Call) or "P" (Put).

Dynamic Strike Price Extraction:

The strike price is dynamically extracted from the input option symbol, eliminating the need for hardcoding and reducing user errors.

Key Metrics Plotted:

Time Value: The premium paid above the intrinsic value, plotted in blue.

Intrinsic Value: The calculated intrinsic value of the option, plotted in green.

Seamless Integration:

Designed for ease of use and integration into existing TradingView setups.

Automatically adjusts to the timeframe and pricing data of the selected instruments.

Options Cumulative Chart AnalysysThis Pine Script is a comprehensive tool designed for traders analyzing options data on TradingView. It aggregates multiple symbols to calculate and visualize cumulative performance, providing essential insights for decision-making.

Key Features:

Symbol and Strike Price Configuration:

Supports up to four configurable symbols (e.g., NIFTY options).

Allows defining buy/sell actions, quantities, and entry premiums for each symbol.

Customizable Chart Display:

Plot candlesticks and line charts for cumulative data.

Configurable Exponential Moving Averages (EMAs) for technical analysis.

Entry and price lines with customizable colors.

Timeframe Management:

Supports higher timeframe (HTF) candles.

Ensures compatibility with the current chart timeframe to maintain accuracy.

Dynamic Coloring and Visualization:

Red, green, and gray color schemes for body and wicks of candlesticks based on price movements.

Customizable positive and negative color schemes.

Table for Data Representation:

Displays an info table showing symbols, quantities, entry prices, and latest traded prices (LTP).

Adjustable table position, overlay, and styling.

Premium and Profit/Loss Calculations:

Calculates cumulative open, high, low, and close prices considering premiums and quantities.

Tracks the profit and loss dynamically based on cumulative premiums and market prices.

Alerts and Notifications:

Alerts triggered on specific conditions, such as when the profit/loss turns negative.

Modular Functions:

Functions for calculating high/low/open/close values, combining premiums, and drawing candlesticks.

Utilities for symbol management and security requests.

Custom Settings:

Includes a wide range of input options for customization:

Timeframes, EMA lengths, colors, table configurations, and more.

Error Handling:

Validates timeframe inputs to ensure compatibility and prevent runtime errors.

This script is designed for advanced traders looking for a customizable tool to analyze cumulative options data efficiently. By leveraging its modular design and visual elements, users can make informed trading decisions with a holistic view of market movements.

GEX Profile [PRO] Real Auto-Updated Gamma Exposure Levels𝗥𝗲𝗮𝗹 𝗚𝗘𝗫 𝗟𝗲𝘃𝗲𝗹𝘀 𝘄𝗶𝘁𝗵 𝗦𝗲𝗮𝗺𝗹𝗲𝘀𝘀 𝗔𝘂𝘁𝗼-𝗨𝗽𝗱𝗮𝘁𝗲𝘀 𝗳𝗼𝗿 𝗼𝘃𝗲𝗿 𝟭𝟲𝟱+ 𝗼𝗳 𝘁𝗵𝗲 𝗠𝗼𝘀𝘁 𝗟𝗶𝗾𝘂𝗶𝗱 𝗨.𝗦. 𝗠𝗮𝗿𝗸𝗲𝘁 𝗦𝘆𝗺𝗯𝗼𝗹𝘀 (including 𝟬𝗗𝗧𝗘 𝗳𝗼𝗿 𝗦𝗣𝗫, SPY, QQQ, TLT, IWM, etc...)

🔃 Dynamic Updates : Receive precise GEX levels with auto-updating metrics up to 5 times a day throughout the trading session—no manual refresh needed!

🍒 Strategically Developed : Built by experienced options traders to meet the needs of serious options market participants.

🕒 0DTE? No Problem! : Designed with 0DTE traders in mind, our indicator keeps you updated with GEX levels and seamless auto-refresh to capture every crucial market shift.

📈 Optimized for Option Traders : See accurate GEX and NETGEX profiles for multiple expirations to maximize strategic potential.

🔶 Comprehensive GEX Levels

This indicator provides unparalleled insight into market dynamics with levels like Call/Put Support, Resistance, HVL (High Volatility Level), and Call/Put Walls. These levels are auto-updated based on live market movements and reflect gamma shifts and volatility signals essential for options traders.

🔶 Ideal for 0DTE and Multi-Leg Strategies

Track essential GEX levels across expirations with our unique Cumulative (⅀) and Selected Alone (⊙) calculation models. Customize your view to reveal high-impact levels across multiple expirations or focus on a specific expiration for a targeted strategy.

🔶 Coverage of 165+ Highly Liquid U.S. Symbols

Compatible with over 165 U.S. market symbols, including SP:SPX , AMEX:SPY , NASDAQ:QQQ , NASDAQ:TLT , AMEX:GLD , NASDAQ:NVDA , and more. The watchlist is expanding continuously to meet the needs of active traders. List of Compatible Symbols Available Here: www.tradingview.com

🔶How does the indicator work and why is it unique?

This is not just another GEX indicator. It incorporates 15min delayed option chain data from ORATS as data provider, processes and refines the delayed data package using pineseed, and sends it to TradingView, visualizing the key GEX levels using specific formulas (see detailed below). This method of incorporating options data into a visualization framework is unique and entirely innovative on TradingView.

Unlike other providers that only set GEX levels at market open, this indicator adjusts dynamically throughout the day, providing updated insights across the trading day and capturing gamma shifts as the market moves.

_________________________________

-----------------------------------------------

🌑 𝗗 𝗢 𝗖 𝗨 𝗠 𝗘 𝗡 𝗧 𝗔 𝗧 𝗜 𝗢 𝗡 🌑

-----------------------------------------------

_________________________________

🔶 Understanding GEX (Gamma Exposure) and Gamma Profiling

Gamma Exposure (GEX) is a crucial concept in options trading because it reveals how options market positions can influence the dynamics of asset prices. In essence, GEX measures the collective gamma exposure of options market participants, impacting overall market stability and price movements.

🔹 What is GEX?

At its core, GEX captures the aggregate impact of gamma, a key options Greek, which tells us how an option's delta changes in response to price movements in the underlying asset. Positive or negative GEX levels can reflect the collective bullish or bearish stance of the market:

Positive GEX (far above HVL) : Indicates a net bullish positioning by options holders. When GEX is strongly positive, it suggests that as the asset price increases, market participants might need to buy more of the asset to maintain their hedges. This behavior can fuel further upward momentum.

Negative GEX (far below HVL) : Implies a net bearish positioning. In a strongly negative GEX environment, declines in the asset's price might prompt participants to sell, potentially exacerbating the downward movement.

🔹 The Influence of GEX on Strike Prices and Expiration

A unique feature of GEX is its impact near expiration dates. As options approach expiration, GEX levels can “pin” the price to specific strike levels, where options positions are concentrated. This pinning effect arises as market makers adjust their hedging strategies, often causing the asset price to gravitate towards certain strike prices, where a large volume of options contracts sits.

🟨 Overview of our GEX Calculation Models for Options Traders 🟨

Our GEX indicator models were developed with serious options traders in mind, providing flexibility beyond typical GEX providers. We know that using GEX levels for multi-leg strategies, where the underlying doesn't need a strong trend to be profitable , calls for a nuanced approach that aligns with different trading horizons. Here’s a detailed breakdown of our GEX calculation models and how they support strategic trading across varying timeframes.

Thus, the HVL an orher CALL/PUT WALLS depends on the indicator's selected calculation mode and expiration. The NETGEX profile of the chosen expiration appears on the HVL line , which automatically updates five times during trading hours , except for 0DTE, which reflects the value set at market open.

🔶 Cumulative Expiration (⅀) Calculation Method

This method aggregates GEX data for all expirations up to the selected date , giving you a more comprehensive view of market dynamics. We recommend using this method, as it allows you to see how combined expirations impact GEX levels, which can be critical when setting up trades with a longer time horizon.

🔶 Selected Alone (⊙) Calculation Method

This option displays the GEX profile specific to only the chosen expiration , providing a unique, time-bound view. This approach is ideal for those seeking precise insight into how an individual expiration is performing without the broader context of other expirations.

🔶 Example of using calculation methods:

With options trading, especially for multi-leg strategies, choosing the right expiration and calculation model is crucial. Let’s break down an example:

Suppose you’re considering a Friday (4DTE) front-leg diagonal on the SPX at the start of the week. In this case, the focus isn’t strictly on any single expiration (like 0DTE or 4DTE individually), but rather on what might happen cumulatively by Friday across all expirations . Here, the Cumulative Expiration (⅀) model comes into play, as it shows you an aggregated view of the GEX profile, factoring in all strikes and legs for all expirations leading up to the selected date.