Cash And Carry Arbitrage BTC Compare Month 6 by SeoNo1Detailed Explanation of the BTC Cash and Carry Arbitrage Script

Script Title: BTC Cash And Carry Arbitrage Month 6 by SeoNo1

Short Title: BTC C&C ABT Month 6

Version: Pine Script v5

Overlay: True (The indicators are plotted directly on the price chart)

Purpose of the Script

This script is designed to help traders analyze and track arbitrage opportunities between the spot market and futures market for Bitcoin (BTC). Specifically, it calculates the spread and Annual Percentage Yield (APY) from a cash-and-carry arbitrage strategy until a specific expiry date (in this case, June 27, 2025).

The strategy helps identify profitable opportunities when the futures price of BTC is higher than the spot price. Traders can then buy BTC in the spot market and short BTC futures contracts to lock in a risk-free profit.

1. Input Settings

Spot Symbol: The real-time BTC spot price from Binance (BTCUSDT).

Futures Symbol: The BTC futures contract that expires in June 2025 (BTCUSDM2025).

Expiry Date: The expiration date of the futures contract, set to June 27, 2025.

These inputs allow users to adjust the symbols or expiry date according to their trading needs.

2. Price Data Retrieval

Spot Price: Fetches the latest closing price of BTC from the spot market.

Futures Price: Fetches the latest closing price of BTC futures.

Spread: The difference between the futures price and the spot price (futures_price - spot_price).

The spread indicates how much higher (or lower) the futures price is compared to the spot market.

3. Time to Maturity (TTM) and Annual Percentage Yield (APY) Calculation

Current Date: Gets the current timestamp.

Time to Maturity (TTM): The number of days left until the futures contract expires.

APY Calculation:

Formula:

APY = ( Spread / Spot Price ) x ( 365 / TTM Days ) x 100

This represents the annualized return from holding a cash-and-carry arbitrage position if the trader buys BTC at the spot price and sells BTC futures.

4. Display Information Table on the Chart

A table is created on the chart's top-right corner showing the following data:

Metric: Labels such as Spread and APY

Value: Displays the calculated spread and APY

The table automatically updates at the latest bar to display the most recent data.

5. Alert Condition

This sets an alert condition that triggers every time the script runs.

In practice, users can modify this alert to trigger based on specific conditions (e.g., APY exceeds a threshold).

6. Plotting the APY and Spread

APY Plot: Displays the annualized yield as a blue line on the chart.

Spread Plot: Visualizes the futures-spot spread as a red line.

This helps traders quickly identify arbitrage opportunities when the spread or APY reaches desirable levels.

How to Use the Script

Monitor Arbitrage Opportunities:

A positive spread indicates a potential cash-and-carry arbitrage opportunity.

The larger the APY, the more profitable the arbitrage opportunity could be.

Timing Trades:

Execute a buy on the BTC spot market and simultaneously sell BTC futures when the APY is attractive.

Close both positions upon futures contract expiry to realize profits.

Risk Management:

Ensure you have sufficient margin to hold both positions until expiry.

Monitor funding rates and volatility, which could affect returns.

Conclusion

This script is an essential tool for traders looking to exploit price discrepancies between the BTC spot market and futures market through a cash-and-carry arbitrage strategy. It provides real-time data on spreads, annualized returns (APY), and visual alerts, helping traders make informed decisions and maximize their profit potential.

"2025年2月3日+美元指数+兑换欧元+汇率"に関するスクリプトを検索

Full Moon and New Moon IndicatorThe Full Moon & New Moon Indicator is a custom Pine Script indicator which marks Full Moon (Pournami) and New Moon (Amavasya) events on the price chart. This indicator helps traders who incorporate lunar cycles into their market analysis, as certain traders believe these cycles influence market sentiment and price action. The current script is added for the year 2024 and 2025 and the dates are considered as per the Telugu calendar.

Features

✅ Identifies and labels Full Moon & New Moon days on the chart for the year 2024 and 2025

How it Works!

On a Full Moon day, it places a yellow label ("Pournami") above the corresponding candle.

On a New Moon day, it places a blue label ("Amavasya") above the corresponding candle.

Example Usage

When a Full Moon label appears, check for potential trend reversals or high volatility.

When a New Moon label appears, watch for market consolidation or a shift in sentiment.

Combine with candlestick patterns, support/resistance, or momentum indicators for a stronger trading setup.

🚀 Add this indicator to your TradingView chart and explore the market’s reaction to lunar cycles! 🌕

TASC 2025.03 A New Solution, Removing Moving Average Lag█ OVERVIEW

This script implements a novel technique for removing lag from a moving average, as introduced by John Ehlers in the "A New Solution, Removing Moving Average Lag" article featured in the March 2025 edition of TASC's Traders' Tips .

█ CONCEPTS

In his article, Ehlers explains that the average price in a time series represents a statistical estimate for a block of price values, where the estimate is positioned at the block's center on the time axis. In the case of a simple moving average (SMA), the calculation moves the analyzed block along the time axis and computes an average after each new sample. Because the average's position is at the center of each block, the SMA inherently lags behind price changes by half the data length.

As a solution to removing moving average lag, Ehlers proposes a new projected moving average (PMA) . The PMA smooths price data while maintaining responsiveness by calculating a projection of the average using the data's linear regression slope.

The slope of linear regression on a block of financial time series data can be expressed as the covariance between prices and sample points divided by the variance of the sample points. Ehlers derives the PMA by adding this slope across half the data length to the SMA, creating a first-order prediction that substantially reduces lag:

PMA = SMA + Slope * Length / 2

In addition, the article includes methods for calculating predictions of the PMA and the slope based on second-order and fourth-order differences. The formulas for these predictions are as follows:

PredictPMA = PMA + 0.5 * (Slope - Slope ) * Length

PredictSlope = 1.5 * Slope - 0.5 * Slope

Ehlers suggests that crossings between the predictions and the original values can help traders identify timely buy and sell signals.

█ USAGE

This indicator displays the SMA, PMA, and PMA prediction for a specified series in the main chart pane, and it shows the linear regression slope and prediction in a separate pane. Analyzing the difference between the PMA and SMA can help to identify trends. The differences between PMA or slope and its corresponding prediction can indicate turning points and potential trade opportunities.

The SMA plot uses the chart's foreground color, and the PMA and slope plots are blue by default. The plots of the predictions have a green or red hue to signify direction. Additionally, the indicator fills the space between the SMA and PMA with a green or red color gradient based on their differences:

Users can customize the source series, data length, and plot colors via the inputs in the "Settings/Inputs" tab.

█ NOTES FOR Pine Script® CODERS

The article's code implementation uses a loop to calculate all necessary sums for the slope and SMA calculations. Ported into Pine, the implementation is as follows:

pma(float src, int length) =>

float PMA = 0., float SMA = 0., float Slope = 0.

float Sx = 0.0 , float Sy = 0.0

float Sxx = 0.0 , float Syy = 0.0 , float Sxy = 0.0

for count = 1 to length

float src1 = src

Sx += count

Sy += src

Sxx += count * count

Syy += src1 * src1

Sxy += count * src1

Slope := -(length * Sxy - Sx * Sy) / (length * Sxx - Sx * Sx)

SMA := Sy / length

PMA := SMA + Slope * length / 2

However, loops in Pine can be computationally expensive, and the above loop's runtime scales directly with the specified length. Fortunately, Pine's built-in functions often eliminate the need for loops. This indicator implements the following function, which simplifies the process by using the ta.linreg() and ta.sma() functions to calculate equivalent slope and SMA values efficiently:

pma(float src, int length) =>

float Slope = ta.linreg(src, length, 0) - ta.linreg(src, length, 1)

float SMA = ta.sma(src, length)

float PMA = SMA + Slope * length * 0.5

To learn more about loop elimination in Pine, refer to this section of the User Manual's Profiling and optimization page.

TASC 2025.02 Autocorrelation Indicator█ OVERVIEW

This script implements the Autocorrelation Indicator introduced by John Ehlers in the "Drunkard's Walk: Theory And Measurement By Autocorrelation" article from the February 2025 edition of TASC's Traders' Tips . The indicator calculates the autocorrelation of a price series across several lags to construct a periodogram , which traders can use to identify market cycles, trends, and potential reversal patterns.

█ CONCEPTS

Drunkard's walk

A drunkard's walk , formally known as a random walk , is a type of stochastic process that models the evolution of a system or variable through successive random steps.

In his article, John Ehlers relates this model to market data. He discusses two first- and second-order partial differential equations, modified for discrete (non-continuous) data, that can represent solutions to the discrete random walk problem: the diffusion equation and the wave equation. According to Ehlers, market data takes on a mixture of two "modes" described by these equations. He theorizes that when "diffusion mode" is dominant, trading success is almost a matter of luck, and when "wave mode" is dominant, indicators may have improved performance.

Pink spectrum

John Ehlers explains that many recent academic studies affirm that market data has a pink spectrum , meaning the power spectral density of the data is proportional to the wavelengths it contains, like pink noise . A random walk with a pink spectrum suggests that the states of the random variable are correlated and not independent. In other words, the random variable exhibits long-range dependence with respect to previous states.

Autocorrelation function (ACF)

Autocorrelation measures the correlation of a time series with a delayed copy, or lag , of itself. The autocorrelation function (ACF) is a method that evaluates autocorrelation across a range of lags , which can help to identify patterns, trends, and cycles in stochastic market data. Analysts often use ACF to detect and characterize long-range dependence in a time series.

The Autocorrelation Indicator evaluates the ACF of market prices over a fixed range of lags, expressing the results as a color-coded heatmap representing a dynamic periodogram. Ehlers suggests the information from the periodogram can help traders identify different market behaviors, including:

Cycles : Distinguishable as repeated patterns in the periodogram.

Reversals : Indicated by sharp vertical changes in the periodogram when the indicator uses a short data length .

Trends : Indicated by increasing correlation across lags, starting with the shortest, over time.

█ USAGE

This script calculates the Autocorrelation Indicator on an input "Source" series, smoothed by Ehlers' UltimateSmoother filter, and plots several color-coded lines to represent the periodogram's information. Each line corresponds to an analyzed lag, with the shortest lag's line at the bottom of the pane. Green hues in the line indicate a positive correlation for the lag, red hues indicate a negative correlation (anticorrelation), and orange or yellow hues mean the correlation is near zero.

Because Pine has a limit on the number of plots for a single indicator, this script divides the periodogram display into three distinct ranges that cover different lags. To see the full periodogram, add three instances of this script to the chart and set the "Lag range" input for each to a different value, as demonstrated in the chart above.

With a modest autocorrelation length, such as 20 on a "1D" chart, traders can identify seasonal patterns in the price series, which can help to pinpoint cycles and moderate trends. For instance, on the daily ES1! chart above, the indicator shows repetitive, similar patterns through fall 2023 and winter 2023-2024. The green "triangular" shape rising from the zero lag baseline over different time ranges corresponds to seasonal trends in the data.

To identify turning points in the price series, Ehlers recommends using a short autocorrelation length, such as 2. With this length, users can observe sharp, sudden shifts along the vertical axis, which suggest potential turning points from upward to downward or vice versa.

Highs & Lows RTH/OVN/IBs/D/W/M/YOverview

Plots the highs and lows of RTH, OVN/ETH, IBs of those sessions, previous Day, Week, Month, and Year.

Features

Allows the user to enable/disable plotting the high/low of each period.

Lines' length, offset, and colors can be customized

Labels' position, size, color, and style can be customized

Support

Questions, feedbacks, and requests are welcomed. Please feel free to use Comments or direct private message via TradingView.

Disclaimer

This stock chart indicator provided is for informational purposes only and should not be considered as financial or investment advice. The data and information presented in this indicator are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy.

Users should be aware that:

Any investment decisions made based on this indicator are at your own risk.

The creators and providers of this indicator disclaim all liability for any losses, damages, or other consequences resulting from its use. By using this stock chart indicator, you acknowledge and accept the inherent risks associated with trading and investing in financial markets.

Release Date: 2025-01-17

Release Version: v1 r1

Release Notes Date: 2025-01-17

TASC 2025.01 Linear Predictive Filters█ OVERVIEW

This script implements a suite of tools for identifying and utilizing dominant cycles in time series data, as introduced by John Ehlers in the "Linear Predictive Filters And Instantaneous Frequency" article featured in the January 2025 edition of TASC's Traders' Tips . Dominant cycle information can help traders adapt their indicators and strategies to changing market conditions.

█ CONCEPTS

Conventional technical indicators and strategies often rely on static, unchanging parameters, which may fail to account for the dynamic nature of market data. In his article, John Ehlers applies digital signal processing principles to address this issue, introducing linear predictive filters to identify cyclic information for adapting indicators and strategies to evolving market conditions.

This approach treats market data as a complex series in the time domain. Analyzing the series in the frequency domain reveals information about its cyclic components. To reduce the impact of frequencies outside a range of interest and focus on a specific range of cycles, Ehlers applies second-order highpass and lowpass filters to the price data, which attenuate or remove wavelengths outside the desired range. This band-limited analysis isolates specific parts of the frequency spectrum for various trading styles, e.g., longer wavelengths for position trading or shorter wavelengths for swing trading.

After filtering the series to produce band-limited data, Ehlers applies a linear predictive filter to predict future values a few bars ahead. The filter, calculated based on the techniques proposed by Lloyd Griffiths, adaptively minimizes the error between the latest data point and prediction, successively adjusting its coefficients to align with the band-limited series. The filter's coefficients can then be applied to generate an adaptive estimate of the band-limited data's structure in the frequency domain and identify the dominant cycle.

█ USAGE

This script implements the following tools presented in the article:

Griffiths Predictor

This tool calculates a linear predictive filter to forecast future data points in band-limited price data. The crosses between the prediction and signal lines can provide potential trade signals.

Griffiths Spectrum

This tool calculates a partial frequency spectrum of the band-limited price data derived from the linear predictive filter's coefficients, displaying a color-coded representation of the frequency information in the pane. This mode's display represents the data as a periodogram . The bottom of each plotted bar corresponds to a specific analyzed period (inverse of frequency), and the bar's color represents the presence of that periodic cycle in the time series relative to the one with the highest presence (i.e., the dominant cycle). Warmer, brighter colors indicate a higher presence of the cycle in the series, whereas darker colors indicate a lower presence.

Griffiths Dominant Cycle

This tool compares the cyclic components within the partial spectrum and identifies the frequency with the highest power, i.e., the dominant cycle . Traders can use this dominant cycle information to tune other indicators and strategies, which may help promote better alignment with dynamic market conditions.

Notes on parameters

Bandpass boundaries:

In the article, Ehlers recommends an upper bound of 125 bars or higher to capture longer-term cycles for position trading. He recommends an upper bound of 40 bars and a lower bound of 18 bars for swing trading. If traders use smaller lower bounds, Ehlers advises a minimum of eight bars to minimize the potential effects of aliasing.

Data length:

The Griffiths predictor can use a relatively small data length, as autocorrelation diminishes rapidly with lag. However, for optimal spectrum and dominant cycle calculations, the length must match or exceed the upper bound of the bandpass filter. Ehlers recommends avoiding excessively long lengths to maintain responsiveness to shorter-term cycles.

Ripple (XRP) Model PriceAn article titled Bitcoin Stock-to-Flow Model was published in March 2019 by "PlanB" with mathematical model used to calculate Bitcoin model price during the time. We know that Ripple has a strong correlation with Bitcoin. But does this correlation have a definite rule?

In this study, we examine the relationship between bitcoin's stock-to-flow ratio and the ripple(XRP) price.

The Halving and the stock-to-flow ratio

Stock-to-flow is defined as a relationship between production and current stock that is out there.

SF = stock / flow

The term "halving" as it relates to Bitcoin has to do with how many Bitcoin tokens are found in a newly created block. Back in 2009, when Bitcoin launched, each block contained 50 BTC, but this amount was set to be reduced by 50% every 210,000 blocks (about 4 years). Today, there have been three halving events, and a block now only contains 6.25 BTC. When the next halving occurs, a block will only contain 3.125 BTC. Halving events will continue until the reward for minors reaches 0 BTC.

With each halving, the stock-to-flow ratio increased and Bitcoin experienced a huge bull market that absolutely crushed its previous all-time high. But what exactly does this affect the price of Ripple?

Price Model

I have used Bitcoin's stock-to-flow ratio and Ripple's price data from April 1, 2014 to November 3, 2021 (Daily Close-Price) as the statistical population.

Then I used linear regression to determine the relationship between the natural logarithm of the Ripple price and the natural logarithm of the Bitcoin's stock-to-flow (BSF).

You can see the results in the image below:

Basic Equation : ln(Model Price) = 3.2977 * ln(BSF) - 12.13

The high R-Squared value (R2 = 0.83) indicates a large positive linear association.

Then I "winsorized" the statistical data to limit extreme values to reduce the effect of possibly spurious outliers (This process affected less than 4.5% of the total price data).

ln(Model Price) = 3.3297 * ln(BSF) - 12.214

If we raise the both sides of the equation to the power of e, we will have:

============================================

Final Equation:

■ Model Price = Exp(- 12.214) * BSF ^ 3.3297

Where BSF is Bitcoin's stock-to-flow

============================================

If we put current Bitcoin's stock-to-flow value (54.2) into this equation we get value of 2.95USD. This is the price which is indicated by the model.

There is a power law relationship between the market price and Bitcoin's stock-to-flow (BSF). Power laws are interesting because they reveal an underlying regularity in the properties of seemingly random complex systems.

I plotted XRP model price (black) over time on the chart.

Estimating the range of price movements

I also used several bands to estimate the range of price movements and used the residual standard deviation to determine the equation for those bands.

Residual STDEV = 0.82188

ln(First-Upper-Band) = 3.3297 * ln(BSF) - 12.214 + Residual STDEV =>

ln(First-Upper-Band) = 3.3297 * ln(BSF) – 11.392 =>

■ First-Upper-Band = Exp(-11.392) * BSF ^ 3.3297

In the same way:

■ First-Lower-Band = Exp(-13.036) * BSF ^ 3.3297

I also used twice the residual standard deviation to define two extra bands:

■ Second-Upper-Band = Exp(-10.570) * BSF ^ 3.3297

■ Second-Lower-Band = Exp(-13.858) * BSF ^ 3.3297

These bands can be used to determine overbought and oversold levels.

Estimating of the future price movements

Because we know that every four years the stock-to-flow ratio, or current circulation relative to new supply, doubles, this metric can be plotted into the future.

At the time of the next halving event, Bitcoins will be produced at a rate of 450 BTC / day. There will be around 19,900,000 coins in circulation by August 2025

It is estimated that during first year of Bitcoin (2009) Satoshi Nakamoto (Bitcoin creator) mined around 1 million Bitcoins and did not move them until today. It can be debated if those coins might be lost or Satoshi is just waiting still to sell them but the fact is that they are not moving at all ever since. We simply decrease stock amount for 1 million BTC so stock to flow value would be:

BSF = (19,900,000 – 1.000.000) / (450 * 365) =115.07

Thus, Bitcoin's stock-to-flow will increase to around 115 until AUG 2025. If we put this number in the equation:

Model Price = Exp(- 12.214) * 114 ^ 3.3297 = 36.06$

Ripple has a fixed supply rate. In AUG 2025, the total number of coins in circulation will be about 56,000,000,000. According to the equation, Ripple's market cap will reach $2 trillion.

Note that these studies have been conducted only to better understand price movements and are not a financial advice.

US Elections Democrate-Republicain (1920-2025)This script shows the different U.S. presidents and indicates whether each was Democratic or Republican. It allows users to analyze the market based on the president in office.

CAP - KC/AC 2.20462 Converter// ───────────────────────────────────────────────────────────────────────────────

// Purpose: Conversion Indicator for ICE “C” (KC) and “C Metric” (AC) Contracts

//

// Background:

// - The Intercontinental Exchange (ICE) is phasing out the legacy Coffee “C” contract (symbol: KC),

// which has been quoted in U.S. cents per pound, and replacing it with the new Coffee “C Metric” contract (symbol: AC),

// quoted in U.S. dollars per metric ton :contentReference {index=0}.

// - The final KC futures expire in March 2028; AC contracts begin trading in September 2025 and use modern specifications

// including pricing per metric ton and flexible bulk delivery formats :contentReference {index=1}.

//

// Why this script matters:

// - Traders are accustomed to the KC pricing format (¢/lb); the AC contract’s USD/MT may create confusion.

// - This indicator visually converts the current chart price—whether from KC or AC contracts—directly into its equivalent unit,

// helping traders quickly assess parity and compare trends across both contract types.

// - It simplifies head-to-head comparison during this transition period, improving clarity on chart price behavior.

//

// Usage instructions:

// - If the symbol starts with "KC", the script divides the price by 2.20462 to convert from ¢/lb to approximate ¢/kg.

// - If the symbol starts with "AC", the script multiplies the price by 2.20462 to reverse the conversion.

// - The results (converted values) are displayed in a table for immediate visual clarity.

// ───────────────────────────────────────────────────────────────────────────────

Futubull VWAPTo apply Futubull’s VWAP (Volume Weighted Average Price) indicator to TradingView, the key is to understand Futubull’s VWAP calculation logic and features, then replicate them using TradingView’s Pine Script language. Below are detailed steps and methods, incorporating the provided context and prior discussions, to help you create a custom VWAP indicator in TradingView that mirrors Futubull’s functionality. The script will be tailored for day trading CIEN (Ciena Corporation) on September 4, 2025, during pre-market (Hong Kong time 11:25 PM, equivalent to US Eastern Time 11:25 AM), leveraging its earnings-driven breakout ($115.50, +21.81%).

BBMA Enhanced Pro - Multi-Timeframe Band Breakout StrategyShort Title : BBMA Pro

Overview

The BBMA Enhanced Pro is a professional-grade trading indicator that builds on the Bollinger Bands Moving Average (BBMA) strategy, pioneered by Omar Ali , a Malaysian forex trader and educator. Combining Bollinger Bands with Weighted Moving Averages (WMA) , this indicator identifies high-probability breakout and reversal opportunities across multiple timeframes. With advanced features like multi-timeframe Extreme signal detection, eight professional visual themes, and a dual-mode dashboard, it’s designed for traders seeking precision in trending and consolidating markets. Optimized for dark chart backgrounds, it’s ideal for forex, stocks, and crypto trading.

History

The BBMA strategy was developed by Omar Ali (BBMA Oma Ally) in the early 2010s, gaining popularity in the forex trading community, particularly in Southeast Asia. Building on John Bollinger’s Bollinger Bands, Omar Ali integrated Weighted Moving Averages and a multi-timeframe approach to create a structured system for identifying reversals, breakouts, and extreme conditions. The BBMA Enhanced Pro refines this framework with modern features like real-time dashboards and customizable visualizations, making it accessible to both novice and experienced traders.

Key Features

Multi-Timeframe Extreme Signals : Detects Extreme signals (overbought/oversold conditions) on both current and higher timeframes simultaneously, a rare feature that enhances signal reliability through trend alignment.

Professional Visual Themes : Eight distinct themes (e.g., Neon Contrast, Fire Gradient) optimized for dark backgrounds.

Dual-Mode Dashboard : Choose between Full Professional (detailed metrics) or Simplified Trader (essential info with custom notes).

Bollinger Band Squeeze Detection : Identifies low volatility periods (narrow bands) signaling potential sideways markets or breakouts.

Confirmation Labels : Displays labels when current timeframe signals align with recent higher timeframe signals, highlighting potential consolidations or squeezes.

Timeframe Validation : Prevents selecting the same timeframe for current and higher timeframe analysis.

Customizable Visualization : Toggle signal dots, EMA 50, and confirmation labels for a clean chart experience.

How It Works

The BBMA Enhanced Pro combines Bollinger Bands (20-period SMA, ±2 standard deviations) with WMA (5 and 10 periods) to generate trade signals:

Buy Signal : WMA 5 Low crosses above the lower Bollinger Band, indicating a recovery from an oversold condition (Extreme buy).

Sell Signal : WMA 5 High crosses below the upper Bollinger Band, signaling a rejection from an overbought condition (Extreme sell).

Extreme Signals : Occur when prices or WMAs move significantly beyond the Bollinger Bands (±2σ), indicating statistically rare overextensions. These often coincide with Bollinger Band Squeezes (narrow bands, low standard deviation), signaling potential sideways markets or impending breakouts.

Multi-Timeframe Confirmation : The indicator’s unique strength is its ability to detect Extreme signals on both the current and higher timeframe (HTF) within the same chart. When the HTF generates an Extreme signal (e.g., buy), and the current timeframe follows with an identical signal, it suggests the lower timeframe is aligning with the HTF’s trend, increasing reliability. Labels appear only when this alignment occurs within a user-defined lookback period (default: 50 bars), highlighting periods of band contraction across timeframes.

Bollinger Band Squeeze : Narrow bands (low standard deviation) indicate reduced volatility, often preceding consolidation or breakouts. The indicator’s dashboard tracks band width, helping traders anticipate these phases.

Why Multi-Timeframe Extremes Matter

The BBMA Enhanced Pro’s multi-timeframe approach is rare and powerful. When the higher timeframe shows an Extreme signal followed by a similar signal on the current timeframe, it suggests the market is following the HTF’s trend or entering a consolidation phase. For example:

HTF Sideways First : If the HTF Bollinger Bands are shrinking (low volatility, low standard deviation), it signals a potential sideways market. Waiting for the current timeframe to show a similar Extreme signal confirms this consolidation, reducing the risk of false breakouts.

Risk Management : By requiring HTF confirmation, the indicator encourages traders to lower risk during uncertain periods, waiting for both timeframes to align in a low-volatility state before acting.

Usage Instructions

Select Display Mode :

Current TF Only : Shows Bollinger Bands and WMAs on the chart’s timeframe.

Higher TF Only : Displays HTF bands and WMAs.

Both Timeframes : Combines both for comprehensive analysis.

Choose Higher Timeframe : Select from 1min to 1D (e.g., 15min, 1hr). Ensure it differs from the current timeframe to avoid validation errors.

Enable Signal Dots : Visualize buy/sell Extreme signals as dots, sourced from current, HTF, or both timeframes.

Toggle Confirmation Labels : Display labels when current timeframe Extremes align with recent HTF Extremes, signaling potential squeezes or consolidations.

Customize Dashboard :

Full Professional Mode : View metrics like BB width, WMA trend, and last signal.

Simplified Trader Mode : Focus on essential info with custom trader notes.

Select Visual Theme : Choose from eight themes (e.g., Ice Crystal, Royal Purple) for optimal chart clarity.

Trading Example

Setup : 5min chart, HTF set to 1hr, signal dots and confirmation labels enabled.

Buy Scenario : On the 5min chart, WMA 5 Low crosses above the lower Bollinger Band (Extreme buy), confirmed by a recent 1hr Extreme buy signal within 50 bars. The dashboard shows narrow bands (squeeze), and a green label appears.

Action : Enter a long position, targeting the middle band, with a stop-loss below the recent low. The HTF confirmation suggests a strong trend or consolidation phase.

Sell Scenario : WMA 5 High crosses below the upper Bollinger Band on the 5min chart, confirmed by a recent 1hr Extreme sell signal. The dashboard indicates a squeeze, and a red label appears.

Action : Enter a short position, targeting the middle band, with a stop-loss above the recent high. The aligned signals suggest a potential reversal or sideways market.

Customization Options

BBMA Display Mode : Current TF Only, Higher TF Only, or Both Timeframes.

Higher Timeframe : 1min to 1D.

Visual Theme : Eight professional themes (e.g., Neon Contrast, Forest Glow).

Line Style : Smooth or Step Line for HTF plots.

Signal Dots : Enable/disable, select timeframe source (Current, Higher, or Both).

Confirmation Labels : Toggle and set lookback window (1-100 bars).

Dashboard : Enable/disable, choose mode (Full/Simplified), and set position (Top Right, Bottom Left, etc.).

Notes

Extreme Signals and Squeezes : Extreme signals often occur during Bollinger Band contraction (low standard deviation), signaling potential sideways markets or breakouts. Use HTF confirmation to filter false signals.

Risk Management : If the HTF shows a squeeze (narrow bands), wait for the current timeframe to confirm with an Extreme signal to reduce risk in choppy markets.

Limitations : Avoid trading Extremes in highly volatile markets without additional confirmation (e.g., volume, RSI).

Author Enhanced Professional Edition, inspired by Omar Ali’s BBMA strategy

Version : 6.0 Pro - Simplified

Last Updated : September 2025

License : Mozilla Public License 2.0

We’d love to hear your feedback! Share your thoughts or questions in the comments below.

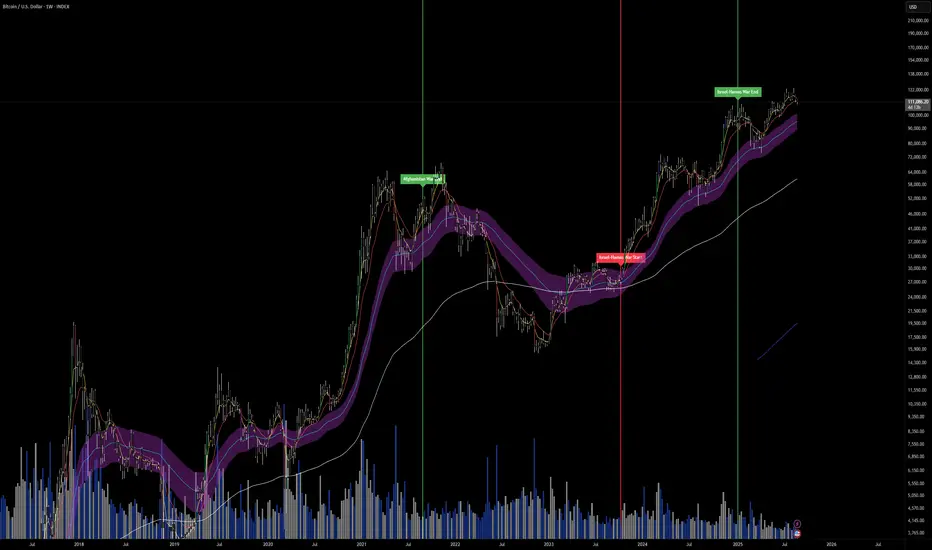

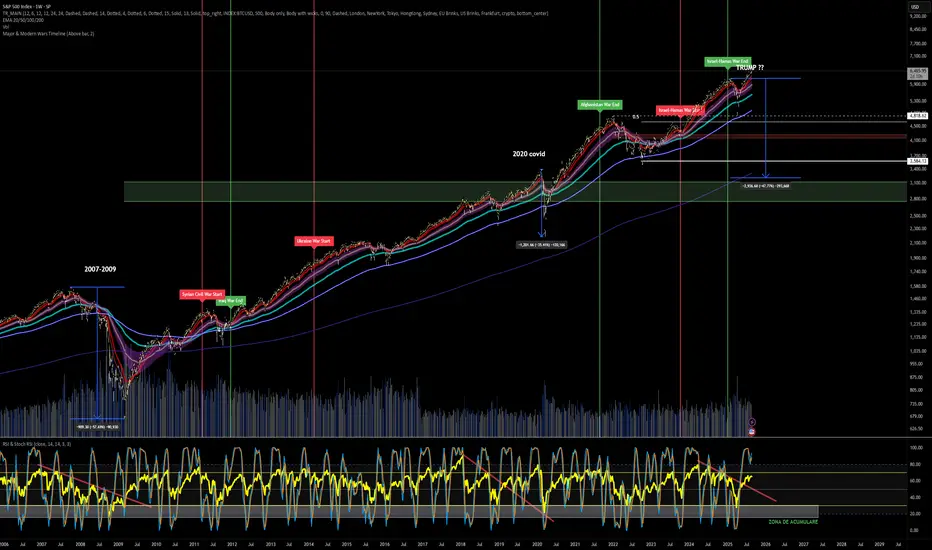

Major & Modern Wars TimelineDescription:

This indicator overlays vertical lines and labels on your chart to mark the start and end dates of major global wars and modern conflicts.

Features:

Displays start (red line + label) and end (green line + label) for each war.

Covers 20th century wars (World War I, World War II, Korean War, Vietnam War, Gulf War, Afghanistan, Iraq).

Includes modern conflicts: Syrian Civil War, Ukraine War, and Israel–Hamas War.

For ongoing conflicts, the end date is set to 2025 for timeline visualization.

Customizable: label position (above/below bar), line width.

Works on any chart timeframe, overlaying events on financial data.

Use case:

Useful for historical market analysis (e.g., gold, oil, S&P 500), helping traders and researchers see how wars and conflicts align with market movements.

Major & Modern Wars TimelineDescription:

This indicator overlays vertical lines and labels on your chart to mark the start and end dates of major global wars and modern conflicts.

Features:

Displays start (red line + label) and end (green line + label) for each war.

Covers 20th century wars (World War I, World War II, Korean War, Vietnam War, Gulf War, Afghanistan, Iraq).

Includes modern conflicts: Syrian Civil War, Ukraine War, and Israel–Hamas War.

For ongoing conflicts, the end date is set to 2025 for timeline visualization.

Customizable: label position (above/below bar), line width.

Works on any chart timeframe, overlaying events on financial data.

Use case:

Useful for historical market analysis (e.g., gold, oil, S&P 500), helping traders and researchers see how wars and conflicts align with market movements.

Sorry Cryptoface Market Cypher B//@version=5

indicator("Sorry Cryptoface Market Cypher B", shorttitle="SorryCF B", overlay=false)

// 🙏 Respect to Cryptoface

// Market Cipher is the brainchild of Cryptoface, who popularized the

// combination of WaveTrend, Money Flow, RSI, and divergence signals into a

// single package that has helped thousands of traders visualize momentum.

// This script is *not* affiliated with or endorsed by him — it’s just an

// open-source educational re-implementation inspired by his ideas.

// Whether you love him or not, Cryptoface deserves credit for taking complex

// oscillator theory and making it accessible to everyday traders.

// -----------------------------------------------------------------------------

// Sorry Cryptoface Market Cypher B

//

// ✦ What it is

// A de-cluttered, optimized rework of the popular Market Cipher B concept.

// This fork strips out repaint-prone code and redundant signals, adds

// higher-timeframe and trend filters, and introduces volatility &

// money-flow gating to cut down on the "confetti signals" problem.

//

// ✦ Key Changes vs. Original MC-B

// - Non-repainting security(): switched to request.security(..., lookahead_off)

// - Inputs updated to Pine v5 (input.int, input.float, etc.)

// - Trend filter: EMA or HTF WaveTrend required for alignment

// - Volatility filter: minimum ADX & ATR % threshold to avoid chop

// - Money Flow filter: signals require minimum |MFI| magnitude

// - WaveTrend slope check: reject flat or contra-slope crosses

// - Cooldown filter: prevents multiple signals within N bars

// - Bar close confirmation: dots/alerts only fire once a candle is closed

// - Hidden divergences + “second range” divergences disabled by default

// (to reduce noise) but can be toggled on

//

// ✦ Components

// - WaveTrend oscillator (2-line system + VWAP line)

// - Money Flow Index + RSI overlay

// - Stochastic RSI

// - Divergence detection (WT, RSI, Stoch)

// - Optional Schaff Trend Cycle

// - Optional Sommi flags/diamonds (HTF confluence markers)

//

// ✦ Benefits

// - Fewer false positives in sideways markets

// - Signals aligned with trend & volatility regimes

// - Removes repaint artifacts from higher-timeframe sources

// - Cleaner chart (reduced “dot spam”)

// - Still flexible: all original toggles/visuals retained

//

// ✦ Notes

// - This is NOT the official Market Cipher.

// - Educational / experimental use only. Do your own testing.

// - Best tested on 2H–4H timeframes; short TFs may still look choppy

//

// ✦ Credits

// Original open-source inspirations by LazyBear, RicardoSantos, LucemAnb,

// falconCoin, dynausmaux, andreholanda73, TradingView community.

// This fork modified by Lumina+Thomas (2025).

// -----------------------------------------------------------------------------

MATEOANUBISANTIDear traders, investors, and market enthusiasts,

We are excited to share our High-Low Indicator Range for on . This report aims to provide a clear and precise overview of the highest and lowest values recorded by during this specific hour, equipping our community with a valuable tool for making informed and strategic market decisions.

MATEOANUBISANTI-BILLIONSQUATDear traders, investors, and market enthusiasts,

We are excited to share our High-Low Indicator Range for on . This report aims to provide a clear and precise overview of the highest and lowest values recorded by during this specific hour, equipping our community with a valuable tool for making informed and strategic market decisions.

Kitti-Playbook ATR Study R0

Date : Aug 22 2025

Kitti-Playbook ATR Study R0

This is used to study the operation of the ATR Trailing Stop on the Long side, starting from the calculation of True Range.

1) Studying True Range Calculation

1.1) Specify the Bar graph you want to analyze for True Range.

Enable "Show Selected Price Bar" to locate the desired bar.

1.2) Enable/disable "Display True Range" in the Settings.

True Range is calculated as:

TR = Max (|H - L|, |H - Cp|, |Cp - L|)

• Show True Range:

Each color on the bar represents the maximum range value selected:

◦ |H - L| = Green

◦ |H - Cp| = Yellow

◦ |Cp - L| = Blue

• Show True Range on Selected Price Bar:

An arrow points to the range, and its color represents the maximum value chosen:

◦ |H - L| = Green

◦ |H - Cp| = Yellow

◦ |Cp - L| = Blue

• Show True Range Information Table:

Displays the actual values of |H - L|, |H - Cp|, and |Cp - L| from the selected bar.

2) Studying Average True Range (ATR)

2.1) Set the ATR Length in Settings.

Default value: ATR Length = 14

2.2) Enable/disable "Display Average True Range (RMA)" in Settings:

• Show ATR

• Show ATR Length from Selected Price Bar

(An arrow will point backward equal to the ATR Length)

3) Studying ATR Trailing

3.1) Set the ATR Multiplier in Settings.

Default value: ATR Multiply = 3

3.2) Enable/disable "Display ATR Trailing" in Settings:

• Show High Line

• Show ATR Bands

• Show ATR Trailing

4) Studying ATR Trailing Exit

(Occurs when the Close price crosses below the ATR Trailing line)

Enable/disable "Display ATR Trailing" in Settings:

• Show Close Line

• Show Exit Points

(Exit points are marked by an orange diamond symbol above the price bar)

44 MA Near & Green Candle ScannerStocks that have closed just about 44 MA on 14th Aug 2025 and are forming green candles now

Prime NumbersPrime Numbers highlights prime numbers (no surprise there 😅), tokens and the recent "active" feature in "input".

🔸 CONCEPTS

🔹 What are Prime Numbers?

A prime number (or a prime) is a natural number greater than 1 that is not a product of two smaller natural numbers.

Wikipedia: Prime number

🔹 Prime Factorization

The fundamental theorem of arithmetic states that every integer larger than 1 can be written as a product of one or more primes. More strongly, this product is unique in the sense that any two prime factorizations of the same number will have the same number of copies of the same primes, although their ordering may differ. So, although there are many different ways of finding a factorization using an integer factorization algorithm, they all must produce the same result. Primes can thus be considered the "basic building blocks" of the natural numbers.

Wikipedia: Fundamental theorem of arithmetic

Math Is Fun: Prime Factorization

We divide a given number by Prime Numbers until only Primes remain.

Example:

24 / 2 = 12 | 24 / 3 = 8

12 / 3 = 4 | 8 / 2 = 4

4 / 2 = 2 | 4 / 2 = 2

|

24 = 2 x 3 x 2 | 24 = 3 x 2 x 2

or | or

24 = 2² x 3 | 24 = 2² x 3

In other words, every natural/integer number above 1 has a unique representation as a product of prime numbers, no matter how the number is divided. Only the order can change, but the factors (the basic elements) are always the same.

🔸 USAGE

The Prime Numbers publication contains two use cases:

Prime Factorization: performed on "close" prices, or a manual chosen number.

List Prime Numbers: shows a list of Prime Numbers.

The other two options are discussed in the DETAILS chapter:

Prime Factorization Without Arrays

Find Prime Numbers

🔹 Prime Factorization

Users can choose to perform Prime Factorization on close prices or a manually given number.

❗️ Note that this option only applies to close prices above 1, which are also rounded since Prime Factorization can only be performed on natural (integer) numbers above 1.

In the image below, the left example shows Prime Factorization performed on each close price for the latest 50 bars (which is set with "Run script only on 'Last x Bars'" -> 50).

The right example shows Prime Factorization performed on a manually given number, in this case "1,340,011". This is done only on the last bar.

When the "Source" option "close price" is chosen, one can toggle "Also current price", where both the historical and the latest current price are factored. If disabled, only historical prices are factored.

Note that, depending on the chosen options, only applicable settings are available, due to a recent feature, namely the parameter "active" in settings.

Setting the "Source" option to "Manual - Limited" will factorize any given number between 1 and 1,340,011, the latter being the highest value in the available arrays with primes.

Setting to "Manual - Not Limited" enables the user to enter a higher number. If all factors of the manual entered number are in the 1 - 1,340,011 range, these factors will be shown; however, if a factor is higher than 1,340,011, the calculation will stop, after which a warning is shown:

The calculated factors are displayed as a label where identical factors are simplified with an exponent notation in superscript.

For example 2 x 2 x 2 x 5 x 7 x 7 will be noted as 2³ x 5 x 7²

🔹 List Prime Numbers

The "List Prime Numbers" option enables users to enter a number, where the first found Prime Number is shown, together with the next x Prime Numbers ("Amount", max. 200)

The highest shown Prime Number is 1,340,011.

One can set the number of shown columns to customize the displayed numbers ("Max. columns", max. 20).

🔸 DETAILS

The Prime Numbers publication consists out of 4 parts:

Prime Factorization Without Arrays

Prime Factorization

List Prime Numbers

Find Prime Numbers

The usage of "Prime Factorization" and "List Prime Numbers" is explained above.

🔹 Prime Factorization Without Arrays

This option is only there to highlight a hurdle while performing Prime Factorization.

The basic method of Prime Factorization is to divide the base number by 2, 3, ... until the result is an integer number. Continue until the remaining number and its factors are all primes.

The division should be done by primes, but then you need to know which one is a prime.

In practice, one performs a loop from 2 to the base number.

Example:

Base_number = input.int(24)

arr = array.new()

n = Base_number

go = true

while go

for i = 2 to n

if n % i == 0

if n / i == 1

go := false

arr.push(i)

label.new(bar_index, high, str.tostring(arr))

else

arr.push(i)

n /= i

break

Small numbers won't cause issues, but when performing the calculations on, for example, 124,001 and a timeframe of, for example, 1 hour, the script will struggle and finally give a runtime error.

How to solve this?

If we use an array with only primes, we need fewer calculations since if we divide by a non-prime number, we have to divide further until all factors are primes.

I've filled arrays with prime numbers and made libraries of them. (see chapter "Find Prime Numbers" to know how these primes were found).

🔹 Tokens

A hurdle was to fill the libraries with as many prime numbers as possible.

Initially, the maximum token limit of a library was 80K.

Very recently, that limit was lifted to 100K. Kudos to the TradingView developers!

What are tokens?

Tokens are the smallest elements of a program that are meaningful to the compiler. They are also known as the fundamental building blocks of the program.

I have included a code block below the publication code (// - - - Educational (2) - - - ) which, if copied and made to a library, will contain exactly 100K tokens.

Adding more exported functions will throw a "too many tokens" error when saving the library. Subtracting 100K from the shown amount of tokens gives you the amount of used tokens for that particular function.

In that way, one can experiment with the impact of each code addition in terms of tokens.

For example adding the following code in the library:

export a() => a = array.from(1) will result in a 100,041 tokens error, in other words (100,041 - 100,000) that functions contains 41 tokens.

Some more examples, some are straightforward, others are not )

// adding these lines in one of the arrays results in x tokens

, 1 // 2 tokens

, 111, 111, 111 // 12 tokens

, 1111 // 5 tokens

, 111111111 // 10 tokens

, 1111111111111111111 // 20 tokens

, 1234567890123456789 // 20 tokens

, 1111111111111111111 + 1 // 20 tokens

, 1111111111111111111 + 8 // 20 tokens

, 1111111111111111111 + 9 // 20 tokens

, 1111111111111111111 * 1 // 20 tokens

, 1111111111111111111 * 9 // 21 tokens

, 9999999999999999999 // 21 tokens

, 1111111111111111111 * 10 // 21 tokens

, 11111111111111111110 // 21 tokens

//adding these functions to the library results in x tokens

export f() => 1 // 4 tokens

export f() => v = 1 // 4 tokens

export f() => var v = 1 // 4 tokens

export f() => var v = 1, v // 4 tokens

//adding these functions to the library results in x tokens

export a() => const arraya = array.from(1) // 42 tokens

export a() => arraya = array.from(1) // 42 tokens

export a() => a = array.from(1) // 41 tokens

export a() => array.from(1) // 32 tokens

export a() => a = array.new() // 44 tokens

export a() => a = array.new(), a.push(1) // 56 tokens

What if we could lower the amount of tokens, so we can export more Prime Numbers?

Look at this example:

829111, 829121, 829123, 829151, 829159, 829177, 829187, 829193

Eight numbers contain the same number 8291.

If we make a function that removes recurrent values, we get fewer tokens!

829111, 829121, 829123, 829151, 829159, 829177, 829187, 829193

//is transformed to:

829111, 21, 23, 51, 59, 77, 87, 93

The code block below the publication code (// - - - Educational (1) - - - ) shows how these values were reduced. With each step of 100, only the first Prime Number is shown fully.

This function could be enhanced even more to reduce recurrent thousands, tens of thousands, etc.

Using this technique enables us to export more Prime Numbers. The number of necessary libraries was reduced to half or less.

The reduced Prime Numbers are restored using the restoreValues() function, found in the library fikira/Primes_4.

🔹 Find Prime Numbers

This function is merely added to show how I filled arrays with Prime Numbers, which were, in turn, added to libraries (after reduction of recurrent values).

To know whether a number is a Prime Number, we divide the given number by values of the Primes array (Primes 2 -> max. 1,340,011). Once the division results in an integer, where the divisor is smaller than the dividend, the calculation stops since the given number is not a Prime.

When we perform these calculations in a loop, we can check whether a series of numbers is a Prime or not. Each time a number is proven not to be a Prime, the loop starts again with a higher number. Once all Primes of the array are used without the result being an integer, we have found a new Prime Number, which is added to the array.

Doing such calculations on one bar will result in a runtime error.

To solve this, the findPrimeNumbers() function remembers the index of the array. Once a limit has been reached on 1 bar (for example, the number of iterations), calculations will stop on that bar and restart on the next bar.

This spreads the workload over several bars, making it possible to continue these calculations without a runtime error.

The result is placed in log.info() , which can be copied and pasted into a hardcoded array of Prime Number values.

These settings adjust the amount of workload per bar:

Max Size: maximum size of Primes array.

Max Bars Runtime: maximum amount of bars where the function is called.

Max Numbers To Process Per Bar: maximum numbers to check on each bar, whether they are Prime Numbers.

Max Iterations Per Bar: maximum loop calculations per bar.

🔹 The End

❗️ The code and description is written without the help of an LLM, I've only used Grammarly to improve my description (without AI :) )

VWATR + VIX + VVIX Trend Regime### 🤖 VWATR + VIX + VVIX Trend Regime — Your Ultimate Volatility Dashboard! 📊

This isn't just another indicator; it's a comprehensive dashboard that brings together everything you need to understand market volatility focused on Futures. It merges price-based movement with market-wide fear and sentiment, giving you a powerful edge in your trading and risk management. Think of it as your personal volatility sidekick, ready to help you navigate market uncertainty like a pro!

***

### ✨ What's Inside?

* **VWATR (Volume-Weighted ATR):** A super-smart measure of price movement that pays close attention to where the big money is flowing.

* **VIX (The "Fear Gauge"):** Tracks the expected volatility of the S&P 500, essentially telling you how nervous the market is feeling.

* **VVIX (The "VIX of VIX"):** This one's for the pros! It measures how volatile the VIX itself is, giving you an early heads-up on potential fear spikes.

* **VX Term Structure:** A clever way to see if traders are preparing for a crisis. It compares the two nearest VIX futures to spot a rare signal called "backwardation."

* **Z-Scores:** It helps you spot when VIX and VVIX are at historic highs or lows, making it easier to predict when things might return to normal.

* **Divergence Score:** A unique tool to flag potential market shifts when the VIX and VVIX start moving in completely different directions.

* **Regime Classification:** The script automatically labels the market as "Full Panic," "Known Crisis," "Surface Calm," "Stress," or "Normal," so you always know where you stand.

* **Gradient Bars:** A visual treat! The background of your chart changes color to reflect real-time volatility shifts, giving you an instant feel for the market's mood.

* **Alerts:** Get push notifications on your phone for key events like "Full Panic" or "Backwardation" so you never miss a beat.

***

### 📝 Panel/Table Outputs

This is your mission control! The on-screen table gives you a clean summary of the current market regime, VIX and VVIX values, their ratios, term structure, Z-scores, and signals. Everything you need, right where you can see it.

***

### 🚀 How to Get Started

1. **Check your data:** You'll need access to real-time data for VIX, VVIX, VX1!, and VX2!. A paid subscription might be necessary for this.

2. **Add it to your chart:** Use the indicator on any chart (we've set it to `overlay=false`) to get your full volatility dashboard.

3. **Tweak it to perfection:** Head over to the Settings panel to customize the thresholds, colors, and your all-important "Jolt Value."

4. **Start trading smarter:** Use the dashboard to inform your trades, hedge your portfolio, and manage risk with confidence.

***

### ⚙️ Customization & Key Settings

* `showVWATR`: Toggle your price-volatility metric on or off.

* `showExpectedVol`: See the expected volatility as a percentage of the current price.

* `joltLevel`: This is a very important line on your chart! It's your personal trigger for when volatility is getting a little too wild. More on this below.

* `enableGradientBars`: Turn the awesome colored background on or off.

* `enableTable`: Hide or show your information table.

* `VIX/VVIX/VX1!/VX2! symbols`: If your broker uses different symbols for these, you can change them here.

* `VIX/VVIX thresholds`: Adjust these levels to fine-tune the indicator to your personal risk tolerance.

***

### 💡 Jolt Value: A Quick Guide for Smart Traders 🧠

The **jolt value** is your personal tripwire for volatility. Think of it as a warning light on your car's dashboard. You set the level, and when volatility (VWATR) crosses that line, you get an instant signal that something interesting is happening.

**How to Set Your Jolt Value:**

The ideal jolt value is dynamic. You want to keep it just a little above the current VIX level to stay alert without getting too many false alarms.

| Current VIX Level | Market Regime | Recommended Jolt Value |

| :--- | :--- | :--- |

| Under 15 | Calm/Complacent | 15–16 |

| 15–20 | Typical/Normal | 16–18 |

| 20–30 | Cautious/Active | 18–22 |

| Over 30 | Stress/Panic | 30+ |

**A Pro Tip for August 2025:** Since the VIX is hovering around 14.7, setting your jolt value to **16.5** is a great starting point for keeping an eye on things. If the VIX starts to climb above 20, you should adjust your jolt level to match the new reality.

***

### ⚠️ Important Things to Note

* You might experience some data delays if you're not on a paid TradingView plan or your broker does not provide real-time data for the VIX also VIX is only active during NY session, so it's not advised to use it outside of normal trading hours!

Intraday Volume Pulse GSK-VIZAG-AP-INDIAIntraday Volume Pulse Indicator

Overview

This indicator is designed to track and visualize intraday volume dynamics during a user-defined trading session. It calculates and displays key volume metrics such as buy volume, sell volume, cumulative delta (difference between buy and sell volumes), and total volume. The data is presented in a customizable table overlay on the chart, making it easy to monitor volume pulses throughout the session. This can help traders identify buying or selling pressure in real-time, particularly useful for intraday strategies.

The indicator resets its calculations at the start of each new day and only accumulates volume data from the specified session start time onward. It uses simple logic to classify volume as buy or sell based on candle direction:

Buy Volume: Assigned to green (up) candles or half of neutral (doji) candles.

Sell Volume: Assigned to red (down) candles or half of neutral (doji) candles.

All calculations are approximate and based on available volume data from the chart. This script does not incorporate external data sources, order flow, or tick-level information—it's purely derived from standard OHLCV (Open, High, Low, Close, Volume) bars.

Key Features

Session Customization: Define the start time of your trading session (e.g., market open) and select from common timezones like Asia/Kolkata, America/New_York, etc.

Volume Metrics:

Buy Volume: Total volume attributed to bullish activity.

Sell Volume: Total volume attributed to bearish activity.

Cumulative Delta: Net difference (Buy - Sell), highlighting overall market bias.

Total Volume: Sum of all volume during the session.

Formatted Display: Volumes are formatted for readability (e.g., in thousands "K", lakhs "L", or crores "Cr" for large numbers).

Color-Coded Table: Uses a patriotic color scheme inspired by general themes (Saffron, White, Green) with dynamic backgrounds based on positive/negative values for quick visual interpretation.

Table Options: Toggle visibility and position (top-right, top-left, etc.) for a clean chart layout.

How to Use

Add to Chart: Apply this indicator to any symbol's chart (works best on intraday timeframes like 1-min, 5-min, or 15-min).

Configure Inputs:

Session Start Hour/Minute: Set to your market's open time (default: 9:15 for Indian markets).

Timezone: Choose the appropriate timezone to align with your trading hours.

Show Table: Enable/disable the metrics table.

Table Position: Place the table where it doesn't obstruct your view.

Interpret the Table:

Monitor for spikes in buy/sell volume or shifts in cumulative delta.

Positive delta (green) suggests buying pressure; negative (red) suggests selling.

Use alongside price action or other indicators for confirmation—e.g., high total volume with positive delta could indicate bullish momentum.

Limitations:

Volume classification is heuristic and not based on actual order flow (e.g., it splits doji volume evenly).

Data accumulation starts from the session time and resets daily; historical backtesting may be limited by the max_bars_back=500 setting.

This is for educational and visualization purposes only—do not use as sole basis for trading decisions.

Calculation Details

Session Filter: Uses timestamp() to define the session start and filters bars with time >= sessionStart.

New Day Detection: Resets volumes on daily changes via ta.change(time("D")).

Volume Assignment:

Buy: Full volume if close > open; half if close == open.

Sell: Full volume if close < open; half if close == open.

Cumulative Metrics: Accumulated only during the session.

Formatting: Custom function f_format() scales large numbers for brevity.

Disclaimer

This script is for educational and informational purposes only. It does not provide financial advice or signals to buy/sell any security. Always perform your own analysis and consult a qualified financial professional before making trading decisions.

© 2025 GSK-VIZAG-AP-INDIA

Awesome Indicator# Moving Average Ribbon with ADR% - Complete Trading Indicator

## Overview

The **Moving Average Ribbon with ADR%** is a comprehensive technical analysis indicator that combines multiple analytical tools to provide traders with a complete picture of price trends, volatility, relative performance, and position sizing guidance. This multi-faceted indicator is designed for both swing and positional traders looking for data-driven entry and exit signals.

## Key Components

### 1. Moving Average Ribbon System

- **4 Customizable Moving Averages** with default periods: 13, 21, 55, and 189

- **Multiple MA Types**: SMA, EMA, SMMA (RMA), WMA, VWMA

- **Color-coded visualization** for easy trend identification

- **Flexible configuration** allowing users to modify periods, types, and colors

### 2. Average Daily Range Percentage (ADR%)

- Calculates the average daily volatility as a percentage

- Uses a 20-period simple moving average of (High/Low - 1) * 100

- Helps traders understand the stock's typical daily movement range

- Essential for position sizing and stop-loss placement

### 3. Volume Analysis (Up/Down Ratio)

- Analyzes volume distribution over the last 55 periods

- Calculates the ratio of volume on up days vs down days

- Provides insight into buying vs selling pressure

- Values > 1 indicate more buying volume, < 1 indicate more selling volume

### 4. Absolute Relative Strength (ARS)

- **Dual timeframe analysis** with customizable reference points

- **High ARS**: Performance relative to benchmark from a high reference point (default: Sep 27, 2024)

- **Low ARS**: Performance relative to benchmark from a low reference point (default: Apr 7, 2025)

- Uses NSE:NIFTY as default comparison symbol

- Color-coded display: Green for outperformance, Red for underperformance

### 5. Relative Performance Table

- **5 timeframes**: 1 Week, 1 Month, 3 Months, 6 Months, 1 Year

- Shows stock performance **relative to benchmark index**

- Formula: (Stock Return - Index Return) for each period

- **Color coding**:

- Lime: >5% outperformance

- Yellow: -5% to +5% relative performance

- Red: <-5% underperformance

### 6. Dynamic Position Allocation System

- **6-factor scoring system** based on price vs EMAs (21, 55, 189)

- Evaluates:

- Price above/below each EMA

- EMA alignment (21>55, 55>189, 21>189)

- **Allocation recommendations**:

- 100% allocation: Score = 6 (all bullish signals)

- 75% allocation: Score = 4

- 50% allocation: Score = 2

- 25% allocation: Score = 0

- 0% allocation: Score = -2, -4, -6 (bearish signals)

## Display Tables

### Performance Table (Top Right)

Shows relative performance vs benchmark across multiple timeframes with intuitive color coding for quick assessment.

### Metrics Table (Bottom Right)

Displays key statistics:

- **ADR%**: Average Daily Range percentage

- **U/D**: Up/Down volume ratio

- **Allocation%**: Recommended position size

- **High ARS%**: Relative strength from high reference

- **Low ARS%**: Relative strength from low reference

## How to Use This Indicator

### For Trend Analysis

1. **Moving Average Ribbon**: Look for price above ascending MAs for bullish trends

2. **MA Alignment**: Bullish when shorter MAs are above longer MAs

3. **Color coordination**: Use consistent color scheme for quick visual analysis

### For Entry/Exit Timing

1. **Performance Table**: Enter when showing consistent outperformance across timeframes

2. **Volume Analysis**: Confirm entries with U/D ratio > 1.5 for strong buying

3. **ARS Values**: Look for positive ARS readings for relative strength confirmation

### For Position Sizing

1. **Allocation System**: Use the recommended allocation percentage

2. **ADR% Consideration**: Adjust position size based on volatility

3. **Risk Management**: Lower allocation in high ADR% stocks

### For Risk Management

1. **ADR% for Stop Loss**: Set stops at 1-2x ADR% below entry

2. **Relative Performance**: Reduce positions when consistently underperforming

3. **Volume Confirmation**: Be cautious when U/D ratio deteriorates

## Best Practices

### Timeframe Recommendations

- **Intraday**: Use lower MA periods (5, 13, 21, 55)

- **Swing Trading**: Default settings work well (13, 21, 55, 189)

- **Position Trading**: Consider higher periods (21, 50, 100, 200)

### Market Conditions

- **Trending Markets**: Focus on MA alignment and relative performance

- **Sideways Markets**: Rely more on ADR% for range trading

- **Volatile Markets**: Reduce allocation percentage regardless of signals

### Customization Tips

1. Adjust reference dates for ARS calculation based on significant market events

2. Change comparison symbol to sector-specific indices for better relative analysis

3. Modify MA periods based on your trading style and market characteristics

## Technical Specifications

- **Version**: Pine Script v6

- **Overlay**: Yes (plots on price chart)

- **Real-time Updates**: Yes

- **Data Requirements**: Minimum 252 bars for complete calculations

- **Compatible Timeframes**: All standard timeframes

## Limitations

- Performance calculations require sufficient historical data

- ARS calculations depend on selected reference dates

- Volume analysis may be less reliable in low-volume stocks

- Relative performance is only as good as the chosen benchmark

This indicator is designed to provide a comprehensive analysis framework rather than simple buy/sell signals. It's recommended to use this in conjunction with your overall trading strategy and risk management rules.

RSI DJ GUTO 2025RSI do Samuca, tem de trocar as cores, esse e o usado nas lives, tem de trocar as cores pra ficar igual ao do Samuca pois aqui nao consegui trocar as cores.

Samuca's RSI, you have to change the colors, this is the one used in the lives, you have to change the colors to be the same as Samuca's because I couldn't change the colors here.