Rainbow Price Chart This indicator is a technical and on-chain analysis tool for Bitcoin, designed to help investors better understand the different phases of the market cycle and underlying sentiment. It directly overlays on the price chart (overlay=true).

Indicator Name: "Rainbow Price Chart & V/T Ratio Signals"

General Purpose:

It combines two popular methodologies for visualizing Bitcoin's value and sentiment: the classic "Rainbow Price Chart" and signals derived from the "Value per Transaction Ratio" (V/T Ratio) based on blockchain data. It is ideal for long-term investors looking for strategic entry/exit points.

Main Components:

Rainbow Price Chart:

Concept: Divides Bitcoin's price range into different market "sentiment zones" (e.g., "Bubble Zone," "FOMO Zone," "HODL Zone," "Accumulation Zone," "Buy Zone," "Fire Sale Zone") using colored bands. These bands are calculated as ascending and descending multiples of a base Exponential Moving Average (EMA), configurable by default to 200 periods.

Visualization: The zones are represented with transparent color fills on the price chart. A detailed legend in the top right corner of the chart explains the meaning of each color and sentiment zone.

Important Note: This type of chart is designed to be viewed and analyzed correctly on a logarithmic price scale. The indicator includes a visual reminder to activate this scale.

Value per Transaction (V/T) Ratio Signals:

Concept: Measures the average value per transaction on the Bitcoin blockchain by dividing the total transacted volume in USD by the number of transactions. This ratio is smoothed with an Exponential Moving Average (by default, 7 periods) and is framed within a dynamic Linear Regression Channel (LRC) based on standard deviation.

Signal Generation: Based on the position of the smoothed V/T Ratio within this LRC channel, the indicator generates signals directly on the price chart, such as:

"BOTTOM": Low price, V/T Ratio in the lower band of the LRC.

"SEMI-LOW" / "SEMI-HIGH": Intermediate phases within the channel.

"ATH" (All-Time High): Potentially overvalued price, V/T Ratio in the upper band of the LRC.

On-Chain Data: The indicator requests external daily on-chain data for total transacted volume (TVTVR) and number of transactions (NTRAN) from the Bitcoin blockchain.

Diagnostic Panes: Includes plots of the raw on-chain data (volume and number of transactions) in a separate pane, which are useful for debugging or verifying the data source. The lines for the V/T Ratio itself and its LRC channel are not plotted by default but can be activated in the code for deeper analysis.

Ideal for:

Bitcoin investors and "hodlers" who desire a visual tool that combines price-based market cycle context with fundamental signals derived from on-chain activity, to help identify key moments for accumulation or potential distribution.

Considerations:

Relies on the availability of external on-chain data (QUANDL:BCHAIN) within TradingView.

Functions best on a daily timeframe.

"Cycle"に関するスクリプトを検索

Schaff Trend Cycle (STC)The STC (Schaff Trend Cycle) indicator is a momentum oscillator that combines elements of MACD and stochastic indicators to identify market cycles and potential trend reversals.

Key features of the STC indicator:

Oscillates between 0 and 100, similar to a stochastic oscillator

Values above 75 generally indicate overbought conditions

Values below 25 generally indicate oversold conditions

Signal line crossovers (above 75 or below 25) can suggest potential entry/exit points

Faster and more responsive than traditional MACD

Designed to filter out market noise and identify cyclical trends

Traders typically use the STC indicator to:

Identify potential trend reversals

Confirm existing trends

Generate buy/sell signals when combined with other technical indicators

Filter out false signals in choppy market conditions

This STC implementation includes multiple smoothing options that act as filters:

None: Raw STC values without additional smoothing, which provides the most responsive but potentially noisier signals.

EMA Smoothing: Applies a 3-period Exponential Moving Average to reduce noise while maintaining reasonable responsiveness (default).

Sigmoid Smoothing: Transforms the STC values using a sigmoid (S-curve) function, creating more gradual transitions between signals and potentially reducing whipsaw trades.

Digital (Schmitt Trigger) Smoothing: Creates a binary output (0 or 100) with built-in hysteresis to prevent rapid switching.

The STC indicator uses dynamic color coding to visually represent momentum:

Green: When the STC value is above its 5-period EMA, indicating positive momentum

Red: When the STC value is below its 5-period EMA, indicating negative momentum

The neutral zone (25-75) is highlighted with a light gray fill to clearly distinguish between normal and extreme readings.

Alerts:

Bullish Signal Alert:

The STC has been falling

It bottoms below the 25 level

It begins to rise again

This pattern helps confirm potential uptrend starts with higher reliability.

Bearish Signal Alert:

The STC has been rising

It peaks above the 75 level

It begins to decline

This pattern helps identify potential downtrend starts.

Wyckoff Method IndicatorThe Wyckoff Method Market Cycle Indicator is a powerful tool designed to help traders identify the current market phase based on the principles of the Wyckoff Method. This indicator analyzes price action and volume patterns to determine whether the market is in an accumulation, markup, distribution, or markdown phase.

The Wyckoff Method, developed by Richard D. Wyckoff, is a time-tested approach to understanding market dynamics and identifying potential trading opportunities. By studying the interaction between price and volume, the Wyckoff Method aims to provide insight into the actions of market participants and the potential direction of the market.

This indicator automatically detects the key market phases as defined by the Wyckoff Method:

Accumulation: This phase occurs when large institutional investors are quietly accumulating positions, often leading to a period of consolidation with low volatility and decreasing volume.

Markup: Following the accumulation phase, the markup phase is characterized by a breakout above the accumulation range, accompanied by increasing volume. This indicates a potential bullish trend.

Distribution: After a significant price advance, the distribution phase emerges. It is marked by high volatility and increasing volume as large investors begin to distribute their holdings to the public.

Markdown: The markdown phase follows the distribution phase and is characterized by a breakdown below the distribution range, accompanied by increasing volume. This suggests a potential bearish trend.

The indicator plots the detected market phases on the chart using the following signals:

Green triangle pointing upwards: Accumulation phase

Blue triangle pointing downwards: Markup phase

Red triangle pointing downwards: Distribution phase

Orange triangle pointing upwards: Markdown phase

By utilizing this indicator, traders can gain valuable insights into the underlying market structure and make more informed trading decisions. However, it is important to note that the Wyckoff Method Market Cycle Indicator should be used in conjunction with other technical analysis tools and risk management strategies.

The indicator provides two input parameters:

Lookback Period: The number of bars used to calculate the volatility and determine the market phases. The default value is 50.

Volume Condition Multiple: The multiple used to compare the current volume with the volume of the lookback period. The default value is 2.

Traders can adjust these parameters to suit their specific trading style and the characteristics of the asset being analyzed.

Please note that this indicator is intended for educational and informational purposes only. It does not constitute financial advice. Always conduct your own analysis and exercise proper risk management when trading.

Happy trading!

Financial Astrology Venus DeclinationVenus crossing zero declination towards the south direction until the minima is reached seems to produce that the price change slows down and calms the volatility. This also coincides with few small corrections in ETHUSD, looks that Venus moving from South to North declination path produce much more strong trends.

This Venus declination pattern needs more research in others markets, I have analysed BTCUSD and was not able to see any clear cycle with Venus declination, will be great to get the participation from more financial astrologers that could research this declination cycle in other markets and share feedback with us.

Note: The Venus declination indicator is based on an ephemeris array that covers years 2010 to 2030, prior or after this years the declination is not available, this daily ephemeris are based on UTC time so in order to align properly with the price bars times you should set UTC as your chart reference timezone.

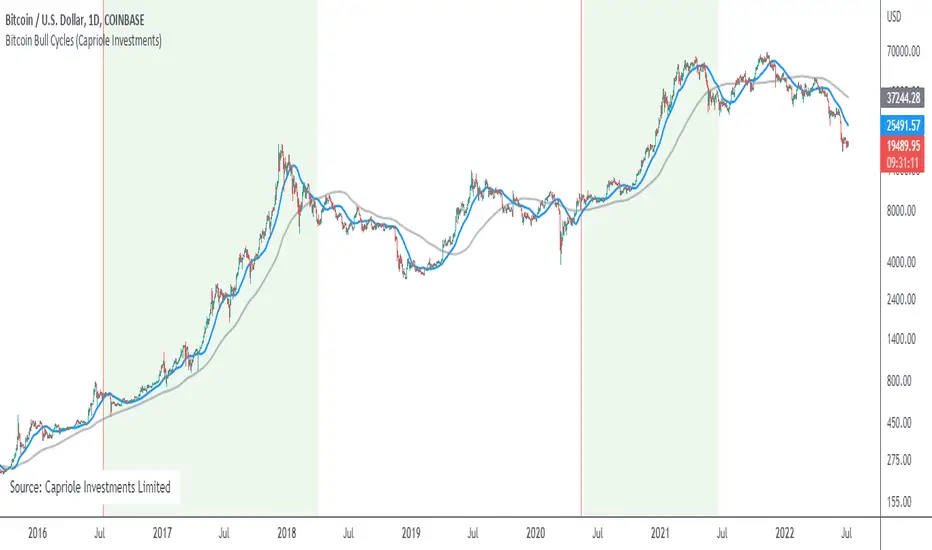

Bitcoin Bull CyclesA simple indicator that identifies the primary upswing of Bitcoin following each Halving, the "Bull Cycle".

A "Bull Cycle" is identified as the first period of positive momentum after each Halving date, defined as the 50 Daily Moving Average (DMA) being above the 200 DMA.

Ehlers Spectrum Derived Filter Bank [CC]The Spectrum Derived Filter Bank was created by John Ehlers (Stocks & Commodities V. 26:3 (16-22)) and this is technically two indicators in one. This will let you know the current cycle period which is in blue and the other indicator will let you know if you should buy the stock or not. Buy when it is green and sell when it is red.

Let me know if you would like me to publish other scripts or if you want something custom done!

Note: I'm republishing this because the original script couldn't be found in searches so this will fix that.

TOP & BOTTOM Cycle [aamonkey]Works best on BTC and only on the daily timeframe!

This is a TOP / BOTTOM indicator for big market cycles.

These tops and bottoms are based on the difference between the 200MA on the daily and the price.

Crypto MACD SignalsUnlocking Enhanced Market Insights: A Next-Generation MACD Indicator for Cryptocurrency Trading

Introduction: Beyond Traditional MACD

In the vast landscape of technical analysis tools, the Moving Average Convergence Divergence (MACD) stands as one of the most ubiquitous and trusted momentum indicators. However, its classic formulation often leaves traders sifting through frequent crossovers, struggling to distinguish high-probability signals from market noise, especially in the volatile cryptocurrency markets. This script represents a significant evolution of the classic MACD, transforming it from a standalone oscillator into a comprehensive, multi-layered signal detection system. Its core originality lies not in reinventing the MACD calculation, but in augmenting it with proprietary filtering mechanisms, quantitative signal scoring, and visual prioritization to enhance decision clarity and timing.

Core Functionality: What It Does and How It Achieves It

This indicator, titled "Crypto MACD Signals," is a dedicated, non-overlay oscillator built for clarity and actionability. It performs three primary functions simultaneously:

Enhanced MACD Visualization: It plots the traditional MACD line, Signal line, and Histogram with a refined color scheme. The histogram is dynamically colored (blue for bullish, orange for bearish) but introduces a key innovation: the identification of "Huge" or "Anomalous" Bars. A bar is highlighted in bright white when its size exceeds twice the 20-bar Simple Moving Average of the absolute histogram values. This instantly draws attention to moments of exceptional momentum surge or capitulation, which often precede significant trend accelerations or reversals.

Context-Aware Signal Generation: Instead of marking every MACD line crossover, the script applies a crucial logical filter. It only plots a "BUY" signal (green upward triangle) when a bullish crossover occurs while the histogram is below the zero line. Conversely, a "SELL" signal (red downward triangle) is plotted only when a bearish crossover occurs while the histogram is above the zero line. This filter ensures signals are generated in the context of a potential trend reversal from an oversold or overbought state, rather than during the middle of a strong trend, dramatically increasing the signal's statistical edge. This aligns with a classic "Oscillator Reversal from Extremes" methodology within trend-following systems.

Real-Time Performance Dashboard: A fixed table in the top-right corner serves as a live statistical dashboard. It tracks and displays the total count of:

Generated Buy Signals

Generated Sell Signals

Total "Huge" Histogram Bars (both bullish and bearish)

This provides traders with an at-a-glance understanding of recent market activity—whether it has been signal-rich or quiet, and the frequency of high-momentum events—aiding in assessing the current market regime (e.g., trending vs. consolidating).

Implementation and Practical Usage

The indicator is designed for tactical swing trading and momentum-based intraday positioning in crypto assets. Its primary use case is for identifying "Pullback Entries within a Trend" and "Early Trend Reversal Confirmations."

For Trend-Following: A trader in an established uptrend would wait for a pullback that drives the MACD histogram negative. A subsequent bullish crossover that triggers a "BUY" signal, especially if accompanied by a "Huge" bullish histogram bar, offers a high-confidence entry point to re-join the trend.

For Counter-Trend/Reversal Scenarios (Scalping): The script is highly effective for a specific scalping technique: "Fading Extreme Momentum Exhaustion." A cluster of "Huge" bearish bars followed by a diminishing histogram and a bullish crossover signal can indicate selling exhaustion, presenting a short-term long scalp opportunity. The inverse applies for short scalps. The labels ("🔥") and arrows provide clear visual cues for these setups directly on the chart.

Workflow: Traders are advised to first observe the statistical table to gauge recent activity. Then, they should look for convergence between a filtered arrow signal (BUY/SELL) and the appearance of a "Huge" bar or a cluster of them. This multi-factor confirmation is the cornerstone of the strategy.

Underlying Philosophy and Calculation Logic

The script's intelligence is built on a layered philosophy of "Momentum Quantification and Contextual Validation."

Dynamic Thresholding for Anomalies: The "Huge Bar" detection does not use a fixed threshold. By comparing the current histogram value to a recent average of absolute momentum (ta.sma(math.abs(hist_line), 20)), it creates an adaptive, market-responsive benchmark. A bar that is 200% larger than recent average momentum is statistically anomalous, suggesting institutional-sized order flow or a major shift in sentiment. This is a direct application of statistical volatility band principles to momentum, not price.

Signal Filtering for Phase Alignment: The conditional logic for plotting arrows (bullish_cross and hist_line < 0) ensures the MACD crossover signal is aligned with the correct momentum phase of the market cycle. A buy signal is only valid if momentum (histogram) is coming from a "recharging" or bearish area (below zero), not when it's already extended above zero. This prevents buying at a peak and selling at a trough, which is a common pitfall of the raw indicator. This embodies the trading axiom: "Trade the turn, not the continuation."

Quantitative Self-Awareness: The integrated counter and dashboard represent a meta-analysis layer. It allows the tool to provide feedback on its own performance density. A market generating many signals might be choppy and range-bound, while a market with few signals but several "Huge Bars" might be in a strong, steady trend. This helps the trader select the appropriate strategy (trend riding vs. reversal scalping) for the current environment.

In essence, this script synthesizes several respected trading concepts: the core trend/momentum logic of MACD, the anomaly detection common to volatility-based indicators like Keltner Channels, and the signal-verification philosophy of multi-indicator systems—all packaged into a single, coherent, and visually intuitive tool specifically tuned for the unique amplitude and speed of cryptocurrency markets.

Bullish Divergence SMI Base & Trigger with ATR FilterDescription:

A bullish divergence indicator combining the Stochastic Momentum Index (SMI) and Average True Range (ATR) to pinpoint high-probability entries:

1. Base Arrow (Orange ▲):

• Marks every SMI %K / %D bullish crossover where %K < –70 (deep oversold)—the first half of the divergence setup.

• Each new qualifying crossover replaces the previous base, continuously “arming” the divergence signal.

• Configurable SMI lookbacks, oversold threshold, and a base timeout (default 100 days) to clear stale bases.

2. Trigger Arrow (Green ▲):

• Completes the bullish divergence: fires on the next SMI bullish crossover where %K > –60 and price has dropped below the base arrow’s close by at least N × ATR (default 1 × 14-day ATR).

• A dashed green line links the base and trigger to visually confirm the divergence.

• Resets after triggering, ready for a new divergence cycle.

Inputs:

• SMI %K Length, EMA Smoothing, %D Length

• Oversold Base Level (–70), Trigger Level (–60)

• ATR Length (14), ATR Multiplier (1.0)

• Base Timeout (100 days)

Ideal for any market, this study highlights genuine bullish divergences—oversold momentum crossovers that coincide with significant price reactions—before entering long trades.

IlluminateThe Illuminate script predicts the potential range of Bitcoin's top and bottom prices based on a logarithmic regression model, referencing Bitcoin's historical price trends and halvings. This script is designed to provide valuable insights into Bitcoin's price dynamics and long-term trends using principles derived from the "Bitcoin Law."

Key Features

Power Law Trend Lines

Primary Trend:

Projects the general growth trajectory of Bitcoin prices over time based on a logarithmic power law.

Resistance Line:

Identifies a potential upper limit of Bitcoin prices during market peaks.

Includes an offset trendline for an additional buffer zone.

Support Line:

Represents a possible bottom for Bitcoin prices during market downturns.

Offset trendlines highlight potential zones of price fluctuation near the support line.

Fill Zones:

Between resistance and offset: Semi-transparent Red.

Between support and offset: Semi-transparent Green/Blue.

Bitcoin Halving Events

Automatically marks significant Bitcoin halving dates with yellow vertical lines and labeled annotations.

Current and future halvings (approximate) are included.

Trending Phase Indication

A dynamic visual color fill highlights different phases of Bitcoin's price evolution based on a 4-year cycle.

Colors: Red, Green, Blue, Orange (indicating each phase).

"Trending Phase" label provides insight into the current phase.

Interactive Inputs

Show/Hide Resistance: Toggle resistance trend lines.

Show/Hide Support: Toggle support trend lines.

Show/Hide Halving Dates: Toggle visibility of halving annotations.

Customizable Parameters

Fine-tune parameters (A and n) for the main trend line to match your analysis needs.

How to Use

Overlay Analysis:

Add this script to your TradingView chart for direct overlay on Bitcoin's price data.

Interpret the Zones:

Use the resistance and support lines as potential upper and lower bounds for price movements.

Analyze fill zones for areas of likely price oscillation.

Halving Significance:

Observe price behavior before and after halving dates, which historically influence market trends.

Long-Term Perspective:

The model is optimized for long-term projections, making it suitable for strategic, rather than short-term, trading decisions.

Disclaimer:

This indicator is for educational purposes only and should not be used as investment advice. Always do your own research and consult with a financial advisor before making trading decisions.

Chuck Dukas Market Phases of Trends (based on 2 Moving Averages)This script is based on the article “Defining The Bull And The Bear” by Chuck Duckas, published in Stocks & Commodities V. 25:13 (14-22); (S&C Bonus Issue, 2007).

The article “Defining The Bull And The Bear” discusses the concepts of “bullish” and “bearish” in relation to the price behavior of financial instruments. Chuck Dukas explains the importance of analyzing price trends and provides a framework for categorizing price activity into six phases. These phases, including recovery, accumulation, bullish, warning, distribution, and bearish, help to assess the quality of the price structure and guide decision-making in trading. Moving averages are used as tools for determining the context preceding the current price action, and the slope of a moving average is seen as an indicator of trend and price phase analysis.

The six phases of trends

// Definitions of Market Phases

recovery_phase = src > ma050 and src < ma200 and ma050 < ma200 // color: blue

accumulation_phase = src > ma050 and src > ma200 and ma050 < ma200 // color: purple

bullish_phase = src > ma050 and src > ma200 and ma050 > ma200 // color: green

warning_phase = src < ma050 and src > ma200 and ma050 > ma200 // color: yellow

distribution_phase = src < ma050 and src < ma200 and ma050 > ma200 // color: orange

bearish_phase = src < ma050 and src < ma200 and ma050 < ma200 // color red

Recovery Phase : This phase marks the beginning of a new trend after a period of consolidation or downtrend. It is characterized by the gradual increase in prices as the market starts to recover from previous losses.

Accumulation Phase : In this phase, the market continues to build a base as prices stabilize before making a significant move. It is a period of consolidation where buying and selling are balanced.

Bullish Phase : The bullish phase indicates a strong upward trend in prices with higher highs and higher lows. It is a period of optimism and positive sentiment in the market.

Warning Phase : This phase occurs when the bullish trend starts to show signs of weakness or exhaustion. It serves as a cautionary signal to traders and investors that a potential reversal or correction may be imminent.

Distribution Phase : The distribution phase is characterized by the market topping out as selling pressure increases. It is a period where supply exceeds demand, leading to a potential shift in trend direction.

Bearish Phase : The bearish phase signifies a strong downward trend in prices with lower lows and lower highs. It is a period of pessimism and negative sentiment in the market.

These rules of the six phases outline the cyclical nature of market trends and provide traders with a framework for understanding and analyzing price behavior to make informed trading decisions based on the current market phase.

60-period channel

The 60-period channel should be applied differently in each phase of the market cycle.

Recovery Phase : In this phase, the 60-period channel can help identify the beginning of a potential uptrend as price stabilizes or improves. Traders can look for new highs frequently in the 60-period channel to confirm the trend initiation or continuation.

Accumulation Phase : During the accumulation phase, the 60-period channel can highlight that the current price is sufficiently strong to be above recent price and longer-term price. Traders may observe new highs frequently in the 60-period channel as the slope of the 50-period moving average (SMA) trends upwards while the 200-period moving average (SMA) slope is losing its downward slope.

Bullish Phase : In the bullish phase, the 60-period channel showing a series of higher highs is crucial for confirming the uptrend. Additionally, traders should observe an upward-sloping 50-period SMA above an upward-sloping 200-period SMA for further validation of the bullish phase.

Warning Phase : When in the warning phase, the 60-period channel can provide insights into whether the current price is weaker than recent prices. Traders should pay attention to the relationship between the price close, the 50-period SMA, and the 200-period SMA to gauge the strength of the phase.

Distribution Phase : In the distribution phase, traders should look for new lows frequently in the 60-period channel, hinting at a weakening trend. It is crucial to observe that the 50-period SMA is still above the 200-period SMA in this phase.

Bearish Phase : Lastly, in the bearish phase, the 60-period channel reflecting a series of lower lows confirms the downtrend. Traders should also note that the price close is below both the 50-period SMA and the 200-period SMA, with the relationship of the 50-period SMA being less than the 200-period SMA.

By carefully analyzing the 60-period channel in each phase, traders can better understand market trends and make informed decisions regarding their investments.

Color Agreement Aggregate (CAA)This indicator helps finding patterns within market structure in a highly intuitive manner.

It does this by painting a picture instead of presenting numerical values.

It greatly reduces noise in trend/structure analysis.

----- HOW TO USE IT -----

1) Zoom out of chart to get a clearer picture of overall color patterns.

2) Consider areas of intense reds and greens as areas of interest.

3) There is always a pattern of intense reds followed by intense greens. Consider this pattern as the start of a new cycle.

4) Key spikes and dips are shown when all 3 bands are matching of intense colors.

5) Turn on Precision in the Style tab to get more information on decisive spikes in price (See "Precision" below).

Reach (top band):

This is the fast and more volatile movement of the market. It shows the direction in which the recent price action is reaching towards.

Energy (middle band):

This is the medium speed of market movement. It shows the energy of the Reach and how influential it is to market change.

Frequent and intense change of color in this band can be a precursor of change within the Basis.

Basis (bottom band):

This is the slower, broader movement of the market. It is the basis on which the Reach and Energy sit on.

Intense colors in this band show major changes in price levels and market structure.

Precision:

Precision shows the weaker levels of colors. It does this by making bars in a band half its size.

For example, if there is a light green bar that is half, it means that the current bar is on the weaker level of the light green level.

Precision helps in identifying where there are influential moves in price action. Note, there will never be a half-sized bar in the highest and lowest levels.

This is because these levels are the limits and don't have a weaker half.

See notes in chart for more information. Note, you can turn off the labels in the Style tab.

----- HOW THIS INDICATOR IS ORIGINAL; WHAT IT DOES AND HOW IT DOES IT -----

This indicator has an original, unique ability to paint the overall market structure in a highly intuitive manner. It "paints" an image instead of showing numbers.

It does this by color-coding different levels of varying speeds of market movement. It then presents these levels as simple bars.

Finally, it stacks them all and creates an overall image of clear breaks and/or repeats within market structure.

This greatly reduces noise in pattern finding, finding breaks in market structure, and in confirming repeated patterns.

----- VERSION -----

The only significant information from this indicator are the colors themselves and the patterns, agreement, and aggregate of the colors.

This indicator does not provide any numerical information of the underlying, mathematical calculations.

The levels for the Reach are made by the KPAM; for the Energy, the CCI; and for the Basis, the RSI.

However, this indicator is not a variant, replacement, or presentation of the KPAM, CCI, or the RSI in any way, shape, or form -- this indicator does not present itself as such.

The 3 indicators are only useful to this indicator in as much as they are what the colors are derived from -- nothing more.

They are needed in order to obtain, visualize, and create the overall aggregate and agreement of colors.

Thus, the KPAM, CCI, and RSI cannot be adjust nor are they plotted. They are not, in any way, a focus of this indicator.

BTC ATH ROIThis indicator shows the ROI % of Bitcoin from when it passed its ATH of the previous bull cycle. I found it interesting that each time it crossed its ATH it took around 260-280 days to peak for each one. This bull run seems to follow between both of the previous bull runs including this recent dip.

There are a couple issues I want to fix but can't figure out:

1. You need to completely scroll out and move towards 2013 on the Daily chart for all 3 lines to show up. Would be nice to load all of that data at the start.

2. I can't query the value of the plots after they have been offset. This would be useful to create a prediction bias for the current plot so would could see where btc might go.

If you peeps know of a way to load all data or query plot values after offsets, please share. That would be awesome.

Ehler Stochastic Cyber Cycle Signals/AlertsThis script works based on @everget's version of Ehler Stochastic Cyber Cycle. Unlike @everget's work, my adaptation prints only crossovers into the chart that occur above or below the overbought/oversold zone.

You can find @everget's script with all related documentation here

I didn't change the calculation, I only reinvented how it is presented on the chart and added alerts.

5x Period Cycle SeasonalityShows the average from the last 5 periods for close price cycle. For example to see the annual seasonality of a stock for the last 5 years use on daily chart with the default setting of 252, the number of trading days in a year, approximately.

Multi-cycle EMA50 full-screen solid lineA small tool to help you check the price of EMA50 over multiple periods.

STIME3H Time High/Low Triangles (Correct Time • Wick/Body • Timezone Control)

This indicator plots 3-Hour (3H) High & Low levels using triangle markers, aligned to exact clock-based time blocks such as 00:00, 03:00, 06:00, 09:00, 12:00, 15:00, 18:00, 21:00.

It is designed for ICT / CRT / intraday traders who need precise session and time-cycle reference points without cluttering the chart.

🔹 Key Features

▲ High triangle & ▼ Low triangle for each 3-hour block

⏱ Correct time alignment using selectable timezones

🌍 Timezone dropdown

UTC

UTC-5 (Fixed)

New York (DST auto)

London (DST auto)

Tokyo

Custom timezone (IANA / Etc format)

🕒 Toggle individual times ON/OFF (00, 03, 06, 09, 12, 15, 18, 21)

📍 Triangles can touch candle wicks or bodies

🗂 Displays last 2 days by default (configurable)

🔠 Adjustable time text size (tiny → large)

🎨 Clean visuals, no background boxes, no repaint

Intervalo de la confianza usando VWMA 5,10,14,55,90,200Varios Itervalos de Confianza usando VWMA

-LOS QUE MANIPULAN LOS MERCADOS, ES COMPRAR DONDE LA VOLATILIDAD ES BAJA, NO HAY RUIDO.

-DESPUES QUE COMPRAN, SU PROXIMO TRABAJO ES CREAR LA VARICIA=FOMO Y MANDAR UNA TARJETA DE INVITACION A LOS INVERSIONISTA MINORITARIOS.

-DESPUES QUE LOS MINORISTA ENTRAN EN CONFIANZA Y VARICIA-FOMO,VENDEN LOS QUE MANIPULAN LOS MERCADOS

-SU ULTIMA ETAPA ES VENDER MAS AGRESIVO PARA CREAR UN MIEDO=FUD Y DARLES EN EL CODO A LOS MINORISTAS PARA QUE SALGAN PERDIENDO.

ESTE CICLOS SE REPITE EN LOS MERCADOS.

Si las personas que operan los mercados tiene sintimentos donde el meido y la varicia entran en el juego de las inversiones y trade, entoces hay que medir como esta su miedo y varicia en diferentes temporaliades.

Que es mejor mediar esta varicia y miedo usando Intervalo de la Confianza usando el VWMA .

AHORA CON ESTA HERRAMIENTA

Ustedes solo tiene que encontrar como esta esta el FOMO o FUD en diferentes temporalidades.

Multiple Confidence Intervals Using VWMA

- Market manipulators buy where volatility is low and there is no noise.

- After they buy, their next step is to create volatility (FOMO) and send an invitation to retail investors.

- Once retail investors gain confidence and experience volatility (FOMO), the market manipulators sell.

- Their final stage is to sell more aggressively to create fear (FUD) and force retailers to lose money.

This cycle repeats itself in the markets. If people who trade the markets experience feelings where fear and greed come into play in their investments and trading, then it's necessary to measure how their fear and greed manifest across different timeframes.

What's the best way to measure this greed and fear using the Confidence Interval with the VWMA?

NOW WITH THIS TOOL

You only need to determine how FOMO or FUD manifests across different timeframes.

ETH Vol Breakout - NO ERROR VERSIONThis strategy examines the impact of Eth.d Vol on Ethereum price. Looking at ETHDVOL -60 (Support) and 78 (Resistance)—tell a very specific story - analyzing a High Volatility Regime.

The support level around 60 and resistance 78, tend to only occurs during Bull Runs or Market Crashes.

In the "Quiet Years", ETHDVOL rarely touched 60, let alone 78.

Trying to develop a strategy that is perfectly tuned for a Bull Market or a Crisis,

1. The "60 Floor" (Support)

Context: In a high-volatility regime, when ETHDVOL drops to 60, it indicates the market has "cooled off" just enough to reload leverage.

Historical Behavior (2021-2022 Context):

July 2021: After the May crash, ETHDVOL compressed down and found support at ~65.

Result: This marked the local bottom before the massive run-up to the November All-Time Highs ($4,800).

Outcome: Strong Buy Signal (Trend Continuation).

January 2022: ETHDVOL dropped to ~58-60 while price was hovering around $3,000.

Result: The floor broke, volatility spiked to 80+, and price crashed to $2,200.

Outcome: Trap / Warning Signal.

The Pattern: When Volatility hits 60 (Support), price is usually Coiling.

If Price is trending UP: This is a "dip buy" opportunity. The coil resolves upwards.

If Price is trending DOWN: This is the "calm before the flush." The coil resolves downwards.

2. The "78 Ceiling" (Resistance)

Context: 78 is an extreme reading. It represents panic (bottom) or euphoria (blow-off top).

Historical Behavior:

May 2021 (The Crash): ETHDVOL smashed through 78, peaking at 100+.

Price Action: Price collapsed from $4,000 to $1,700.

Signal: If Vol > 78, you are in a capitulation event. Buying spot here is usually profitable within 3-6 months (buying the blood).

November 2022 (FTX Collapse): ETHDVOL spiked to ~75-80.

Price Action: ETH hit $1,100 (Cycle Lows).

Signal: Hitting 78 marked the Absolute Bottom.

November 2021 (The Top): Interestingly, at the $4,800 price peak, Volatility was NOT at 78. It was lower (~60-70).

Insight: Bull market tops often happen on lower volatility than bear market bottoms.

Bitcoin Power Law Zones (Dunk)Introduction When viewed on a standard linear chart, Bitcoin’s long-term price action can appear chaotic and exponential. However, when analyzed through the lens of physics and network growth models, a distinct structure emerges.

This indicator implements the Bitcoin Power Law , a mathematical model that suggests Bitcoin’s price evolves in a straight line when plotted against time on a "log-log" scale. By calculating parallel bands around this regression line, we create a "Rainbow" of valuation zones that help investors visualize whether the asset is historically overheated, undervalued, or sitting at fair value.

The Math Behind the Model The Power Law dictates that price scales with time according to the formula: Price = A * (days since genesis)^b

This script uses the specific parameters popularized by recent physics-based analyses of the network: Slope (b): 5.78 (Representing the scaling law of the network adoption). Amplitude (A): 1.45 x 10^-17 (The intercept coefficient).

While simple moving averages react to price, this model is predictive based on time and network growth physics, providing a long-term "gravity" center for the asset.

Guide to the Valuation Zones

Upper Bands (Red/Orange): Extr. Overvalued, High Premium, Overvalued. Historically, these zones have marked cycle peaks where price moved too far, too fast ahead of the network's steady growth. The Baseline (Black Line): Fair Value. The mathematical mean of the Power Law. Price has historically oscillated around this line, treating it as a center of gravity. Lower Bands (Green/Blue): Undervalued, Discount, Deep Discount. These zones represent periods where the market price has historically lagged behind the network's intrinsic value, often marking accumulation phases.

Note: The lowest theoretical tiers ("Bitcoin Dead") have been trimmed from this chart to focus on relevant historical support levels.

How to Use Logarithmic Scale: You MUST set your chart to "Log" scale (bottom right of the TradingView window) for this indicator to function correctly. On a linear chart, the bands will appear to curve upwards aggressively; on a Log chart, they will appear as smooth, parallel channels. Timeframe: This is a macro-economic indicator. It is best viewed on Daily or Weekly timeframes. Overlay Labels: The indicator includes dynamic labels on the right-side axis, allowing you to instantly see the current price requirements for each valuation zone without manually tracing lines.

Credits This script is based on the Power Law theory popularized by Giovanni Santostasi and the original Corridor concepts by Harold Christopher Burger .

Disclaimer This tool is for educational and informational purposes only. It visualizes historical mathematical trends and does not constitute financial advice. Past performance of a model is not indicative of future results.

Further Reading

www.hcburger.com

giovannisantostasi.medium.com

Consolidation Tracker🧭 Consolidation Tracker — Visualize Market Reversals in Real Time

The Consolidation Tracker is a minimalist yet powerful tool designed to map the anatomy of market reversals and trend transitions. It highlights the structural evolution of price through four key phases, helping traders anticipate shifts with clarity and confidence.

🔄 The Four Stages of a Market Reversal:

Failure to Displace — Price fails to break beyond recent highs or lows, signaling potential exhaustion of the current trend.

Consolidation (CAMP) — A range-bound phase where price compresses between a dynamic high and low. These zones are shaded gray, representing indecision and balance.

Engulfing (ENGULF) — A decisive candle closes beyond the CAMP high or low, suggesting a directional shift. These are highlighted in orange.

Fair Value Gap (FVG) — A three-candle pattern forms a price imbalance. If this FVG also engulfs the CAMP range, it confirms the reversal and resets the CAMP. Bullish FVGs are shaded green, bearish FVGs in red.

🔁 From Reversal to Trend:

Once a reversal is confirmed via an FVG, the market often transitions into a trend cycle characterized by:

Displacement — Strong directional movement away from the prior range.

Fair Value Gaps — Continuation imbalances that offer high-probability entries on retracements.

🧠 How It Works:

The indicator dynamically tracks CAMP highs and lows, updating only when a candle engulfs the range or a valid FVG forms.

FVGs are detected when a three-candle sequence creates a gap between candle 2 and 0, and the middle candle (candle 1) breaks the CAMP boundary.

CAMP levels are plotted as horizontal lines, while background colors narrate the evolving structure in real time.

This tool is ideal for traders who value market structure, price efficiency, and narrative clarity. Whether you're anticipating reversals or riding trends, the Consolidation Tracker offers a clean, actionable lens into price behavior.

Predicted Funding RatesOverview

The Predicted Funding Rates indicator calculates real-time funding rate estimates for perpetual futures contracts on Binance. It uses triangular weighting algorithms on multiple different timeframes to ensure an accurate prediction.

Funding rates are periodic payments between long and short position holders in perpetual futures markets

If positive, longs pay shorts (usually bullish)

If negative, shorts pay longs (usually bearish)

This is a prediction. Actual funding rates depend on the instantaneous premium index, derived from bid/ask impacts of futures. So whilst it may imitate it similarly, it won't be completely accurate.

This only applies currently to Binance funding rates, as HyperLiquid premium data isn't available. Other Exchanges may be added if their premium data is uploaded.

Methods

Method 1: Collects premium 1-minunute data using triangular weighing over 8 hours. This granular method fills in predicted funding for 4h and less recent data

Method 2: Multi-time frame approach. Daily uses 1 hour data in the calculation, 4h + timeframes use 15M data. This dynamic method fills in higher timeframes and parts where there's unavailable premium data on the 1min.

How it works

1) Premium data is collected across multiple timeframes (depending on the timeframe)

2) Triangular weighing is applied to emphasize recent data points linearly

Tri_Weighing = (data *1 + data *2 + data *3 + data *4) / (1+2+3+4)

3) Finally, the funding rate is calculated

FundingRate = Premium + clamp(interest rate - Premium, -0.05, 0.05)

where the interest rate is 0.01% as per Binance

Triangular weighting is calculated on collected premium data, where recent data receives progressively higher weight (1, 2, 3, 4...). This linear weighting scheme provides responsiveness to recent market conditions while maintaining stability, similar to an exponential moving average but with predictable, linear characteristics

A visual representation:

Data points: ──────────────>

Weights: 1 2 3 4 5

Importance: ▂ ▃ ▅ ▆ █

How to use it

For futures traders:

If funding is trending up, the market can be interpreted as being in a bull market

If trending down, the market can be interpreted as being in a bear market

Even used simply, it allows you to gauge roughly how well the market is performing per funding. It can basically be gauged as a sentiment indicator too

For funding rate traders:

If funding is up, it can indicate a long on implied APR values

If funding is down, it can indicate a short on implied APR values

It also includes an underlying APR, which is the annualized funding rate. For Binance, it is current funding * (24/8) * 365

For Position Traders: Monitor predicted funding rates before entering large positions. Extremely high positive rates (>0.05% for 8-hour periods) suggest overleveraged longs and potential reversal risk. Conversely, extreme negative rates indicate shorts dominance

Table:

Funding rate: Gives the predicted funding rate as a percentage

Current premium: Displays the current premium (difference between perpetual futures price and the underlying spot) as a percentage

Funding period: You can choose between 1 hour funding (HyperLiquid usually) and 8 hour funding (Binance)

APR: Underlying annualized funding rate

What makes it original

Whilst some predicted funding scripts exist, some aren't as accurate or have gaps in data. And seeing as funding values are generally missing from TV tickers, this gives traders accessibility to the script when they would have to use other platforms

Notes

Currently only compatible with symbols that have Binance USDT premium indices

Optimal accuracy is found on timeframes that are 4H or less. On higher timeframes, the accuracy drops off

Actual funding rates may differ

Inputs

Funding Period: Choose between "8 Hour" (standard Binance cycle) or "1 Hour" (divides the 8-hour rate by 8 for granular comparison)

Plot Type: Display as "Funding Rate" (percentage per interval) or "APR" (annualized rate calculated as 8-hour rate × 3 × 365)

Table: Toggle the information table showing current funding rate, premium, funding period, and APR in the top-right corner

Positive Colour: Sets the colour for positive funding rates where longs pay shorts (default: #00ffbb turquoise)

Negative Colour: Sets the colour for negative funding rates where shorts pay longs (default: red)

Table Background: Controls the background colour and transparency of the information table (default: transparent dark blue)

Table Text Colour: Sets the colour for all text labels in the information table (default: white)

Table Text Size: Controls font size with options from Tiny to Huge, with Small as the default balance of readability and space

Super-Elliptic BandsThe core of the "Super-Elliptic Bands" indicator lies in its use of a super-ellipse mathematical model to create dynamic price bands around a central Simple Moving Average (SMA). Here's a concise breakdown of its essential components:

Central Moving Average (MA):

A Simple Moving Average (ta.sma(close, maLen)) serves as the baseline, anchoring the bands to the average price over a user-defined period (default: 50 bars).

Super-Ellipse Formula:

The bands are generated using the super-ellipse equation: |y/b| = (1 - |x/a|^p)^(1/p), where:

x is a normalized bar index based on a user-defined cycle period (periodBase, default: 64), scaled to range from -1 to +1.

a = 1 (fixed semi-major axis).

b is the volatility-based semi-minor axis, calculated as volRaw * mult, where volRaw comes from ta.stdev, ta.atr, or ta.tr (user-selectable).

p (shapeP, default: 2.0) controls the band shape:

p = 2: Elliptical bands.

p < 2: Pointier, diamond-like shapes.

p > 2: Flatter, rectangular-like shapes.

This formula creates bands that dynamically adjust their width and shape based on price volatility and a cyclical component.

enjoy....