Walnut LevelsThis indicator was specifically designed to plot levels published by Walnut on SPY and ES charts. In the indicator's configuration settings, you are required to input the desired levels in the following format: (Description), (Description), (Description), .... Additionally, you have the option to configure whether to display labels and if those labels should include the numeric value of the level or just the description.

Moreover, the indicator allows customization of both color and line style via configuration settings. This flexibility enables users to tailor the appearance of the plotted levels according to their preferences. If there are no levels to plot, a message will be displayed indicating so.

Overall, the indicator streamlines the process of incorporating Walnut's published levels into trading analysis on SPY and ES charts, offering enhanced visualization and customization options to suit individual trading strategies.

"spy"に関するスクリプトを検索

RSI and MACD Crossover SignalsBest for Short-Term/Intraday Trading on SPY, TSLA, NVDA

Strategy Concept:

This strategy is designed for short-term trading across various assets and timeframes (Recommend: 1min, 5min, 15min, 1hr, 4hr, 1day). It leverages the Relative Strength Index (RSI) and Moving Average Convergence Divergence (MACD) to identify potential buy and sell signals. The strategy aims to capture moments where the asset's price is likely to experience a reversal or a significant momentum shift.

By combining the RSI and MACD indicators, the strategy seeks to increase the accuracy of identifying potential trend reversals or continuations, taking into account both the momentum and the trend direction of the asset.

RSI (Relative Strength Index) Parameters:

The RSI period is set to 14

Overbought and oversold levels are set at 70 and 30, respectively

The RSI is used to identify potential reversal points when the asset is overbought or oversold

MACD (Moving Average Convergence Divergence) Parameters:

The MACD settings are configured with a fast length of 8, a slow length of 34, and a signal smoothing of 8

The MACD line crossing over or under the signal line is used to confirm the potential buy or sell signals indicated by the RSI

Signal Generation Logic:

Buy Signal:

Triggered when the RSI crosses above the oversold level (30).

Confirmed if the MACD line crosses above the signal line within a delay period of up to 4 candles after the RSI signal.

Sell Signal:

Triggered when the RSI crosses below the overbought level (70).

Confirmed if the MACD line crosses below the signal line within a delay period of up to 4 candles after the RSI signal.

Additional Features:

The script includes a notification system that alerts the trader when either a buy or sell signal is detected. The alert signal is combined with both the buy and sell signal in 1 so people without premium can be alerted when any signal appears.

Buy signals are visually represented on the chart below the price bars with a green "BUY" label.

Sell signals are indicated above the price bars with a red "SELL" label.

Usage and Application:

This strategy is versatile and recommended to be played with scalps and day trades. I prefer SPY 0DTE on the 1 and 5 minute timeframe and looking for bigger trend reversals on the 1hr, 4hr, and 1 day timeframe.

Z-Score Forecaster[SS]Hello everyone,

I just released a neat library for Forecasting stock and equities. In it, it has a couple of novel approaches to forecasting (namely, a Moving Average forecaster and a Z-Score Forecaster). These were accomplished applying basic theories on Autoregression, ARIMA modelling and Z-Score to make new approaches to forecasting.

This is one of the novel approaches, the Z-Score forecaster.

How this function works is it identifies the current trend over the duration of the Z-Score assessment period. So, if the Z-Score is being assessed over the previous 75 candles, it will identify the trend over the previous 75 candles. It will then plot out the forecasted levels according to the trend, up to a maximum of the max Z-Score the ticker has reached within its period. At that point, it will show a likely trend reversal.

Here is an example:

This shows that SPY may go to 475.42 before reversing, as 475.42 is the highest z-score that has been achieved in the current trend.

When it is in an uptrend, the forecast line will be green, when in a downtrend, it will be red.

The forecasting line is accomplished through pinescript's new polyline feature.

In addition to the line, you can also have the indicator plot out a forecast table. The Z-Score Forecast table was formatted in a similar way to ARIMA, where it makes no bias about trend, it simply plots out both ends of the spectrum. So, if an uptrend were to continue, it will list the various uptrend targets along the way, vice versa for downtrends.

It will also display what Z-Score these targets would amount to. Here is an example:

Looking at SPY on the daily, we can see that a likely upside target would be around 484 at just over 2 Standard Deviations (Z-Score).

Its not liklely to go higher than that because then we are getting into 3 and 4 standard deviations.

Remember, everything generally should be within 1 and -1 standard deviations of the mean. So if we look at the table, we can see that would be between 466 and 430.

Customization

You can customize the Z-Score length and source. You can also toggle off and on alerts. The alerts will pop up when a ticker is trading at a previous maximum or previous minimum.

I have also added a manual feature to plot the Z-Score SMA, which is simply the SMA over the desired Z-Score lookback time.

And that's the indicator!

If you are interested in the library, you can access it here .

Thanks for checking this out and leave your questions below!

Pairs strategyHello, Tradingview community,

I am been playing with this idea that nowadays trading instruments are interconnected and when one goes too far "out of order" it should return to the mean.

So, here's a relatively simple idea.

This is a LONG-ONLY strategy.

Buy when your traded instrument's last bar closes down, and the comparing instrument closes up.

Sell when close is higher than the previous bar's high.

Best results I found with medium timeframes: 45min, 120min, 180min.

Also, feel free to test non-typical timeframes such as 59min, 119min, 179min, etc.

My reasoning for medium timeframes would be, that they are big enough to avoid "market noise"

of smaller timeframes + commissions & slippage is less negligible, and small enough to avoid exposure of higher timeframes, although, I haven't tested D timeframe and above.

The best results, I found were with instruments that aren't directly correlated. I mostly tested equities and equity futures, so for equity indexes, equity index futures, or large-cap stocks, NASDAQ:SMH , NASDAQ:NVDA , EURUSD, and Crude Oil would be a good candidate for comparing symbols.

When testing either futures or stocks, please adjust the commission for each asset, for stocks I use % equity, so it compounds over time, whereas, for futures, I use 1 contract all the time.

Here's NASDAQ:MSFT on 119min chart

Here's AMEX:SPY on 59min chart using NASDAQ:NVDA as comparison

Here's CME_MINI:ES1! on 179min chart using NYMEX:CL1! as comparison

To change comparison symbol just insert your symbol between the brackets on both fields down here.

SymbolClose = request.security("YOUR SYMBOL HERE", timeframe.period, close)

SymbolOpen = request.security("YOUR SYMBOL HERE", timeframe.period, open)

Since I am still relatively new to testing, hence, I am publishing this idea, so you can point out some crucial things I may have missed.

Thanks,

Enjoy the strategy!

TSI Market Timer + Volatility MeterThis is the TSI Market Timer. It is years in the making and it is comprised of four indicators in one. The stock (or source) is run through an indicator called the True Strength Indicator with settings(5,15) , then the TSI is run on both the Index(SPY) by default and what I call a Trigger line which is basically the TSI applied to the DXY (US Dollar Index).

Midline Volatility Indicator:

Lastly, we have a volatility indicator on the midline. The colors of the midline indicate levels of volatility. For the lowest volatility in the last 100 days, the dot turns dark blue. For the lowest volatility in 30 days, the dot turns aqua. For regular volatility, it remains orange. And last, for higher volatility of the last 100 days, it turns red. These are more or less arbitrary but they do come in handy.

Settings for Green/Red Shading:

Next on the indicator are the settings. You can toggle a color change between the stock/source and the index(spy). If the stock/source is greater than the index, it will color the area in between a green and if it is below the index, it will be red.

There is also a toggle for the stock/source and the trigger/DXY. This will also show green when the stock is above the trigger and red if it is below the trigger.

By turning on both of these, you get light green and dark green areas as well as red and darker red areas. The lighter green represent when the stock is above both the index and the trigger and conversely for the red areas.

Settings for vertical line crossings:

When the stock crosses the trigger/dxy line, it shows a green vertical line signal. When the stock crosses below the trigger/dxy, a red vertical line is shown.

You can turn these off by toggling them in the settings.

Stacked Condition:

Lastly, we have a "stacked condition" which shows up as a white triangle at the bottom when the condition of the stock being above the index and the trigger below the zero line.

New Highs:

If you see the stock line turn lime green, this indicates a new high was reached for the last 255 days/periods. This is like a new 52 week high signal.

Note:

This indicator is made mostly for the stock market. It may work ok during the week for crypto but using the trigger/dxy and index lines on the weekends doesn't work too well as they will be flat.

Also note that this indicator is not a recommendation to buy or sell any stock/instrument. It is only a study of market conditions. Any analysis should be followed up with volume analysis or other confirming indicators.

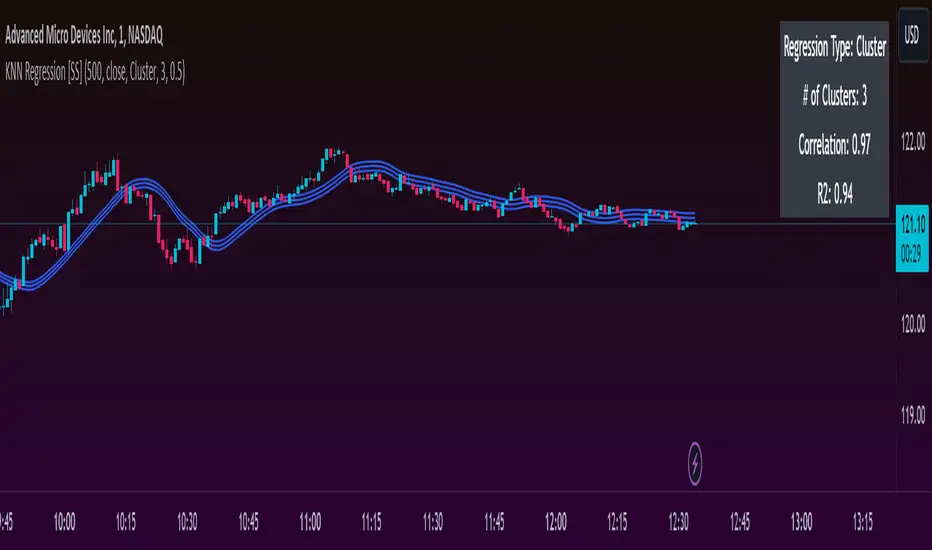

KNN Regression [SS]Another indicator release, I know.

But note, this isn't intended to be a stand-alone indicator, this is just a functional addition for those who program Machine Learning algorithms in Pinescript! There isn't enough content here to merit creating a library for (it's only 1 function), but it's a really useful function for those who like machine learning and Nearest Known Neighbour Algos (or KNN).

About the indicator:

This indicator creates a function to perform KNN-based regression.

In contrast to traditional linear regression, KNN-based regression has the following advantages over linear regression:

Advantages of KNN Regression vs. Linear Regression:

🎯 Non-linearity: KNN is a non-parametric method, meaning it makes no assumptions about the underlying data distribution. This allows it to capture non-linear relationships between features and the target variable.

🎯Simple Implementation: KNN is conceptually simple and easy to understand. It doesn't require the estimation of parameters, making it straightforward to implement.

🎯Robust to Outliers: KNN is less sensitive to outliers compared to linear regression. Outliers can have a significant impact on linear regression models, but KNN tends to be less affected.

Disadvantages of KNN Regression vs. Linear Regression:

🎯 Resource Intensive for Computation: Because KNN operates on identifying the nearest neighbors in a dataset, each new instance has to be searched for and identified within the dataset, vs. linear regression which can create a coefficient-based model and draw from the coefficient for each new data point.

🎯Curse of Dimensionality: KNN performance can degrade with an increasing number of features, leading to a "curse of dimensionality." This is because, in high-dimensional spaces, the concept of proximity becomes less meaningful.

🎯Sensitive to Noise: KNN can be sensitive to noisy data, as it relies on the local neighborhood for predictions. Noisy or irrelevant features may affect its performance.

Which is better?

I am very biased, coming from a statistics background. I will always love linear regression and will always prefer it over KNN. But depending on what you want to accomplish, KNN makes sense. If you are using highly skewed data or data that you cannot identify linearity in, KNN is probably preferable.

However, if you require precise estimations of ranges and outliers, such as creating co-integration models, I would advise sticking with linear regression. However, out of curiosity, I exported the function into a separate dummy indicator and pulled in data from QQQ to predict SPY close, and the results are actually very admirable:

And plotted with showing the standard error variance:

Pretty impressive, I must say I was a little shocked, it's really giving linear regression a run for its money. In school I was taught LinReg is the gold standard for modeling, nothing else compares. So as with most things in trading, this is challenging some biases of mine ;).

Functionality of the function

I have permitted 3 types of KNN regression. Traditional KNN regression, as I understand it, revolves around clustering. ( Clustering refers to identifying a cluster, normally 3, of identical cases and averaging out the Dependent variable in each of those cases) . Clustering is great, but when you are working with a finite dataset, identifying exact matches for 2 or 3 clusters can be challenging when you are only looking back at 500 candles or 1000 candles, etc.

So to accommodate this, I have added a functionality to clustering called "Tolerance". And it allows you to set a tolerance level for your Euclidean distance parameters. As a default, I have tested this with a default of 0.5 and it has worked great and no need to change even when working with large numbers such as NQ and ES1!.

However, I have added 2 additional regression types that can be done with KNN.

#1 One is a regression by the last IDENTICAL instance, which will find the most recent instance of a similar Independent variable and pull the Dependent variable from that instance. Or

#2 Average from all IDENTICAL instances.

Using the function

The code has the instructions for integrating the function into your own code, the parameters, and such, so I won't exhaust you with the boring details about that here.

But essentially, it exports 3, float variables, the Result, the Correlation, and the simplified R2.

As this is KNN regression, there are no coefficients, slopes, or intercepts and you do not need to test for linearity before applying it.

Also, the output can be a bit choppy, so I tend to like to throw in a bit of smoothing using the ta.sma function at a deault of 14.

For example, here is SPY from QQQ smoothed as a 14 SMA:

And it is unsmoothed:

It seems relatively similar but it does make a bit of an aesthetic difference. And if you are doing it over 14, there is no data loss and it is still quite reactive to changes in data.

And that's it! Hopefully you enjoy and find some interesting uses for this function in your own scripts :-).

Safe trades everyone!

TASC 2023.12 Growth and Value Switching System█ OVERVIEW

This script implements a rotation system for trading value and growth ETFs, as developed by Markos Katsanos and detailed in the article titled 'Growth Or Value?' in TASC's December 2023 edition of Traders' Tips . The purpose of this script is to demonstrate how short-term momentum can be employed to track market trends and provide clarity on when to switch between value and growth.

█ CONCEPTS

The central concept of the presented rotation strategy is based on the observation that the stock market undergoes cycles favoring either growth or value stocks. Consequently, the script introduces a momentum trading system that is designed to switch between value and growth equities based on prevailing market conditions. Specifically tailored for long-term index investors, the system focuses on trading Vanguard's value and growth ETFs ( VTV and VUG ) on a weekly timeframe.

To identify the ETF likely to outperform, the script uses a custom relative strength indicator applied to both VTV and VUG in comparison with an index ( SPY ). To minimize risk and drawdowns during bear markets, when both value and growth experience downtrends, the script employs the author's custom volume flow indicator (VFI) and blocks trades when its reading indicates money outflow . Positions are closed if the relative strength of the current open trade ETF falls below that of the other ETF for two consecutive weeks and is also below its moving average. Additionally, the script implements a stop-loss when the ETF is trading below its 40-week moving average, but only during bear markets.

The script plots the relative strengths of the value and growth equities along with the signals triggered by the aforementioned rules. Information about the current readings of the relative strength and volume flow indicators, along with the current open position, is displayed in a table.

█ CALCULATIONS

The script uses the request.security() function to gather price data for both equities and the reference index. Custom relative strength and volume flow indicators are calculated based on the formulas presented in the original article. By default, the script employs the same parameters for these indicators as proposed in the original article for VTV and VUG on a weekly timeframe.

Divergences RefurbishedJust as "a butterfly can flap its wings over a flower in China and cause a hurricane in the Caribbean" (Edward Lorenz), small divergences in markets can signal big trading opportunities.

█Introduction

This is a script forked from LonesomeTheBlue's Divergence for Many Indicators v4.

It is a script that checks for divergence between price and many indicators.

In this version, I added more indicators and also added 40 symbols to check for divergences.

More info on the original script can be found here:

█ Improvements

The following improvements have been implemented over v4:

1. Added parameters to customize indicators.

2. Added new indicators:

- Stoch RSI

- Volume Oscillator

- PVT (Price Volume Trend)

- Ultimate Oscillator

- Fisher Transform

- Z-Score/T-Score

3. Now there is the possibility of using 2 external indicators.

4. New option to show tooltips inside labels.

This allows you to save space on the screen if you choose the option to only show the number of divergences or just the abbreviations.

5. New option to show additional text next to the indicator name.

This allows for grouping of indicators and symbols and better visualization, whether through emojis, for example.

6. Added 40 customizable symbols to check for divergences.

7. Option "show only the first letter" of the indicator replaced by: "show the abbreviation of the indicator".

Reason: the indicator abbreviation is more informative and easier to read.

8. Script converted to PineScript version 5.

█ CONCEPTS

Below I present a brief description of the available indicators.

1. Moving Average Convergence/Divergence (MACD):

Shows the difference between short-term and long-term exponential moving averages.

2. MACD Histogram:

Shows the difference between MACD and its signal line.

3. Relative Strength Index (RSI):

Measures the relative strength of recent price gains to recent price losses of an asset.

4. Stochastic Oscillator (Stoch):

Compares the current price of an asset to its price range over a specified time period.

5. Stoch RSI:

Stochastic of RSI.

6. Commodity Channel Index (CCI):

Measures the relationship between an asset's current price and its moving average.

7. Momentum: Shows the difference between the current price and the price a few periods ago.

Shows the difference between the current price and the price of a certain period in the past.

8. Chaikin Money Flow (CMF):

A variation of A/D that takes into account the daily price variation and weighs trading volume accordingly. Accumulation/Distribution (A/D) identifies buying and selling pressure by tracking the flow of money into and out of an asset based on volume patterns.

9. On-Balance Volume (OBV):

Identify divergences between trading volume and an asset's price.

Sum of trading volume when the price rises and subtracts volume when the price falls.

10. Money Flow Index (MFI):

Measures volume pressure in a range of 0 to 100.

Calculates the ratio of volume when the price goes up and when the price goes down.

11. Volume Oscillator (VO):

Identify divergences between trading volume and an asset's price. Ratio of change of volume, from a fast period in relation to a long period.

12. Price-Volume Trend (PVT):

Identify the strength of an asset's price trend based on its trading volume. Cumulative change in price with volume factor. The PVT calculation is similar to the OBV calculation, but it takes into account the percentage price change multiplied by the current volume, plus the previous PVT value.

13. Ultimate Oscillator (UO):

Combines three different time periods to help identify possible reversal points.

14. Fisher Transform (FT):

Normalize prices into a Gaussian normal distribution.

15. Z-Score/T-Score: Shows the difference between the current price and the price a few periods ago. I is a statistical measurement that indicates how many standard deviations a data point is from the mean of a data set.

When to use t-score instead of z-score? When the sample size is small (length < 30).

Here, the use of z-score or t-score is chosen automatically based on the length parameter.

█ What to look for

The operation is simple. The script checks for divergences between the price and the selected indicators.

Now with the possibility of using multiple symbols, it is possible to check divergences between different assets.

A well-described view on divergences can be found in this cheat sheet:

◈ Examples with SPY ETF versus indicators:

1. Regular bullish divergence with external indicator:

1. Regular bearish divergence with Fisher Transform:

1. Positive hidden divergence with Momentum indicator:

1. Negative hidden divergence with RSI:

◈ Examples with SPY ETF versus other symbols:

1. Regular bearish divergence with European Stoch Market:

2. Regular bearish divergence with DXY inverted:

3. Regular bullish divergence with Taiwan Dollar:

4. Regular bearish divergence with US10Y (10-Year US Treasury Note):

5. Regular bullish divergence with QQQ ETF (Nasdaq 100):

6. Regular bullish divergence with ARKK ETF (ARK Innovation):

7.Positive hidden divergence with RSP ETF (S&P 500 Equal Weight):

8. Negative hidden divergence with EWZ ETF (Brazil):

◈ Examples with BTCUSD versus other symbols:

1. Regular bearish divergence with BTCUSDLONGS from Bitfinex:

2. Regular bearish divergence with BLOK ETF (Amplify Transformational Data Sharing):

3. Negative hidden divergence with NATGAS (Natural Gas):

4. Positive hidden divergence with TOTALDEFI (Total DeFi Market Cap):

█ Conclusion

The symbols available to check divergences were chosen in such a way as to cover the main markets, in the most generic way possible.

You can adjust them according to your needs.

A trader in the American market, for example, could add more ETFs, American stocks, and sectoral indices, such as the XLF (Financial Select Sector SPDR Fund), the XLK (Technology Select Sector SPDR), etc.

On the other hand, a cryptocurrency trader could add more currency pairs and sector indicators, such as BTCUSDSHORTS (Bitfinex), USDT.D (Tether Dominance), etc.

If the chart becomes too cluttered, you can use the option to show only the number of divergences or only the indicator abbreviations.

Or even disable certain indicators and symbols, if they are not of interest to you.

I hope this script is useful.

Don't forget to support LonesomeTheBlue's work too.

Ticker Correlation Matrix Table and Heatmap [SS]Hello everyone,

I am in the process of releasing some of my own utility indicators/things I use to reference and perform analyses.

I do a lot of quantitative/math based analyses, including correlation assessments that I traditionally would need to export data from Tradingview and perform in SPSS, Excel or R. I have been slowly building a repertoire of Excel/R functionality right on pinescript so I do not need to constantly export data and can perform the assessments right on Tradingview.

This is an example of such an indicator.

About the Indicator:

It is a correlation table/matrix indicator. It will allow up to 10 ticker inputs, which can be stocks, economic data, anything available on Tradingview, and it will perform a correlation assessment in a matrix / heatmap style.

The indicator will show the various correlations among all of the selected ticker inputs and will colour them based on correlation strength and type.

Strong negative correlations will appear bright red.

Strong positive correlations will appear bright green.

Complete absence of correlation (i.e. 0) will show bright orange.

The rest will show a darker shade to indicate less strength/correlation.

Calculation Functions

In addition to outputting a correlation matrix, the indicator is also able to express the relationship between tickers in a linear expression using the y = mx + b formula.

If we look at table, we can see that MSFT and AAPL have a significantly strong correlation of 0.82.

If we wanted to express this relationship mathmatically, we can ask the indicator to represent the linear relationship in our y = mx + b format. We simply toggle to our menu and select the Convert From MSFT (Ticker 2) and convert to APPL (Ticker 3):

When we select this, a new table will populate below and give you the expression as well as the amount of error associated with it:

In this case, we can see that the equation is y = 0.553x + 0.626 with a range of around 10 points in either direction.

This means that, to convert MSFT to AAPL, we would multiply the MSFT price by 0.553 and then add 0.626. So if we try it, MSFT closed at 328.41. So we substitute:

AAPL price = 0.553(328.41) + 0.626

AAPL price = 181.61 + 0.626

AAPL Price = 182.24 +/- 10

AAPL actually closed at 184.12. So pretty good. If we try another, let's do SPY to XLF:

So we substitute, SPY closed at 449.16.

XLF Price = 449.16(0.077) + 0.084

XLF price = 34.59 + 0.084

XLF price = 34.67

XLF actually closed at 34.49.

This is handy if you want to see how one stock price may affect another. If you are long on one stock and short on another, you can use this to determine what the likely outcome may be for the alternative stock. However, I recommend only performing this on tickers that have a relationship of 0.7 or higher, or a relationship of -0.7 or lower.

I always had to use SPSS to do this, so being able to do this right in Pinescript for me is a huge convenience!

Some other uses:

As I tend to post educational stuff on Tradingview and I frequently use correlation matrices, I have formatted the indicator to be more aesthetically pleasing for these purposes. Thus, you can unselect extra ticker slots that you do not need. IF I only need to display 3 tickers, I can unselect tickers 4 - 10. The end result is a cleaner table:

Essential Functions:

The assessment length is defaulted to 75 candles on the daily timeframe. Be sure to have the daily timeframe opened when you are viewing the indicator.

You can increase or decrease the assessment length as you desire.

You can also specify the source. The source is defaulted to close, but if you want to see the direct correlation of ticker's highs and/or lows, you can modify the source input in the settings menu to look at this.

Just remember to have the chart opened to whatever timeframe you are looking at.

And that's the indicator! Hopefully you find it helpful. Its more of an academic indicator, but it is performing a function that I personally use frequently in analyses, so I hope you may also benefit from it as well!

Thanks for checking it out! Safe trades everyone!

CE - 42MACRO Equity Factor Table This is Part 1 of 2 from the 42MACRO Recreation Series

The CE - 42MACRO Equity Factor Table is a whole toolbox packaged in a single indicator.

It aims to provide a probabilistic insight into the market realized GRID Macro Regime, use a multiplex of important Assets and Indices to form a high probability Implied Correlation expectation and allows to derive extra market insights by showing the most important aggregates and their performance over multiple timeframes... and what that might mean for the whole market direction, as well as the underlying asset.

WARNING

By the nature of the macro regimes, the outcomes are more accurate over longer Chart Timeframes (Week to Months).

However, it is also a valuable tool to form a proper,

market realized, short to medium term bias.

NOTE

This Indicator is intended to be used alongside the 2nd part "CE - 42MACRO Yield and Macro"

for a more wholistic approach and higher accuracy.

Due to coding limitations they can not be merged into one Indicator.

Methodology:

The Equity Factor Table tracks specifically chosen Assets to identify their performance and add the combined performances together to visualize 42MACRO's GRID Equity Model.

For this it uses the below Assets, with more to come:

Dividend Compounders ( AMEX:SPHD )

Mid Caps ( AMEX:VO )

Emerging Markets ( AMEX:EEM )

Small Caps ( AMEX:IWM )

Mega Cap Growth ( NASDAQ:QQQ )

Brazil ( AMEX:EWZ )

United Kingdom ( AMEX:EWU )

Growth ( AMEX:IWF )

United States ( AMEX:SPY )

Japan ( AMEX:DXJ )

Momentum ( AMEX:MTUM )

China ( AMEX:FXI )

Low Beta ( AMEX:SPLV )

International ex-US ( NASDAQ:ACWX )

India ( AMEX:INDA )

Eurozone ( AMEX:EZU )

Quality ( AMEX:QUAL )

Size ( AMEX:OEF )

Functionalities:

1. Correlations

Takes a measure of Cross Market Correlations

2. Implied Trend

Calculates the trend for each Asset and uses the Correlation to obtain the Implied Trend for the underlying Asset

There are multiple functionalities to enhance Signal Speed and precision...

Reading a signal only over a certain threshold, otherwise being colored in gray to signal noise or unclear market behavior

Normalization of Signal

Double Normalization of Signal for more Speed... ideal for the Crypto Market

Using an additional Hull Moving Average to enhance Signal Speed

Additional simple Background coloring to get a Signal from the HMA

Barcoloring based on the Implied Correlation

3. Equity Factor Table

Shows market realized Asset performance

Provides the approximate realized GRID market regimes

Informs about "Risk ON" and "Risk OFF" market states

Now into the juicy stuff...

Visuals:

There is a variety of options to change visual settings of what is plotted and where

+ additional considerations.

Everything that is relevant in the underlying logic which can improve comprehension can be visualized with these options.

More to come

Market Correlation:

The Market Correlation Table takes the Correlation of all the Assets to the Asset on the Chart,

it furthermore uses the Normalized KAMA Oscillator by IkkeOmar to analyse the current trend of every single Asset.

(To enhance the Signal you can apply the mentioned Indicator on the relevant Assets to find your target Asset movements that you intend to capture...

and then change the length of the Indicator in here)

It then Implies a Correlation based on the Trend and the Correlation to give a probabilistically adjusted expectation for the future Chart Asset Movement.

This is strengthened by taking the average of all Implied Trends.

Thus the Correlation Table provides valuable insights about probabilistically likely Movement of the Asset over the defined time duration,

providing alpha for Traders and Investors alike.

Equity Factors:

The table provides valuable information about the current market environment (whether it's risk on or risk off),

the rough GRID models from 42MACRO and the actual market performance.

This allows you to obtain a deeper understanding of how the market works and makes it simple to identify the actual market direction,

makes it possible to derive overall market Health and shows market strength or weakness.

Utility:

The Equity Factor Table is divided in 4 Sections which are the GRID regimes:

Economic Growth:

Goldilocks

Reflation

Economic Contraction:

Inflation

Deflation

Top 5 Equity Factors:

Are the values green for a specific Column?

If so then the market reflects the corresponding GRID behavior.

Bottom 5 Equity Factors:

Are the values red for a specific Column?

If so then the market reflects the corresponding GRID behavior.

So if we have Goldilocks as current regime we would see green values in the Top 5 Goldilocks Cells and red values in the Bottom 5 Goldilocks Cells.

You will find that Reflation will look similar, as it is also a sign of Economic Growth.

Same is the case for the two Contraction regimes.

This whole Indicator, as well as the second part, is based to a majority on 42MACRO's models.

I only brought them into TV and added things on top of it.

If you have questions or need a more in-depth guide DM me.

Will make a guide to all functionalities if necessity becomes apparent.

GM

Wick-to-Body Ratio Trend Forecast | Flux ChartsThe Wick-to-Body Ratio Trend Forecast Indicator aims to forecast potential movements following the last closed candle using the wick-to-body ratio. The script identifies those candles within the loopback period with a ratio matching that of the last closed candle and provides an analysis of their trends.

➡️ USAGE

Wick-to-body ratios can be used in many strategies. The most common use in stock trading is to discern bullish or bearish sentiment. This indicator extends candle ratios, revealing previous patterns that follow a candle with a similar ratio. The most basic use of this indicator is the single forecast line.

➡️ FORECASTING SYSTEM

This line displays a compilation of the averages of all the previous trends resulting from those historical candles with a matching ratio. It shows the average movements of the trends as well as the 'strength' of the trend. The 'strength' of the trend is a gradient that is blue when the trend deviates more from the average and red when it deviates less.

Chart: AMEX:SPY 30 min; Indicator Settings: Loopback 700, Previous Trends ON

The color-coded deviation is visible in this image of the indicator with the default settings (except for Forecast Lines > Previous Trends ), and the trend line grows bluer as the past patterns deviate more.

➡️ ADAPTIVE ACCEPTABLE RANGE

The algorithm looks back at every candle within the loopback period to find candles that match the last closed candle. The algorithm adaptively changes the acceptable range to which a candle can differ from the ratio of the last closed candle. The algorithm will never have more than 15 historical points used, as it will lower its sensitivity before it reaches that point.

Chart: BITSTAMP:BTCUSD 5 min; Indicator Settings: Loopback 700

Here is the BTC chart on 7/6/23 with default settings except for the loopback period at 700.

Chart: BITSTAMP:BTCUSD 5 min; Indicator Settings: Loopback 200

Here is the exact same chart with a loopback period of 200. While the first ratio for both is the same, a new ratio is revealed for the chart with a loopback of only 200 because the adaptive range is adjusted in the algorithm to find an acceptable number of reference points. Note the table in the top right however, while the algorithm adapts the acceptable range between the current ratio and historical ones to find reference points, there is a threshold at which candles will be considered too inaccurate to be considered. This prevents meaningless associations between candles due to a particularly rare ratio. This threshold can be adjusted in the settings through "Default Accuracy".

Regression Candle Conversion IndicatorHey everyone!

I got a pseudo-request a while ago for something like this, essentially the ability to track where another ticker would fall based on an alternative ticker.

I did create my ticker correlation reference indicator which directly looks at the correlation between 2 tickers. However, this is an indicator that operates on the same principle but is more pragmatic for trading.

What does it do?

Well, in keeping with the theme of what I call my indicators, this has a title that explains exactly what it does, "Regression Candle Conversion Indicator" or "RCCI" for short. It uses simple regression to convert one ticker to another. So while you are tracking one indicator, you can see where the expected value should fall on the other.

Applications?

The big application of this for me is being able to track where SPY/QQQ or IWM is falling during overnight trading sessions. Extended trading hours close at 8 pm NYSE time. After that, you have to guess where futures prices will put the ETF version of it. This indicator will allow you to track where, theoretically, the underlying ETF ticker will fall based on the current trading behaviour.

Some other applications are just the ability to track how similar or dissimilar one stock is to the other. For example, if we wanted to trade, say, Boeing using shares of DFEN or ITA (a defence specific ETF), here is what we get:

In the chart above we can see BA as the primary chart and ITA as the RCCI converted chart. We will see 2 major things that should cause us concern.

First, there is a really poor correlation between the two tickers. This indicates that ITA may not produce the best exposure if I am directly looking for Boeing exposure.

Second, there is a wide standard error. this means that the results that the RCCI is providing may be skewed up to +/- 2 points (as indicated by the standard error chart).

Let's take a look at BA and DFEN:

In the above, we can see that the correlation is not great, but the standard error is quite low.

This means that, while this may not be the best ticker for Boeing exposure, the RCCI is able to confidently calculate the ticker within +/- 0.50 cents based on BA's underlying data.

However, its important to note that it is not advisable to really rely on these results if the correlation is less than + 0.5 or greater than -0.5.

Let's take a look at a few more examples:

Above we have BA (NYSE) vs BA (NEO TSX CAD Hedged). We can see the strong relationship and high confidence calculations.

And some others:

SPX (primary) and ES1! (secondary):

RTY and IWM:

ES1! and SPY:

Customizations:

As you can see above, it is pretty straight forward. There are 3 options:

Lookback Length: Determines the length of assessment for correlation and the regression assessment.

Manual Ticker Input: The indicator will pull the data from your current chart and compare it against a manually selected indicator. You must tell the indicator which ticker you are comparing against.

Data Table: This will show you the data table which contains the standard error assessment and the correlation assessment. These are determined by your lookback length. The lookback length is defaulted to 500.

And that's the indicator! It's pretty straight forward. Hopefully you find it helpful, especially if you track futures during overnight sessions.

Leave your comments/questions and feedback below.

Thanks for checking it out!

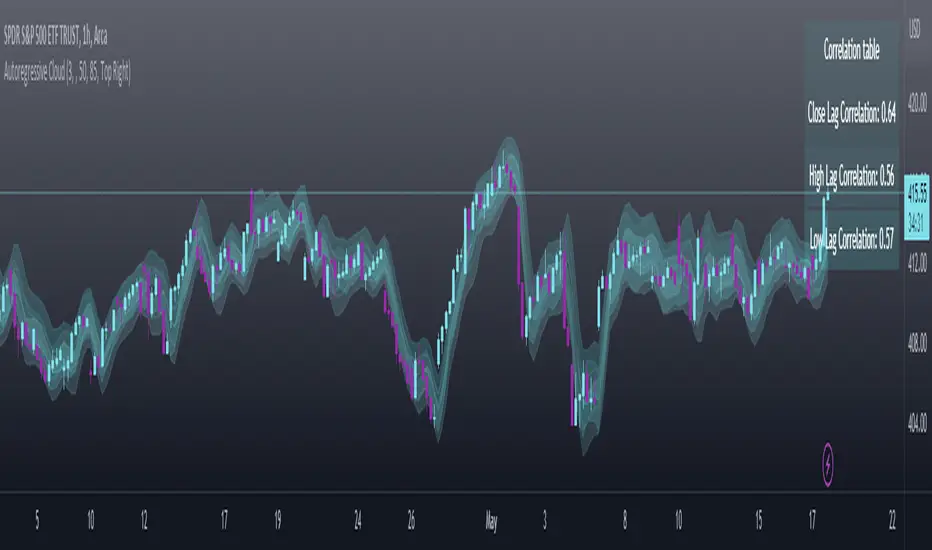

Autoregressive CloudHello,

I am releasing this indicator called the Autoregressive Cloud Indicator.

What it does:

The indicator performs an autoregression analysis on 3 price variables of a ticker, those being the High, the Low and the Close. It uses a 1-lag system and looks back at the previous close, high and low’s effect on the proceeding high, low and close. It then plots out the anticipated range for the ticker based on the autoregression analysis, as well as displays the lag-correlation (autocorrelation) in a table.

What is Autoregression analysis?

Autoregression is a modelling technique used to describe a time series based on its own past values. It assumes that the current value of a variable is a linear combination of its previous values and a random error term.

And what is autocorrelation?

Autocorrelation measures the correlation between a time series and its lagged values. It quantifies the degree to which the current value of a series is related to its past values at different lags, indicating any patterns or dependencies in the data over time. Autoregression and autocorrelation are closely related concepts used to analyze and model time series data.

So how does it work?

The indicator calculates autoregressive values for the close, high, and low prices of a security based on the specified lookback length (which is defaulted to 50). It then plots three sets of clouds representing the smoothed autoregressive values for each price component (done using the SMA function). The transparency of the clouds can be adjusted using the "Transparency" input. Additionally, the code includes a correlation table that displays the correlation coefficients between the lagged values of the close, high, and low prices. The table's position can be customized using the "Position" input.

The indicator defaults to the chart timeframe; however, you can manually adjust the indicator to display the range for whatever timeframe you would like. You can view the 30 minute, 15 or even hourly range on the 1 minute or 5 minute chart if you want.

The indicator will show the anticipated “true trading range” of the stock based on the autoregression and autocorrelation of all 3 variables:

Above is SPY on the 5 minute timeframe with 15 minute levels overlayed. Here, you can see the anticipated trading range for that 15 minute time period.

Using the Correlation Table:

The correlation table displays the Pearson Coefficient for all 3 autoregressions.

A positive correlation: A positive autocorrelation indicates a positive relationship between past and current values of a time series variable. It suggests that when the variable has a high value at a certain time, it is more likely to have a high value in the future, and when it has a low value, it is more likely to have a low value in the future. This positive autocorrelation can imply persistence or trend in the data, indicating that past values can provide useful information for predicting future values. The rule of thumb is anything over 0.5 is considered significant.

A positive correlation among all 3 variables also indicates an uptrend. If you see a strong positive (i.e. the values are all greater than 0.8), it indicates an incredibly decisive and strong uptrend.

A negative correlation: A negative autocorrelation indicates an inverse relationship between past and current values of a time series variable. It suggests that when the variable has a high value at a certain time, it is more likely to have a low value in the future, and vice versa. This negative autocorrelation can imply mean reversion or oscillatory behavior in the data, where extreme values tend to be followed by values closer to the average. It indicates that past values can provide useful information for predicting future values by anticipating a reversal in the direction of the variable. The rule of thumb is anything below or equal to -0.5 is considered significant.

A negative correlation among all 3 variables also indicates a downtrend. If you see a strong negative (i.e. the values are all less than or equal to -0.8), it indicates an incredibly decisive and strong downtrend.

Uses of the Indicator:

The indicator can be used for the following functions:

1. Day trading and scalping within an expected range;

2. Determining the strength or weakness of an uptrend or downtrend on various timeframes;

3. Determining the relationship between previous values and past performance and its effect on future performance;

4. Can alert to changes in trend direction in advance (you may see high, low or close turn negative before others, signifying that weakness is beginning to materialize in an uptrend, or inverse in a downtrend (value changes positive)).

Customizability:

SMA: The autoregression data is smoothed by a 3 period lookback. You can change this if you want, but in order for the indicator to present the true trading range, it is recommended to leave it at <= 3.

Lookback Length: This is the length of the lookback period for the autoregression and autocorrelation functions.

Transparency settings: You can adjust the transparency of the clouds manually.

Timeframe: You can adjust the timeframe, as explained above, to display the timeframe of interest. When you adjust the timeframe, the data will all reflect that timeframe and not necessarily the current TF you have open (i.e. you select 30 minutes while viewing it on the 5 minute, it will show the data for the 30 minute TF period).

Video Tutorial:

I have prepared a video outlining the indicator and also explaining the theory of autoregression/correlation. You can find it below:

Let me know any comments, questions or suggestions below.

Thank you for taking the time to read/watch and check out this indicator.

Safe trades everyone!

Put to Call Ratio CorrelationHello!

Excited to share this with the community!

This is actually a very simple indicator but actually usurpingly helpful, especially for those who trade indices such as SPX, IWM, QQQ, etc.

Before I get into the indicator itself, let me explain to you its development.

I have been interested in the use of option data to detect sentiment and potential reversals in the market. However, I found option data on its own is full of noise. Its very difficult if not impossible for a trader to make their own subjective assessment about how option data is reflecting market sentiment.

Generally speaking, put to call ratios generally range between 0.8 to 1.1 on average. Unless there is a dramatic pump in calls or puts causing an aggressive spike up to over this range, or fall below this range, its really difficult to make the subjective assessment about what is happening.

So what I thought about trying to do was, instead of looking directly at put to call ratio, why not see what happens when you perform a correlation analysis of the PTC ratio to the underlying stock.

So I tried this in pinescript, pulling for Tradingview's ticker PCC (Total Equity Put to Call Ratio) and using the ta.correlation function against whichever ticker I was looking at.

I played around with this idea a bit, pulled the data into excel and from this I found something interesting. When there is a very significant negative or positive correlation between PTC ratio and price movement, we see a reversal impending. In fact, a significant negative or positive correlation (defined as a R value of 0.8 or higher or -0.8 or lower) corresponded to a stock reversal about 92% of the time when data was pulled on a 5 minute timeframe on SPY.

But wait, what is a correlation?

If you are not already familiar, a correlation is simply a statistical relationship. It is defined with a Pearson R correlation value which ranges from 0 (no correlation) to 1 (significant positive correlation) and 0 to -1 (significant negative correlation).

So what does positive vs negative mean?

A significant positive correlation means the correlation is moving the same as the underlying. In the case of this indicator, if there is a significant positive correlation could mean the stock price is climbing at the same time as the PTC ratio.

Inversely, it could mean the stock price is falling as well as the PTC ratio.

A significant negative correlation means the correlation is moving in the opposite direction. So in this case, if the stock price is climbing and the PTC ratio is falling proportionately, we would see a significant negative correlation.

So how does this work in real life?

To answer this, let's get into the actual indicator!

In the image above, you will see the arrow pointing to an area of significant POSITIVE correlation.

The indicator will paint the bars on the actual chart purple (customizable of course) to signify this is an area of significant correlation.

So, in the above example this means that the PTC ratio is increase proportionately to the increase in the stock price in the SAME direction (Puts are going up proportionately to the stock price). Thus, we can make the assumption that the underlying sentiment is overwhelmingly BEARISH. Why? Because option trading activity is significantly proportionate to stock movement, meaning that there is consensus among the options being traded and the movement of the market itself.

And in the above example we will see, the stock does indeed end up selling:

In this case, IWM fell roughly 1 point from where there was bearish consensus in the market.

Let's use this same trading day and same example to show the inverse:

You will see a little bit later, a significant NEGATIVE correlation developed.

In this case identified, the stock wise RISING and the PTC ratio was FALLING.

This means that Puts were not being bought up as much as calls and the sentiment had shifted to bullish .

And from that point, IWM ended up going up an additional 0.75 points from where there was a significant INVERSE correlation.

So you can see that it is helpful for identifying reversals. But what is also can be used for is identifying areas of LOW conviction. Meaning, areas where there really is no relationship between option activity and stock movement. Let's take spy on the 1 hour timeframe for this example:

You can see in the above example there really is no consensus in the option trading activity with the overarching sentiment. The price action is choppy and so too is option trading activity. Option traders are not pushing too far in one direction or the other. We can also see the lack of conviction in the option trading activity by looking at the correlation SMA (the white line).

When a ticker is experiencing volatile and good movement up and down, the SMA will generally trade to the top of the correlation range (roughly + 1.0) and then make a move down to the bottom (roughly - 1.0), see the example below:

When the SMA is not moving much and accumulating around the centerline, it generally means a lot of indecision.

Additional Indicator Information:

As I have said, the indicator is very simple. It pulls the data from the ticker PCC and runs a correlation assessment against whichever ticker you are on.

PCC pulls averaged data from all equities within the market and is not limited to a single equity. As such, its helpful to use this with indices such as SPY, IWM and QQQ, but I have had success with using it on individual tickers such as NVDA and AMD.

The correlation length is defaulted to 14. You can modify it if you wish, but I do recommend leaving it at this as the default and the testing I have done with this have all been on the 14 correlation length.

You can chose to smooth the SMA over whichever length of period you wish as well.

When the indicator is approaching a significant negative or positive relationship, you will see the indicator flash red in the upper or lower band to signify the relationship. As well, the chart will change the bar colour to purple:

Everything else is pretty straight forward.

Let me know your questions/comments or suggestions around the indicator and its applications.

As always, no indicator is meant to provide a single, reliable strategy to your trading regimen and no indicator or group of indicators should be relied on solely. Be sure to do your own analysis and assessments of the stock prior to taking any trades.

Safe trades everyone!

Opening Hour/Closing Hour Indices Statistics: high/low times; 5mVery specific indicator designed for 5min timeframe, to show the statistical timings of the highs and lows of Opening hour (9:30-10am) and Closing hour (3pm-4pm) NY time

~~Shown here on SPX 5min chart. Works all variants of the US indices. SPX and SPY typically show more days of history (non-extended session =>> more bars).

//Purpose:

-To get statistics on the timings of the high and low of the opening hour and the high & low of the closing hour.

//Design & Limitations:

- Designed for the 5minute chart ONLY . Need a sweet spot of 'bucket' size for the statistics: to allow meaningful comparison between times.

-Will also display on 1min chart but NOT the statistics panel, only the realtime data (today's opening hour/ closing hour timings).

-Can be slow to load depending on server load at the time. This is becasue of the multiple usage of looping array functions. Please be patient when loading or changing settings.

//User inputs:

-Standard formatting options: highlight color, table text color. Toggle on/off independently

-Decimal % percision (default = 0, i.e. 23%. If set to 1 => 22.8%)

-Show statistics: Show Opening hour statistics, Show Closing hour statistics

//Notes:

-Days of history shown at top of table; this is the size of the dataset. i.e. 254 here (254 trading days) =>> 254 opening hour highs, 254 closing hour lows etc.

--to illustrate with the above: 18% of those 254 closing hour highs occured on the 15:00 5min candle (i.e. between 15:00 and 15:05).

-SPY or SPX offer the largest history/dataset (circa 254 trading days).

-Note that the final timing in each hour is 10:25am and 15:55pm respectively: this is because the 10:25am 5min candle essentially ends at 10:30am =>> we properly captures the opening hour this way

-Pro+ users will get less data history than Premium users (half as much, due to 10k vs 20k bars history limit).

Big 8 Intraday TICKAt the start of each trading day (0930 EST), this indicator calculates the intraday price difference between open and close for the eight largest market cap stocks (AAPL, AMZN, GOOGLE, META, MSFT, NFLX, NVDA, and TSLA), assigns a +/-1 for each, and then plots the cumulative change. An EMA has been added for smoothing purposes that is set to 5 but can be changed. Please note indicator is best used on lower timeframes (15 min or less) and has no applicability to time frames above 1 hour.

The thought behind this indicator is those eight major stocks drive a majority of intraday price change in indices like SPY and QQQ that are heavily weighted towards these stocks, therefore they should be a leading indicator in price change. You can often catch a move in SPY or QQQ one to two bars (on 1 min chart) ahead of the actual move because you see this indicator moving strong to one direction.

It's not perfect as there are divergences you will see when you compare historical charts, but oftentimes those divergences ultimately lead to significant price swings in the same direction as this indicator, so recommend being on watch to pull the trigger when you see those and price confirms.

You can use this indicator in a few ways:

1. Confirmation that your current trade is in the same direction as this indicator

2. Use the zero cross as a trigger for put or call entry

3. Focusing only on calls/longs if the value is above 0, or only puts/shorts if the value is below zero. Just be sure to keep an eye on reversals.

If you have recommendations on how to improve, let me know and I'll do my best to make changes.

Relative Strength/Weakness ArrowsHello everyone,

This Script is designed to show relative strength or relative weakness. It takes the stock your looking at and compares it to the sector it is in and to SPY. It evaluates strength or weakness on every candle. In this specific script it is only designed for the communications sector(XLC), so all the names I have inputted into the script fall within XLC. It works for all timeframes. It really helps me stay in trades longer as even though stock might be consolidating it can still be weak, making me more confident in holding. Each green arrow shows that the stock is relatively strong compared to SPY and its SECTOR, in this case, XLC. Each red arrow means that the stock is relatively weak to the market and its sector. When there are no arrows on the candles, then the stock is following the market and its sector. Tell me what yall think.

Just add it to your chart, go to any of the stocks within XLC and it will populate arrows based on relative strength and relative weakness. The weakness and strength is based on movement of price using ATR. So if the price of the stock is moving up and so is the sector it will only populate based on how large the move is. So if SPY had ATR of 1 and it moved up .50c that means the stock you're looking at would need to move more than .50c in the same candle if it also had an ATR or 1.

You can add or delete tickers in the code by going to the list of symbols and adding or removing them. Just remember that if you add a stock that doesn't fall within XLC then the arrows wont represent strength/weakness properly.

Munich's Momentum Wave V2MUNICH'S MOMENTUM WAVE VERSION 2 IS LIVE!!!

There are a few big things to note with this one.

I decided to upload this as an entirely new script due to the number of changes differing from the first version, but as the last one, this will still work on ANY TIMEFRAME, ANY ASSET CLASS, ANY PRICE! .

This momentum wave indicator now will give you data for when trend could turn, and two momentum indicators to help you decide when to take an entry.

First off,

*I have added an alma ma (alma) that will track momentum alongside price action and further lead the indicator consisting of the Munich waves.

* The background feature will track the price using a method derived from the Bollinger bands, after calculations, it will color the background based on the average of the momentum's ema's, the alma ma, and also the alma in comparison to the alma's value pre offset ( the offset is 3, following the basis).

*There are now 5 basis values given from the increase in ema samples.

If anyone has any questions feel free to pm me or comment below. Thank you guys for the support! :)

INDEX:BTCUSD TVC:NDQ AMEX:SPY BITSTAMP:ETHUSD BINANCE:BTCUSDT FX:USDJPY NASDAQ:AAPL

Strategy: Combo Z ScoreStrategy version of Combo Z Score

Objective:

Can we use both VIX and MOVE relationships to indicate movement in the SPY? VIX (forward contract on SPY options) correlations are quite common as forward indicators however MOVE (forward contract on bonds) also provides a slightly different level of insight

Using the Z-Score of VIX vs VVIX and MOVE vs inverted VIX (there is no M of Move so we use inverted Vix as a proxy) we get some helpful indications of potential future moves. Added %B to give us some exposure to momentum. Toggle VIX or MOVE.

If anyone has a better idea of inverted Vix to proxy forward interest in MOVE let me know.

Noticeable delta is that Vix only approach over the back test period is slightly better. Questions would be, what is the structure and nature of the market over the test period and in a bear market would MOVE or combined perform better.

Combo Z ScoreObjective:

Can we use both VIX and MOVE relationships to indicate movement in the SPY? VIX (forward contract on SPY options) correlations are quite common as forward indicators however MOVE (forward contract on bonds) also provides a slightly different level of insight

Using the Z-Score of VIX vs VVIX and MOVE vs inverted VIX (there is no M of Move so we use inverted Vix as a proxy) we get some helpful indications of potential future moves. Added %B to give us some exposure to momentum. Toggle VIX or MOVE.

If anyone has a better idea of inverted Vix to proxy forward interest in MOVE let me know.

Gap Size Outcome Statistics [vnhilton]This indicator displays a table with statistics showing the outcomes of gap ups or downs based on your threshold (i.e. does the day end in green or red?). This can be useful for trading, where you're using relevant ETFs & see that they've gapped up/down, & can assume based on statistics that the ETF will end in green/red depending on which has the higher probability (however, you can use these on any other instruments such as stocks to find edges e.g. seeing whether stock XYZ is more likely to end in green/red when it gaps up 100%).

The table also includes sample sizes for your threshold tests for more confidence in the statistics, & also displays average gap up & downs & their respective sample sizes as well. This indicator is intended to be used on the daily timeframe, but can be used on lower or higher timeframes if you prefer.

In the chart snapshot image above, we can see that when the SPY gaps up > 1%, the day is more likely to end in green than in red. But when the SPY gaps down < -1%, it's also more likely to end in green than in red.

( IMPORTANT NOTE : There's 1 limitation with this indicator & it's that it assumes that days where close=open are green days, & that 0% gaps exact are considered gap ups.)

Parabolic SAR Heikin Ashi MTF Candle ScalperThis is scalper strategy designed around parabolic sar indicator, where as an input candle value it uses the heikinashi from a higher timeframe.

This example has been adapted to SPY/SPX chart

In this case ,we are using a 5 min chart, but the calculations are made on a 15 min heikin ashi chart for the PSAR and then on 5 min chart we plot the results.

At the same time we are conditioning the entry to be base on a time/session for daytrading/scalper mentality

In this case we only enter within the first 30 min of SPY opening session , and then we exit after 3-4 hours of staying in the position ( unless we hit a reverse condition).

For long condition we enter when the mtf ha candle close is above the mtf psar and for short condition we enter when the mtf ha candle close is below the mtf psar

This script is made with an educational purpose to show the power of multiple time frame approach compared to a single chart.

If you have any questions, let me know !

HLC True Strength Indicator (with Vix)HLC True Strength Indicator Volume Weighted with Vix Line by SpreadEagle71

This indicator is a True Strength Indicator with Close, High and Low used together, along with the TSI of the Vix.

The white line is the close. The red line is the lows and the blue is the highs. These are also volume-weighted.

How to Interpret:

1. zero line crosses. If SPY/SPX500 crosses the zero line, then its bullish. If the purple Vix line crosses up, watch out because this is bearish.

2. white/blue/red lines cross purple (Vix). If they cross upwards, this is bullish. If downward, this is bearish. Basically, SPX, ES1!, SPY or even DIA can be used. The security and the Vix should travel in opposite directions and cross the zero-line at the same time. But this is not always the case.

3. Black area infills. These are used between the close and the highs (blue) and the lows(red). Close should not be between these in order to have momentum.

4. Close (white line) leads. Close is the last price so it tends to show where the others (highs and lows) are going. If the close is sagging below a high where the blue lines are on top, this could mean that there is a reversal coming. Same holds true for a white line above a "valley" formed by the blue and red lines; it could mean a reversal to the upside soon.

5. The Black Infill areas as a squeeze or contraction/expansion area. The thinner the black infill areas, the more of a momentum "squeeze" could be present. Wide black infill areas mean increased volatility and what may come next is a reversion to the mean for volatility. See TTM Squeeze Indicator or the Squeeze Momentum Indicator (kudos LazyBear).

Lastly, just remember indicators indicate; they are not magic. :)

SpreadEagle71