"vwap"に関するスクリプトを検索

VWAP From Multiple Sources With Cloud & Percentage GapVWAP CLOUD FROM CLOSE, OPEN, HIGH & LOW SOURCES WITH CLOUD & PERCENTAGE GAP

VWAP stands for volume weighted average price and shows the average price of buys/sells based on volume traded across the current session. This VWAP is based off of the Daily session.

***HOW TO USE***

Use the purple cloud between the VWAPs as your entry points as price will typically bounce from that cloud area.

The Yellow Line is the VWAP using the close price as a source.

The Green Line is the VWAP using the open price as a source.

The Blue Line is the VWAP using the high price as a source.

The Purple Line is the VWAP using the low price as a source.

When price is above the VWAP cloud, the background will paint green because the trend is bullish.

When price is below the VWAP cloud, the background will paint red because the trend is bearish.

In the bottom right hand corner, three is a table that will show you the current percentage gap between current price and the VWAP using close as the source.

All sources and colors can be easily switched in the settings menu.

***MARKETS***

This indicator can be used as a signal on all markets, including stocks, crypto, futures and forex.

***TIMEFRAMES***

This vwap indicator can be used on all timeframes but is calculated using the daily session.

***TIPS***

Try using numerous indicators of ours on your chart so you can instantly see the bullish or bearish trend of multiple indicators in real time without having to analyze the data. Some of our favorites are our Auto Fibonacci, Volume Profile, Directional Movement Index, Momentum, Auto Support And Resistance and Money Flow Index in combination with this VWAP Cloud. The other indicators all have real time Bullish and Bearish labels as well so you can immediately understand each indicator's trend.

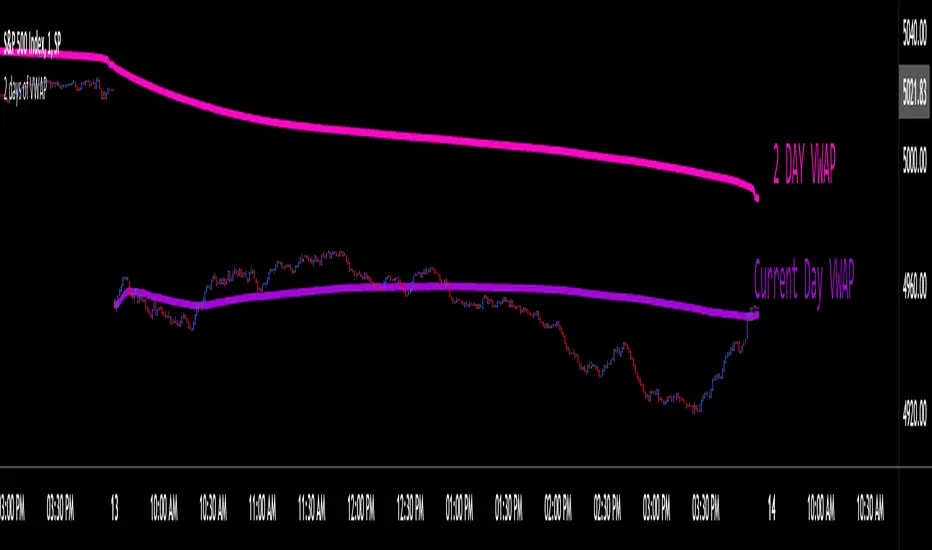

VWAP_CURRENT_YESTERDAY

The "VWAP CURRENT YESTERDAY" is a Pine Script designed for TradingView that automatically calculates and plots the Volume Weighted Average Price (VWAP) for the current day, the previous day.

Dynamic VWAP Calculation:

Automatically generates VWAPs for 1 day and 2 day.

User-Friendly Customization:

Through input options, users can easily toggle the visibility of each VWAP line, adjust colors, and set line thicknesses to their preference.

Configuration Options

1. VWAP Source:

Choose the price source for VWAP calculation. Default is the typical price (`hlc3` - the average of high, low, and close).

2. VWAP Lines:

Toggle the display for Today's VWAP, Yesterday's VWAP, and the VWAP from 2 days ago.

Customize colors and thickness for each VWAP line for clear visual distinction.

3. VWAP Labels:

Configure label sizes and positions to ensure that VWAP values are easily identifiable on the chart.

How It Works:

- The script calculates the sum of price multiplied by volume (`vwapsum`) and the sum of volumes (`volumesum`) for the specified periods.

- It utilizes an impulse function to reset calculations at the start of each new session or custom date, ensuring accurate and relevant VWAP values .

- Final VWAP values are plotted as lines on the chart, with optional labels for current and 2-day VWAPs for quick reference.

Customization Guide:

- To activate or deactivate specific VWAP lines, navigate to the 'VWAP Lines' section in the script's settings and toggle the respective options.

- Adjust the color and thickness of each VWAP line under the same section to match your charting preferences.

- Label settings, including size and offset, can be customized in the 'VWAP Labels' section, allowing for personalized label positioning and readability.

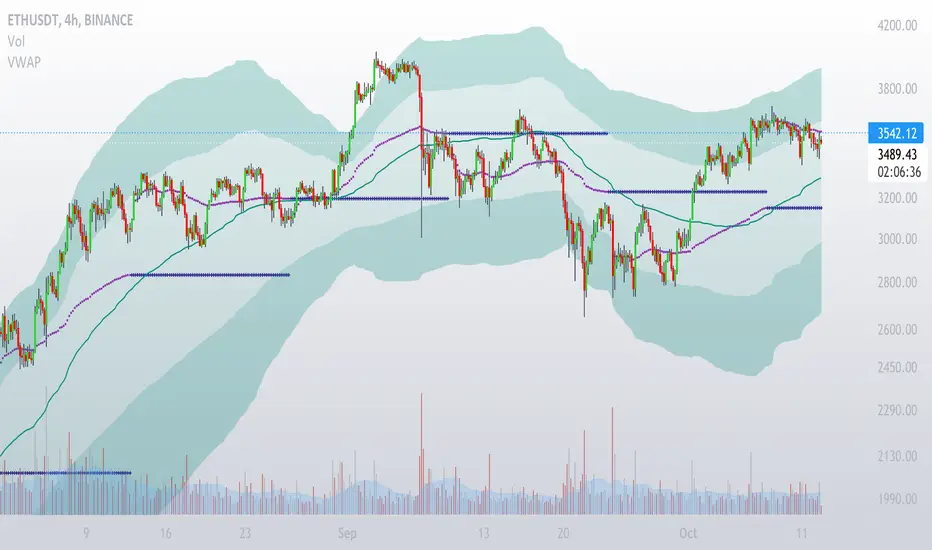

VWAP w/ Std Deviation bands extensionsVWAP with Standard Deviation Bands and Extensions

This indicator does 3 things:

1. Plot session VWAP

2. Plot up to 5 Standard Deviation Bands of VWAP

3. Plot extension of previous session's VWAP and Extension Bands

Comments are welcome.

Enjoy.

VWAP_ multi exchanges for crypto marketvwap of multiple exchanges to smooth the signal.

above the ribbon long.

under the ribbon short

VWAP Standard Deviation Multi-Time FrameVWAP Standard Deviation Multi-Time Frame indicator shows VWAP , 1 standard deviation price from the VWAP, 2 standard deviation price from the VWAP and 3 standard deviation price from the VWAP

These lines are value regions and usually act as great support and resistance .

For best results allow the VWAP to develop in the beginning of the time frame, for almost about 20% of the total time period

For example, in a daily time frame, wait for about 4hrs for VWAP to develop before using the VWAP and Standard devaitions of VWAP as support and resistance zones

Change the values in timeframe input to use it for intraday, swing and long term trades.

Possible values are based on standard timeframe values 5,15,D,W,M, 12M etc

VWAP Bands @shrilssVWAP Bands Integrates VWAP with standard deviation bands to provide traders with insights into potential support and resistance levels based on volume dynamics. VWAP is a key metric used by institutional traders to gauge the average price a security has traded at throughout the trading day, taking into account both price and volume.

This script calculates the VWAP for each trading session and overlays it on the price chart as a solid line. Additionally, it plots multiple standard deviation bands around the VWAP to indicate potential areas of price extension or contraction. These bands are derived from multiplying the standard deviation of price by predetermined factors, offering traders a visual representation of potential price ranges.

VWAP MTF (Multi Timeframe)VWAP that can be be plotted from different timeframes.

Ex if you chose 60 min, it will plot a new vwap line at the start of every hour.

Intraday:

Used code from SandroTurriate to create this.

VWAP OscilatorVWAP Oscillator - Awesome Oscillator but using different period Volume Weighted Average Price values instead of moving averages. Used to get an idea of the momentum of price movements and when momentum might be reversing.

Vwap Comp [Auto+Osc] [Intromoto]This script compares the spot or USDT vwaps to the perpetuals, or USDTPERP, specifically for Binance.

This script will only work properly on binance perpetual charts. It auto detects which chart you're on and shows the appropriate comparison.

I made this due to the volume discrepancies between the derivative and spot markets.When the oscillator is below zero, the perpetual vwap is below the spot vwap, if it's above, the perpetual vwap is above the spot vwap.

Colors become more extreme the further away the vwaps are. Bright green increase the odds of a bullish reversal, red or pink columns indicate a potential for bearish reversal.

For example. If I'm on the BINANCE:ETHUSDTPERP chart, the script will compare the BINANCE:ETHUSDT to the BINANCE:ETHUSDTPERP vwaps with the input metrics.

Users can change the thresholds that determine the colors of the plots on the oscillator. Users can also input the time frame observed. The default is set to 'D' or daily Vwaps. If you change the time frame you'll likely have to tweak the thresholds to give reasonable color indication.

DM for access.

Thanks.

VwapWhaleBasically it is an indicator that is based on different vwap

You have the vwap of the day, of the week, and the vwap at overbought and oversold levels.

This will help you distribute the different buy and sell orders. think like a whale

You no longer have an excuse to make money.

You have a twap line with the volumes that are generated over the session. Every band can be used to help you to your target profits in every trade direction

Remember to put it in a "session" timeframe, as it is useful for scalping and daytrading.

Trading tips:

The vwap of the week, if it is below, acts as support. If it is above it acts as resistance, and gives you a slight idea of the market trend. During the day, the candles will be attracted to the different vwap , with the vwap of the session having greater weight. The different vwaps can be considered as zones of order diversification

Let me know if was useful for you :)

Thanks for the idea -

-dysrupt

-jaggedsoft

VWAP2D+Displays the current and previous days' VWAP. A useful tool for intraday VWAP traders or to optimize longer term entries or exits.

Features:

Shows levels exceeding the average deviation for the time of day as either warm or cool gradients.

Custom alerts including "Closing In Range" which uses the ATR to determine if the closing value in in the vicinity of the current day's VWAP.

VWAP with Standard Deviation BandsVolume Weighted Average Price (VWAP), with Standard Deviation Bands

VWAP is a moving average with weighting for traded volume, so heavier trading activity has a greater impact on its direction. Low volume periods will move the VWAP less than high volume periods.

The VWAP is important because institutional investors often use it to determine what is ‘fair value’. You can often see the market reacting when it gets close to the VWAP.

This version is time segmented VWAP. It reset ma values when selected time period expires.

Time periods are able to be selected in the settings: "1D", "2D", "W", "14D", "M", "60D", "12M", "24M", "Custom".

Additionally script determines VWAP standard deviations.

Multipliers for VWAP Standard Deviation Bands can be changed in the settings.

There is also option to show previous VWAP and its Standard Deviation Bands before timeframe reset.

VWAPPIVWAPPI (Volume Weighted Average Price Performance Index) measures the strength of each trend using VWAP and various other factors. We can use the strength of the VWAPPI to plan entries and exits. It is also possible to play it's divergences.

Works on any market and on any timeframe.

1m/1W VWAPs X WVWAPVWAP indicator great for intraday trading. Includes a 1-minute VWAP, Weekly VWAP colored red/green, and an adjustable MVWAP with the default set to 21.

VWAP SuiteThis indicator automates the plotting of various timeframe based VWAP Values. This utilizes a different calculation method for the standard deviations bands compared to the native Tradingview AVWAP. While the Tradingview AVWAP indicator calculates the standard devation based on the VWAP variance, this indicator calculates the std dev based on the price sum variance (i.e. the variance of the hlc3, ohlc4, etc. values).

Current timeframes include:

- Daily VWAP with three user configurable standard deviation bands

- Multi-Day VWAP that allows you to plot 2-day to 5-day VWAP

- Weekly VWAP with three user configurable standard deviation bands

- Monthly VWAP with three user configurable standard deviation bands

Some unique aspects of this indicator is that it allows the user to calculate VWAP for only a specific session range if you are only interested in the VWAP when specific participants are active in the market. For example, the default session range only calculates VWAP for the New York RTH session (0930-1600).

If the user wants to compare how the session range chosen varies from the VWAP calculation with ETH you can select the 'Include Extended Trading Hours' check box which will ignore the session range input variable and simply calculate what is exactly on the chart without filtering.

You can also toggle whether the VWAP values show up in the price scale, status line, or both which can limit the amount of clutter that shows up on the chart based upon the user's preferences.

VWAP Stdev Bands v2This is an update to my original VWAP Stdev Bands indicator found here:

* Fixed the calculation of the opening bar

* Added two additional deviation bands

* Added horizontal line of previous VWAP close

This update adds support for two more sets of bands, allowing you to show 1st, 2nd, and 3rd deviations. These extra bands are disabled by default as to not crowd the chart, but are shown in the screenshot and can be enabled under the indicator settings. The numbers 3.09 and 1.28 were recommended by coondawg71 in a comment on the original version. The previous version started calculating VWAP on a change of day, instead of a change of session. It now correctly calculates the VWAP when a new session begins. The last addition allows you to plot the previous day's VWAP close. The VWAP is where price has found balance, which makes these levels significant among the noise.

Thanks to coondawg71 for all suggestions.

VWAP DelayedDisplay VWAP and VWAP standard deviation plots only during the specified time period. Useful if you want to avoid seeing all of the lines bunched up at the beginning of the day. Note that VWAP is calculated for the full day just not displayed until the specified time period. Optionally, you can include/exclude pre-market data in the VWAP calculation for the day.

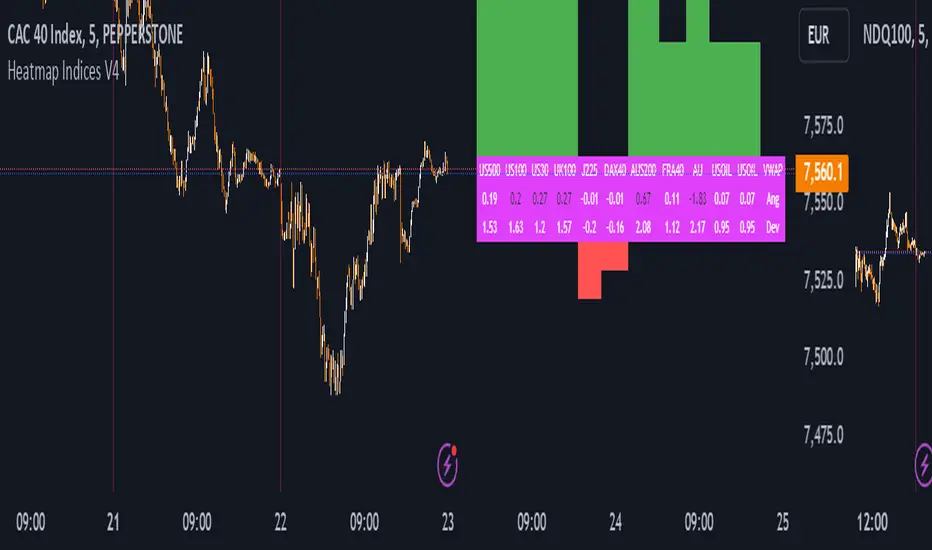

VWAP Heatmap Commodities and Indices V2Here is the Crashcourse trading VWAP for indices and Commodities. Same deal as the forex heatmap. It works best being on a 5 minute chart. Suggestion is to put it on the EURUSD together with the forex heatmap so you can see all the price action on one screen. You are looking for an approach to the VWAP and looking for a bounce. Remember if you have no gradient you have no trade!!!

The instruments covered:

1. US500 / S&P500 Capital.com

2. US100 / Nasdaq Capital.com

2. US30 / Dow Jones Capital.com

4. UK100 / FTSE100 Capital.com

5. JP225 / Nikkei225 Capital.com

6. DAX / DE40 Currency.com

7. AUS200 Capital.com

8. HK50 Capital.com

9. FRA40 / CAC Capital.com

10. Gold Capital.com

11. USoil / WTI Capital.com

12. UKoil / Brent Capital.com

These present the best volume and price data to give you the most reliable signals as far as I have determined.

Improvements coming for this will be to incorporate a slope for the vwap and to make better levels.

VWAP with editable Volume Time Frame1. This custom indicator is based on TradingView VWAP preset indicator.

2. I added this line input("D", type=input.resolution, title="Time Frame") so I can adjust the time frame for the calculation of VWAP

3. The original VWAP setting is set at "D" while in this custom indicator, we can choose which time frame we prefer to suit our trading style.

VWAP TF-Aware===========================================================

8/Feb/2020 02:57 PM AUTHOR: Brandon Gum

-

DESCRIPTION:

This is a timeframe aware VWAP indicator. The built-in VWAP indicator was changed in late 2019 which resulted in it no longer being restricted to low timeframes. As a result the indicator would plot on higher timeframe charts and create "noise" between candles.

This Version of vwap only displays vwap on 30 minute and below times frames.

===========================================================