QuantLabs The MTF Nasdaq 30 Scanner [Capital Flow and Pressure]Trading the QQQ (Nasdaq) without knowing what the Generals (Apple, Nvidia, Microsoft) are doing is like driving at night with your headlights off. You might see the road right in front of you, but you'll miss the turn coming up.

The QuantLabs MTF Nasdaq 30 Scanner is not just a trend indicator, it is a professional-grade Market Dashboard that visualizes the heartbeat of the entire Nasdaq 100.

Why You Need This

Standard indicators lag. They tell you what happened after the move. This Heatmap tracks the Real-Time Capital Flow of the Top 30 companies that actually move the index ($Trillions in Market Cap).

Key Features

1. The "Spectacular" Precision Heatmap

Organized by Market Cap Size (AAPL/NVDA first).

Instantly spot divergent behavior. Is the market rallying, or is it just Nvidia holding everything up? The Heatmap reveals the truth instantly.

Colors: Neon Cyan (Bullish) vs Hot Pink (Bearish).

2. Triple Spectrum Technology (3-in-1 Timeframes) Why look at one timeframe when you can see three? Every cell in the dashboard displays the trend distance for:

8h (Fast): For scalping entries.

16h (Mid): For swing trends.

24h (Slow): For the major "Big Picture" bias.

Values denote % distance from the Flux Ribbon.

3. The "Net Pressure" Gauge (The Speedometer) A predictive summary footer that calculates the Weighted Pressure of the entire market.

HEAVY (> 0.5%): Strong Trend / Breakout Mode.

MODERATE (0.2% - 0.5%): Healthy, sustained move.

FLAT: Chop / Noise. Stay out.

It also shows exactly how much Capital ($Trillions) is sitting Bullish vs Bearish.

How to Trade with It

Check the "Net Pressure": If it says MODERATE BULLISH, you are looking for Longs only.

Scan the Top Row: Are the "Big 5" (AAPL, NVDA, MSFT...) aligned with the pressure?

Wait for Alignment: If the 8h, 16h, and 24h metrics all turn Cyan, that is a "Quantum Lock"—a high probability breakout signal.

Simple. Powerful. Neon. Add it to your chart and stop guessing the direction.

Credits: Built with 💜 by David James @ QuantLabs

Statistic

Strategy Validator - Backtest & Live TradeStrategy Validator is an analytical indicator for TradingView designed to evaluate trade setups, risk structure, and price behavior in real time.

The indicator builds trade scenarios, visualizes key trade levels, and provides statistical context based on historical data.

Its purpose is to help traders better understand current trade conditions and make decisions based on market structure rather than isolated signals.

🔶 Conceptual Approach

Many tools focus on a single question:

“Is there a signal right now?”

Strategy Validator approaches the market differently by analyzing a trade as a structured scenario that includes:

• current market state

• price position relative to key levels

• acceptable risk boundaries

• potential price expansion range

The indicator evaluates how well the active trade configuration aligns with historically observed market conditions and visualizes its boundaries directly on the chart.

🔶 Trade Condition Analysis

For each active configuration, the indicator evaluates:

• alignment of the entry with market structure

• market phase (directional movement, range, or elevated activity)

• risk-to-outcome relationship

• historical behavior of similar setups

The goal is to highlight trades with a clear structure and controlled risk , while filtering out weak or unstable conditions.

🎯 Trade Structure on Chart

Each trade is displayed directly on the chart with clearly defined elements:

• Entry — trade entry level

• Take Profit — projected target level

• Stop Loss — risk limitation level based on market structure and volatility

This allows immediate understanding of trade boundaries without manual calculations.

🧪 Statistical Context & Backtest

The indicator includes an integrated statistical panel showing:

• Win Rate

• Profit Factor

• Maximum Drawdown

• Net Result

• Total Trades

Two information blocks are available:

• BACKTEST — historical behavior of similar trade conditions

• POSITION — parameters and real-time state of the current trade

Historical data is used to provide analytical context, not to predict future performance.

🔶 Markets & Timeframes

🌍 Compatible with all TradingView markets:

• Crypto

• Forex

• Stocks & ETFs

• Indices

• Commodities

• Futures

⏱ Works on all timeframes — from intraday analysis to long-term charts.

🔶 Intended Use

Strategy Validator is designed for traders who:

• focus on risk-aware decision making

• prefer structured market analysis

• evaluate trades in context rather than isolation

• use statistics as a supporting decision layer

Important Notice

This indicator is an analytical tool and does not guarantee profitability.

It is not a trading robot or an automated execution system.

Past results do not guarantee future outcomes.

Always apply proper risk management.

Strategy Validator PRO - Backtest & Alerts📊 Strategy Validator PRO is a professional analytical indicator for TradingView designed to evaluate trade configurations, risk structure, and potential outcomes under current market conditions.

The indicator generates trade signals, visualizes entry and exit levels, and provides statistical context to support data-driven trading decisions rather than assumptions.

⚠️ PRO version is available by invitation only.

A simplified FREE version is publicly available for concept evaluation.

🔶 Core Concept

Most indicators answer the question:

“Where to enter?”

Strategy Validator PRO focuses on a more important one:

“How justified is this trade under current market conditions?”

The indicator applies a predefined analytical logic and evaluates how well the current trade setup aligns with statistically stable market conditions identified on an extended historical dataset.

🔶 Key Features

📈 Trade Configuration Analysis

The indicator evaluates:

• signal quality

• current market regime (trend, consolidation, volatility)

• risk-to-outcome structure

• historical behavior of similar setups

🎯 The goal is to filter weak or unfavorable trade conditions rather than simply generate signals.

🎯 Trade Structure on Chart

Each trade is displayed directly on the chart with a clear structure:

• Entry — trade entry level

• Take Profit — projected target level

• Stop Loss — risk limitation level based on market structure and volatility

This allows immediate understanding of trade boundaries without manual calculations.

🧪 Integrated Backtest Dashboard

The indicator displays performance statistics for the active logic:

• Win Rate

• Profit Factor

• Maximum Drawdown

• Net Profit

• Total Trades

Two panels are available:

• BACKTEST — historical performance overview

• POSITION — details of the current open trade

📌 Historical data is used to provide statistical context, not to predict future performance.

🔔 TradingView Alerts (PRO)

In the PRO version, alerts can be configured using TradingView’s native alert system.

Alerts may be created for:

• trade configuration formation

• target level reached

• risk limitation triggered

Available alert formats:

• Simple — plain text

• With levels — including price levels

• JSON — structured format for external analysis

🔶 PRO vs FREE

🟢 FREE

• Base analytical logic

• Limited historical depth

• Core trade structure

• Backtest dashboard

• Trade history

🔵 PRO

• Extended historical analysis

• Higher statistical sampling depth

• Trade condition filtering

• TradingView alerts

FREE version is intended for concept evaluation.

PRO version is designed for systematic and disciplined trading.

🔶 Markets & Timeframes

🌍 Compatible with all TradingView markets:

• Crypto

• Forex

• Stocks & ETFs

• Indices

• Commodities

• Futures

⏱ Works on all timeframes — from intraday to long-term.

🔶 Access

🔓 FREE version

Publicly available.

🔐 PRO version

Available by invitation.

Access can be requested via the author’s profile links or by contacting the author directly.

⚠️ Important Notice

This indicator is an analytical tool and does not guarantee profitability.

It is not a trading robot or automated execution system.

Past performance does not guarantee future results.

Always apply proper risk management.

Market Session Terrain Monitor vs 1.0 (UTC)Summary

Market Session Terrain Monitor helps traders understand where the market is within its normal intraday behavior, not where it should go. It is a decision-support tool designed to reduce late entries, over-trading, and narrative bias by grounding intraday analysis in historical session statistics.

Purpose

Market Session Terrain Monitor provides statistical context for intraday market movement by analyzing how much each major trading session typically moves, how much it has moved so far, and what market state the current session inherits from previous sessions.

The indicator is designed to answer one core question:

Is the current session early, normal, or already expanded relative to its historical behavior?

This indicator does not predict direction and does not generate buy or sell signals. It is intended as a context and state-awareness tool to support independent, structure-based decision making.

Sessions Analyzed

The trading day is divided into three independent sessions, defined in UTC time:

• Asia

• London

• New York

Each session is analyzed separately using its own historical data. No session is assumed to control or predict the behavior of another.

Session Range

For each session, the indicator measures the session range, defined as the session high minus the session low. This captures how much the market actually moved during that session, regardless of direction.

P90 Expansion Benchmark

For each session, the indicator calculates a P90 expansion benchmark.

• P90 represents the range that only about ten percent of historical sessions exceed

• It reflects a large but repeatable expansion, not an extreme outlier

• It is used as a normalization reference so sessions with different volatility characteristics can be compared on equal terms

The P90 values are displayed in the table header in price units, such as USD, as a reference for scale.

Percent of P90

Current and previous session ranges are expressed as a percentage of that session’s own P90.

This shows:

• How much of a statistically large session has already been used

• Whether the session is still early, behaving normally, or approaching expansion

Rolling Comparative Table

The table displays three rows, ordered by time and anchored to the current active session:

• Current · Session

• Previous · Session

• Previous-2 · Session

Each row shows:

• Session name

• Session range in price units

• Session range as a percentage of that session’s P90

This rolling layout provides context about the market state inherited by the current session without implying causality.

How to Use the Indicator

The indicator helps with:

• Identifying whether a session is early or late in its statistical range

• Avoiding entries when a session is already stretched

• Recognizing compression versus expansion regimes

• Understanding the market state the current session inherits

The indicator does not:

• Predict direction

• Forecast highs or lows

• Assume that one session determines the next

Directional decisions should come from price structure, execution rules, and risk management.

Design Philosophy

• Range first, direction second

• State awareness over narrative

• Statistical normalization instead of absolute numbers

• Comparative, not predictive

The indicator intentionally avoids estimating remaining range or subtracting previous session movement, as those approaches introduce bias and false causality.

Suitable Markets

• Gold and silver

• Forex pairs

• Indices

• Other liquid instruments with clear session behavior

Market Session Terrain Monitor v1.0Summary

Market Session Terrain Monitor helps traders understand where the market is within its normal intraday behavior, not where it should go. It is a decision-support tool designed to reduce late entries, over-trading, and narrative bias by grounding intraday analysis in historical session statistics.

Purpose

Market Session Terrain Monitor provides statistical context for intraday market movement by analyzing how much each major trading session typically moves, how much it has moved so far, and what market state the current session inherits from previous sessions.

The indicator is designed to answer one core question:

Is the current session early, normal, or already expanded relative to its historical behavior?

This indicator does not predict direction and does not generate buy or sell signals. It is intended as a context and state-awareness tool to support independent, structure-based decision making.

Sessions Analyzed

The trading day is divided into three independent sessions, defined in UTC time:

• Asia

• London

• New York

Each session is analyzed separately using its own historical data. No session is assumed to control or predict the behavior of another.

Session Range

For each session, the indicator measures the session range, defined as the session high minus the session low. This captures how much the market actually moved during that session, regardless of direction.

P90 Expansion Benchmark

For each session, the indicator calculates a P90 expansion benchmark.

• P90 represents the range that only about ten percent of historical sessions exceed

• It reflects a large but repeatable expansion, not an extreme outlier

• It is used as a normalization reference so sessions with different volatility characteristics can be compared on equal terms

The P90 values are displayed in the table header in price units, such as USD, as a reference for scale.

Percent of P90

Current and previous session ranges are expressed as a percentage of that session’s own P90.

This shows:

• How much of a statistically large session has already been used

• Whether the session is still early, behaving normally, or approaching expansion

Rolling Comparative Table

The table displays three rows, ordered by time and anchored to the current active session:

• Current · Session

• Previous · Session

• Previous-2 · Session

Each row shows:

• Session name

• Session range in price units

• Session range as a percentage of that session’s P90

This rolling layout provides context about the market state inherited by the current session without implying causality.

How to Use the Indicator

The indicator helps with:

• Identifying whether a session is early or late in its statistical range

• Avoiding entries when a session is already stretched

• Recognizing compression versus expansion regimes

• Understanding the market state the current session inherits

The indicator does not:

• Predict direction

• Forecast highs or lows

• Assume that one session determines the next

Directional decisions should come from price structure, execution rules, and risk management.

Design Philosophy

• Range first, direction second

• State awareness over narrative

• Statistical normalization instead of absolute numbers

• Comparative, not predictive

The indicator intentionally avoids estimating remaining range or subtracting previous session movement, as those approaches introduce bias and false causality.

Suitable Markets

• Gold and silver

• Forex pairs

• Indices

• Other liquid instruments with clear session behavior

Dynamic Breakout Odds [RayAlgo]█ OVERVIEW

Dynamic Breakout Odds is a probability-based breakout tool that uses ATR and pattern matching to estimate how likely price is to expand up or down from the current candle.

Instead of guessing, the indicator scans historical candles that look like the current one and measures how often price broke above or below by a volatility-based amount.

It then projects those probabilities forward as clean levels and a bias dashboard on your chart.

Use it to quickly answer:

• “Is the next move statistically more likely up or down?”

• “How far does price typically travel from here, in ATR terms?”

█ CONCEPTS

Candle Profile Matching

The script builds a “profile” of the current setup using two elements:

• The color of the previous candle (bullish close vs bearish close)

• The trend environment (above/below EMA, if the filter is enabled)

Only historical candles with the same profile are used for statistics. This keeps the probabilities specific to the current context instead of mixing all market conditions together.

ATR-Based Expansion

For every matching historical candle, the script checks how far price moved away from the open using ATR:

• Upward move thresholds

• Moderate expansion (≈ 0.5 ATR above the open)

• Stronger expansion (≈ 1.0 ATR above the open)

• Downward move thresholds

• Moderate expansion (≈ 0.5 ATR below the open)

• Stronger expansion (≈ 1.0 ATR below the open)

It counts how often each expansion happened, then converts those counts into probabilities.

Normalized Probability Scores

The indicator doesn’t just show raw percentages; it normalizes them so that all scenarios together form a consistent probability set.

Internally it tracks four outcomes for similar candles:

• Chance of a moderate move upward

• Chance of a strong move upward

• Chance of a moderate move downward

• Chance of a strong move downward

These are then normalized so the total is roughly 100%. From this, two main metrics are derived:

• Bullish Strength = combined normalized odds of upside moves

• Bearish Strength = combined normalized odds of downside moves

Whichever side has the higher score defines the current directional bias .

█ WHAT YOU SEE ON THE CHART

1. Breakout Projection Levels

Four horizontal levels are projected around the open of the current bar:

• Two upside levels

• Nearer upside expansion (~0.5 ATR above the open)

• Further upside expansion (~1.0 ATR above the open)

• Two downside levels

• Nearer downside expansion (~0.5 ATR below the open)

• Further downside expansion (~1.0 ATR below the open)

Each line extends a configurable number of bars into the future, so you visually see a breakout “corridor” above and below price.

2. Probability Labels

At the right edge of each line, you’ll see a label such as:

• “X% – near upside”

• “Y% – further downside”

These labels tell you how frequently similar candles in the chosen lookback reached that expansion. You immediately know which scenario has been more common historically.

3. Breakout Zones

Between the paired upside lines and the paired downside lines, shaded “probability zones” can be shown:

• The upper shaded band highlights the typical upside expansion range

• The lower shaded band highlights the typical downside expansion range

These zones visually group probable target areas instead of just single lines.

4. Background Tint

The background behind price is softly tinted towards:

• Bullish color when Bullish Strength > Bearish Strength

• Bearish color when Bearish Strength > Bullish Strength

The stronger the statistical imbalance between the two, the more pronounced the tint. This gives you an instant feel for whether conditions lean more Long, more Short, or are nearly Neutral.

5. Directional Bias Arrow

On the last bar the script can plot a clean arrow:

• Up-arrow below price when bullish odds dominate

• Down-arrow above price when bearish odds dominate

The arrow is positioned beyond all projection lines, making it easy to see even on cluttered charts and reminding you of the current statistical bias without text.

6. Origin Marker

A small horizontal mark is drawn at the open of the current candle.

This acts as the “starting point” from which all ATR-based expansions above and below are measured.

7. Dashboard Panel

A compact dashboard is drawn in a corner of the chart (location configurable). It displays:

• Bullish Strength – combined normalized probability for upside expansions

• Bearish Strength – combined normalized probability for downside expansions

• Bias – “Long Bias”, “Short Bias”, or “Neutral”

• Trend Filter – shows whether EMA-based filtering is ON or OFF and which length is used

This gives you a quick, text-based summary of the current statistical environment.

█ SETTINGS

Analysis Lookback Period

• Controls how many historical bars the script inspects when searching for similar candles.

• Larger values = more history, smoother statistics, slower adaptation.

• Smaller values = faster adaptation, but more noise and less stability.

ATR Length

• The period used to compute ATR volatility.

• Defines how “big” 0.5 ATR and 1.0 ATR moves are on your current symbol and timeframe.

Trend Filter (EMA)

• Filter by Trend?

• When ON, only historical candles in a similar trend regime are used.

• When OFF, all past candles with similar color are considered, regardless of trend.

• Trend EMA Length

• EMA period used to classify trend.

• Price above EMA → uptrend environment.

• Price below EMA → downtrend environment.

This filter helps you separate behavior in uptrends from downtrends, which can significantly change breakout dynamics.

Visual Settings

• Projection Width (bars)

• How far the lines and zones extend into the future.

• Show Probability Zones

• Toggle shaded bands between each pair of levels.

• Label Size

• Choose smaller or larger text for the probability labels on the right.

• Tint Background by Bias

• Turn the bias-based background on or off.

• Show Bias Marker on Last Candle

• Toggle the up/down arrow marker.

• Dashboard Location

• Select top/bottom left/right corner for the panel.

█ HOW TO USE IT

1. Start With the Dashboard

Look at Bullish Strength vs Bearish Strength:

• If bullish is clearly larger → environment statistically favors upside expansion.

• If bearish is clearly larger → environment statistically favors downside expansion.

• If they are close → treat the situation as Neutral; consider reducing position size or waiting for more clarity.

2. Use Levels as Dynamic Targets

The projected lines and zones can serve as:

• Profit targets based on typical expansion distance

• Logical regions for scaling out

• Areas where you expect price behavior to change (e.g., loss of momentum)

Short-term traders often focus on the nearer expansion levels, while swing traders may use the farther levels as extended targets.

3. Align With Trend (Optional)

With the trend filter ON:

• Prefer Long setups when price is above the EMA and bullish probabilities dominate.

• Prefer Short setups when price is below the EMA and bearish probabilities dominate.

With the filter OFF, you get pure color-plus-pattern statistics across the whole lookback, which can be useful if you deliberately trade counter-trend or range conditions.

4. Combine With Your Existing System

Dynamic Breakout Odds is best used as a confirmation and targeting layer :

• Combine it with structure (support/resistance, supply/demand, order blocks).

• Combine it with volume or orderflow tools if you use them.

• Use the probability zones to validate whether your planned target is realistic relative to recent volatility.

It is not designed to be a standalone “buy/sell” signal generator, but a statistical map around your entries.

█ PRACTICAL EXAMPLES

Example A – Bullish, Moderate Expansion Frequently Hit

• Bullish Strength significantly higher than Bearish Strength.

• The nearer upside level shows a strong historical hit rate.

Interpretation: similar setups often produce at least a moderate push upward before failing.

Use case: trade pullbacks in the direction of the bias, targeting the nearer upside projection as an initial take-profit.

Example B – Bearish, Deeper Downside Often Reached

• Bearish Strength clearly dominant.

• Both the nearer and farther downside levels show decent probabilities.

Interpretation: similar conditions historically saw follow-through to the downside.

Use case: use rallies against the direction of the bias to position into shorts, planning partial exits around the first downside projection and runners toward the second.

Example C – Neutral, Balanced Probabilities

• Bullish and Bearish Strength scores are close.

• Background tint is very light or absent.

Interpretation: the market is statistically indecisive; expansions up or down are similarly likely.

Use case: consider range trading tactics, mean-reversion ideas, or simply standing aside until a clearer skew develops.

█ BEST PRACTICES

• Use on liquid symbols and reasonable timeframes to avoid distorted ATR behavior.

• Don’t overfit lookback length to a single instrument; test across markets.

• Let the indicator provide context, not absolute certainty.

• Always combine with proper risk management (position sizing, max loss per trade, etc.).

• Be cautious with very small sample sizes (e.g., very short lookbacks on low-volume assets).

█ LIMITATIONS & NOTES

• All probabilities are based on historical behavior ; markets can change regime.

• ATR distances are relative to recent volatility and may shrink/expand over time.

• The script intentionally does not guarantee any direction or target; it only reports what has been most common in similar past situations.

█ DISCLAIMER

This tool is for educational and informational purposes only.

It does not constitute financial advice or a guarantee of performance.

Always do your own research, test on demo or historical data, and use appropriate risk management when trading live capital.

Stock Relative Strength Rotation Graph🔄 Visualizing Market Rotation & Momentum (Stock RSRG)

This tool visualizes the sector rotation of your watchlist on a single graph. Instead of checking 40 different charts, you can see the entire market cycle in one view. It plots Relative Strength (Trend) vs. Momentum (Velocity) to identify which assets are leading the market and which are lagging.

📜 Credits & Disclaimer

Original Code: Adapted from the open-source " Relative Strength Scatter Plot " by LuxAlgo.

Trademark: This tool is inspired by Relative Rotation Graphs®. Relative Rotation Graphs® is a registered trademark of JOOS Holdings B.V. This script is neither endorsed, nor sponsored, nor affiliated with them.

📊 How It Works (The Math)

The script calculates two metrics for every symbol against a benchmark (Default: SPX):

X-Axis (RS-Ratio): Is the trend stronger than the benchmark? (>100 = Yes)

Y-Axis (RS-Momentum): Is the trend accelerating? (>100 = Yes)

🧩 The 4 Market Quadrants

🟩 Leading (Top-Right): Strong Trend + Accelerating. (Best for holding).

🟦 Improving (Top-Left): Weak Trend + Accelerating. (Best for entries).

⬜ Weakening (Bottom-Right): Strong Trend + Decelerating. (Watch for exits).

🟥 Lagging (Bottom-Left): Weak Trend + Decelerating. (Avoid).

✨ Significant Improvements

This open-source version adds unique features not found in standard rotation scripts:

📝 Quick-Input Engine: Paste up to 40 symbols as a single comma-separated list (e.g., NVDA, AMD, TSLA). No more individual input boxes.

🎯 Quadrant Filtering: You can now hide specific quadrants (like "Lagging") to clear the noise and focus only on actionable setups.

🐛 Trajectory Trails: Visualizes the historical path of the rotation so you can see the direction of momentum.

🛠️ How to Use

Paste Watchlist: Go to settings and paste your symbols (e.g., US Sectors: XLK, XLF, XLE...).

Find Entries: Look for tails moving from Improving ➔ Leading.

Find Exits: Be cautious when tails move from Leading ➔ Weakening.

Zoom: Use the "Scatter Plot Resolution" setting to zoom in or out if dots are bunched up.

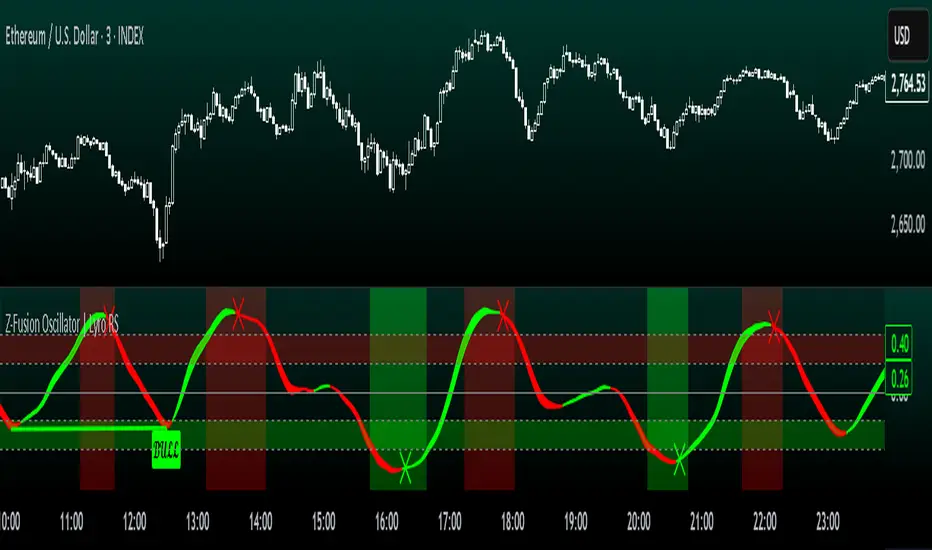

Z-Fusion Oscillator | Lyro RSThe Z-Fusion Oscillator converts five momentum indicators into Z-scores and blends them into one normalized signal that adapts across markets.

By combining normalization, smoothing, and divergence detection, users can easily identify when momentum is accelerating, weakening, reversing, or entering extreme zones

🔶 USAGE

The Z-Fusion Oscillator is designed to give traders a unified reading of market momentum—removing the noise of comparing tools that normally run on different scales.

By transforming RSI, MACD histogram, Stochastic, Momentum, and Rate of Change into Z-scores, this tool standardizes all inputs, making trend strength and shifts easier to interpret.

A dual-line system (fast Z-fusion line + slower baseline) highlights turning points, while overbought/oversold bands and “X-marks” help traders spot exhaustion and potential reversals.

🔹 Unified Momentum Structure

The indicator’s core strength comes from combining five Z-scored signals into one average.

Which makes momentum behavior more consistent across assets, reduces false extremes, and highlights true shifts in trend conviction.

🔹 Divergence Detection

The tool includes fully integrated divergence detection:

Regular Bullish Divergence: Price makes a lower low while Z-Fusion forms a higher low.

Regular Bearish Divergence: Price makes a higher high while Z-Fusion forms a lower high

Bullish and bearish divergences are marked directly on the oscillator with labels and colored pivot connections, making hidden momentum shifts obvious.

🔹 Visual Extremes

Two sets of upper and lower Z-score thresholds help identify:

Extreme overbought surges

Extreme oversold drops

Reversal zones

Potential exhaustion conditions

Background coloring reinforces when the oscillator moves beyond major levels, helping traders quickly assess momentum pressure.

🔹 Detecting Momentum Anomalies

Z-scores allow the oscillator to highlight when market momentum behaves abnormally relative to its own recent history.

For example:

The oscillator reaching +1 or –1 after an extended trend may indicate a climax.

A sharp Z-score reversal within an extreme zone can signal a trend exhaustion or a corrective move.

Divergences often appear earlier due to normalization smoothing out indicator noise.

This makes the Z-Fusion Oscillator particularly useful for spotting subtle shifts in trend direction that traditional indicators may miss.

🔶 DETAILS

🔹 Composite Z-Score Framework

Each momentum tool is smoothed, normalized, and transformed:

RSI → EMA-smoothed, Z-scored

MACD histogram → Z-scored

Stochastic → EMA + SMA smoothing, then Z-scored

Momentum → EMA-smoothed, Z-scored

Rate of Change → EMA-smoothed, Z-scored

These are averaged into one composite Z-score to provide a consistent reading across assets and market conditions.

🔹 Fusion Trend Lines

Two lines serve as the core signal:

Fast Line (savg) – reacts quicker to trend changes

Slow Line (savg2) – acts as a baseline filter

Crossovers between these lines highlight momentum shifts, while their color reflects trend bias.

🔹 Overbought/Oversold Zones

Two upper and two lower Z-score thresholds define “zones”:

Upper zones highlight overheated momentum or potential bearish reversals

Lower zones highlight depressed momentum or potential bullish reversals

Filled regions and background colors help visually confirm extreme conditions.

🔹 Pivot-Based Divergence Engine

The script includes filtered pivot detection with customizable look-backs and range limits to ensure divergences are meaningful, not noise-driven.

🔶 SETTINGS

🔹 Indicator Settings

Source — Price series used for all calculations.

Z-Score Length — Lookback period for Z-score normalization.

Z-Score MA Length — Smoothing length for the fusion signal lines.

Overbought/Oversold Levels — Four customizable threshold lines.

Color Palette — Choose from preset themes or define custom colors.

🔹 RSI

Length — RSI calculation period.

EMA Smoothing Length — Smooths RSI before Z-score conversion.

🔹 MACD

Fast Length — Fast EMA length.

Slow Length — Slow EMA length.

Signal Line Length — MACD signal smoothing.

🔹 Stochastic

%K Length — Main stochastic length.

EMA Smoothing — Smooths %K for stability.

%D Length — Smoothing for the signal line.

🔹 Momentum

Length — Momentum lookback.

EMA Smoothing — Smooths momentum before Z-scoring.

🔹 Rate of Change

Length — ROC lookback.

EMA Smoothing — Smooths ROC values.

🔹 Divergence

Enable/Disable Divergence Detection — Toggle divergence engine.

Pivot Left/Right Lookback — Defines pivot detection sensitivity.

Detection Range Limits — Controls allowable range for divergence.

Bull/Bear Colors & Styling — Customize divergence visualization.

🔶 SUMMARY

The Z-Fusion Oscillator combines multiple momentum signatures into a single normalized signal, enabling traders to:

Identify reversals early

Detect momentum exhaustion

Spot bullish and bearish divergences

Track overbought/oversold conditions

Visualize trend strength with clarity

Whether you're a swing trader, intraday analyst, or trend-reversal hunter, the Z-Fusion Oscillator provides a powerful and adaptive way to read momentum.

Multi-Asset % Performance Table | v2.1 | TCP Multi-Asset % Performance Table | v2.1 | TCP

ESSENTIAL SUMMARY:

Multi-Asset % Performance Table eliminates the need to manually draw and manage individual "Price Range" tools for every asset. It automatically tracks up to 15 tickers independently in a single dashboard, calculating a TOTAL SCORE (Portfolio Average) for you. Unlike manual drawings, it supports a Global Range while allowing Custom Dates for specific assets, ensuring each ticker is calculated based on its own precise entry/exit. The Smart Visuals dynamically draw the correct date lines only for the ticker you are currently viewing, keeping your chart automatic, accurate, and clutter-free.

FUL DESCRIPTION:

📊 What is this tool?

The Multi-Asset % Performance Table is a powerful portfolio dashboard designed to track the percentage performance of up to 15 different assets simultaneously.

Instead of checking tickers one by one or manually drawing price ranges, this indicator aggregates everything into a single, clean table. It allows you to compare the ROI (Return on Investment) of a basket of coins or stocks over a specific time period and calculates an aggregate TOTAL SCORE (Average %) for your selection.

🚀 Key Features

15 Asset Slots: Monitor up to 15 different tickers (Crypto, Stocks, Forex, etc.) in one view.

Global vs. Custom Dates: Set a "Global" start/end date for the whole portfolio, but override specific assets with Custom Dates if they entered the portfolio at a different time.

Smart Visuals: Automatically draws vertical dashed lines on your chart representing the start and end dates of the ticker you are currently viewing.

Total Score Calculation: Calculates the average percentage change of your portfolio. You can dynamically include or exclude specific assets from this average using the settings.

Status Column: A quick visual reference (✔ or ✘) in the table showing which assets are currently included in the Total Score calculation.

⚙️ How it Works

Data Fetching: The script pulls "Close" prices from the Daily timeframe to ensure accuracy across long periods.

Smart Matching: The visual lines automatically detect which asset you are viewing. For example, if you are looking at BTCUSDT and have custom dates set for it, the vertical lines will jump to those specific dates. If you view a ticker not in your list, it defaults to the Global dates.

Visual Protection: The script uses advanced logic to ensure only one set of range lines appears on the chart at a time, keeping your workspace clean.

🛠️ Instructions & Settings

1. Setting up your Assets

Open the Settings (Cogwheel icon).

Under ASSET 1 through ASSET 15, enter the tickers you want to track (e.g., BINANCE:BTCUSDT).

Include in Avg?: Uncheck this if you want to see the asset in the table but exclude it from the "TOTAL SCORE" average.

2. Defining Time Ranges

Global Settings: Set the Global Start and Global End dates at the top. This applies to all assets by default.

Custom Dates: If a specific asset (e.g., Asset 4) was bought on a different day, check the "Custom Dates?" box for that asset and enter its specific Start/End time.

3. Reading the Table

The table appears on the chart (default: Bottom Right) with three columns:

Asset: The name of the ticker.

% Change: The percentage move from Start Date to End Date. (Green = Positive, Red = Negative).

Inc: Shows a ✔ if the asset is included in the Total Score average, or a ✘ if excluded.

4. The Visual Lines

Two vertical dashed lines will appear on your chart.

Note: These lines are visual references only. You cannot drag them to change the dates. To change the dates, you must use the Settings menu.

💡 Tips

Hover for Details: Hover your mouse over the % Change value in the table to see a tooltip showing the exact Start Price and End Price used for the calculation.

Resolution: The script defaults to 1 Day resolution for optimal accuracy on historical data.

v2.1 | TCP - Custom Built for Precision Performance Tracking

Spot-Futures SpreadSpot-Futures Spread Indicator

A comprehensive indicator that automatically calculates and visualizes the percentage spread between spot and perpetual futures prices across multiple exchanges.

Key Features:

Automatic Exchange Detection - Automatically detects your current exchange and finds the corresponding spot/futures pair

Smart Fallback System - If the counterpart isn't available on your exchange, it automatically searches across 7+ major exchanges (Binance, Bybit, OKX, Gate.io, MEXC, KuCoin, HTX) and uses the first valid match

Multi-Exchange Support - Works with 14 exchanges including Binance, Bybit, OKX, MEXC, BitGet, Gate.io, KuCoin, and more

Clear Exchange Attribution - Shows exactly which exchanges are providing spot and futures data in the statistics table

Configurable Moving Average - Track the average spread with customizable period

Standard Deviation Bands - Identify unusual spread conditions with Bollinger-style bands

Built-in Alerts - Get notified when spread crosses bands or zero (parity)

Statistics Table - Real-time stats showing current spread, MA, std dev, and bands

Manual Override Options - Advanced users can manually specify exchanges and symbols

How It Works:

The indicator calculates the spread as: (Futures Price - Spot Price) / Spot Price × 100

Positive spread = Futures trading at a premium (contango)

Negative spread = Futures trading at a discount (backwardation)

Zero = Parity between spot and futures

Use Cases:

Funding Rate Analysis - Correlates with perpetual funding rates

Arbitrage Opportunities - Identify significant spot-futures divergences

Market Sentiment - Premium/discount indicates bullish/bearish positioning

Cross-Exchange Analysis - Compare spreads when spot and futures are on different exchanges

Smart Features:

Works whether you're viewing a spot or futures chart

Automatically handles exchange-specific perpetual contract naming (.P, PERP, SWAP, etc.)

Color-coded visualization (green for premium, red for discount)

Customizable colors and display options

Background shading based on spread direction

Perfect For:

Crypto traders monitoring funding rates, arbitrage traders, market makers, and anyone interested in spot-futures dynamics across multiple exchanges.

Getting Started:

Simply add the indicator to any spot or perpetual futures chart. It will automatically detect the exchange and find the corresponding pair. The statistics table shows which exchanges are being used for maximum transparency.

Note: The indicator automatically ignores invalid symbols, so you'll never see errors even if a specific pair doesn't exist on a particular exchange.

Kudos to @AlekMel that made the "Spot - Fut Spread v2" indicator that I enhance the Automatic detection feature which was not working in some case.

LibWghtLibrary "LibWght"

This is a library of mathematical and statistical functions

designed for quantitative analysis in Pine Script. Its core

principle is the integration of a custom weighting series

(e.g., volume) into a wide array of standard technical

analysis calculations.

Key Capabilities:

1. **Universal Weighting:** All exported functions accept a `weight`

parameter. This allows standard calculations (like moving

averages, RSI, and standard deviation) to be influenced by an

external data series, such as volume or tick count.

2. **Weighted Averages and Indicators:** Includes a comprehensive

collection of weighted functions:

- **Moving Averages:** `wSma`, `wEma`, `wWma`, `wRma` (Wilder's),

`wHma` (Hull), and `wLSma` (Least Squares / Linear Regression).

- **Oscillators & Ranges:** `wRsi`, `wAtr` (Average True Range),

`wTr` (True Range), and `wR` (High-Low Range).

3. **Volatility Decomposition:** Provides functions to decompose

total variance into distinct components for market analysis.

- **Two-Way Decomposition (`wTotVar`):** Separates variance into

**between-bar** (directional) and **within-bar** (noise)

components.

- **Three-Way Decomposition (`wLRTotVar`):** Decomposes variance

relative to a linear regression into **Trend** (explained by

the LR slope), **Residual** (mean-reversion around the

LR line), and **Within-Bar** (noise) components.

- **Local Volatility (`wLRLocTotStdDev`):** Measures the total

"noise" (within-bar + residual) around the trend line.

4. **Weighted Statistics and Regression:** Provides a robust

function for Weighted Linear Regression (`wLinReg`) and a

full suite of related statistical measures:

- **Between-Bar Stats:** `wBtwVar`, `wBtwStdDev`, `wBtwStdErr`.

- **Residual Stats:** `wResVar`, `wResStdDev`, `wResStdErr`.

5. **Fallback Mechanism:** All functions are designed for reliability.

If the total weight over the lookback period is zero (e.g., in

a no-volume period), the algorithms automatically fall back to

their unweighted, uniform-weight equivalents (e.g., `wSma`

becomes a standard `ta.sma`), preventing errors and ensuring

continuous calculation.

---

**DISCLAIMER**

This library is provided "AS IS" and for informational and

educational purposes only. It does not constitute financial,

investment, or trading advice.

The author assumes no liability for any errors, inaccuracies,

or omissions in the code. Using this library to build

trading indicators or strategies is entirely at your own risk.

As a developer using this library, you are solely responsible

for the rigorous testing, validation, and performance of any

scripts you create based on these functions. The author shall

not be held liable for any financial losses incurred directly

or indirectly from the use of this library or any scripts

derived from it.

wSma(source, weight, length)

Weighted Simple Moving Average (linear kernel).

Parameters:

source (float) : series float Data to average.

weight (float) : series float Weight series.

length (int) : series int Look-back length ≥ 1.

Returns: series float Linear-kernel weighted mean; falls back to

the arithmetic mean if Σweight = 0.

wEma(source, weight, length)

Weighted EMA (exponential kernel).

Parameters:

source (float) : series float Data to average.

weight (float) : series float Weight series.

length (simple int) : simple int Look-back length ≥ 1.

Returns: series float Exponential-kernel weighted mean; falls

back to classic EMA if Σweight = 0.

wWma(source, weight, length)

Weighted WMA (linear kernel).

Parameters:

source (float) : series float Data to average.

weight (float) : series float Weight series.

length (int) : series int Look-back length ≥ 1.

Returns: series float Linear-kernel weighted mean; falls back to

classic WMA if Σweight = 0.

wRma(source, weight, length)

Weighted RMA (Wilder kernel, α = 1/len).

Parameters:

source (float) : series float Data to average.

weight (float) : series float Weight series.

length (simple int) : simple int Look-back length ≥ 1.

Returns: series float Wilder-kernel weighted mean; falls back to

classic RMA if Σweight = 0.

wHma(source, weight, length)

Weighted HMA (linear kernel).

Parameters:

source (float) : series float Data to average.

weight (float) : series float Weight series.

length (int) : series int Look-back length ≥ 1.

Returns: series float Linear-kernel weighted mean; falls back to

classic HMA if Σweight = 0.

wRsi(source, weight, length)

Weighted Relative Strength Index.

Parameters:

source (float) : series float Price series.

weight (float) : series float Weight series.

length (simple int) : simple int Look-back length ≥ 1.

Returns: series float Weighted RSI; uniform if Σw = 0.

wAtr(tr, weight, length)

Weighted ATR (Average True Range).

Implemented as WRMA on *true range*.

Parameters:

tr (float) : series float True Range series.

weight (float) : series float Weight series.

length (simple int) : simple int Look-back length ≥ 1.

Returns: series float Weighted ATR; uniform weights if Σw = 0.

wTr(tr, weight, length)

Weighted True Range over a window.

Parameters:

tr (float) : series float True Range series.

weight (float) : series float Weight series.

length (int) : series int Look-back length ≥ 1.

Returns: series float Weighted mean of TR; uniform if Σw = 0.

wR(r, weight, length)

Weighted High-Low Range over a window.

Parameters:

r (float) : series float High-Low per bar.

weight (float) : series float Weight series.

length (int) : series int Look-back length ≥ 1.

Returns: series float Weighted mean of range; uniform if Σw = 0.

wBtwVar(source, weight, length, biased)

Weighted Between Variance (biased/unbiased).

Parameters:

source (float) : series float Data series.

weight (float) : series float Weight series.

length (int) : series int Look-back length ≥ 2.

biased (bool) : series bool true → population (biased); false → sample.

Returns:

variance series float The calculated between-bar variance (σ²btw), either biased or unbiased.

sumW series float The sum of weights over the lookback period (Σw).

sumW2 series float The sum of squared weights over the lookback period (Σw²).

wBtwStdDev(source, weight, length, biased)

Weighted Between Standard Deviation.

Parameters:

source (float) : series float Data series.

weight (float) : series float Weight series.

length (int) : series int Look-back length ≥ 2.

biased (bool) : series bool true → population (biased); false → sample.

Returns: series float σbtw uniform if Σw = 0.

wBtwStdErr(source, weight, length, biased)

Weighted Between Standard Error.

Parameters:

source (float) : series float Data series.

weight (float) : series float Weight series.

length (int) : series int Look-back length ≥ 2.

biased (bool) : series bool true → population (biased); false → sample.

Returns: series float √(σ²btw / N_eff) uniform if Σw = 0.

wTotVar(mu, sigma, weight, length, biased)

Weighted Total Variance (= between-group + within-group).

Useful when each bar represents an aggregate with its own

mean* and pre-estimated σ (e.g., second-level ranges inside a

1-minute bar). Assumes the *weight* series applies to both the

group means and their σ estimates.

Parameters:

mu (float) : series float Group means (e.g., HL2 of 1-second bars).

sigma (float) : series float Pre-estimated σ of each group (same basis).

weight (float) : series float Weight series (volume, ticks, …).

length (int) : series int Look-back length ≥ 2.

biased (bool) : series bool true → population (biased); false → sample.

Returns:

varBtw series float The between-bar variance component (σ²btw).

varWtn series float The within-bar variance component (σ²wtn).

sumW series float The sum of weights over the lookback period (Σw).

sumW2 series float The sum of squared weights over the lookback period (Σw²).

wTotStdDev(mu, sigma, weight, length, biased)

Weighted Total Standard Deviation.

Parameters:

mu (float) : series float Group means (e.g., HL2 of 1-second bars).

sigma (float) : series float Pre-estimated σ of each group (same basis).

weight (float) : series float Weight series (volume, ticks, …).

length (int) : series int Look-back length ≥ 2.

biased (bool) : series bool true → population (biased); false → sample.

Returns: series float σtot.

wTotStdErr(mu, sigma, weight, length, biased)

Weighted Total Standard Error.

SE = √( total variance / N_eff ) with the same effective sample

size logic as `wster()`.

Parameters:

mu (float) : series float Group means (e.g., HL2 of 1-second bars).

sigma (float) : series float Pre-estimated σ of each group (same basis).

weight (float) : series float Weight series (volume, ticks, …).

length (int) : series int Look-back length ≥ 2.

biased (bool) : series bool true → population (biased); false → sample.

Returns: series float √(σ²tot / N_eff).

wLinReg(source, weight, length)

Weighted Linear Regression.

Parameters:

source (float) : series float Data series.

weight (float) : series float Weight series.

length (int) : series int Look-back length ≥ 2.

Returns:

mid series float The estimated value of the regression line at the most recent bar.

slope series float The slope of the regression line.

intercept series float The intercept of the regression line.

wResVar(source, weight, midLine, slope, length, biased)

Weighted Residual Variance.

linear regression – optionally biased (population) or

unbiased (sample).

Parameters:

source (float) : series float Data series.

weight (float) : series float Weighting series (volume, etc.).

midLine (float) : series float Regression value at the last bar.

slope (float) : series float Slope per bar.

length (int) : series int Look-back length ≥ 2.

biased (bool) : series bool true → population variance (σ²_P), denominator ≈ N_eff.

false → sample variance (σ²_S), denominator ≈ N_eff - 2.

(Adjusts for 2 degrees of freedom lost to the regression).

Returns:

variance series float The calculated residual variance (σ²res), either biased or unbiased.

sumW series float The sum of weights over the lookback period (Σw).

sumW2 series float The sum of squared weights over the lookback period (Σw²).

wResStdDev(source, weight, midLine, slope, length, biased)

Weighted Residual Standard Deviation.

Parameters:

source (float) : series float Data series.

weight (float) : series float Weight series.

midLine (float) : series float Regression value at the last bar.

slope (float) : series float Slope per bar.

length (int) : series int Look-back length ≥ 2.

biased (bool) : series bool true → population (biased); false → sample.

Returns: series float σres; uniform if Σw = 0.

wResStdErr(source, weight, midLine, slope, length, biased)

Weighted Residual Standard Error.

Parameters:

source (float) : series float Data series.

weight (float) : series float Weight series.

midLine (float) : series float Regression value at the last bar.

slope (float) : series float Slope per bar.

length (int) : series int Look-back length ≥ 2.

biased (bool) : series bool true → population (biased); false → sample.

Returns: series float √(σ²res / N_eff); uniform if Σw = 0.

wLRTotVar(mu, sigma, weight, midLine, slope, length, biased)

Weighted Linear-Regression Total Variance **around the

window’s weighted mean μ**.

σ²_tot = E_w ⟶ *within-group variance*

+ Var_w ⟶ *residual variance*

+ Var_w ⟶ *trend variance*

where each bar i in the look-back window contributes

m_i = *mean* (e.g. 1-sec HL2)

σ_i = *sigma* (pre-estimated intrabar σ)

w_i = *weight* (volume, ticks, …)

ŷ_i = b₀ + b₁·x (value of the weighted LR line)

r_i = m_i − ŷ_i (orthogonal residual)

Parameters:

mu (float) : series float Per-bar mean m_i.

sigma (float) : series float Pre-estimated σ_i of each bar.

weight (float) : series float Weight series w_i (≥ 0).

midLine (float) : series float Regression value at the latest bar (ŷₙ₋₁).

slope (float) : series float Slope b₁ of the regression line.

length (int) : series int Look-back length ≥ 2.

biased (bool) : series bool true → population; false → sample.

Returns:

varRes series float The residual variance component (σ²res).

varWtn series float The within-bar variance component (σ²wtn).

varTrd series float The trend variance component (σ²trd), explained by the linear regression.

sumW series float The sum of weights over the lookback period (Σw).

sumW2 series float The sum of squared weights over the lookback period (Σw²).

wLRTotStdDev(mu, sigma, weight, midLine, slope, length, biased)

Weighted Linear-Regression Total Standard Deviation.

Parameters:

mu (float) : series float Per-bar mean m_i.

sigma (float) : series float Pre-estimated σ_i of each bar.

weight (float) : series float Weight series w_i (≥ 0).

midLine (float) : series float Regression value at the latest bar (ŷₙ₋₁).

slope (float) : series float Slope b₁ of the regression line.

length (int) : series int Look-back length ≥ 2.

biased (bool) : series bool true → population; false → sample.

Returns: series float √(σ²tot).

wLRTotStdErr(mu, sigma, weight, midLine, slope, length, biased)

Weighted Linear-Regression Total Standard Error.

SE = √( σ²_tot / N_eff ) with N_eff = Σw² / Σw² (like in wster()).

Parameters:

mu (float) : series float Per-bar mean m_i.

sigma (float) : series float Pre-estimated σ_i of each bar.

weight (float) : series float Weight series w_i (≥ 0).

midLine (float) : series float Regression value at the latest bar (ŷₙ₋₁).

slope (float) : series float Slope b₁ of the regression line.

length (int) : series int Look-back length ≥ 2.

biased (bool) : series bool true → population; false → sample.

Returns: series float √((σ²res, σ²wtn, σ²trd) / N_eff).

wLRLocTotStdDev(mu, sigma, weight, midLine, slope, length, biased)

Weighted Linear-Regression Local Total Standard Deviation.

Measures the total "noise" (within-bar + residual) around the trend.

Parameters:

mu (float) : series float Per-bar mean m_i.

sigma (float) : series float Pre-estimated σ_i of each bar.

weight (float) : series float Weight series w_i (≥ 0).

midLine (float) : series float Regression value at the latest bar (ŷₙ₋₁).

slope (float) : series float Slope b₁ of the regression line.

length (int) : series int Look-back length ≥ 2.

biased (bool) : series bool true → population; false → sample.

Returns: series float √(σ²wtn + σ²res).

wLRLocTotStdErr(mu, sigma, weight, midLine, slope, length, biased)

Weighted Linear-Regression Local Total Standard Error.

Parameters:

mu (float) : series float Per-bar mean m_i.

sigma (float) : series float Pre-estimated σ_i of each bar.

weight (float) : series float Weight series w_i (≥ 0).

midLine (float) : series float Regression value at the latest bar (ŷₙ₋₁).

slope (float) : series float Slope b₁ of the regression line.

length (int) : series int Look-back length ≥ 2.

biased (bool) : series bool true → population; false → sample.

Returns: series float √((σ²wtn + σ²res) / N_eff).

wLSma(source, weight, length)

Weighted Least Square Moving Average.

Parameters:

source (float) : series float Data series.

weight (float) : series float Weight series.

length (int) : series int Look-back length ≥ 2.

Returns: series float Least square weighted mean. Falls back

to unweighted regression if Σw = 0.

Z-Score Momentum | MisinkoMasterThe Z-Score Momentum is a new trend analysis indicator designed to catch reversals, and shifts in trends by comparing the "positive" and "negative" momentum by using the Z-Score.

This approach helps traders and investors get unique insight into the market of not just Crypto, but any market.

A deeper dive into the indicator

First, I want to cover the "Why?", as I believe it will ease of the part of the calculation to make it easier to understand, as by then you will understand how it fits the puzzle.

I had an attempt to create a momentum oscillator that would catch reversals and provide high tier accuracy while maintaining the main part => the speed.

I thought back to many concepts, divergences between averages?

- Did not work

Maybe a MACD rework?

- Did not work with what I tried :(

So I thought about statistics, Standard Deviation, Z-Score, Sharpe/Sortino/Omega ratio...

Wait, was that the Z-Score? I only tried the For Loop version of it :O

So on my way back from school I formulated a concept (originaly not like this but to that later) that would attempt to use the Z-Score as an accurate momentum oscillator.

Many ideas were falling out of the blue, but not many worked.

After almost giving up on this, and going to go back to developing my strategies, I tried one last thing:

What if we use divergences in the average, formulated like a Z-score?

Surprise-surprise, it worked!

Now to explain what I have been so passionately yapping about, and to connect the pieces of the puzzle once and for all:

The indicator compares the "strength" of the bullish/bearish factors (could be said differently, but this is my "speach bubble", and I think this describes it the best)

What could we use for the "bullish/bearish" factors?

How about high & low?

I mean, these are by definitions the highest and lowest points in price, which I decided to interpret as: The highest the bull & bear "factors" achieved that bar.

The problem here is comparison, I mean high will ALWAYS > low, unless the asset decided to unplug itself and stop moving, but otherwise that would be unfair.

Now if I use my Z-score, it will get higher while low is going up, which is the opposite of what I want, the bearish "factor" is weaker while we go up!

So I sat on my ret*rded a*s for 25 minutes, completly ignoring the fact the number "-1" exists.

Surprise surprise, multiplying the Z-Score of the low by -1 did what I wanted!

Now it reversed itself (magically). Now while the low keeps going down, the bear factor increases, and while it goes up the bear factor lowers.

This was btw still too noisy, so instead of the classic formula:

a = current value

b = average value

c = standard deviation of a

Z = (a-b)/c

I used:

a = average value over n/2 period

b = average value over n period

c = standard deviation of a

Z = (a-b)/c

And then compared the Z-Score of High to the Z-Score of Low by basic subtraction, which gives us final result and shows us the strength of trend, the direction of the trend, and possibly more, which I may have not found.

As always, this script is open source, so make sure to play around with it, you may uncover the treasure that I did not :)

Enjoy Gs!

Trade-o-Scope: Plot Custom Data v2Meet — a major tool upgrade for plotting your own data on TradingView charts. Simple and intuitive input format, large volume limits, and robust plotting for your own datasets — forecasts, backtests, or external data and model outputs.

You can apply/overlay other indicators from the TradingView catalog (such as Bollinger Bands, RSI, etc.) on top of custom data charts. The indicator you want to overlay must support selecting an input data source — i.e., have a dropdown where you can choose as the source.

🧩 How to use

Simply select and copy two columns — with dates and values — from your spreadsheet (Excel, Google Sheets, etc.) and paste them into the indicator’s input field. The indicator will automatically process the input and plot your data on the chart.

Example data:

Date XYZ_value

2025-10-08 84.57

2025-10-01 80.66

2025-09-24 86.24

2025-09-17 84.76

📅 Supported date format

The indicator recognizes standard international date formats commonly used in spreadsheets and data exports.

• ISO 8601 — "YYYY-MM-DD" or "YYYY-MM-DDThh:mm:ss"

2025-10-13

2025-10-13 14:30

2025-10-13 14:30:00

2025-10-13T14:30

2025-10-13T14:30:00

• RFC 2822 — "DD MMM YYYY" or "DD MMM YYYY hh:mm:ss"

13 Oct 2025

13 Oct 2025 14:30

13 Oct 2025 14:30:00

The time part is optional — if omitted, midnight (00:00:00) is assumed.

By default, all date–time values are interpreted in the exchange timezone of the chart’s symbol, but you can select a different data timezone in the indicator settings if needed.

💡 Supported value format

Integers (e.g., 12345, -12345)

Decimals (e.g., 1234.56, -1234.56)

The decimal separator must be a dot (.)

Thousands separators are not supported

⚙️ Advanced Features

Value Multiplier — scale your values by a chosen factor.

Formatting Options — display values as price, percentage, or volume.

Conditional Coloring — automatically change plot color based on thresholds.

Plot Style Selection — choose from line, histogram, area, or column plots.

Additional Visual References — enable fixed horizontal lines for better visual interpretation.

📝 General Notes

Maximum input size: 40,960 characters (~1,500–3,000 rows depending on format). If an error occurs after pasting data, simply remove a few rows until it disappears.

First Passage Time - Distribution AnalysisThe First Passage Time (FPT) Distribution Analysis indicator is a sophisticated probabilistic tool that answers one of the most critical questions in trading: "How long will it take for price to reach my target, and what are the odds of getting there first?"

Unlike traditional technical indicators that focus on what might happen, this indicator tells you when it's likely to happen.

Mathematical Foundation: First Passage Time Theory

What is First Passage Time?

First Passage Time (FPT) is a concept in stochastic processes that measures the time it takes for a random process to reach a specific threshold for the first time. Originally developed in physics and mathematics, FPT has applications in:

Quantitative Finance: Option pricing, risk management, and algorithmic trading

Neuroscience: Modeling neural firing patterns

Biology: Population dynamics and disease spread

Engineering: Reliability analysis and failure prediction

The Mathematics Behind It

This indicator uses Geometric Brownian Motion (GBM), the same stochastic model used in the Black-Scholes option pricing formula:

dS = μS dt + σS dW

Where:

S = Asset price

μ = Drift (trend component)

σ = Volatility (uncertainty component)

dW = Wiener process (random walk)

Through Monte Carlo simulation, the indicator runs 1,000+ price path simulations to statistically determine:

When each threshold (+X% or -X%) is likely to be hit

Which threshold is hit first (directional bias)

How often each scenario occurs (probability distribution)

🎯 How This Indicator Works

Core Algorithm Workflow:

Calculate Historical Statistics

Measures recent price volatility (standard deviation of log returns)

Calculates drift (average directional movement)

Annualizes these metrics for meaningful comparison

Run Monte Carlo Simulations

Generates 1,000+ random price paths based on historical behavior

Tracks when each path hits the upside (+X%) or downside (-X%) threshold

Records which threshold was hit first in each simulation

Aggregate Statistical Results

Calculates percentile distributions (10th, 25th, 50th, 75th, 90th)

Computes "first hit" probabilities (upside vs downside)

Determines average and median time-to-target

Visual Representation

Displays thresholds as horizontal lines

Shows gradient risk zones (purple-to-blue)

Provides comprehensive statistics table

📈 Use Cases

1. Options Trading

Selling Options: Determine if your strike price is likely to be hit before expiration

Buying Options: Estimate probability of reaching profit targets within your time window

Time Decay Management: Compare expected time-to-target vs theta decay

Example: You're considering selling a 30-day call option 5% out of the money. The indicator shows there's a 72% chance price hits +5% within 12 days. This tells you the trade has high assignment risk.

2. Swing Trading

Entry Timing: Wait for higher probability setups when directional bias is strong

Target Setting: Use median time-to-target to set realistic profit expectations

Stop Loss Placement: Understand probability of hitting your stop before target

Example: The indicator shows 85% upside probability with median time of 3.2 days. You can confidently enter long positions with appropriate position sizing.

3. Risk Management

Position Sizing: Larger positions when probability heavily favors one direction

Portfolio Allocation: Reduce exposure when probabilities are near 50/50 (high uncertainty)

Hedge Timing: Know when to add protective positions based on downside probability

Example: Indicator shows 55% upside vs 45% downside—nearly neutral. This signals high uncertainty, suggesting reduced position size or wait for better setup.

4. Market Regime Detection

Trending Markets: High directional bias (70%+ one direction)

Range-bound Markets: Balanced probabilities (45-55% both directions)

Volatility Regimes: Compare actual vs theoretical minimum time

Example: Consistent 90%+ bullish bias across multiple timeframes confirms strong uptrend—stay long and avoid counter-trend trades.

First Hit Rate (Most Important!)

Shows which threshold is likely to be hit FIRST:

Upside %: Probability of hitting upside target before downside

Downside %: Probability of hitting downside target before upside

These always sum to 100%

⚠️ Warning: If you see "Low Hit Rate" warning, increase this parameter!

Advanced Parameters

Drift Mode

Allows you to explore different scenarios:

Historical: Uses actual recent trend (default—most realistic)

Zero (Neutral): Assumes no trend, only volatility (symmetric probabilities)

50% Reduced: Dampens trend effect (conservative scenario)

Use Case: Switch to "Zero (Neutral)" to see what happens in a pure volatility environment, useful for range-bound markets.

Distribution Type

Percentile: Shows 10%, 25%, 50%, 75%, 90% levels (recommended for most users)

Sigma: Shows standard deviation levels (1σ, 2σ)—useful for statistical analysis

⚠️ Important Limitations & Best Practices

Limitations

Assumes GBM: Real markets have fat tails, jumps, and regime changes not captured by GBM

Historical Parameters: Uses recent volatility/drift—may not predict regime shifts

No Fundamental Events: Cannot predict earnings, news, or macro shocks

Computational: Runs only on last bar—doesn't give historical signals

Remember: Probabilities are not certainties. Use this indicator as part of a comprehensive trading plan with proper risk management.

Created by: Henrique Centieiro. feedback is more than welcome!

PPP – Info Table (Anchor + Corr/Alpha/Beta) v3PPP – Info Table (Anchor + Corr/Alpha/Beta)

- By P3 Analytics, run by Puranam Pradeep Picasso Sharma

🔎 Overview

This indicator creates a clean, dynamic information table on your chart that lets you quickly analyze how your chosen asset is performing relative to BTC, ETH, or any other benchmarks.

With a single glance, you can see:

% change from today’s open (for the anchor asset, BTC, and ETH)

Previous day % change (self + benchmarks)

Correlation, Beta, and Alpha statistics for the selected window (1W, 1M, 1Y)

Anchor values at any bar you choose (via Bars Back or Anchor Time)

Perfect for traders who want to measure coin strength vs benchmarks and make better rotation, risk, or hedging decisions.

📊 Key Metrics

Correlation (Corr): How closely the asset moves with the benchmark.

+1 = moves together, 0 = no relation, -1 = moves opposite.

Beta (β): Sensitivity of returns vs the benchmark.

β = 1 → moves 1:1 with BTC.

β > 1 → more volatile (amplifies BTC moves).

β < 1 → less volatile (defensive).

Alpha (α): Excess return beyond what Beta predicts.

Positive α = outperforming benchmark-adjusted expectation.

Negative α = underperforming.

⚙️ Features

Flexible Anchor Mode:

Bars Back → quickly step through bars.

Time → pin analysis to a specific historical candle.

Customizable Benchmarks: Default BTC & ETH (futures), but replaceable with any ticker.

Adjustable Stats Window:

1 Week, 1 Month, 1 Year (auto-scales if using chart timeframe).

Compact Mode for a smaller table layout.

Dark/Light Theme, font size, corner placement, transparency, and decimal control.

Runs efficiently with minimal chart clutter.

🧑💻 About P3 Analytics

This indicator is developed under P3 Analytics, a research & trading technology initiative led by Puranam Pradeep Picasso Sharma.

P3 Analytics builds tools that merge machine learning, statistics, and trading strategy into accessible products for traders across crypto, equities, forex, and commodities.

✅ How to Use

Add indicator to your chart.

In settings:

Pick your benchmarks (default = BTCUSDT.P, ETHUSDT.P).

Choose your anchor (Bars Back or Time).

Set window length for correlation/alpha/beta.

Read the table:

Left side = your asset.

Right side = benchmarks.

Colors: Green = positive % change, Red = negative.

🚀 Why Use This?

Quickly compare your asset vs BTC/ETH without juggling multiple charts.

Spot whether a coin is truly leading or just following BTC.

Identify outperformance (alpha) coins for rotation or trend plays.

Manage risk by knowing which assets are high beta (high leverage-like moves).

✦ Indicator by P3 Analytics

✦ Created & published by Puranam Pradeep Picasso Sharma

Extended CANSLIM Indicator❖ Extended CANSLIM Indicator.

The Extended CANSLIM indicator is an indicator that concentrates all the tools usually used by CANSLIM traders.

It shows a table where all the stock fundamental information is shown at once first for the last quarter and then up to 5 years back.

The fundamental data is checked against well known CANSLIM validation criteria and is shown over 4 state levels.

1. Good = Value is CANSLIM Compliant.

2. Acceptable = Value is not CANSLIM compliant but still good. value is shown with a lighter background color.

3. Warning = Value deserves special attention. Value is shown over orange background color.

3. Stop = Value is non CANSLIM compliant or indicates a stop trading condition. Value is shown over red background color.

The indicator has also a set of technical tools calculated on price or index and shown directly on the chart.

❖ Fundamental data shown in the table.

The table is arranged in 4 sets of data:

1. Table Header, showing Indicator and Company data.

2. CANSLIM.

3. 3Rs: RS Rating, Revenue and ROE.

4. Extra Data: Piotroski score, ATR, Trend Days, D to E, Avg Vol and Vol today.

Sets 3 and 4 can be hidden from the table.

❖ Indicator and Compay Data.

The table header shows, Indicator name and version.

It then displays Company Name, sector and industry, human size and its capitalization.

❖ CANSLIM Data.

Displays either genuine CANSLIM data from TradinView or custom data as best effort when that data cannot be obtained in TV.

C = EPS diluted growth, Quarterly YoY.

>= 25% = Good, >= 0% = Acceptable, < 0% = Stop

A = EPS diluted growth, Annual YoY.

>= 25% = Good, >= 0% = Acceptable, < 0% = Stop

N = New High as best effort (Cust).

Always Good

S = Float shares as best effort.

Always Good

L = One year performance relative to S&P 500 (Cust),

Positive : 0% .. 50% = Neutral, 50%+ = Leader, 80%+ = Leader+, 100%+ = Leader++

Negative : 0% .. -10% = Laggard, -10% .. -30% = Laggard+, -30%+ = Laggard++

>= 50% = Good, >= 0% = Acceptable, >= -10% Warning, < -10% = Stop

I = Accumulation/Distribution days over last 25 days as a clue for institutional support (Cust).

A delta is calculated by subtracting Distribution to Accumulation days.

> 0 = Good, = 0 = Acceptable, < 0 = Warning, < -5 = Stop

M = Market direction and exposure measured on S&500 closing between averages (Cust).

Varies from 0% Full Bear to 100% Full Bull

>= 80% = Good, >= 60% = Acceptable, >= 40% = Warning, < 40% = Stop

❖ Extra non CANSLIM Data.

RS = RS Rating.

>= 90 = Good, >= 80 = Accept, >= 50 = Warning, < 50 = Stop

Rev. = Revenue Growth Quarterly YoY.

>= 0% = Good, <0% = Stop

ROE = Return on Equity, Quarterly YoY.

>= 17% = Good, >= 0% = Acceptable, < 0% = Stop

Piotr. = Piotroski Score, www.investopedia.com (TV)

>= 7 = Good, >= 4 = Acceptable, < 4 = Stop

ATR = Average True Range over the last 20 days (Cust).

0% - 2% = Acceptable, 2% - 4% = Ideal, 4% - 6% = Warning, 5%+ = Stop.

Trend Days = Days since EMA150 is over EMA200 (Cust).

Always Good

D. to E. = Days left before Earnings. Maybe not a good idea buying just before earnings (Cust).

>= 28 = Good, >= 21 = Acceptable, >= 14 = Warning, < 14 = Stop

Avg Vol. = 50d Average Volume (Cust).

>= 100K = Good, < 100K = Acceptable

Vol. Today = Today's percentage volume compared to 50d average (Cust).

Always Good.

❖ Historical Data.

Optionally selectable historical data can be displayed for C, A, Revenue and ROE up to 20 quarters if available.

Quarterly numbers can also be displayed for A, C and Revenue.

Information can be shown in Chronological or Reverse Chronological order (default).

Increasing growth quarters are shown in white, while diminuing ones are shown in Yellow.

Transition from Losing to Profitable quarters are shown with an exclamation mark ‘!’

Finally, losing quarters are shown between parenthesis.

❖ MAs on chart.

Displays 200, 100, 50 and 20 days MAs on chart.

The MAs are also automatically scaled in the 1W time frame.

❖ New 52 Week High on chart.

A sun is shown on the chart the first time that a new 52 week high is reached.

The N cell shows a filled sun when a 52 week high is no older than a month, an lighter sun when it’s no older than a quarter or a moon otherwise.

❖ Pocket Pivots on chart.

Small triangles below the price are signaling pocket pivots.

❖ Bases on chart, formerly Darvas Boxes.

Draw bases as defined by Darvas boxes, both top or bottom of bases can be selected to be shown in order to only show resistance or support.

❖ Market exposure/direction indicator.

When charting S&P500 (SPX), Nasdaq 100 Index (NDX), Nasdaq composite (IXIC) or Dow Jownes Index (DJIA), the indicator switches to Market Exposure indicator, showing also Accumulation/Distribution days when volume information is available. This indication which varies from 0% to 100% is what is shown under the M letter in the CANSLIM table which is calculated on the S&P500.