SILLibrary "SIL"

mean_src(x, y)

calculates moving average : x is the source of price (OHLC) & y = the lookback period

Parameters:

x

y

stan_dev(x, y, z)

calculates standard deviation, x = source of price (OHLC), y = the average lookback, z = average given prior two float and intger inputs, call the f_avg_src() function in f_stan_dev()

Parameters:

x

y

z

vawma(x, y)

calculates volume weighted moving average, x = source of price (OHLC), y = loookback period

Parameters:

x

y

gethurst(x, y, z)

calculates the Hurst Exponent and Hurst Exponent average, x = source of price (OHLC), y = lookback period for Hurst Exponent Calculation, z = lookback period for average Hurst Exponent

Parameters:

x

y

z

Techindicator

OfekIndicatorsLibLibrary "OfekIndicatorsLib"

TODO: add library description here

ichiClouds(conversionPeriods, basePeriods, laggingSpan2Periods)

Parameters:

conversionPeriods

basePeriods

laggingSpan2Periods

trama(tramaSrc, tramaLength)

Parameters:

tramaSrc

tramaLength

kdj(ilong, isig, startFrom)

Parameters:

ilong

isig

startFrom(look into history)

ulibLibrary "ulib"

Stochastic(length, d_smooth)

Parameters:

length

d_smooth

bull_stoch_condition(k, d)

Parameters:

k

d

ema_condition(ema_1, ema_2, ema_3)

Parameters:

ema_1

ema_2

ema_3

bull_fractal_condition(n)

Parameters:

n

Bull(Fractal, ema, stochastic_osc)

Parameters:

Fractal

ema

stochastic_osc

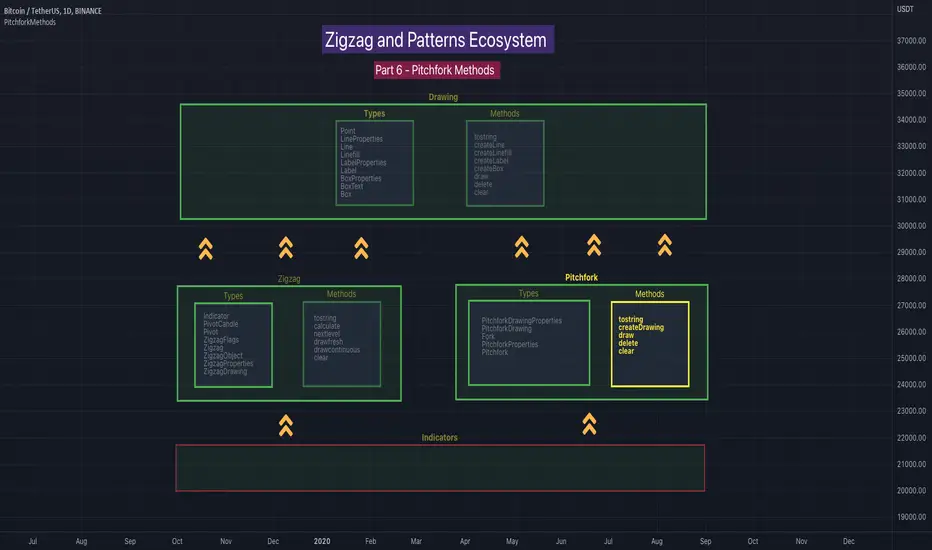

PitchforkMethodsLibrary "PitchforkMethods"

Methods associated with Pitchfork and Pitchfork Drawing. Depends on the library PitchforkTypes for Pitchfork/PitchforkDrawing objects which in turn use DrawingTypes for basic objects Point/Line/LineProperties. Also depends on DrawingMethods for related methods

tostring(this)

Converts PitchforkTypes/Fork object to string representation

Parameters:

this : PitchforkTypes/Fork object

Returns: string representation of PitchforkTypes/Fork

tostring(this)

Converts Array of PitchforkTypes/Fork object to string representation

Parameters:

this : Array of PitchforkTypes/Fork object

Returns: string representation of PitchforkTypes/Fork array

tostring(this, sortKeys, sortOrder)

Converts PitchforkTypes/PitchforkProperties object to string representation

Parameters:

this : PitchforkTypes/PitchforkProperties object

sortKeys : If set to true, string output is sorted by keys.

sortOrder : Applicable only if sortKeys is set to true. Positive number will sort them in ascending order whreas negative numer will sort them in descending order. Passing 0 will not sort the keys

Returns: string representation of PitchforkTypes/PitchforkProperties

tostring(this, sortKeys, sortOrder)

Converts PitchforkTypes/PitchforkDrawingProperties object to string representation

Parameters:

this : PitchforkTypes/PitchforkDrawingProperties object

sortKeys : If set to true, string output is sorted by keys.

sortOrder : Applicable only if sortKeys is set to true. Positive number will sort them in ascending order whreas negative numer will sort them in descending order. Passing 0 will not sort the keys

Returns: string representation of PitchforkTypes/PitchforkDrawingProperties

tostring(this, sortKeys, sortOrder)

Converts PitchforkTypes/Pitchfork object to string representation

Parameters:

this : PitchforkTypes/Pitchfork object

sortKeys : If set to true, string output is sorted by keys.

sortOrder : Applicable only if sortKeys is set to true. Positive number will sort them in ascending order whreas negative numer will sort them in descending order. Passing 0 will not sort the keys

Returns: string representation of PitchforkTypes/Pitchfork

createDrawing(this)

Creates PitchforkTypes/PitchforkDrawing from PitchforkTypes/Pitchfork object

Parameters:

this : PitchforkTypes/Pitchfork object

Returns: PitchforkTypes/PitchforkDrawing object created

createDrawing(this)

Creates PitchforkTypes/PitchforkDrawing array from PitchforkTypes/Pitchfork array of objects

Parameters:

this : array of PitchforkTypes/Pitchfork object

Returns: array of PitchforkTypes/PitchforkDrawing object created

draw(this)

draws from PitchforkTypes/PitchforkDrawing object

Parameters:

this : PitchforkTypes/PitchforkDrawing object

Returns: PitchforkTypes/PitchforkDrawing object drawn

delete(this)

deletes PitchforkTypes/PitchforkDrawing object

Parameters:

this : PitchforkTypes/PitchforkDrawing object

Returns: PitchforkTypes/PitchforkDrawing object deleted

delete(this)

deletes underlying drawing of PitchforkTypes/Pitchfork object

Parameters:

this : PitchforkTypes/Pitchfork object

Returns: PitchforkTypes/Pitchfork object deleted

delete(this)

deletes array of PitchforkTypes/PitchforkDrawing objects

Parameters:

this : Array of PitchforkTypes/PitchforkDrawing object

Returns: Array of PitchforkTypes/PitchforkDrawing object deleted

delete(this)

deletes underlying drawing in array of PitchforkTypes/Pitchfork objects

Parameters:

this : Array of PitchforkTypes/Pitchfork object

Returns: Array of PitchforkTypes/Pitchfork object deleted

clear(this)

deletes array of PitchforkTypes/PitchforkDrawing objects and clears the array

Parameters:

this : Array of PitchforkTypes/PitchforkDrawing object

Returns: void

clear(this)

deletes array of PitchforkTypes/Pitchfork objects and clears the array

Parameters:

this : Array of Pitchfork/Pitchfork object

Returns: void

PitchforkTypesLibrary "PitchforkTypes"

User Defined Types to be used for Pitchfork and Drawing elements of Pitchfork. Depends on DrawingTypes for Point, Line, and LineProperties objects

PitchforkDrawingProperties

Pitchfork Drawing Properties object

Fields:

extend : If set to true, forks are extended towards right. Default is true

fill : Fill forklines with transparent color. Default is true

fillTransparency : Transparency at which fills are made. Only considered when fill is set. Default is 80

forceCommonColor : Force use of common color for forks and fills. Default is false

commonColor : common fill color. Used only if ratio specific fill colors are not available or if forceCommonColor is set to true.

PitchforkDrawing

Pitchfork drawing components

Fields:

medianLine : Median line of the pitchfork

baseLine : Base line of the pitchfork

forkLines : fork lines of the pitchfork

linefills : Linefills between forks

Fork

Fork object property

Fields:

ratio : Fork ratio

forkColor : color of fork. Default is blue

include : flag to include the fork in drawing. Default is true

PitchforkProperties

Pitchfork Properties

Fields:

forks : Array of Fork objects

type : Pitchfork type. Supported values are "regular", "schiff", "mschiff", Default is regular

inside : Flag to identify if to draw inside fork. If set to true, inside fork will be drawn

Pitchfork

Pitchfork object

Fields:

a : Pivot Point A of pitchfork

b : Pivot Point B of pitchfork

c : Pivot Point C of pitchfork

properties : PitchforkProperties object which determines type and composition of pitchfork

dProperties : Drawing properties for pitchfork

lProperties : Common line properties for Pitchfork lines

drawing : PitchforkDrawing object

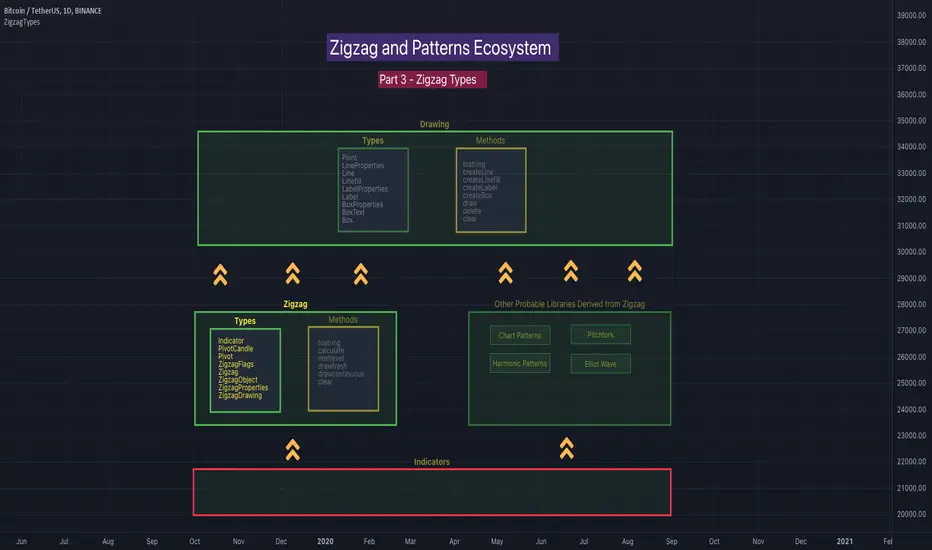

ZigzagMethodsLibrary "ZigzagMethods"

Object oriented implementation of Zigzag methods. Please refer to ZigzagTypes library for User defined types used in this library

tostring(this, sortKeys, sortOrder, includeKeys)

Converts ZigzagTypes/Pivot object to string representation

Parameters:

this : ZigzagTypes/Pivot

sortKeys : If set to true, string output is sorted by keys.

sortOrder : Applicable only if sortKeys is set to true. Positive number will sort them in ascending order whreas negative numer will sort them in descending order. Passing 0 will not sort the keys

includeKeys : Array of string containing selective keys. Optional parmaeter. If not provided, all the keys are considered

Returns: string representation of ZigzagTypes/Pivot

tostring(this, sortKeys, sortOrder, includeKeys)

Converts Array of Pivot objects to string representation

Parameters:

this : Pivot object array

sortKeys : If set to true, string output is sorted by keys.

sortOrder : Applicable only if sortKeys is set to true. Positive number will sort them in ascending order whreas negative numer will sort them in descending order. Passing 0 will not sort the keys

includeKeys : Array of string containing selective keys. Optional parmaeter. If not provided, all the keys are considered

Returns: string representation of Pivot object array

tostring(this)

Converts ZigzagFlags object to string representation

Parameters:

this : ZigzagFlags object

Returns: string representation of ZigzagFlags

tostring(this, sortKeys, sortOrder, includeKeys)

Converts ZigzagTypes/Zigzag object to string representation

Parameters:

this : ZigzagTypes/Zigzagobject

sortKeys : If set to true, string output is sorted by keys.

sortOrder : Applicable only if sortKeys is set to true. Positive number will sort them in ascending order whreas negative numer will sort them in descending order. Passing 0 will not sort the keys

includeKeys : Array of string containing selective keys. Optional parmaeter. If not provided, all the keys are considered

Returns: string representation of ZigzagTypes/Zigzag

calculate(this, ohlc, indicators, indicatorNames)

Calculate zigzag based on input values and indicator values

Parameters:

this : Zigzag object

ohlc : Array containing OHLC values. Can also have custom values for which zigzag to be calculated

indicators : Array of indicator values

indicatorNames : Array of indicator names for which values are present. Size of indicators array should be equal to that of indicatorNames

Returns: current Zigzag object

calculate(this)

Calculate zigzag based on properties embedded within Zigzag object

Parameters:

this : Zigzag object

Returns: current Zigzag object

nextlevel(this)

Calculate Next Level Zigzag based on the current calculated zigzag object

Parameters:

this : Zigzag object

Returns: Next Level Zigzag object

clear(this)

Clears zigzag drawings array

Parameters:

this : array

Returns: void

drawfresh(this)

draws fresh zigzag based on properties embedded in ZigzagDrawing object

Parameters:

this : ZigzagDrawing object

Returns: ZigzagDrawing object

drawcontinuous(this)

draws zigzag based on the zigzagmatrix input

Parameters:

this : ZigzagDrawing object

Returns:

ZigzagTypesLibrary "ZigzagTypes"

Zigzag related user defined types. Depends on DrawingTypes library for basic types

Indicator

Indicator is collection of indicator values applied on high, low and close

Fields:

indicatorHigh : Indicator Value applied on High

indicatorLow : Indicator Value applied on Low

PivotCandle

PivotCandle represents data of the candle which forms either pivot High or pivot low or both

Fields:

_high : High price of candle forming the pivot

_low : Low price of candle forming the pivot

length : Pivot length

pHighBar : represents number of bar back the pivot High occurred.

pLowBar : represents number of bar back the pivot Low occurred.

pHigh : Pivot High Price

pLow : Pivot Low Price

indicators : Array of Indicators - allows to add multiple

Pivot

Pivot refers to zigzag pivot. Each pivot can contain various data

Fields:

point : pivot point coordinates

dir : direction of the pivot. Valid values are 1, -1, 2, -2

level : is used for multi level zigzags. For single level, it will always be 0

ratio : Price Ratio based on previous two pivots

indicatorNames : Names of the indicators applied on zigzag

indicatorValues : Values of the indicators applied on zigzag

indicatorRatios : Ratios of the indicators applied on zigzag based on previous 2 pivots

ZigzagFlags

Flags required for drawing zigzag. Only used internally in zigzag calculation. Should not set the values explicitly

Fields:

newPivot : true if the calculation resulted in new pivot

doublePivot : true if the calculation resulted in two pivots on same bar

updateLastPivot : true if new pivot calculated replaces the old one.

Zigzag

Zigzag object which contains whole zigzag calculation parameters and pivots

Fields:

length : Zigzag length. Default value is 5

numberOfPivots : max number of pivots to hold in the calculation. Default value is 20

offset : Bar offset to be considered for calculation of zigzag. Default is 0 - which means calculation is done based on the latest bar.

level : Zigzag calculation level - used in multi level recursive zigzags

zigzagPivots : array which holds the last n pivots calculated.

flags : ZigzagFlags object which is required for continuous drawing of zigzag lines.

ZigzagObject

Zigzag Drawing Object

Fields:

zigzagLine : Line joining two pivots

zigzagLabel : Label which can be used for drawing the values, ratios, directions etc.

ZigzagProperties

Object which holds properties of zigzag drawing. To be used along with ZigzagDrawing

Fields:

lineColor : Zigzag line color. Default is color.blue

lineWidth : Zigzag line width. Default is 1

lineStyle : Zigzag line style. Default is line.style_solid.

showLabel : If set, the drawing will show labels on each pivot. Default is false

textColor : Text color of the labels. Only applicable if showLabel is set to true.

maxObjects : Max number of zigzag lines to display. Default is 300

xloc : Time/Bar reference to be used for zigzag drawing. Default is Time - xloc.bar_time.

ZigzagDrawing

Object which holds complete zigzag drawing objects and properties.

Fields:

properties : ZigzagProperties object which is used for setting the display styles of zigzag

drawings : array which contains lines and labels of zigzag drawing.

zigzag : Zigzag object which holds the calculations.

DrawingMethodsLibrary "DrawingMethods"

tostring(this, sortKeys, sortOrder, includeKeys)

Converts DrawingTypes/Point object to string representation

Parameters:

this : DrawingTypes/Point object

sortKeys : If set to true, string output is sorted by keys.

sortOrder : Applicable only if sortKeys is set to true. Positive number will sort them in ascending order whreas negative numer will sort them in descending order. Passing 0 will not sort the keys

includeKeys : Array of string containing selective keys. Optional parmaeter. If not provided, all the keys are considered

Returns: string representation of DrawingTypes/Point

tostring(this, sortKeys, sortOrder, includeKeys)

Converts DrawingTypes/LineProperties object to string representation

Parameters:

this : DrawingTypes/LineProperties object

sortKeys : If set to true, string output is sorted by keys.

sortOrder : Applicable only if sortKeys is set to true. Positive number will sort them in ascending order whreas negative numer will sort them in descending order. Passing 0 will not sort the keys

includeKeys : Array of string containing selective keys. Optional parmaeter. If not provided, all the keys are considered

Returns: string representation of DrawingTypes/LineProperties

tostring(this, sortKeys, sortOrder, includeKeys)

Converts DrawingTypes/Line object to string representation

Parameters:

this : DrawingTypes/Line object

sortKeys : If set to true, string output is sorted by keys.

sortOrder : Applicable only if sortKeys is set to true. Positive number will sort them in ascending order whreas negative numer will sort them in descending order. Passing 0 will not sort the keys

includeKeys : Array of string containing selective keys. Optional parmaeter. If not provided, all the keys are considered

Returns: string representation of DrawingTypes/Line

tostring(this, sortKeys, sortOrder, includeKeys)

Converts DrawingTypes/LabelProperties object to string representation

Parameters:

this : DrawingTypes/LabelProperties object

sortKeys : If set to true, string output is sorted by keys.

sortOrder : Applicable only if sortKeys is set to true. Positive number will sort them in ascending order whreas negative numer will sort them in descending order. Passing 0 will not sort the keys

includeKeys : Array of string containing selective keys. Optional parmaeter. If not provided, all the keys are considered

Returns: string representation of DrawingTypes/LabelProperties

tostring(this, sortKeys, sortOrder, includeKeys)

Converts DrawingTypes/Label object to string representation

Parameters:

this : DrawingTypes/Label object

sortKeys : If set to true, string output is sorted by keys.

sortOrder : Applicable only if sortKeys is set to true. Positive number will sort them in ascending order whreas negative numer will sort them in descending order. Passing 0 will not sort the keys

includeKeys : Array of string containing selective keys. Optional parmaeter. If not provided, all the keys are considered

Returns: string representation of DrawingTypes/Label

tostring(this, sortKeys, sortOrder, includeKeys)

Converts DrawingTypes/Linefill object to string representation

Parameters:

this : DrawingTypes/Linefill object

sortKeys : If set to true, string output is sorted by keys.

sortOrder : Applicable only if sortKeys is set to true. Positive number will sort them in ascending order whreas negative numer will sort them in descending order. Passing 0 will not sort the keys

includeKeys : Array of string containing selective keys. Optional parmaeter. If not provided, all the keys are considered

Returns: string representation of DrawingTypes/Linefill

tostring(this, sortKeys, sortOrder, includeKeys)

Converts DrawingTypes/BoxProperties object to string representation

Parameters:

this : DrawingTypes/BoxProperties object

sortKeys : If set to true, string output is sorted by keys.

sortOrder : Applicable only if sortKeys is set to true. Positive number will sort them in ascending order whreas negative numer will sort them in descending order. Passing 0 will not sort the keys

includeKeys : Array of string containing selective keys. Optional parmaeter. If not provided, all the keys are considered

Returns: string representation of DrawingTypes/BoxProperties

tostring(this, sortKeys, sortOrder, includeKeys)

Converts DrawingTypes/BoxText object to string representation

Parameters:

this : DrawingTypes/BoxText object

sortKeys : If set to true, string output is sorted by keys.

sortOrder : Applicable only if sortKeys is set to true. Positive number will sort them in ascending order whreas negative numer will sort them in descending order. Passing 0 will not sort the keys

includeKeys : Array of string containing selective keys. Optional parmaeter. If not provided, all the keys are considered

Returns: string representation of DrawingTypes/BoxText

tostring(this, sortKeys, sortOrder, includeKeys)

Converts DrawingTypes/Box object to string representation

Parameters:

this : DrawingTypes/Box object

sortKeys : If set to true, string output is sorted by keys.

sortOrder : Applicable only if sortKeys is set to true. Positive number will sort them in ascending order whreas negative numer will sort them in descending order. Passing 0 will not sort the keys

includeKeys : Array of string containing selective keys. Optional parmaeter. If not provided, all the keys are considered

Returns: string representation of DrawingTypes/Box

delete(this)

Deletes line from DrawingTypes/Line object

Parameters:

this : DrawingTypes/Line object

Returns: Line object deleted

delete(this)

Deletes label from DrawingTypes/Label object

Parameters:

this : DrawingTypes/Label object

Returns: Label object deleted

delete(this)

Deletes Linefill from DrawingTypes/Linefill object

Parameters:

this : DrawingTypes/Linefill object

Returns: Linefill object deleted

delete(this)

Deletes box from DrawingTypes/Box object

Parameters:

this : DrawingTypes/Box object

Returns: DrawingTypes/Box object deleted

delete(this)

Deletes lines from array of DrawingTypes/Line objects

Parameters:

this : Array of DrawingTypes/Line objects

Returns: Array of DrawingTypes/Line objects

delete(this)

Deletes labels from array of DrawingTypes/Label objects

Parameters:

this : Array of DrawingTypes/Label objects

Returns: Array of DrawingTypes/Label objects

delete(this)

Deletes linefill from array of DrawingTypes/Linefill objects

Parameters:

this : Array of DrawingTypes/Linefill objects

Returns: Array of DrawingTypes/Linefill objects

delete(this)

Deletes boxes from array of DrawingTypes/Box objects

Parameters:

this : Array of DrawingTypes/Box objects

Returns: Array of DrawingTypes/Box objects

clear(this)

clear items from array of DrawingTypes/Line while deleting underlying objects

Parameters:

this : array

Returns: void

clear(this)

clear items from array of DrawingTypes/Label while deleting underlying objects

Parameters:

this : array

Returns: void

clear(this)

clear items from array of DrawingTypes/Linefill while deleting underlying objects

Parameters:

this : array

Returns: void

clear(this)

clear items from array of DrawingTypes/Box while deleting underlying objects

Parameters:

this : array

Returns: void

draw(this)

Creates line from DrawingTypes/Line object

Parameters:

this : DrawingTypes/Line object

Returns: line created from DrawingTypes/Line object

draw(this)

Creates lines from array of DrawingTypes/Line objects

Parameters:

this : Array of DrawingTypes/Line objects

Returns: Array of DrawingTypes/Line objects

draw(this)

Creates label from DrawingTypes/Label object

Parameters:

this : DrawingTypes/Label object

Returns: label created from DrawingTypes/Label object

draw(this)

Creates labels from array of DrawingTypes/Label objects

Parameters:

this : Array of DrawingTypes/Label objects

Returns: Array of DrawingTypes/Label objects

draw(this)

Creates linefill object from DrawingTypes/Linefill

Parameters:

this : DrawingTypes/Linefill objects

Returns: linefill object created

draw(this)

Creates linefill objects from array of DrawingTypes/Linefill objects

Parameters:

this : Array of DrawingTypes/Linefill objects

Returns: Array of DrawingTypes/Linefill used for creating linefills

draw(this)

Creates box from DrawingTypes/Box object

Parameters:

this : DrawingTypes/Box object

Returns: box created from DrawingTypes/Box object

draw(this)

Creates labels from array of DrawingTypes/Label objects

Parameters:

this : Array of DrawingTypes/Label objects

Returns: Array of DrawingTypes/Label objects

createLabel(this, lblText, tooltip, properties)

Creates DrawingTypes/Label object from DrawingTypes/Point

Parameters:

this : DrawingTypes/Point object

lblText : Label text

tooltip : Tooltip text. Default is na

properties : DrawingTypes/LabelProperties object. Default is na - meaning default values are used.

Returns: DrawingTypes/Label object

createLine(this, other, properties)

Creates DrawingTypes/Line object from one DrawingTypes/Point to other

Parameters:

this : First DrawingTypes/Point object

other : Second DrawingTypes/Point object

properties : DrawingTypes/LineProperties object. Default set to na - meaning default values are used.

Returns: DrawingTypes/Line object

createLinefill(this, other, fillColor, transparency)

Creates DrawingTypes/Linefill object from DrawingTypes/Line object to other DrawingTypes/Line object

Parameters:

this : First DrawingTypes/Line object

other : Other DrawingTypes/Line object

fillColor : fill color of linefill. Default is color.blue

transparency : fill transparency for linefill. Default is 80

Returns: Array of DrawingTypes/Linefill object

createBox(this, other, properties, textProperties)

Creates DrawingTypes/Box object from one DrawingTypes/Point to other

Parameters:

this : First DrawingTypes/Point object

other : Second DrawingTypes/Point object

properties : DrawingTypes/BoxProperties object. Default set to na - meaning default values are used.

textProperties : DrawingTypes/BoxText object. Default is na - meaning no text will be drawn

Returns: DrawingTypes/Box object

createBox(this, properties, textProperties)

Creates DrawingTypes/Box object from DrawingTypes/Line as diagonal line

Parameters:

this : Diagonal DrawingTypes/PoLineint object

properties : DrawingTypes/BoxProperties object. Default set to na - meaning default values are used.

textProperties : DrawingTypes/BoxText object. Default is na - meaning no text will be drawn

Returns: DrawingTypes/Box object

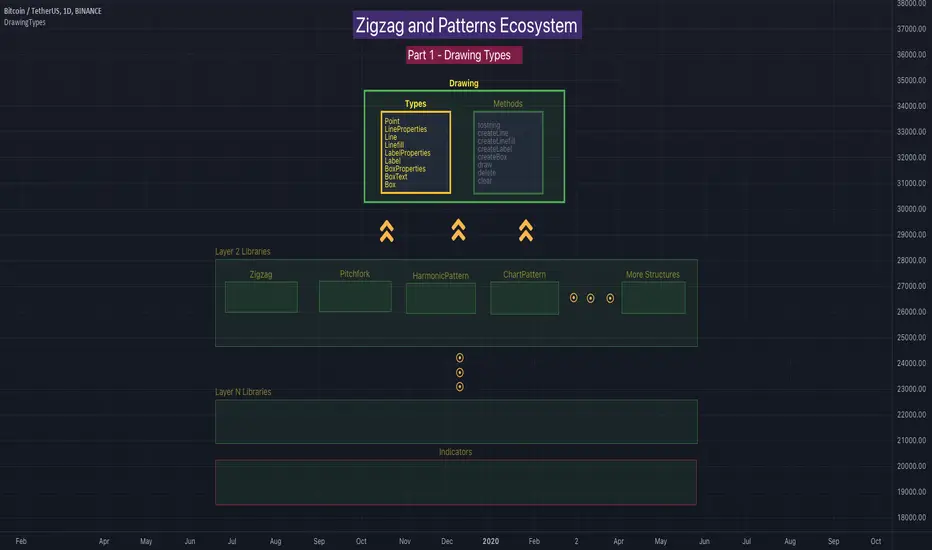

DrawingTypesLibrary "DrawingTypes"

User Defined Types for basic drawing structure. Other types and methods will be built on these.

Point

Point refers to point on chart

Fields:

price : pivot price

bar : pivot bar

bartime : pivot bar time

LineProperties

Properties of line object

Fields:

xloc : X Reference - can be either xloc.bar_index or xloc.bar_time. Default is xloc.bar_index

extend : Property which sets line to extend towards either right or left or both. Valid values are extend.right, extend.left, extend.both, extend.none. Default is extend.none

color : Line color

style : Line style, valid values are line.style_solid, line.style_dashed, line.style_dotted, line.style_arrow_left, line.style_arrow_right, line.style_arrow_both. Default is line.style_solid

width : Line width. Default is 1

Line

Line object created from points

Fields:

start : Starting point of the line

end : Ending point of the line

properties : LineProperties object which defines the style of line

object : Derived line object

LabelProperties

Properties of label object

Fields:

xloc : X Reference - can be either xloc.bar_index or xloc.bar_time. Default is xloc.bar_index

yloc : Y reference - can be yloc.price, yloc.abovebar, yloc.belowbar. Default is yloc.price

color : Label fill color

style : Label style as defined in www.tradingview.com Default is label.style_none

textcolor : text color. Default is color.black

size : Label text size. Default is size.normal. Other values are size.auto, size.tiny, size.small, size.normal, size.large, size.huge

textalign : Label text alignment. Default if text.align_center. Other allowed values - text.align_right, text.align_left, text.align_top, text.align_bottom

text_font_family : The font family of the text. Default value is font.family_default. Other available option is font.family_monospace

Label

Label object

Fields:

point : Point where label is drawn

lblText : label text

tooltip : Tooltip text. Default is na

properties : LabelProperties object

object : Pine label object

Linefill

Linefill object

Fields:

line1 : First line to create linefill

line2 : Second line to create linefill

fillColor : Fill color

transparency : Fill transparency range from 0 to 100

object : linefill object created from wrapper

BoxProperties

BoxProperties object

Fields:

border_color : Box border color. Default is color.blue

bgcolor : box background color

border_width : Box border width. Default is 1

border_style : Box border style. Default is line.style_solid

extend : Extend property of box. default is extend.none

xloc : defines if drawing needs to be done based on bar index or time. default is xloc.bar_index

BoxText

Box Text properties.

Fields:

boxText : Text to be printed on the box

text_size : Text size. Default is size.auto

text_color : Box text color. Default is color.yellow.

text_halign : horizontal align style - default is text.align_center

text_valign : vertical align style - default is text.align_center

text_wrap : text wrap style - default is text.wrap_auto

text_font_family : Text font. Default is

Box

Box object

Fields:

p1 : Diagonal point one

p2 : Diagonal point two

properties : Box properties

textProperties : Box text properties

object : Box object created

Liquidation_linesLibrary "Liquidationline"

f_calculateLeverage(_leverage, _maintainance, _value, _direction)

Parameters:

_leverage

_maintainance

_value

_direction

f_liqline_update(_Liqui_Line, _killonlowhigh)

Parameters:

_Liqui_Line

_killonlowhigh

f_liqline_draw(_Liqui_Line, _priceorliq)

Parameters:

_Liqui_Line

_priceorliq

f_liqline_add(_Liqui_Line, linetoadd, _limit)

Parameters:

_Liqui_Line

linetoadd

_limit

Liquidationline

Fields:

creationtime

stoptime

price

leverage

maintainance

line_active

line_color

line_thickness

line_style

line_direction

line_finished

text_active

text_size

text_color

this library can draw typical liquidation lines, which can be called e.g. by indicator signals

You can see the default implementation in the lower part of the code, starting with RUNTIME

Don't forget to increase max lines to 500 in your script.

It can look like this screenshot here, with only minor changes to your executing script.

The base is the same

AntaresLibrary "Antares"

this library contains some utility functions that I use in my open source scripts including moving average helpers, candlstick helpers, money management, formatters, convertors, webhook integration, analysis, filters and drawing helpers

ma(type, length, source)

Wraps all ma functions

Parameters:

type : Either SMA or EMA or RMA or WMA or VWMA

length : Number of bars (length).

source : Series of values to process.

Returns: Moving average of `source` for `length` bars back by the of MA.

bb(ma, length, mult, source)

Overwrites `ta.bb` duo to limitations of simple int.float mult. Bollinger Bands. A Bollinger Band is a technical analysis tool defined by a set of lines plotted two standard deviations (positively and negatively) away from a simple moving average (SMA) of the security's price, but can be adjusted to user preferences.

Parameters:

ma : Either SMA or EMA or RMA or WMA or VWMA

length : Number of bars (length).

mult : Standard deviation factor.

source : Series of values to process.

Returns: Bollinger Bands.

atr(length, h, l, c)

Overwrites `ta.atr` duo to limitations of simple int length. Function atr (average true range) returns the RMA of true range. True range is max(high - low, abs(high - close ), abs(low - close )).

Parameters:

length : Number of bars (length).

h : High price high price.

l : low price.

c : Close price close price.

Returns: Average true range.

rsi(length, source)

Overwrites `ta.rsi` duo to limitations of simple int length. Relative strength index. It is calculated using the `ta.rma()` of upward and downward changes of `source` over the last `length` bars.

Parameters:

length : Number of bars (length).

source : Series of values to process.

Returns: Relative strength index.

lowest(length, source, start)

Lowest value for a given number of bars back.

Parameters:

length : Number of bars (length).

source : Series of values to process.

start : Series number of bars that should be skipped before process.

Returns: Lowest value in the series.

highest(length, source, start)

Highest value for a given number of bars back.

Parameters:

length : Number of bars (length).

source : Series of values to process.

start : Series number of bars that should be skipped before process.

Returns: Highest value in the series.

atr_multiplier(rsi, atr_max_multiplier)

Dynamic atr multiplier calculated by RSI.

Parameters:

rsi : Relative strength index.

atr_max_multiplier : The maximum multiplier of atr

Returns: Dynamic multiplier of ATR

offset(atr, atr_multiplier)

Safe dynamic offset you need to use in your stoploss, stop buy/sell, etc.

Parameters:

atr : Average true range.

atr_multiplier : ATR multiplier got from `atr_multiplier(rsi, atr_max_multiplier)`

Returns: Dynamic offset

rsi_emotional(rsi, bottom, top)

Tells you if RSI is in emotional zone.

Parameters:

rsi : Relative Strength Index

bottom : The zone that below it market reacts emotionally

top : The zone that above it market reacts emotionally

Returns: false if RSI was between `bottom` and `top` otherwise true

rsi_signal(rsi, bottom, top)

Tells you if RSI is in good point to check your other strategy conditions.

Parameters:

rsi : Relative Strength Index

bottom : The zone that below it market reacts emotionally

top : The zone that above it market reacts emotionally

Returns: 1 if RSI crossed out 30, 50 or 70. -1 if RSI crossed under 70, 50, 30. otherwise is 0

MLExtensionsLibrary "MLExtensions"

normalizeDeriv(src, quadraticMeanLength)

Returns the smoothed hyperbolic tangent of the input series.

Parameters:

src : The input series (i.e., the first-order derivative for price).

quadraticMeanLength : The length of the quadratic mean (RMS).

Returns: nDeriv The normalized derivative of the input series.

normalize(src, min, max)

Rescales a source value with an unbounded range to a target range.

Parameters:

src : The input series

min : The minimum value of the unbounded range

max : The maximum value of the unbounded range

Returns: The normalized series

rescale(src, oldMin, oldMax, newMin, newMax)

Rescales a source value with a bounded range to anther bounded range

Parameters:

src : The input series

oldMin : The minimum value of the range to rescale from

oldMax : The maximum value of the range to rescale from

newMin : The minimum value of the range to rescale to

newMax : The maximum value of the range to rescale to

Returns: The rescaled series

color_green(prediction)

Assigns varying shades of the color green based on the KNN classification

Parameters:

prediction : Value (int|float) of the prediction

Returns: color

color_red(prediction)

Assigns varying shades of the color red based on the KNN classification

Parameters:

prediction : Value of the prediction

Returns: color

tanh(src)

Returns the the hyperbolic tangent of the input series. The sigmoid-like hyperbolic tangent function is used to compress the input to a value between -1 and 1.

Parameters:

src : The input series (i.e., the normalized derivative).

Returns: tanh The hyperbolic tangent of the input series.

dualPoleFilter(src, lookback)

Returns the smoothed hyperbolic tangent of the input series.

Parameters:

src : The input series (i.e., the hyperbolic tangent).

lookback : The lookback window for the smoothing.

Returns: filter The smoothed hyperbolic tangent of the input series.

tanhTransform(src, smoothingFrequency, quadraticMeanLength)

Returns the tanh transform of the input series.

Parameters:

src : The input series (i.e., the result of the tanh calculation).

smoothingFrequency

quadraticMeanLength

Returns: signal The smoothed hyperbolic tangent transform of the input series.

n_rsi(src, n1, n2)

Returns the normalized RSI ideal for use in ML algorithms.

Parameters:

src : The input series (i.e., the result of the RSI calculation).

n1 : The length of the RSI.

n2 : The smoothing length of the RSI.

Returns: signal The normalized RSI.

n_cci(src, n1, n2)

Returns the normalized CCI ideal for use in ML algorithms.

Parameters:

src : The input series (i.e., the result of the CCI calculation).

n1 : The length of the CCI.

n2 : The smoothing length of the CCI.

Returns: signal The normalized CCI.

n_wt(src, n1, n2)

Returns the normalized WaveTrend Classic series ideal for use in ML algorithms.

Parameters:

src : The input series (i.e., the result of the WaveTrend Classic calculation).

n1

n2

Returns: signal The normalized WaveTrend Classic series.

n_adx(highSrc, lowSrc, closeSrc, n1)

Returns the normalized ADX ideal for use in ML algorithms.

Parameters:

highSrc : The input series for the high price.

lowSrc : The input series for the low price.

closeSrc : The input series for the close price.

n1 : The length of the ADX.

regime_filter(src, threshold, useRegimeFilter)

Parameters:

src

threshold

useRegimeFilter

filter_adx(src, length, adxThreshold, useAdxFilter)

filter_adx

Parameters:

src : The source series.

length : The length of the ADX.

adxThreshold : The ADX threshold.

useAdxFilter : Whether to use the ADX filter.

Returns: The ADX.

filter_volatility(minLength, maxLength, useVolatilityFilter)

filter_volatility

Parameters:

minLength : The minimum length of the ATR.

maxLength : The maximum length of the ATR.

useVolatilityFilter : Whether to use the volatility filter.

Returns: Boolean indicating whether or not to let the signal pass through the filter.

backtest(high, low, open, startLongTrade, endLongTrade, startShortTrade, endShortTrade, isStopLossHit, maxBarsBackIndex, thisBarIndex)

Performs a basic backtest using the specified parameters and conditions.

Parameters:

high : The input series for the high price.

low : The input series for the low price.

open : The input series for the open price.

startLongTrade : The series of conditions that indicate the start of a long trade.`

endLongTrade : The series of conditions that indicate the end of a long trade.

startShortTrade : The series of conditions that indicate the start of a short trade.

endShortTrade : The series of conditions that indicate the end of a short trade.

isStopLossHit : The stop loss hit indicator.

maxBarsBackIndex : The maximum number of bars to go back in the backtest.

thisBarIndex : The current bar index.

Returns: A tuple containing backtest values

init_table()

init_table()

Returns: tbl The backtest results.

update_table(tbl, tradeStatsHeader, totalTrades, totalWins, totalLosses, winLossRatio, winrate, stopLosses)

update_table(tbl, tradeStats)

Parameters:

tbl : The backtest results table.

tradeStatsHeader : The trade stats header.

totalTrades : The total number of trades.

totalWins : The total number of wins.

totalLosses : The total number of losses.

winLossRatio : The win loss ratio.

winrate : The winrate.

stopLosses : The total number of stop losses.

Returns: Updated backtest results table.

BasicVisibleChartBasic library for the visible range chart; with functions to allow plotting Fibs from body high/low as well as wick high/low

-Thanks to code from @PineCoders Visible Chart library (PineCoders/VisibleChart/4), which is a much more comprehensive library than this, but which does not include some functions that I find useful:

-Added the following exportable functions: highest/lowest body, highest/lowest close, highest/lowest open. These allow one to anchor fibs from bodies rather than wicks

-Added a Fib Box function in the example code

The above chart shows the example code plotting a Fib range drawn from bodies and a highlighted retracement zone (61.8 % - 78.6% )

~~All Exportable Functions~~

barIsVisible()

highestClose()

highestOpen()

highestBody()

lowestClose()

lowestOpen()

lowestBody()

high()

highBarTime()

low()

lowBarTime()

open()

close()

MyLibraryLibrary "MyLibrary"

TODO: add library description here

isHammer(fib, colorMatch)

TODO: add function description here

Parameters:

fib

colorMatch

Returns: TODO: add what function returns

eHarmonicpatternsLogScaleLibrary "eHarmonicpatternsLogScale"

Library provides functions to scan harmonic patterns both or normal and log scale

getSupportedPatterns()

get_prz_range(x, a, b, c, patternArray, errorPercent, start_adj, end_adj, logScale)

Provides PRZ range based on BCD and XAD ranges

Parameters:

x : X coordinate value

a : A coordinate value

b : B coordinate value

c : C coordinate value

patternArray : Pattern flags for which PRZ range needs to be calculated

errorPercent : Error threshold

start_adj : - Adjustments for entry levels

end_adj : - Adjustments for stop levels

logScale : - calculate on log scale. Default is false

Returns: Start and end of consolidated PRZ range

get_prz_range_xad(x, a, b, c, patternArray, errorPercent, start_adj, end_adj, logScale)

Provides PRZ range based on XAD range only

Parameters:

x : X coordinate value

a : A coordinate value

b : B coordinate value

c : C coordinate value

patternArray : Pattern flags for which PRZ range needs to be calculated

errorPercent : Error threshold

start_adj : - Adjustments for entry levels

end_adj : - Adjustments for stop levels

logScale : - calculate on log scale. Default is false

Returns: Start and end of consolidated PRZ range

get_projection_range(x, a, b, c, patternArray, errorPercent, start_adj, end_adj, logScale)

Provides Projection range based on BCD and XAD ranges

Parameters:

x : X coordinate value

a : A coordinate value

b : B coordinate value

c : C coordinate value

patternArray : Pattern flags for which PRZ range needs to be calculated

errorPercent : Error threshold

start_adj : - Adjustments for entry levels

end_adj : - Adjustments for stop levels

logScale : - calculate on log scale. Default is false

Returns: Array containing start and end ranges

isHarmonicPattern(x, a, b, c, d, flags, defaultEnabled, errorPercent, logScale)

Checks for harmonic patterns

Parameters:

x : X coordinate value

a : A coordinate value

b : B coordinate value

c : C coordinate value

d : D coordinate value

flags : flags to check patterns. Send empty array to enable all

defaultEnabled

errorPercent : Error threshold

logScale : - calculate on log scale. Default is false

Returns: Array of boolean values which says whether valid pattern exist and array of corresponding pattern names

isHarmonicProjection(x, a, b, c, flags, defaultEnabled, errorPercent, logScale)

Checks for harmonic pattern projection

Parameters:

x : X coordinate value

a : A coordinate value

b : B coordinate value

c : C coordinate value

flags : flags to check patterns. Send empty array to enable all

defaultEnabled

errorPercent : Error threshold

logScale : - calculate on log scale. Default is false

Returns: Array of boolean values which says whether valid pattern exist and array of corresponding pattern names.

E5TradingLibrary

This library replaces the previous MetaWorldEngineFilterLibrary3.

Library "E5TradingLibrary"

GetCandleStickSize(_src_high, _src_low)

returns size of the candle

Parameters:

_src_high

_src_low

Returns: candlestick size

GetCandleStickBodySize(_src_open, _src_close)

returns size of the candle body

Parameters:

_src_open

_src_close

Returns: candlestick body size

FilterLongerLowerWickCandles(_src_open, _src_close, _src_low)

Alters Candlestick Value to Magnify Candles with Long Wicks

Parameters:

_src_open

_src_close

_src_low

Returns: Midpoint of the candle body less the lower wick. If value returned has a large delta from midpoint of the body, then it is short wick

IsBullish(_src_open, _src_close)

Determine if Candle is Bullish or Bearish

Parameters:

_src_open

_src_close

Returns: True is Bullish

IsDoji(_candleIndex, _precision)

Determine if Candle is a Doji

Parameters:

_candleIndex

_precision

Returns: True if a Doji

MACD(_src, _fastLength, _slowLength, _signalLength)

Computes MACD

Parameters:

_src

_fastLength

_slowLength

_signalLength

Returns: Returns MACD and Signal Line

isFastSlowCrossed(SeriesA, SeriesB)

Computes if SeriesA crosses SeriesB

Parameters:

SeriesA

SeriesB

Returns: if SeriesA crosses SeriesB then true else false

isReversalUpTrend(SeriesA, SeriesB)

Computes if SeriesA crosses over SeriesB to determine reversal uptrend

Parameters:

SeriesA

SeriesB

Returns: if SeriesA crosses over SeriesB then true else false

isReversalDownTrend(SeriesA, SeriesB)

Computes if SeriesA crosses over SeriesB to determine reversal uptrend

Parameters:

SeriesA

SeriesB

Returns: if SeriesA crosses over SeriesB then true else false

SSMA(_src, smalength)

Computes smoothed SMA

Parameters:

_src

smalength

Returns: a single concatenated string for evaluation

GetTimeFrame()

Get Current timeframe in minutes

Returns: an integer value in minutes

getMA(_src, length, maType)

Gets a Moving Average based on type

Parameters:

_src

length

maType

Returns: A moving average with the given parameters

ATRSwitch(_src, _ATRMult, _ATRLength)

Average True Range Trailing Stops by Sylvain Vervoort

Parameters:

_src

_ATRMult

_ATRLength

Returns: upper ATR Line, lower ATR Line and the switch point

HiveLibraryLibrary "HiveLibrary"

: Custom library

RoundDown(number, decimals)

RoundDown() rounds the specified number down to the given number

of decimal places.

Parameters:

number : is the argument for rounding down & decimals is the number of digits after dot

decimals

Returns: return is the rounded down value of the number

Library_SmoothersLibrary "Library_Smoothers"

CorrectedMA(Src, Len)

CorrectedMA The strengths of the corrected Average (CA) is that the current value of the time series must exceed a the current volatility-dependent threshold, so that the filter increases or falls, avoiding false signals when the trend is in a weak phase.

Parameters:

Src

Len

Returns: The Corrected source.

EHMA(src, len)

EMA Exponential Moving Average.

Parameters:

src : Source to act upon

len

Returns: EMA of source

FRAMA(src, len, FC, SC)

FRAMA Fractal Adaptive Moving Average

Parameters:

src : Source to act upon

len : Length of moving average

FC : Fast moving average

SC : Slow moving average

Returns: FRAMA of source

Jurik(src, length, phase, power)

Jurik A low lag filter

Parameters:

src : Source

length : Length for smoothing

phase : Phase range is ±100

power : Mathematical power to use. Doesn't need to be whole numbers

Returns: Jurik of source

SMMA(src, len)

SMMA Smoothed moving average. Think of the SMMA as a hybrid of its better-known siblings — the simple moving average (SMA) and the exponential moving average (EMA).

Parameters:

src : Source

len

Returns: SMMA of source

SuperSmoother(src, len)

SuperSmoother

Parameters:

src : Source to smooth

len

Returns: SuperSmoother of the source

TMA(src, len)

TMA Triangular Moving Average

Parameters:

src : Source

len

Returns: TMA of source

TSF(src, len)

TSF Time Series Forecast. Uses linear regression.

Parameters:

src : Source

len

Returns: TSF of source

VIDYA(src, len)

VIDYA Chande's Variable Index Dynamic Average. See www.fxcorporate.com

Parameters:

src : Source

len

Returns: VIDYA of source

VAWMA(src, len, startingWeight, volumeDefault)

VAWMA = VWMA and WMA combined. Simply put, this attempts to determine the average price per share over time weighted heavier for recent values. Uses a triangular algorithm to taper off values in the past (same as WMA does).

Parameters:

src : Source

len : Length

startingWeight

volumeDefault : The default value to use when a chart has no volume.

Returns: The VAWMA of the source.

WWMA(src, len)

WWMA Welles Wilder Moving Average

Parameters:

src : Source

len

Returns: The WWMA of the source

ZLEMA(src, len)

ZLEMA Zero Lag Expotential Moving Average

Parameters:

src : Source

len

Returns: The ZLEMA of the source

SmootherType(mode, src, len, fastMA, slowMA, offset, phase, power, startingWeight, volumeDefault, Corrected)

Performs the specified moving average

Parameters:

mode : Name of moving average

src : the source to apply the MA type

len

fastMA : FRAMA fast moving average

slowMA : FRAMA slow moving average

offset : Linear regression offset

phase : Jurik phase

power : Jurik power

startingWeight : VAWMA starting weight

volumeDefault : VAWMA default volume

Corrected

Returns: The MA smoothed source

HendrixLIBRARY - utilsLibrary "HendrixLIBRARY"

getVolumeData()

getLTF(customTimeframe, ltf)

Parameters:

customTimeframe

ltf

sumArray(a)

Parameters:

a

arrs2vals(upVolumeArray, downVolumeArray, volArr)

Parameters:

upVolumeArray

downVolumeArray

volArr

getVolumesFromUpDownArrays(upVolumeArray, downVolumeArray)

Parameters:

upVolumeArray

downVolumeArray

getDeltaFromVolumes(upVolume, downVolume)

Parameters:

upVolume

downVolume

getDeltaFromUpDownArrays(upVolumeArray, downVolumeArray)

Parameters:

upVolumeArray

downVolumeArray

getUpColor()

getDownColor()

getBlackColor()

getColors()

printTableTR(txt)

Parameters:

txt

printTableBR(txt)

Parameters:

txt

printTableMR(txt)

Parameters:

txt

print(txt, lbl)

Parameters:

txt

lbl

printSyminfo(sym)

Parameters:

sym

HSupertrendLibrary "HSupertrend"

Supertrend implementation based on harmonic patterns

hsupertrend(zProperties, pProperties, errorPercent, showPatterns, patternColor)

derives supertrend based on harmonic patterns

Parameters:

zProperties : ZigzagProperties containing Zigzag length and source array

pProperties : PatternProperties used for calculation

errorPercent : Error threshold for scanning patterns

showPatterns : Draw identified patterns structure on chart

patternColor : Color of the pattern lines to be drawn

Returns:

ZigzagProperties

ZigzagProperties contains values required for zigzag calculation

Fields:

length : Zigzag length

source : Array containing custom OHLC. If not set, array.from(high, low) is used

PatternProperties

PatternProperties are essential pattern parameters used for calculation of bullish and bearish zones

Fields:

base : Base for calculating entry and stop of pattern. Can be CD, minmax or correction. Default is CD

entryPercent : Distance from D in terms of percent of Base in the direction of pattern

stopPercent : Distance from D in terms of percent of Base in the opposite direction of pattern

useClosePrices : When set uses close price for calculation of supertrend breakout

ChasinAlts_LibraryLibrary "ChasinAlts_Library"

rci(_BCgtg, _Tgtg, _close, _smaLen, _bar_index)

Parameters:

_BCgtg

_Tgtg

_close

_smaLen

_bar_index

printedBC(_time, _minPerc, _Tgtg, _lkbk)

Parameters:

_time

_minPerc

_Tgtg

_lkbk

form123(_ppLen, _BCgtg, _Tgtg, _high, _low, _close, _bar_index)

Parameters:

_ppLen

_BCgtg

_Tgtg

_high

_low

_close

_bar_index

obosCnt(_BCgtg, _Tgtg, _rci, _obosMin, _obosMax, _thresh)

Parameters:

_BCgtg

_Tgtg

_rci

_obosMin

_obosMax

_thresh

div(_thresh, _HLestLen, _Tgtg, _BCgtg, _rci, _time, _price, _LSL, _SSL, _LTP, _STP, _colorid, _long, _short)

Parameters:

_thresh

_HLestLen

_Tgtg

_BCgtg

_rci

_time

_price

_LSL

_SSL

_LTP

_STP

_colorid

_long

_short

tradeSim(_SL, _TP, _BCgtg, _Tgtg, _ppLen, _high, _low, _close, _bar_index, _time, _bull_rev, _bear_rev, _bull_obosCnt_gtg, _bear_obosCnt_gtg)

Parameters:

_SL

_TP

_BCgtg

_Tgtg

_ppLen

_high

_low

_close

_bar_index

_time

_bull_rev

_bear_rev

_bull_obosCnt_gtg

_bear_obosCnt_gtg

TrailingStopsLibrary "TrailingStops"

This library contains functions to output trailing stop lines.

f_marketStructureStop(_restartMode, _flipMode, _restartLowIn, _restartHighIn)

Parameters:

_restartMode - Defines how the stop lines persist. Allowed values are:

"Always On" - The stop lines are always present and they just reset when they're crossed.

"Flip" - The stop lines flip when they're crossed.

"Manual" - The stop lines turn off when they're crossed, and turn back on again when _restartLowIn or _restartHighIn are passed into the function as true.

_flipMode - Defines whether the stop lines are broken by wicks or closes. Allowed values are "Wick", and "Close".

_restartLowIn - If _restartMode is "Manual", passing this parameter as true restarts the Low stop line.

_restartHighIn - If _restartMode is "Manual", passing this parameter as true restarts the High stop line.

@returns - floats for the Low and High stop line.

MarketStructureLibrary "MarketStructure"

This library contains functions for identifying Lows and Highs in a rule-based way, and deriving useful information from them.

f_simpleLowHigh()

This function finds Local Lows and Highs, but NOT in order. A Local High is any candle that has its Low taken out on close by a subsequent candle (and vice-versa for Local Lows).

The Local High does NOT have to be the candle with the highest High out of recent candles. It does NOT have to be a Williams High. It is not necessarily a swing high or a reversal or anything else.

It doesn't have to be "the" high, so don't be confused.

By the rules, Local Lows and Highs must alternate. In this function they do not, so I'm calling them Simple Lows and Highs.

Simple Highs and Lows, by the above definition, can be useful for entries and stops. Because I intend to use them for stops, I want them all, not just the ones that alternate in strict order.

@param - there are no parameters. The function uses the chart OHLC.

@returns boolean values for whether this bar confirms a Simple Low/High, and ints for the bar_index of that Low/High.

f_localLowHigh()

This function finds Local Lows and Highs, in order. A Local High is any candle that has its Low taken out on close by a subsequent candle (and vice-versa for Local Lows).

The Local High does NOT have to be the candle with the highest High out of recent candles. It does NOT have to be a Williams High. It is not necessarily a swing high or a reversal or anything else.

By the rules, Local Lows and Highs must alternate, and in this function they do.

@param - there are no parameters. The function uses the chart OHLC.

@returns boolean values for whether this bar confirms a Local Low/High, and ints for the bar_index of that Low/High.

f_enhancedSimpleLowHigh()

This function finds Local Lows and Highs, but NOT in order. A Local High is any candle that has its Low taken out on close by a subsequent candle (and vice-versa for Local Lows).

The Local High does NOT have to be the candle with the highest High out of recent candles. It does NOT have to be a Williams High. It is not necessarily a swing high or a reversal or anything else.

By the rules, Local Lows and Highs must alternate. In this function they do not, so I'm calling them Simple Lows and Highs.

Simple Highs and Lows, by the above definition, can be useful for entries and stops. Because I intend to use them for trailing stops, I want them all, not just the ones that alternate in strict order.

The difference between this function and f_simpleLowHigh() is that it also tracks the lowest/highest recent level. This level can be useful for trailing stops.

In effect, these are like more "normal" highs and lows that you would pick by eye, but confirmed faster in many cases than by waiting for the low/high of that particular candle to be taken out on close,

because they are instead confirmed by ANY subsequent candle having its low/high exceeded. Hence, I call these Enhanced Simple Lows/Highs.

The levels are taken from the extreme highs/lows, but the bar indexes are given for the candles that were actually used to confirm the Low/High.

This is by design, because it might be misleading to label the extreme, since we didn't use that candle to confirm the Low/High..

@param - there are no parameters. The function uses the chart OHLC.

@returns - boolean values for whether this bar confirms an Enhanced Simple Low/High

ints for the bar_index of that Low/High

floats for the values of the recent high/low levels

floats for the trailing high/low levels (for debug/post-processing)

bools for market structure bias

f_trueLowHigh()

This function finds True Lows and Highs.

A True High is the candle with the highest recent high, which then has its low taken out on close by a subsequent candle (and vice-versa for True Lows).

The difference between this and an Enhanced High is that confirmation requires not just any Simple High, but confirmation of the very candle that has the highest high.

Because of this, confirmation is often later, and multiple Simple Highs and Lows can develop within ranges formed by a single big candle without any of them being confirmed. This is by design.

A True High looks like the intuitive "real high" when you look at the chart. True Lows and Highs must alternate.

@param - there are no parameters. The function uses the chart OHLC.

@returns - boolean values for whether this bar confirms an Enhanced Simple Low/High

ints for the bar_index of that Low/High

floats for the values of the recent high/low levels

floats for the trailing high/low levels (for debug/post-processing)

bools for market structure bias