P/E Ratio vs Median + Bollinger Band- 📝 This indicator highlights potential buying opportunities by analyzing the Price-to-Earnings (P/E) ratio in relation to Bollinger Bands and its historical median.

- 🎯 The goal is to provide a visually intuitive signal for value-oriented entries, especially when valuation compression aligns with historical context.

- 💡 Vertical green shading is applied when the P/E ratio drops below the lower Bollinger Band, which is calculated directly from the P/E ratio itself — not price. This condition often signals the ticker may be oversold.

- 🟢 Lighter green appears when the ratio is below the lower band but above the median, suggesting a possible shorter-term entry with slightly more risk.

- 🟢 Darker green appears when the ratio is both below the lower band and below the median, pointing to a potentially stronger, longer-term value entry.

- ⚠️ This logic was tested using 1 and 2-day time frames. It may not be as helpful in longer time frames, as the financial data TradingView pulls in begins in Q4 2017.

- ⚠️ Note: This script relies on financial data availability through TradingView. It may not function properly with certain tickers — especially ETFs, IPOs, or thinly tracked assets — where P/S ratio data is missing or incomplete.

- ⚠️ This indicator will not guarantee successful results. Use in conjunction with other indicators and do your due diligence.

- 🤖 This script was iteratively refined with the help of AI to ensure clean logic, minimalist design, and actionable signal clarity.

- 📢 Idea is based on the script "Historical PE ratio vs median" by haribotagada

- 💬 Questions, feedback, or suggestions? Drop a comment — I’d love to hear how you’re using it or what you'd like to see changed.

価値

P/S Ratio vs Median + Bollinger Band- 📝 This indicator highlights potential buying opportunities by analyzing the Price-to-Sales (P/S) ratio in relation to Bollinger Bands and its historical median.

- 🎯 The goal is to provide a visually intuitive signal for value-oriented entries, especially when valuation compression aligns with historical context.

- 💡 Vertical green shading is applied when the P/S ratio drops below the lower Bollinger Band, which is calculated directly from the P/S ratio itself — not price. This condition often signals the ticker may be oversold.

- 🟢 Lighter green appears when the ratio is below the lower band but above the median, suggesting a possible shorter-term entry with slightly more risk.

- 🟢 Darker green appears when the ratio is both below the lower band and below the median, pointing to a potentially stronger, longer-term value entry.

- ⚠️ This logic was tested using 1 and 2-day time frames. It may not be as helpful in longer time frames, as the financial data TradingView pulls in begins in Q4 2017.

- ⚠️ Note: This script relies on financial data availability through TradingView. It may not function properly with certain tickers — especially ETFs, IPOs, or thinly tracked assets — where P/S ratio data is missing or incomplete.

- ⚠️ This indicator will not guarantee successful results. Use in conjunction with other indicators and do your due diligence.

- 🤖 This script was iteratively refined with the help of AI to ensure clean logic, minimalist design, and actionable signal clarity.

- 📢 Idea is based on the script "Historical PE ratio vs median" by @haribotagada

- 💬 Questions, feedback, or suggestions? Drop a comment — I’d love to hear how you’re using it or what you'd like to see changed.

Future Value ProjectionFuture Value Projection with Actual CAGR

This indicator calculates the future value (FV) of the current ticker’s price using its historical Compound Annual Growth Rate (CAGR). It measures how much the price has grown over a chosen lookback period, derives the average annual growth rate, and then projects the current price forward into the future.

Formulae:

CAGR:

CAGR = ( PV_now / PV_past )^(1 / t) - 1

Future Value:

FV = PV_now × ( 1 + CAGR / n )^( n × T )

Where:

PV_now = Current price

PV_past = Price t years ago

t = Lookback period (years)

CAGR = Compound Annual Growth Rate

n = Compounding periods per year (1=annual, 12=monthly, 252=daily, etc.)

T = Projection horizon (years forward)

How it works:

Select a lookback period (e.g., 3 years).

The script finds the price from that time and computes the CAGR.

It then projects the current price forward by T years using the CAGR.

The chart shows:

Current price (blue)

Projected FV target (green)

A table with CAGR and projection details

Use case:

Helps investors and traders visualize long-term growth projections if the ticker continues growing at its historical pace.

BTC Power Law Valuation BandsBTC Power Law Rainbow

A long-term valuation framework for Bitcoin based on Power Law growth — designed to help identify macro accumulation and distribution zones, aligned with long-term investor behavior.

🔍 What Is a Power Law?

A Power Law is a mathematical relationship where one quantity varies as a power of another. In this model:

Price ≈ a × (Time)^b

It captures the non-linear, exponentially slowing growth of Bitcoin over time. Rather than using linear or cyclical models, this approach aligns with how complex systems, such as networks or monetary adoption curves, often grow — rapidly at first, and then more slowly, but persistently.

🧠 Why Power Law for BTC?

Bitcoin:

Has finite supply and increasing adoption.

Operates as a monetary network , where Metcalfe’s Law and power laws naturally emerge.

Exhibits exponential growth over logarithmic time when viewed on a log-log chart .

This makes it uniquely well-suited for power law modeling.

🌈 How to Use the Valuation Bands

The central white line represents the modeled fair value according to the power law.

Colored bands represent deviations from the model in logarithmic space, acting as macro zones:

🔵 Lower Bands: Deep value / Accumulation zones.

🟡 Mid Bands: Fair value.

🔴 Upper Bands: Euphoria / Risk of macro tops.

📐 Smart Money Concepts (SMC) Alignment

Accumulation: Occurs when price consolidates near lower bands — often aligning with institutional positioning.

Markup: As price re-enters or ascends the bands, we often see breakout behavior and trend expansion.

Distribution: When price extends above upper bands, potential for exit liquidity creation and distribution events.

Reversion: Historically, price mean-reverts toward the model — rarely staying outside the bands for long.

This makes the model useful for:

Cycle timing

Long-term DCA strategy zones

Identifying value dislocations

Filtering short-term noise

⚠️ Disclaimer

This tool is for educational and informational purposes only . It is not financial advice. The power law model is a non-predictive, mathematical framework and does not guarantee future price movements .

Always use additional tools, risk management, and your own judgment before making trading or investment decisions.

US Macro Cycle (Z-Score Model)US Macro Cycle (Z-Score Model)

This indicator tracks the US economic cycle in real time using a weighted composite of seven macro and market-based indicators, each converted into a rolling Z-score for comparability. The model identifies the current phase of the cycle — Expansion, Peak, Contraction, or Recovery — and suggests sector tilts based on historical performance in each phase.

Core Components:

Yield Curve (10y–2y): Positive & steepening = growth; inverted = slowdown risk.

Credit Spreads (HYG/LQD): Tightening = risk-on; widening = risk-off.

Sector Leadership (Cyclicals vs. Defensives): Measures market leadership regime.

Copper/Gold Ratio: Higher copper = growth signal; higher gold = defensive.

SPY vs. 200-day MA: Equity trend strength.

SPY/IEF Ratio: Stocks vs. bonds relative strength.

VIX (Inverted): Low/falling volatility = supportive; high/rising = risk-off.

Methodology:

Each series is transformed into a rolling Z-score over the selected lookback period (optionally using median/MAD for robustness and winsorization to clip outliers).

Z-scores are combined using user-defined weights and normalized.

The smoothed composite is compared against phase thresholds to classify the macro environment.

Features:

Customizable Weights: Emphasize the indicators most relevant to your strategy.

Adjustable Thresholds: Fine-tune cycle phase definitions.

Background Coloring: Visual cue for the current phase.

Summary Table: Displays composite Z, confidence %, and individual Z-scores.

Alerts: Trigger when the phase changes, with details on the composite score and recommended tilt.

Use Cases:

Align sector rotation or relative strength strategies with the macro backdrop.

Identify favorable or defensive phases for tactical allocation.

Monitor macro turning points to manage portfolio risk.

It's doesn't fill nan gaps so there is quite a bit of zeroes, non-repainting.

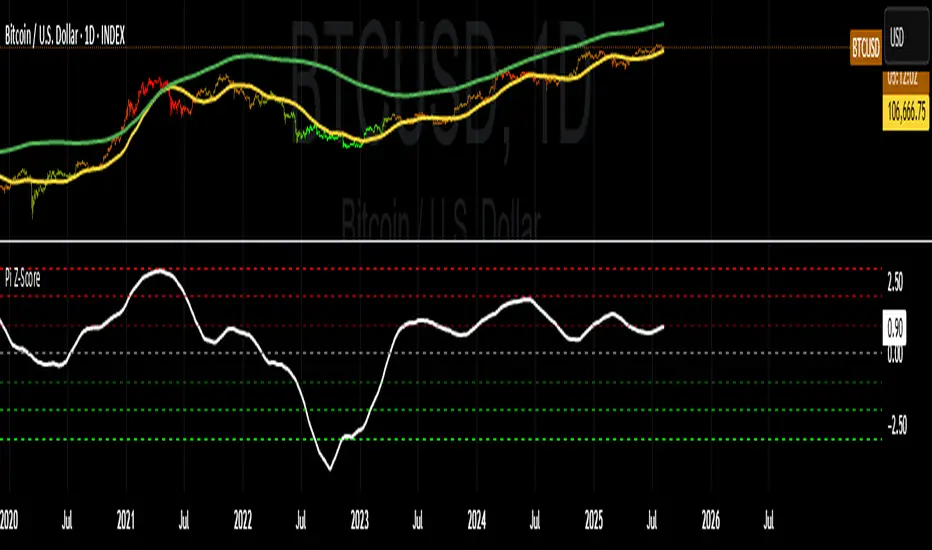

CVDD Z-ScoreCumulative Value Days Destroyed (CVDD) - The CVDD was created by Willy Woo and is the ratio of the cumulative value of Coin Days Destroyed in USD and the market age (in days). While this indicator is used to detect bottoms normally, an extension is used to allow detection of BTC tops. When the BTC price goes above the CVDD extension, BTC is generally considered to be overvalued. Because the "strength" of the BTC tops has decreased over the cycles, a logarithmic function for the extension was created by fitting past cycles as log extension = slope * time + intercept. This indicator is triggered for a top when the BTC price is above the CVDD extension. For the bottoms, the CVDD is shifted upwards at a default value of 120%. The slope, intercept, and CVDD bottom shift can all be modified in the script.

Now with the automatic Z-Score calculation for ease of classification of Bitcoin's valuation according to this metric.

Created for TRW.

Bitcoin: Pi Cycle Top & Bottom Indicator Z ScoreIndicator Overview

The Pi Cycle Top Indicator has historically been effective in picking out the timing of market cycle highs within 3 days.

It uses the 111 day moving average (111DMA) and a newly created multiple of the 350 day moving average, the 350DMA x 2.

Note: The multiple is of the price values of the 350DMA, not the number of days.

For the past three market cycles, when the 111DMA moves up and crosses the 350DMA x 2 we see that it coincides with the price of Bitcoin peaking.

It is also interesting to note that 350 / 111 is 3.153, which is very close to Pi = 3.142. In fact, it is the closest we can get to Pi when dividing 350 by another whole number.

It once again demonstrates the cyclical nature of Bitcoin price action over long time frames. However, in this instance, it does so with a high degree of accuracy over Bitcoin's adoption phase of growth.

Bitcoin Price Prediction Using This Tool

The Pi Cycle Top Indicator forecasts the cycle top of Bitcoin’s market cycles. It attempts to predict the point where Bitcoin price will peak before pulling back. It does this on major high time frames and has picked the absolute tops of Bitcoin’s major price moves throughout most of its history.

How It Can Be Used

Pi Cycle Top is useful to indicate when the market is very overheated. So overheated that the shorter-term moving average, which is the 111-day moving average, has reached an x2 multiple of the 350-day moving average. Historically, it has proved advantageous to sell Bitcoin around this time in Bitcoin's price cycles.

It is also worth noting that this indicator has worked during Bitcoin's adoption growth phase, the first 15 years or so of Bitcoin's life. With the launch of Bitcoin ETF's and Bitcoin's increased integration into the global financial system, this indicator may cease to be relevant at some point in this new market structure.

Added the Z-Score metric for easy classification of the value of Bitcoin according to this indicator.

Created for TRW

Crowding model ║ BullVision🔬 Overview

The Crypto Crowding Model Pro is a sophisticated analytical tool designed to visualize and quantify market conditions across multiple cryptocurrencies. By leveraging Relative Strength Index (RSI) and Z-score calculations, this indicator provides traders with an intuitive and detailed snapshot of current crypto market dynamics, highlighting areas of extreme momentum, crowded trades, and potential reversal points.

⚙️ Key Concepts

📊 RSI and Z-Score Analysis

RSI (Relative Strength Index) evaluates the momentum and strength of each cryptocurrency, identifying overbought or oversold conditions.

Z-Score Normalization measures each asset's current price deviation relative to its historical average, identifying statistically significant extremes.

🎯 Crowding Analytics

An integrated analytics panel provides real-time crowding metrics, quantifying market sentiment into four distinct categories:

🔥 FOMO (Fear of Missing Out): High momentum, potential exhaustion.

❄️ Fear: Low momentum, potential reversal or consolidation.

📈 Recovery: Moderate upward momentum after a downward trend.

💪 Strength: Stable bullish conditions with sustained momentum.

🖥️ Visual Scatter Plot

Assets are plotted on a dynamic scatter plot, positioning each cryptocurrency according to its RSI and Z-score.

Color coding, symbol shapes, and sizes help quickly identify main market segments (BTC, ETH, TOTAL, OTHERS) and individual asset conditions.

🧩 Quadrant Classification

Assets are categorized into four quadrants based on their momentum and deviation:

Overbought Extended: High RSI and positive Z-score.

Recovery Phase: Low RSI but positive Z-score.

Oversold Compressed: Low RSI and negative Z-score.

Strong Consolidation: High RSI but negative Z-score.

🔧 User Customization

🎨 Visual Settings

Bar Scale: Adjust the scatter plot visual scale.

Asset Visibility: Optionally display key market benchmarks (TOTAL, BTC, ETH, OTHERS).

Gradient Background: Enhances visual interpretation of asset clusters.

Crowding Analytics Panel: Toggle the analytics panel on/off.

📊 Indicator Parameters

RSI Length: Defines the calculation period for RSI.

Z-score Lookback: Historical lookback period for normalization.

Crowding Alert Threshold: Sets alert sensitivity for crowded market conditions.

🎯 Zone Settings

Quadrant Labels: Displays descriptive labels for each quadrant.

Danger Zones: Highlights extreme RSI levels indicative of heightened market risk.

📈 Visual Output

Dynamic Scatter Plot: Visualizes asset positioning clearly and intuitively.

Gradient and Grid: Professional gridlines and subtle gradient backgrounds assist visual assessment.

Danger Zone Highlights: Visually indicates RSI extremes to warn of potential market turning points.

Crowding Analytics Panel: Real-time summary of market sentiment and asset distribution.

🔍 Use Cases

This indicator is particularly beneficial for traders and analysts looking to:

Identify crowded trades and potential reversal points.

Quickly assess overall market sentiment and individual asset strength.

Integrate a robust momentum analysis into broader technical or fundamental strategies.

Enhance market timing and improve risk management decisions.

⚠️ Important Notes

This indicator does not provide explicit buy or sell signals.

It is intended solely for informational, analytical, and educational purposes.

Past performance and signals are not indicative of future market results.

Always combine with additional tools and analysis as part of comprehensive decision-making.

Greer Value Yields Line📈 Greer Value Yields Line – Valuation Signal Without the Clutter

Part of the Greer Financial Toolkit, this streamlined indicator tracks four valuation-based yield metrics and presents them clearly via the Data Window, GVY Score badge, and an optional Yield Table:

Earnings Yield (EPS ÷ Price)

FCF Yield (Free Cash Flow ÷ Price)

Revenue Yield (Revenue per Share ÷ Price)

Book Value Yield (Book Value per Share ÷ Price)

✅ Each yield is compared against its historical average

✅ A point is scored for each metric above average (0–4 total)

✅ Color-coded GVY Score badge highlights valuation strength

✅ Yield trend-lines Totals (TVAVG & TVPCT) help assess direction

✅ Clean layout: no chart clutter – just actionable insights

🧮 GVY Score Color Coding (0–4):

⬜ 0 = None (White)

⬜ 1 = Weak (Gray)

🟦 2 = Neutral (Aqua)

🟩 3 = Strong (Green)

🟨 4 = Gold Exceptional (All metrics above average)

Total Value Average Line Color Coding:

🟥 Red – Average trending down

🟩 Green – Average trending up

Ideal for long-term investors focused on fundamental valuation, not short-term noise.

Enable the table and badge for a compact yield dashboard — or keep it minimal with just the Data Window and trend-lines.

Greer Book Value Yield📘 Script Title

Greer Book Value Yield – Valuation Insight Based on Balance Sheet Strength

🧾 Description

Greer Book Value Yield is a valuation-focused indicator in the Greer Financial Toolkit, designed to evaluate how much net asset value (book value) a company provides per share relative to its current market price. This script calculates the Book Value Per Share Yield (BV%) using the formula:

Book Value Yield (%) = Book Value Per Share ÷ Stock Price × 100

This yield helps investors assess whether a stock is trading at a discount or premium to its underlying assets. It dynamically highlights when the yield is:

🟢 Above its historical average (potentially undervalued)

🔴 Below its historical average (potentially overvalued)

🔍 Use Case

Analyze valuation through asset-based metrics

Identify buy opportunities when book value yield is historically high

Combine with other scripts in the Greer Financial Toolkit:

📘 Greer Value – Tracks year-over-year growth consistency across six key metrics

📊 Greer Value Yields Dashboard – Visualizes multiple valuation-based yields

🟢 Greer BuyZone – Highlights long-term technical buy zones

🛠️ Inputs & Data

Uses Book Value Per Share (BVPS) from TradingView’s financial database (Fiscal Year)

Calculates and compares against a static average yield to assess historical valuation

Clean visual feedback via dynamic coloring and overlays

⚠️ Disclaimer

This tool is for educational and informational purposes only and should not be considered financial advice. Always conduct your own research before making investment decisions.

Greer EPS Yield📘 Script Title

Greer EPS Yield – Valuation Insight Based on Earnings Productivity

🧾 Description

Greer EPS Yield is a valuation-focused indicator from the Greer Financial Toolkit, designed to evaluate how efficiently a company generates earnings relative to its current stock price. This script calculates the Earnings Per Share Yield (EPS%), using the formula:

EPS Yield (%) = Earnings Per Share ÷ Stock Price × 100

This yield metric provides a quick snapshot of valuation through the lens of profitability per share. It dynamically highlights when the EPS yield is:

🟢 Above its historical average (potentially undervalued)

🔴 Below its historical average (potentially overvalued)

🔍 Use Case

Quickly assess valuation attractiveness based on earnings yield.

Identify potential buy opportunities when EPS% is above its long-term average.

Combine with other indicators in the Greer Financial Toolkit for a fundamentals-driven investment strategy:

📘 Greer Value – Tracks year-over-year growth consistency across six key metrics

📊 Greer Value Yields Dashboard – Visualizes valuation-based yield metrics

🟢 Greer BuyZone – Highlights long-term technical buy zones

🛠️ Inputs & Data

Uses fiscal year EPS data from TradingView’s built-in financial database.

Tracks a static average EPS Yield to compare current valuation to historical norms.

Clean, intuitive visual with automatic color coding.

⚠️ Disclaimer

This tool is for educational and informational purposes only and should not be considered financial advice. Always conduct your own research before making investment decisions.

H turnoverTrading Value refers to the total monetary amount of all transactions for a particular stock or the entire market over a specific period. It is calculated by multiplying the trading volume (the number of shares traded) by the price at which they were traded. For example, if 10,000 shares of a stock are traded in a day at an average price of 50,000 KRW, the trading value for that day would be 500,000,000 KRW.

Key points about trading value:

Market Activity and Liquidity: A high trading value indicates an active and liquid market.

Flow of Investment Funds: Increasing trading value suggests more money is flowing into the market or a particular stock.

Relationship with Price Movements: When both trading value and price rise together, it often signals strong buying interest. Conversely, significant price changes with low trading value may be less reliable.

Market Sentiment Indicator: Changes in trading value can reflect shifts in investor interest and sentiment.

In summary, trading value is the total amount of money exchanged in trades and serves as an important indicator of market activity, liquidity, and investor sentiment.

Dynamic VWAP: Fair Value & Divergence SuiteDynamic VWAP: Fair Value & Divergence Suite

Dynamic VWAP: Fair Value & Divergence Suite is a comprehensive tool for tracking contextual valuation, overextension, and potential reversal signals in trending markets. Unlike traditional VWAP that anchors to the start of a session or a fixed period, this indicator dynamically resets the VWAP anchor to the most recent swing low. This design allows you to monitor how far price has extended from the most recent significant low, helping identify zones of potential profit-taking or reversion.

Deviation bands (standard deviations above the anchored VWAP) provide a clear visual framework to assess whether price is in a fair value zone (±1σ), moderately extended (+2σ), or in zones of extreme extension (+3σ to +5σ). The indicator also highlights contextual divergence signals, including slope deceleration, weak-volume retests, and deviation failures—giving you actionable confluence around potential reversal points.

Because the anchor updates dynamically, this tool is particularly well suited for trend-following assets like BTC or stocks in sustained moves, where price rarely returns to deep negative deviation zones. For this reason, the indicator focuses on upside extension rather than symmetrical reversion to a long-term mean.

🎯 Key Features

✅ Dynamic Swing Low Anchoring

Continuously re-anchors VWAP to the most recent swing low based on your chosen lookback period.

Provides context for trend progression and overextension relative to structural lows.

✅ Standard Deviation Bands

Plots up to +5σ deviation bands to visualize levels of overextension.

Extended bands (+3σ to +5σ) can be toggled for simplicity.

✅ Conditional Zone Fills

Colored background fills show when price is inside each valuation zone.

Helps you immediately see if price is in fair value, moderately extended, or highly stretched territory.

✅ Divergence Detection

VWAP Slope Divergence: Flags when price makes a higher high but VWAP slope decelerates.

Low Volume Retest: Highlights weak re-tests of VWAP on low volume.

Deviation Failure: Identifies when price reverts back inside +1σ after closing beyond +3σ.

✅ Volume Fallback

If volume is unavailable, uses high-low range as a proxy.

✅ Highly Customizable

Adjust lookbacks, show/hide extended bands, toggle fills, and enable or disable divergences.

🛠️ How to Use

Identify Buy and Sell Zones

Price in the fair value band (±1σ) suggests equilibrium.

Reaching +2σ to +3σ signals increasing overextension and potential areas to take profits.

+4σ to +5σ zones can be used to watch for exhaustion or mean-reversion setups.

Monitor Divergence Signals

Use slope divergence and deviation failures to look for confluence with overextension.

Low volume retests can flag rallies lacking conviction.

Adapt Swing Lookback

30–50 bars: Faster re-anchoring for swing trading.

75–100 bars: More stable anchors for longer-term trends.

🧭 Best Practices

Combine the anchored VWAP with higher timeframe structure.

Confirm signals with other tools (momentum, volume profiles, or trend filters).

Use extended deviation zones as context, not as standalone signals.

⚠️ Disclaimer

This script is for educational and informational purposes only. It does not constitute financial advice or a recommendation to buy or sell any security or asset. Always do your own research and consult a qualified financial professional before making any trading decisions. Past performance does not guarantee future results.

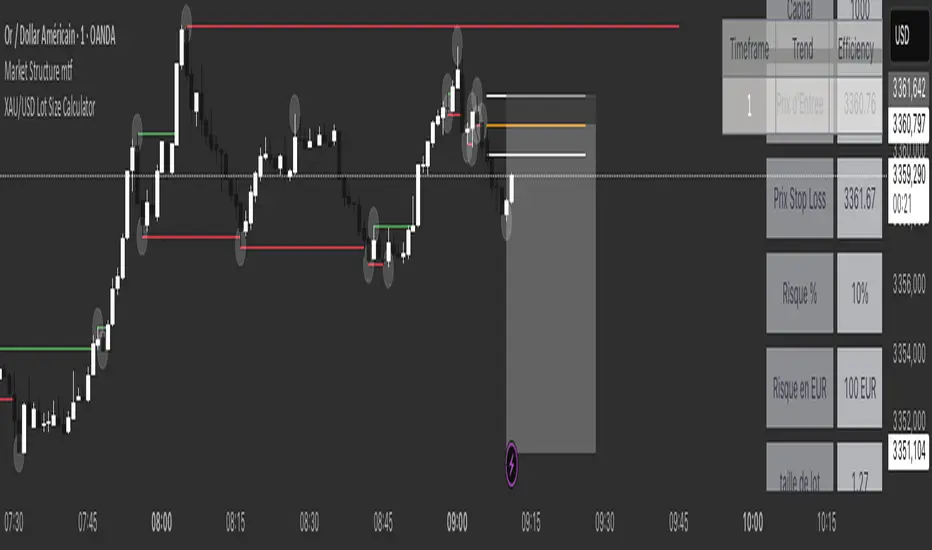

XAU/USD Lot Size CalculatorThis indicator automatically calculates the optimal lot size for XAUUSD (gold) based on the level of risk the trader wants to take. It is designed for traders using MetaTrader 4 or 5 and helps adjust position size according to the specific volatility of gold. The user can set the percentage of capital they are willing to risk on a single trade, for example 1%. The indicator also takes into account the stop loss level, which can be entered in pips or in dollars, as well as the account size (balance or equity).

Based on these parameters, it calculates the exact lot size that matches the risk amount. It then displays on the chart the recommended lot size, the risk amount in dollars, the pip value for XAUUSD, and a confirmation of the stop loss level. This type of indicator is useful for maintaining disciplined risk management and avoiding position sizing errors, especially on a highly volatile asset like gold.

TPO[Fixed Range, Anchored, Bars Back]TPO Bars Back, Fixed Range and Anchored

Overview

The TPO Profile (Time Price Opportunity Profile) is a powerful market profile indicator that displays the amount of time price spent at different levels during a specified period. Unlike traditional volume profile indicators that show volume distribution, TPO Profile shows time distribution , providing insights into where price has spent the most time and identifying key support and resistance levels.

Key Advantages Over TradingView's Built-in TPO

Simplified Composite Creation : Automatically creates TPO profiles for any time range without manual split/merge operations

Instant Value Area Calculation : Immediately shows Value Area, POC, VAH, and VAL for your selected period

No Manual Assembly Required : TradingView's native TPO requires you to manually split sessions and merge them to create composites - this indicator does it automatically

Flexible Time Ranges : Create composites for any custom time period (multiple days, weeks, specific events) with a few clicks

Real-time Composite Updates : Anchor mode creates live composites that update as new data arrives

Multiple Composite Analysis : Easily compare different time periods without the tedious manual process

Key Features

Core Functionality

Time-Based Analysis : Shows time spent at each price level rather than volume

Configurable Time Blocks : Use any timeframe for TPO counting (30min, 1H, 4H, etc.)

Multiple Price Levels : Adjustable from 5 to 200 levels for granular analysis

Point of Control (POC) : Automatically identifies the price level with highest time activity

Value Area Calculation : Shows the price range containing 70% (configurable) of time activity

Automatic Composite Generation : Creates multi-session composites without manual intervention

Three Operating Modes

1. Bars Back Mode

Analyzes the last N bars from the current bar

Perfect for recent market activity analysis

Range: 10-500 bars

Use Case : Intraday analysis, recent session review

2. Fixed Range Mode

Analyzes a specific time period between start and end times

Ideal for historical analysis of specific events

Creates perfect composites for multi-day periods

Use Case : Earnings periods, news events, specific trading sessions, weekly/monthly composites

3. Anchor Mode (NEW)

Starts from a specific time and extends to the current bar

Dynamically updates as new bars form

Perfect for building live composites from any starting point

Use Case : Live session monitoring, event-based analysis from a specific point, growing composites

Visual Elements

TPO Bars

Horizontal bars showing time distribution at each price level

Longer bars = more time spent at that level

Color-coded to distinguish Value Area from outlying levels

Point of Control (POC)

Red line marking the price level with highest time activity

Most significant support/resistance level

Configurable line style (Solid/Dashed/Dotted) and width

Value Area High/Low (VAH/VAL)

Green and Orange lines marking the boundaries of the Value Area

Shows the price range containing the specified percentage of time activity

Optional display with customizable line styles

Single Print Detection

Identifies price levels touched by only one time block

Display options: Lines or Boxes

Purple color highlighting these significant levels

Often act as strong support/resistance in future trading

Customization Options

Time Block Configuration

Block Time : Choose timeframe for TPO counting (30min, 1H, 4H, etc.)

Allows analysis at different time granularities

Higher timeframes = broader perspective, Lower timeframes = finer detail

Visual Styling

Line Styles : Solid, Dashed, or Dotted for all line elements

Line Widths : 1-5 pixels for POC, VAH, and VAL lines

Colors : Fully customizable colors for all elements

Transparency : Adjustable transparency for better chart readability

Label Management

Show/Hide Labels : Toggle POC, VAH, VAL labels

Font Sizes : Tiny, Small, Normal, Large, Huge

Label Positioning : 8 different position options relative to lines

Offset Controls : Fine-tune label positioning

Line Extension

Level Offset Right : Controls how far lines extend

Smart extension logic:

Value ≤ 0: Infinite extension (extend.right)

Value ≥ 1: Extends exactly N bars ahead

Trading Applications

Support & Resistance

POC often acts as strong support/resistance

Value Area boundaries provide key levels

Single prints frequently become significant levels

Market Structure Analysis

Identify areas of price acceptance (thick TPO bars)

Spot areas of price rejection (thin TPO bars)

Understand where market participants are comfortable trading

Composite Profile Analysis

Create multi-day, weekly, or monthly composites instantly

Compare different composite periods without manual work

Analyze longer-term price acceptance levels

Build composites around specific events or announcements

Session Analysis

Monitor intraday session development in real-time

Compare different sessions (London, New York, Asia)

Track how profiles change throughout the trading day

Build live composites across multiple sessions

Event Analysis

Use Fixed Range mode for earnings, news events

Use Anchor mode to track price development from specific events

Compare pre/post event price acceptance levels

Create event-based composites automatically

Input Parameters

Mode Selection

Mode : Bars Back | Fixed Range | Anchor

Bars Back : Number of bars to analyze (10-500)

Start Time : Beginning time for Fixed Range and Anchor modes

End Time : Ending time for Fixed Range mode only

Analysis Configuration

Block Time : Timeframe for TPO blocks (e.g., "30" for 30-minute blocks)

TPO Levels : Number of price levels (5-200)

Value Area % : Percentage for Value Area calculation (50-95%)

Display Options

Show POC : Display Point of Control line

Show Value Area : Display Value Area box

Show VAH/VAL Lines : Display Value Area boundary lines

Show Single Prints : Display single print detection

Single Print Style : Lines or Boxes

Styling Controls

Colors : TPO, POC, Value Area, VAH, VAL, Single Print colors

Line Styles : POC, VAH, VAL line styles

Line Widths : POC, VAH, VAL line widths

Labels : Show/hide, font size, position, offset controls

Technical Details

Calculation Method

Divides the price range into equal levels based on TPO Levels setting

For each time block, determines which price levels it crosses

Adds +1 count to each crossed level

Identifies POC as the level with highest count

Calculates Value Area by expanding from POC until target percentage is reached

Performance Considerations

Historical data limited to prevent buffer overflow errors

Smart bounds checking for different timeframes

Optimized cleanup routines to prevent drawing object accumulation

Pine Script Version

Built on Pine Script v6

Uses modern Pine Script best practices

Efficient array handling and drawing object management

Best Practices

Timeframe Selection

Block Time = Chart Timeframe : Traditional TPO approach

Block Time > Chart Timeframe : Smoother, broader perspective

Block Time < Chart Timeframe : More granular, detailed analysis

Level Count Guidelines

Low levels (10-20) : Better for swing trading, major levels

High levels (50-100) : Better for scalping, precise entries

Very high levels (100+) : For very detailed analysis

Mode Selection

Bars Back : Daily analysis, recent activity

Fixed Range : Historical events, specific periods, manual composites

Anchor : Live monitoring, event-based analysis, growing composites

Composite Creation Workflow

Select Fixed Range or Anchor mode

Set your desired start time (and end time for Fixed Range)

Adjust TPO Levels for desired granularity

Enable VAH/VAL lines to see Value Area boundaries

The composite profile generates automatically with all key levels

This indicator eliminates the tedious manual process of creating composite TPO profiles in TradingView. Instead of splitting sessions and manually merging them, you get instant composite analysis with automatic Value Area calculation, POC identification, and single print detection. The combination of time-based analysis, multiple operating modes, and extensive customization options makes it a powerful tool for understanding market structure and price acceptance levels across any time period.

Greer Revenue Yield📊 Greer Revenue Yield – RPS%

Author: Sean Lee Greer

Date Published: June 23, 2025

🔍 Overview

The Greer Revenue Yield indicator evaluates a stock's Revenue Per Share Yield (RPS%), giving investors a unique lens into how much top-line revenue a company produces per share relative to its stock price. This can help identify under- or over-valued conditions based on fundamental efficiency.

Revenue per Share = Total Revenue ÷ Shares Outstanding

Revenue Yield (%) = Revenue per Share ÷ Stock Price × 100

A simple yet powerful valuation metric, dynamically visualized with smart coloring:

🟢 Green = Yield is above average (potential value opportunity)

🔴 Red = Yield is below average (potentially overvalued)

🧠 Use Case

Use this tool to assess whether a company’s price justifies its revenue output on a per-share basis. Especially useful in combination with other indicators in the Greer Financial Toolkit:

📘 Greer Value – Tracks year-over-year growth consistency across 6 key financial metrics

📊 Greer Value Yields Dashboard – Visualizes multiple valuation-based yields

🟢 Greer BuyZone – Identifies long-term technical entry points based on trend cycles and valuation zones

⚠️ Disclaimer

This script is for educational purposes only and should not be considered financial advice. Always conduct your own research or consult a financial advisor before making investment decisions.

Greer Value Yields Dashboard🧾 Greer Value Yields Dashboard – v1.0

Author: Sean Lee Greer

Release Date: June 22, 2025

🧠 Overview

The Greer Value Yields Dashboard visualizes and evaluates four powerful valuation metrics for any publicly traded company:

📘 Earnings per Share Yield

💵 Free Cash Flow Yield

💰 Revenue Yield

🏦 Book Value Yield

Each yield is measured as a percentage of current stock price and compared against its historical average. The script assigns 1 point per metric when the current yield exceeds its long-term average. The total score (0 to 4) is displayed as a color-coded column chart, helping long-term investors quickly assess fundamental valuation strength.

✅ Key Features

📊 Real-time calculation of 4 yield-based valuation metrics

⚖ Historical average tracking for each yield

🎯 Visual scoring system:

🟥 0–1 = Weak

🟨 2 = Neutral

🟩 4 = Strong (all metrics above average)

🎛️ Toggle visibility of each yield independently

🧮 Fully compatible with other Greer Financial Toolkit indicators

🛠 Ideal For

Long-term value investors

Dividend and cash-flow-focused investors

Analysts seeking clean yield visualizations

Greer Toolkit users combining with Greer Value and BuyZone

Greer Free Cash Flow Yield✅ Title

Greer Free Cash Flow Yield (FCF%) — Long-Term Value Signal

📝 Description

The Greer Free Cash Flow Yield indicator is part of the Greer Financial Toolkit, designed to help long-term investors identify fundamentally strong and potentially undervalued companies.

📊 What It Does

Calculates Free Cash Flow Per Share (FY) from official financial reports

Divides by the current stock price to produce Free Cash Flow Yield %

Tracks a static average across all available financial years

Color-codes the yield line:

🟩 Green when above average (stronger value signal)

🟥 Red when below average (weaker value signal)

💼 Why It Matters

FCF Yield is a powerful metric that reveals how efficiently a company turns revenue into usable cash. This can be a better long-term value indicator than earnings yield or P/E ratios, especially in capital-intensive industries.

✅ Best used in combination with:

📘 Greer Value (fundamental growth score)

🟢 Greer BuyZone (technical buy zone detection)

🔍 Designed for:

Fundamental investors

Value screeners

Dividend and FCF-focused strategies

📌 This tool is for informational and educational use only. Always do your own research before investing.

Discount to Net Asset ValueOverview

This indicator helps investors and analysts identify when a company’s stock is trading below or above its intrinsic value. A persistent discount may highlight potential value opportunities, while a sustained premium could signal overvaluation or strong market sentiment. By visually shading the background and plotting the discount/premium percentage, users can quickly screen for undervalued stocks, confirm fundamental research, and make more informed buy or sell decisions.

Usage

Calculates the Net Asset Value discount (or premium) for any symbol.

By default the indicator uses the current chart symbol’s TOTAL_ASSETS, TOTAL_LIABILITIES, and TOTAL_SHARES_OUTSTANDING.

You can select another symbol by checking “Use Custom Symbol” and entering the ticker of the other symbol. This is useful for comparing the Discount to NAV across symbols.

Shows the percentage discount (or premium) of market capitalization relative to net asset value.

Recommended timeframes: daily bars or higher.

Reporting Periods:

• FQ = Fiscal Quarter

• FY = Fiscal Year

• TTM = Trailing Twelve Months

Note: NAV is pulled on the chosen reporting period (FQ, FY, TTM).

By default the background is shaded red to illustrate a discount to NAV and green to illustrate a premium to NAV. This can be toggled in the settings.

Futures vs CFD Price Display

🎯 Trading the same asset in CFDs and Futures but tired of switching charts to compare prices? This is your indicator!

Stop the constant chart hopping! This live price comparison shows you instantly where the better conditions are.

✨ What you get:

Bidirectional: Works in both Futures AND CFD charts

Live prices: Real-time comparison of both markets

Spread calculation: Automatic difference in points and percentage

Fully customizable: Colors, position, size to your liking

Professional design: Clean display with symbol header

🎯 Perfect for:

Gold traders (Futures vs CFD)

Arbitrage strategies

Spread monitoring

Multi-broker comparisons

⚙️ Customization:

3 sizes (Small/Normal/Large) for all screens

4 positions available

Individual color schemes

Toggle features on/off

💡 Simply enter the symbol and keep both markets in sight!

Notice: "Co-developed with Claude AI (Anthropic) - because even AI needs to pay the server bills! 😄"

GCM Centre Line Candle MarkerGCM Centre Line Candle Marker (GCM-CLCM) - Descriptive Notes

Indicator Overview:

The "GCM Centre Line Candle Marker" is a versatile TradingView overlay indicator designed to enhance chart analysis by drawing short horizontal lines at user-defined "centre" points of candles. These lines provide a quick visual reference to key price levels within each candle, such as midpoints, open, close, or typical prices. The indicator offers extensive customization for line appearance, positioning, and conditional display, including an option to highlight only bullish engulfing patterns.

Key Features:

1. Customizable Line Position:

o Users can choose from various methods to calculate the "centre" price for the line:

(High + Low) / 2 (Default)

(Open + Close) / 2

Close

Open

(Open + High + Low + Close) / 4 (HLCO/4)

(Open + High + Close) / 3 (Typical Price HLC/3 variation)

(Open + Close + Low) / 3 (Typical Price OCL/3 variation)

2. Line Appearance Customization:

o Visibility: Toggle lines on/off.

o Style: Solid, dotted, or dashed lines.

o Width: Adjustable line thickness (1 to 5).

o Length: Defines how many candles forward the line extends (1 to 10).

o Color: Lines are colored based on candle type (bullish/bearish), with user-selectable base colors.

o Dynamic Opacity: Line opacity is dynamically adjusted based on the candle's size relative to recent candles. Larger candles produce more opaque lines (up to the user-defined maximum opacity), while smaller candles result in more transparent lines. This helps significant candles stand out.

3. Price Labels:

o Show Labels: Option to display price labels at the end of each center line.

o Label Background Color: Customizable.

o Dynamic Text Color: Label text color can change based on the movement of the center price:

Green: Current center price is higher than the previous.

Red: Current center price is lower than the previous.

Gray: No change or first label.

o Static Text Color: Alternatively, a fixed color can be used for all labels.

4. Conditional Drawing - Bullish Engulfing Filter:

o Users can enable an option to Only Show Bullish Engulfing Candles. When active, center lines will only be drawn for candles that meet bullish engulfing criteria (current bull candle's body engulfs the previous bear candle's body).

5. Performance Management:

o Max Lines to Show: Limits the number of historical lines displayed on the chart to maintain clarity and performance. Older lines are automatically removed as new ones are drawn.

6. Alert Condition:

o Includes a built-in alert: Big Bullish Candle. This alert triggers when a bullish candle's range (high - low) is greater than the 20-period simple moving average (SMA) of candle ranges.

How It Works:

• For each new candle, the script calculates the "center" price based on the user's Line Position selection.

• If showLines is enabled and (if applicable) the bullish engulfing condition is met, a new line is drawn from the current candle's bar_index at the calculated _center price, extending lineLength candles forward.

• The line's color is determined by whether the candle is bullish (close > open) or bearish (close < open).

• Opacity is calculated dynamically: scaledOpacity = int((100 - maxUserOpacity) * (1 - dynamicFactor) + maxUserOpacity), where dynamicFactor is candleSize / maxSize (current candle size relative to the max size in the last 20 candles). This means maxUserOpacity is the least transparent the line will be (for the largest candles), and smaller candles will have lines approaching full transparency.

• Optional price labels are added at the end of these lines.

• The script manages an array of drawn lines, removing the oldest ones if the maxLines limit is exceeded.

Potential Use Cases:

• Visualizing Intra-Candle Levels: Quickly see midpoints or other key price points without manual drawing.

• Short-Term Reference Points: The extended lines can act as very short-term dynamic support/resistance or points of interest.

• Pattern Recognition: Highlight bullish engulfing patterns or simply emphasize candles based on their calculated center.

• Volatility Indication: The dynamic opacity can subtly indicate periods of larger or smaller candle ranges.

• Confirmation Tool: Use in conjunction with other indicators or trading strategies.

User Input Groups:

• Line Settings: Controls all aspects of the line's appearance and calculation.

• Label Settings: Manages the display and appearance of price labels.

• Other Settings: Contains options for line management and conditional filtering (like Bullish Engulfing).

This indicator provides a clean and customizable way to mark significant price levels within candles, aiding traders in their technical analysis.

FVG Candle HighlighterThis indicator highlights only the true Fair Value Gap (FVG) creator candle — the middle candle in a 3-bar FVG formation — with zero clutter.

🔹 Bullish FVG: Candle is colored if price gaps above the high two bars back

🔹 Bearish FVG: Candle is colored if price gaps below the low two bars back

✨ No boxes. No zones. Just pure, visual price-action accuracy.

🔧 Powered by Pine Script v6

🧠 Based on institutional-style FVG logic

🎯 Ideal for Smart Money / ICT / Order Block strategies

QoQ PAT, Sales & OPM% Labels by GauravThis indicator automatically displays the Quarter-over-Quarter (QoQ) percentage change in Sales, PAT (Profit After Tax), and Operating Profit Margin (OPM%) directly on the price chart.

It fetches quarterly financial data using TradingView’s request.financial() function for:

Sales (TOTAL_REVENUE),

PAT (NET_INCOME),

Operating Profit (OPER_INCOME).

For each earnings update, it calculates:

Sales QoQ %: Growth in sales vs. the previous quarter,

PAT QoQ %: Growth in PAT vs. the previous quarter,

OPM %: Operating Profit Margin = (Operating Profit / Sales) × 100.

This helps traders and investors quickly visualize fundamental growth trends right alongside the candlestick chart, improving fundamental + technical analysis integration.