Debt-Cycle vs Bitcoin-CycleDebt-Cycle vs Bitcoin-Cycle Indicator

The Debt-Cycle vs Bitcoin-Cycle indicator is a macro-economic analysis tool that compares traditional financial market cycles (debt/credit cycles) against Bitcoin market cycles. It uses Z-score normalization to track the relative positioning of global financial conditions versus cryptocurrency market sentiment, helping identify potential turning points and divergences between traditional finance and digital assets.

Key Features

Dual-Cycle Analysis: Simultaneously tracks traditional financial cycles and Bitcoin-specific cycles

Z-Score Normalization: Standardizes diverse data sources for meaningful comparison

Multi-Asset Coverage: Analyzes currencies, commodities, bonds, monetary aggregates, and on-chain metrics

Divergence Detection: Identifies when Bitcoin cycles move independently from traditional finance

21-Day Timeframe: Optimized for Long-term cycle analysis

What It Measures

Finance-Cycle (White Line)

Tracks traditional financial market health through:

Currencies: USD strength (DXY), global currency weights (USDWCU, EURWCU)

Commodities: Oil, gold, natural gas, agricultural products, and Bitcoin price

Corporate Bonds: Investment-grade spreads, high-yield spreads, credit conditions

Monetary Aggregates: M2 money supply, foreign exchange reserves (weighted by currency)

Treasury Bonds: Yield curve (2Y/10Y, 3M/10Y), term premiums, long-term rates

Bitcoin-Cycle (Orange Line)

Tracks Bitcoin market positioning through:

On-Chain Metrics:

MVRV Ratio (Market Value to Realized Value)

NUPL (Net Unrealized Profit/Loss)

Profit/Loss Address Distribution

Technical Indicators:

Bitcoin price Z-score

Moving average deviation

Relative Strength:

ETH/BTC ratio (altcoin strength indicator)

Visual Elements

White Line: Finance-Cycle indicator (positive = expansionary conditions, negative = contractionary)

Orange Line: Bitcoin-Cycle indicator (positive = bullish positioning, negative = bearish)

Zero Line: Neutral reference point

Interpretation

Cycle Alignment

Both positive: Risk-on environment, favorable for crypto

Both negative: Risk-off environment, caution warranted

Divergence: Potential opportunities or warning signals

Divergence Signals

Finance positive, Bitcoin negative: Bitcoin may be undervalued relative to macro conditions

Finance negative, Bitcoin positive: Bitcoin may be overextended or decoupling from traditional finance

Important Limitations

This indicator uses some technical and macro data but still has significant gaps:

⚠️ Limited monetary data - missing:

Funding rates (repo, overnight markets)

Comprehensive bond spread analysis

Collateral velocity and quality metrics

Central bank balance sheet details

⚠️ Basic economic coverage - missing:

GDP growth rates

Inflation expectations

Employment data

Manufacturing indices

Consumer confidence

⚠️ Simplified on-chain analysis - missing:

Exchange flow data

Whale wallet movements

Mining difficulty adjustments

Hash rate trends

Network fee dynamics

⚠️ No sentiment data - missing:

Fear & Greed Index

Options positioning

Futures open interest

Social media sentiment

The indicator provides a high-level cycle comparison but should be combined with comprehensive fundamental analysis, detailed on-chain research, and proper risk management.

Settings

Offset: Adjust the horizontal positioning of the indicators (default: 0)

Timeframe: Fixed at 21 days for optimal cycle detection

Use Cases

Macro-crypto correlation analysis: Understand when Bitcoin moves with or against traditional markets

Cycle timing: Identify potential tops and bottoms in both cycles

Risk assessment: Gauge overall market conditions across asset classes

Divergence trading: Spot opportunities when cycles diverge significantly

Portfolio allocation: Balance traditional and crypto assets based on cycle positioning

Technical Notes

Uses Z-score normalization with varying lookback periods (40-60 bars)

Applies HMA (Hull Moving Average) smoothing to reduce noise

Asymmetric multipliers for upside/downside movements in certain metrics

Requires access to FRED economic data, Glassnode, CoinMetrics, and IntoTheBlock feeds

21-day timeframe optimized for cycle analysis

Strategy Applications

This indicator is particularly useful for:

Cross-asset allocation - Decide between traditional finance and crypto exposure

Cycle positioning - Identify where we are in credit/debt cycles vs. Bitcoin cycles

Regime changes - Detect shifts in market leadership and correlation patterns

Risk management - Reduce exposure when both cycles turn negative

Disclaimer: This indicator is a cycle analysis tool and should not be used as the sole basis for investment decisions. It has limited coverage of monetary conditions, economic fundamentals, and on-chain metrics. The indicator provides directional insight but cannot predict exact timing or magnitude of market moves. Always conduct thorough research, consider multiple data sources, and maintain proper risk management in all investment decisions.

Statistics

Market Sentiment [NeuraAlgo]

Market Sentiment

This indicator provides a real-time view of market momentum and sentiment by analyzing bullish and bearish impulses using price and volatility-based calculations. It visualizes trends on the chart and offers a dashboard with key statistics.

1.Status Calculation

The Status measures bullish momentum by identifying strong upward impulses.

Equation:

Status Source = Average of lows where(Low - High ) > ATR

For each bar, it checks if the current low minus the high from two bars ago exceeds the Average True Range (ATR) .

All lows that satisfy this condition are collected.

The average of these lows forms the Status Source , representing the level of strong buying pressure.

This helps traders visualize where significant bullish activity is concentrated and gauge upward momentum.

2.Status Source Calculation

Similarly, bearish impulses are detected by checking if highs fall below lows from two bars ago beyond ATR thresholds. The corresponding levels form the reference for selling pressure.

3. Trend Strength and States

Strength is Quantifies how far the price is from bullish or bearish reference levels as a percentage.

Trend States

Stability Phase (Gray): Market is quiet, minimal momentum.

Positive Flow (Green): Bullish pressure dominates; buyers are in control.

Negative Flow (Red): Bearish pressure dominates; sellers lead.

State Transition: Market is shifting; momentum is building.

4. Visuals

Bar colors indicate trend state: green for bullish, red for bearish, gray for neutral.

Filled zones highlight bullish and bearish reference levels for intuitive trend analysis.

5. Dashboard

An optional dashboard displays:

Sentiment: Visual gradient representing bullish or bearish dominance.

Status: Current trend state in concise, human-readable terms.

6. Purpose:

This indicator is designed to identify the current market status and the behavior of the asset by analyzing bullish and bearish impulses. It helps traders understand whether the market shows signs of stability, growth, or decline based on the asset’s price action and volatility.

Understand the asset behavior

Healthy asset behavior

Weak asset behavior

Market Sentiment combines price action, ATR-based volatility, and impulse tracking to provide a clear and actionable view of market conditions. The BullLine equation ensures that only meaningful bullish moves are highlighted, giving traders a reliable reference for momentum and potential entry points.

2s10s Bull/Bear Steepener/Flattener (Intraday bars)A simple indicator that tracks the curve of the US2y and US10y

Spot-derivatives divergenceThe indicator works only on the spot chart, provided that there is a derivative of the same asset on the same exchange.

The white line represents the derivative chart.

The blue line represents the spot chart.

The purple icon indicates that there is a price divergence.

It is possible to create alerts for a list of coins.

Important! Before simultaneously buying the asset on the spot market and opening a short position on derivatives, make sure that the funding rate is positive.

Z-Score IndicatorThis script calculates the Z-Score to measure how many standard deviations the current price is from its mean (SMA). It is a classic tool for identifying statistical extremes and mean reversion opportunities.

Formula Z = (Close - Mean) / Standard Deviation

Visual Guide

Blue Line: The Z-Score value.

Red Dotted Lines (+/- 2): Statistical extremes.

> 2: Potentially Overbought.

< -2: Potentially Oversold.

Grey Dotted Line (0): The mean (fair value).

Settings

Lookback Period: Default is 30. Adjust to change sensitivity.

Highlight TimeHighlight Time shades the chart background during user‑defined hours. Choose start/end times and a time zone to visually mark key trading windows like the spread hour.

𝙐𝙡𝙩𝙧𝙖 𝘼𝙡𝙜𝙤Ultra Algo एक multi-layer trend analysis system है जो price behavior, range expansion और trend flow ko combine करके साफ़ और structured market indications प्रदान करता है।

इसका उद्देश्य chart को simplify करके traders ko directional clarity aur disciplined analysis में मदद देना है।

Core Features

Trend direction aur strength identify करने वाला dynamic filter

Structured rules par आधारित automatic long/short indications

Pre-defined levels par आधारित take-profit markers

ATR logic par बना हुआ risk reference framework

Coral-based visual trend component jo market flow को smooth तरीके से दिखाता है

Use Case

यह system short-term से mid-term analysis tak किसी भी trading style के साथ उपयोग किया जा सकता है।

Script ka उद्देश्य:

✔ clearer structure

✔ reduced chart noise

✔ disciplined analysis

✔ better trend visibility

provide करना है ताकि user market movement ko zyada organized तरीके से समझ सके।

Important Note

Yeh tool discretionary decision-making ko replace nahi karta, balki chart-reading ko structured banane mein madad karta hai.

포지션 계산기이 지표는 트레이더가 설정한 리스크에 맞춰 **적정 진입금액(포지션 사이즈)**을 자동으로 계산해주는 도구입니다.

사용자가 입력하는 값:

레버리지

손절 거리(%)

손실 허용 금액($)

위 세 가지를 입력하면,

지표가 즉시 현재 리스크에 맞는 진입금액을 계산해 표시해줍니다.

복잡한 계산 없이 차트 상에서 바로 포지션 크기를 산출할 수 있어,

리스크 관리의 일관성을 유지하는 데 매우 유용합니다.

주요 기능

직관적인 UI로 빠른 값 조정 가능

실시간 진입금액(포지션 사이즈) 계산

선물·마진·레버리지 거래에 모두 활용 가능

고정 손실금 기반 전략(Risk Fixed Dollar)에 최적화

이 계산기를 사용하면,

시장 변동성과 무관하게 항상 동일한 리스크로 거래 진입이 가능합니다.

----------------------------------------------------------------------------------------------------------

Position Calculator – Entry Size Based on Risk

This indicator helps traders automatically calculate the optimal entry amount based on their predefined risk parameters.

Simply input:

Leverage

Stop Distance (%)

Loss Amount ($)

The script instantly returns the required entry size to match your risk level.

It helps maintain consistent risk management and prevents oversizing positions during volatile market conditions.

Key Features

Clean, minimal UI for quick adjustments

Real-time calculation of position size

Suitable for futures, margin, and leveraged trading

Ideal for traders who use fixed-dollar risk per trade

This tool ensures you always enter with the correct size—no external calculator needed.

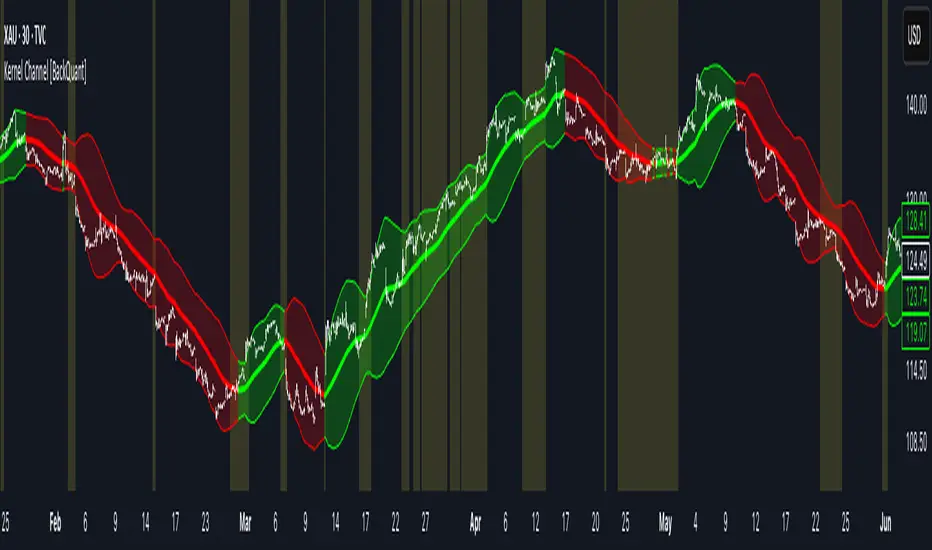

Kernel Channel [BackQuant]Kernel Channel

A non-parametric, kernel-weighted trend channel that adapts to local structure, smooths noise without lagging like moving averages, and highlights volatility compressions, expansions, and directional bias through a flexible choice of kernels, band types, and squeeze logic.

What this is

This indicator builds a full trend channel using kernel regression rather than classical averaging. Instead of a simple moving average or exponential weighting, the midline is computed as a kernel-weighted expectation of past values. This allows it to adapt to local shape, give more weight to nearby bars, and reduce distortion from outliers.

You can think of it as a sliding local smoother where you define both the “window” of influence (Window Length) and the “locality strength” (Bandwidth). The result is a flexible midline with optional upper and lower bands derived from kernel-weighted ATR or kernel-weighted standard deviation, letting you visualize volatility in a structurally consistent way.

Three plotting modes help demonstrate this difference:

When the midline is shown alone, you get a smooth, adaptive baseline that behaves almost like a regression moving average, as shown in this view:

When full channels are enabled, you see how standard deviation reacts to local structure with dynamically widening and tightening bands, a mode illustrated here:

When ATR mode is chosen instead of StdDev, band width reflects breadth of movement rather than variance, creating a volatility-aware envelope like the example here:

Why kernels

Classical moving averages allocate fixed weights. Kernels let the user define weighting shape:

Epanechnikov — emphasizes bars near the current bar, fades fast, stable and smooth.

Triangular — linear decay, simple and responsive.

Laplacian — exponential decay from the current point, sharper reactivity.

Cosine — gentle periodic decay, balanced smoothness for trend filters.

Using these in combination with a bandwidth parameter gives fine control over smoothness vs responsiveness. Smaller bandwidths give sharper local sensitivity, larger bandwidths give smoother curvature.

How it works (core logic)

The indicator computes three building blocks:

1) Kernel-weighted midline

For every bar, a sliding window looks back Window Length bars. Each bar in this window receives a kernel weight depending on:

its index distance from the present

the chosen kernel shape

the bandwidth parameter (locality)

Weights form the denominator, weighted values form the numerator, and the resulting ratio is the kernel regression mean. This midline is the central trend.

2) Kernel-based width

You choose one of two band types:

Kernel ATR — ATR values are kernel-averaged, producing a smooth, volatility-based width that is not dependent on variance. Ideal for directional trend channels and regime separation.

Kernel StdDev — local variance around the midline is computed through kernel weighting. This produces a true statistical envelope that narrows in quiet periods and widens in noisy areas.

Width is scaled using Band Multiplier , controlling how far the envelope extends.

3) Upper and lower channels

Provided midline and width exist, the channel edges are:

Upper = midline + bandMult × width

Lower = midline − bandMult × width

These create smooth structures around price that adapt continuously.

Plotting modes

The indicator supports multiple visual styles depending on what you want to emphasize.

When only the midline is displayed, you get a pure kernel trend: a smooth regression-like curve that reacts to local structure while filtering noise, demonstrated here: This provides a clean read on direction and slope.

With full channels enabled, the behavior of the bands becomes visible. Standard deviation mode creates elastic boundaries that tighten during compressions and widen during turbulence, which you can see in the band-focused demonstration: This helps identify expansion events, volatility clusters, and breakouts.

ATR mode shifts interpretation from statistical variance to raw movement amplitude. This makes channels less sensitive to outliers and more consistent across trend phases, as shown in this ATR variation example: This mode is particularly useful for breakout systems and bar-range regimes.

Regime detection and bar coloring

The slope of the midline defines directional bias:

Up-slope → green

Down-slope → red

Flat → gray

A secondary regime filter compares close to the channel:

Trend Up Strong — close above upper band and midline rising.

Trend Down Strong — close below lower band and midline falling.

Trend Up Weak — close between midline and upper band with rising slope.

Trend Down Weak — close between lower band and midline with falling slope.

Compression mode — squeeze conditions.

Bar coloring is optional and can be toggled for cleaner charts.

Squeeze logic

The indicator includes non-standard squeeze detection based on relative width , defined as:

width / |midline|

This gives a dimensionless measure of how “tight” or “loose” the channel is, normalized for trend level.

A rolling window evaluates the percentile rank of current width relative to past behavior. If the width is in the lowest X% of its last N observations, the script flags a squeeze environment. This highlights compression regions that may precede breakouts or regime shifts.

Deviation highlighting

When using Kernel StdDev mode, you may enable deviation flags that highlight bars where price moves outside the channel:

Above upper band → bullish momentum overextension

Below lower band → bearish momentum overextension

This is turned off in ATR mode because ATR widths do not represent distributional variance.

Alerts included

Kernel Channel Long — midline turns up.

Kernel Channel Short — midline turns down.

Price Crossed Midline — crossover or crossunder of the midline.

Price Above Upper — early momentum expansion.

Price Below Lower — downward volatility expansion.

These help automate regime changes and breakout detection.

How to use it

Trend identification

The midline acts as a bias filter. Rising midline means trend strength upward, falling midline means downward behavior. The channel width contextualizes confidence.

Breakout anticipation

Kernel StdDev compressions highlight areas where price is coiling. Breakouts often follow narrow relative width. ATR mode provides structural expansion cues that are smooth and robust.

Mean reversion

StdDev mode is suitable for fade setups. Moves to outer bands during low volatility often revert to the midline.

Continuation logic

If price breaks above the upper band while midline is rising, the indicator flags strong directional expansion. Same logic for breakdowns on the lower band.

Volatility characterization

Kernel ATR maps raw bar movements and is excellent for identifying regime shifts in markets where variance is unstable.

Tuning guidance

For smoother long-term trend tracking

Larger window (150–300).

Moderate bandwidth (1.0–2.0).

Epanechnikov or Cosine kernel.

ATR mode for stable envelopes.

For swing trading / short-term structure

Window length around 50–100.

Bandwidth 0.6–1.2.

Triangular for speed, Laplacian for sharper reactions.

StdDev bands for precise volatility compression.

For breakout systems

Smaller bandwidth for sharp local detection.

ATR mode for stable envelopes.

Enable squeeze highlighting for identifying setups early.

For mean-reversion systems

Use StdDev bands.

Moderate window length.

Highlight deviations to locate overextended bars.

Settings overview

Kernel Settings

Source

Window Length

Bandwidth

Kernel Type (Epanechnikov, Triangular, Laplacian, Cosine)

Channel Width

Band Type (Kernel ATR or Kernel StdDev)

Band Multiplier

Visuals

Show Bands

Color Bars By Regime

Highlight Squeeze Periods

Highlight Deviation

Lookback and Percentile settings

Colors for uptrend, downtrend, squeeze, flat

Trading applications

Trend filtering — trade only in direction of the midline slope.

Breakout confirmation — expansion outside the bands while slope agrees.

Squeeze timing — compression periods often precede the next directional leg.

Volatility-aware stops — ATR mode makes channel edges suitable for adaptive stop placement.

Structural swing mapping — StdDev bands help locate midline pullbacks vs distributional extremes.

Bias rotation — bar coloring highlights when regime shifts occur.

Notes

The Kernel Channel is not a signal generator by itself, but a structural map. It helps classify trend direction, volatility environment, distribution shape, and compression cycles. Combine it with your entry and exit framework, risk parameters, and higher-timeframe confirmation.

It is designed to behave consistently across markets, to avoid the bluntness of classical averages, and to reveal subtle curvature in price that traditional channels miss. Adjust kernel type, bandwidth, and band source to match the noise profile of your instrument, then use squeeze logic and deviation highlighting to guide timing.

Indices ALN SessionsIndices ALN Sessions - Pattern Analysis with Historical Probabilities

Overview

This indicator analyzes overnight trading patterns across Asia, London, and New York sessions for major index futures (NQ, ES, YM), providing real-time probability analysis based on 15 years of historical data (2010-2025).

Pattern Detection Methodology

The indicator detects four distinct overnight patterns by comparing session high/low relationships:

1. London Engulfs Asia

Condition: London High > Asia High AND London Low < Asia Low

Interpretation: London session completely engulfed the Asia range

2. Asia Engulfs London

Condition: Asia High > London High AND Asia Low < London Low

Interpretation: London session remained within Asia's range

3. London Partial Up

Condition: London High > Asia High AND London Low ≥ Asia Low

Interpretation: London broke Asia high but not its low

4. London Partial Down

Condition: London Low < Asia Low AND London High ≤ Asia High

Interpretation: London broke Asia low but not the high

Probability Calculation

Probabilities are derived from historical analysis of 1-minute price data spanning 2010-2025 across all three indices. The system tracks:

Primary Targets: Most likely level to be taken during NY session based on pattern

Secondary Targets: Second most likely level

Asia Targets: Probability of reaching untouched Asia levels (for partial patterns)

Engulfment Probability: Likelihood of NY session taking all four levels

Day-of-Week Specificity

Each pattern has unique probability profiles for Monday through Friday, as market behavior varies significantly by day. The indicator automatically selects the appropriate probability set based on the current trading day.

Conditional Probability Logic

The indicator dynamically adjusts probabilities as levels are taken during the NY session:

When the Primary target is taken first → Shows conditional probability for Secondary target

When Secondary is taken before Primary → Adjusts Primary probability based on historical sequences

Real-time tracking shows which levels have been hit with checkmark confirmations

How Probabilities Were Derived

Data was collected from 15 years of 1-minute futures data for NQ, ES, and YM. For each trading day:

Asia session high/low recorded (8:00 PM - 2:00 AM EST)

London session high/low recorded (2:00 AM - 8:00 AM EST)

Pattern type classified

NY session behavior tracked (8:00 AM - 4:00 PM EST)

Level breaks recorded with sequence order

Statistical frequencies calculated by pattern, day, and instrument

Sample sizes vary but typically include 200-500+ occurrences per pattern/day combination over the 15-year period.

Visual Components

Session Boxes: Color-coded rectangles showing Asia (Yellow), London (Blue), and NY (Red) sessions with their high/low ranges.

Pivot Lines: Horizontal lines marking session highs and lows that extend until broken or until the drawing cutoff time.

Pattern Labels: Automatic labeling at NY open identifying which of the four patterns has formed.

Probability Table: Real-time table showing:

Current pattern type

Instrument type (NQ/ES/YM) and day of week

Sample size (when using dynamic stats)

Primary, Secondary, and Asia target probabilities

Engulfment probability

Live confirmations as levels are taken

Color Coding:

Green background: 70%+ probability

Lime: 50-70% probability

Orange: 30-50% probability

Red: Confirmed (level taken)

Settings & Inputs

Historical Stats

Instrument Type: Select NQ, ES, or YM (each has unique probability data)

Use Dynamic Stats: Toggle between historical probabilities and live collection mode

Sessions:

Customizable session times (default: Asia 8PM-2AM, London 2AM-8AM, NY 8AM-4PM EST)

Session box transparency and colors

Toggle session boxes and text on/off

Pivots:

Show/hide pivot lines and labels

Extend pivots until mitigated or past mitigation

Alert when pivots are broken

Midpoint display option

Probabilities:

Show/hide probability table

Table position and size customization

Pattern label display toggle

Opening Prices:

Optional horizontal lines at key times (midnight,18:00, 09:30, etc.)

How to Use:

Apply to 5-minute chart of NQ, ES, or YM futures

Select your instrument in settings to match the chart

Wait for NY session open - Pattern will be identified and probabilities displayed

Monitor the probability table - Primary targets show highest probability levels

Watch for confirmations - Checkmarks appear as levels are taken

Note conditional updates - Probabilities adjust based on which level breaks first

Trading Applications:

Directional bias: High probability targets suggest likely NY session movement

Level awareness: Know which session highs/lows are most likely to be tested

Risk management: Lower probability scenarios may warrant tighter stops

Sequence planning: Conditional probabilities help anticipate multi-level moves

What Makes This Different:

Unlike standard session indicators that only display ranges, this tool:

Classifies specific overnight pattern formations:

Provides quantified probabilities based on extensive historical analysis

Updates in real-time with conditional logic as the session develops

Distinguishes between different indices (NQ/ES/YM) and days of week

Tracks level-break sequences, not just final outcomes

Notes:

Probabilities are based on historical frequencies and do not guarantee future results

Best used on 1, 5, and 15-minute timeframes for optimal session visualization

Works on continuous futures contracts or /NQ, /ES, /YM symbols

Alt Trading: FuturesOne

The FuturesOne Indicator + Strategy will be continuously enhanced to ensure our users receive the most effective and profit-focused trading system at the best possible value. Version 0 (V0) of the FuturesOne Strategy is built on a refined Opening Range Breakout (ORB) framework, augmented with a quantitative regime-detection and filtering layer. This design allows users to tailor their approach: they may opt for consistent daily ORB opportunities or select a mode that applies quantitative filters to surface fewer, but higher-probability, trade setups.

STRATEGY 1 │ Red Dragon │ Model 1 │ Pro │ [Titans_Invest]The Red Dragon Model 1 is a fully automated trading strategy designed to operate BTC/USDT.P on the 4-hour chart with precision, stability, and consistency. It was built to deliver reliable behavior even during strong market movements, maintaining operational discipline and avoiding abrupt variations that could interfere with the trader’s decision-making.

Its core is based on a professionally engineered logical structure that combines trend filters, confirmation criteria, and balanced risk management. Every component was designed to work in an integrated way, eliminating noise, avoiding unnecessary trades, and protecting capital in critical moments. There are no secret mechanisms or hidden logic: everything is built to be objective, clean, and efficient.

Even though it is based on professional quantitative engineering, Red Dragon Model 1 remains extremely simple to operate. All logic is clearly displayed and fully accessible within TradingView itself, making it easy to understand for both beginners and experienced traders. The structure is organized so that any user can quickly view entry conditions, exit criteria, additional filters, adjustable parameters, and the full mechanics behind the strategy’s behavior.

In addition, the architecture was built to minimize unnecessary complexity. Parameters are straightforward, intuitive, and operate in a balanced way without requiring deep adjustments or advanced knowledge. Traders have full freedom to analyze the strategy, understand the logic, and make personal adaptations if desired—always with total transparency inside TradingView.

The strategy was also designed to deliver consistent operational behavior over the long term. Its confirmation criteria reduce impulsive trades; its filters isolate noise; and its overall logic prioritizes high-quality entries in structured market movements. The goal is to provide a stable, clear, and repeatable flow—essential characteristics for any medium-term quantitative approach.

Combining clarity, professional structure, and ease of use, Red Dragon Model 1 offers a solid foundation both for users who want a ready-to-use automated strategy and for those looking to study quantitative models in greater depth.

This entire project was built with extreme dedication, backed by more than 14,000 hours of hands-on experience in Pine Script, continuously refining patterns, techniques, and structures until reaching its current level of maturity. Every line of code reflects this long process of improvement, resulting in a strategy that unites professional engineering, transparency, accessibility, and reliable execution.

🔶 MAIN FEATURES

• Fully automated and robust: Operates without manual intervention, ideal for traders seeking consistency and stability. It delivers reliable performance even in volatile markets thanks to the solid quantitative engineering behind the system.

• Multiple layers of confirmation: Combines 10 key technical indicators with 15 adaptive filters to avoid false signals. It only triggers entries when all trend, market strength, and contextual criteria align.

• Configurable and adaptable filters: Each of the 15 filters can be enabled, disabled, or adjusted by the user, allowing the creation of personalized statistical models for different assets and timeframes. This flexibility gives full freedom to optimize the strategy according to individual preferences.

• Clear and accessible logic: All entry and exit conditions are explicitly shown within the TradingView parameters. The strategy has no hidden components—any user can quickly analyze and understand each part of the system.

• Integrated exclusive tools: Includes complete backtest tables (desktop and mobile versions) with annualized statistics, along with real-time entry conditions displayed directly on the chart. These tools help monitor the strategy across devices and track performance and risk metrics.

• No repaint: All signals are static and do not change after being plotted. This ensures the trader can trust every entry shown without worrying about indicators rewriting past values.

🔷 ENTRY CONDITIONS & RISK MANAGEMENT

Red Dragon Model 1 triggers buy (long) or sell (short) signals only when all configured conditions are satisfied. For example:

• Volume:

• The system only trades when current volume exceeds the volume moving average multiplied by a user-defined factor, indicating meaningful market participation.

• RSI:

• Confirms bullish bias when RSI crosses above its moving average, and bearish bias when crossing below.

• ADX:

• Enters long when +DI is above –DI with ADX above a defined threshold, indicating directional strength to the upside (and the opposite conditions for shorts).

• Other indicators (MACD, SAR, Ichimoku, Support/Resistance, etc.)

Each one must confirm the expected direction before a final signal is allowed.

When all bullish criteria are met simultaneously, the system enters Long; when all criteria indicate a bearish environment, the system enters Short.

In addition, the strategy uses fixed Take Profit and Stop Loss targets for risk control:

Currently: TP around 1.5% and SL around 2.0% per trade, ensuring consistent and transparent risk management on every position.

⚙️ INDICATORS

__________________________________________________________

1) 🔊 Volume: Avoids trading on flat charts.

2) 🍟 MACD: Tracks momentum through moving averages.

3) 🧲 RSI: Indicates overbought or oversold conditions.

4) 🅰️ ADX: Measures trend strength and potential entry points.

5) 🥊 SAR: Identifies changes in price direction.

6) ☁️ Cloud: Accurately detects changes in market trends.

7) 🌡️ R/F: Improves trend visualization and helps avoid pitfalls.

8) 📐 S/R: Fixed support and resistance levels.

9)╭╯MA: Moving Averages.

10) 🔮 LR: Forecasting using Linear Regression.

__________________________________________________________

🟢 ENTRY CONDITIONS 🔴

__________________________________________________________

IF all conditions are 🟢 = 📈 Long

IF all conditions are 🔴 = 📉 Short

__________________________________________________________

🚨 CURRENT TRIGGER SIGNAL 🚨

__________________________________________________________

🔊 Volume

🟢 LONG = (volume) > (MA_volume) * (Volume Mult)

🔴 SHORT = (volume) > (MA_volume) * (Volume Mult)

🧲 RSI

🟢 LONG = (RSI) > (RSI_MA)

🔴 SHORT = (RSI) < (RSI_MA)

🟢 ALL ENTRY CONDITIONS AVAILABLE 🔴

__________________________________________________________

🔊 Volume

🟢 LONG = (volume) > (MA_volume) * (Volume Mult)

🔴 SHORT = (volume) > (MA_volume) * (Volume Mult)

🔊 Volume

🟢 LONG = (volume) > (MA_volume) * (Volume Mult) and (close) > (open)

🔴 SHORT = (volume) > (MA_volume) * (Volume Mult) and (close) < (open)

🍟 MACD

🟢 LONG = (MACD) > (Signal Smoothing)

🔴 SHORT = (MACD) < (Signal Smoothing)

🧲 RSI

🟢 LONG = (RSI) < (Upper)

🔴 SHORT = (RSI) > (Lower)

🧲 RSI

🟢 LONG = (RSI) > (RSI_MA)

🔴 SHORT = (RSI) < (RSI_MA)

🅰️ ADX

🟢 LONG = (+DI) > (-DI) and (ADX) > (Treshold)

🔴 SHORT = (+DI) < (-DI) and (ADX) > (Treshold)

🥊 SAR

🟢 LONG = (close) > (SAR)

🔴 SHORT = (close) < (SAR)

☁️ Cloud

🟢 LONG = (Cloud A) > (Cloud B)

🔴 SHORT = (Cloud A) < (Cloud B)

☁️ Cloud

🟢 LONG = (Kama) > (Kama )

🔴 SHORT = (Kama) < (Kama )

🌡️ R/F

🟢 LONG = (high) > (UP Range) and (upward) > (0)

🔴 SHORT = (low) < (DOWN Range) and (downward) > (0)

🌡️ R/F

🟢 LONG = (high) > (UP Range)

🔴 SHORT = (low) < (DOWN Range)

📐 S/R

🟢 LONG = (close) > (Resistance)

🔴 SHORT = (close) < (Support)

╭╯MA2️⃣

🟢 LONG = (Cyan Bar MA2️⃣)

🔴 SHORT = (Red Bar MA2️⃣)

╭╯MA2️⃣

🟢 LONG = (close) > (MA2️⃣)

🔴 SHORT = (close) < (MA2️⃣)

╭╯MA2️⃣

🟢 LONG = (Positive MA2️⃣)

🔴 SHORT = (Negative MA2️⃣)

__________________________________________________________

🎯 TP / SL 🛑

__________________________________________________________

🎯 TP: 1.5 %

🛑 SL: 2.0 %

__________________________________________________________

🪄 UNIQUE FEATURES OF THIS STRATEGY

____________________________________

1) 𝄜 Table Backtest for Mobile.

2) 𝄜 Table Backtest for Computer.

3) 𝄜 Table Backtest for Computer & Annual Performance.

4) 𝄜 Live Entry Conditions.

1) 𝄜 Table Backtest for Mobile.

2) 𝄜 Table Backtest for Computer.

3) 𝄜 Table Backtest for Computer & Annual Performance.

4) 𝄜 Live Entry Conditions.

_____________________________

𝄜 BACKTEST / PERFORMANCE 𝄜

_____________________________

• Net Profit: +634.47%, Maximum Drawdown: -18.44%.

🪙 PAIR / TIMEFRAME ⏳

🪙 PAIR: BINANCE:BTCUSDT.P

⏳ TIME: 4 hours (240m)

✅ ON ☑️ OFF

✅ LONG

✅ SHORT

🎯 TP / SL 🛑

🎯 TP: 1.5 (%)

🛑 SL: 2.0 (%)

⚙️ CAPITAL MANAGEMENT

💸 Initial Capital: 10000 $ (TradingView)

💲 Order Size: 10 % (Of Equity)

🚀 Leverage: 10 x (Exchange)

💩 Commission: 0.03 % (Exchange)

📆 BACKTEST

🗓️ Start: Setember 24, 2019

🗓️ End: November 21, 2025

🗓️ Days: 2250

🗓️ Yers: 6.17

🗓️ Bars: 13502

📊 PERFORMANCE

💲 Net Profit: + 63446.89 $

🟢 Net Profit: + 634.47 %

💲 DrawDown Maximum: - 10727.48 $

🔴 DrawDown Maximum: - 18.44 %

🟢 Total Closed Trades: 1042

🟡 Percent Profitable: 63.92 %

🟡 Profit Factor: 1.247

💲 Avg Trade: + 60.89 $

⏱️ Avg # Bars in Trades

🕯️ Avg # Bars: 4

⏳ Avg # Hrs: 15

✔️ Trades Winning: 666

❌ Trades Losing: 376

✔️ Maximum Consecutive Wins: 11

❌ Maximum Consecutive Losses: 7

📺 Live Performance : br.tradingview.com

• Use this strategy on the recommended pair and timeframe above to replicate the tested results.

• Feel free to experiment and explore other settings, assets, and timeframes.

CME Gap Tracker + Live StatisticsThis script automatically finds the gaps inherent in the time data of any given chart, and displays them in color-coated buckets of how long it takes for the close of the gap to get filled. Add it on any CME Futures chart on the daily, and it will find all the weekend gaps. Set your period to an hour, and it will find the intraday gaps. Also displays a statistical calculation for each bucket.

Larry Williams COT Analysis Enhanced [tradeviZion]Larry Williams COT Analysis Enhanced - Complete Description

📖 Introduction

Welcome to the Larry Williams COT Analysis Enhanced indicator. This comprehensive description explains every setting, feature, and capability of this advanced Commitments of Traders (COT) analysis tool.

This indicator implements Larry Williams' professional COT analysis methodology with enhanced features including statistical validation, combination analysis, and adaptive signal generation.

---

🎯 Quick Start

Add the indicator to your chart

The script will automatically detect your symbol's CFTC code and asset type

Review the main COT analysis table (displayed by default)

Customize settings based on your trading style

Review the Trading Edge & Signals section for signal information

---

⚙️ Settings Groups Overview

The indicator is organized into 9 logical groups of settings:

1. Core COT Settings - Data source and report configuration

2. Analysis Parameters - Calculation methods and lookback periods

3. Signal Generation - Buy/sell signals and trend weighting

4. Plot Display Settings - Visual customization of chart lines

5. Smoothing Settings - Data smoothing options

6. COT Proximity Index Settings - Price-based proxy indicator configuration

7. Common Table Settings - Shared table appearance

8. Main Table Display Settings - Main analysis table customization

9. Historical Comparison Settings - Historical data table configuration

---

📋 Group 1: Core COT Settings

COT Report Type

Options: Legacy | Disaggregated | Financial

What it is: Selects the type of COT report data to analyze.

Legacy - Traditional COT report format. Recommended for most users. Uses "Commercial Positions" and "Noncommercial Positions" metrics. Shows Commercial, Non-Commercial, and Small Speculator positions in the classic format.

Commercials: "Commercial Positions"

Speculators: "Noncommercial Positions"

Small Specs: "Nonreportable Positions"

Disaggregated - Separates managed money from other speculators. Uses different metrics than Legacy format.

Commercials: "Producer Merchant Positions"

Speculators: "Managed Money Positions"

Small Specs: "Nonreportable Positions"

Important: When using Disaggregated report type, the table will still show "Non-Comm" as the label, but the data displayed is actually " Managed Money Positions " (hedge funds and CTAs). The underlying data changes based on your report type selection, even though the table label remains "Non-Comm" for consistency.

Where you'll see this data:

📊 Current Positions section - The "Non-Comm" row shows Managed Money long, short, and net positions

📊 Open Interest Analysis section - "Non-Comm" net changes reflect Managed Money position changes

📈 Analysis section - "Non-Comm" percentile and LW Index values are calculated from Managed Money positions

Chart plots - The blue "Non-Commercial" line shows Managed Money net positions

Useful when you want to analyze hedge funds (Managed Money) separately from other large speculators. The "Commercial" row will show " Producer Merchant Positions " instead of general "Commercial Positions".

Financial - Designed for financial instruments (currencies, bonds, stock indices). Uses financial-specific metrics.

Commercials: "Dealer Positions"

Speculators: "Leveraged Funds Positions"

Small Specs: "Nonreportable Positions"

Important: When using Financial report type, the table will still show "Commercial" and "Non-Comm" as labels, but the data displayed is actually " Dealer Positions " (commercials) and " Leveraged Funds Positions " (speculators). The underlying data changes based on your report type selection.

Where you'll see this data:

📊 Current Positions section - "Commercial" row shows Dealer long/short/net, "Non-Comm" row shows Leveraged Funds positions

📊 Open Interest Analysis section - Net changes reflect Dealer and Leveraged Funds position changes

📈 Analysis section - Percentile and LW Index values are calculated from Dealer and Leveraged Funds positions

Chart plots - Lines show Dealer and Leveraged Funds net positions

Use this for currency futures, bond futures, and stock index futures.

Trading Use: Most traders use Legacy as it provides the most comprehensive view and works with all asset types. Switch to Disaggregated if you want to analyze managed money positions separately. Use Financial specifically for financial instruments (currencies, bonds, stock indices).

---

Include Options Data

Default: Off (false)

What it is: Toggles whether to include options positions in addition to futures positions.

Trading Use: Larry Williams observed no significant difference in COT analysis when including options data. Keep this disabled unless you specifically need options data. Most traders leave it off for cleaner analysis.

---

Auto-detect CFTC Code

Default: On (true)

What it is: Automatically finds the correct CFTC code for your symbol.

Trading Use: Keep this enabled unless you need a specific CFTC code. The script automatically detects codes for:

- Currency futures: CME:6E1! , CME:6B1! , CME:6J1!

- Stock index futures: CME_MINI:ES1! , CBOT_MINI:YM1! , CME_MINI:NQ1!

- Commodities: NYMEX:CL1! , COMEX:GC1! , CBOT:ZC1!

- And many more

Only disable if you're analyzing a symbol that requires a specific CFTC code not in the auto-detection database.

---

Manual CFTC Code

Default: Empty

What it is: Enter a specific CFTC code manually (e.g. for E-mini S&P 500). "13874+"

Trading Use: Only used when Auto-detect CFTC Code is disabled. Most users never need this setting.

---

📊 Group 2: Analysis Parameters

Display Mode

Options: COT Report | COT Index | COT Proximity Index

What it is: Controls what data is displayed on the chart and in the table.

COT Report - Shows raw position data (Long, Short, Net positions) plus analysis. Best for detailed analysis. Displays Commercial, Non-Commercial, Small Speculator, and Open Interest lines.

COT Index - Shows index values based on your selected Analysis Method (Percentile or LW Index). Best for quick sentiment analysis. Displays index lines for Commercial, Non-Commercial, Small Speculator, and Open Interest. Percentile can exceed 0-100% for extremes, LW Index stays 0-100%.

Percentile can exceed 0-100% for extremes

LW Index stays 0-100%

COT Proximity Index - Shows a price-based proxy indicator. Useful when COT data is delayed or unavailable. Calculates sentiment based on price action patterns.

Trading Use:

- Use COT Report for comprehensive analysis

- Use COT Index when you want to focus on extreme sentiment levels

- Use COT Proximity Index as a backup when COT data is delayed or unavailable.

---

Analysis Method

Options: Percentile | LW Index

What it is: Selects the calculation method for position rankings.

Percentile - Professional approach. Excludes current bar from range calculation. Can show extremes (>100% or <0%) when today's value breaks historical range. More sensitive to recent extremes.

LW Index - Original Larry Williams method. Includes current bar in range, always 0-100%. Traditional approach.

Trading Use:

Percentile - Better for catching new extremes and recent market shifts

LW Index - Better for traditional Larry Williams analysis

Most traders prefer Percentile for its ability to show when positions break historical ranges.

---

Lookback Mode

Options: Auto | Manual

What it is: Controls how the historical lookback period is determined.

Auto - Automatically sets lookback period based on detected asset type

Manual - Choose your own lookback period

Trading Use: Use Auto unless you have a specific reason to customize. The script automatically sets optimal periods:

Currencies: 26 weeks

Metals: 13 weeks

Grains: 26 weeks

Stocks/Indices: 13 weeks

Bonds: 52 weeks

Energies: 13 weeks

---

Manual Lookback Period

Options: 1 Month | 3 Months | 6 Months | 1 Year | 3 Years | Asset-specific presets | Manual

What it is: How far back to look for historical comparison. Only used when Lookback Mode is set to Manual .

---

Manual Lookback Weeks

Default: 18 weeks | Range: 1-500

What it is: Exact number of weeks to look back. Only used when Manual Lookback Period is set to Manual .

Trading Use: Set a custom period if you want precise control. 18 weeks = approximately one quarter (3 months).

---

🎯 Group 3: Signal Generation

Show Signal Arrows

Default: Off (false)

What it is: Displays buy/sell arrows on the chart when extreme positions are detected.

Trading Use: Enable to get visual alerts for signals. Signals use strict multi-factor conditions requiring:

- Commercial extreme positioning

- Speculator positioning alignment

- Open Interest confirmation

- Trend consistency

- And more...

---

Show Background Colors

Default: Off (false)

What it is: Colors the chart background during extreme market conditions.

Trading Use: Enable for visual market state awareness:

- Strong signals = Darker background colors

- Moderate signals = Lighter background colors

- Green background = Bullish extreme

- Red background = Bearish extreme

Useful for quick visual assessment of market conditions.

---

Use Price Trend Weighting

Default: On (true)

What it is: Weights signals based on price trend alignment.

How it works:

Uptrend + Commercials long = Stronger bullish signal

Downtrend + Commercials short = Stronger bearish signal

Counter-trend signals = Harder to trigger (more conservative)

Trading Use: Keep enabled for more reliable signals. Commercials aligned with price trend are historically more accurate.

This feature makes signals easier to trigger when commercials align with the trend and harder when they're counter-trend.

---

Trend MA Period

Default: 40 | Range: 1-200

What it is: Moving average period for price trend detection.

How it works:

Price above MA with the MA rising = Uptrend

Price below MA with the MA declining = Downtrend

---

📈 Group 4: Plot Display Settings

Commercial Line Settings

Default Color: Red | Default Width: 2

What it is: Controls the Commercial traders net position line appearance.

Trading Use: Commercials are considered "smart money." Watch for:

Extreme long positions (high index ≥74%) = Heavy buyers = BULLISH signal

Extreme short positions (low index ≤26%) = Heavy sellers = BEARISH signal

Red is traditional for commercials. When Commercials are heavy buyers (high index), it's a bullish signal. When they're heavy sellers (low index), it's a bearish signal.

---

Non-Commercial Line Settings

Default Color: Blue | Default Width: 2

What it is: Controls the Non-Commercial (Large Speculators) net position line appearance.

Trading Use: Large speculators are often trend-followers. Watch for:

Extreme long = Potential top (contrarian sell signal)

Extreme short = Potential bottom (contrarian buy signal)

They're often wrong at extremes - use as contrarian indicator.

---

Small Speculator Line Settings

Default Color: Green | Default Width: 2

What it is: Controls the Small Speculators net position line appearance.

Trading Use: Small specs are typically wrong at extremes:

Extreme long = Potential top (sell signal)

Extreme short = Potential bottom (buy signal)

Exception: In Meats markets, small specs are accurate (like commercials).

---

Small Speculator Multiplier

Default: 5.0x | Range: 0.1-20.0

What it is: Multiplies Small Speculator PLOTTED values for visual comparison.

Important: This only affects the visual plot line, NOT calculations or table values. Raw values used in all calculations remain unchanged.

Trading Use: Small spec positions are often much smaller than commercials. Use multiplier (default 5.0x) to scale the line for easier visual comparison.

---

Open Interest Line Settings

Default Color: Black | Default Width: 1

What it is: Controls the Open Interest line appearance.

Trading Use: Open Interest shows market participation:

Rising OI = New money entering (confirms trend)

Falling OI = Money leaving (potential reversal)

Watch WHO is driving OI changes - This is critical

---

Scale Open Interest

Default: On (true)

What it is: Scales Open Interest values to fit chart range.

Important: Only affects plotted lines, not table values. Scaling changes based on lookback period:

- Shorter lookback = More compressed range

- Longer lookback = Wider range

Trading Use: Keep enabled for better visual comparison. Disable if you want absolute OI values.

---

Show Reference Lines

Default: Off (false)

What it is: Toggles the display of horizontal reference lines at 0%, 50%, and 100% levels on the chart.

What it shows:

Zero Line (0%) - Dotted gray line at 0% level

Midline (50%) - Solid gray line at 50% level

100 Line (100%) - Dotted gray line at 100% level

Trading Use: Enable when you want visual reference points for:

0% = Extreme bearish positioning

50% = Neutral/middle range

100% = Extreme bullish positioning

---

🔄 Group 5: Smoothing Settings

Smoothing Method

Options: None | SMA | EMA | WMA | RMA

What it is: Selects the moving average type for smoothing data.

None - Use raw data (no smoothing)

SMA - Simple Moving Average (equal weight to all periods)

EMA - Exponential Moving Average (more weight to recent data)

WMA - Weighted Moving Average (linear weighting)

RMA - Relative Moving Average (Wilder's smoothing)

Trading Use:

None - Best for catching extremes quickly

SMA - Most common, balanced smoothing

EMA - More responsive to recent changes

WMA/RMA - Advanced smoothing methods

Smoothing reduces noise but may delay signal detection. Use None for most responsive signals.

---

Smoothing Period

Default: 4 | Range: 2-20

What it is: Number of periods for the moving average smoothing.

Trading Use:

Shorter periods (2-5) = Less smoothing, more responsive

Longer periods (10-20) = More smoothing, less noise

Default 4 = Good balance

Only used when Smoothing Method is not None.

---

Smooth COT Report Plots

Default: Off (false)

What it is: Applies smoothing to COT Report plotted lines (Commercial, Non-Commercial, Small Speculators, Open Interest).

Trading Use: Enable if you want smoother chart lines. Note: Smoothing affects visual display but calculations use raw data unless Smooth COT Index Plots is also enabled.

---

Smooth COT Index Plots

Default: Off (false)

What it is: Applies smoothing to COT Index plotted lines.

Trading Use: Enable if you want smoother index lines. Important : When enabled, smoothed values are used in table displays and signal calculations. This affects the "user-facing" index values shown in the table and used for signals.

---

📊 Group 6: COT Proximity Index Settings

Proximity Length Mode

Options: Auto | Manual

What it is: Controls how the proximity index calculation period is determined.

Auto - Calculates length based on ZigZag patterns (dynamic)

Manual - Uses fixed length setting

Trading Use: Use Auto for adaptive calculation. Use Manual if you want consistent period regardless of market conditions.

---

Manual Proximity Length

Default: 8 bars | Range: 1+

What it is: Fixed number of bars for COT Proximity Index calculation. Only used when Proximity Length Mode is Manual .

Trading Use: Set based on your timeframe. 8 bars works well for weekly chart.

---

Heavy Buyers Level

Default: 74% | Range: 50-100

What it is: COT Index level above which commercials are considered heavy buyers (extreme long positioning).

Trading Use: This threshold is used for:

- Signal generation

- Market state calculation

- Entry level recommendations

Default 74% means commercials are "heavy buyers" when LW Index ≥ 74%.

---

Heavy Sellers Level

Default: 26% | Range: 0-50

What it is: COT Index level below which commercials are considered heavy sellers (extreme short positioning).

Trading Use: This threshold is used for:

- Signal generation

- Market state calculation

- Entry level recommendations

Default 26% means commercials are "heavy sellers" when LW Index ≤ 26%.

---

ZigZag Deviation

Default: 1.0% | Range: 1-100.0

What it is: Minimum price change (%) required to create a new ZigZag pivot point.

Trading Use:

Smaller values = More sensitive, more pivots

Larger values = Less sensitive, fewer pivots

Used for Auto proximity length calculation.

---

ZigZag Depth

Default: 1 | Range: 1+

What it is: Minimum number of bars between pivot points.

Trading Use: Higher values filter out minor pivots. Default 1 captures all significant pivots.

---

Extend ZigZag to Last Bar

Default: Off (false)

What it is: Draws ZigZag lines to the current bar (may show incomplete patterns).

Trading Use: Enable to see current ZigZag pattern, but be aware it may change as new bars form.

---

Show ZigZag Lines

Default: Off (false)

What it is: Displays ZigZag pivot lines on the chart for visual reference.

Trading Use: Enable to see the ZigZag pattern used for proximity index calculation. Useful for understanding how Auto mode works.

---

🎨 Group 7: Common Table Settings

Color Theme

Options: Dark | Light | Midnight Blue | Ocean Blue | Forest Green | Amber Gold | Slate Gray

What it is: Color scheme for both main and historical comparison tables.

Trading Use: Choose based on your preference:

Dark/Light - Classic themes

Midnight Blue - Professional dark theme

Ocean Blue - Calming blue tones

Forest Green - Natural green theme

Amber Gold - Warm gold tones

Slate Gray - Modern gray theme

Theme applies to both tables simultaneously for consistency.

---

📋 Group 8: Main Table Display Settings

Show COT Table

Default: On (true)

What it is: Toggles the main COT analysis table display.

Trading Use: Disable only if you want to use chart plots only. Most traders keep this enabled for comprehensive analysis.

---

Table Mode

Options: Full | Compact

What it is: Controls the detail level of the main table.

Full - Complete analysis table with all sections

Compact - Essential info only (mobile-friendly)

Trading Use:

Full - Desktop trading, comprehensive analysis

Compact - Mobile trading, quick reference

See "Table Modes Explained" section below for details.

---

Table Position

Options: Top Right | Top Left | Bottom Right | Bottom Left | Middle Right | Middle Left

What it is: Position of the main COT analysis table on the chart.

Trading Use: Choose based on your chart layout and preference. Top Right is default and works well for most traders.

---

Table Text Size

Options: Tiny | Small | Normal | Large

What it is: Size of text in the COT analysis table.

---

Section Visibility Controls

All default: On (true)

What it is: Individual toggles to show/hide specific table sections.

⚙️ Settings - Report Type, CFTC Code, Options setting

📊 Current Positions - Long, Short, Net positions for each group

📈 Analysis - LW Index, Percentile, Market State

🎯 Trading Edge & Signals - Current Signal, Entry Level, Best Setup

💡 Trading Tips - Context-aware trading insights

📈 Trend Analysis - Trend Direction, Strength, Cum Change, ROC, vs MA

🔄 Market Maker Activity - Spreading, Activity Level, Trading Edge

Trading Use: Customize your table to show only what you need:

Quick traders - Show only Trading Edge & Signals

Detailed analysis - Show all sections

Mobile users - Hide less critical sections

Each section can be toggled independently for maximum customization.

---

📊 Group 9: Historical Comparison Settings

Show Historical Comparisons

Default: On (true)

What it is: Toggles the historical comparison table display.

Trading Use: This table shows how current positions rank over different time periods (1M, 3M, 6M, 1Y, 3Y, All Time). Very useful for context.

---

Historical Table Mode

Options: Full | Compact

What it is: Controls the detail level of the historical comparison table.

Full - Complete historical comparison with all time periods (1M, 3M, 6M, 1Y, 3Y, All Time) and all COT groups

Compact - Essential periods only (1M, 3M, 6M, 1Y, All Time) showing Commercial % only

Trading Use:

- Full - Comprehensive historical analysis

- Compact - Quick reference, mobile-friendly

---

Table Position (Historical)

Options: Top Right | Top Left | Bottom Right | Bottom Left

What it is: Position of the historical comparison table on the chart.

---

Table Text Size (Historical)

Options: Tiny | Small | Normal | Large

What it is: Size of text in the historical comparison table.

---

Trading Days

Options: Weekdays | 24/7

What it is: How to calculate time periods for historical comparisons.

Weekdays - Calculate based on trading days only (5 days/week)

24/7 - Include all calendar days (7 days/week), Use for 24/7 markets like cryptocurrencies

Used for both main COT data and COT Proximity Index historical comparisons.

---

📊 Table Modes Explained

Full Mode - Main Table

The Full mode displays all available sections:

⚙️ Settings - Report type, CFTC code, options setting

📊 Current Positions - Long, Short, Net for Commercial, Non-Commercial, Small Speculators

📊 Open Interest Analysis - OI value, change, who's driving changes, concentration

📈 Analysis - Percentile ranks, LW Index values, Market State

🎯 Trading Edge & Signals - Current Signal, Entry Level, What to Watch, Best Setup

💡 Trading Tips - Context-aware insights

📈 Trend Analysis - Trend Direction, Strength, Consistency, Cumulative Change, ROC %, vs MA

🔄 Market Maker Activity - Spreading %, Activity Level, Interpretation, Trading Edge

Best for: Desktop trading, comprehensive analysis, detailed market assessment

---

📋 Understanding Each Table Section

This section explains what each part of the main table means and how to use it for trading decisions.

⚙️ Settings Section

Report Type - Shows which COT report format you're using (Legacy, Disaggregated, or Financial). Verify this matches your asset type.

Options - Indicates if options data is included ("Included") or excluded ("Excluded"). Most traders exclude options for cleaner analysis.

CFTC Code - Unique identifier for your futures contract. Shows "Auto" when automatically detected, or displays the manual code if set.

Trading Use: Always verify your CFTC code is correct. Wrong code = wrong data = wrong signals.

---

📊 Current Positions Section

Shows the actual position sizes for each trader group.

What Each Column Means:

Long - Total long contracts held by this group

Short - Total short contracts held by this group

Net - Net position (Long - Short). This is the key number.

How to Interpret:

Commercial Net Position:

- Negative (Net Short) = Commercials expect prices to fall

- Positive (Net Long) = Commercials expect prices to rise

- Commercials are "smart money" - their positioning often precedes major moves

Non-Commercial Net Position:

- Positive (Net Long) = Large speculators bullish

- Negative (Net Short) = Large speculators bearish

- Often trend-followers, can be caught at extremes

Small Spec Net Position:

- Positive (Net Long) = Small traders bullish

- Negative (Net Short) = Small traders bearish

- Often contrarian indicator - wrong at extremes

Trading Edge: Watch for extremes in Commercial net positions. When Commercials are heavy buyers (high index ≥74%), it's a bullish signal. When they're heavy sellers (low index ≤26%), it's a bearish signal.

---

📊 Open Interest Analysis Section

Open Interest - Total number of outstanding contracts. Shows market participation level.

Change - Week-over-week change in Open Interest. Rising OI = new money entering, Falling OI = money leaving.

Net Changes - Shows which group is driving Open Interest changes. This is Larry Williams' most important insight.

🎯 Critical Question: Who is Driving OI Changes?

EXTREMELY BULLISH SIGNAL (Very Rare - Pay Close Attention):

- Commercials driving OI increase + Commercials raising positions + Uptrend market

- Meaning: Smart money (commercials) accumulating long positions while market is rising

- Action: Extremely bullish - very rare setup, pay close attention to this signal

- This is the strongest bullish signal possible

BULLISH SIGNAL (Strong Buy):

- Commercials driving OI increase + Commercials net long

- Meaning: Smart money accumulating long positions

- Action: Strong bullish setup

BEARISH SIGNAL (Strong Sell - Market Topping):

- Commercials exiting + OI increasing due to Small Specs + Non-Commercials

- Meaning: Smart money leaving while speculative money entering

- Action: Market top forming - most likely scenario for bearish reversal

- This indicates speculative excess and potential market top

BEARISH SIGNAL (Speculative Excess):

- Small Specs + Non-Commercials driving OI increase + They are net long

- Meaning: Speculative excess, "dumb money" driving market

- Action: Bearish reversal likely

Trading Use:

- Rising OI = New money entering (confirms trend)

- Falling OI = Money leaving (potential reversal)

- Watch WHO is driving OI changes - This is critical

- When Commercials drive OI increases while raising positions in an uptrend = Extremely bullish and very rare - pay attention

- When Commercials exit while OI increases due to Small Specs and Non-Commercials = Market topping signal

Concentration - Shows how much of the market is controlled by the largest traders:

- Top 4 - Four largest traders' share of total OI

- Top 8 - Eight largest traders' share of total OI

Trading Use: High concentration (>30%) means fewer dominant players, potential for volatility. Low concentration means more distributed positions, healthier market.

---

📈 Analysis Section

Proximity Index (when in COT Proximity Index mode):

- Value: Current proximity index reading (0-100%)

- Length: Number of bars used in calculation

- Status: Heavy Buyers, Heavy Sellers, or Neutral

Analysis Method - Shows whether you're using Percentile or LW Index calculation.

Small Spec Mode - Shows how Small Speculators are interpreted:

- Contrarian (Traditional) - Small specs are wrong at extremes (default)

- Accurate (Meats) - Small specs are accurate like commercials (for Meats markets)

Market State - Overall market sentiment assessment:

- STRONG BULLISH - Multiple factors aligned bullish, strong buy signal

- MODERATE BULLISH - Several bullish factors, moderate buy signal

- LEANING BULLISH - Slight bullish bias, watch for confirmation

- NEUTRAL - Mixed signals, trade with existing trend

- LEANING BEARISH - Slight bearish bias, watch for confirmation

- MODERATE BEARISH - Several bearish factors, moderate sell signal

- STRONG BEARISH - Multiple factors aligned bearish, strong sell signal

Trading Use: Start your analysis here. Market State gives you the overall picture before diving into details.

---

🎯 Trading Edge & Signals Section

Current Signal - Shows which combination is active based on current positioning extremes and its expected accuracy percentage:

- Comm+Spec+OI - All three groups at extremes (highest accuracy)

- Comm+Spec - Commercials and specs at extremes (opposite extremes - Larry Williams' favorite)

- Comm+OI - Commercials and Open Interest at extremes (smart money + participation)

- Commercials - Only Commercials at extreme (smart money indicator)

- Wait - No extremes detected, wait for setup

Entry - Trading signal based on Commercial positioning:

- LONG - Commercials are heavy buyers (≥Heavy Buyers Level), bullish signal

- SHORT - Commercials are heavy sellers (≤Heavy Sellers Level), bearish signal

- Wait - Commercials neutral, no clear signal

Best Setup - Shows the historically highest accuracy combination found in the data:

- Comm+Spec+SmallSpec+OI - All four groups aligned (strongest signal)

- Comm+Spec+OI (All) - Commercials + Speculators + Open Interest aligned

- Comm+Spec+SmallSpec - Commercials + Speculators + Small Specs aligned

- Comm+Spec (Both) - Commercials + Speculators (opposite extremes - Larry Williams' favorite)

- Comm+OI (Both) - Commercials + Open Interest (participation confirms smart money)

- Comm+SmallSpec - Commercials + Small Specs (especially strong in Meats markets)

- Commercials Alone - Commercial positioning only (baseline - smart money indicator)

Trading Use: This is your action center . Focus on Entry signals when Market State confirms. Higher accuracy setups (shown in Best Setup) are more reliable.

---

💡 Trading Tips Section

Context-aware insights based on current market conditions.

What You'll See:

Commercial positioning assessment (extreme long/short, favorable/unfavorable)

Speculator positioning (contrarian support or warning)

Open Interest guidance (who's driving changes)

Trend assessment (aligning or conflicting)

Information about entry timing, position sizing, and confirmation needs

Trading Use: Review these tips when analyzing. They provide context-specific information tailored to current conditions.

---

📈 Trend Analysis Section

Trend Direction - Overall price trend:

- Bullish - Price trending up

- Bearish - Price trending down

- Mixed - No clear direction

Consistency - How stable the trend is:

- Consistent - Trend is stable and maintaining direction

- Mixed - Trend is unstable, direction changing

- Accelerating - Trend is gaining momentum

Strength - Trend intensity:

- Strong - Powerful trend

- Steady - Moderate trend

- Weak - Weak trend

This Week - Net position change this week (percentage).

Cumulative Change - Total net position change over different periods:

- 4W - 4-week cumulative change

- 13W - 13-week cumulative change (one quarter)

- 26W - 26-week cumulative change (half year)

ROC % - Rate of Change percentage over different periods. Shows momentum.

vs MA - Current net position compared to moving average:

- Positive = Above average (strong positioning)

- Negative = Below average (weak positioning)

Trading Use: Align COT signals with trend direction for higher accuracy. When COT signals align with price trend, signals are more reliable. Counter-trend signals require more confirmation.

---

🔄 Market Maker Activity Section

Total Spreading - Percentage of open interest in spread positions (simultaneous long and short in different months).

Percentile - Where current spreading level ranks historically. High percentile = unusual spreading activity.

13W Trend - 13-week trend in spreading activity (+ = increasing, - = decreasing).

Activity Level - Market maker activity intensity:

- High - Very active, expect volatility

- Moderate - Normal activity

- Low - Quiet, less volatility expected

vs 13W Avg - Current activity compared to 13-week average.

Trading Edge - Interpretation of market maker activity:

- High & Rising - Expect volatility, market makers hedging risk

- High & Stable - Active hedging, monitor for changes

- Low & Falling - Reduced activity, potential for directional moves

Trading Use: High market maker activity often precedes volatility. Use this to adjust position sizing and risk management. When spreading is high and rising, expect choppy conditions.

---

📋 Understanding Compact Mode Fields

The Compact mode provides essential information for quick trading decisions. Here's what each field means:

State

Shows the overall market sentiment based on combined COT analysis.

Possible Values:

- STRONG BULLISH - Multiple factors aligned bullish, strong buy signal

- MODERATE BULLISH - Several bullish factors, moderate buy signal

- LEANING BULLISH - Slight bullish bias, watch for confirmation

- NEUTRAL - Mixed signals, trade with existing trend

- LEANING BEARISH - Slight bearish bias, watch for confirmation

- MODERATE BEARISH - Several bearish factors, moderate sell signal

- STRONG BEARISH - Multiple factors aligned bearish, strong sell signal

Trading Use: Start your analysis here. Strong signals (STRONG BULLISH/BEARISH) indicate higher confidence setups. Neutral means trade with price trend.

---

Entry

Your actionable trading signal based on Commercial positioning.

Possible Values:

- LONG - Commercials are heavy buyers (≥Heavy Buyers Level), bullish signal

- SHORT - Commercials are heavy sellers (≤Heavy Sellers Level), bearish signal

- Wait - Commercials neutral, no clear signal

Trading Use: This is your go/no-go decision point. Only take trades when Entry shows LONG or SHORT. When Entry = Wait, stay on sidelines until clearer signal develops.

---

Comm Index

Commercial LW Index percentage showing where Commercial net position ranks historically.

Range: 0% to 100%

- 0-26% = Commercials heavy sellers (bearish positioning)

- 27-73% = Commercials neutral (no extreme)

- 74-100% = Commercials heavy buyers (bullish positioning)

Trading Use: Commercial extremes are most reliable. Values ≥74% (heavy buyers/extreme long) = BULLISH signal. Values ≤26% (heavy sellers/extreme short) = BEARISH signal. When Commercials are heavy buyers, it indicates bullish sentiment. When they're heavy sellers, it indicates bearish sentiment.

---

OI Status

Open Interest condition showing market participation level and trend.

Format: Status (Percentile %)

Examples:

- High (100.0%) - OI at extreme high, strong participation

- Moderate (50.0%) - OI at average level

- Low (10.0%) - OI at extreme low, weak participation

Trend Indicators:

- Rising - OI increasing (new money entering)

- Falling - OI decreasing (money leaving)

- Stable - OI unchanged

Trading Use: High OI with rising trend = strong market participation, confirms directional moves. Falling OI = watch for potential reversals. Low OI = reduced participation, potential for volatility.

---

Best Setup

Shows which combination of factors has the highest historical accuracy.

Format: Combination Name (Accuracy %)

Examples:

- Commercials Alone (75.3%) - Commercial positioning only

- Commercials + Speculators (68.2%) - Commercials and specs aligned

- Commercials + Open Interest (72.1%) - Commercials with OI confirmation

- Commercials + Speculators + OI (82.1%) - All factors aligned (strongest)

Trading Use: Higher accuracy values indicate signals with higher historical accuracy. When Best Setup shows "Commercials + Speculators + OI" with high accuracy, it indicates a combination with strong historical performance.

---

Trend

13-week cumulative trend direction based on net position changes.

Possible Values:

- Bullish - Net positions trending bullish over 13 weeks

- Bearish - Net positions trending bearish over 13 weeks

- Mixed - No clear directional trend

Trading Use: Align Entry signals with Trend for higher accuracy. When Entry = LONG and Trend = Bullish, signal is stronger. When Entry = LONG but Trend = Bearish, wait for price confirmation before entering. Counter-trend signals require more confirmation.

---

Full Mode - Historical Table

The Full historical mode shows:

All time periods: 1 Month, 3 Months, 6 Months, 1 Year, 3 Years, All Time

All COT groups: Commercial, Non-Commercial, Small Speculators, Open Interest

Complete header with asset type and lookback information

Best for: Comprehensive historical analysis, understanding long-term positioning

---

Compact Mode - Historical Table

The Compact historical mode shows:

Essential periods only: 1M, 3M, 6M, 1Y, All Time

Commercial % only (most important indicator)

Simplified header

Best for: Quick reference, mobile-friendly, focused analysis

---

🎯 How to Use Each Feature for Trading

Using Display Modes

COT Report Mode - Use for:

Understanding raw position sizes

Analyzing net position changes

Comparing absolute positions across groups

Detailed market structure analysis

COT Index Mode - Use for:

Quick sentiment assessment

Identifying extremes (Percentile can show >100% or <0%, LW Index shows 0-100%)

Comparing relative positioning

Signal generation

COT Proximity Index Mode - Use for:

When COT data is delayed

Real-time sentiment estimation

Price-action based analysis

---

Using Analysis Methods

Percentile Method - Use when:

You want to catch new extremes (>100% or <0%)

You need responsive signals

You're analyzing recent market regime changes

You want to use the professional approach (excludes current bar from range)

LW Index Method - Use when:

You want traditional Larry Williams analysis

You prefer stable, conservative signals

You're doing long-term analysis

You want always 0-100% range

---

Using Signal Generation

Enable Signal Arrows when:

You want visual alerts for high-quality setups

You're scanning multiple charts

You want to catch extreme positioning

Enable Background Colors when:

You want quick visual market state assessment

You're monitoring multiple timeframes

You want to see market conditions at a glance

Use Price Trend Weighting to:

Increase signal reliability

Align COT signals with price action

Filter counter-trend signals

---

Using Smoothing

No Smoothing - Best for:

Catching extremes quickly

Responsive signal generation

Active trading

With Smoothing - Best for:

Reducing noise

Trend identification

Swing trading

Remember: Smoothing affects visual display. Enable "Smooth COT Index Plots" if you want smoothed values in calculations.

---

Using Heavy Buyers/Sellers Levels

Default 74%/26% - Good starting point