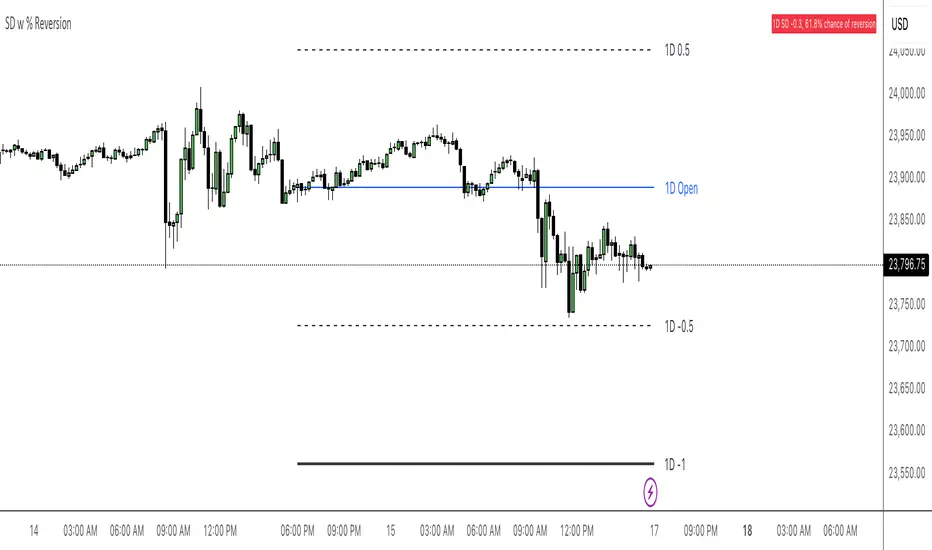

NQ Stats Mean ReversionBased off of Multi-timeframe support by keypoems, modified to be anchored on a HTF and added a dynamic label to give current SD level with chance of reversion

Statistics

Extended CANSLIM Indicator❖ Extended CANSLIM Indicator.

The Extended CANSLIM indicator is an indicator that concentrates all the tools usually used by CANSLIM traders.

It shows a table where all the stock fundamental information is shown at once first for the last quarter and then up to 5 years back.

The fundamental data is checked against well known CANSLIM validation criteria and is shown over 4 state levels.

1. Good = Value is CANSLIM Compliant.

2. Acceptable = Value is not CANSLIM compliant but still good. value is shown with a lighter background color.

3. Warning = Value deserves special attention. Value is shown over orange background color.

3. Stop = Value is non CANSLIM compliant or indicates a stop trading condition. Value is shown over red background color.

The indicator has also a set of technical tools calculated on price or index and shown directly on the chart.

❖ Fundamental data shown in the table.

The table is arranged in 4 sets of data:

1. Table Header, showing Indicator and Company data.

2. CANSLIM.

3. 3Rs: RS Rating, Revenue and ROE.

4. Extra Data: Piotroski score, ATR, Trend Days, D to E, Avg Vol and Vol today.

Sets 3 and 4 can be hidden from the table.

❖ Indicator and Compay Data.

The table header shows, Indicator name and version.

It then displays Company Name, sector and industry, human size and its capitalization.

❖ CANSLIM Data.

Displays either genuine CANSLIM data from TradinView or custom data as best effort when that data cannot be obtained in TV.

C = EPS diluted growth, Quarterly YoY.

>= 25% = Good, >= 0% = Acceptable, < 0% = Stop

A = EPS diluted growth, Annual YoY.

>= 25% = Good, >= 0% = Acceptable, < 0% = Stop

N = New High as best effort (Cust).

Always Good

S = Float shares as best effort.

Always Good

L = One year performance relative to S&P 500 (Cust),

Positive : 0% .. 50% = Neutral, 50%+ = Leader, 80%+ = Leader+, 100%+ = Leader++

Negative : 0% .. -10% = Laggard, -10% .. -30% = Laggard+, -30%+ = Laggard++

>= 50% = Good, >= 0% = Acceptable, >= -10% Warning, < -10% = Stop

I = Accumulation/Distribution days over last 25 days as a clue for institutional support (Cust).

A delta is calculated by subtracting Distribution to Accumulation days.

> 0 = Good, = 0 = Acceptable, < 0 = Warning, < -5 = Stop

M = Market direction and exposure measured on S&500 closing between averages (Cust).

Varies from 0% Full Bear to 100% Full Bull

>= 80% = Good, >= 60% = Acceptable, >= 40% = Warning, < 40% = Stop

❖ Extra non CANSLIM Data.

RS = RS Rating.

>= 90 = Good, >= 80 = Accept, >= 50 = Warning, < 50 = Stop

Rev. = Revenue Growth Quarterly YoY.

>= 0% = Good, <0% = Stop

ROE = Return on Equity, Quarterly YoY.

>= 17% = Good, >= 0% = Acceptable, < 0% = Stop

Piotr. = Piotroski Score, www.investopedia.com (TV)

>= 7 = Good, >= 4 = Acceptable, < 4 = Stop

ATR = Average True Range over the last 20 days (Cust).

0% - 2% = Acceptable, 2% - 4% = Ideal, 4% - 6% = Warning, 5%+ = Stop.

Trend Days = Days since EMA150 is over EMA200 (Cust).

Always Good

D. to E. = Days left before Earnings. Maybe not a good idea buying just before earnings (Cust).

>= 28 = Good, >= 21 = Acceptable, >= 14 = Warning, < 14 = Stop

Avg Vol. = 50d Average Volume (Cust).

>= 100K = Good, < 100K = Acceptable

Vol. Today = Today's percentage volume compared to 50d average (Cust).

Always Good.

❖ Historical Data.

Optionally selectable historical data can be displayed for C, A, Revenue and ROE up to 20 quarters if available.

Quarterly numbers can also be displayed for A, C and Revenue.

Information can be shown in Chronological or Reverse Chronological order (default).

Increasing growth quarters are shown in white, while diminuing ones are shown in Yellow.

Transition from Losing to Profitable quarters are shown with an exclamation mark ‘!’

Finally, losing quarters are shown between parenthesis.

❖ MAs on chart.

Displays 200, 100, 50 and 20 days MAs on chart.

The MAs are also automatically scaled in the 1W time frame.

❖ New 52 Week High on chart.

A sun is shown on the chart the first time that a new 52 week high is reached.

The N cell shows a filled sun when a 52 week high is no older than a month, an lighter sun when it’s no older than a quarter or a moon otherwise.

❖ Pocket Pivots on chart.

Small triangles below the price are signaling pocket pivots.

❖ Bases on chart, formerly Darvas Boxes.

Draw bases as defined by Darvas boxes, both top or bottom of bases can be selected to be shown in order to only show resistance or support.

❖ Market exposure/direction indicator.

When charting S&P500 (SPX), Nasdaq 100 Index (NDX), Nasdaq composite (IXIC) or Dow Jownes Index (DJIA), the indicator switches to Market Exposure indicator, showing also Accumulation/Distribution days when volume information is available. This indication which varies from 0% to 100% is what is shown under the M letter in the CANSLIM table which is calculated on the S&P500.

❖ Follow Through Days indicator.

If you are an adept of the Low-cheat entry, then you will be highly interested by the Follow Through days indicator as measured in the S&P 500 and shown as diamonds on the chart.

The follow-through days are calculated on S&P500 but shown in current stock chart so you don’t need to chart the S&P 500 to know that a follow through day occurred.

Follow Through days show correctly on Daily time frame and most are also shown on the Weekly time frame as well.

They are also classified according to the market zone in which they occur:

0%-5% from peak = Pullback : FT day is not shown.

5%-10% from peak = Minor Correction : Minor FT days is shown.

10%-20% from peak = Correction : Intermediate FT days us shown

20+% from peak = Bear Market : Makor FT days is shown

❖ RS Line and Rating indicator.

A RS Line and Rating indicator can be added to the chart.

Relative Strength Rating Accuracy.

Please note that the RS Rating is not 100% accurate when compared to IBD values.

❖ Earning Line indicator.

An Earning Line indicator can be added to the chart.

❖ ATR Bands and ATR Trade calculator.

The motivation for this calculator came from my own need to enter trades on volatile stocks where the simple 7% Stop Loss rule doest not work.

It simply calculates the number of shares you can buy at any moment based on current stock price and using the lower ATR band as a stop loss.

A few words about the ATR Bands.

On this indicator the ATR bands are not drawn as a classical channel that follows the price.

The lower band is drawn as a support until it’s broken on a closing basis. It can’t be in a down trend.

The upper band is drawn as a resistance until it’s broken on a closing basis. It can’t be in an up trend.

The idea is that when price starts to fall down from a peak, it should not violate its lower band ATR and that means that we can use that level as a Stop Loss.

You must look back for the stock volatility and find out which ATR multiplier works well meaning that the ATR bands are not violated on normal pullbacks. By default, the indicator uses 5x multiplier.

❖ Extra things, visual features and default settings.

The first square cell of current quarter displays a check mark ‘V’ if the CANSLIM criteria is OK or acceptable or a cross ‘X’ otherwise.

The first square cell of historical C and Rev show respectively the count of last consecutive positive quarters.

There are different color themes from “Forest” to “Space” you can chose from to best fit your eyes.

You also have different table sizes going from “Micro” to “Huge” for better adjustment to the size of your display.

The default settings view show: Pocket Pivots, FT Days, MA50, RS Line and ATR Bands.

That's all, Enjoy!

Chaos Theory : public release

What is Chaos Theory?

Chaos theory is the study of complex systems that appear random but actually follow deterministic mathematical laws. Discovered by meteorologist Edward Lorenz in the 1960s, it revealed that seemingly chaotic behavior often hides precise mathematical patterns.

Key Concepts:

The Butterfly Effect

The famous principle that tiny changes in initial conditions can lead to vastly different outcomes. In markets, this means a small price movement at a critical juncture can cascade into major trend changes. Named after Lorenz's discovery that a butterfly flapping its wings in Brazil could theoretically cause a tornado in Texas.

Sensitive Dependence on Initial Conditions

Chaotic systems are extremely sensitive to their starting state. While we cannot predict exact long-term outcomes, we can identify probability zones where the system is likely to evolve. This is why weather forecasts work for days, not months - and why our indicator predicts price destinations, not timing.

Strange Attractors

In chaos theory, systems tend to evolve toward certain states called attractors. Price doesn't move randomly - it's drawn toward these mathematical attractors that we identify as probability zones.

Fractals and Self-Similarity

Chaotic systems display similar patterns at different scales. This is why price charts look similar whether viewing 1-minute or daily timeframes - the same mathematical forces operate across all time scales.

Deterministic Chaos

The paradox at the heart of chaos theory: systems that are completely deterministic (following precise mathematical rules) can produce behavior that appears random. Markets aren't random - they're chaotic, which means they're predictable within probability bounds.

Why This Matters for Trading

Traditional technical analysis assumes markets are either random (efficient market hypothesis) or follow simple patterns (support/resistance). Chaos theory reveals a third truth: markets are complex dynamical systems that follow mathematical laws we can model and predict - not with certainty, but with probability.

This is the foundation of our indicator: applying the same mathematics that predicts weather patterns and planetary orbits to identify where price is mathematically likely to travel next.

🌟 Welcome to the World of Chaos Theory

We hope to provide our clients with a program that will define future points to which we believe price will expand to, based on a given probability % of one event occurring rather than another. In this case, the other event = price not expanding to our predicted area and reaching an invalidation state. This entire theory and the work done assumes that price behaves like a complex dynamical system that is highly sensitive to initial conditions.

🔮 Predictive vs. Reactive Systems

Pay special attention to the language used. Our belief is that we can provide you a tool that is predictive, not reactive - the latter of which falls into the class of descriptive systems. Although the term of price action study is referred to as time-series forecasting, most if not all of the works done under this umbrella do not forecast anything. They only describe the current or recent past state of affairs using averages, volume, volatility, and other concepts.

📊 Understanding Probability-Based Prediction

A predictive system conjured from the world of chaos theory is not a final solution to the mystery of price. In reality, we only can give you probabilities of where price may end up - this would be a point in space, not time, which we believe would be more likely than another, depending on the analysis of the initial conditions.

To make the point of the last paragraph crystal clear: while we can tell you, with respect to the probabilities, where price will end up in terms of a price point, we don't know WHEN. That is another part of the mystery that perhaps only clairvoyance can hope to uncover.

📈 Performance Statistics

For the question of what the probabilities are, meaning the success of the follow through of price, the answer is given in a stats panel, which measures the success of promises made by the indicator - that price would reach a certain point before being invalidated by moving too far in the opposing direction. It's not helpful to advertise or make false claims, therefore one should take advantage that we offer a free version, and using a pre-defined lookback window, confirm the probability calculations and determine the follow through rate with respect to the specific symbol and timeframe that the user decides to use.

⚠️ What This Is Not

What this is not → Descriptive. We have zero interest in describing what price is doing. In fact, the entire industry of price forecasting is dedicated to this task, therefore you can rest assured that any coincidence with an RSI or any type of moving average etc. is simply that - coincidence. We do not use any known pre-made indicators or formulas.

It has been our belief that price has an underlying mathematical pattern that can be predicted within probability bounds. If you read that carefully, we are predicting the pattern, not looking to find and describe some sort of underlying structure.

🧩 Understanding Market Complexity

It should be understood that price is a complex system, even if our initial assessment of the conditions are correct. We have to remember that price is a fractal structure - there are always different initial conditions clashing, as well as forming. This is without taking into account the manipulation of the system, as well as external intervention in the natural progression of the system by news or other significant events.

---

📋 To Summarize:

🔬 1. Chaos Theory Application to Markets

- Novel Concept: Treating price as a chaotic particle rather than random movement

- What This Means: Chaotic systems have underlying mathematical patterns that can be predicted within probability bounds

- Your Benefit: Access to predictive mathematics previously used only in physics and meteorology

🧮 2. Complex Systems Mathematics

- Novel Concept: Applying non-linear dynamical systems theory to financial markets

- What This Means: Markets behave like complex adaptive systems with emergent properties

- Your Benefit: Understanding market behavior at a fundamental mathematical level

🎯 3. Probability Field Mapping

- Novel Concept: Creating mathematical probability fields for future price locations

- What This Means: Each zone represents a calculated probability destination, not arbitrary support/resistance

- Your Benefit: Trade toward mathematically-derived targets instead of guessing

---

💡 Why This is Fundamentally Different from All Other Indicators

📉 Traditional Indicators:

- Use historical price data to create lagging signals

- Based on statistical averages and linear mathematics

- Assume markets are random or follow simple patterns

- React to what already happened

🚀 This Chaos Theory Approach:

- Uses mathematical modeling to predict future probability zones

- Based on non-linear complex systems mathematics

- Treats markets as chaotic but predictable systems

- Proactively identifies where price is likely to go

No Curve Fitting: Unlike indicators optimized for specific timeframes or instruments, chaos theory principles are universal mathematical laws that apply consistently across all markets.

---

🎁 Concrete Benefits You Receive

💫 1. Predictive Intelligence

- Know probable price destinations before they're reached

- Eliminate guesswork in setting profit targets

- Make informed decisions about trade direction

🎯 2. Mathematical Precision

- Every zone placement has mathematical justification

- No subjective interpretation required

- Consistent application across all market conditions

🌍 3. Universal Market Application

- Works identically on forex, stocks, crypto, commodities

- No need to adjust parameters for different instruments

- Mathematical principles transcend market types

🏆 4. Professional-Grade Analysis

- Access to institutional-level mathematical modeling

- Same complexity as quantitative hedge fund systems

- Simplified visual output for practical trading

✅ 5. Real-Time Performance Validation

- Built-in statistics track actual prediction accuracy

- Transparent performance measurement

- Data-driven confidence in signal quality

🛡️ 6. Risk Management Precision

- Mathematically-defined probable targets of desired and undesired price locations

- Systematic approach eliminates emotional decisions

⏱️ 7. Multi-Timeframe Consistency

- Zones maintain mathematical validity across timeframes

- Higher timeframe bias with lower timeframe precision

- Coherent analysis from scalping to position trading

---

🌟 Novel Trading Advantages

Probability-Based Targeting: Instead of hoping price reaches your target, you're trading toward mathematically-calculated probability zones.

Chaos Pattern Recognition: Probability-based predictions of the underlying chaotic patterns that govern price movement gives you an edge other traders don't possess.

Dynamic Adaptation: Unlike static indicators, this system continuously recalculates based on evolving market mathematics.

---

🔄 Why This Represents a Trading Evolution

From Reactive to Predictive: Traditional analysis tells you what happened. Chaos theory mathematics tells you what's likely to happen.

From Subjective to Objective: No more debating support and resistance levels. Mathematics determines probable price destinations.

From Curve-Fitted to Universal: Based on fundamental mathematical principles that work consistently across all markets and timeframes.

From Emotional to Systematic: Clear mathematical signals eliminate the psychological challenges that destroy most traders.

This indicator doesn't just give you another way to analyze markets - it gives you access to an entirely different mathematical framework for understanding price behavior. You're not getting a variation of existing concepts; you're getting a completely novel approach based on advanced mathematical principles that treat markets as the complex systems they actually are.

---

📚 How to Use the Indicator

🎨 Zone Mechanics

• Orange Zones: Target areas for price expansion

• Activation Trigger: Price must close outside any zone (full candle body, not just wicks)

• Primary Rule: Price travels to the next zone before closing back behind the originating zone border

🔴 Understanding the Red Dots

• Red dots on chart: Represent areas where we had valid zone sets available for trading

• Empty spaces indicate: Areas where price closed past the highest/lowest zone or where zone invalidation occurred

• Important note: We cannot always identify zones. Simply wait or switch timeframe/symbol

Session Volatility MonitorOverview

Session Volatility Monitor is a versatile volatility indicator tailored for intraday and session-based trading. It computes the average maximum price deviation (either up or down) from the session's opening price over a user-specified number of prior days, providing insights into expected "room to move" in the current session. This helps traders gauge potential exhaustion points, set realistic targets or stops, and identify when a directional move has reached historical norms (flagged as "REACHED" with the exact price level).

Displayed via a customisable table and optional horizontal target lines, it's ideal for markets like forex, crypto, futures, or stocks where session volatility matters. The indicator supports custom sessions with timezone adjustments, making it adaptable to global trading hours (e.g., London, NY, or Asia kill zones). For assets with small tick sizes (e.g., forex pairs at 0.0001), a multiplier scales values for readability (e.g., showing pips as 67.0 instead of 0.00670).

Key Features

Session-Based Calculations:

Defines sessions via presets (e.g., "NY Kill Zone: 07:00-10:00") or custom HHMM-HHMM inputs. (please note that preset sessions are mainly for futures e.g. "Full Day18:01-17:00", but also can be useful for forex and crypto)

Adjustable UTC offset (e.g., -5 for ET) to align with your asset's timezone—ensures accurate detection regardless of TradingView's UTC internal clock.

Tracks the max one-sided move (high - open or open - low) per session, averaging over 1–N previous days (default: 14).

Table Display:

Avg Max Move: Historical average deviation, labeled with days averaged and session time.

Current Move: Real-time displacement from session open (positive for up, negative for down).

Room to Go Up/Down: Remaining distance to reach the average, updating live; appends "REACHED (price)" if hit during the session.

Customisable: Text color, font size (tiny to huge), position (e.g., bottom_left), and value scaling via multiplier/decimal places.

Target Lines:

Optional horizontal lines at "Up Target" (open + avg move) and "Down Target" (open - avg move).

Lines start at the session open bar and extend only through the session duration (e.g., stops at 12:00 for a 07:00-12:00 session)—no further projection post-session.

Fully customisable: Toggle on/off, color, style (solid/dotted/dashed), width, label text/background.

Display Adjustments for Forex/Crypto:

Multiplier: Scales raw values (e.g., set to 10000 for EURUSD to show pips like 45.0 instead of 0.0045).

Decimals: Controls precision (0–5 places) for table values.

How to Use

Add to Chart: Search for "Session Volatility Monitor" in TradingView's indicators and apply to your symbol (e.g., EURUSD for forex, NQ1! for futures, BTCUSD for crypto).

Configure Settings:

Select a session preset or custom range; adjust UTC offset if needed (e.g., +0 for UTC symbols like crypto).

Set "Number of Previous Days to Average" (e.g., 14 for a two-week look back).

For small-tick assets, set Multiplier (e.g., 100 for crypto points, 10000 for forex pips) and Decimals (e.g., 0 for whole numbers).

Customise table position/size/color and target lines for visibility.

Interpret Outputs:

Monitor the table for "room to go"—if Room Up is low/negative, upside might be limited; "REACHED" signals a potential reversal or exhaustion.

Use target lines as visual S/R levels; they auto-start at session open and halt at close.

Combine with price action, volume, or other indicators for entries (e.g., buy near down target if bullish bias).

Example Scenario:

Forex (GBPUSD, 1-min): Set session to "London Kill Zone: 02:00-05:00" (UTC+0), multiplier=10000. Table shows pips; lines mark expected highs/lows.

Limitations and Tips

Historical Data Limits: Averages are capped by TradingView's bar history (e.g., ~14 days on 1-min for free plans). Upgrade for deeper look backs or use higher timeframes.

Session Accuracy: Ensure UTC offset matches your chart—test with the "In Session" plot (enable in Style tab, zoom y-axis if columns are tiny).

No Alerts/Signals: Purely informational; add custom alerts via TradingView for "REACHED" conditions.

Performance: On very low timeframes with long sessions, lines might consume line limits (max ~50)—toggle off if needed.

Tips: For crypto/forex, experiment with multiplier to match your preferred units (e.g., points vs. decimals). Hide debug plot in Style tab for clean charts. If "REACHED" doesn't trigger, verify on historical data where moves exceed averages.

This tool draws from concepts like Average Daily Range but focuses on directional, session-specific volatility for precise intraday decision-making. Feedback welcome!

Disclaimer

This indicator is for educational purposes only and does not constitute financial advice. Always consult a professional before trading.

Cheat CodeWhy Monday & Friday

Monday evening (NY): frequently seeds the weekly expansion. Its DR/IDR often acts as a weekly “starter envelope,” useful for breakout continuation or fade back into the box plays as liquidity builds.

Friday evening (NY): often exposes end-of-week traps (run on stops into the close) and sets expectation boundaries into the following week. Carry these levels forward to catch Monday’s reaction to Friday’s closing structure.

Typical use-cases

Breakout & retest:

Price closes outside the Monday DR/IDR → look for retests of the band edge for continuation.

Liquidity sweep (“trap”) recognition:

Friday session wicks briefly beyond Friday DR/IDR then closes back inside → watch for mean reversion early next week.

Bias filter:

Above both Monday DR midline and Friday DR midline → bias long until proven otherwise; the inverse for shorts.

Session open confluence:

Reactions at the open line frequently mark decision points for momentum vs. fade setups.

(This is a levels framework, not a signals engine. Combine with your execution model: orderflow, S/R, session timing, or higher-TF bias.)

Inputs & styling (quick reference)

Display toggles (per day):

Show DR / IDR / Middle DR / Middle IDR

Show Opening Line

Show DR/IDR Box (choose DR or IDR as box source)

Show Price Labels

Style controls (per day):

Line width (1–4), style (Solid/Dashed/Dotted)

Independent colors for DR, IDR, midlines, open line

Box background opacity

Timezone:

Default America/New_York (changeable).

Optional on-chart warning if your chart TZ differs.

Practical notes

Works on intraday charts; levels are anchored using weekly timestamps for accuracy on any symbol.

Live updating: During the Mon/Fri calc windows, DR/IDR highs/lows and midlines keep updating until the session ends.

Clean drawings: Lines, box, and labels are created once per session and then extended/updated—efficient on resources even with long display windows.

Max elements: Script reserves ample line/box/label capacity for stability across weeks.

Session Highs and LowsThis indicator plots the following:

- Previous day high and low (based on previous daily candle) - purple lines

- Asian high and low (1800-0200) - red lines

- London high and low (0300-0930) - blue lines

During NY session, once one of these point of interest has been hit or passed, the line thickness reduces so you can tell at a glance which points have been taken, but they still remain on the chart for reference.

Correlation Heatmap Matrix [TradingFinder] 20 Assets Variable🔵 Introduction

Correlation is one of the most important statistical and analytical metrics in financial markets, data mining, and data science. It measures the strength and direction of the relationship between two variables.

The correlation coefficient always ranges between +1 and -1 : a perfect positive correlation (+1) means that two assets or currency pairs move together in the same direction and at a constant ratio, a correlation of zero (0) indicates no clear linear relationship, and a perfect negative correlation (-1) means they move in exactly opposite directions.

While the Pearson Correlation Coefficient is the most common method for calculation, other statistical methods like Spearman and Kendall are also used depending on the context.

In financial market analysis, correlation is a key tool for Forex, the Stock Market, and the Cryptocurrency Market because it allows traders to assess the price relationship between currency pairs, stocks, or coins. For example, in Forex, EUR/USD and GBP/USD often have a high positive correlation; in stocks, companies from the same sector such as Apple and Microsoft tend to move similarly; and in crypto, most altcoins show a strong positive correlation with Bitcoin.

Using a Correlation Heatmap in these markets visually displays the strength and direction of these relationships, helping traders make more accurate decisions for risk management and strategy optimization.

🟣 Correlation in Financial Markets

In finance, correlation refers to measuring how closely two assets move together over time. These assets can be stocks, currency pairs, commodities, indices, or cryptocurrencies. The main goal of correlation analysis in trading is to understand these movement patterns and use them for risk management, trend forecasting, and developing trading strategies.

🟣 Correlation Heatmap

A correlation heatmap is a visual tool that presents the correlation between multiple assets in a color-coded table. Each cell shows the correlation coefficient between two assets, with colors indicating its strength and direction. Warm colors (such as red or orange) represent strong negative correlation, cool colors (such as blue or cyan) represent strong positive correlation, and mid-range tones (such as yellow or green) indicate correlations that are close to neutral.

🟣 Practical Applications in Markets

Forex : Identify currency pairs that move together or in opposite directions, avoid overexposure to similar trades, and spot unusual divergences.

Crypto : Examine the dependency of altcoins on Bitcoin and find independent movers for portfolio diversification.

Stocks : Detect relationships between stocks in the same industry or find outliers that move differently from their sector.

🟣 Key Uses of Correlation in Trading

Risk management and diversification: Select assets with low or negative correlation to reduce portfolio volatility.

Avoiding overexposure: Prevent opening multiple positions on highly correlated assets.

Pairs trading: Exploit temporary deviations between historically correlated assets for arbitrage opportunities.

Intermarket analysis: Study the relationships between different markets like stocks, currencies, commodities, and bonds.

Divergence detection: Spot when two typically correlated assets move apart as a possible trend change signal.

Market forecasting: Use correlated asset movements to anticipate others’ behavior.

Event reaction analysis: Evaluate how groups of assets respond to economic or political events.

❗ Important Note

It’s important to note that correlation does not imply causation — it only reflects co-movement between assets. Correlation is also dynamic and can change over time, which is why analyzing it across multiple timeframes provides a more accurate picture. Combining correlation heatmaps with other analytical tools can significantly improve the precision of trading decisions.

🔵 How to Use

The Correlation Heatmap Matrix indicator is designed to analyze and manage the relationships between multiple assets at once. After adding the tool to your chart, start by selecting the assets you want to compare (up to 20).

Then, choose the Correlation Period that fits your trading strategy. Shorter periods (e.g., 20 bars) are more sensitive to recent price movements, making them suitable for short-term trading, while longer periods (e.g., 100 or 200 bars) provide a broader view of correlation trends over time.

The indicator outputs a color-coded matrix where each cell represents the correlation between two assets. Warm colors like red and orange signal strong negative correlation, while cool colors like blue and cyan indicate strong positive correlation. Mid-range tones such as yellow or green suggest correlations that are close to neutral. This visual representation makes it easy to spot market patterns at a glance.

One of the most valuable uses of this tool is in portfolio risk management. Portfolios with highly correlated assets are more vulnerable to market swings. By using the heatmap, traders can find assets with low or negative correlation to reduce overall risk.

Another key benefit is preventing overexposure. For example, if EUR/USD and GBP/USD have a high positive correlation, opening trades on both is almost like doubling the position size on one asset, increasing risk unnecessarily. The heatmap makes such relationships clear, helping you avoid them.

The indicator is also useful for pairs trading, where a trader identifies assets that are usually correlated but have temporarily diverged — a potential arbitrage or mean-reversion opportunity.

Additionally, the tool supports intermarket analysis, allowing traders to see how movements in one market (e.g., crude oil) may impact others (e.g., the Canadian dollar). Divergence detection is another advantage: if two typically aligned assets suddenly move in opposite directions, it could signal a major trend shift or a news-driven move.

Overall, the Correlation Heatmap Matrix is not just an analytical indicator but also a fast, visual alert system for monitoring multiple markets at once. This is particularly valuable for traders in fast-moving environments like Forex and crypto.

🔵 Settings

🟣 Logic

Correlation Period : Number of bars used to calculate correlation between assets.

🟣 Display

Table on Chart : Enable/disable displaying the heatmap directly on the chart.

Table Size : Choose the table size (from very small to very large).

Table Position : Set the table location on the chart (top, middle, or bottom in various alignments).

🟣 Symbol Custom

Select Market : Choose the market type (Forex, Stocks, Crypto, or Custom).

Symbol 1 to Symbol 20: In custom mode, you can define up to 20 assets for correlation calculation.

🔵 Conclusion

The Correlation Heatmap Matrix is a powerful tool for analyzing correlations across multiple assets in Forex, crypto, and stock markets. By displaying a color-coded table, it visually conveys both the strength and direction of correlations — warm colors for strong negative correlation, cool colors for strong positive correlation, and mid-range tones such as yellow or green for near-zero or neutral correlation.

This helps traders select assets with low or negative correlation for diversification, avoid overexposure to similar trades, identify arbitrage and pairs trading opportunities, and detect unusual divergences between typically aligned assets. With support for custom mode and up to 20 symbols, it offers high flexibility for different trading strategies, making it a valuable complement to technical analysis and risk management.

Seasonality Monte Carlo Forecaster [BackQuant]Seasonality Monte Carlo Forecaster

Plain-English overview

This tool projects a cone of plausible future prices by combining two ideas that traders already use intuitively: seasonality and uncertainty. It watches how your market typically behaves around this calendar date, turns that seasonal tendency into a small daily “drift,” then runs many randomized price paths forward to estimate where price could land tomorrow, next week, or a month from now. The result is a probability cone with a clear expected path, plus optional overlays that show how past years tended to move from this point on the calendar. It is a planning tool, not a crystal ball: the goal is to quantify ranges and odds so you can size, place stops, set targets, and time entries with more realism.

What Monte Carlo is and why quants rely on it

• Definition . Monte Carlo simulation is a way to answer “what might happen next?” when there is randomness in the system. Instead of producing a single forecast, it generates thousands of alternate futures by repeatedly sampling random shocks and adding them to a model of how prices evolve.

• Why it is used . Markets are noisy. A single point forecast hides risk. Monte Carlo gives a distribution of outcomes so you can reason in probabilities: the median path, the 68% band, the 95% band, tail risks, and the chance of hitting a specific level within a horizon.

• Core strengths in quant finance .

– Path-dependent questions : “What is the probability we touch a stop before a target?” “What is the expected drawdown on the way to my objective?”

– Pricing and risk : Useful for path-dependent options, Value-at-Risk (VaR), expected shortfall (CVaR), stress paths, and scenario analysis when closed-form formulas are unrealistic.

– Planning under uncertainty : Portfolio construction and rebalancing rules can be tested against a cloud of plausible futures rather than a single guess.

• Why it fits trading workflows . It turns gut feel like “seasonality is supportive here” into quantitative ranges: “median path suggests +X% with a 68% band of ±Y%; stop at Z has only ~16% odds of being tagged in N days.”

How this indicator builds its probability cone

1) Seasonal pattern discovery

The script builds two day-of-year maps as new data arrives:

• A return map where each calendar day stores an exponentially smoothed average of that day’s log return (yesterday→today). The smoothing (90% old, 10% new) behaves like an EWMA, letting older seasons matter while adapting to new information.

• A volatility map that tracks the typical absolute return for the same calendar day.

It calculates the day-of-year carefully (with leap-year adjustment) and indexes into a 365-slot seasonal array so “March 18” is compared with past March 18ths. This becomes the seasonal bias that gently nudges simulations up or down on each forecast day.

2) Choice of randomness engine

You can pick how the future shocks are generated:

• Daily mode uses a Gaussian draw with the seasonal bias as the mean and a volatility that comes from realized returns, scaled down to avoid over-fitting. It relies on the Box–Muller transform internally to turn two uniform random numbers into one normal shock.

• Weekly mode uses bootstrap sampling from the seasonal return history (resampling actual historical daily drifts and then blending in a fraction of the seasonal bias). Bootstrapping is robust when the empirical distribution has asymmetry or fatter tails than a normal distribution.

Both modes seed their random draws deterministically per path and day, which makes plots reproducible bar-to-bar and avoids flickering bands.

3) Volatility scaling to current conditions

Markets do not always live in average volatility. The engine computes a simple volatility factor from ATR(20)/price and scales the simulated shocks up or down within sensible bounds (clamped between 0.5× and 2.0×). When the current regime is quiet, the cone narrows; when ranges expand, the cone widens. This prevents the classic mistake of projecting calm markets into a storm or vice versa.

4) Many futures, summarized by percentiles

The model generates a matrix of price paths (capped at 100 runs for performance inside TradingView), each path stepping forward for your selected horizon. For each forecast day it sorts the simulated prices and pulls key percentiles:

• 5th and 95th → approximate 95% band (outer cone).

• 16th and 84th → approximate 68% band (inner cone).

• 50th → the median or “expected path.”

These are drawn as polylines so you can immediately see central tendency and dispersion.

5) A historical overlay (optional)

Turn on the overlay to sketch a dotted path of what a purely seasonal projection would look like for the next ~30 days using only the return map, no randomness. This is not a forecast; it is a visual reminder of the seasonal drift you are biasing toward.

Inputs you control and how to think about them

Monte Carlo Simulation

• Price Series for Calculation . The source series, typically close.

• Enable Probability Forecasts . Master switch for simulation and drawing.

• Simulation Iterations . Requested number of paths to run. Internally capped at 100 to protect performance, which is generally enough to estimate the percentiles for a trading chart. If you need ultra-smooth bands, shorten the horizon.

• Forecast Days Ahead . The length of the cone. Longer horizons dilute seasonal signal and widen uncertainty.

• Probability Bands . Draw all bands, just 95%, just 68%, or a custom level (display logic remains 68/95 internally; the custom number is for labeling and color choice).

• Pattern Resolution . Daily leans on day-of-year effects like “turn-of-month” or holiday patterns. Weekly biases toward day-of-week tendencies and bootstraps from history.

• Volatility Scaling . On by default so the cone respects today’s range context.

Plotting & UI

• Probability Cone . Plots the outer and inner percentile envelopes.

• Expected Path . Plots the median line through the cone.

• Historical Overlay . Dotted seasonal-only projection for context.

• Band Transparency/Colors . Customize primary (outer) and secondary (inner) band colors and the mean path color. Use higher transparency for cleaner charts.

What appears on your chart

• A cone starting at the most recent bar, fanning outward. The outer lines are the ~95% band; the inner lines are the ~68% band.

• A median path (default blue) running through the center of the cone.

• An info panel on the final historical bar that summarizes simulation count, forecast days, number of seasonal patterns learned, the current day-of-year, expected percentage return to the median, and the approximate 95% half-range in percent.

• Optional historical seasonal path drawn as dotted segments for the next 30 bars.

How to use it in trading

1) Position sizing and stop logic

The cone translates “volatility plus seasonality” into distances.

• Put stops outside the inner band if you want only ~16% odds of a stop-out due to noise before your thesis can play.

• Size positions so that a test of the inner band is survivable and a test of the outer band is rare but acceptable.

• If your target sits inside the 68% band at your horizon, the payoff is likely modest; outside the 68% but inside the 95% can justify “one-good-push” trades; beyond the 95% band is a low-probability flyer—consider scaling plans or optionality.

2) Entry timing with seasonal bias

When the median path slopes up from this calendar date and the cone is relatively narrow, a pullback toward the lower inner band can be a high-quality entry with a tight invalidation. If the median slopes down, fade rallies toward the upper band or step aside if it clashes with your system.

3) Target selection

Project your time horizon to N bars ahead, then pick targets around the median or the opposite inner band depending on your style. You can also anchor dynamic take-profits to the moving median as new bars arrive.

4) Scenario planning & “what-ifs”

Before events, glance at the cone: if the 95% band already spans a huge range, trade smaller, expect whips, and avoid placing stops at obvious band edges. If the cone is unusually tight, consider breakout tactics and be ready to add if volatility expands beyond the inner band with follow-through.

5) Options and vol tactics

• When the cone is tight : Prefer long gamma structures (debit spreads) only if you expect a regime shift; otherwise premium selling may dominate.

• When the cone is wide : Debit structures benefit from range; credit spreads need wider wings or smaller size. Align with your separate IV metrics.

Reading the probability cone like a pro

• Cone slope = seasonal drift. Upward slope means the calendar has historically favored positive drift from this date, downward slope the opposite.

• Cone width = regime volatility. A widening fan tells you that uncertainty grows fast; a narrow cone says the market typically stays contained.

• Mean vs. price gap . If spot trades well above the median path and the upper band, mean-reversion risk is high. If spot presses the lower inner band in an up-sloping cone, you are in the “buy fear” zone.

• Touches and pierces . Touching the inner band is common noise; piercing it with momentum signals potential regime change; the outer band should be rare and often brings snap-backs unless there is a structural catalyst.

Methodological notes (what the code actually does)

• Log returns are used for additivity and better statistical behavior: sim_ret is applied via exp(sim_ret) to evolve price.

• Seasonal arrays are updated online with EWMA (90/10) so the model keeps learning as each bar arrives.

• Leap years are handled; indexing still normalizes into a 365-slot map so the seasonal pattern remains stable.

• Gaussian engine (Daily mode) centers shocks on the seasonal bias with a conservative standard deviation.

• Bootstrap engine (Weekly mode) resamples from observed seasonal returns and adds a fraction of the bias, which captures skew and fat tails better.

• Volatility adjustment multiplies each daily shock by a factor derived from ATR(20)/price, clamped between 0.5 and 2.0 to avoid extreme cones.

• Performance guardrails : simulations are capped at 100 paths; the probability cone uses polylines (no heavy fills) and only draws on the last confirmed bar to keep charts responsive.

• Prerequisite data : at least ~30 seasonal entries are required before the model will draw a cone; otherwise it waits for more history.

Strengths and limitations

• Strengths :

– Probabilistic thinking replaces single-point guessing.

– Seasonality adds a small but meaningful directional bias that many markets exhibit.

– Volatility scaling adapts to the current regime so the cone stays realistic.

• Limitations :

– Seasonality can break around structural changes, policy shifts, or one-off events.

– The number of paths is performance-limited; percentile estimates are good for trading, not for academic precision.

– The model assumes tomorrow’s randomness resembles recent randomness; if regime shifts violently, the cone will lag until the EWMA adapts.

– Holidays and missing sessions can thin the seasonal sample for some assets; be cautious with very short histories.

Tuning guide

• Horizon : 10–20 bars for tactical trades; 30+ for swing planning when you care more about broad ranges than precise targets.

• Iterations : The default 100 is enough for stable 5/16/50/84/95 percentiles. If you crave smoother lines, shorten the horizon or run on higher timeframes.

• Daily vs. Weekly : Daily for equities and crypto where month-end and turn-of-month effects matter; Weekly for futures and FX where day-of-week behavior is strong.

• Volatility scaling : Keep it on. Turn off only when you intentionally want a “pure seasonality” cone unaffected by current turbulence.

Workflow examples

• Swing continuation : Cone slopes up, price pulls into the lower inner band, your system fires. Enter near the band, stop just outside the outer line for the next 3–5 bars, target near the median or the opposite inner band.

• Fade extremes : Cone is flat or down, price gaps to the upper outer band on news, then stalls. Favor mean-reversion toward the median, size small if volatility scaling is elevated.

• Event play : Before CPI or earnings on a proxy index, check cone width. If the inner band is already wide, cut size or prefer options structures that benefit from range.

Good habits

• Pair the cone with your entry engine (breakout, pullback, order flow). Let Monte Carlo do range math; let your system do signal quality.

• Do not anchor blindly to the median; recalc after each bar. When the cone’s slope flips or width jumps, the plan should adapt.

• Validate seasonality for your symbol and timeframe; not every market has strong calendar effects.

Summary

The Seasonality Monte Carlo Forecaster wraps institutional risk planning into a single overlay: a data-driven seasonal drift, realistic volatility scaling, and a probabilistic cone that answers “where could we be, with what odds?” within your trading horizon. Use it to place stops where randomness is less likely to take you out, to set targets aligned with realistic travel, and to size positions with confidence born from distributions rather than hunches. It will not predict the future, but it will keep your decisions anchored to probabilities—the language markets actually speak.

Weekly High/Low Weekday Stats by [M1rage]Патч: условная статистика по дню недельного экстремума

Добавлена новая функция, позволяющая строить условное распределение по дням недели.

Что нового.

Два новых параметра в настройках:

Condition: Weekly High on — зафиксировать день недели, в который сформировался недельный High.

Condition: Weekly Low on — зафиксировать день недели, в который сформировался недельный Low.

Таблица автоматически перестраивается:

Левая колонка показывает — вероятности минимума недели при выбранном дне максимума.

Правая колонка показывает — вероятности максимума недели при выбранном дне минимума.

В заголовках колонок появляется подпись формата:

Weekly Low | High=Tue

Weekly High | Low=Thu

---------------------------------------------------------------------------------------------------------------------

Patch: Conditional Statistics by Day of the Weekly Extremum

A new feature has been added that builds a conditional distribution by weekdays.

What’s new

Two new settings:

Condition: Weekly High on — fix the weekday on which the weekly High formed.

Condition: Weekly Low on — fix the weekday on which the weekly Low formed.

The table updates automatically:

Left column — probabilities of the weekly Low given the selected day of the High.

Right column — probabilities of the weekly High given the selected day of the Low.

Column headers now display labels in the format:

Weekly Low | High=Tue

Weekly High | Low=Thu

Weekly High/Low Weekday Stats by [M1rage]Weekly High/Low Weekday Stats by

---------------------------------------------------------------------------------------------------------------------

Индикатор показывает, в какие дни недели чаще всего формируются недельные High и Low инструмента. Поддерживает режимы 24/5 (FX) и 24/7 (крипто). Работает на Daily (D) таймфрейме.

Что делает:

Скользит по дневным барам, собирает недельные экстремумы.

Для каждой завершённой недели фиксирует день недели недельного High и Low.

Строит таблицу-частот Mon..Fri (24/5) или Mon..Sun (24/7) с процентами/счётчиками.

Опционально помечает на графике лейблами бары, где сформировались недельные High/Low (для быстрой визуальной проверки).

Параметры:

Lookback (years) — глубина истории (примерно 52 недели × годы).

Show percentages — показывать проценты.

Show raw counts — показывать «сырые» счётчики.

Show debug labels (weekly H/L) — лейблы H/L на графике для завершённых недель.

Debug: keep last N weeks — сколько последних недель держать на графике лейблами (старые удаляются).

Market mode — режим рынка: 24/5 (Mon..Fri) или 24/7 (Mon..Sun).

Table theme — цветовая тема таблицы: Dark Theme / Light Theme

(меняет цвет текста, шапки, внешней рамки и внутренних границ).

Очень короткие праздничные недели фильтруются, чтобы не искажать статистику.

---------------------------------------------------------------------------------------------------------------------

The indicator shows on which weekdays a symbol most often sets its weekly High and Low. It supports 24/5 (FX) and 24/7 (crypto) modes. Works on the Daily (D) timeframe.

What it does:

Scans daily bars to build weekly extremes.

For each completed week, records the weekday of the weekly High and Low.

Builds a frequency table Mon–Fri (24/5) or Mon–Sun (24/7) with percentages/counts.

Optionally labels on the chart the bars where the weekly High/Low formed (for quick visual verification).

Inputs:

Lookback (years) — history depth (≈ 52 weeks × years).

Show percentages — display percentages.

Show raw counts — display raw counts.

Show debug labels (weekly H/L) — H/L labels on the chart for completed weeks.

Debug: keep last N weeks — how many recent weeks to keep as labels on the chart (older labels are deleted).

Market mode — market schedule: 24/5 (Mon–Fri) or 24/7 (Mon–Sun).

Table theme — table color theme: Dark Theme / Light Theme (changes text color, header, outer frame, and inner grid).

Very short holiday weeks are filtered out to avoid skewing the statistics.

Line color best indices grouped by Artificial Intelligence

The script uses the best buy indicators, such as moving average crossovers, RSI, and others selected by AI. The idea is to determine whether the stock is classified as a strong buy (yellow line), a buy (green line), or a red (sell)

Strong Indicator for ISM PMI EURUSD (mtbr)Overview:

This indicator is designed for EURUSD traders who want to analyse the market's reaction to the ISM Services PMI economic event. It automatically detects the event candle, calculates the “surprise” between Actual and Forecast, and generates a full trading plan with entry, take profit, and stop loss levels.

How it works:

Set the event time (or a custom date/time) and input Forecast, Previous, and Actual values.

The indicator calculates the surprise: Actual − Forecast.

Based on the surprise magnitude, it classifies the strength as Weak, Moderate, or Strong, and as Bullish or Bearish.

Direction is set automatically but can be inverted via the “Invert Signal Logic” option.

Entry, TP1, TP2, TP3, and SL are calculated based on your percentage settings.

Levels are plotted on the chart, with labels and a vertical dashed line marking the event candle.

A table displays key event data: name, forecast, actual, surprise, and strength classification.

How to use:

Select your trading asset (EURUSD by default).

Choose between automatic event time logic or a custom date/time.

Input the Forecast, Previous, and Actual values from the economic calendar.

Adjust percentage settings for entry, take profits, and stop loss.

Use the plotted lines as a reference for trade planning.

Optionally enable pullback confirmation before entry.

Disclaimer:

This tool is for educational and analytical purposes only. It is not financial advice. Always use proper risk management and perform independent analysis before trading.

TimeSeriesBenchmarkMeasuresLibrary "TimeSeriesBenchmarkMeasures"

Time Series Benchmark Metrics. \

Provides a comprehensive set of functions for benchmarking time series data, allowing you to evaluate the accuracy, stability, and risk characteristics of various models or strategies. The functions cover a wide range of statistical measures, including accuracy metrics (MAE, MSE, RMSE, NRMSE, MAPE, SMAPE), autocorrelation analysis (ACF, ADF), and risk measures (Theils Inequality, Sharpness, Resolution, Coverage, and Pinball).

___

Reference:

- github.com .

- medium.com .

- www.salesforce.com .

- towardsdatascience.com .

- github.com .

mae(actual, forecasts)

In statistics, mean absolute error (MAE) is a measure of errors between paired observations expressing the same phenomenon. Examples of Y versus X include comparisons of predicted versus observed, subsequent time versus initial time, and one technique of measurement versus an alternative technique of measurement.

Parameters:

actual (array) : List of actual values.

forecasts (array) : List of forecasts values.

Returns: - Mean Absolute Error (MAE).

___

Reference:

- en.wikipedia.org .

- The Orange Book of Machine Learning - Carl McBride Ellis .

mse(actual, forecasts)

The Mean Squared Error (MSE) is a measure of the quality of an estimator. As it is derived from the square of Euclidean distance, it is always a positive value that decreases as the error approaches zero.

Parameters:

actual (array) : List of actual values.

forecasts (array) : List of forecasts values.

Returns: - Mean Squared Error (MSE).

___

Reference:

- en.wikipedia.org .

rmse(targets, forecasts, order, offset)

Calculates the Root Mean Squared Error (RMSE) between target observations and forecasts. RMSE is a standard measure of the differences between values predicted by a model and the values actually observed.

Parameters:

targets (array) : List of target observations.

forecasts (array) : List of forecasts.

order (int) : Model order parameter that determines the starting position in the targets array, `default=0`.

offset (int) : Forecast offset related to target, `default=0`.

Returns: - RMSE value.

nmrse(targets, forecasts, order, offset)

Normalised Root Mean Squared Error.

Parameters:

targets (array) : List of target observations.

forecasts (array) : List of forecasts.

order (int) : Model order parameter that determines the starting position in the targets array, `default=0`.

offset (int) : Forecast offset related to target, `default=0`.

Returns: - NRMSE value.

rmse_interval(targets, forecasts)

Root Mean Squared Error for a set of interval windows. Computes RMSE by converting interval forecasts (with min/max bounds) into point forecasts using the mean of the interval bounds, then compares against actual target values.

Parameters:

targets (array) : List of target observations.

forecasts (matrix) : The forecasted values in matrix format with at least 2 columns (min, max).

Returns: - RMSE value for the combined interval list.

mape(targets, forecasts)

Mean Average Percentual Error.

Parameters:

targets (array) : List of target observations.

forecasts (array) : List of forecasts.

Returns: - MAPE value.

smape(targets, forecasts, mode)

Symmetric Mean Average Percentual Error. Calculates the Mean Absolute Percentage Error (MAPE) between actual targets and forecasts. MAPE is a common metric for evaluating forecast accuracy, expressed as a percentage, lower values indicate a better forecast accuracy.

Parameters:

targets (array) : List of target observations.

forecasts (array) : List of forecasts.

mode (int) : Type of method: default=0:`sum(abs(Fi-Ti)) / sum(Fi+Ti)` , 1:`mean(abs(Fi-Ti) / ((Fi + Ti) / 2))` , 2:`mean(abs(Fi-Ti) / (abs(Fi) + abs(Ti))) * 100`

Returns: - SMAPE value.

mape_interval(targets, forecasts)

Mean Average Percentual Error for a set of interval windows.

Parameters:

targets (array) : List of target observations.

forecasts (matrix) : The forecasted values in matrix format with at least 2 columns (min, max).

Returns: - MAPE value for the combined interval list.

acf(data, k)

Autocorrelation Function (ACF) for a time series at a specified lag.

Parameters:

data (array) : Sample data of the observations.

k (int) : The lag period for which to calculate the autocorrelation. Must be a non-negative integer.

Returns: - The autocorrelation value at the specified lag, ranging from -1 to 1.

___

The autocorrelation function measures the linear dependence between observations in a time series

at different time lags. It quantifies how well the series correlates with itself at different

time intervals, which is useful for identifying patterns, seasonality, and the appropriate

lag structure for time series models.

ACF values close to 1 indicate strong positive correlation, values close to -1 indicate

strong negative correlation, and values near 0 indicate no linear correlation.

___

Reference:

- statisticsbyjim.com

acf_multiple(data, k)

Autocorrelation function (ACF) for a time series at a set of specified lags.

Parameters:

data (array) : Sample data of the observations.

k (array) : List of lag periods for which to calculate the autocorrelation. Must be a non-negative integer.

Returns: - List of ACF values for provided lags.

___

The autocorrelation function measures the linear dependence between observations in a time series

at different time lags. It quantifies how well the series correlates with itself at different

time intervals, which is useful for identifying patterns, seasonality, and the appropriate

lag structure for time series models.

ACF values close to 1 indicate strong positive correlation, values close to -1 indicate

strong negative correlation, and values near 0 indicate no linear correlation.

___

Reference:

- statisticsbyjim.com

adfuller(data, n_lag, conf)

: Augmented Dickey-Fuller test for stationarity.

Parameters:

data (array) : Data series.

n_lag (int) : Maximum lag.

conf (string) : Confidence Probability level used to test for critical value, (`90%`, `95%`, `99%`).

Returns: - `adf` The test statistic.

- `crit` Critical value for the test statistic at the 10 % levels.

- `nobs` Number of observations used for the ADF regression and calculation of the critical values.

___

The Augmented Dickey-Fuller test is used to determine whether a time series is stationary

or contains a unit root (non-stationary). The null hypothesis is that the series has a unit root

(is non-stationary), while the alternative hypothesis is that the series is stationary.

A stationary time series has statistical properties that do not change over time, making it

suitable for many time series forecasting models. If the test statistic is less than the

critical value, we reject the null hypothesis and conclude the series is stationary.

___

Reference:

- www.jstor.org

- en.wikipedia.org

theils_inequality(targets, forecasts)

Calculates Theil's Inequality Coefficient, a measure of forecast accuracy that quantifies the relative difference between actual and predicted values.

Parameters:

targets (array) : List of target observations.

forecasts (array) : Matrix with list of forecasts, ordered column wise.

Returns: - Theil's Inequality Coefficient value, value closer to 0 is better.

___

Theil's Inequality Coefficient is calculated as: `sqrt(Sum((y_i - f_i)^2)) / (sqrt(Sum(y_i^2)) + sqrt(Sum(f_i^2)))`

where `y_i` represents actual values and `f_i` represents forecast values.

This metric ranges from 0 to infinity, with 0 indicating perfect forecast accuracy.

___

Reference:

- en.wikipedia.org

sharpness(forecasts)

The average width of the forecast intervals across all observations, representing the sharpness or precision of the predictive intervals.

Parameters:

forecasts (matrix) : The forecasted values in matrix format with at least 2 columns (min, max).

Returns: - Sharpness The sharpness level, which is the average width of all prediction intervals across the forecast horizon.

___

Sharpness is an important metric for evaluating forecast quality. It measures how narrow or wide the

prediction intervals are. Higher sharpness (narrower intervals) indicates greater precision in the

forecast intervals, while lower sharpness (wider intervals) suggests less precision.

The sharpness metric is calculated as the mean of the interval widths across all observations, where

each interval width is the difference between the upper and lower bounds of the prediction interval.

Note: This function assumes that the forecasts matrix has at least 2 columns, with the first column

representing the lower bounds and the second column representing the upper bounds of prediction intervals.

___

Reference:

- Hyndman, R. J., & Athanasopoulos, G. (2018). Forecasting: principles and practice. OTexts. otexts.com

resolution(forecasts)

Calculates the resolution of forecast intervals, measuring the average absolute difference between individual forecast interval widths and the overall sharpness measure.

Parameters:

forecasts (matrix) : The forecasted values in matrix format with at least 2 columns (min, max).

Returns: - The average absolute difference between individual forecast interval widths and the overall sharpness measure, representing the resolution of the forecasts.

___

Resolution is a key metric for evaluating forecast quality that measures the consistency of prediction

interval widths. It quantifies how much the individual forecast intervals vary from the average interval

width (sharpness). High resolution indicates that the forecast intervals are relatively consistent

across observations, while low resolution suggests significant variation in interval widths.

The resolution is calculated as the mean absolute deviation of individual interval widths from the

overall sharpness value. This provides insight into the uniformity of the forecast uncertainty

estimates across the forecast horizon.

Note: This function requires the forecasts matrix to have at least 2 columns (min, max) representing

the lower and upper bounds of prediction intervals.

___

Reference:

- (sites.stat.washington.edu)

- (www.jstor.org)

coverage(targets, forecasts)

Calculates the coverage probability, which is the percentage of target values that fall within the corresponding forecasted prediction intervals.

Parameters:

targets (array) : List of target values.

forecasts (matrix) : The forecasted values in matrix format with at least 2 columns (min, max).

Returns: - Percent of target values that fall within their corresponding forecast intervals, expressed as a decimal value between 0 and 1 (or 0% and 100%).

___

Coverage probability is a crucial metric for evaluating the reliability of prediction intervals.

It measures how well the forecast intervals capture the actual observed values. An ideal forecast

should have a coverage probability close to the nominal confidence level (e.g., 90%, 95%, or 99%).

For example, if a 95% prediction interval is used, we expect approximately 95% of the actual

target values to fall within those intervals. If the coverage is significantly lower than the

nominal level, the intervals may be too narrow; if it's significantly higher, the intervals may

be too wide.

Note: This function requires the targets array and forecasts matrix to have the same number of

observations, and the forecasts matrix must have at least 2 columns (min, max) representing

the lower and upper bounds of prediction intervals.

___

Reference:

- (www.jstor.org)

pinball(tau, target, forecast)

Pinball loss function, measures the asymmetric loss for quantile forecasts.

Parameters:

tau (float) : The quantile level (between 0 and 1), where 0.5 represents the median.

target (float) : The actual observed value to compare against.

forecast (float) : The forecasted value.

Returns: - The Pinball loss value, which quantifies the distance between the forecast and target relative to the specified quantile level.

___

The Pinball loss function is specifically designed for evaluating quantile forecasts. It is

asymmetric, meaning it penalizes underestimates and overestimates differently depending on the

quantile level being evaluated.

For a given quantile τ, the loss function is defined as:

- If target >= forecast: (target - forecast) * τ

- If target < forecast: (forecast - target) * (1 - τ)

This loss function is commonly used in quantile regression and probabilistic forecasting

to evaluate how well forecasts capture specific quantiles of the target distribution.

___

Reference:

- (www.otexts.com)

pinball_mean(tau, targets, forecasts)

Calculates the mean pinball loss for quantile regression.

Parameters:

tau (float) : The quantile level (between 0 and 1), where 0.5 represents the median.

targets (array) : The actual observed values to compare against.

forecasts (matrix) : The forecasted values in matrix format with at least 2 columns (min, max).

Returns: - The mean pinball loss value across all observations.

___

The pinball_mean() function computes the average Pinball loss across multiple observations,

making it suitable for evaluating overall forecast performance in quantile regression tasks.

This function leverages the asymmetric Pinball loss function to evaluate how well forecasts

capture specific quantiles of the target distribution. The choice of which column from the

forecasts matrix to use depends on the quantile level:

- For τ ≤ 0.5: Uses the first column (min) of forecasts

- For τ > 0.5: Uses the second column (max) of forecasts

This loss function is commonly used in quantile regression and probabilistic forecasting

to evaluate how well forecasts capture specific quantiles of the target distribution.

___

Reference:

- (www.otexts.com)

Franco Varacalli binary options |ENGLISH|

What if you could know, with mathematical precision, when your trades have the highest probability of success?

Franco V. ~ Stats is not just an indicator: it’s a real-time performance tracking and analysis system that transforms price action into clear, actionable metrics.

🔍 What it does

It analyzes candle sequences and detects changes in price dynamics, filtering opportunities according to your settings (buy only, sell only, or both). From there, it records each entry, counts wins and losses, and calculates success probabilities for different scenarios.

🛠 How it works (core concepts)

-Evaluates proportional relationships between open, close, high, and low prices.

-Detects shifts in the balance of buying/selling pressure.

-Classifies trades by the number of prior consecutive losses.

-Calculates success probabilities based on accumulated historical data.

📈 What you get

-On-chart table showing entries, wins, losses, and win percentage.

-Dynamic colors to instantly spot the best-performing scenarios.

-Optional arrows marking moments when conditions are met.

-Filters and thresholds to adapt the analysis to your trading style.

💡 How to use it

-Set your preferred signal type and consecutive loss threshold.

-Monitor the table to see which sequences show higher probability.

-Use the signals as a reference and confirm with your own technical analysis.

⚠ Disclaimer: This tool is designed for market analysis and performance tracking. It should be used in combination with your own research, risk management, and decision-making process.

Franco Varacalli

XAUUSD Strength Dashboard with VolumeXAUUSD Strength Dashboard with Volume Analysis

📌 Description

This advanced Pine Script indicator provides a multi-timeframe dashboard for XAUUSD (Gold vs. USD), combining price action analysis with volume confirmation to generate high-probability trading signals. It detects:

✅ Break of Structure (BOS)

✅ Fair Value Gaps (FVG)

✅ Change of Character (CHOCH)

✅ Trendline Breaks (9/21 SMA Crossover)

✅ Volume Spikes (Confirmation of Strength)

The dashboard displays strength scores (0-100%) and action recommendations (Strong Buy/Buy/Neutral/Sell/Strong Sell) across multiple timeframes, helping traders identify confluences for better trade decisions.

🎯 How It Works

1. Multi-Timeframe Analysis

Fetches data from 1m, 5m, 15m, 30m, 1h, 4h, Daily, and Weekly timeframes.

Compares trend direction, BOS, FVG, CHOCH, and volume spikes across all timeframes.

2. Volume-Confirmed Strength Score

The Strength Score (0-100%) is calculated using:

Trend Direction (25 points) → 9 SMA vs. 21 SMA

Break of Structure (20 points) → New highs/lows with momentum

Fair Value Gaps (10 points) → Imbalance zones

Change of Character (10 points) → Shift in market structure

Trendline Break (20 points) → SMA crossover confirmation

Volume Spike (15 points) → High volume confirms moves

Score Interpretation:

≥75% → Strong Buy (High confidence bullish move)

60-74% → Buy (Bullish but weaker confirmation)

40-59% → Neutral (No strong bias)

25-39% → Sell (Bearish but weaker confirmation)

≤25% → Strong Sell (High confidence bearish move)

3. Dashboard & Chart Markers

Dashboard Table: Shows Trend, BOS, Volume, CHOCH, TL Break, Strength %, Key Level, and Action for each timeframe.

Chart Markers:

🟢 Green Triangles → Bullish BOS

🔴 Red Triangles → Bearish BOS

🟢 Green Circles → Bullish CHOCH

🔴 Red Circles → Bearish CHOCH

📈 Green Arrows → Bullish Trendline Break

📉 Red Arrows → Bearish Trendline Break

"Vol↑" (Lime) → Bullish Volume Spike

"Vol↓" (Maroon) → Bearish Volume Spike

🚀 How to Use

1. Dashboard Interpretation

Higher Timeframes (D/W) → Show the dominant trend.

Lower Timeframes (1m-4h) → Help with entry timing.

Strength Score ≥75% or ≤25% → Look for high-confidence trades.

Volume Spikes → Confirm breakouts/reversals.

2. Trading Strategy

📈 Long (Buy) Setup:

Higher TFs (D/W/4h) show bullish trend (↑).

Current TF has BOS & Volume Spike.

Strength Score ≥60%.

Key Level (Low) holds as support.

📉 Short (Sell) Setup:

Higher TFs (D/W/4h) show bearish trend (↓).

Current TF has BOS & Volume Spike.

Strength Score ≤40%.

Key Level (High) holds as resistance.

3. Customization

Adjust Volume Spike Multiplier (Default: 1.5x) → Controls sensitivity to volume spikes.

Toggle Timeframes → Enable/disable higher/lower timeframes.

🔑 Key Benefits

✔ Multi-Timeframe Confluence → Avoids false signals.

✔ Volume Confirmation → Filters low-quality breakouts.

✔ Clear Strength Scoring → Removes emotional bias.

✔ Visual Chart Markers → Easy to spot key signals.

This indicator is ideal for gold traders who follow institutional order flow, market structure, and volume analysis to improve their trading decisions.

🎯 Best Used With:

Support/Resistance Levels

Fibonacci Retracements

Price Action Confirmation

🚀 Happy Trading! 🚀

Correlation HeatMap Matrix Data [TradingFinder]🔵 Introduction

Correlation is a statistical measure that shows the degree and direction of a linear relationship between two assets.

Its value ranges from -1 to +1 : +1 means perfect positive correlation, 0 means no linear relationship, and -1 means perfect negative correlation.

In financial markets, correlation is used for portfolio diversification, risk management, pairs trading, intermarket analysis, and identifying divergences.

Correlation HeatMap Matrix Data TradingFinder is a Pine Script v6 library that calculates and returns raw correlation matrix data between up to 20 symbols. It only provides the data – it does not draw or render the heatmap – making it ideal for use in other scripts that handle visualization or further analysis. The library uses ta.correlation for fast and accurate calculations.

It also includes two helper functions for visual styling :

CorrelationColor(corr) : takes the correlation value as input and generates a smooth gradient color, ranging from strong negative to strong positive correlation.

CorrelationTextColor(corr) : takes the correlation value as input and returns a text color that ensures optimal contrast over the background color.

Library

"Correlation_HeatMap_Matrix_Data_TradingFinder"

CorrelationColor(corr)

Parameters:

corr (float)

CorrelationTextColor(corr)

Parameters:

corr (float)

Data_Matrix(Corr_Period, Sym_1, Sym_2, Sym_3, Sym_4, Sym_5, Sym_6, Sym_7, Sym_8, Sym_9, Sym_10, Sym_11, Sym_12, Sym_13, Sym_14, Sym_15, Sym_16, Sym_17, Sym_18, Sym_19, Sym_20)

Parameters:

Corr_Period (int)

Sym_1 (string)

Sym_2 (string)

Sym_3 (string)

Sym_4 (string)

Sym_5 (string)

Sym_6 (string)

Sym_7 (string)

Sym_8 (string)

Sym_9 (string)

Sym_10 (string)

Sym_11 (string)

Sym_12 (string)

Sym_13 (string)

Sym_14 (string)

Sym_15 (string)

Sym_16 (string)

Sym_17 (string)

Sym_18 (string)

Sym_19 (string)

Sym_20 (string)

🔵 How to use

Import the library into your Pine Script using the import keyword and its full namespace.

Decide how many symbols you want to include in your correlation matrix (up to 20). Each symbol must be provided as a string, for example FX:EURUSD .

Choose the correlation period (Corr\_Period) in bars. This is the lookback window used for the calculation, such as 20, 50, or 100 bars.

Call Data_Matrix(Corr_Period, Sym_1, ..., Sym_20) with your selected parameters. The function will return an array containing the correlation values for every symbol pair (upper triangle of the matrix plus diagonal).

For example :

var string Sym_1 = '' , var string Sym_2 = '' , var string Sym_3 = '' , var string Sym_4 = '' , var string Sym_5 = '' , var string Sym_6 = '' , var string Sym_7 = '' , var string Sym_8 = '' , var string Sym_9 = '' , var string Sym_10 = ''

var string Sym_11 = '', var string Sym_12 = '', var string Sym_13 = '', var string Sym_14 = '', var string Sym_15 = '', var string Sym_16 = '', var string Sym_17 = '', var string Sym_18 = '', var string Sym_19 = '', var string Sym_20 = ''

switch Market

'Forex' => Sym_1 := 'EURUSD' , Sym_2 := 'GBPUSD' , Sym_3 := 'USDJPY' , Sym_4 := 'USDCHF' , Sym_5 := 'USDCAD' , Sym_6 := 'AUDUSD' , Sym_7 := 'NZDUSD' , Sym_8 := 'EURJPY' , Sym_9 := 'EURGBP' , Sym_10 := 'GBPJPY'

,Sym_11 := 'AUDJPY', Sym_12 := 'EURCHF', Sym_13 := 'EURCAD', Sym_14 := 'GBPCAD', Sym_15 := 'CADJPY', Sym_16 := 'CHFJPY', Sym_17 := 'NZDJPY', Sym_18 := 'AUDNZD', Sym_19 := 'USDSEK' , Sym_20 := 'USDNOK'

'Stock' => Sym_1 := 'NVDA' , Sym_2 := 'AAPL' , Sym_3 := 'GOOGL' , Sym_4 := 'GOOG' , Sym_5 := 'META' , Sym_6 := 'MSFT' , Sym_7 := 'AMZN' , Sym_8 := 'AVGO' , Sym_9 := 'TSLA' , Sym_10 := 'BRK.B'