Combo Backtest 123 Reversal & Relative Volatility Index This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

The RVI is a modified form of the relative strength index (RSI).

The original RSI calculation separates one-day net changes into

positive closes and negative closes, then smoothes the data and

normalizes the ratio on a scale of zero to 100 as the basis for the

formula. The RVI uses the same basic formula but substitutes the

10-day standard deviation of the closing prices for either the up

close or the down close. The goal is to create an indicator that

measures the general direction of volatility. The volatility is

being measured by the 10-days standard deviation of the closing prices.

WARNING:

- For purpose educate only

- This script to change bars colors.

M-oscillator

Сalculation a position size based on riskThis is an example how to calculate position size based on risk and stop loss for educational purpose .

Combo Backtest 123 Reversal & Relative Momentum Index This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

The Relative Momentum Index (RMI) was developed by Roger Altman. Impressed

with the Relative Strength Index's sensitivity to the number of look-back

periods, yet frustrated with it's inconsistent oscillation between defined

overbought and oversold levels, Mr. Altman added a momentum component to the RSI.

As mentioned, the RMI is a variation of the RSI indicator. Instead of counting

up and down days from close to close as the RSI does, the RMI counts up and down

days from the close relative to the close x-days ago where x is not necessarily

1 as required by the RSI). So as the name of the indicator reflects, "momentum" is

substituted for "strength".

WARNING:

- For purpose educate only

- This script to change bars colors.

Supertrend - IntradaySupertrend Intraday Strategy

Basic supertrend strategy purpose built for intraday trading. Users can define intraday session during which the strategy will run.

Position is reversed when signal changes by using double quantity. Once the intraday session is over & if the position is open; it is squared off.

Parameters:

Intraday Session - Defines the duration for which the strategy should execute.

Multiplier

ATR Period

Combo Backtest 123 Reversal & Recursive Moving Trend Average This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

Taken from an article "The Yen Recused" in the December 1998 issue of TASC,

written by Dennis Meyers. He describes the Recursive MA in mathematical terms

as "recursive polynomial fit, a technique that uses a small number of past values

of the estimated price and today's price to predict tomorrows price."

Red bars color - short position. Green is long.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & RAVI This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

The indicator represents the relative convergence/divergence of the moving

averages of the financial asset, increased a hundred times. It is based on

a different principle than the ADX. Chande suggests a 13-week SMA as the

basis for the indicator. It represents the quarterly (3 months = 65 working days)

sentiments of the market participants concerning prices. The short moving average

comprises 10% of the one and is rounded to seven.

WARNING:

- For purpose educate only

- This script to change bars colors.

Daily PercentR StrategyThe PercentR strategy from Larry Williams is highly profitable on the daily nasdaq chart

Buy at the open if PercentR Indicator is above –87 and below –20

Exit at the end of the day.

Simple MACD strategy Simple macd strategy

Rules:

if MACD bullish crosses below 0 and above 200 EMA a buy signal is created

if MACD bearish crosses above 0 and below 200 EMA a sell signal is created

best settings for winrate and profit :

1. is taking 1:1 trades so with a tp of 2% and sl of 2% winrate is around 62%

Moriceau_Crypto_strategies_Long_short_indicator_ThesisAfter 3 years of analysis and trading I decided to publish a modify version of my indicator of my thesis. It not a recommandation of trade or an advice it is just for training

The Goal Of this indicator is to avoid sell panic and Maximise drawdown and Money management I used mainly KRAKEN:BCHEUR but you can use it at you own risk on equity or other Crypto

You have the possibility to manage your trade with this indicator and allow you to Buy and Sell (Vente) But also to Short

The Profitability over the past 10 days on 1 min chart 23% against -33 buy and Hold, Over 1 hour candle over the years is 180% against 238% buy and hold. So it is for that you have to use it Mainly on 1 min candles chart.

If you have any question let me know.

Combo Backtest 123 Reversal & Rainbow Oscillator This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

Ever since the people concluded that stock market price movements are not

random or chaotic, but follow specific trends that can be forecasted, they

tried to develop different tools or procedures that could help them identify

those trends. And one of those financial indicators is the Rainbow Oscillator

Indicator. The Rainbow Oscillator Indicator is relatively new, originally

introduced in 1997, and it is used to forecast the changes of trend direction.

As market prices go up and down, the oscillator appears as a direction of the

trend, but also as the safety of the market and the depth of that trend. As

the rainbow grows in width, the current trend gives signs of continuity, and

if the value of the oscillator goes beyond 80, the market becomes more and more

unstable, being prone to a sudden reversal. When prices move towards the rainbow

and the oscillator becomes more and more flat, the market tends to remain more

stable and the bandwidth decreases. Still, if the oscillator value goes below 20,

the market is again, prone to sudden reversals. The safest bandwidth value where

the market is stable is between 20 and 80, in the Rainbow Oscillator indicator value.

The depth a certain price has on a chart and into the rainbow can be used to judge

the strength of the move.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & Qstick Indicator This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

A technical indicator developed by Tushar Chande to numerically identify

trends in candlestick charting. It is calculated by taking an 'n' period

moving average of the difference between the open and closing prices. A

Qstick value greater than zero means that the majority of the last 'n' days

have been up, indicating that buying pressure has been increasing.

Transaction signals come from when the Qstick indicator crosses through the

zero line. Crossing above zero is used as the entry signal because it is indicating

that buying pressure is increasing, while sell signals come from the indicator

crossing down through zero. In addition, an 'n' period moving average of the Qstick

values can be drawn to act as a signal line. Transaction signals are then generated

when the Qstick value crosses through the trigger line.

WARNING:

- For purpose educate only

- This script to change bars colors.

RatingsThis strategy script is a modified version of the built-in 'Technical Ratings' strategy script.

English:

www.tradingview.com

Russian:

www.tradingview.com

Changes:

1) Added option to disable long and short positions (checkboxes 'Long' and 'Short').

2) Added date selection option.

3) The default commission is 0.1% (original 0%).

4) 100% of capital is used by default (5% in the original version).

cRSI + Waves Strategy with VWMA overlay + sessions and order qtyThis is a fork of the cRSI + Waves Strategy with VWMA overlay strategy by Dr_Roboto , which adds two additional features, namely:

the ability to limit trade signals to certain defined periods of time ("Sessions") during the trading day and, optionally, to close any open position at the end of either or both "Sessions"

the ability to control the maximum order size suggested by the strategy on the "Inputs" tab of the strategy's "Settings" window

If you are trading on a daily chart (or longer) you must disable the Limit Signals to Trading Sessions? option in order for the strategy to produce signals.

All other features are identical to the original strategy (revision 2.0).

Jaws Mean Reversion [Strategy]This very simple strategy is an implementation of PJ Sutherlands' Jaws Mean reversion algorithm. It simply buys when a small moving average period (e.g. 2) is below

a longer moving average period (e.g. 5) by a certain percentage and closes when the small period average crosses over the longer moving average.

If you are going to use this, you may wish to apply this to a range of investment assets using a screener for setups, as the amount signals are low. Alternatively, you may wish to tweak the settings to provide more signals.

Context can be found here:

LINK

Wave Trend w/ VWMA overlayThis is a trend-following strategy and indicator which combines the Wave Trend Strategy (Lazy Bear) by thomas.gigure with the cRSI + Waves Strategy with VWMA overlay by Dr_Roboto .

You may update the parameters of the Wave Trend oscillator or the VWMA indicator to match your own preferences. You may also adjust the Base Quantity used for determining trade size (as described below) to suit your account size and risk tolerance.

The strategy identifies potential signals based on the on the Wave Trend oscillator, originally ported to TradingView by LazyBear. When a signal is produced by the Wave Trend oscillator, trade size is determined by the VWMA.

When the VWMA is trending against the direction of the Wave Trend signal, Base Quantity x 1 is used

When the VWMA is trending neutral, Base Quantity x 2 is used

When the VWMA is trending with the direction of the Wave Trend signal, Base Quantity x 4 is used

The strategy includes the ability to limit trade signals to certain defined periods of time ("Sessions") during the trading day and, optionally, to close any open position at the end of either or both "Sessions." This may be enabled/disabled via the Limit Signals to Trading Sessions? option on the "Inputs" tab of the strategy's "Settings" window.

If you are trading on a daily chart (or longer) you must disable the Limit Signals to Trading Sessions? in order for the strategy to produce signals.

Sentiment OscillatorPrice moves when there are more market takers than there are market makers at a certain price (i.e. price moves up when there are more market buys than limit sells and vice versa). The idea of this indicator is to show the ratio between market takers and market makers in a way that is intuitive to technical analysis methods, and hopefully revealing the overall sentiment of the market in doing so. You can use it in the same way you would other oscillators (histogram crossing zero, divergences, etc). The main difference between this and most volume-weighted indicators is that the price is divided by volume instead of multiplied by it, thus giving you a rough idea of how much "effort" it took to move the price. My hypothesis is that when more volume is needed to move the price, that means bulls and bears are not in agreement of what the "fair price" should be for an asset (e.g. if the candle closes only a bit higher than its open but there's a huge spike in volume, that tells you that a majority of the market are starting to think the price is too high and they've started selling).

Methods of Calculation

1. Price Change Per Volume

The main method this indicator uses to reveal market sentiment is by comparing price change to the volume of trades in a bar.

You will see this calculation plotted in its most basic form by ticking the "Show Bar per Bar Change/Volume" box in the inputs dialog. I personally found that the plots were too noisy and cannot be used in real time reliably due to the fact that there is not much volume at the open of a new bar. I decided to leave in the option to use this method, in case you'd like to experiment with it or get a better grasp of how the indicator works.

2. Exponential Moving Averages

In my quest to smooth out the plotted data, I experimented with exponential moving averages. Applying an EMA on the change per volume data did smooth it out a bit, but still left in a lot of noise. So I worked around it by applying the EMA to the price change first, and then dividing it by the EMA of the volume. The term I use for the result of this calculation is "Market Sentiment" (do let me know if you have a better-fitting term for it ;-)), and I have kept it as an option that you can use in the way you would use other oscillators like CMF, OBV, etc. This option is unticked by default.

3. MACD

I left "Market Sentiment" unchecked as the default option because I thought an easier way to use this indicator would be as a momentum indicator like the MACD . So that's what I turned it into! I applied another EMA on the Market Sentiment, added a slower EMA to subtract from the first, and now we have a MACD line. I added a signal line to subtract from the MACD , and the result is plotted as a histogram... ish . I used area instead of columns for plot style so you don't get confused when comparing with a regular MACD indicator, but you can always change it if an actual histogram is more your taste.

The "histogram" is the main gauge of sentiment change momentum and it is easiest to use, that is why it is the only calculation plotted by default.

Methods of Use

As I have mentioned before, you can use this as you would other oscillators.

-The easiest way to use this indicator is with the Momentum histogram, where crosses over 0 indicate increasing bullish sentiment, and crosses below 0 indicate increasing bearish sentiment. You may also spot occasional divergences with the histogram.

-For the Market Sentiment option, the easiest way to use it is to look for divergences.

-And if you use the "Price Change per Volume of Each Bar", well... I honestly don't know. I guess divergences would be apparent towards the close of a bar, but in realtime, I don't recommend you use this. Maybe if you'd like to study the market movement, looking at historical data and comparing price, volume , and Change per Volume of each bar would come in handy in a pseudo-tape-reading kind of way.

Anyway, that's my explanation of this indicator. The default values were tested on BTC/USDT (Binance) 4h with decent results. You'll have to adjust the parameters for different markets and timeframes.

I have published this as a strategy so you can test out how the indicator performs as you're tweaking the parameters.

I'm aware that the code might not be the cleanest as I have only started learning pine (and code in general) for about a month, so any suggestions to improve the script would be appreciated!

Good luck and happy trading :-)

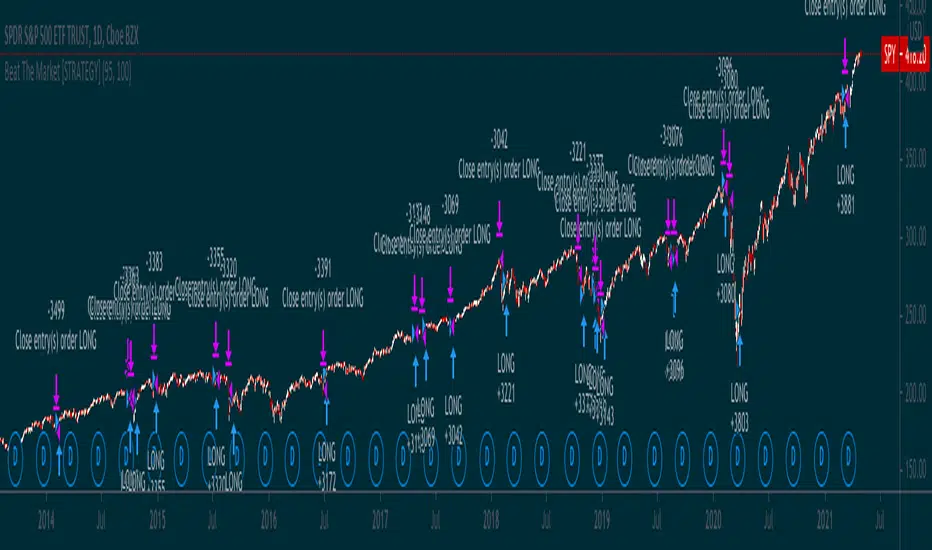

Simple way to BEAT the market [STRATEGY]This script has been created to demonstrate the effectiveness of using market regime filters in your trading strategy, and how they can improve your returns and lower your drawdowns

This strategy adds a simple filter (A historical volatility percentile filter, an implementation of which can be found on my trading profile) to a traditional buy and hold strategy of the index SPY.

Note, There are other filters that could also be added including a long-term moving average/percentile rank filter/ADX filter etc, to improve the returns further.

The filter closes our long position during periods of volatility that exceed the 95th percentile (or in the top 5% of volatile days) and buys back when the volatility is below 95% rank of the past 100 days

Have included the backtest results since 1993 which is 28 years of data at the time of writing. Comparison of traditional buy and hold with this modified strategy can be found below:

Traditional buy and hold:

Return per year: 7.95 % (ex Dividends)

Total return: 851.1 %

Max drawdown: 50.79 %

'Modified' buy and hold (this script):

Return per year: 9.92 % (ex Dividends)

Total return: 1412.2 %

Max drawdown: 31.57 %

Feel free to use some of the market filters in my trading profile to improve and refine your strategies further, or make a copy and play around with the code yourself. This is just a simple example for demo purposes.

Strategy - DMI Indicator with DPO Indicator as a GuardThe Directional Movement Index Indicator is one of my favorite indicators in tradingview's built-in library. It is free to use for all

For more information on what the DMI is, please visit: www.tradingview.com

The only problem I've come across with the DMI is that when it hits a 'trade range zone' it triggers false new trends (this is the case with almost every indicator I've ever tested).

This script modifies the DMI by removing the need for the ADX logic. It only focuses on the +DI and the -DI.

In order to remove the 'noise' generated during a trade range zone I have added another powerful indicator called the Detrended Price Oscillator.

The DPO is also a 'built-in' indicator on tradingview. www.tradingview.com

The DPO is used in conjunction with the DMI to stop trade ranges from wrecking your profits.

This strategy logic simply checks for the DMI indicator to cross itself. If the +DI crosses over the -DI this is a bullish cross and visa versa, if the -DI crosses over the +DI then it could mean bearish sentiment is building.

But then strategy logic uses the DPO to check if the DPO is above 0 or below 0 value

If the +DI crosses over the -DI and the DPO is above 0 value, then it's a Long entry point.

However, if the +DI crosses over the -DI and the DPO is below 0 value, then the Long signal is void.

And visa versa, if the -DI crosses over the +DI and the DPO is below 0 value, then it's a Short entry point (unless the DPO is greater than 0)

With this DPO 'guard' in place, it helps us keep the total trades executed to a minimum.

This is vital to push through trade ranges that can wreck your profit potential.

I wish I could create a better plotting mechanism for this indicator so you can better see the visuals. But combining the DMI to scale with the DPO is not possible.

The best solution is to simply add another DMI indicator to your chart so you can compare the DMI to this script that is dominated by the DPO (yellow line).

Enjoy! Likes are much appreciated!

DRSI DMA Scalping Strategy No RepaintThis strategy compares the slope of a Moving Average (of your choosing) to the slope of a Momentum Indicator (of your choosing). Zero is the center line because 0 slope means sideways movement. When both lines cross your buy threshold, it buys. When both lines cross your Sell threshold, it sells. The lines may look choppy, but that is probably because it is referencing a different timeframe than what the chart is set to. I left as many settings adjustable by the user as possible so you can tune this strategy to the relative behavior of whatever you are trading.

This also includes a No Repaint function so the backtest should be as close to live trading as possible.

Combo Backtest 123 Reversal & Psychological line This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

Psychological line (PSY), as an indicator, is the ratio of the number of

rising periods over the total number of periods. It reflects the buying

power in relation to the selling power.

If PSY is above 50%, it indicates that buyers are in control. Likewise,

if it is below 50%, it indicates the sellers are in control. If the PSY

moves along the 50% area, it indicates balance between the buyers and

sellers and therefore there is no direction movement for the market.

WARNING:

- For purpose educate only

Jigga - Heatmap ComparisionHi All,

I always have a question on how to know which sector is performing. I have created this Heatmap comparison to know strength of sector.

I have used RSI and MACD calculation and put it across 5 different index. Color shows bullishness and Gray shows weakness.

You can select RSI or MACD or Both to have calculation. And you can also compare stocks if you want.

Note: Use it for Medium / Long term investment. Can not be use for Intraday.

Happy investing !!

Linear RSIThis is an attempt to create a strategy based on the previous post. The strategy, as before, is based on the RSI, which is calculated using linear regression, but with the addition of EMA. The crossing of EMA and RSI is a buy and sell signal. There are also two functions to buy (because I haven't decided which is really better), so please use checkbox to order which one you would like to use.

Combo Backtest 123 Reversal & Prime Number Oscillator This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

Determining market trends has become a science even though a high number or people

still believe it’s a gambling game. Mathematicians, technicians, brokers and investors

have worked together in developing quite several indicators to help them better understand

and forecast market movements.

Developed by Modulus Financial Engineering Inc., the prime number oscillator indicates the

nearest prime number, be it at the top or the bottom of the series, and outlines the

difference between that prime number and the respective series.

WARNING:

- For purpose educate only

- This script to change bars colors.