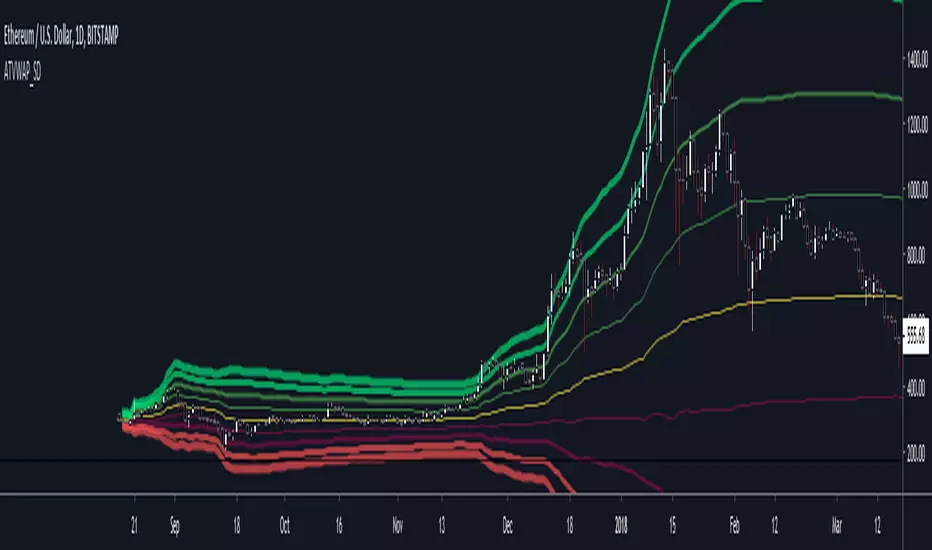

All Time VWAP & Standard DeviationsAll time VWAP and standard deviations.

Either enable "scale price chart only" or disable deviations that go negative in the style options.

--------------------------------------

If you find it useful please consider a tip/donation :

BTC - 3BMEXEDyWJ58eXUEALYPadbn1wwWKmf6sA

--------------------------------------

"vwap"に関するスクリプトを検索

Volume Trends (VWMA & VWAP)Basic indicator for tracking volume trends. Includes blue SMA and pink VWMA (volume-weighted moving average), to help gauge the strength of price movement -- is it supported by volume, or is there divergence. Intraday charts also have VWAP (volume-weighted average price) as dark purple dots.

Here's a couple of good articles explaining how to use them effectively:

www.tradeciety.com

stockcharts.com

Adjustable Starting VWAPIn this script it's possible adjust the start where the VWAP (technically is a VWMA) starts to calculate.

Use this to try to show where is the suport and resistance.

I coded 6 lines.

Use low sources for suport.

Use high sources for resistance.

Volume Weighted Average Price Oscillator [NeoButane]VWAP on PPO but not PPO. Two histograms, with the second one being SMAs of the first and signals color/trend change.

1.0 - Release

Framework laid out

Power level readings should be within 9000

Triple Anchored Volume Weighted Average Price [JustinPrime]This indicator provides three separate Volume Weighted Average Price (VWAP) calculations, each anchored from different key points on the chart:

High Anchored VWAP: Resets from the highest price reached since the start date.

Low Anchored VWAP: Resets from the lowest price since the start date.

Start Date VWAP: Calculated from the trading data beginning at the user-defined start date.

Features:

Selectable Timeframe: Choose from timeframes like 1 minute, 5 minutes, 15 minutes, 1 hour, daily, and weekly.

Custom Start Date: Set a specific start date for the VWAP calculations.

Source Data: Uses high, low, and close prices (HLC3) for calculations.

How to Use:

Adjust the start date to focus on significant market periods or events.

Differentiate each VWAP with unique colors for clarity.

MultiWAPThe VWAP tracks the average price, giving weight to each candle based upon its' relative volume.

In other words, high-volume candles move the VWAP faster than low-volume candles.

On a good day, market maker:

-Buys the dip

-Pumps past resistance, causing bullish FOMO

-Sells into the bullish FOMO, causing bearish FOMO

-Buys the dip (rinse and repeat)

By default, MultiWAP begins at the first visible bar.

Range low/high - tracks the most recent high/low

Upper VWAP - tracks retail's average buy price (MM is selling)

Lower VWAP - tracks MM's average buy price (MM is buying)

If price closes below the lower VWAP or the range low, the lower VWAP and range low are reset.

If price closes above the upper VWAP or the range high, the upper VWAP and range high are reset.

Resets are indicated by the dots. Resetting either VWAP moves it close to last price, making it easy to breach again.

A down-trend that lasts many bars will produce a string of green dots. When the accumulation phase ends, price pulls away from the lower VWAP, so it stops resetting. The ABSENCE of green dots tells you that we're in the markup phase/up-trend.

An up-trend that lasts many bars will produce a string of red dots. When the distribution phase ends, price pulls away from the upper VWAP, so it stops resetting. The ABSENCE of red dots tells you that we're in the markdown phase/down-trend.

By default, the net result is two VWAP's that automatically anchor themselves to the most recent, significant, and visible, high and low.

Usage:

For any timeframe, I recommend starting zoomed way out. Find the last green dot and drop an "Anchored VWAP" there. Now, zoom in until that candle is no longer visible. Find the last green dot and drop an anchored VWAP there. Continue doing so until you notice the lower VWAP getting reset to basically the same place.

This works the same, in reverse, during down-trends.

Spot v Perp aggrRollingVWAPThis indicator is a rolling VWAP that shows an aggregated BTC VWAP for both spot markets and futures markets

Spot VWAP is shown in BTC orange while perp VWAP is shown in blue

This is useful for identifying which market (spot or perps) is pushing trending moves

If the spot VWAP is more closely following the trend, then spot is pushing the move

If the perp VWAP is more closely following the trend, then perps are pushing the move

e.g. In the following picture you can see that the move down was followed much more closely by the spot VWAP, therefore you can assume that the move is being pushed my spot

Two Days Auto Anchored VWAPEasier way to set anchors to today and last trading day's open.

All you need to do is to select today from the dates picker in Setting ➔ Inputs ➔ Anchor Today .

If last workday is holiday for the market, then overwrite by selecting Manually Set Prev Day

Next update: auto set today's anchor, so completely automatic

Custom_AVWAP_Harpal's-AnchorsAutomated VWAP Indicator written in PineScript for TradingView charts. Automatically Anchored at key swing H/L levels extracted from price and volume time-series.

Indicator takes one Argument, "LookBack (# of Periods)", and then for a given security finds three key anchors, the highest and lowest values in the 'hlc3' column (average of high low and close on the daily timeframe) in the last 'LookBack' # of days. The script displays up to three color coded time-series corresponding to a trailing Volume Weighted Average Price beginning at the anchor dates corresponding to the anchor points listed above.

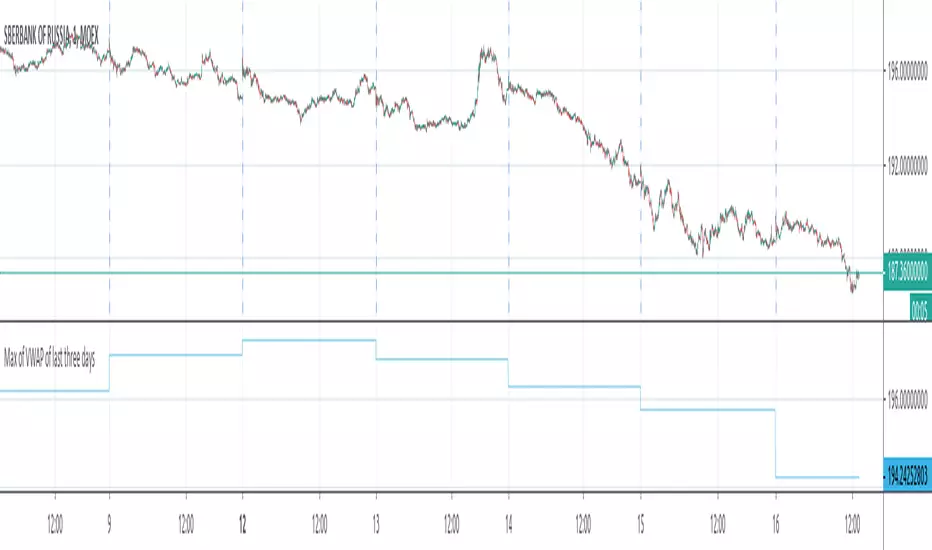

Max of VWAP of last three daysThe script searches for max values of last three days and then calculates average of those values

TurboVWAPVWAP indicator based in the built-in one but completely rewritten. Features:

- more standard deviation bands, up to 3.

- added the possibility to not anchor the VWAP but make it a rolling one instead, like a VWMA, being in this case able to specify days, hours or minutes for the rolling VWAP.

- for rolling VWAPs, the indicator doesn't count bars but real days, hours or minutes instead, so regardless of the chart timeframe the indicator will always show the correct values.

- for rolling VWAPs, if you specify x days as the rolling time, the indicator will always count exactly 24 hours from the current time backwards - so, from the same time yesterday or x days ago.

- in rolling VWAPs, although the indicator counts real time elapsed as per your settings and not chart bars, it will automatically skip holidays, so you needn't worry about that.

- for the anchored VWAP, added the possibility to specify custom session times (for example, for ES 0830-1500, instead of Globex, which is the Tradingview default as of today)

- complete customization of all fills and linetypes

For illustration purposes in the attached 1min chart I have:

- a 30min rolling VWAP in BLUE with no standard deviation plots,

- a 1 day rolling VWAP in RED with standard deviations in light red and green (these are the default settings)

- a RTH-session-anchored VWAP in ORANGE with standard deviations in light orange and light blue

VWAP, MFI, RSI with S/R StrategyBest for 0dte/intraday trading on AMEX:SPY with 1 minute chart

Strategy Concept

This strategy aims to identify potential reversal points in a price trend by combining momentum indicators (RSI and MFI), volume-weighted price (VWAP), and recent price action trends. It looks for conditions where the price is poised to change direction, either bouncing off a support level in a potential uptrend or falling from a resistance level in a potential downtrend.

By incorporating both price level analysis (support/resistance) and momentum indicators, the strategy seeks to increase the likelihood of identifying significant trend reversals, taking into consideration both recent price movements and the current price's position relative to historical highs and lows.

VWAP (Volume-Weighted Average Price)

VWAP acts as a benchmark to determine the general market trend. It's an average price weighted by volume.

A price above VWAP is often considered bullish, and a price below VWAP is seen as bearish.

MFI (Money Flow Index) and RSI (Relative Strength Index) Parameters

MFI is a volume-weighted RSI, used to identify overbought (above 70) or oversold (below 30) conditions.

RSI is a momentum indicator that measures the magnitude of recent price changes to identify overbought or oversold conditions, similar to MFI.

The script uses standard overbought (70) and oversold (30) thresholds for both MFI and RSI.

Trend Check Function

The function trendCheck analyzes the past pastBars candles to count how many were bullish (closing price higher than the opening price) and bearish.

This function is used to assess the recent trend direction.

Support and Resistance Detection

The script calculates the highest high (highestHigh) and lowest low (lowestLow) over the last lookbackSR (50) periods to identify potential support and resistance levels.

isNearSupport and isNearResistance are conditions to check if the current price is within 0.08% of these identified levels, indicating proximity to support or resistance.

Buy and Sell Logic

Buy Signal:

The RSI crosses over the oversold threshold (30).

The MFI is also below its oversold level (30).

The current price is above the VWAP.

The recent trend (past 20 bars) has been predominantly bearish.

The price is near the identified support level.

Sell Signal:

The RSI crosses under the overbought threshold (70).

The MFI is above its overbought level (70).

The current price is below the VWAP.

The recent trend has been predominantly bullish.

The price is near the identified resistance level.

Vwap MTFExplanatory Note: VWAP Multi-Timeframe Script (Dedicated to Intraday Trading)

Description:

This Pine script has been specifically designed for intraday traders to display the VWAP (Volume Weighted Average Price) from four different timeframes (15 minutes, 1 hour, 4 hours, and daily) on a single TradingView chart. The VWAP is calculated by considering the volume-weighted average price over a specified period, providing a perspective on the market's average value. This script streamlines your analysis by avoiding the need to navigate through multiple timeframes to identify the trend.

Usage Instructions:

Apply the script to your TradingView chart.

The script will showcase the average VWAP for 15 minutes, 1 hour, 4 hours, and daily on the current chart.

The color of the VWAP indicates the direction: blue if the VWAP is higher than the previous period, red otherwise.

Parameters:

VWAP Period Length (length): The length of the period used for VWAP calculation. By default, the length is set to 30 bars.

Explanation of VWAP: "This VWAP will be more precise for your analysis and closer to price/volume."

VWAP is a crucial indicator for intraday traders, taking into account transaction volume. It provides a volume-weighted average price over a specified period, assisting traders in evaluating the average value at which an asset has been traded throughout the day. "It can be wise for the self-directed investor to use VWAP in combination with moving averages or other technical indicators to confirm buy and sell signals."

You have the option to change the colors.

Relative Average Extrapolation [ChartPrime]Relative Average Extrapolation (ChartPrime) is a new take on session averages, like the famous vwap . This indicator leverages patterns in the market by leveraging average-at-time to get a footprint of the average market conditions for the current time. This allows for a great estimate of market conditions throughout the day allowing for predictive forecasting. If we know what the market conditions are at a given time of day we can use this information to make assumptions about future market conditions. This is what allows us to estimate an entire session with fair accuracy. This indicator works on any intra-day time frame and will not work on time frames less than a minute, or time frames that are a day or greater in length. A unique aspect of this indicator is that it allows for analysis of pre and post market sessions independently from regular hours. This results in a cleaner and more usable vwap for each individual session. One drawback of this is that the indicator utilizes an average for the length of a session. Because of this, some after hour sessions will only have a partial estimation. The average and deviation bands will work past the point where it has been extrapolated to in this instance however. On low time frames due to the limited number of data points, the indicator can appear noisy.

Generally crypto doesn't have a consistent footprint making this indicator less suitable in crypto markets. Because of this we have implemented other weighting schemes to allow for more flexibility in the number of use cases for this indicator. Besides volume weighting we have also included time, volatility, and linear (none) weighting. Using any one of these weighting schemes will transform the vwap into a wma, volatility adjusted ma, or a simple moving average. All of the style are still session period and will become longer as the session progresses.

Relative Average Extrapolation (ChartPrime) works by storing data for each time step throughout the day by utilizing a custom indexing system. It takes the a key , ie hour/minute, and transforms it into an array index to stor the current data point in its unique array. From there we can take the current time of day and advance it by one step to retrieve the data point for the next bar index. This allows us to utilize the footprint the extrapolate into the future. We use the relative rate of change for the average, the relative deviation, and relative price position to extrapolate from the current point to the end of the session. This process is fast and effective and possibly easier to use than the built in map feature.

If you have used vwap before you should be familiar with the general settings for this indicator. We have made a point to make it as intuitive for anyone who is already used to using the standard vwap. You can pick the source for the average and adjust/enable the deviation bands multipliers in the settings group. The average period is what determines the number of days to use for the average-at-time. When it is set to 0 it will use all available data. Under "Extrapolation" you will find the settings for the estimation. "Direction Sensitivity" adjusts how sensitive the indicator is to the direction of the vwap. A higher number will allow it to change directions faster, where a lower number will make it more stable throughout the session. Under the "Style" section you will find all of the color and style adjustments to customize the appearance of this indicator.

Relative Average Extrapolation (ChartPrime) is an advanced and customizable session average indicator with the ability to estimate the direction and volatility of intra-day sessions. We hope you will find this script fascinating and useful in your trading and decision making. With its unique take on session weighting and forecasting, we believe it will be a secret weapon for traders for years to come.

Enjoy

Temporary imbalancesThis indicator is designed to identify imbalances in order flow and market liquidity, It highlights candles with significant imbalances and draws reference lines

The indicator calculates imbalance based on changes in closing prices and volume. It uses the standard deviation to determine the significant imbalance threshold. Candles with bullish imbalances are highlighted in green, while candles with bearish imbalances are highlighted in red.

Furthermore, the indicator includes features of latency arbitrage and liquidity analysis. Latency arbitrage looks for price differences between the anchored VWAP and bid/ask quotes, targeting trading opportunities based on these differences. The liquidity analysis verifies the liquidity imbalance and calculates the VWAP anchored on this value in total using 4 VWAP.

This indicator can be adjusted according to the preferences and characteristics of the specific asset or market. It provides clear visual information and can be used as a complementary tool for technical analysis in trading strategies.

Interesting Segment Length 20,50,80,200

and Interesting lookback period 20,50,80,200

Interesting imbalance threshold 1.5, 2.4, 3.3 ,4.2

Este indicador é projetado para identificar desequilíbrios no fluxo de ordens e na liquidez do mercado, Ele destaca velas com desequilíbrios significativos e traça linhas de referência

O indicador calcula o desequilíbrio com base nas mudanças nos preços de fechamento e no volume. Ele usa o desvio padrão para determinar o limiar de desequilíbrio significativo. As velas com desequilíbrios de alta são destacadas em verde, enquanto as velas com desequilíbrios de baixa são destacadas em vermelho.

Além disso, o indicador inclui recursos de arbitragem de latência e análise de liquidez. A arbitragem de latência procura diferenças de preços entre a VWAP ancorada e as cotações de compra/venda, visando oportunidades de negociação com base nessas diferenças. A análise de liquidez verifica o desequilíbrio de liquidez e calcula a VWAP ancorada nesse valor ao total utiliza 4 VWAP.

Este indicador pode ser ajustado de acordo com as preferências e características do ativo ou mercado específico. Ele fornece informações visuais claras e pode ser usado como uma ferramenta complementar para análise técnica em estratégias de negociação.

Comprimento do Segmento interessante para usa 20,50,80,200

e Período de lookback interessante para usa 20,50,80,200

Limiar de desequilíbrio interessante para usa 1.5 ,2.4, 3.3 ,4.2

VWAP and MA Crossover SignalsDescription: The VWAP and 20 MA Crossover Indicator is a powerful trading tool designed to capitalize on trend reversals and momentum shifts. This indicator overlays two key technical analysis tools on the price chart: the Volume Weighted Average Price (VWAP) and the 20-period Moving Average (MA).

Functionality:

VWAP: Represents the average price a security has traded at throughout the day, based on volume and price. It is a measure of the market's trend and trading volume.

20 MA: Offers a smoothed average of the closing prices over the last 20 periods, providing a glimpse of the underlying trend.

Signals:

Buy Signal: Generated when the VWAP crosses above the 20-period MA, suggesting an upward momentum and a potential bullish trend reversal.

Sell Signal: This occurs when the VWAP crosses below the 20-period MA, indicating a downward momentum and a potential bearish trend reversal.

Usage: This indicator is ideal for traders focusing on intraday and swing trading strategies, providing clear visual cues for entry and exit points based on the interaction between VWAP and the 20 MA. By identifying key crossover points, traders can make informed decisions about potential bullish or bearish movements in the market.

Application: To use this indicator, simply add it to your TradingView chart setup. The buy and sell signals will be displayed directly on the chart, allowing for easy interpretation and quick action. Adjust the settings to fit your specific trading strategy or market conditions.

VWAP/EMA50/EMA200We script this one for combining VWAP , EMA50 and EMA200. The tool is fantastic if traders know how VWAP , EMA work? Just adding this script in your favorite and work like charm:

VWAP: How to trade with that

- One of the simplest uses of the VWAP is gauging support and/or resistance.

- A trader who is long a stock can use the VWAP as a target exit if its trading below.

- A stock trading over intraday VWAP may be bullish , while a stock trading under may be bearish .

EMA 50/EMA200: How to trade with that timeframe 50-day or 200-day period

- Identify the trend of market in longterm

- Golden-cross (short term EMA cross above longterm EMA ) is call golden-cross signals. It is opportunity for buying.

- Deal-cross ( short term EMA cross below longterm EMA ) is call dead-cross signals. It is opportunity for selling.

- Identify support levels

- Identify resistance levels

Let me know if you see anything else that should be added/changed.