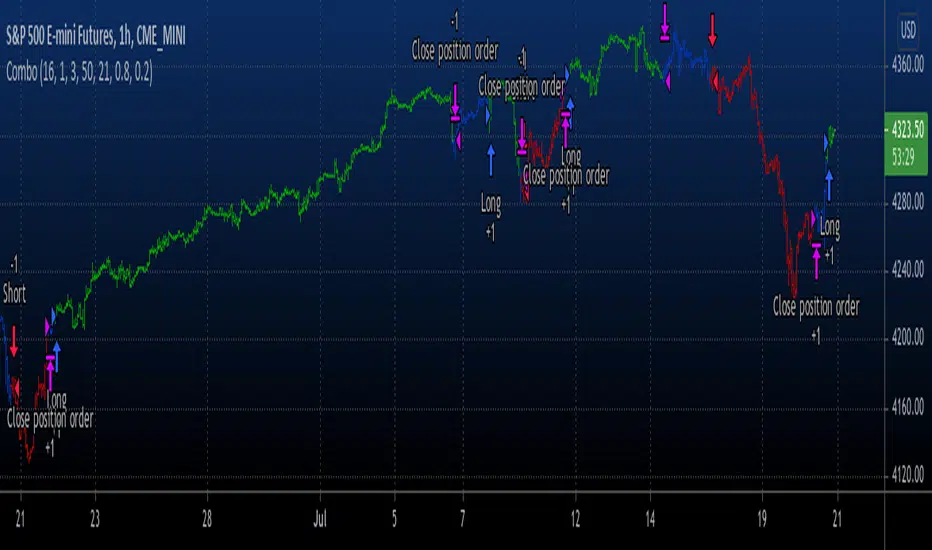

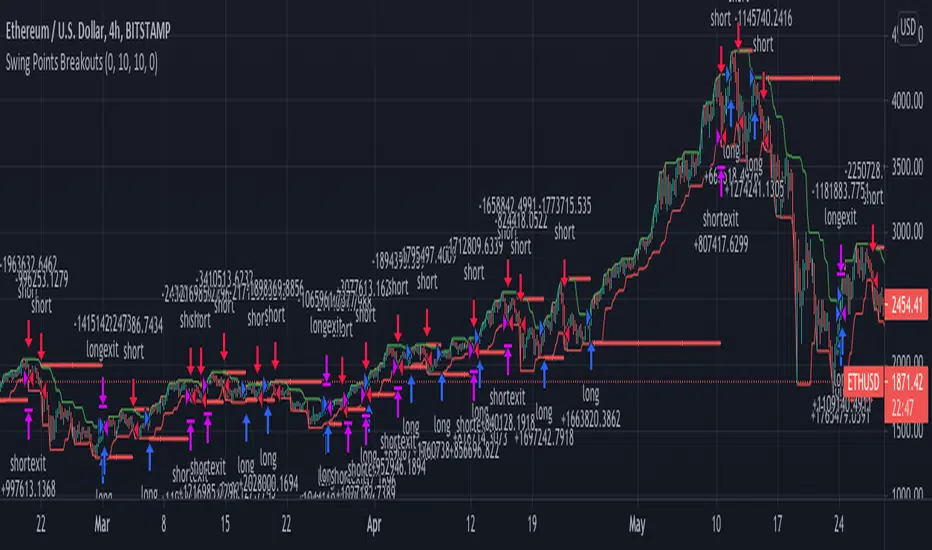

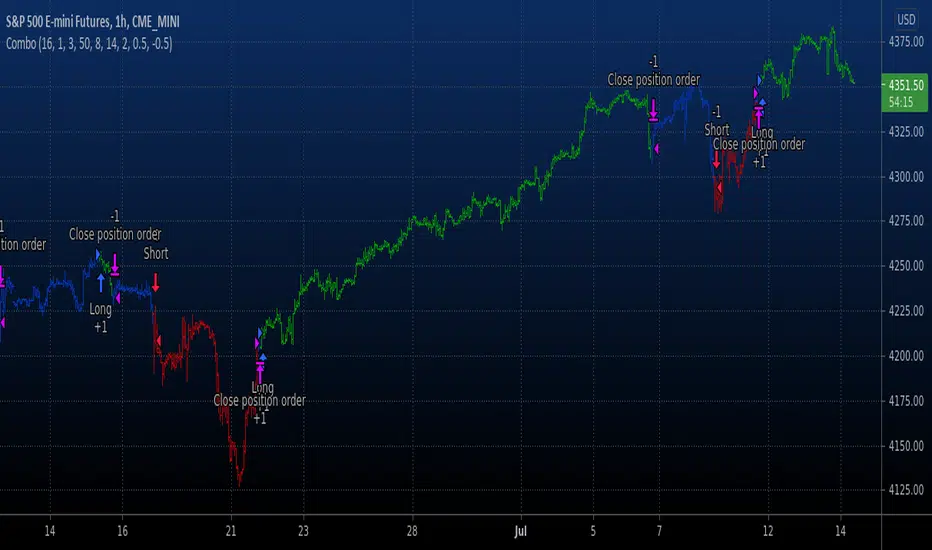

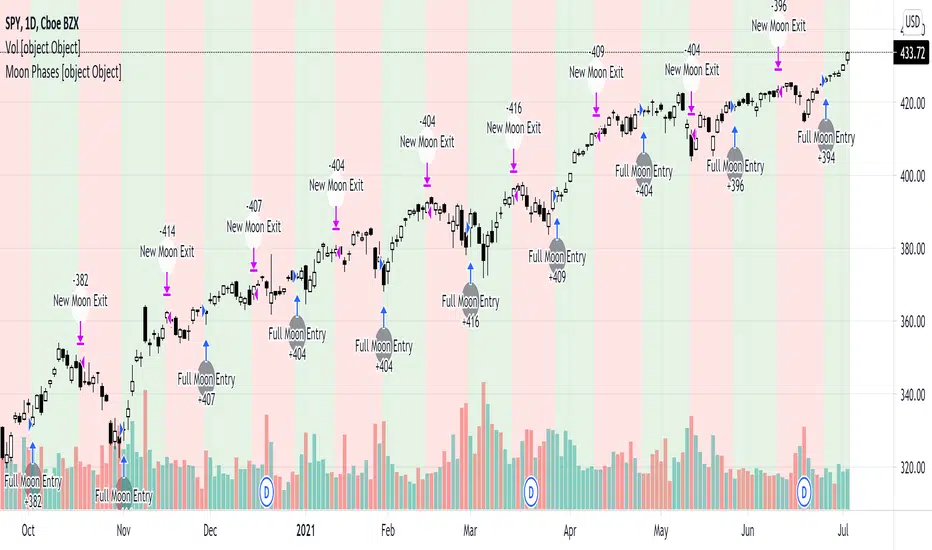

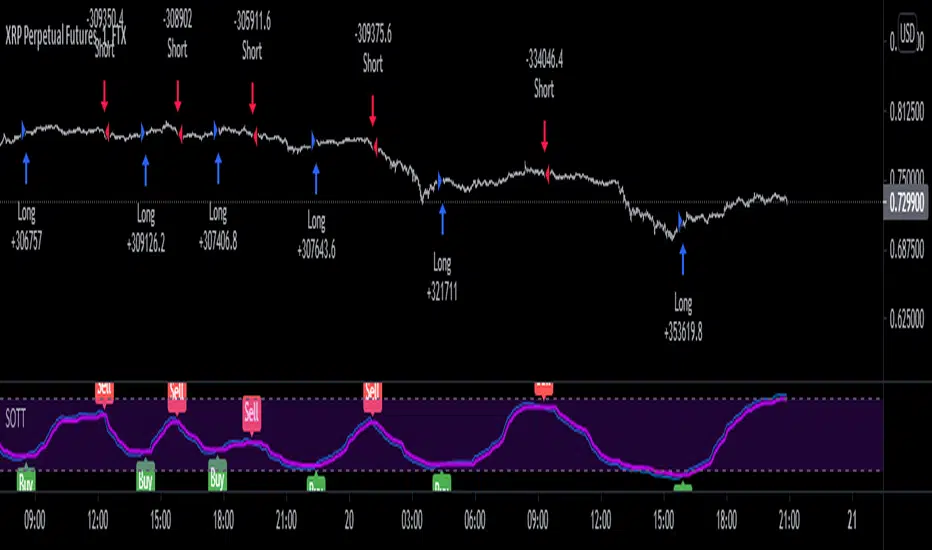

Combo Backtest 123 Reversal & Smoothed RSIThis is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

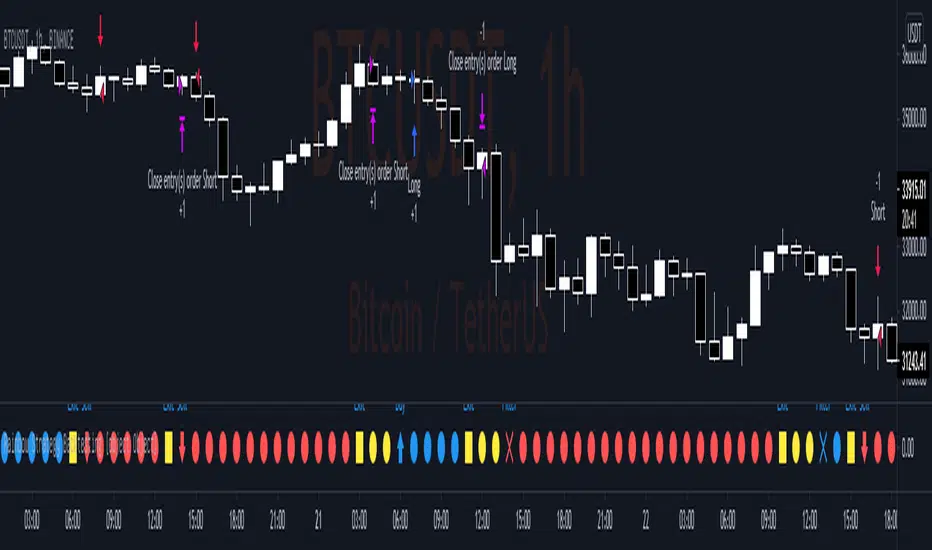

Second strategy

This is new version of RSI oscillator indicator, developed by John Ehlers.

The main advantage of his way of enhancing the RSI indicator is smoothing

with minimum of lag penalty.

WARNING:

- For purpose educate only

- This script to change bars colors.

Pine Script® ストラテジー